Costing and Cost Transfers John Caruso Campus Relations Manager, Sponsored Projects Administration.

51

Costing and Cost Transfers John Caruso Campus Relations Manager, Sponsored Projects Administration

-

Upload

amice-powell -

Category

Documents

-

view

216 -

download

1

Transcript of Costing and Cost Transfers John Caruso Campus Relations Manager, Sponsored Projects Administration.

Costing and Cost Transfers

John Caruso

Campus Relations Manager,

Sponsored Projects Administration

Audience

This course is intended for “department administrative staff”—including department administrators, division managers, department fiscal managers, department effort coordinators, etc.

Costing Basics

As a condition of receiving award funds from federal sponsors, OHSU is required to follow basic government regulations and Cost Accounting Standards (CAS)

Agency regulations include the following:OMB Circular A-212 CFR Part 215 (formerly OMB Circular A-110)OMB Circular A-133CAS 501, 502, 505 and 506

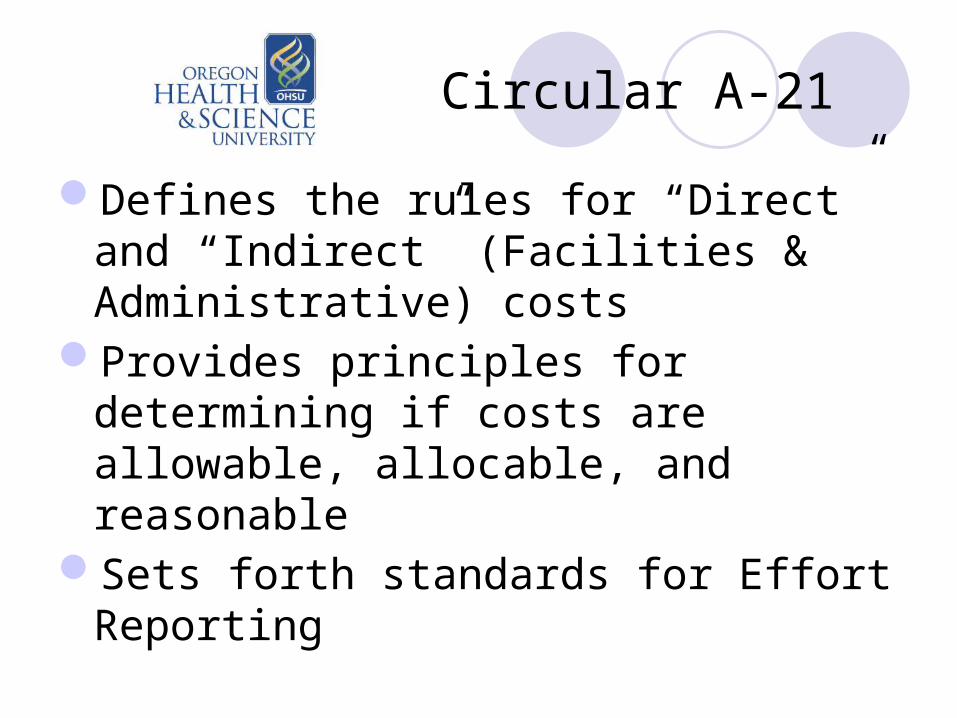

Circular A-21

Defines the rules for “Direct” and “Indirect” (Facilities & Administrative) costs

Provides principles for determining if costs are allowable, allocable, and reasonable

Sets forth standards for Effort Reporting

Circular 2 CFR Part 215

Defines reporting requirementsSets forth acceptable forms of cost sharingDefines methods for handling program incomeExplains when prior approvals are required for

revisions to budget or program plansDefines procurement standards and proceduresSets forth accounting standards for equipment

Circular A-133

Provides the standards for consistency and uniformity in the auditing of states, local governments, and non-profit organizations receiving and expending federal funding

Cost Accounting Standards

CAS 501, 502, 505 and 506 were developed to create consistency in the following areas:Estimating, accumulating, and reporting costs

(CAS 501)Allocating costs incurred for the same

purpose in like circumstances (CAS 502)Accounting for unallowable costs (CAS 505)Cost accounting periods (CAS 506)

Purposes of CAS

Cost Accounting Standards are designed to help promote consistency and fairness

It is essential to consistently follow OHSU’s disclosed accounting practices on costs:http://www.ohsu.edu/research/rda/spa/direct.shtml

Direct Costs

Cost Accounting Standards reduce the risk of “double dipping” or charging expenditures as both “direct” and “indirect” costs

Department administrators need to understand OHSU accounting practices and be familiar with the regulations defining “direct” costs

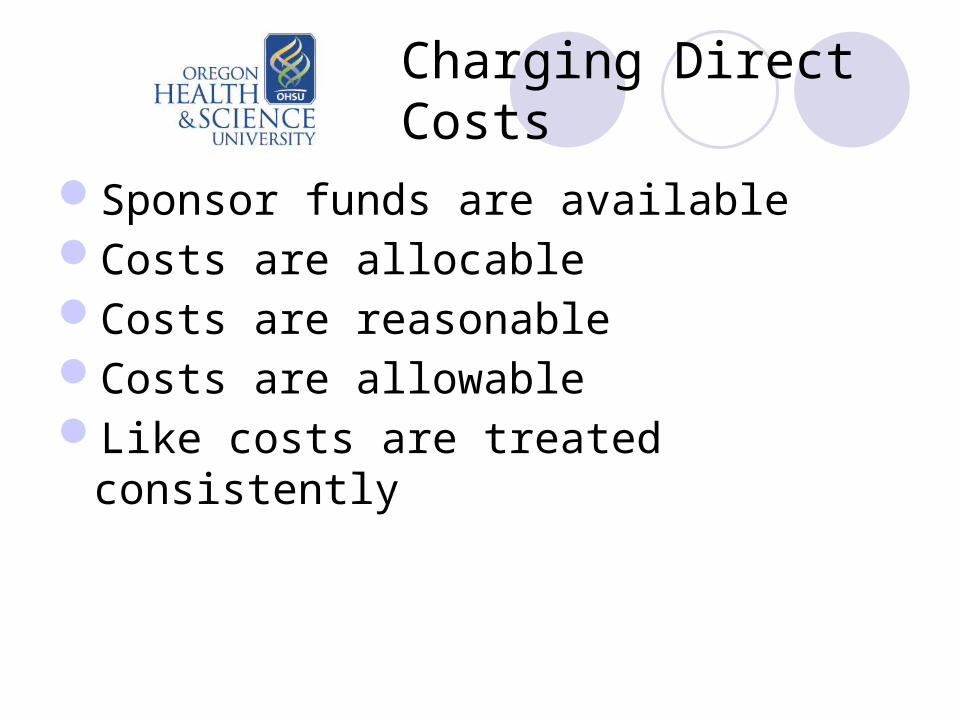

Charging Direct Costs

Sponsor funds are availableCosts are allocableCosts are reasonableCosts are allowableLike costs are treated consistently

Sponsor Funds Available

Appropriate direct cost items should be charged to sponsor funds

Expenditures must be between award start and end dates

Funds must remain unspent and uncommitted

If sponsor funds are unavailable, costs may be identified as Cost Sharing

Allocable

To be allocable as a direct cost, the expenditure must benefit only one project, or must be easily and proportionally assigned to multiple projects that benefit

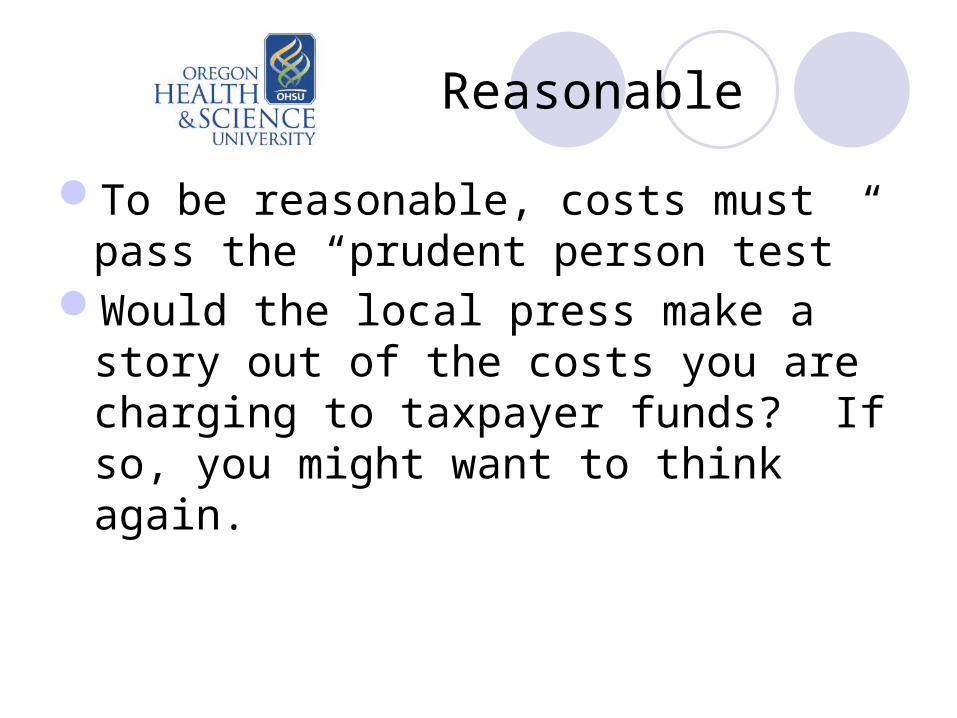

Reasonable

To be reasonable, costs must pass the “prudent person test”

Would the local press make a story out of the costs you are charging to taxpayer funds? If so, you might want to think again.

Allowable

For costs to be allowable on a federally sponsored award, “they must conform to any limitations or exclusions set forth in these [federal] principles or in the sponsored agreement as to types or amounts of cost items” (OMB Circular A-21, C.2.d)

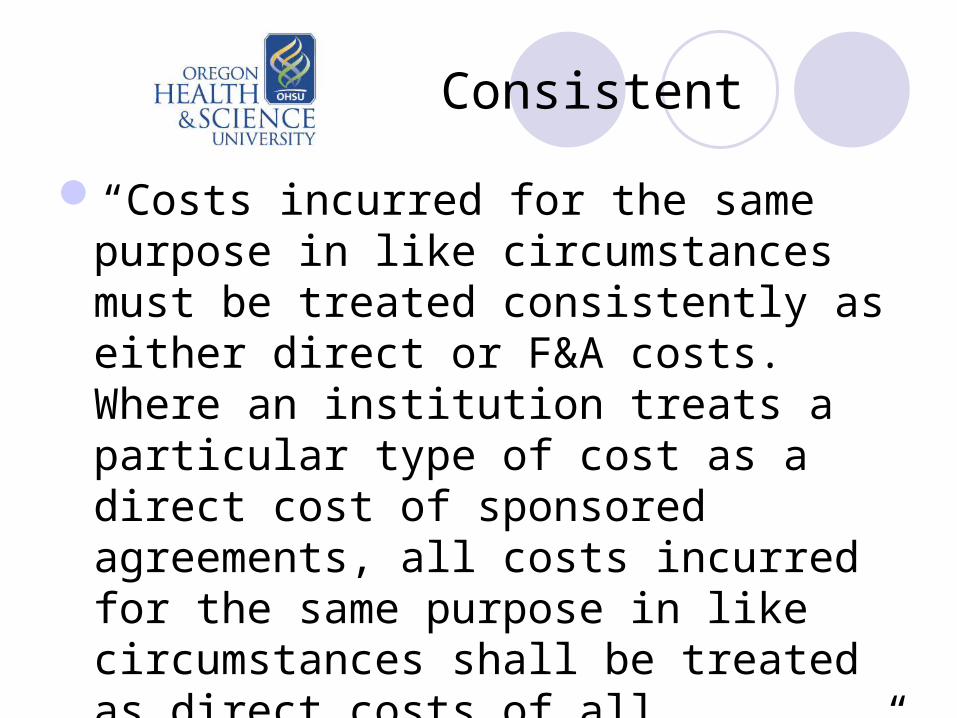

Consistent

“Costs incurred for the same purpose in like circumstances must be treated consistently as either direct or F&A costs. Where an institution treats a particular type of cost as a direct cost of sponsored agreements, all costs incurred for the same purpose in like circumstances shall be treated as direct costs of all activities of the institution.” (OMB Circular A-21, D.1)

Consistent

Certain items are generally considered “indirect” (F & A) costs—unless a direct relationship to a specific sponsored project can be establishedSalaries of departmental staffOffice suppliesTelephone expensesPhotocopying and postageEtc

Responsibilities

Principal Investigators, department administrators, and Sponsored Projects Administration (SPA) have specific roles and responsibilities related to the proper handling of costs

PI Responsibilities

The Principal Investigator (PI) is ultimately responsible for justifying the appropriateness of all direct costs budgeted and charged on sponsored projects, and must abide by the following:overall government regulationsagency guidelinesterms and conditions specific to the individual awardOHSU’s policies and guidelines

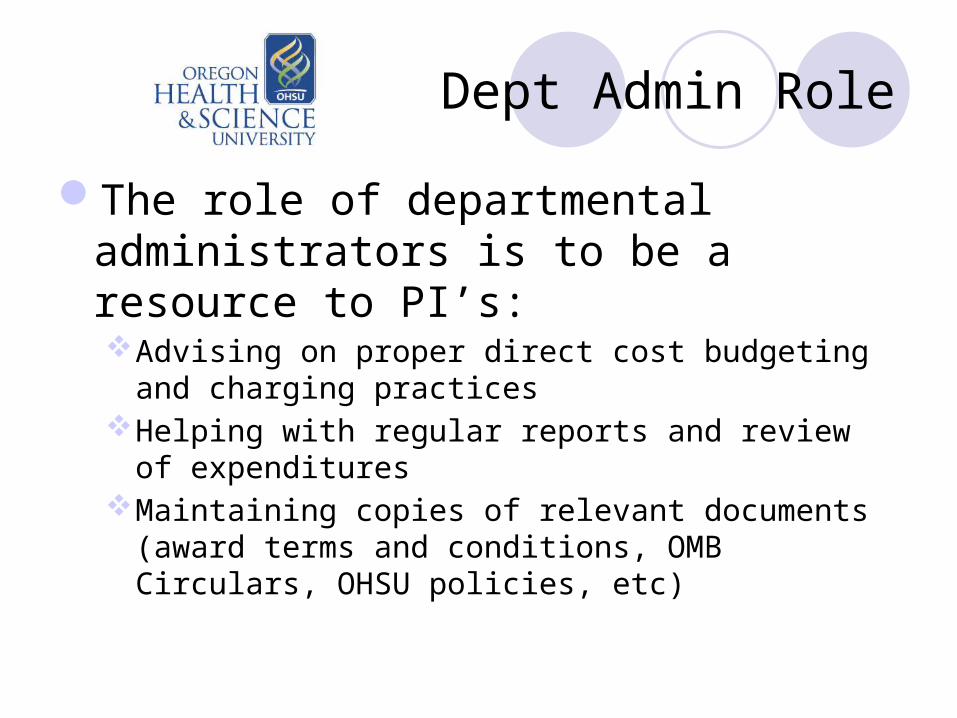

Dept Admin Role

The role of departmental administrators is to be a resource to PI’s:Advising on proper direct cost budgeting and charging

practicesHelping with regular reports and review of expendituresMaintaining copies of relevant documents (award terms

and conditions, OMB Circulars, OHSU policies, etc)

Role of Dean/Director

The Dean/Director must ensure that guidance is provided to PI’s and departmental administrators on the criteria to be used in budgeting and charging direct costs

The Dean/Director is also responsible for making sure mechanisms are in place to ensure accountability for budgeting and charging costs

SPA Responsibilities

SPA is responsible for providing guidance and assistance to PI’s and departmental administrators in the proper charging of direct costs

SPA also oversees and assists with cost transfers

Cost Transfers

Cost Transfer: the process for moving an item of expenditure between sponsored projects, expenditure types, or different types of funds

Cost Transfers need justification, documentation, and approval

Cost Transfer Overview

Rules governing Cost TransfersNecessary approvalsWalk through of OHSU Adjustment FormCost Transfers and AuditsStrategies for Prevention of Cost

TransfersExamples

Avoid the Need

All project costs should be appropriately charged to accounts according to accepted accounting principles as well as OHSU policies and the regulations applicable to sponsoring agencies

Ideally, completed transactions should not need correction

Transfer When Necessary

However, in certain circumstances, changes are required to move expenses—Cost TransferBetween projects Between expenditure typesBetween different types of funds

Cost Transfers need all of the following: justification, documentation, and authorization

Federal Requirements

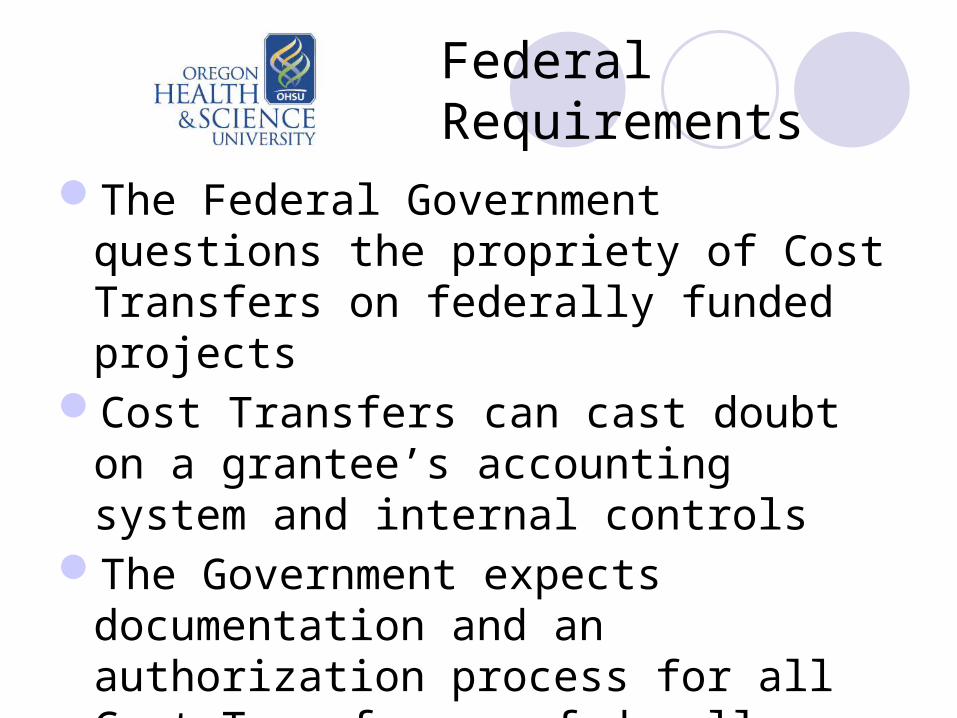

The Federal Government questions the propriety of Cost Transfers on federally funded projects

Cost Transfers can cast doubt on a grantee’s accounting system and internal controls

The Government expects documentation and an authorization process for all Cost Transfers on federally assisted projects

Federal Requirements

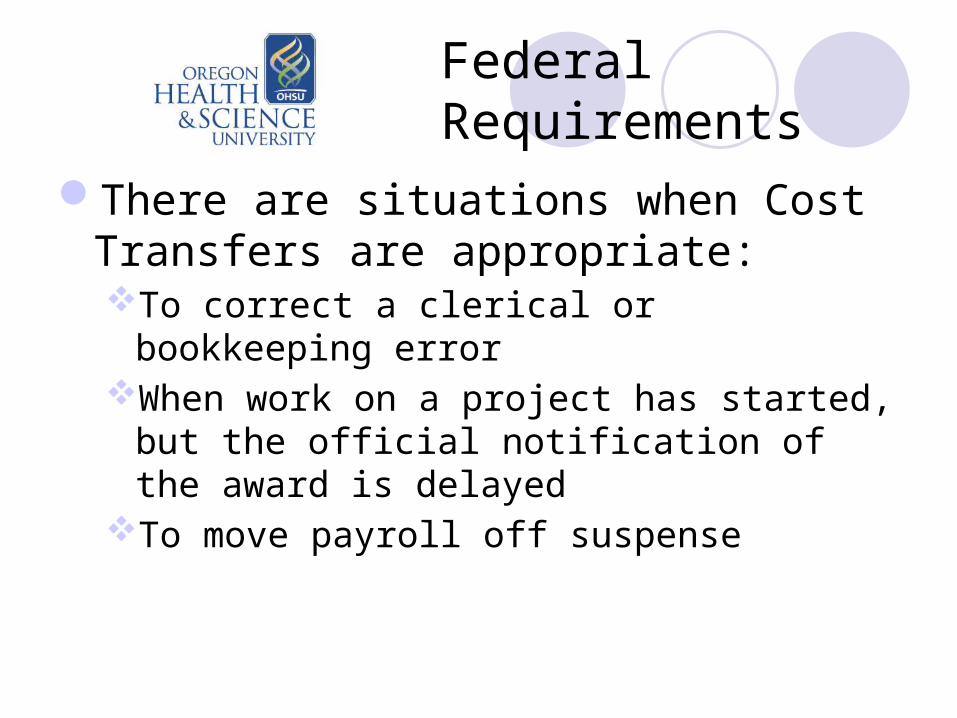

There are situations when Cost Transfers are appropriate:To correct a clerical or bookkeeping errorWhen work on a project has started, but the

official notification of the award is delayedTo move payroll off suspense

Federal Requirements

Under no circumstances may a Cost Transfer be made with the sole intent of using up the unexpended balance in a federal account.

SPA Procedure

The Principal Investigator (or Dept Admin) initiates the OHSU Adjustment Form as soon as possible (within 90 days of expense being charged)

The PI provides all information on the Form—note that “to correct error” is not sufficient cause

The Department Chair/Division Head reviews the Form, and forwards it to SPA if approved

SPA Procedure

SPA reviews the OHSU Adjustment Form forAllowabilityAcceptabilityPropriety of charges

If the request does not meet these criteria, it will be returned to the PI

If the request is approved, SPA forwards the form for processing

Acceptable Reasons

Correction of error—but be more specificCharges benefit more than one program

(distribution of costs based on benefits received)

Programs involve closely related work

Unacceptable Reasons

To reduce overruns if the transfer is from one federal project to another

For reasons of convenienceTo use unspent money in a projectBecause the bookkeeper was on leave,

etc

Walk Through of Form

Make Cost Transfers using the OHSU (“Transfer Between”) Adjustment Form: http://ozone.ohsu.edu/ais/docs/adjustmentForm.xls

There are also online instructions to this form: http://ozone.ohsu.edu/ais/docs/adjustmentInstructions.doc

Audits

Cost Transfers can be a “red flag” to auditors

Auditors examineFrequencyJustificationRemedies

Audit Questions

Are Cost Transfers supported by documentation which adequately explains and justifies why the transfers were made?

Are Cost Transfers caused by work which is supported by more than one funding source?

Are there Cost Transfers between projects which are in an overrun condition to those with unexpended balances?

Audit Questions

Are Cost Transfers which represent corrections of clerical errors made promptly after discovery?

Are Cost Transfers dated?Is an explanation provided that fully

explains how the error occurred?

Strategies for Prevention

Formal policies and related procedures governing Cost Transfers

Compliance training sessionsAwareness of the risks involved in making

inappropriate transfersReview of account balances, open orders,

etc, three months prior to close out

Cost Transfer Case Study #1

An OHSU employee transfers expenses from one account to another and annotates the cost transfer “to correct an accounting error”

Is this an appropriate justification?Why or why not?

Case Study #1

If it was an accounting error, the transfer must be supported by documentation that fully explains how the error occurred and a certification of the correctness of the new charge by a responsible organization official

Transfers made solely to cover cost overruns are not allowable

Cost Transfer Case Study #2

You are asked by a PI to stop at an office supply store on your way to work and pick up a few items. The PI also asked you to get donuts for the lab meeting that morning. When you arrive at work, the PI tells you that all the items should be charged to the grant

Your Department Administrator tells you that these purchases must come from departmental funds. Why?

Case Study #2

If the supplies are not specifically allocable to the grant, they are considered general office supplies and should not be charged as a “direct” cost to the grant account

Entertainment, such as food, is unallowable under the provisions of A-21

Cost Transfer Case Study #3

Dr. Miller purchases a much needed piece of specialized equipment for her research on hypertension. When preparing the purchase request, she realizes that the only account with enough money is her grant for research on sleep disorders. Because both grants are funded by NIH, she charges the equipment to the sleep disorder grant. Is this acceptable?

Case Study #3

The cost principles address four tests to determine allowability of costs:

AllocabilityReasonablenessConsistencyConformance

Allocable

A cost is allocable to a specific grant if it is incurred solely in order to advance work under the grant and is deemed assignable, at least in part, to the grant

Reasonable

A cost may be considered reasonable if the nature of the goods or services reflect the action that a “prudent person” would have taken under the circumstances prevailing at the time the decision to incur the cost was made

Consistent

Grantees must be consistent in assigning costs. Although costs may be charged as either “direct” costs or F&A costs, depending on their identifiable benefit to a particular project or program, they must be treated consistently for all work of the organization under similar circumstances, regardless of the source of funding

Conformance

Conformance with limitations and exclusions as contained in the terms and conditions of award—varies by type of activity, type of recipient, and other variables on individual awards

Cost Transfer Summary

Cost Transfer is the process of moving an expenditure between research projects, expenditure types, or different types of funds

Cost Transfers should be an exception, not a standard means of operating

Cost Transfers need justification, documentation, and approval

Course Summary

This course has examined the importance of Cost Accounting Standards in the successful management of federal award funds

With proper planning and regular review, costs should be charged correctly the first time

When necessary, cost transfers can be used to correct errors, as long as they include proper justification, documentation and authorization

Some Useful Websites

Grants Page/OER homepage:http://grants.nih.gov/grants/oer.htm

NIH Grants Policy Statement (12/03)http://grants.nih.gov/grants/policy/nihgps_2003/

index.htm

NIH Guide for Grants and Contracts:http://grants.nih.gov/grants/guide/index.html

Cost Transfers

Questions?