Costs and Benefits of Business information Disciosure - …raw.rutgers.edu/docs/Elliott/15Cost and...

18

® 1994 American Accounting Association Accounting Horizons Vol. 8 No. 4 >' December 1994 .*' pp. 80-96 ;" COMMENTARY Robert K. Elliott and Peter D. Jacobson Robert K. Elliott and Peter D. Jacobson are members of the Executive Office of KPMG Peat Marwick in New York. I Costs and Benefits of Business information Disciosure This article analyzes the costs and benefits of disclosures of information by profit-making enterprises. It excludes the costs and benefits of disclosure by governmental entities and private-sector, not-for-profit entities. Entirely different issues arise when disclosure must be related to the goals and effective functioning of democracy and charitable undertakings. Even when narrowed, however, the range of enterprise disclosure to be considered is enormous. It can vary from none to complete. None is a total right of privacy. Complete dis- closure is a public right to see anything and everything. Some parties might benefit and others might suffer from any disciosure, though it is also true that some disclosure is immaterial in cost and in effect. The types of costs and benefits are economic, political, social, and ethical. Parties may be affected by both costs and benefits. For example, the costs of corpo- rate disclosure are borne by owners, but they are also beneficiaries of the disclosure they pay for. Financial report users do not neatly share in costs and benefits. Although owners pay for corporate disclosure, stock market investors considering ownership are free riders who pay nothing at all. These kinds of complexities are one rea- son this article does not circumscribe the range of costs and benefits it considers. There is another. There are no agreed-upon mea- sures of the dollar value of costs and benefits from disclosure. The appropriate starting place for a consideration of costs and benefits is therefore to identify their range and nature and to explore their relationships. The costs and benefits treated in this ar- ticle are categorized by interests. The catego- ries are: • The entity's interests. • Nonowner investors' interests. • The national interest. The analysis of these three sets of costs and benefits in sections I through III below is followed by a section that assesses future changes in the costs and benefits (section IV) and a concluding section on the limits of cost- benefit analysis. The article makes an assumption through- out that must be understood in order to fol- low what is being said. All references to dis- closure pertain only to "informative disclo- sure." Informative disclosure is useful for de- cision making, even if it involves costs that outweigh its usefulness. It is unbiased and un- tarnished by misleading omissions. Moreover, informative disclosure provides an opportu- This article is a modified version of a paper prepared for the AICPA Special Committee on Financial Report- ing, and the authors acknowledge the helpful sugges- tions and advice of committee members. However, the views expressed in the Eirticle are solely those of the authors.

Transcript of Costs and Benefits of Business information Disciosure - …raw.rutgers.edu/docs/Elliott/15Cost and...

® 1994 American Accounting AssociationAccounting HorizonsVol. 8 No. 4 > 'December 1994 .*'pp. 80-96 ;"

COMMENTARY

Robert K. Elliott and Peter D. Jacobson

Robert K. Elliott and Peter D. Jacobson are members of the Executive Office of KPMGPeat Marwick in New York. I

Costs and Benefits of Business informationDisciosure

This article analyzes the costs and benefitsof disclosures of information by profit-makingenterprises. It excludes the costs and benefitsof disclosure by governmental entities andprivate-sector, not-for-profit entities. Entirelydifferent issues arise when disclosure must berelated to the goals and effective functioningof democracy and charitable undertakings.

Even when narrowed, however, the rangeof enterprise disclosure to be considered isenormous. It can vary from none to complete.None is a total right of privacy. Complete dis-closure is a public right to see anything andeverything.

Some parties might benefit and othersmight suffer from any disciosure, though it isalso true that some disclosure is immaterialin cost and in effect. The types of costs andbenefits are economic, political, social, andethical. Parties may be affected by both costsand benefits. For example, the costs of corpo-rate disclosure are borne by owners, but theyare also beneficiaries of the disclosure they payfor. Financial report users do not neatly sharein costs and benefits. Although owners pay forcorporate disclosure, stock market investorsconsidering ownership are free riders who paynothing at all.

These kinds of complexities are one rea-son this article does not circumscribe therange of costs and benefits it considers. Thereis another. There are no agreed-upon mea-sures of the dollar value of costs and benefits

from disclosure. The appropriate startingplace for a consideration of costs and benefitsis therefore to identify their range and natureand to explore their relationships.

The costs and benefits treated in this ar-ticle are categorized by interests. The catego-ries are:• The entity's interests.• Nonowner investors' interests.• The national interest.

The analysis of these three sets of costsand benefits in sections I through III below isfollowed by a section that assesses futurechanges in the costs and benefits (section IV)and a concluding section on the limits of cost-benefit analysis.

The article makes an assumption through-out that must be understood in order to fol-low what is being said. All references to dis-closure pertain only to "informative disclo-sure." Informative disclosure is useful for de-cision making, even if it involves costs thatoutweigh its usefulness. It is unbiased and un-tarnished by misleading omissions. Moreover,informative disclosure provides an opportu-

This article is a modified version of a paper preparedfor the AICPA Special Committee on Financial Report-ing, and the authors acknowledge the helpful sugges-tions and advice of committee members. However, theviews expressed in the Eirticle are solely those of theauthors.

Costs and Benefits of Business Information Disclosure

nity for a decision maker to obtain an incre-mental improvement in assessing the realprospects of an enterprise. Thus informativedisclosure, as used in this article, is an idealconcept created to illustrate the costs and ben-efits of disclosure. (The appendix presents amore formal definition of informativedisclosure.)

There is, however, a practical side to thisapproach. Frivolous and misleading disclo-sures by definition entail more costs than ben-efits. Investigating the costs and benefits ofsuch disclosures is therefore not a very con-structive enterprise.

I. THE ENTITY'S INTERESTSFor our purposes the entity will be treated

as owners and employees, including manage-rial employees. Owners, of course, are a classof investors and share interests with thenonowner investors in the next section. Theseparation is justified because the entity's in-terests are hard to conceive of apart fi'om thoseof owners. The interests of owners and em-ployees can be different, but both share adominating interest in maximizing long-termcash fiow. The bigger the pie, the larger theshares to be divided, whether cooperatively orthrough conflict. "Long-term" presumes thatthe viability and earning power of the entityare not put at risk for the sake of short-termprofits.

The remarks below treat "the entity" asan individual business entity, not as the col-lected set of "entities," which creates a group.Thus, what is in "the entity's" interest neednot be in the interests of all entities as a groupor in the interests of all entities in the subsetrepresented by an industry. The "entity" is alsothe average entity Differences in circum-stances are sometimes addressed, but whenthey are not, assume the average entity.

Cost of CapitalThe entity benefits when disclosure leads

to a lower cost of capital. Disclosure accom-plishes this by helping investors and creditorsunderstand the economic risk of the invest-ment. Inadequacy and incompleteness of in-

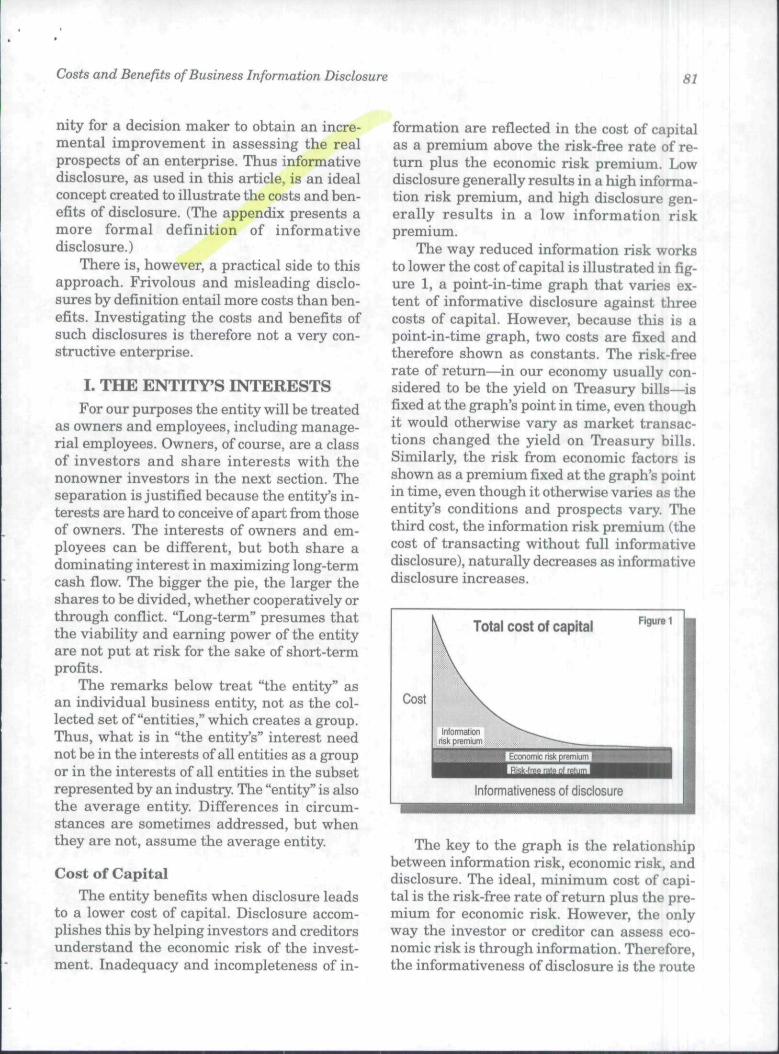

formation are refiected in the cost of capitalas a premium above the risk-free rate of re-turn plus the economic risk premium. Lowdisclosure generally results in a high informa-tion risk premium, and high disclosure gen-erally results in a low information riskpremium.

The way reduced information risk worksto lower the cost of capital is illustrated in fig-ure 1, a point-in-time graph that varies ex-tent of informative disclosure against threecosts of capital. However, because this is apoint-in-time graph, two costs are fixed andtherefore shown as constants. The risk-freerate of return—in our economy usually con-sidered to be the yield on Treasury bills—isfixed at the graph's point in time, even thoughit would otherwise vary as market transac-tions changed the yield on Treasury bills.Similarly, the risk fi-om economic factors isshown as a premium fixed at the graph's pointin time, even though it otherwise varies as theentity's conditions and prospects vary. Thethird cost, the information risk premium (thecost of transacting without full informativedisclosure), naturally decreases as informativedisclosure increases. i

Cost

\̂ Total cost of capital

\Inlofmalton ^~~—.^_^^

risk pfemium - . ^^''•'^—-~-

^ B B B B I B B l Economic risk pr&miurri||^^^B

Informativeness of disclosure

Figure 1

i\•The key to the graph is the relationship

between information risk, economic risk, anddisclosure. The ideal, minimum cost of capi-tal is the risk-free rate of return plus the pre-mium for economic risk. However, the onlyway the investor or creditor can assess eco-nomic risk is through information. Therefore,the informativeness of disclosure is the route

for the investor to arrive at the economic riskof the transfer of capital. With no informationto assess economic risk, the capital supplierwill charge a high (but not infinite) price forthe capital, a price approximating the "loanshark" rate. As the company provides moreinformative disclosure, the demanded ratesdecline, because the capital supplier has abetter and better understanding of theenterprise's economic risk. These events areshown by a curve for the information risk pre-mium that declines as informativeness of dis-closure increases and thereby approaches therisk-fi'ee plus economic-risk rate of return.

In understanding the graph, it is impor-tant to keep in mind the relationship betweenthe information risk premium and economicrisk premium. Information about a companycan give either positive or negative impres-sions of a company's prospects, and the com-bination of such types of information contrib-utes to learning the economic risk of the busi-ness. Thus when the information indicatespoor prospects, it means that the economicrisk premium is high, not that the informa-tion is functioning to raise the cost of capital.Ignorance of a company's risks (the highestlevel of information risk premium) is still anincrement above the risk-free rate of returnplus the economic risk premium. Getting abetter understanding of the true economic riskwould still lower the cost of capital.

The curve is based on the definition of in-formative disclosure given above and is oth-erwise illustrative only. It does not, for ex-ample, include the risk of misinterpretationof informative disclosure, and it does not in-clude the investor's uncertainty as to the reli-ability of the informative disclosure. Nor doesit take into account prior experiences withsuch factors. For these reasons, as well as be-cause we are talking about the average en-tity, the curve cannot be expected to accordwith every entity's cost-of-capital experience.For example, if the market misinterpreted in-formative disclosure and underestimated theeconomic risk, a company's securities wouldbe overpriced. In that situation, additional in-formative disclosure accompanying an issue

Accounting Horizons /December 1994

of new shares could correct the overestimateof the company's prospects and thereby raisethe company's cost of capital. Only if it is as-sumed that informative disclosure is misin-terpreted this way most of the time would theillustrative value of the graph be undermined.But it is far more reasonable to assume thatmisinterpretations distribute normally be-tween under- and overestimates of economicrisk, with the net result for all entities thatinformative disclosure reduces the cost ofcapital.

It is difficult to prove empirically that thecost of capital is lowered by informative dis-closure, even though it is logically and practi-cally impossible to assess an entity's economicriskiness without relevant information. Thereis abundant evidence that prices are influ-enced by disclosure (efficient markets re-search), but that is not the same as empiricalevidence that informative disclosure lowersthe cost of capital. We also know that capitalsuppliers request and sometimes demand dis-closures — that is, they sometimes make dis-closure a condition of the transaction. Presum-ably the desired information is considered rel-evant to their decision making, but, again, thisis not the same as empirical evidence that in-formative disclosure lowers the cost of capi-tal. Finally, there is anecdotal evidence, suchas the recent article by Sweeney (1994) in theNew York Times, which argued that manycompanies "realize that institutional investorsprefer to put money into companies that pro-vide lots of information and that good inves-tor relations can help their stock price."

Apart from the fact that the disclosure se-lected for testing must indeed be informative,practical problems have prevented empiricalstudy. Dhaliwal (1978), however, took advan-tage of voluntary reporting of line-of-businessinformation prior to the SEC's requirement toreport it. Using three surrogate measures tocompare the cost of equity capital for twopopulations (a control group unaffected by therequirement and a group that would disclosethe information for the first time), his find-ings were consistent with the lower-cost-of-capital thesis. ,

Costs and Benefits of Business Information Disclosure 83

More recently Conover and Wallace (1994)found that greater extent of disaggregated dis-closure for geographical segments correlatedwith higher stock prices. Their research ana-lyzed the disclosures for the year 1983 by 230multinational companies listed on the NewYork or American stock exchanges. The year1983 was chosen because it was the first yearthat FASB Statements 14 (on segments) and52 (on foreign currency translation) were bothapplicable. As compared to the market as awhole, the firms' market performance wasbetter in relation to the extent of their geo-graphic segment disclosures by a statisticallysignificant margin.

Cost of Developing and PresentingDisclosure

Owners alone ultimately pay for the costof disclosure, just as they ultimat.ely bear allentity costs. Disclosure costs include the costof gathering, processing, auditing (if the in-formation is audited), and disseminating theinformation. However, since costs affect cashflows, employees, as parts of the entity withan interest in its cash fiows, have an interestin minimizing the cost of disclosure.

The cost of developing and presenting in-formation that is also used by or needed bymanagement must be excluded from the costof developing such information for externaldisclosure. To the degree that the work hasalready been done or would be done for mana-gerial purposes, there would be no need toduplicate it. Other disclosure costs (format-ting, packaging, and disseminating informa-tion), however, would be unaffected by theoverlap between costs incurred for manage-rial purposes and costs incurred for purposesof external disclosure.

Litigation CostsLitigation can arise from allegations of in-

sufficient informative disclosure or from alle-gations of misleading disclosure. All suits thatarise from insufficient informative disclosuresupport the thesis that litigation costs de-crease with extent of disclosure.

Litigation arising from disclosure that isalleged to be misleading requires closer analy-sis. Cases of genuinely misleading disclosureare not relevant, because they cannot tell usabout the costs of informative disclosure,which we have defined as unbiased and help-ful to financial report users. Suits alleging thatinformative disclosure is misleading aremeritless, that is, they are unjust. But weknow that such suits occur and that they canimpose costs on the entity.

The costs of such suits can vary from mi-nor to very significant. Although litigation costarising from increased informative disclosureis not a regular cost for all companies, direc-tors and officers insurance is a widespread costthat is arguably attributable in significantmeasure to meritless suits. For those sued,apart from the legal fees, court awards, andthe costs of settlements made strictly as busi-ness decisions (the lesser of two cost evils),there is a cost in public relations and in thedistraction of executives from productive ac-tivities in the entity's interests.

It may be held that litigation costs increasewith the extent of informative disclosure, butit is unhkely that this is true overall. The casefor increase lies in instances where voluntarydisclosure, particularly of forward-looking in-formation, followed by share-price declines,have led to allegations of fraudulently mis-leading disclosure. Such suits have beenwidely protested by the financial-reportingcommunity and cited in Congressional hear-ings. Their existence raises the question of therelationship between the population ofmeritless suits and the population of volun-tary informative disclosures that did not re-sult in suits. The latter population is presum-ably by far the larger, and it weighs againstthe thesis that litigation costs increase withextent of informative disclosure increases. Inaddition, four other perspectives must bebrought to bear: \\ [

• First, fuller disclosure should lead tosmaller claims because the stock marketwould have more realistic expectations ofthe company's prospects. The smaller the

84 Accounting Horizons /December 1994

discrepancy between the valuation implicitin the market price and the valuationbased on the company's true prospects, thesmaller declines in share prices from dis-appointed expectations. Since damages arebased on the extent of the decline, thesmaller declines would lead to smallerdamage claims.

• Second, defendants would have better de-fenses. Assume, for example, richer disclo-sure of enterprise risks. Defense attorneyscould point to such disclosures to arguethat the plaintiffs were adequately in-formed of the potential decline in shareprices. This would increase the proportionof cases won by defendants and reduce thesettlement amounts. The more importanteffect is the reduction in settlementamounts, because the cost of pursuing liti-gation leads to the settlement of most se-curities class actions.

• Third, there would be fewer suits as a con-sequence of the two conditions just cited.A higher proportion of the share price de-clines would be too small to justify a suit.Better defenses from richer disclosurewould warn class-action attorneys thatthey would have a more difficult time win-ning and gain less in settlement. Thiswould also be factored into class-actionattorneys' decisions to bring suit.

• Fourth, the relationship between shareprice volatility and meritless suits raisesthe question of the degree to which thenature of the business rather than extentof disclosure is the reason for a given suit.In instances where companies volunteeredforward-looking information and were sub-sequently sued after share-price declinesfor allegedly misleading investors, extentof disclosure is causative, if not the onlycause. However, because of the way inwhich these suits occur, triggered by de-clines in share prices, the nature of thebusiness is a major factor.For these reasons, we can conclude that con-

sidered in full context, litigation costs causedby meritless suits decrease, rather than in-crease, with increasing extent of disclosure.

Competitive DisadvantageDisclosure that would weaken a company's

ability to generate future cash flows by aid-ing its competition is not in the interests ofthat company's employees and owners. Pub-lic companies have traditionally been verysensitive about disclosing information thatmight create competitive disadvantage, andprivate companies, though not faced with pub-lic disclosure obligations, sometimes showsimilar concern (for example, about whethera supplier who receives disclosure reveals suchinformation to the disclosing company's com-petitor who is also the supplier's customer).

The types of information that might cre-ate competitive disadvantage are:

• Information about technological andmanagerial innovation (e.g., productionprocesses, more effective quality-improve-ment techniques, marketing approaches).

• Strategies, plans, and tactics (e.g., plannedproduct development, new market target-ing).

• Information about operations (e.g., seg-ment sales and production-cost figures,workforce statistics).^The level of potential competitive disad-

vantage from disclosure in the categoriesabove varies considerably, from zero to veryhigh. Some operational data create no com-petitive disadvantage. However, segment prof-itability data could allow competitors to con-centrate on the most profitable areas of thedisclosing entity's business. A potential com-petitor could learn something about the capi-tal investment required to enter into compe-tition. Disclosing product development planscould lead a competitor to develop the samekind of product, with a race to the market-place, or it could lead to counter-product de-velopment that would render a planned prod-uct either less attractive when it was releasedor soon to be leap-frogged. Information on tar-geting new markets could lead to defensive

^Stevenson (1980, 9-11) provides these categories andgives some examples within the categories. More areavailable in Mautz and May (1978), for example, onpp. 95-96

Costs and Benefits of Business Information Disclosure 85

measures, such as increased advertising. In-formation on technological innovation couldhelp lead competitors to improvements of theirown.

The key factor in determining whether in-formation in the categories above creates com-petitive disadvantage is timing. Products indevelopment eventually come to market.Strategies become obvious from actions, andinformation about them can then no longerlead to competitive disadvantage. At some agedisclosure simply loses its capacity to createcompetitive disadvantage. A given category ofdisclosure can be competitively disadvanta-geous or competitively meaningless depend-ing on when the disclosure is made.

The role of timing suggests the possibilityof differential disclosure based on estimatedrisks of competitive disadvantage. For ex-ample, capital suppliers might receive disclo-sures promptly under agreement with the dis-closing entity to keep the disclosures confiden-tial. The disclosure would be released publiclyonly when time has reduced or eliminated theestimated risks of competitive disadvantage.

Timing is not the only factor that deter-mines the level of competitive disadvantagefrom disclosure. Other factors implicit in theexamples above are the type of information,the level of detail, and the audience for thedisclosure. We have already noted that rou-tine operating data is less likely to cause com-petitive disadvantage than information onproduct development. But the greater the levelof detail about new product plans—for ex-ample, including all unique features and thereasons for their potential appeal—the greaterthe likelihood of competitive disadvantage. Fi-nally, as shown by the example of restrictingdisclosure to capital suppliers under confiden-tiality agreements, the parties with access toa disclosure determine its influence on com-petitive disadvantage.

Even with awareness of the factors justcited, it is difficult to generalize or be certainabout the effect of particular disclosures oncompetitiveness. For example, the potentialcompetitor determining the investment hurdleto enter an industry might as likely be dis-

suaded by the disclosures as convinced to be-come a competitor. Japanese companies' leadin analog HDTV would have suggested thatalmost any information about their technol-ogy was competitively disadvantageous, butthe absence of such information was probablya factor in the move to a digital approach thatappears to have given U.S. companies a tech-nological lead. ]' I

There is also disclosure behavior that runscounter to the notion of competitive disadvan-tage. New products are sometimes announcedearly in order to convince competitors themarket has been taken and to give the prod-uct a headstart in name recognition. An-nouncements of new products and plannedproducts are also a form of public relations,keeping a corporate name in the public mindassociated with progress. Finally, productplans are often revealed to capital suppliersin order to keep or win their support.

There is a vast difference between the pur-pose of disclosure to investors and creditors,on the one hand, and competitors' purposes,on the other. The purpose of disclosure to in-vestors is to help them to estimate the amount,timing, and certainty of future cash fiows frominvesting in the disclosing entity. Competitorsare not trying to predict the enterprise's fu-ture cash fiows, and information solely of usein that endeavor is not of use in obtaining com-petitive advantage. Overlap between informa-tion designed to meet investors' needs andinformation designed to further the purposesof a competitor is therefore coincidental.

Every entity that could suffer competitivedisadvantage from disclosure could gain com-petitive advantage from comparable disclo-sure by competitors. There cannot be competi-tive disadvantage to one entity without oneor more others gaining competitive advantage.Assuming it is required, competitors wouldhave access to each other's disclosures. Thissuggests a net equality of competitive advan-tage and disadvantage for each enterprise.However, individual circumstances would un-doubtedly differ. A technological leader wouldpresumably have more to lose in reciprocatedtechnological disclosure than a technological

86 Accounting Horizons / December 1994

laggard. And those subject to direct competi-tion from foreign companies with lower levelsof disclosure could suffer competitive disad-vantage from disclosures used by those com-petitors without access to the reciprocal dis-closure that could bring offsetting competitiveadvantage. Nevertheless, for any given entity,competitive advantage from others' disclo-sures or the potential for such advantage mustbe counted along with whatever competitivedisadvantage stems from that entity's owndisclosures.

This creates the concept of net competitivedisadvantage from disclosure. It would varyfrom entity to entity and from time to time,could be positive or negative, and could there-fore also be called net competitive advantagefrom disclosure.

At least one distinguished CFO believesthat disclosure of research ideas to competi-tors benefits the entity because it enhancesresearch productivity. Here is the way JudyLewent, CFO of Merck, explained her thought.

We know that in order to advance swiftly to-ward successful research, it is often neces-sary to have our competitors working veryclosely in the same area. For example, I'mconvinced that our research productivity isenhanced because so few boundaries existamong scientists at different companies anduniversities and at government-sponsoredresearch at the National Institutes of Health.Tremendous spillover benefits arise as a re-sult of scientists' propensity to publish andexchange ideas, particularly at the discoverystage; yet this in no way diminishes thehighly competitive nature of the research pro-cess. (Nichols 1994, 97-98)

Put another way, reciprocal disclosure canbe mutually beneficial because of the fillip itgives to the rate of technological progress. Theimproved rate brings advantages sooner.

There is some interaction between com-petitive disadvantage and other costs and ben-efits of disclosure. The cost of developing andpresenting disclosure reduces competitivenessto the degree that it exceeds competitors' simi-lar costs. The same is true of any litigationcosts arising from disclosure. A lower cost ofcapital from disclosure improves competitive-ness, and good relations with capital suppli-ers could help do the same.

Entity BehaviorEntities sometimes alter their behavior in

response to disclosure requirements or the in-formation that is disclosed, and the behaviorcan lead to costs or benefits. Today, there istalk of developing substitutes for stock optionsin the event the FASB requires that the costsof such options be recognized. The FASB's pro-nouncement on postretirement benefits otherthan pensions acknowledged the argumentthat preparers would change the designs oftheir postretirement benefit plans or the waythe plans were financed (FASB 1990, par. 130).

However, disclosure-responsive economicbehavior may decrease as well as increasecosts. Developing new approaches to remu-neration to replace stock options is a cost thatwould be borne by the entity. The postretire-ment benefits statement, on the other hand,contributed to an increasing appreciation ofthe dimensions and growth of health benefitscosts and the need to control them.

It is very difficult to predict the results ofdisclosure on enterprise behavior. The immi-nent adoption of the FASB's pronouncementon contingencies in 1975 led to predictionsthat corporate risk and insurance manage-ment would be changed (e.g., increased limitson insured exposures, increased legal expen-ditures, changed coverages to accommodateincreased exposures from the disclosure re-quirements, revised insurance and rein-surance contracts by captive insurance com-panies). There was concern about adverse con-sequences. In a study performed after theStatement was issued, however, Goshay(1978) found that there were no impressivedifferences between the risk management de-cisions of the companies he studied and thoseof a control group.

The FASB's first statement on foreign cur-rency translation in 1975 evoked controversyover potential costs in enterprise behavior. Apost-issuance study three years later did findbehavioral changes in foreign exchange riskmanagement as a result of the new require-ment. However, some of the changes were ben-eficial (for example, companies became moreaware of exchange risk and more sophisticated

Costs and Benefits of Business Information Disclosure 87

in evaluating the cost of foreign currency loantransactions). The researchers could not con-clude either that the increased level of re-sources devoted to exchange risk managementresulted in significant cash flow benefits orthat the disclosure requirement's effects wereof overall benefit or detriment to entities orsociety at large (Evans et al. 1978, 15-20).

There seems no basis for concluding thatextent of disclosure results either in net dam-age from enterprise behavior or net benefits.Each case is unique. However, if new disclo-sure is truly informative and previouslyunderappreciated by enterprise management,as was the case with the costs of postretire-ment medical benefits, there is likely to be anet economic benefit.

An important element of entity behavioris the exercise of corporate suffrage and deci-sions by directors. Information prepared forexternal reporting also contributes to corpo-rate suffrage and directorial decisions.^ TD thedegree that informative disclosure to inves-tors and creditors serves the health of a cor-porate entity by enabling those who partici-pate in corporate governance as shareholdersor directors to make wise decisions that af-fect the entity's future economic success, it isa benefit.

Public RelationsDisclosure can have public relations ben-

efits. For our purposes, the primary public-relations issue is relations with the invest-ment community

Investors and creditors get impressions ofcompanies' openness and forthrightness. Amore formal assessment is the annual evalu-ation of corporate financial reporting by theAssociation for Investment Management andResearch. Each year the Association's Corpo-rate Information Committee rates the qual-ity of reporting in 31 industries. Financialanalysts aware ofthe companies that receivedawards for excellence are likely to have a morefavorable impression of those companies be-cause of it.

Corporate citizenship is another aspect ofpublic relations served by disclosure. Busi-nesses discharge some part of their account-

ability obligations to the community throughdisclosure.

Cost Summary 1"The major entity costs from informative

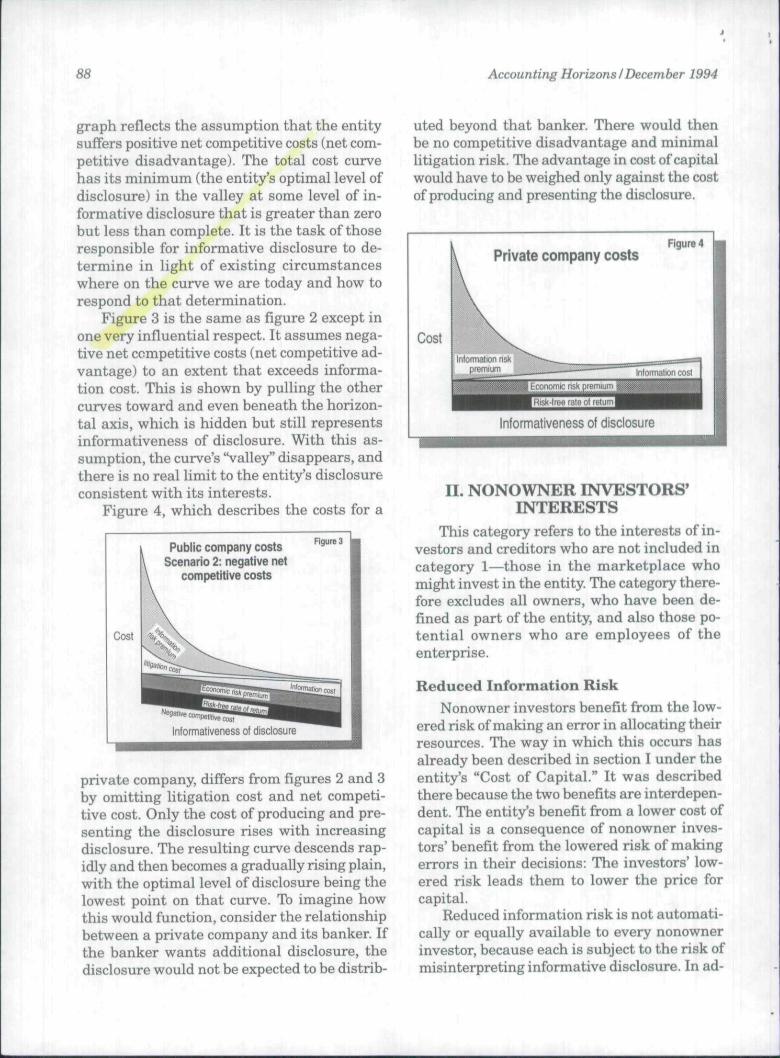

disclosure that have been discussed in this sec-tion are summarized in figures 2, 3, and 4.These treat in sequence the total cost of in-creasing disclosure for a public company as-suming positive net competitive costs, for apublic company assuming negative net com-petitive costs, and for a private company,where competitive disadvantage and litigationare omitted as, relatively speaking, insignifi-cant cost risks.

As with figure 1, these graphs reflect costsat a point in time, hypothetically varying onlyextent of disclosure and describing by thecurves estimated cost changes from thosevariations. (Future cost changes from othercircumstances are treated in section IV below.)Again the graphs are illustrative only. Thecurves are estimates. 1, |

In figure 2, two costs decrease with moreinformative disclosure (information risk pre-mium and litigation cost) and two increase (in-formation cost and net competitive cost). The

Cost

Public company costsScenario 1: positive net

competitive costs

Figure 2

jrmaliveness of disclosure

^Statement of Financial Accounting Concepts No. 1notes: "Financial reporting should provide informationabout how management of an enterprise has dis-charged its stewardship responsibility to owners(stockholders) for the use of enterprise resources en-trusted to it. Management of an enterprise is periodi-cally accountable to the owners .... Financial repori;-ing should provide information that is useful to man-agers and directors in making decisions in the inter-ests of owners." (FASB 1978, pars. 50, 52)

88 Accounting Horizons /December 1994

graph reflects the assumption that the entitysuffers positive net competitive costs (net com-petitive disadvantage). The total cost curvehas its minimum (the entity's optimal level ofdisclosure) in the valley at some level of in-formative disclosure that is greater than zerohut less than complete. It is the task of thoseresponsible for informative disclosure to de-termine in light of existing circumstanceswhere on the curve we are today and how torespond to that determination.

Figure 3 is the same as figure 2 except inone very influential respect. It assumes nega-tive net competitive costs (net competitive ad-vantage) to an extent that exceeds informa-tion cost. This is shown by pulling the othercurves toward and even beneath the horizon-tal axis, which is hidden but still representsinformativeness of disclosure. With this as-sumption, the curve's "valley" disappears, andthere is no real limit to the entity's disclosureconsistent with its interests.

Figure 4, which describes the costs for a

Public company costsScenario 2: negative net

competitive costs

private company, differs from figures 2 and 3by omitting litigation cost and net competi-tive cost. Only the cost of producing and pre-senting the disclosure rises with increasingdisclosure. The resulting curve descends rap-idly and then becomes a gradually rising plain,with the optimal level of disclosure being thelowest point on that curve. Tb imagine howthis would function, consider the relationshipbetween a private company and its banker. Ifthe banker wants additional disclosure, thedisclosure would not be expected to be distrib-

uted beyond that banker. There would thenbe no competitive disadvantage and minimallitigation risk. The advantage in cost of capitalwould have to be weighed only against the costof producing and presenting the disclosure.

Private company costsFigure 4

informativeness of disclosure

Cost

II. NONOWNER INVESTORS*INTERESTS

This category refers to the interests of in-vestors and creditors who are not included incategory 1—those in the marketplace whomight invest in the entity. The category there-fore excludes all owners, who have been de-fined as part of the entity, and also those po-tential owners who are employees of theenterprise. ,

Reduced Information RiskNonowner investors benefit from the low-

ered risk of making an error in allocating theirresources. The way in which this occurs hasalready been described in section I under theentity's "Cost of Capital." It was describedthere because the two benefits are interdepen-dent. The entity's benefit fi'om a lower cost ofcapital is a consequence of nonowner inves-tors' benefit from the lowered risk of makingerrors in their decisions: The investors' low-ered risk leads them to lower the price forcapital.

Reduced information risk is not automati-cally or equally available to every nonownerinvestor, because each is subject to the risk ofmisinterpreting informative disclosure. In ad-

Costs and Benefits of Business Information Disclosure 89

dition, depending on the type of new informa-tion provided, there will he a learning curvein taking advantage of it. Nevertheless, thebasic relationship between informative disclo-sure and nonowner investors remains thatinvestors' likelihood of allocating their capi-tal unprofitably diminishes with the increaseof informative disclosure.

The benefit of lower information risk ac-cruing to nonowner investors generates ben-efits to other interests. In fact, it is a greatengine of such benefits. We have already notedthe interdependence between the entity'slower cost of capital and investors' reduced in-formation risk. In addition, the national in-terest in effective capital allocation and mar-ket liquidity depends on nonowner investorsand creditors acting on disclosure in their de-cision making. Similarly, reduced informationrisk is integral to the social benefit of con-sumer protection.

CostsPotential owners obtain the benefits of dis-

closure without the costs. They are free rid-ers, not paying the costs of litigation, competi-tive disadvantage, or developing and present-ing disclosure. However, they would pay thesecosts if they became owners in the sense thatthe stream of cash fiows to the entity wouldbe curtailed by the costs the potential ownershad previously avoided as fi-ee riders.

III. THE NATIONAL INTERESTSome may question whether the costs and

benefits to the national interest should beweighed in evaluating disclosure, taking theposition that accounting should be neutral inthe sense of not being entwined with issues ofpublic policy. However, neutrality in account-ing in the sense of focusing on effective eco-nomic measurement is consistent with thenational interest, and such accounting neednot be entwined with narrower issues of pub-lic policy. There is no question that the fullrange of costs and benefits from disclosureincludes those that fall to the national inter-est. Interpretations of the national interest inspecific accounting issues are cited in public

debate; the FASB's mission statement con-tains a national-interest paragraph;"* and thesecurities laws' establishment of a statutorydisclosure system is Congressional testimonyto the fact that corporate disclosure is a mat-ter of national interest. These reasons and ci-tations suggest that the national interestshould not be excluded in considering the costsand benefits of informative disclosure.

The U.S. national interest is lodged in theconcept of the greatest good for the greatestnumber. As with individuals, there is a differ-ence between enlightened and unenlightenedinterests. On the national level it consists pri-marily of short-term (unenlightened) as op-posed to long-term (enlightened) interests.The remarks below refer to long-terminterests.

Cost of CapitalI

To the degree that disclosure contributesto lower capital costs, it is in the national in-terest. Low capital costs are desirable for theircontribution to economic growth, jobs, and animproved standard of living. All these followfrom the fact that low capital costs increasethe rate of investment by entities. I' |

The exception to the generalization thatlow capital costs are in the national interestis when infiation is being fought by highercapital costs. Even then, the national inter-est is served by the lowest cost of capital con-sistent with controlling infiation. More impor-tantly, disclosure is not a useful technique inraising capital costs. Such a course (tempo-rarily decreasing informative disclosure) ismore likely to lead to chaos than macroeco-nomic benefits. Federal Reserve and fiscalpolicy, the accepted tools, are unquestionablymore efficient and effective.

^"Accounting standards are essential to the efficientfunctioning of the economy because decisions aboutthe allocation of resources rely heavily on credible,concise, and understandable financial information.Financial information about the operations and finan-cial position of individual entities also is used by thepublic in making various other kinds of decisions."(FASB 1987, par, 2)

90 Accounting Horizons /December 1994

Effective Allocation of CapitalThe national interest in effective alloca-

tion of capital cannot be underestimated. Ithas been of concern in recent years, with in-creased international competition. That is oneof the explanations for "industrial policy" andstudies on building competitiveness. Rich dis-closure contributes to effective allocation ofcapital by enabling investors and creditors toidentify the most productive enterprises. Un-wise investments are bad for economic growthand national competitiveness. Apart fi"om theobvious case of an investment that quicklyends in bankruptcy, companies capable of highlevel performance should have adequate sup-plies of capital.

The effective allocation of capital refers tomore than the allocation of financial capital.It also includes human capital because humancapital tends to fiow to the best opportunitiesand informative disclosure helps talentedpeople identify the best opportunities. Withthe increasing rate at which financial capitalflows across borders, human capital, whichcrosses borders at a much slower rate, iswidely recognized for its contribution to na-tional competitiveness. '

LiquidityDisclosure contributes to the liquidity of

the capital markets, also a benefit to the na-tional economy. A more liquid market assiststhe effective allocation of capital. Liquidityvaries according to the bid-ask spread. Thewider the bid-ask spread the less liquidity (i.e.,fewer transactions take place), and the nar-rower the bid-ask spread the greater the li-quidity {i.e., more transactions take place).Two principal determinants of the bid-askspread are the degree of information asym-metry between the buyer and seller and thedegree of uncertainty of the buyer and theseller. Both larger asymmetry and greateruncertainty widen the spread, but lower asym-metry and less uncertainty—two products ofbroad, public disclosure—diminish it, therebyincreasing liquidity.

National Competition AmongBusinesses

If there are indeed competitive advantagesand disadvantages from entity disclosure,there must be a resulting increase in the in-tensity of competition. Tb the degree that dis-closure adds to competition among U.S. busi-nesses, other things being equal, it serves thenational interest.

Vigorous competition among businessesleads to greater efficiency and national com-petitiveness. This has been part of our na-tional political ideology and law for genera-tions (e.g., the anti-trust laws and the FTC'smandate to fight restraints on trade). Econo-mists and public policy-makers support theidea that competition is needed for long-termeconomic growth, and anticompetitive fea-tures in other societies are widely cited to ex-plain slow growth and difficulties in emerg-ing fi'om recession.

The U.S. is not, of course, a land of unfet-tered competition. There are types of tradeprotection and subsidies that reduce the vigorof marketplace competition. Although theseinconsistencies often refiect the power of rela-tively narrow interests or concern for theirplight, rather than the national interest in itsfull breadth, there is also a set of inconsisten-cies based on national security needs and asmaller set based on the economic policy ofassisting research-and-development projectsconsidered underfunded and promising. How-ever, national policy and our economy, on bal-ance, are heavily weighted toward market-determined economic decisions, which meansfree and fair competition.

Apart from the exceptions just cited, thereare specific devices to give monopoly advan-tages to companies and other economic agents.These are patents, copyrights, and trade se-cret law.** Their economic rationale is that a

''The subject matter of a trade seeret may be a formula,machine, process, or compilation of information thatconfers competitive advantage and that is known onlyto its owner and employees (Stevenson 1980, 15-16).

Costs and Benefits of Business Information Disclosure 91

certain level of anticompetitive advantage isnecessary to encourage innovation and risktaking. Other justifications can be made basedon notions of fairness and ideas of property,but only the economic rationale is of interesthere.

Three conclusions follow from the exist-ence of these devices and their economic ra-tionale. First, our society recognizes that thereshould be limits on competition. Second, in thecase of trade secret law, our society recognizesthat there must be some protection againstunauthorized disclosure even if it is anticom-petitive. (Patents and copyrights are not lim-its on disclosure; they are forms of disclosurethat are accompanied by monopoly rights toprotect competitive advantage.) Third, discus-sions of competitive disadvantage from disclo-sure must consider that these devices protectcompetitive advantage that otherwise mightbe lost from disclosure.

There are limits to the need for anti-com-petitive devices to encourage innovation andrisk taking. First, in our economy most inno-vation and risk taking is encouraged by theprofit motive functioning apart from anticom-petitive devices and, ironically, by competition.Innovation enables one competitor to stay£Lhead of another as does risk-taking invest-ment in cost-lowering technology. Second, onceconferred or otherwise in hand, monopolyrights function as a drag, rather than a spur,to innovation and risk taking. They are a spuronly when they are a profit-protecting prizeto be sought.

We can conclude that the existence ofanticompetitive devices does not alter the gen-eralization that, other things being equal,disclosure's encouragement of competition isin the national interest.

International CompetitionForeign corporations selling to the U.S.

market do not have in their home countriesthe same disclosure requirements that U.S.corporations have here. It is typically morecostly for U.S. firms to prepare disclosure un-der the U.S. requirements, a competitive dis-advantage. Another potential competitive dis-

advantage is that U.S. disclosures allow for-eign competitors to know more about publiclytraded U.S. firms than such firms know aboutcompetitors from abroad.

The competitive advantage overseas firmshave from lower disclosure requirements intheir home countries could be cured by tariffsor other forms of trade restriction. Althoughthe debate over free trade is beyond the scopeof this article, the context puts the competi-tive-cost issue in a different light.^ The differ-ence in costs of disclosure can be seen as oneof many cost differences that go into the eco-nomics of international trade. U.S. spendingper pupil in excess of competitors', for ex-ample, could be considered a subsidy to thebusinesses that pay more for disclosure thantheir foreign competitors. Such cost differ-ences are ingredients in the mix of compara-tive advantages that drives trade.

U.S. firms also compete with foreign cor-porations in third-country markets. Again, thecompetitive advantage derived from disclosureis one of the full set of cost differences that gointo the economics of international trade.Trade restrictions, however, are not an optionin such cases.

One mentioned remedy, assuming it wereavailable, is the so-called level playing field,a U.S. level of disclosure identical to the lev-els in foreign competitors' home countries.However, equality of disclosure by itself is nota rational approach to the national interest.It ignores the quality and sufficiency of dis-closure. No disclosure, foreign or domestic,creates a playing field as level as any other.An approach that totally ignores the objectivesof effective capital allocation and the interestsof investors cannot be considered rational. Thebenefits of informative disclosure obviouslyweigh against leveling by reduced disclosure.Moreover, the U.S. has long had a distinctionbetween public-company disclosure require-ments and private-company disclosure re-quirements that is inconsistent with a purelylevel playing field on disclosure.

a concise modern statement of free trade argu-ments, in the context of a rebuttal, see Bhagwhati(1988).

92 Accounting Horizons / December 1994

There is also the question of what is meantby a "playing field." A disclosure system is onlypart of a capital allocation system and cannotbe understood out of that context. This pointis made in the study on national competitive-ness by Michael Porter of Harvard BusinessSchool for the Council on Competitiveness(1980, 83, 85). Porter notes that German andJapanese enterprises have fewer external re-porting requirements, but have closer, long-term relationships with dominant owners,who are informed by other mechanisms. Inthis way Porter justifies recommending moreand better disclosure in the U.S. to improvecapital allocation in the interest of nationalcompetitiveness. For our purposes, the differ-ences among national capital allocation sys-tems means that comparisons based on dis-closure alone must be considered incomplete.

Globally harmonized disclosure standardsthat adequately serve users' needs and meetcost-benefit tests would end the problem ofinternational differences in disclosure. Butthat is down the road. For the present, it isimportant to note that U.S. companies canraise capital abroad if they choose to or en-gage in private placements in the U.S. Theirdecisions to stay in the U.S. public marketsuggest its advantages outweigh its disadvan-tages. The advantages include low cost andliquidity that are partly attributable todisclosure.

The U.S. also has an interest in attract-ing overseas firms to its capital markets. How-ever, the arguments that apply to the nationalinterest in the disclosures of domestic issuersapply to foreign issuers. It is again in the na-tional interest, for example, that the stock ofU.S. capital be effectively allocated and for themarkets to be liquid. If attracting foreign is-suers is in the national interest, the benefitof lower capital costs from fuller disclosureserves that interest.

Litigation CostsLitigation arising from informative disclo-

sure—i.e., meritless suits—creates a socialcost. There is evidence that high-tech compa-nies, with high share-price volatility, have

been particular targets, sued when theirshares decline. Thus it is arguable thatmeritless suits have their greatest infiuenceon the smaller, cutting-edge firms that con-tribute disproportionately to economic growthand job creation.

As described in section I, there are vari-ous components to the costs of litigation, butin sum they weaken enterprises financiallyand distract them from their economic mis-sions. The national cost is a less effectiveeconomy. There are also costs in economicgrowth from a higher cost of capital (since thethreat of litigation has curtailed disclosure)and from less effective corporate governance(since independent directors, fearing liability,are harder to obtain).

Consumer ProtectionDisclosure plays a major role in the

government's consumer protection efforts.This includes regulated disclosures on prod-uct labels, in advertising, and in lending. Forour purposes, the important element is theconsumer-protection aspect of corporate finan-cial disclosure. The SEC regulates corporatefinancial disclosure largely to protect the in-terests of investors and creditors, the consum-ers of corporate securities. To the degree thatinformative disclosure provides needed con-sumer protection, other things equal, it is abenefit in the national interest.

ExternalitiesSociety has an interest in the externali-

ties of business operations (e.g., environmen-tal pollution and effects on communities). Fed-eral and local governments have acted in allsorts of ways to regulate externalities andremedy their effects. Measurement and dis-closure have been a key part of these efforts(e.g., the environmental impact statement). Tbthe degree that public disclosure by businessentities (e.g., risks and uncertainties) assistsgovernments in assessing problems caused byexternalities and making socially useful deci-sions in response, disclosure is in the nationalinterest.

Costs and Benefits of Business Information Disclosure 93

IV. LOOKING TO THE FUTUREA full consideration of costs and benefits

includes hov\̂ they could change in the future.The objective is to contribute some perspec-tive on long-term, net costs and benefits. Manyof the generalizations below depend on theconclusions reached above, but only major fac-tors are considered.

For the entity, the lowered cost of capi-tal would continue to be a benefit. If we pre-sume additional informative disclosure, thebenefit should increase. The rate of increasedepends on the degree of informativeness ofcurrent disclosure. If it is very high, only mar-ginal improvements are available. Researchon the needs of financial report users wouldclarify this.

The cost of developing and presentingtoday's disclosure will decrease in the futureprimarily because of advances in informationtechnology. A greater overlap between mana-gerial information needs and those of inves-tors and creditors should have a similar, ifsmaller, effect. If we postulate increasing dis-closure, there would still be a cost-of-prepa-ration decline in the long term. In the future,information technology will totally transformthe economics of developing and presentingdisclosure.

Litigation cost is extraordinarily difficultto predict because of possible changes in lawsand regulations. Additional safe harbors forforward-looking information, for example, area genuine possibility. An extrapolation fromtoday's litigation costs suggests significantincreases in the future, but such increaseswould not bear a one-to-one relationship withlitigation costs from increased informativedisclosure. Tbday's costs derive from merito-rious as well as meritless suits, and manymeritless suits originate in business volatil-ity that precipitates drops in stock prices, notincreased extent of disclosure. When consid-ered in full context, increased informative dis-closure, as we have seen, should reduce liti-gation exposure.

Greater informative disclosure would in-crease competitive disadvantage for publicentities, but not sharply. The mitigating cir-

cumstances cited above would continue tolimit the level of disadvantage. Competitorswill improve their ability to learn fi-om infor-mative disclosure, which would help to maxi-mize competitive disadvantage for disclosingcompanies, but this would be partly offset bythe increasing dependence of business on sci-ence and technology and the advantage ofmore rapid fi-uition of profitable ideas fi-ommutual disclosure. If the level of disclosure byU.S. public companies increases faster thanthat of foreign companies, competitive disad-vantage from foreign competitors' use of in-creased disclosure by U.S. companies willgrow. However, if the reverse occurs (the levelof disclosure by foreign competitors increasesfaster than that of U.S. companies), competi-tive disadvantage to U.S. public companiesfrom added disclosure will decrease.

Nonowner investors' benefits from in-formative disclosure would increase in the fu-ture as those disclosures increased. Again, therate of increase depends on the degree of in-formativeness of current disclosure.

Information overload has long been an im-portant concern, but the analytical power ofinvestors and creditors, assisted by comput-ers and software, should keep pace with anylikely increase in informative disclosure. Atthe moment, institutional investors and credi-tors have access to greater analytical powerthan is necessary for current levels of disclo-sure. The only potential caveat in this scenarioapplies to individual investors. As a group,they would be less well prepared to benefit byprocessing additional disclosure than institu-tional investors, but should nevertheless. Ef-ficient market research shows that securitiesprices refiect all publicly available informa-tion, which means that individual investorswould benefit fi"om information analyzed byinstitutional investors. In addition, many in-dividual investors rely on investment advisorswho would either perform or have access toanalyses of additional informative disclosure.Finally, any substantial market demand forsimplified analytical software is likely to befilled, making it possible for an increasingnumber of individual investors to perform

94 Accounting Horizons I December 1994

their own analyses of increased informativedisclosure.

The national interest in informative dis-closure will continue and will become stron-ger. The advantages of lower cost of capital,market liquidity, increased competition in thebusiness world, and, most importantly, effec-tive allocation of capital would improve withgreater informative disclosure. The nationalinterest in consumer protection and corporateexternalities should grow only moderately, inpart because they are, in the circumstances,rather high at the moment. Their standing ismasked by the difficulty in getting any issueat the top of the national agenda and by theparamountcy of economic growth and jobcreation.

SummaryIn light of the trends just discussed and

recalling figures 2, 3, and 4, we can ask, first,whether the optimal level of informative dis-closure is likely to increase or decrease in thefuture when viewed solely fi-om the entity'sperspective. However, unlike figures 2, 3, and4, the costs would be changing over time,rather than responsive to hypothetical in-creases in disclosure as of today.

The dominant trend appears to be the rap-idly decreasing costs of preparing and com-municating disclosure. This would increasethe optimal disclosure level for private com-panies. For public companies, unless competi-tors develop the capability to impose signifi-cantly greater competitive disadvantagesthrough use of the information or litigationcosts become more perverse, the most likelyresult is that the optimal level of disclosurewill increase in the future. This applies bothto public companies with negative net com-petitive cost from increased disclosure (com-petitive advantage) and for those with posi-tive net competitive cost.

The second information-technology trend,users' greater power to access and interpretinformation, will increase all users' benefits.Users* interests in increased disclosure areconsistent with an increase in the opti-mal level of disclosure from the entity'sperspective.

These changes would be consistent withthe national interest. From the perspective ofthe national interest, an increase in the opti-mal level of disclosure would be a long-termbenefit.

V. THE LIMITS OF COST-BENEFITANALYSIS

Cost-benefit analysis of disclosure is lim-ited in its effectiveness by the nature of socialdecision making, which certainly includes set-ting accounting standards. Nobel-laureateKenneth J. Arrow's studies of collective deci-sion making found that ideal outcomes couldnever be a direct aggregation of constituentpreferences (Arrow 1983). Thus, assuming,fanciful though it may be, that decision-mak-ers determining business disclosure had ab-solute knowledge of every individual and or-ganizational self-interest in terms of dollar-denominated costs and benefits, it would beimpossible to reach a decision that gave thosepreferences equal treatment. No social pref-erence can directly reflect the rank orderingof all constituents' diverse preferences.

These constraints suggest that mecha-nisms for social decision making need to domore to achieve socially desirable ends thantote up representations of constituents'inter-ests or their preferences, even if they claimbacking in cost-benefit data. The constraintsalso suggest that judgments must be broughtto bear to make tradeoffs. Public-interest ob-jectives can help, and so can procedures toensure due consideration of the interests ofall relevant parties, including those in-terests not vehemently expressed or evenunexpressed.

The limited use of cost-benefit informationsuggests the FASB was wise to add this quali-fication to its mission-statement precept onweighing the views of constituents: "The ulti-mate determinant of concepts and standards,however, must be the FASB's judgment, basedon research, public input, and careful delib-eration, about the usefulness of the resultinginformation" (FASB 1987, 3).

Even if it cannot be decisive by itself, ad-ditional academic research on the costs and

Costs and Benefits of Business Information Disclosure 95

benefits of disclosure could be very helpful. Re-search could advance our knowledge and im-prove cost-benefit evaluations. The authorityof credentialed researchers can drive home fi-nally the fact that a full set of dollar-denomi-nated costs and benefits is a hopeless quest.Ideally, research on costs and benefits wouldhave balance. Increases in studies of costs or

benefits alone, or a population of studiesheavily weighted toward one of the two, couldhave a one-sided effect on the public dialog.That would be unfortunate, because one of thepotential contributions of cost-benefit researchis to help ensure that all parties with a stakein disclosure decisions receive the attentionworthy of that stake.

APPENDIXInformativeness of Disclosure

Although the text and graphics in this article are heuristic, it is possible to take a more formal,information-theoretic view of the informativeness of disclosure. Under this approach, the informationcontent of a message is defined as its capacity to reduce uncertainty (i.e., increasing informativeness ofdisclosure equates to decreasing investor imcertainty which leads to a decreasing information risk premiumdemanded by investors). Uncertainty reduction is inversely related to the ex ante probability of receivinga particular true^ and relevant'' message: the more improbable the message ex ante, the more informative.For example, the reliable message that a particle moved faster than the speed of light has zero probabilityex ante, thus infinite information value to a theoretical physicist (but not a teeny bopper). The reliablemessage that a building is on fire has very low ex ante probability, thus very high informativeness to anoccupant. The response "fine" to the question "how are you?" has very high ex ante probability, thus verylow information content. It is well known, for example, that stock prices do not respond to eamings-per-share announcements that equal the expected amounts, but do respond to surprising eamings-per-shareannouncements. I

To express the idea formally, the information content, I^, of a reliable, relevant message, M, equalsthe logarithm of the reciprocal of the ex ante probability of receiving the message (I^ = log^il/piM))).^ Theinformation content of multiple, nonredundant messages is the sum of the contents of the individualmessages. Nonredundancy is expressed as a conditional probability:

Thus X values in figures 1 through 4 in this article can be defined as

X =

where n is the number of messages disclosed.1=2

^If messages were dichotomized as true or false, then true messages would have information content and falsemessages would not. Of course, real messages are not generally dichotomous with respect to truth. Rather, theyhave degrees of reliability, which might be measured, for example, by their standard errors of estimate: the smaller(larger) the standard error, the greater (lesser) the reliability. For simplicity, this appendix assumes highly reliable(i.e., essentially true) messages.

'Investor uncertainty does not refer to a generalized state of mind, but rather to a specific decision problem, such ashow much shares of company X are wortb. Only information tbat reduces uncertainty witb respect to that estimateis relevant for purposes. If an investor were trying to decide tbe worth of shares of company X, tbe receipt ofreliable news tbat a fisb flew througb tbe sky migbt be very informative generally, but would sbed no ligbt on thewortb of company X, would be irrelevant to the investor's decision, suid would bave no information content for thatdecision.

^If message M can take any ofn values and tbe ex ante probability of tbe itb value ition content, £(/), of tbe message (also known as tbe entropy of tbe message) is

j , tben tbe expected informa-

For a primer in information tbeory, see Cover and Tbomas (1991).

^^ • Accounting Horizons /December 1994

Note thatx is independent of the order in which the n messages are disclosed, because each probabilityis conditional on all prior messages. Also note a caveat: managers may bave a bias to present good newsand withhold bad news. To the extent investors suspect such a bias, they discount the news. However,there are at least four mitigating factors to this tendency: (1) accounting and disclosure standards arestructured to produce unbiased presentations^ (e.g., a company must disclose not only assets, revenues,and opportunities, but also liabilities, costs, and risks), (2) independent audits of information reduce bias,(3) managers' (long run) employment potentials are affected by their reputations for integrity, and (4)biased reports may be punished by criminal and civil litigation.

Thus the x axis in the figures in this article assumes that information is unbiased. And, by definition,redundant information has no informative value (i.e., the information content of company reports is notproportionate to their mere volume, but to their capacity to reduce uncertainty to investors).

In this context, unbiased means that companies cannot elect to disclose only the favorable information under gen-erally accepted accounting principles, but must report all the information. Although accounting standards do in-clude some biases (such as conservatism and nonrecognition of research and development assets), they relate tomatters that are not under management's discretion, and users—aware of the biases—can adjust for them.

REFERENCESArrow, K. J. 1983. Collected Papers of Kenneth J. Arrow, vol. 1, Social Choice and Justice. Cambridge,

MA: The Belknap Press of Harvard University Press.Bhagwhati, J. 1988. Protectionism. Cambridge, MA: The MIT Press.Conover, T. L., and W. A. Wallace. 1994. Equity Market Benefits to Disclosure of Geographic Segment

Information: An Argument for Decreased Uncertainty. Working paper.Cover, T. M., and J. A. Thomas. 1991. Elements of Information Theory. John Wiley & Sons, Inc.Dhaliwal, D. S. 1978. The Impact of Disclosure Regulations on the Cost of Capital. Economic Conse-

quences of Financial Accounting Standards: Selected Papers. Stamford, CT: FASB: 73-100.Evans, T. G., W. R. Folks, Jr., and M. Jilling. 1978. The Impact of Statement of Financial Accounting

Standards No, 8 on the Foreign Exchange Risk Management Practices of American Multinationals:An Economic Impact Study. Stamford, CT: FASB.

Financial Accounting Standards Board. 1978. Statement of Financial Accounting Concepts No. 1: Objec-tives of Financial Reporting by Business Enterprises. Stamford, CT: FASB.

. 1987. Rules of Procedure, Amended and Restated Effective January 1. 1987. Stamford, CT: FASB.

. 1990. Statement of Financial Accounting Standards No. 106: Employers'Accounting for Postretire-ment Benefits Other Than Pensions. Stamford, CT: FASB.

Goshay, R. C. 1978. Statement of Financial Accounting Standards No. 5: Impact on Corporate Risk andInsurance Management. Stamford, CT: FASB.

Mautz, R. K., and W. G. May. 1978. Financial Disclosure in a Competitive Economy. New York, NY: Finan-cial Executives Research Foundation.

Nichols, N. A. 1994. Scientific Management at Merck: An Interview with CFO Judy Lewent. HarvardBusiness Review (January-February): 89-99.

Porter, M. E. 1992. Capital Choices: Changing the WayAinerica Invests in Industry. Council on Competi-tiveness and Harvard Business School.

Stevenson, Jr., R. B. 1980. Corporations and Information: Secrecy, Access, and Disclosure. Baltimore,MD: The Johns Hopkins University Press.

Sweeney, P. 1994. Polishing the Tarnished Image of Investor Relations Executives. New York Times (April3).