Country Financial Accountability Assessment

62

September 5, 2003 Document of the World Bank Report No. 29155-MX Mexico Country Financial Accountability Assessment Mexico Country Management Unit Financial Management, Operations Support Unit Latin America and Caribbean Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Country Financial Accountability Assessment

September 5, 2003

Document of the World Bank

Report No. 29155-MX

MexicoCountry Financial Accountability Assessment

Mexico Country Management UnitFinancial Management, Operations Support UnitLatin America and Caribbean Region

Report N

o. 29155-MX

Mexico

Country Financial A

ccountability Assessm

ent

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

MCxico Country Financial Accountabi l i tv Assessment i

ADEFAS APF ASF BANCOMEXT BANOBRAS

BANSEFI

CAFESP

CFE CFAA CLC CMH CNDH COMPRANET

COTEIP

DECLARANET DGCP DGPOP DGPyP

DGPyPS

DOFI

FARAC

IFE IMSS INEGI

IPAB

LCE’s NAFIN OIC PBI PEDIREGAS

PEMEX PND RFT SAT SECODAM

SEGEPLAN SEV

Acronyms

Adeudos de Ejercicios Fiscales Anteriores Administraci6n Pdblica Federal Auditoria Superior de la Federaci6n Banco de Comercio Exterior Banco Nacional de Obras y Servicios Pdblicos S.N.C. Banco de Ahorro Nacional y Servicios Financieros Comisi6n Asesora de Financiamientos Externos del Sector Piiblico Comisi6n Federal de Electricidad Country Financial Accountability Assessment Cuenta por Liquidar Certificada Contaduria Mayor de Hacienda del Congreso Comisi6n Nacional de Derechos Humanos Sistema Electr6nico de Contrataciones Gubernamentales ComitC TCcnico para la Instrumentacih del Plan Especial de CrCdito Extern0

Sistema Electr6nico de Declaraci6n Patrimonial Direcci6n General de CrCdito Pliblico Direcci6n General de Programaci6n Direcci6n General de Programaci6n y Presupuesto Direcciones Generales de Programaci6n y Presupuesto Sectoriales Direcci6n de Organismos Financieros Internacionales Fideicomiso de Apoyo para el Rescate de Autopistas Concesionadas Instituto Federal Electoral Instituto Mexican0 de Seguridad Social Instituto Nacional de Estadistica, Geografia e InformBtica Instituto de Protecci6n al Ahorro Bancario

Lineas de CrCditos Especificas Nacional Financiera S.N.C. Organos Internos de Control Product0 Interno Bruto Proyectos de Infraestructura Productiva de Largo Plazo Petr6leos Mexicanos Plan Nacional de Desarrollo Registro Federal de TrQmites Sistema Administracibn Tributaria Secretaria de Control y Desarrollo Administrativo (hasta Abril 10 de 2003), ahora es la SFP Sistema General de Planeaci6n Sistema de Evaluaci6n

Outstanding from previous fiscal years Federal Public Administration Supreme Audit Office of the Federation Foreign Trade Bank National Bank of Public Works and Services National Savings and Financial Services Bank Advisory Committee on Public Sector Foreign Financing Federal Electricity Commission AnBlisis de l a Gesti6n Financiera Pliblica Certified Account Payable Audit Office (Congress) National Human Rights Commission Electronic Government Procurement System Technical Committee for the Implementation o f the Special Foreign Credit Plan Electronic Financial Disclosure System General Directorate o f Public Credit General Directorate o f Planning General Directorate o f Planning and Budget General Directorates o f Sectorial Planning and Budget Directorate o f International Financial Agencies Trust Fund to Support the Maintenance o f Highways under Concession Federal Electoral Institute Mexican Institute o f Social Security National Institute o f Statistics, Geography and Information Technology Institute for the Protection o f Bank Savings Specific Credit Lines National Financial Agency Internal Control Units Gross Domestic Product Long Term Productive Infrastructure Projects Mexican Oil Company National Development Plan Federal Registry o f Procedures Tax Administration System Administrative Development and Control Secretariat (until April 10,2003), now SFP General Planning System Evaluation System

MCxico Country Financial Accountability Assessment 11

SHCP SIAFF

SICG

SICOM

SIP SFP

TESOFE UCEGP

UCGIGP

UIDEP

UNAM

UPP UR USC

Secretaria de Hacienda y Crtdito Publico Sistema Integrado de Administracih Financiera Federal Sistema Integral de Contabilidad Gubernamental

Sistema de Compensacih de Adeudos entre Dependencias del Sector Pliblico Sistema Integral de Pagos Secretaria de la Funci6n Pdblica (antes SECODAM) Tesoreria de la Federaci6n Unidad de Control y Evaluaci6n de la Gesti6n Pliblica Unidad de Contabilidad Gubernamental e Informes de la Gesti6n Pliblica Unidad de Inversiones de Desincorporaci6n de Entidades Estatales Universidad Nacional Aut6noma de Mtx i co

Unidad de Politica Presupuestaria Unidades Responsables Unidad de Servicio C iv i l

Ministry of Finance Federal Integrated Financial Management System Integrated Government Accounting System System for the compensation o f debts between public sector agencies Integrated Payment System Civi l Service Secretariat (previously SECODAM) Treasury o f the Federation Public Management Control and Evaluation Unit Government Accounting and Public Management Reporting Unit Investment Unit for the decentralization o f State Entities Mexico's National Autonomous University Budgetary Policy Unit Responsible Units Civi l Service Unit

... MCxico Country Financial Accountability Assessment 111

TABLE OF CONTENTS

Executive Summary ............................................................................................ v

I . OBJECTIVES. SCOPE AND INFORMATION SOURCES ...................................... 1 Objectives and Scope of this Document ................................................................. 1 Procedure Used for Information Gathering ................................................................. 2 Sources of Information Used ................................................................................... 2 I1 . FEDERAL PUBLIC SECTOR BUDGET MANAGEMENT ...................................... 3 Summary and Conclusions on Budget Management ........................................................ 3 Strengths and Weaknesses of Budget Management Affecting the Financial Management of the Federal Public Sector ................................................................................... 4 I11 . FEDERAL PUBLIC SECTOR TREASURY MANAGEMENT ............................. 8 Summary and Conclusions on Treasury Management ............................................... 8 Strengths and Weaknesses of Treasury Management ............................................... 9 I V . ACCOUNTING AND FINANCIAL REPORTING OF THE FEDERAL PUBLIC SECTOR ......................................................................... 10 Summary and Conclusions on Accounting ................................................................ 10 Strengths and Weaknesses o f Accounting ................................................................ 11 V.FEDERAL INTEGRATED FINANCIAL MANAGEMENT SYSTEM ................... 14 Summary and Conclusions on the SIAFF ................................................................ 14 Background and Description of the SIAFF ................................................................ 14 Strengths and Weaknesses o f the SIAFF ................................................................ 15 V I . PUBLIC DEBT MANAGEMENT ................................................................ 20 Summary and Conclusions on Public Debt Management .............................................. 20 Management Strengths and Weaknesses ................................................................ 21 VI1 . PUBLIC INVESTMENT MANAGEMENT ....................................................... 22 Summary and Conclusions on Public Investment Management ..................................... 22 Management Strengths and Weaknesses ...................................................................... 23 VI11 . INTERNAL CONTROL MANAGEMENT OF THE FEDERAL PUBLIC SECTOR ........................................................................................... 26 Summary and Conclusions on Internal Control Management ...................................... 26 Management Strengths and Weaknesses ................................................................ 27 I X . AUDIT IN THE FEDERAL PUBLIC SECTOR .............................................. 30 Summary and Conclusions on Audit Management in the Federal Public Sector .................... 30 Management Strengths and Weaknesses ................................................................ 31 X . PARLIAMENTARY OVERSIGHT OF THE FINANCIAL MANAGEMENT OF THE FEDERAL PUBLIC SECTOR ................................................................. 33 Summary and Conclusions on Parliamentary Oversight ............................................... 33 Background ..................................................................................................... 33 Strengths and Weaknesses ................................................................................... 34 X I . TRANSPARENCY AND PUBLIC ACCESS TO THE FINANCIAL INFORMATION OF THE FEDERAL PUBLIC SECTOR Summary and Conclusions on Transparency and Public Access to Information Standards and Codes Compliance Report (ROSC) Fiscal Transparency Module

...................................... 35 .................... 35 .................... 35

Strengths and Weaknesses ................................................................................... 36

Mkxico Country Financial Accountability Assessment i v

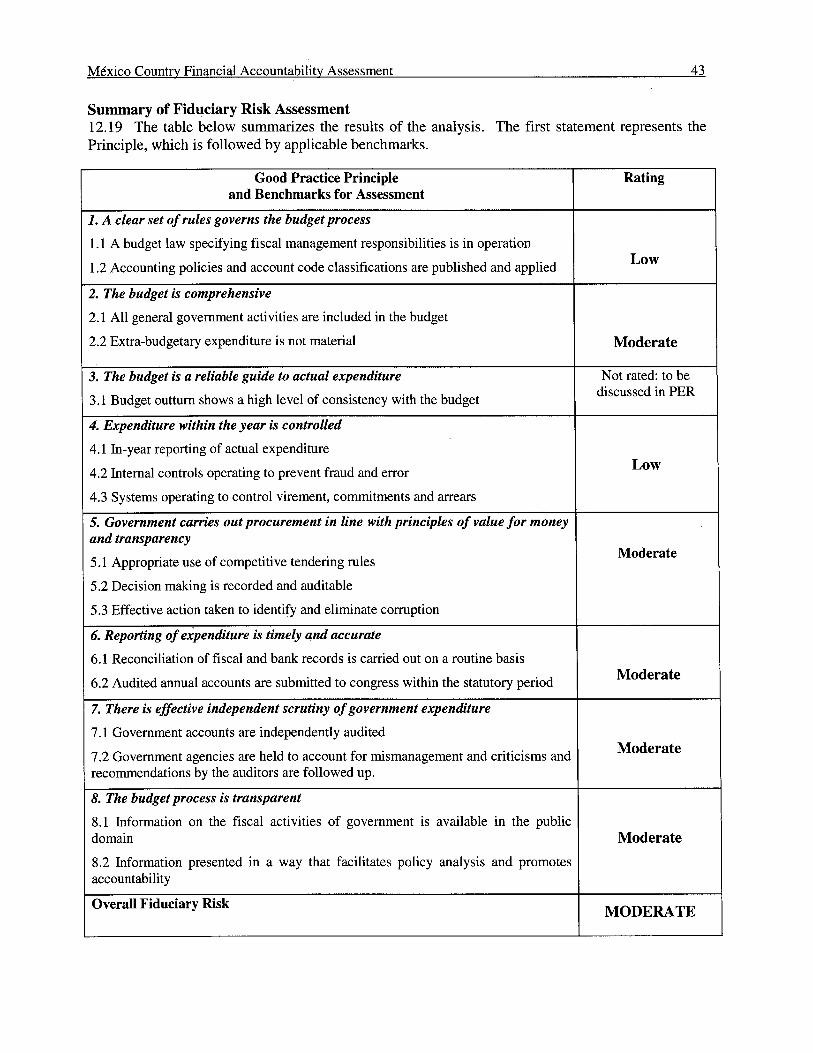

XI1 . FIDUCIARY RISK ASSESSMENT ................................................................ 38 ................................................................ 38

Framework for fiduciary risk assessment ................................................................ 39 Results o f assessment .......................................................................................... 40 Summary o f Fiduciary Risk Assessment ............................................................... 43

ANNEX 1 - SPECIFIC OBJECTIVES AND SCOPE OF THE REVIEW OF EACH SECTOR ........................................................................................... 45

The need for fiduciary risk assessment

I . Budget Management o f the Federal Public Sector I1 . Treasury Management o f the Public Sector

V . Public Debt Management ................................................................................... 47

VI11 . Audit Management in the Federal Public Sector

X . Transparency and Public Access to the Financial Infordat ion of the Federal Public Sector .. . . S O

.............................................. 45 ....................................................... 45

I11 . Accounting and Financial Reporting Management o f the Federal Public Sector ........ 1 . 46 IV . Federal Integrated Financial Management System (SIAFF) ..................................... 46

V I . Public Investment Management ......................................................................... 48 VI1 . Internal Control Management o f the Federal Public Sector ...................................... 48

............................................... 49 IX . Parliamentary Oversight of the Financial management\pf the Federal Public Sector .......... 50

MCxico Country Financial Accountability Assessment V

EXECUTIVE SUMMARY

General Background

1. In the last seven years, the Government of Mexico has been developing a series of measures intended to improve the financial management of the federal public sector. This report has been prepared to summarize the status of implementation of such measures, highlighting those areas where strengths were observed, as well as mentioning those where additional attention may be required.

2. The report essentially covers the financial management at the federal level. I t reflects the contributions of the input received from the officials responsible for each area of public management that was covered (Annex 5), both in the preparation of the text and in the final review, with the aim of ensuring the relevance o f the observations made in each case.

Main Conclusions

3.

4.

5.

6.

7.

The Government of Mexico has adequate mechanisms in place to record and report public expenditures. The budget management of the Federal Government has several management instruments and defined objectives, standards and procedures, fostering an accountable and transparent management of State expenditures. The main strength observed was the existence of clear and complete rules that govern the Federal Government's administrative financial transactions. The gaps in the information received relating to budget execution, which have hindered the projection of cash requirements, were not fully corrected after the implementation of the Federal Integrated Financial Management System (SIAFF). The development and implementation of the SIAFF began in 1997. The slow pace at which this process has occurred i s evidence of the difficulties encountered due to the existence of multiple sub-systems in virtually a l l Government areas. Although the SIAFF i s not conceived as an integrated management process, i t would generate more effective control elements and supply outputs that wi l l improve the process of result evaluation. Particular attention should be given to t h i s limitation of the SIAFF to ensure the interest of i t s users and therefore i t s sustainability. The federal public administration has rigorous internal control systems that evidence the Government's decision to fight against corruption and improper administrative practices. The Civi l Service Secretariat or SFP (previously SECODAM) i s the entity that provides integration and guidance to the internal control systems, enabling a comprehensive vision of internal control problems, as well as the development o f common solutions for the entities of the Federal Government. The SFP i s a control and development entity founded on the recognized experience and effectiveness of the SECODAM. Its top-level professionals are continuously trained on disciplines related to their fields. The main weaknesses of SECODAM were associated with the relatively persecutory and punitive than preventive character of its procedures; however, the new SFP intends to redirect i t s efforts to supporting improved public management. The responsible of independent public audits i s the Supreme Audit Office of the Federation (ASF), a branch of the legislative which started its operations in January o f 2001. I t s institutionalization i s not fully completed, and there i s not enough evidence yet to make an adequate evaluation of i t s management. Given the traditional involvement o f the SECODAM in

MCxico Country Financial Accountabilitv Assessment vi

the area o f governmental auditing, the continuity o f the SFP wi l l be of vital importance to comply with the Agreement o f Technical Cooperation and Exchange entered into by the C M H (now ASF) and SECODAM (now SFP).

BUDGET MANAGEMENT

8. The main strengths of the budget system are associated with the existence of a well-defined, regulated and documented mandatory procedure for all its execution phases. The Federal Public Administration has a Classifier of Expenditures per Objective that allows for the integration and consolidation of institutional financial statements to produce the Financial Statements of the Federation. I t represents the structure o f the chapters, descriptions and entries that define the expenditures according to their nature: current or capital. There i s a 34-digit budgetary classification that makes it possible to track 14 components which classify expenditures by administrative, economic and functional information. A public information system on the Internet reports on legal and administrative procedures, budget execution and government procurement processes, which facilitates management and interaction with the community. From September to December o f 2002, the Manual of Budget Rules for the Federal Public Administration was significantly updated, in order to simplify and expedite the processing procedures.

9. Among the weaknesses of the budget system, i s the complexity of procedures resulting from the large number o f documents, laws, rules, decrees, circulars and instructions that, diminish the efficiency and effectiveness o f budget management. Many of these regulations are issued on an annual basis or are regularly updated or revised within each fiscal year. The budget law in force since 1977 has become outdated in some aspects and this requires the inclusion of some items in the Federation's Decree o f Expenditures Budget that should be part of the law, thus unnecessarily complicating this document that i s issued on an annual basis. On the other hand, the process of modernization and decentralization of financial management requires a more appropriate legal framework, providing continuity to the process of modernization of administration and control procedures so as to achieve the expected effectiveness and efficiency. The integration of information technology to the budget system of the Federal Government i s performe6 through multiple IT instruments, each with its own database. Although the systems allow for the exchange of information whenever required, none of them contains the entirety of the updated information and increasingly more decision making and other powers have been given to the executing agencies, so the information i s available at different levels o f aggregation (these levels correspond to the institutions executing the programs and resources, as well as those that integrate, consolidate and globalize).

TREASURY FUNCTION

10. The greatest strength o f the TESOFE i s the systematic internal order under which i t performs its functions of custody, concentration, oversight and application of federal funds, which i t projects and i s perceived by al l areas and entities of the Federal Public Administration.

MCxico Country Financial Accountability Assessment v i i

11. As the budget management systems do not have al l the information required by the TESOFE (commitments and accruals), this body does not have the information allowing i t to determine the status of budget execution nor what commitments have been entered into.

ACCOUNTING AND FINANCIAL REPORTING FUNCTION OF THE FEDERAL PUBLIC SECTOR

12. Federal government accounting registers and reports a reliable and reasonably timely position of the public accounts. I t s main strengths are associated with a well-defined, regulated and documented mandatory procedure for all i t s phases. I t i s supported by a sound legal and regulatory framework. I t makes use o f advanced technical instruments, such as the accounting manuals that include, among other aspects, accounting principles, charts of accounts, accounting guides, and account management instructions. The accounting rules are homogeneous for the entire Federal Public Sector.

13. Although the Integrated Government Accounting System (SICG) performs all the accounting functions that are required to record transactions, as by design i t was configured in the form of independent modules, the consolidation and reconciling of accounts must be performed in a semiautomatic fashion, which gives rise to a cumbersome, complex and risky procedure.

Parliamentary Oversight

14. The present government administration was preceded by a majority political party with limited effective opposition, for more than 50 years. The current government started of f in Congress with a multiparty arrangement with no prevailing majority, and has thus encountered a still-developing process of analysis, debate and critique of the Executive’s proposals. In this manner, the political transition i s showing a greater and more convenient separation and balance between the three Powers, and the function of Parliamentary oversight i s gaining a degree of force for which it was not prepared, neither politically nor administratively. The Legislative i s empowered to change the annual Budget bill submitted to it by the Executive, but it only has the month of December o f each year to do it, and 15 additional days every six years whenever there i s a change o f government. These conditions restrict the scope of the oversight function.

Transparency and Public Access to Financial Information

15. The current government i s significantly encouraging actions oriented at promoting transparency in the public administration, and to create instruments fostering both the population’s interest in reviewing public finances, and simple and up-to-date access. This i s new for the Government and the public, and at present can only be evaluated on the basis of actions being taken rather than on their results. The main strengths o f the system are the Government’s decisive interest and commitment in this respect, and the fact that a special permanent and inter-secretarial committee has been commissioned to lead on these matters (Inter-Secretarial Committee for Transparency and Anti-Corruption). I t s main weakness lies

in the lack of experience on the subject that thus requires an upfront development of a legal, operational and awareness foundation to support effectively the instruments to be proposed.

One of the strategic goals of the National Program Against Corruption and Development of Transparency and Administrative Development 2001-2006 i s oriented to “Preventing and dismantling practices of corruption and impunity, and promoting quality improvement in public management”.

Activities of the World Bank in the Area of Financial management

16. At the request of the Mexican Government, in July 2003 a mission of the World Bank from the areas of PRMPS and PEFA began talks with representatives from the Ministry of Finance focused on the possible provision of technical assistance in the field of public expenditure. The Government would be interested in assistance to improve the structure o f mid-term expenditures, performance management and budgeting, and transparency and fiduciary responsibility. These tasks would be performed b y members of PRMPS and PEFA, with whom the team of this CFAA has met to coordinate the exchange of information already obtained from the government and possible future activities.

Main Recommendations

a. The Under-Secretariat of Expenditures o f the SHCP should coordinate a comprehensive review of the legal framework regulating the financial management of the federal public sector, in order to simplify said management and make i t compatible with the new concepts of objective and results-based administration that the Government i s implementing. The Under-Secretariat of Expenditures of the SHCP should promote the integration of the budget management systems into a single database, designed to establish a single system allowing all transactions to be sufficiently seen and followed in all their phases. Likewise, i t should define the minimum level of IT automation required by the entities of the Federal Government to optimize the benefits that a government information system may contribute to their management. The definition of results, goals and indicators i s usually a complex task. The Under- Secretariat of Expenditures of the SHCP should promote the use of an appropriate number of indicators reflecting how the planned results and goals are being achieved. These indicators should allow for the follow up of multi-annual investment processes. The GoM should promote a greater simplification of the regulatory framework for budget management. In addition to the progress made with the implementation of the Manual of Information Requirements for the Departments and Entities of the Federal Public Administration and the Attorney General’s Oflice of the Republic, and considering the participation o f the SFP, the SHCP and the Central Bank in the meetings o f the Technical Information Committee (which administers the requirements of the Integrated Information System of Public Revenues and Expenditure), the SHCP and other agencies, such as the SFP, should promote a greater simplification o f the regulatory framework for budget management to facilitate the management of processes in a more fluid manner and to propose the rationalization of systems and reporting needs so as to have relevant and timely information, to reverse the proliferation o f information

b.

c.

d.

Mdxico Country Financial Accountabilitv Assessment i x

of doubtful practical application and scant usefulness in the management of public entities. A correct and timely flow of budget execution information i s essential to plan and keep the budgetary needs coordinated with cash availabilities. The full implementation of the S IAFF wi l l make i t possible to reduce this deficiency to the extent the budget execution information from al l the institutions affecting the federal treasury i s available in the time frame required by the TESOFE. The Government Accounting and Public Management Reporting Unit (UCGIGP) should promote the integration of the different systems presently in use into a single database. In this way, b y using unique records for transactions, reconciling and consolidation of accounts could be performed automatically. In turn, this would make i t possible to have information updated on an ongoing basis. To such end, i t i s of fundamental importance to completely implement the SIAFF. The new needs for automated and integrated management require a comprehensive review of the organizational structures, functions and operations o f the SHCP. For such purpose, a study should be undertaken on this matter to avoid delays in the implementation of the systems. The TESOFE should promote the proper documentation of the SIAFF, defining it clearly in terms o f i t s scope, design, objectives, partial indicators, implementation plan and procedures of institutional interaction, and establishing its interaction with the existing management and control systems.

i. The SHCP should establish mechanisms for the executing entities to evaluate investments based on cost-benefit criteria considering different alternatives. This w i l l make it possible to prioritize investments and improve the efficiency with which State resources are allocated. A modern vision of internal controls assigns preference to exerting control on management procedures as opposed to control enforced on public officials. The SFP should promote this type of control that may be exercised more efficiently and effectively through IT management tools.

e.

f.

g.

h.

j.

MCxico Country Financial Accountability Assessment 1

1. OBJECTIVES, SCOPE AND INFORMATION SOURCES

A. Objectives and Scope of this Document

1.1 This report i s a diagnostic tool designed to contribute to a better understanding of the financial management o f the Federal Government o f the Republic of Mexico, enabling the identification o f i t s strengths as well as the areas requiring improvement to achieve a more efficient, effective and transparent public sector. The report identifies the possible r isks that may affect the management o f the funds administered by the Federal Government, and it w i l l be used as the basis to recommend the actions to counteract them and to help various parts o f the Federal Government succeed in the achievement of their objectives.

1.2 A report i s also planned on the evaluation of the financial management at the state level. The conclusions of this work should be considered along with this report at the Federal level, so it w i l l then be possible to have a more comprehensive understanding of the conditions observed globally in the United Mexican States. Likewise, the conclusions reached through other fiduciary studies, such as the Report on the Observance of Standards and Codes (ROSC), the Fiduciary Risk Assessment (FRA) and the Public Expenditure Review (PER), should provide for an integrated analysis, leaving us with a global tool providing guidance on the areas requiring strengthening.

1.3 The scope of the review performed has included:

0 The financial management of the Federal Government in the following areas: a) budget; b) accounting and financial reporting; c) treasury; d) public debt management; and e) internal control systems including the administration o f accounting records and the use of IT tools. The control o f the public accounts o f the Federal Government for: a) the ex-ante and ex- post audit management performed by the Supreme Audit Office o f the Federation (ASF) and the Public Management Secretariat (SFP); b) Parliamentary oversight o f public finances; and c) public access to information on public finances.

0

1.4 The review has only included the administration of the Federal Government. Information has also been analyzed on the possible impact on the federal financial management o f autonomous and decentralized institutions, state-owned companies, the municipal level, and in general all the institutions mentioned in the Budget Law. This has made i t possible to produce a global picture of the financial management of the Federal Government.

1.5 Special attention has been given to the following aspects:

MCxico Country Financial Accountability Assessment 2

The most important current developments in relation to the SIAFF; The management of the Budgetary Policy Unit (UPP of the SHCP); the General Directorates of Sectorial Programming and Budget (DGPyPS o f the SHCP); the General Directorate of Programming (DGPOP of the Responsible Units); the Treasury of the Federation (TESOFE of the SHCP); the Government Accounting and Public Management Reporting Unit (UCGIGP o f the SHCP); the Public Credit Under- Secretariat; the ASF; the SFP; and the accounting procedures of the public and private sectors; The methodology used in the production and execution o f the budget; Cash flow management; Content and timing of financial reports; How effective and binding the control framework i s in financial management; The ASF and SFP’s role and influence in the supervision of the financial management and procurement procedures of the public sector in general; and, The level of implementation of the recommendations made by auditors in the public sector.

B. Procedures Used for Information Gathering

17. The work program has included: Reviewing previous research on the actual situation, organization, procedures of the Federal Government and its institutions in relation to their handling of financial management; Discussion and understanding of current management procedures, by means of visits to the institutions and meetings with key personnel there and high-ranking officials of the Federal Government; Review and analysis of the documentation provided by our contacts in the Government and the institutions surveyed; Joint preparation by representatives of the G O M and Bank staff of documents on the Federal Government’s financial management.

0

e

C. Sources of Information Used

1.6 reviewed, are included in ANNEXES 4 and 5 of this document.

The list of the institutions visited and the officials interviewed, as well as the documents

MCxico Country Financial Accountability Assessment 3

2. FEDERAL PUBLIC SECTOR BUDGET MANAGEMENT

A. Summary and Conclusions on Budget Management

2.1 A.l. Conclusion. The general conclusion to be drawn i s that the budget management of the Federal Government functions with management instruments and defined objectives, strategies, rules and procedures fostering an accountable and transparent management o f public expenditures. I t s main strength comes from the detailed and comprehensive rules that govern it, as well as the budgeting procedure that ensures i t s connection with the Government’s regional and sectoral plans. I t s main weakness l ies in the limited impact that the Federal Government has on the definition of the relation between current and investment expenditure, since over 93% o f the annual budget i s previously committed (salaries, constitutional transfers, debt service, and other obligations of the Federal Government of a permanent nature).

2.2 A.2. Legal Framework. The legal framework for the budget system i s complete, complex and detailed, apparently regulating all aspects o f budget management. The legal framework i s well coordinated and there would seem to be no substantial differences with the actual practice or contradictions between i ts rules. Although substantial improvements were introduced in 2002 to the manual of Budget Rules for the Federal Public Administration, and considering the obsolescence of some of i t s basic rules, the Annual Budget Decree includes items and updates (that might be better defined in other documents) that make i t unnecessarily complex. In addition, the great number of legal rules applicable to budget management, as well as i t s ongoing updating and rigorous control, create a complex and rigid legal environment for public servants that puts them in a defensive position and reduce their decision-making capacity.

2.3 As the Budget Law provides, i t i s only permitted to spend the Public funds that are approved in the budget. Likewise, further indebtedness or the granting of guarantees by the State are only allowed if expressly approved by Congress. Therefore, any extra budgetary funds, new indebtedness or the granting of guarantees by the State must be formally approved and entered in the budget to be permitted. The budget includes an explicitly defined and quantified item for emergencies and contingencies. In th i s way, no financial expenditure or commitment of the State i s free from budgetary control.

2.4 The link between the management of budget, treasury and accounting i s fully regulated in all phases and provides a satisfactory, planned and controlled flow o f funds, along with the reporting of reasonably adequate information-though with some deficiencies from the treasury point of view. This w i l l be substantially improved with the full implementation of the SIAFF (its partial implementation started in 2003 with the treasury operation) that w i l l produce this automatic and

MCxico Country Financial Accountability Assessment 4

permanent link, and that w i l l allow, among other aspects, improvements on the planning and coordination of the budgetary needs with the availability of fiscal funds.

2.5 Although the budget i s reasonably well executed, the evaluation process o f goals and results that i s currently applied should be improved, emphasizing a more significant and substantial definition of budget indicators and goals. In this respect, the National Budget, the annual Government’s report on the situation of the Nation and the implementation o f the National Development Plan, the Federal Public Account, the quarterly reports to the Lower House of Congress on the conditions of the economy, public finances and public debt, as well as the performance agreements, among the most important ones, include the evaluation o f goals and results of the public budget. At present, the evaluation goes into excessive detail generating very large volumes of information mostly related to actions performed; however, this information does not necessarily represent a clear picture of the status of sector programs. Similarly, this evaluation does not look at the effectiveness of spending, but mostly limits itself to verifying that the expenditure was made and the related procedures. The SFP wi l l continue with the actions begun by SECODAM to develop an evaluation process enhancing the comprehensive knowledge of the problems faced by public institutions and to improve the evaluation of the financial/ physical goals with the intention of verifying spending effectiveness.

2.6 The implementation of the SIAFF supports the updating and standardization o f budget and accounting definitions and procedures, as well as the creation o f a streamlined and integrated platform that wi l l enable more efficient and transparent information management. Among these improvements i s the updating of the Manual of Budget Rules for the Federal Public Sector (which defines the standard budget procedures) and the Classifier of Expenditures per Objective for the Federal Public Sector (which identifies the codes of budget allocations for the entire federal public sector).

B. Strengths and Weaknesses of Budget Management Affecting the Financial Management of the Federal Public Sector

B.l. Strengths

2.7 The following are the main strengths o f the budget system:

0

0

There i s a well-defined, regulated and documented mandatory process for al l execution phases. There i s a Classifier of Expenditures per Objective for the Federal Public Sector that allows for the integration and consolidation of the institutional financial statements in order to produce the Financial Statements of the Federation. There i s a 34-digit budget key that allows tracing the 14 components that classify expenditures based on administrative, economic and functional information. There are specific contingency items based on lessons from previous experiences (Funds for Natural Disasters and Oi l Revenues Stabilization Fund), which free other budget allocations from the incidence of these items.

0

MCxico Countrv Financial Accountabilitv Assessment 5

0 There i s an innovative procedure o f Performance Agreements that increases management efficiency and effectiveness and facilitates budgetary execution by the institutions by means o f increased flexibility in control systems, based on predefined and agreed commitments, results and business plans. There i s a well-organized public information system over the Internet providing information on legal and administrative procedures, budget execution and government procurement processes that facilitates management and community relations. The authorities’ progressive approach encourages a process o f continuous improvement in management procedures, evidenced b y the technological improvements, simplifications and innovations that have been implemented in the last few years, and which facilitated an smooth transition to from some old systems to the SIAFF.

0 There are automatic expenditure adjustments in case the revenues obtained are less than the estimates, criteria for the distribution and application o f surplus revenues, l im i ts and control of the deficit and indebtedness levels, definition o f primary surplus for the main parastatal entities with direct budget control, and monthly disclosure of public finance results over the Internet.

0

0

B.2. Weaknesses

2.8 B.2.1. The legal framework for budget management i s complex. Budget management, in i ts various phases from preparation to execution, i s regulated b y some twenty documents, laws, rules, orders, circulars and instructions (see Table 1 in Annex 2) that create a complex and regulated procedure that decrease efficiency and effectiveness from budget management. Many of these regulations are issued on an annual basis or have updates or revisions; one representing a significant advance i s the revision o f the manual of Budget Rules for the Federal Public Administration (carried out in 2002).

2.9 The Budget Law in force since 1977 has become outdated in many aspects and requires the inclusion in the Federal Budget Decree o f some items that should be part o f said law, thus complicating unnecessarily this annual document. On the other hand, the process of modernization and decentralization o f financial management requires a more adequate legal framework providing continuity to the process o f modernization of administration and control procedures making it possible to achieve the expected effectiveness and efficiency.

2.10 Recommendation: The Under-Secretariat o f Expenditures o f the SHCP should coordinate a comprehensive review o f the legal framework regulating the financial management o f the federal public sector, in order to make management simpler and compatible with the new concepts o f objectives and results based administration that the Government i s putting into practice. This should be supported by actions such as the updating o f the Manual of Budget Rules for the Federal Public Administration carried out in 2002.

2.1 1 B.2.2. Incomplete integration of information technology into the Federal Government’s budget system. Budget management i s performed by means o f several IT tools, each o f which uses i t s own database. Although the systems enable the exchange o f information whenever required,

Mkxico Country Financial Accountability Assessment 6

none o f them has all of the updated information. This detracts from the systems efficiency and might be a source of confusion. On the other hand, as it i s not mandatory for Government entities to be electronically integrated into the SHCP information system, some entities cannot receive the information consolidated by the SHCP in relation to budget follow-up and evaluation. These entities experience an unnecessary reduction o f their efficiency and lose opportunities to f ix management errors. The effectiveness of information systems i s based upon system universality and information sharing capabilities. Because they do not fully participate, they do not have such advantages some institutions reduce the efficiency of the entire system.

2.12 Recommendation: The Under-Secretariat of Expenditures of the SHCP should promote the integration of budget management systems into a single database, and if possible into a single system that allows one to see and monitor al l transactions in all their phases. Likewise, i t should define the minimum level of IT automation required at the entities of the Federal Government to optimize the benefits that a government information system may have for public sector management.

2.13 B.2.3. Goals and results of budget management and their follow-up. The main objective of the definition of budget goals and results i s to verify the effectiveness of public spending, i.e. if the public funds have been used to attain the foreseen ends and if they have produced the expected impact. Therefore, i t i s necessary to make a very clear distinction between objectives, results, goals and actions. In the case of budgets, definitions should make it possible to understand if the expenditure was timely, i f the expenditure was for the intended purpose, and if the expenditure has created the expected benefit. The system of results-based management requires a clear definition of goals, results and objectives; otherwise i t w i l l not be possible to make an evaluation of implementation, and even less of the effect of the investment made. This aspect could be improved at the time o f preparing the budget.

2.14 Recommendation: The definition of results, goals and indicators i s always complicated; for this reason the Under-Secretariat o f Expenditures o f the SHCP should promote the use o f a few but significant indicators reflecting how the planned results and goals are being achieved. These indicators should allow for monitoring of multi-annual investment processes.

2.15 B.2.4. The excessive control over spending and management complexity limit the efficiency of budget execution. Budget execution management -from the point of view of the executing entities- i s subject to: a) a diversity o f rules and regulations on spending that are included in over twenty documents (laws, decrees, regulations, rules, instructions, circulars and their respective updates); and b) a diversity o f control procedures on results, management procedures and institutional and personal performance. As a result, management i s excessively complex as officials are required to be highly knowledgeable and are easily exposed to making mistakes. On the other hand, such a rigorous and extended control system applied on such complex procedures tends to intimidate officials because of the numerous possibilities o f error they are exposed to. As a result the combination of these factors, limited management efficiency may be expected, and this might also affect the effectiveness of public expenditure.

Mkxico Countrv Financial Accountability Assessment 7

2.16 The SHCP, as it i s responsible over planning, programming and budgeting, in coordination with the SFP as the department thatthat supports public sector management, should support a simplification of the framework regulating budget execution so that processes w i l l be more agile management o f processes. Similarly, the SFP should adopt a control methodology more oriented to the evaluation of results than to a thorough control of procedures and individual actions. The application o f Performance Agreements as put into practice with some entities should be encouraged across the entire federal system.

Recommendation:

2.17 B.2.5. Excessive volume of reports on budget management. There i s an endless number of reports on budget execution that are required to comply with regulations, routine controls, regular performance evaluations, partial account rendering, etc.; they include information that i s not necessarily reconciled or that does not match without, and which in many cases may only comply with formal presentation objectives without providing any real information. Reporting i s an activity that consumes resources and time that in many cases are scarce in the public sector. Unnecessary information creates confusion and sources of error.

2.18 Recommendation: The SHCP in coordination with the SFP should propose the rationalization of the reporting systems and information requirements needs in order to work only with useful, certain and current information. This w i l l simplify management, w i l l improve the quality of information and w i l l reduce management costs.

2.19 B.2.6. The information provided by the States i s reflected in the allocations of the federal budget. To understand the financial management of the Mexican Federal Government it i s necessary to consider that in part it reflects the financial management of the States over which it has limited influence. A major part o f the Federal Budget i s planned, budgeted and executed by the States. In some cases, this autonomous management by the States, with their own regulations, i s not consistent with the rules and procedures followed by the Federal Government; this affects all stages of the public spending process as well as the procedures for the registration and reporting of accounts that enable the timely production of the Federal Public Account. In many cases, this deficiency i s due to technological and operational differences, and in other cases, i t i s due to onlypartially compatible rules and procedures. This becomes especially important when deficiencies occur at the time of prioritizing programs and recording and reporting information.

2.20 Recommendation: The SHCP in coordination with the SFP should foster the compatibility between the procedures and operational capacities across the entire Government o f the Republic, so as to allow a timely exchange o f information, and to be able to ensure at least a minimum (but comprehensive) quality level for the administration and the financial information that i s going to be shared.

MCxico Country Financial Accountability Assessment 8

3. FEDERAL PUBLIC SECTOR TREASURY MANAGEMENT

A. Summary and Conclusions on Treasury Management

3.1 As a general conclusion, i t may be said that the Treasury o f the Federation (TESOFE) -which performs ,the treasury function of the Federal Government- operates with management instruments, objectives, strategies, rules and procedures that have allowed i t to meet the cash needs resulting from the execution of the Federation’s budget. I t s main strength stems from the systematic internal order with which it performs i t s functions of custody, concentration, surveillance and application of federal funds. I t s main current weakness relates to the lack of and/or untimely information on the status of budget execution, which makes it difficult to project the cash needs and coordinate them with cash availability. This weakness i s in the process of being overcome with the implementation of the SIAFF.

A.l. Conclusion.

3.2 A.2. Legal Framework. The legal framework o f the treasury system i s complex, and in principle it regulates all aspects of management. The legal framework i s well coordinated and seems to have no divergence with real practice or contradictions among i t s rules.

3.3 The funds administered by the TESOFE are: federal revenues from federal taxes, products and duties; expenditures related to the execution of the federal budget; and public credit federal transactions, al l o f them identified as the administration of federal funds. The TESOFE does not administer the funds related to parastatal companies, nor the funds related to the Legislative and Judicial Powers and autonomous agencies, which because o f their nature, legal personality and own assets, are responsible for the administration of their resources and/or funds.

3.4 The link between the budget, treasury and accounting i s fully regulated in all phases and provides a flow o f information that has enabled a satisfactory administration of funds, but it i s insufficient to project funding needs due to gaps in the information received on budget execution. This would be substantially improved with the full implementation o f the SIAFF that would produce this automatic and permanent link, including information on expenditure commitments, and that w i l l allow, among other aspects, to improve the planning and coordination of the budgetary needs with the availability of funds.

3.5 have been detected that cannot be overcome by the SIAFF.

Treasury management i s reasonably well executed, and no substantial gaps or deficiencies

MCxico Countrv Financial Accountability Assessment 9

3.6 The implementation of the SIAFF (an initiative by the TESOFE) has promoted the updating and standardization o f budgetary and accounting definitions and procedures, as well as the creation o f a uniform and integrated IT platform that w i l l facilitate more efficient and transparent information management. At present, the TESOFE receives very important information from the S IAFF module implemented in 2003. The S IAFF improves quality and timeliness of the information required for the analysis and projection o f cash flows in the Treasury. Presently, the S IAFF has not been linked to accounting and budgeting (the MOF i s analyzing this situation in order to address it).

B. Strengths and Weaknesses of Treasury Management

B.1. Strengths.

3.7 The main strength of the TESOFE comes from the systematic internal order with which i t performs i t s functions of custody, concentration, surveillance and application of the federal funds, which i s projected and i s recognized by all departments and entities o f the Federal Public Administration.

B.2. Weaknesses.

3.8 As the budget management systems do not have all the information required by the TESOFE (commitments and accruals), this agency does not have the information allowing it to determine the budget execution position nor what commitments have been acquired.

The link between budget management and treasury management.

3.9 Recommendation: A correct and timely flow o f budget execution information i s essential to plan and keep the budget needs coordinated with cash availabilities. The full implementation of the SIAFF wi l l allow this deficiency to be reduced to the extent the budget execution information from all the institutions collecting or receiving the federal funds i s available in the conditions required by the TESOFE.

4. ACCOUNTING AND FINANCIAL REPORTING OF THE FEDERAL PUBLIC SECTOR

A. Summary and Conclusions on Accounting

4.1 A.l. Conclusion. As a general conclusion, i t may be said that the federal government accounting registers and reports a reliable and reasonably timely position o f the public account. I t s procedures have been reviewed and updated during the last few years resulting in the standardization of procedures and principles in the federal public sector. Its main strengths are: i t s legal and regulatory basis that provides that the accounting records should be completed 60 days after the transaction, defines a single chart of accounts, and provides for and enforces the mandatory nature of all accounting procedures in the federal public sector; and i t s integration of the assets and liabilities, financial and budget operations of the Federal Government. I t s main weakness l ies in the limited integration o f i t s IT systems making i t difficult to consolidate and reconcile accounts. This weakness i s in the process of being overcome with the implementation of the SIAFF.

4.2 A.2. Legal Framework. The legal framework of the accounting system consists of several laws, regulations and official specialist publications. The legal framework i s up to date, well coordinated and does not seem to have divergence with actual practice or contradictions among its rules. The publication of the SHCP, “Principios Bdsicos de Contabilidad Gubernamental”(“Basic Principles of Government Accounting”), defines the entire conceptual framework o f the federal accounting system and makes it possible to have uniform accounting methods, procedures and practices, and systematic processes for information collection, registration and interpretation. These principles are compatible with international standards and generally accepted principles.

4.3 No substantial divergence has been detected between the current practice and the formal registration and reporting requirements in force. However, the timing o f reporting may be improved reducing the preparation times as well as the frequency of reports. This weakness i s to be overcome with the implementation of the SIAFF.

4.4 The accounting system issues several types of reports, some of a legal nature and others of an operational type that include current and reliable information on public accounts. As the accounting management i s carried out in a decentralized manner, each entity generates as required the necessary reports to support i t s operations (control and follow-up o f public revenues and expenditure) and the decision-making processes.

4.5 The main report issued by the accounting system on an annual basis i s the Public Account of the federal government; this report i s the basis for the Congressional oversight of public finances,

MCxico Country Financial Accountability Assessment 11

and i t s contents may be accessed b y citizens as i t i s available on the Internet page o f the Under- Secretariat o f Expenditures. The Financial Management Progress Report contains the results obtained in the first semester and i s submitted to the Supreme Audit Office o f the Federation in August each year. The entities issue a quarterly report on their budgetary and financial period for i t s review b y the “Government Accounting and Public Management Reporting Unit”.

4.6 deficiencies have been detected.

The accounting management i s reasonably wel l executed, and no substantial gaps or

4.7 The implementation o f the SIAFF w i l l promote the updating and standardization o f budgetary and accounting definitions and procedures, as wel l as the creation o f a streamlined and integrated platform that w i l l enable more efficient and transparent information management.

B. Strengths and Weaknesses in Accounting

B.l. Strengths.

4.8 The fol lowing are the main strengths and benefits provided by the accounting system:

There i s a well-defined, regulated and documented mandatory procedure in al l i t s phases. The accounting system i s the product o f a long period o f development, as governmental accounting has been virtually always applied in Mexico. There i s a sound legal and regulatory framework. There are advanced technical instruments available, such as the accounting manuals that include, among other aspects, accounting principles, charts o f accounts, accounting guidelines, and accounting management instructions. Specific rules are issued on a regular basis, such as those providing for the presentation o f the Federal Public Finance Account, the recognition o f the effects o f inflation, the recognition o f labor obligations upon the retirement o f employees from semi-state entities, the accounting treatment o f investments in long-term productive infrastructure projects, and others. Accounting rules are homogeneous for the entire Federal Public Sector. Accounting i s carried out on the same accounting bases. There i s a single chart o f accounts for al l the centralized departments o f the public sector. Accounting i s performed in a decentralized manner, with departments and entities responsible for i t s proper application and the maintenance o f the supporting documentation. Financial accounting and budget accounting are linked. All transactions performed by the Federal Government in relation to assets and liabilities, finances and budget, are linked. Accounting i s the basic source for the main reports of the Federal Government, such as the Federal Public Finance Account and the Financial Management Progress Report.

MCxico Country Financial Accountability Assessment 12

B.2. Weaknesses.

4.9 B.2.1. The SICG is not an integrated system of accounting information and management. Although the SICG performs al l the accounting functions required for the registration of transactions, as it was configured in the form of independent modules, the consolidation and reconciling of accounts must be carried out in a semi-automated manner, which creates a procedure that i s burdensome (because o f the information volume handled), complex (as the modules record different execution phases), and risky (since it might lead to errors).

4.10 Additionally, the process of information reconciling between the Collection and Expenditures Modules and the Federal Funds Module i s complex. The entry of transactions i s performed by different entities that require in each case the entry o f a common transaction description and identification information; this results in duplicated efforts, creates the possibility of error, and makes i t difficult to reconcile accruals and payments.

4.1 1 Recommendation: The Government Accounting and Public Management Reporting Unit (UCGIGP) should promote the integration of the 5 subsystems into a single database. In this way, through the use o f single records for transactions, the account reconciling and consolidation could be automatic. In addition, i t would thus be possible to have updated information at all times. The SIAFF, once it i s fully implemented, might solve this issue.

4.12 B.2.2. The registration of commitments does not occur in all cases. The registration of commitments i s provided by regulations as mandatory only in the cases of purchases and public works. This reduces the possibility of making a comprehensive evaluation both of management and of results and achievements.

4.13 record commitments in all cases. The SIAFF, once i t i s fully implemented, might solve this issue.

Recommendation: The UCGIGP should promote the generalization o f the obligation to

4.14 B.2.3. The information consolidation process i s on a quarterly basis. As a result of the complexity of the current process of account consolidation and reconciling, the production of the consolidated reports consumes much time and effort, and therefore the reports become outdated and are only useful for the purposes o f follow-up and further control o f public revenues and expenditures. Institutions have their own accounting systems that produce independent management reporting.

4.15 Recommendation. The integration o f the accounting subsystems would make i t possible to obtain reconciled and updated information automatically thus facilitating the production of financial reports. The SIAFF, once it i s fully implemented, might solve this issue and w i l l facilitate the production of financial reports.

MCxico Country Financial Accountability Assessment 13

4.16 B.2.4. Inconsistencies between state and federal accounting records. According to the provisions of the Political Constitution of the United Mexican States and the respective State Constitutions, the governments of the federative entities have management sovereignty, evidenced b y the autonomous definition of their internal organization, legal framework, and administration of financial resources.

4.17 In this context, their accounting systems show diverse characteristics, as by law they are not required to follow a certain model. Significant differences are noted between the approaches used in each State and with respect to the Federal Government.

4.18 The majority of states show serious limitations, such as the lack o f accounting principles expressly established for public sector, and the absence o f adequate technical and regulatory instruments. Besides, there i s no proper linkage between budget and accounting. The structure and information content of state public accounts are heterogeneous, making i t difficult to compare and interpret results.

4.19 In order to solve this situation, the MOF has been implementing since 1995 the Modernization Program of systems for Government Accounting and Public Accounts, with the main purpose of promoting the development of said systems, and attaining technical and regulatory harmonization, and consequently generating compatible information that may be analyzed and interpreted under common criteria.

4.20 I t should be noted that no consolidation i s made of the Federal Public Finance Account with those o f the State Governments. Each government level produces i ts own documents and submits them to the respective Congress. The consolidations that comprise the three government levels (federal, state and municipal) are carried out by the National Institute o f Statistics, Geography and Information Technology (INEGI) to determine economic aggregates, so said consolidations are of an economic nature, not financial or budgetary.

5. V. FEDERAL INTEGRATED FINANCIAL MANAGEMENT SYSTEM

A. Summary and Conclusions on the SIAFF

5.1 The SIAFF i s s t i l l in i t s initial phase of testing and evaluation, having become partially operational in the federal public sector in 2003. I t has been initially designed as an information technology tool that wi l l make i t possible to reach a basic operating level comprising the areas o f budget, treasury and accounting, and it was created with the intention o f providing the treasury system with continuous, timely and reliable information on the position and commitments o f the treasury, as well as better information on the status of public expenditure actions.

5.2 As the system i s s t i l l in i ts pre-operational phase, i t has not been evaluated, so this chapter only includes an analysis of i t s background and possible weak points as detected at the time o f producing the report, which might be overcome at the time o f full implementation.

B. Background and Description of the SIAFF

5.3 The Federal Integrated Financial Management System (SIAFF), as the Mexican Government conceived it, i s a system that w i l l initially enable the oversight o f public resources. The implementation o f an integrated financial management system for the entire Federal Government w i l l consist of several successive stages. In i t s f i rs t stages, the SIAFF wi l l have the following objectives :

0

0

0 Generate electronic payments.

Automate the accounting of budgetary actions; Simplify expenditure related operations; and,

5.4 The SIAFF, in i t s f i rs t stages, i s not conceived as a management system, but only as a tool that w i l l allow the departments to keep records o f expenditure actions; i t w i l l not be a mechanism for expenditure evaluation or of efficiency or effectiveness measurement.

5.5 However, the final SIAFF should be viewed as a management system involving: a) the legal and regulatory framework of public financial management; b) the administrative procedures within and between government institutions; c) policies, strategies, criteria and methodologies applicable to management; and d) the administrative and IT instruments that w i l l make management more efficient. Therefore, the different stages of i t s implementation w i l l have to take these aspects into account in a gradual manner.

Mexico Country Financial Accountability Assessment 15

5.6 The implementation process i s expected to extend to all departments and General Branches of the Federal Executive, the Legislative and Judicial Powers, and the government’s autonomous bodies.

5.7 At the beginning of the S I A F F project (1997), a general and comprehensive analysis and planning process was conducted to identify an initial phase comprising only the expenditure operations; this phase was initiated in 1999. The process was designed as an IT project, not as a managerial or management project, so some of the institutional developments have not been taken into account and limited importance was given to some legal and regulatory aspects. The SIAFF IT tool for the first stage appears to be almost completed.

5.8 Considering the elementary level of implementation foreseen for this phase, as well as the conditions of preparation, standardization and experience o f the institutions in automated budget, accounting and treasury management, no major difficulty should be expected in the implementation o f the SIAFF IT tool in the institutions of the central administration of the Federal Government. However, in the case of those institutions that operate with a certain degree of autonomy from the Executive, the legal framework should be checked for compatibility before proceeding with implementation, as these institutions might be obliged to present accounts to the Executive that might later be considered unacceptable.

5.9 Likewise, as long as the SIAFF i s not conceived and documented as an integrated management process, and the regulatory, legal, organizational, administrative and technological aspects are not properly analyzed and made compatible, the system’s sustainability i s not guaranteed, i t s operation and effectiveness w i l l be limited, and i ts chances o f growth and improvement w i l l be rather improbable.

C. Strengths and Weaknesses of the SIAFF

C.l. Strengths.

5.10 fully operational.

The analysis of the strengths of the SIAFF wi l l be made at a later date, once the system i s

C.2. Weaknesses.

5.11 C.2.1. Operational integration within the SHCP. The SHCP has automated but independent IT management systems for budget production, execution, modification and follow-up. The accounts management i s carried out with 4 independent modules. In the TESOFE, the SIP enters information from seven expenditure components on a daily basis and requires the DGPH (another body within the TESOFE) to perform an additional reading of the same database to get information to track payments (CLCs) entering information from the 14 expenditure components. Databases are only integrated for direct and specific purposes, and such integration i s accessible only for some entities. Each functional entity has been autonomously managing i t s operation

without coordination with the other functional complementary entities. An objective or managerial attitude to share efforts and information, or to develop a coordinated institutional development, process was not found. This not only overload the system with information, duplicates the use of resources and diminishes efficiency and effectiveness, but also shows the limited integration existing between the different departments of the same institution, in addition to the limited leadership to integrate and coordinate institutional efforts.

5.12 Recommendation: The MOF should review i ts organizational, functional and operational principles to check whether they meet the new automated and integrated management needs. Likewise, that they meet the governance requirements of the new integrated systems. The purpose of the regulatory entities i s not simply to regulate procedures or to install new IT systems, but to improve management results, which involves ongoing interaction and coordination with the decentralized entities. In order to ensure an efficient and effective integrated management o f the public sector, i t i s necessary for all management systems of the Federal Government, and in particular the management system of the SHCP, to demonstrate the intention to integrate functions and results.

5.13 C.2.2. The definition of the SIAFF. Although much activity and good intentions are seen in the process of development and implementation of the SIAFF, i t was not possible to find an integrated, clear and well-defined conceptual or functional design (only the f i rs t phase o f the SIAFF has been designed). Neither was it possible to find an integrated implementation plan including a consideration of the institutional, functional, operational and IT aspects. Therefore, i t i s not clear exactly what are the results expected or how developed the implementation process is. Although the entities have already adjusted to a certain degree (see corresponding chapter in Annex 2), i t was not possible to find an analysis o f the impact that the implementation o f the S IAFF w i l l have on the institutions. Restricting the implementation of the S IAFF to the installation of a new IT system i s an over-simplification that might substantially affect the institutions involved.

5.14 The functionality and concept of the SIAFF are established in the S IAFF guidelines that also specify the scope for i t s f i rst stage. Depending on the result of this f irst stage of implementation, and the difficulties to be faced, the additional phases should be defined.

5.15 Recommendation: I t i s necessary and urgent that the TESOFE promote a proper documentation for the SIAFF, with clear definitions in terms o f scope, design, objectives, indicators, implementation plan and procedures for institutional interaction, along with a definition of i t s interaction with the other existing management and control systems.

5.16 C.2.3. Coordination of the S I A F F with the management control and evaluation entities. In the short term, the S IAFF w i l l become the main financial management instrument o f the Government and the main source o f financial information. On the other hand, the implementation of new management procedures always creates some degree of confusion and initial inefficiency that i s usually overcome with time. Finally, an integrated information system provides innovative instruments for the evaluation and control of transactions. It i s important that the agencies

MCxico Country Financial Accountability Assessment 17

responsible for the control and evaluation of the entities' management should become involved in the process of development and implementation, so that:

0

0

0

0

0

The mistakes that might occur at the beginning are understood; Officials are able to verify that the institutional internal control procedures are s t i l l current and effective; Personnel can be trained to obtain the greatest benefits from the new procedures; Constructive opinions may be voiced on the system so as to improve i t and keep i t current; Institutional weaknesses that may reduce the effectiveness o f the Integrated System, can be detected.

5.17 Recommendation: The TESOFE should promote a more active participation of the SFP and the ASF in the design and coordination of actions for the implementation of the SIAFF. These institutions should become the main partners o f the TESOFE and the S I A F F in supporting i t s implementation and promoting the proper use of the system.

5.18 This i s complementary, as the Bank noticed that the internal control body and the General Directorate of Funds and Securities Surveillance have participated from the beginning in the implementation of the SIAFF. There i s already direct involvement by the SFP which w i l l be an advantage. The system wi l l open up various supervision options through the audit trails the system provides, enabling a remote review process that w i l l diminish the pressure on the responsible units for on-site auditing.

5.19 C.2.4. The regulatory framework of financial management. The new integrated financial management may provide, among other things, very powerful instruments to perform an automatic preventive control of transactions, to eliminate discretionality in the public sector, to promote effective results-based management, and to ensure the proper, timely and efficient use of public funds. The new management procedures w i l l render some regulations obsolete, wi l l require new regulatory concepts, and wi l l bring about the simplification of administrative procedures that may be regulated or required by rules presently in force.

5.20 For the f i rs t stage of the SIAFF, the current legislation provides a sufficient legal framework. As the S I A F F evolves, an analysis should be made o f the possible adjustment o f the various legal standards (laws, regulations and administrative agreements).

5.21 Recommendation: The TESOFE should support a comprehensive review of the federal legal framework applicable to financial management systems. A clear definition and observance o f institutional autonomies should be one of the objectives o f the SIAFF'.

The SIAFF wi l l define automatic and generalized accountability procedures in al l i t s affiliate institutions; this might require some adjustments o f current legislation so as not to affect the autonomy o f some institutions.

MCxico Country Financial Accountability Assessment 18

5.22 C.2.5. The legal basis of the SIAFF. After the implementation of the SIAFF, substantial changes wi l l take place within the institutions in terms o f their management procedures and their inter-institutional relations and dependencies. In many cases, these changes w i l l be irreversible and critical. In the future, institutions wi l l possibly have to assume the operating and updating costs of the system, regardless of their technical or financial capacity. This i s even more complex, when considering that the conceptual aspects of the SIAFF are not yet well documented, and they may be subject to modifications based on circumstances that might unnecessarily change i t s critical aspects. The S IAFF should therefore be adequately formalized, as should the inter-institutional relations i t may generate, in order to ensure i t s existence, efficient operation, the quality and timeliness of i t s information, i t s objectives and the obligatory and universal presence it w i l l have in the federal system.

5.23 Recommendation: The TESOFE should promote the adoption of a SIAFF Act providing, among other aspects, for the following: i t s mandatory nature2, i t s objectives, i t s evaluation and updating procedures, responsibilities of the institutions involved, inter-institutional relations, access and disclosure of institutional financial information, and inter-institutional accountability procedures.

5.24 This i s in addition to TESOFE’s Service Law that allows the provision of treasury services via automated equipment or systems, as well as the use o f electronic identification mechanisms. The House of Deputies instructed the Federal Executive b y PEF 2002 to operate the SIAFF as from 2003 as a mandatory requirement; on the basis o f this mandate, on April 30 of 2002, the DOF published the Guidelines relative to the functioning, organization and operation requirements o f the SIAFF. In accordance with the plan3 this was partially fulfilled.

5.25 I t i s convenient to integrate the provisions of the SIAFF in a single legal instrument.

5.26 C.2.6. The institutions have received limited training. The implementation of the SIAFF wi l l change the entities’ management procedures and instruments, and i t s impact w i l l be a function of the operating capacity, the employees’ technological and professional development, the complexity and volume of operations, etc. Therefore, the impact on each entity could vary greatly. Similarly, the need for improvements wi l l become evident within the institutions, but these changes should be tailored to the needs of each institution. These improvements, adjustments and changes might also require investments or expenses not foreseen in the institutional budgets.

5.27 Recommendation: The TESOFE should have institutional diagnostics on all the entities that w i l l become members of the SIAFF, to be able to recommend in due time the improvements necessary with regard to organization, operation or quality and quantity of human, financial or infrastructure resources. Institutions should also be instructed on the internal control aspects that w i l l be automatically taken over by the SIAFF, and on every other aspect that i s expected to be

At present, i t s use is only defined in the 2004 Budget Decree. This plan i s the result o f the adjustment of the original. This adjustment was based on experience acquired and the

progress made in 2002 and part of 2003.

MCxico Country Financial Accountabilitv Assessment 19

covered b y the institutional internal control systems, so as to address weaknesses and avoid unnecessary problems of coordination in these processes.

MCxico Countrv Financial Accountability Assessment 20

6. PUBLIC DEBT MANAGEMENT

A. Summary and Conclusions on Public Debt Management