cost of capital

39

Kevin Campbell, University o f Stirling, November 2005 1 Overview of the Cost of Capital The cost of capital represents the firm’s cost of financing, and is the minimum rate of return that a project must earn to increase firm value. • Financial managers are ethically bound to only invest in projects that they expect to exceed the cost of capital. • The cost of capital reflects the entirety of the firm’s financing activities. Most firms attempt to maintain an optimal mix of debt and equity financing. • To capture all of the relevant financing costs, assuming some desired mix of financing, e need to loo! at the overall cost of capital rather than just the cost of any single source of financing.

-

Upload

lokesh-gowda -

Category

Documents

-

view

213 -

download

0

description

cost of different sources of capital & over all cost

Transcript of cost of capital

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 1/39

Kevin Campbell, University o f Stirling, November 2005 11

Overview of the Cost of

Capital The cost of capital represents the firm’s cost of financing, and

is the minimum rate of return that a project must earn to

increase firm value.

• Financial managers are ethically bound to only invest in projects thatthey expect to exceed the cost of capital.

• The cost of capital reflects the entirety of the firm’s financing activities.

Most firms attempt to maintain an optimal mix of debt and

equity financing.

• To capture all of the relevant financing costs, assuming some desired

mix of financing, e need to loo! at the overall cost of capital rather

than just the cost of any single source of financing.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 2/39

Kevin Campbell, University o f Stirling, November 2005 ""

Overview of the Cost of

Capital The overall cost of capital is a weighted average of

the various sources:

• WACC = Weighted Average Cost of Capital

The cost of capital is normally the relevant discountrate to use in analyzing an investment

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 3/39

Kevin Campbell, University o f Stirling, November 2005 ##

Overview of the Cost of Capital

(cont.)$ firm is currently faced ith an investmentopportunity. $ssume the folloing%

•&est project available today

• 'ost ( )1**,***

• +ife ( "* years

• xpected -eturn ( /

• +east costly financing source available

• 0ebt ( /

• &ecause it can earn / on the investment of fundscosting only /, the firm underta!es the opportunity.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 4/39

Kevin Campbell, University o f Stirling, November 2005 22

Overview of the Cost of Capital

(cont.)3magine that 1 ee! later a ne investmentopportunity is available%

• &est project available 1 ee! later

• 'ost ( )1**,***

• +ife ( "* years

• xpected -eturn ( 1"/

• +east costly financing source available

• quity ( 12/• 3n this instance, the firm rejects the opportunity, because

the 12/ financing cost is greater than the 1"/ expectedreturn.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 5/39

Kevin Campbell, University o f Stirling, November 2005 44

Overview of the Cost of Capital

(cont.)5hat if instead the firm used a combined cost of

financing6

• $ssuming that a 4* –4* mix of debt and equity istargeted, the eighted average cost here ould be%

7*.4* × / debt8 9 7*.4* × 12/ equity8 ( 1*/

• 5ith this average cost of financing, the first

opportunity ould have been rejected 7/ expected

return : 1*/ eighted average cost8, and the second

ould have been accepted

71"/ expected return ; 1*/ eighted average cost8.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 6/39

Kevin Campbell, University o f Stirling, November 2005

Specific Sources of Capital

&asic sources of long<term funds for the business

firm%

• +ong<term debt• =referred stoc!

• 'ommon stoc!

• -etained earnings

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 7/39

Kevin Campbell, University o f Stirling, November 2005

Factors Affecting the Cost of

Capital

>eneral conomic 'onditions

• $ffect interest rates Mar!et 'onditions

• $ffect ris! premiums ?perating 0ecisions

• $ffect business ris! Financial 0ecisions

• $ffect financial ris! $mount of Financing

• $ffect flotation costs and mar!et price ofsecurity

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 8/39

Kevin Campbell, University o f Stirling, November 2005 @@

Cost of Debt The cost of de!t to the firm is the effective yield to

maturity "or interest rate# paid to its !ondholders

$ince interest is ta% deducti!le to the firm& theactual cost of de!t is less than the yield tomaturity:

• After'ta% cost of de!t = yield % "( ' ta% rate#

The cost of de!t should also !e ad)usted forflotation costs "associated with issuing new!onds#

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 9/39

Kevin Campbell, University o f Stirling, November 2005 AA

with stock with debt

EBIT 400,000 400,000

- interest expense 0 (50,000)

EBT 400,000 350,000

- taxes (34) (!3",000) (!!#,000)E$T %"4,000 %3!,000

Example: Tax effects ofExample: Tax effects of

financing with debtfinancing with debt

*ow& suppose the firm pays +,-&--- in dividendsto the shareholders

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 10/39

Kevin Campbell, University o f Stirling, November 2005 1*1*

with stock with debt

EBIT 400,000 400,000

- interest expense 0 (50,000)EBT 400,000 350,000

- taxes (34) (!3",000) (!!#,000)

E$T %"4,000 %3!,000

- di&idends (50,000) 0

'etained earnins %!4,000 %3!,000

Example: Tax effects ofExample: Tax effects of

financing with debtfinancing with debt

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 11/39

Kevin Campbell, University o f Stirling, November 2005 1111

$fter-tax cost Before-tax cost Tax

of ebt of ebt *a&ins

33,000 + 50,000 - !,000

'

33,000 + 50,000 ( ! - .34)

Or, if we want to look at percentage costs:

-+Cost of Debt

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 12/39

Kevin Campbell, University o f Stirling, November 2005 1"1"

$fter-tax Before-tax /arinal

cost of cost of x tax

ebt ebt rate

d + kd (! - T)

.0"" + .!0 (! - .34)

-

+ !!

Cost of Debt

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 13/39

Kevin Campbell, University o f Stirling, November 2005 1#1#

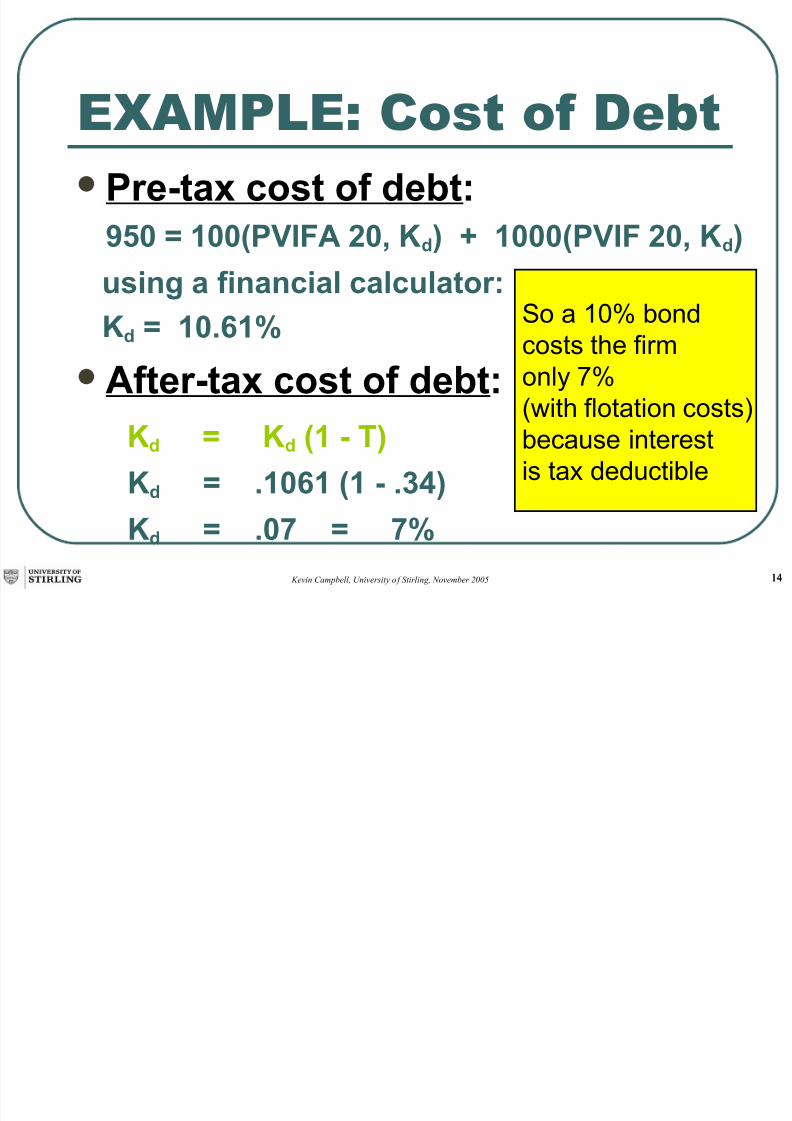

Prescott Corporation issues a $1, par,! "ear bond pa"ing the market rate of

1# Coupons are annual The bond willsell for par since it pa"s the market rate,but flotation costs amount to $% perbond

&hat is the pre'tax and after'tax cost ofdebt for Prescott Corporation(

EXAMPLE Cost of Debt

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 14/39

Kevin Campbell, University o f Stirling, November 2005 1212

Pre'tax cost of debt:)% * 1+P-./ !, 0d 2 1+P-. !, 0d

using a financial calculator: 0d * 131#

/fter'tax cost of debt:

0d * 0d +1 ' T

0d * 131 +1 ' 45

0d * 6 * 6#

EXAMPLE Cost of Debt

$o a (-. !ondcosts the firmonly .

"with flotation costs#!ecause interestis ta% deducti!le

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 15/39

Kevin Campbell, University o f Stirling, November 2005 1414

Cost of !ew Preferre"

#toc$ /referred stoc0:

• has a fi%ed dividend "similar to de!t#

• has no maturity date• dividends are not ta% deducti!le and are

e%pected to !e perpetual or infinite

Cost of preferred stoc0 = dividendprice ' flotation cost

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 16/39

Kevin Campbell, University o f Stirling, November 2005 11

Cost of Preferre" stoc$

E%a&ple&a!er 'orporation has preferred stoc! that sells for )1** per share and pays an annualdividend of )1*.4*. 3f the flotation costs are )2 per share, hat is the cost of ne preferred stoc!6

1*.A2/.1*A22<)1**

)1*.4* B

= ===

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 17/39

Kevin Campbell, University o f Stirling, November 2005 11

Cost of E'it*etaine" EarningsWhy is there a cost for retained earnings1

2arnings can !e reinvested or paid out as

dividends 3nvestors could !uy other securities& and

earn a return4

Thus& there is an opportunity cost ifearnings are retained

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 18/39

Kevin Campbell, University o f Stirling, November 2005 1@1@

Cost of E'it*etaine" Earnings Common stoc0 e5uity is availa!le throughretained earnings "672# or !y issuing new

common stoc0:• Common e5uity = 672 8 *ew common stoc0

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 19/39

Kevin Campbell, University o f Stirling, November 2005 1A1A

Cost of E'it

!ew Co&&on #toc$The cost of new common stoc0 is higher

than the cost of retained earnings

!ecause of flotation costs• selling and distri!ution costs "such as

sales commissions# for the new

securities

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 20/39

Kevin Campbell, University o f Stirling, November 2005 "*"*

Cost of E'it

There are a num!er of methods used todetermine the cost of e5uity

We will focus on two

9ividend growth odel

CA/

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 21/39

Kevin Campbell, University o f Stirling, November 2005 "1"1

+he Divi"en" ,rowth Mo"el

Approach

2stimating the cost of e5uity: the dividend growth modelapproach

According to the constant growth (Gordon) model& D( P - = R E - g

6earranging D(

R E = + g

P -

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 22/39

Kevin Campbell, University o f Stirling, November 2005 """"

E%a&ple Esti&ating the

Divi"en" ,rowth *ate /ercentage;ear 9ividend 9ollar Change Change

(<<- +4-- ''

(<<( 4- +-4- (-4--.

(<<> 4, -4?, 4<,

(<<? ,4>, -4,- (-4,?

(<< ,4@, -4- 4@>

Average rowth 6ate

"(-4-- 8 4<, 8 (-4,? 8 4@>#7 = <4->,.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 23/39

Kevin Campbell, University o f Stirling, November 2005 "#"#

Divi"en" ,rowth Mo"el

This model has draw!ac0s:

$ome firms concentrate on growth and do notpay dividends at all& or only irregularly

rowth rates may also !e hard to estimate Also this model doesn’t ad)ust for mar0et ris0

Therefore many financial managers prefer thecapital asset pricing model "CA/# ' or securitymar0et line "$B# ' approach for estimating thecost of e5uity

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 24/39

Kevin Campbell, University o f Stirling, November 2005 "2"2

Capital /sset Pricing 7odel +C/P7

87 f m f R R β Rkj −+=

Cost of

capital 8isk'freereturn

/9erage rate of return

on common stocks+&-

Co'9ariance

of returns againstthe portfolio

+departure from the a9erage; < 1, securit" is safer than &- a9erage

; = 1, securit" is riskier than &- a9erage

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 25/39

Kevin Campbell, University o f Stirling, November 2005 "4"4

+he #ecrit Mar$et Line (#ML)

'e12ired rateof ret2rn

ercent

0.5 !.0 !.5 %.0

*/ + ' f ( 6 7 ' f )

Beta (risk)

/arket risk pre6i26

%0.0

!8.0

!".0

!4.0

!%.0

!0.0

8.0

5.5

' f

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 26/39

Kevin Campbell, University o f Stirling, November 2005 ""

Fin"ing the *e'ire" *etrn on

Co&&on #toc$ sing the Capital

Asset Pricing Mo"elThe 'apital $sset =ricing Model 7'$=M8 can be used to estimate therequired return on individual stoc!s. The formula%

( ) - B - B f m jf j −+= β

here jB ( -equired return on stoc! j

f - ( -is!<free rate of return 7usually current rate on Treasury &ill8.

jβ ( &eta coefficient for stoc! j represents ris! of the stoc!

mB ( -eturn in mar!et as measured by some proxy portfolio 7index8

Cuppose that &a!er has the folloing values%

f - ( 4.4/

jβ ( 1.*

mB ( 1"/

.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 27/39

Kevin Campbell, University o f Stirling, November 2005 ""

Fin"ing the *e'ire" *etrn on

Co&&on #toc$ sing the Capital

Asset Pricing Mo"el Then, using the '$=M e ould get a required return of

( ) 1"/4.4<1"1.*4.4B j =+=

.

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 28/39

Kevin Campbell, University o f Stirling, November 2005 "@"@

CAPM-#ML approach

/d9antage: 2valuates ris0& applica!leto firms that don’t pay dividends

>isad9antage: *eed to estimate

• eta

• the ris0 premium "usually !ased on past data¬ future pro)ections#

• use an appropriate ris0 free rate of interest

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 29/39

Kevin Campbell, University o f Stirling, November 2005 "A"A

Esti&ation of eta MeasringMar$et *is$

ar0et /ortfolio ' /ortfolio of all assets inthe economy

3n practice a !road stoc0 mar0et inde%&such as the W3& is used to represent themar0et

eta ' sensitivity of a stoc0’s return to thereturn on the mar0et portfolio

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 30/39

Kevin Campbell, University o f Stirling, November 2005 #*#*

Esti&ation of eta

Theoretically& the calculation of !eta isstraightforward:

/ro!lems

(4etas may vary over time4

>4The sample size may !e inade5uate4

?4etas are influenced !y changing financial leverage and !usiness ris04

$olutions

• /ro!lems ( and > "a!ove# can !e moderated !y more sophisticated statisticaltechni5ues4

• /ro!lem ? can !e lessened !y ad)usting for changes in !usiness and financialris04

• Boo0 at average !eta estimates of compara!le firms in the industry4

"87

8,7

M

iM

M

M i

R!ar

R RCov β ==

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 31/39

Kevin Campbell, University o f Stirling, November 2005 #1#1

#tabilit of eta

ost analysts argue that !etas are generallysta!le for firms remaining in the same industry

That’s not to say that a firm’s !eta can’tchange

• Changes in product line

• Changes in technology

• 9eregulation

• Changes in financial leverage

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 32/39

Kevin Campbell, University o f Stirling, November 2005 #"#"

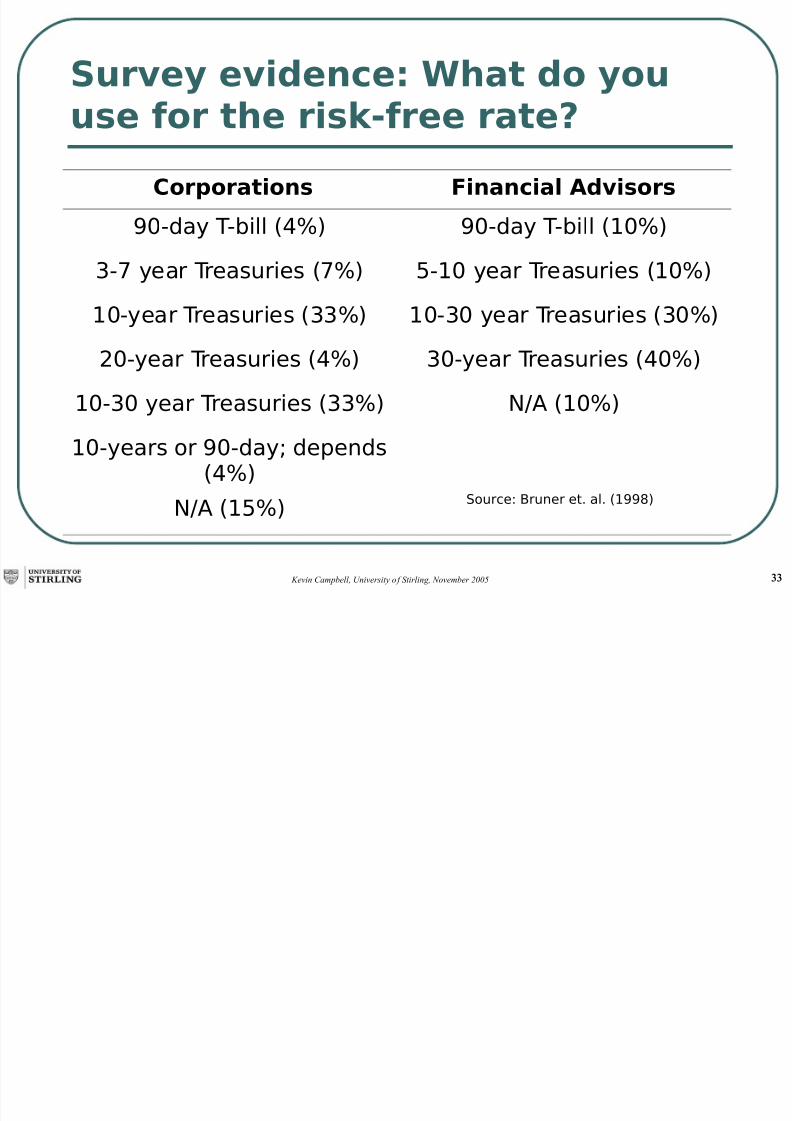

What is the appropriate risk-free rate?

Use the yield on a long-term bond if you areanalyzing cash ows from a long-term investment

For short-term investments, it is entirelyappropriate to use the yield on short-termgovernment securities

Use the nominal risk-free rate if you discountnominal cash ows and real risk-free rate if youdiscount real cash ows

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 33/39

Kevin Campbell, University o f Stirling, November 2005 ####

Survey evidence: What do youuse for the risk-free rate?

Corporations Financial Advisors

90-day -bill !"#$ 90-day -bill !%0#$

&-' year reasuries !'#$ (-%0 year reasuries !%0#$%0-year reasuries !&&#$ %0-&0 year reasuries !&0#$

)0-year reasuries !"#$ &0-year reasuries !"0#$

%0-&0 year reasuries !&&#$ *+ !%0#$

%0-years or 90-day depends!"#$

*+ !%(#$.ource/ runer et1 al1 !%992$

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 34/39

Kevin Campbell, University o f Stirling, November 2005 #2#2

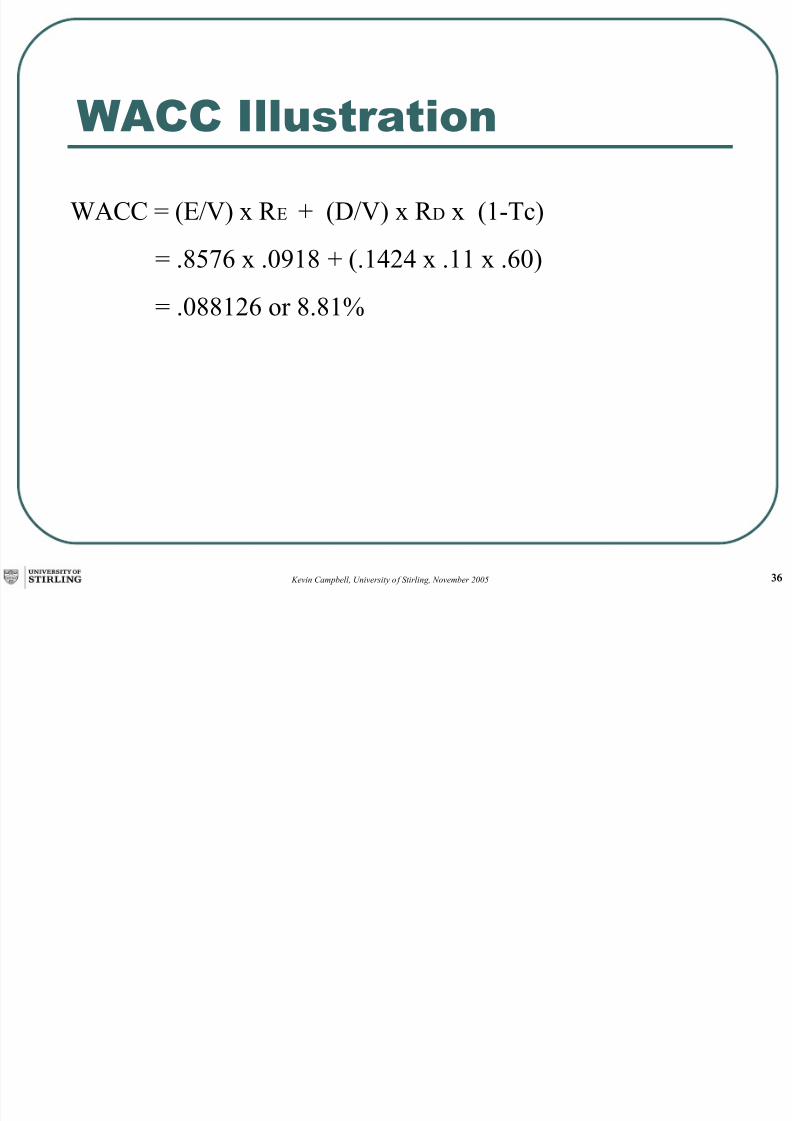

/eighte" Average Cost of Capital

(/ACC)

WACC weights the cost of e5uity and the costof de!t !y the percentage of each used in afirm’s capital structure

WACC="27 D# % 62 8 "97 D# % 69 % "('TC#

• "27D#= 25uity . of total value

• "97D#=9e!t . of total value

• "('Tc#=After'ta% . or reciprocal of corp ta% rate Tc4The after'ta% rate must !e considered !ecauseinterest on corporate de!t is deducti!le

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 35/39

Kevin Campbell, University o f Stirling, November 2005 #4#4

/ACC 0llstration

$&' 'orp has 1.2 million shares common valued at )"* per

share ()"@ million. 0ebt has face value of )4 million and trades

at A#/ of face 7)2.4 million8 in the mar!et. Total mar!et value

of both equity 9 debt thus ()#".4 million. quity / ( .@4and 0ebt / ( .12"2

-is! free rate is 2/, ris! premium(/ and $&'Ds E(.2

-eturn on equity per CM+ % - ( 2/ 9 7/ x .28(A.1@/

Tax rate is 2*/

'urrent yield on mar!et debt is 11/

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 36/39

Kevin Campbell, University o f Stirling, November 2005 ##

/ACC 0llstration

5$'' ( 7G8 x - 9 70G8 x - 0 x 71<Tc8

( .@4 x .*A1@ 9 7.12"2 x .11 x .*8

( .*@@1" or @.@1/

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 37/39

Kevin Campbell, University o f Stirling, November 2005 ##

Final notes on /ACC

WACC should !e !ased on mar0et rates andvaluation& not on !oo0 values of de!t or e5uity

oo0 values may not reflect the current

mar0etplace WACC will reflect what a firm needs to earn on

a new investment4 ut the new investmentshould also reflect a ris0 level similar to the

firm’s eta used to calculate the firm’s 624• 3n the case of AC Co4& the relatively low WACC of

E4E(. reflects AC’s F=44 A ris0ier investmentshould reflect a higher interest rate4

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 38/39

Kevin Campbell, University o f Stirling, November 2005 #@#@

Final notes on /ACC

The WACC is not constant

3t changes in accordance with the ris0

of the company and with the floatationcosts of new capital

7/17/2019 cost of capital

http://slidepdf.com/reader/full/cost-of-capital-568e8cef088f2 39/39

Marginal cost of capital an"invest&ent pro1ects!".0

!4.0

!%.0

!0.0

8.0

".0

4.0

%.0

0.0

ercent

!0 !5 !# 503#$6o2nt of capital (9 6illions)

!!.%3

0 85 #5

/arinal

cost ofcapital

6c

$

B:

E

;<

=

!0.

!0.4!

-

-

-

-

-

-

-

-

-