CostIssues

20

Cost Issues

description

Cost issue in different industrial work

Transcript of CostIssues

Cost Issues

Module Outline

Evaluating plant investments

Plant financing options

Plant ownership costs

Calculating ownership costs

Purchase versus hiring plant

2

Evaluating Plant Investments

Investment appraisal methods

1) Payback period

2) Average rate of return

3) Net present value

4) Internal rate of return

5) Benefit-Cost ratio (Profitability index)

3

1) Payback period method

A simple method popular for small businesses

The time taken for an item of plant to generate sufficient net cash flow to pay for the original capital investment in its entirety

The payback period =

A company considers purchasing an excavator for an investment of $200,000 which is expected to provide annual cash flow of $50,000.The payback period would be four years.

Example:

Ignores the time value of moneyChanges in the cash flows after the payback period are ignored

4

2) Average rate of return (ARR)

Average annual profit you expect over the life of an investment project, compared with the average amount of capital invested (NIBusiness, 2004)

Average rate of return (ARR) =Average annual profit

Average investment cost

If ARR = or > the required rate of return investment accepted

If ARR < the required rate of return investment rejected

5

An excavator requires an average investment of $250,000 and is expected to produce an average annual profit of $37,500. The ARR would be 15 per cent.

Example:

ARR is based on profit rather than cash flow (affected by subjective, non-cash items such as the rate of depreciation)

The higher the ARR, the more attractive investment

Fails to take into account the timing of profit

Average investment =

Book value at beginning of year 1 +book value at end of useful time2

Average investment ~ initial investment cost

Or

6

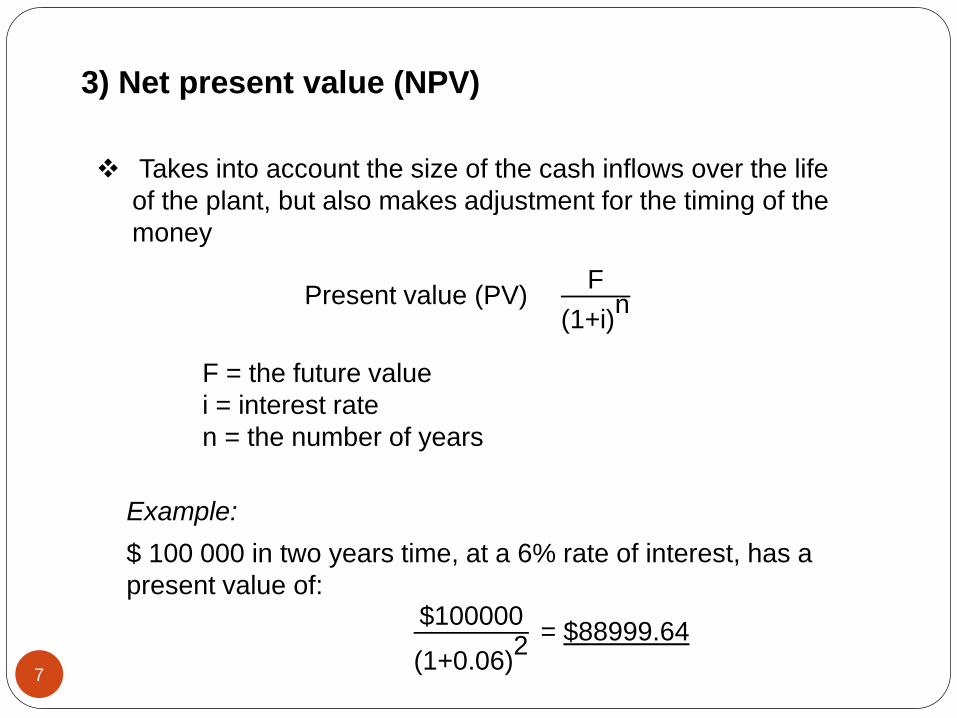

3) Net present value (NPV)

$ 100 000 in two years time, at a 6% rate of interest, has a present value of:

$100000

(1+0.06)2= $88999.64

Example:

Takes into account the size of the cash inflows over the life of the plant, but also makes adjustment for the timing of the money

Present value (PV) = F(1+i)n

F = the future valuei = interest raten = the number of years

7

The sum of the present values (PVs)of incoming (benefit) and outgoing(cost) cash flows over a period of time

Net present value (NPV) =

The higher the NPV the better (NIBusiness, 2004)

The PV of a series of uniform payments (Annuity, A), e.g. annual incomes, over a period of N years:

Present value (PV) = A [(1+i)n−1]i(1+i)n

An investment of $100,000 generates annual cash flow of $28,000 and with an interest rate of10%, the NPV for five years of cash flow is $6,142.

$28000[(1+0.1)5−1]

0.1(1+0.1)5−$100000= $6142

Example:

A cost is negative or outgoing cash flow

Net present value (NPV) = -PV (costs) + PV (benefits)

8

4) Internal rate of return (IRR)

The internal rate of return for an investment is the rate of return (interest rate) that makes the present value of returns (benefits) equal to the present value of costs

An investment of $100,000 is expected to generate an annual return of $28,000 for 5 years. What is the IRR?

Example:

$28000[(1+r)5−1]

r(1+r)5= $100000 or (1+r)5−1

r(1+r)5= 3.57

r = 10% Factor = 3.79 r = 20% Factor = 2.99 r = 12.5% Factor = 3.56 close enough IRR ≈ 12.5%

Try

PV (costs) = PV (benefits) NPV=0

9

5) Benefit-Cost ratio

Benefit-Cost ratio = Discounted value of benefitsDiscounted value of costs

Not useful when choosing between more than one project as it measures the relative profitability of a project.

Appropriate for situations where there is a limited capital budget to be allocated to the most cost effective projects

The greater the benefit cost ratio the more desirable the project

10

Plant Financing Options

Owning equipment Renting equipment

Costs include:• Operating costs• Maintenance• Repairs• Inspections• Transportation• Storage• Long retain period • Escalate over the life

of the equipment

• Reduces the amount of capital tied up in fleet

• Reduces the amount of start-up capital

• Reduces maintenance costs, repairs, inspections, transportation and storage.

11

Plant financing options

2) Financing Lease:

3) Operating Lease

1) Cash Purchase Plant supplier Construction Company

100%

Construction company:• Responsible for all maintenance, taxes and insurance• Can purchase the plant at the end of the lease period (at residual value)• Can renew/terminate the lease period

• Supplier (owner) is responsible for maintenance & taxes • Charges/lease period are usually lower than financing lease• Suitable for large or complex items of plant (skilled personnel for servicing

and maintenance provided by the lessor)

Plant supplier Construction Company

Lease fee

Plant supplier Finance provider Construction Company

Lease fee

12

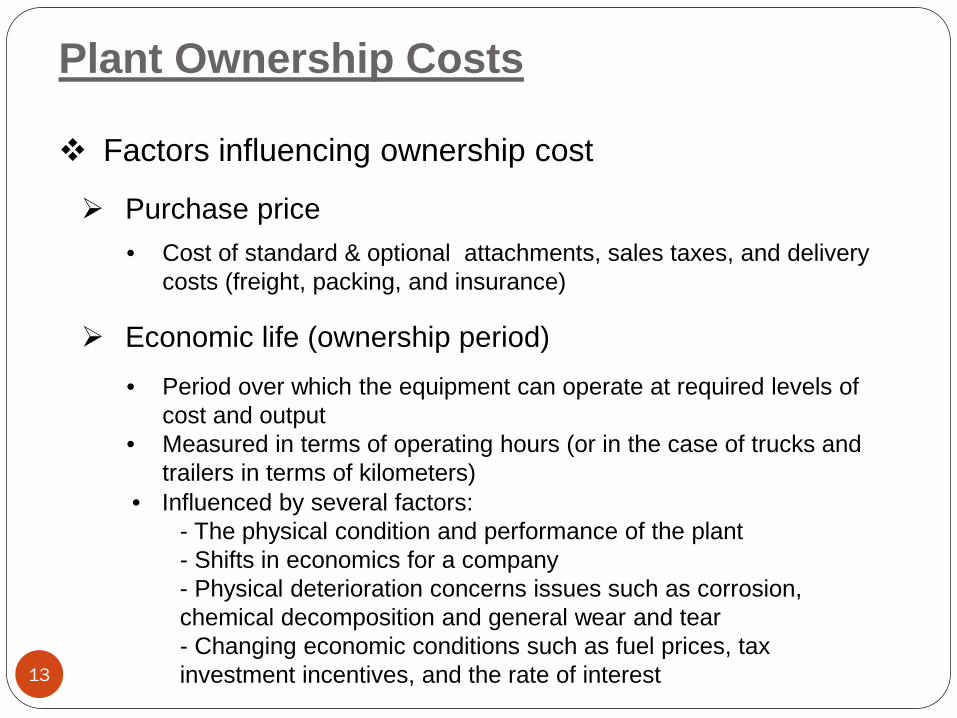

Plant Ownership Costs

Purchase price

Economic life (ownership period)

Factors influencing ownership cost

• Influenced by several factors: - The physical condition and performance of the plant - Shifts in economics for a company - Physical deterioration concerns issues such as corrosion, chemical decomposition and general wear and tear- Changing economic conditions such as fuel prices, tax investment incentives, and the rate of interest

• Cost of standard & optional attachments, sales taxes, and delivery costs (freight, packing, and insurance)

• Period over which the equipment can operate at required levels of cost and output

• Measured in terms of operating hours (or in the case of trucks and trailers in terms of kilometers)

13

Examples of ownership periods for some types of plant

14

Plant utilisation

• An uncertainty even if a company has secure, fixed-term contracts

• Expected rate of utilisation past operational history of the company’s equipment (Agoos, 2012)

A simplified approach to calculate utilization:

Industry-standard operating period: 22 days or 176 hours per month

Utilisation (%) =Operating period

Standard industrial period

• Utilisation > 60-65% of the time owning is more cost effective than renting

A practical guide:

• 40% < Utilisation < 60% increase financial risk

• Utilisation < 40% renting is almost always the best option 15

Calculating ownership costs

Salvage or residual value

The price that equipment can be sold for at the time of its disposal Often estimated as 10-20% of the initial purchase price

Insurance

Definition of terms:

A rough estimate of plant insurance cost : $10 for every $1,000 of the average value (i.e.,1%)

If the actual insurance cost of the plant is known:

Estimated insurance cost / year = Average value ÷ 100

16

Depreciation

Decrease in plant value over time

• Straight-Line depreciation

• Accelerated depreciation

Accelerated Depreciation

Year 1 Year 2 Year 3 Year 4 Year 5

Straight-Line-Depreciation

Cos

t

No. of years used

New price − salvage priceNo. of years used

17

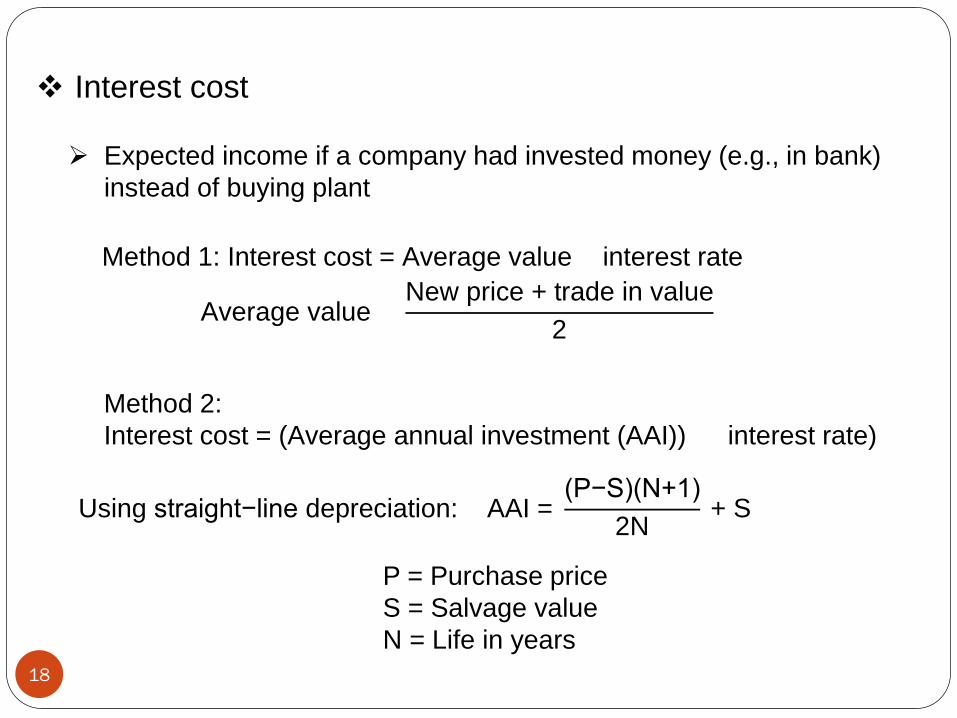

Interest cost

Expected income if a company had invested money (e.g., in bank) instead of buying plant

Method 1: Interest cost = Average value × interest rate

Average value =New price + trade in value

2

Method 2:Interest cost = (Average annual investment (AAI)) × (interest rate)

Using straight−line depreciation: AAI =(P−S)(N+1)

2N+ S

P = Purchase price S = Salvage valueN = Life in years

18

Storage cost

Workshop cost

Registration cost

The cost associated with providing suitable facilities to store and protect plantMethod 1: Storage cost = 0.5-1% of the price of new machine

Method 2: Storage cost = (yearly depreciation of storage facility) x

(proportion of facility occupied by the machine)

The cost the tools and workshop if plant is serviced and repaired on company premises

Workshop cost = (proportion of workshop time used for plant) x (cost (depreciation & interest) of workshop and tools)

Where items of plant such as front end loaders or mobile cranes are going to be driven for short distances on the road 19

Purchase vs. Hiring Plant

Owning equipment Renting equipment

Summary

Can be hired for short periods Repairs and replacements are

the responsibility of the hire company

Contractors do not have to worry about plant utilization after the job is finished

Plant can be hired on an all-in basis including the operator.

Plant availability controlled by contractor

Hourly rate is generally less than hire plant

Owner has the choice of which costing method to use

20