Cost Management Accounting Techniques 1204758241780170 2

35

Cost & Management Accounting Techniques Must for Effective Decision Making BY: A AMIR INSTITUTE OF COST & MANAGEMENT ACCOUNT ANTS OF P AKIST AN

-

Upload

venu-vemula -

Category

Documents

-

view

220 -

download

0

Transcript of Cost Management Accounting Techniques 1204758241780170 2

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 1/35

Cost & Management

Accounting Techniques Must for Effective Decision Making

BY:

A AMIR

INSTITUTE OF COST & MANAGEMENT ACCOUNTANTS OF PAKISTAN

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 2/35

CONTENTS

Cost & Management Accounting

Cost & Management Accounting Techniques

Conclusion

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 3/35

Cost & Management Accounting

The Process of

Identifying

Measuring Analyzing

Interpreting

Communicating Information

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 4/35

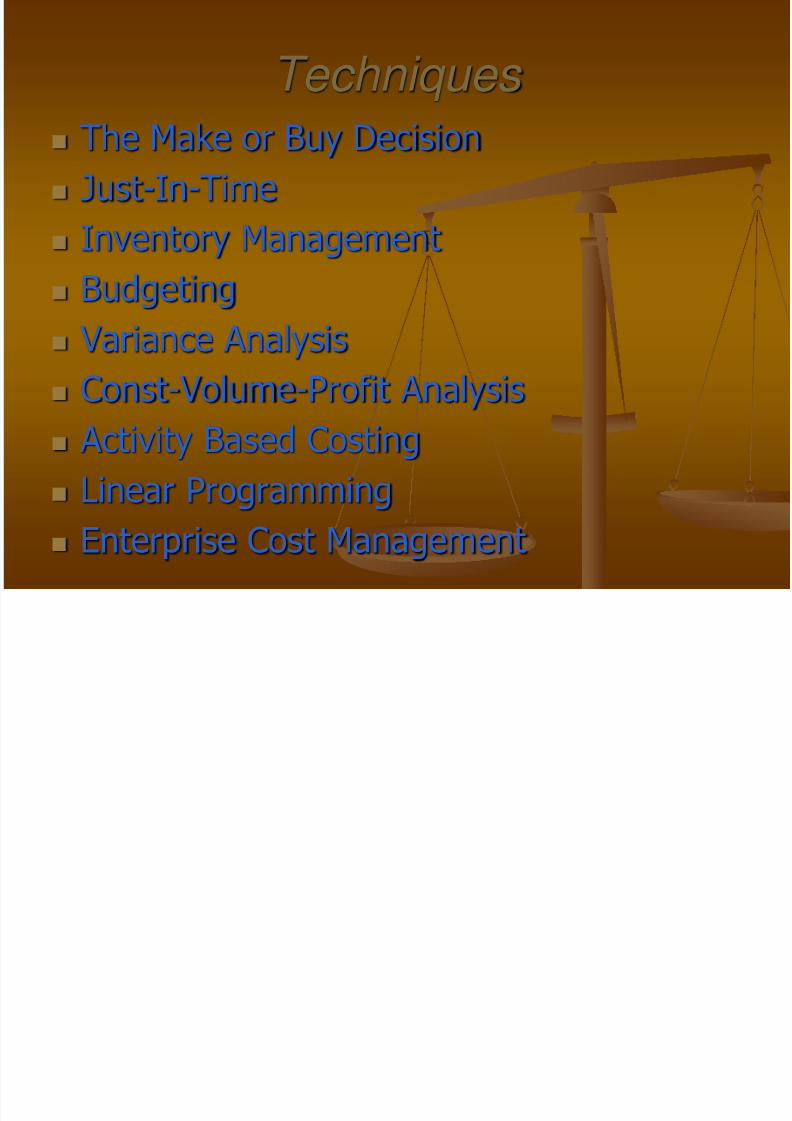

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 5/35

The Make or Buy Decision

A decision concerning whether an item shouldbe produced internally or purchased from an

outside supplier is called a “Make or Buy” decision.

Let’s look at the Astech Company example.

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 6/35

The Make or Buy Decision

Astech manufactures part 4A that is used inone of its products.

The unit product cost of this part is:

Direct materials $ 9

Direct labor 5

Variable overhead 1

Depreciation of special equip. 3 Supervisor's salary 2

General factory overhead 10 Unit product cost 30$

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 7/35

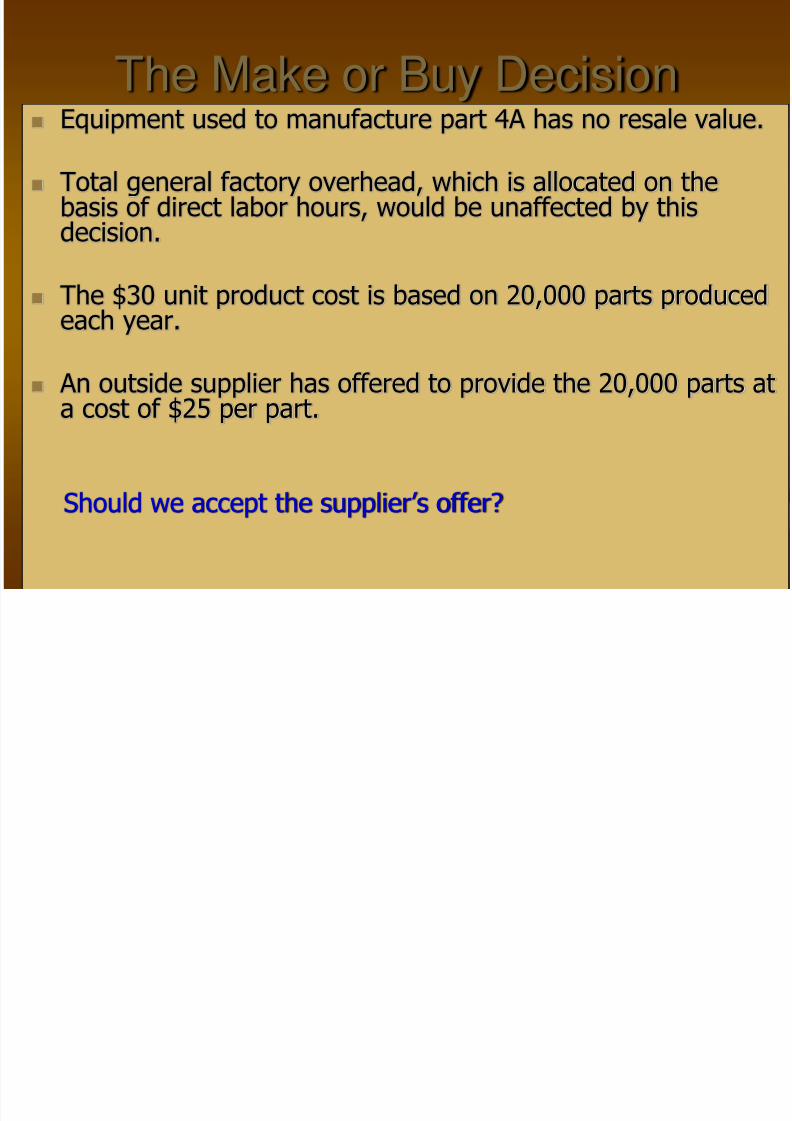

The Make or Buy Decision Equipment used to manufacture part 4A has no resale value.

Total general factory overhead, which is allocated on thebasis of direct labor hours, would be unaffected by thisdecision.

The $30 unit product cost is based on 20,000 parts producedeach year.

An outside supplier has offered to provide the 20,000 parts at

a cost of $25 per part.

Should we accept the supplier’s offer?

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 8/35

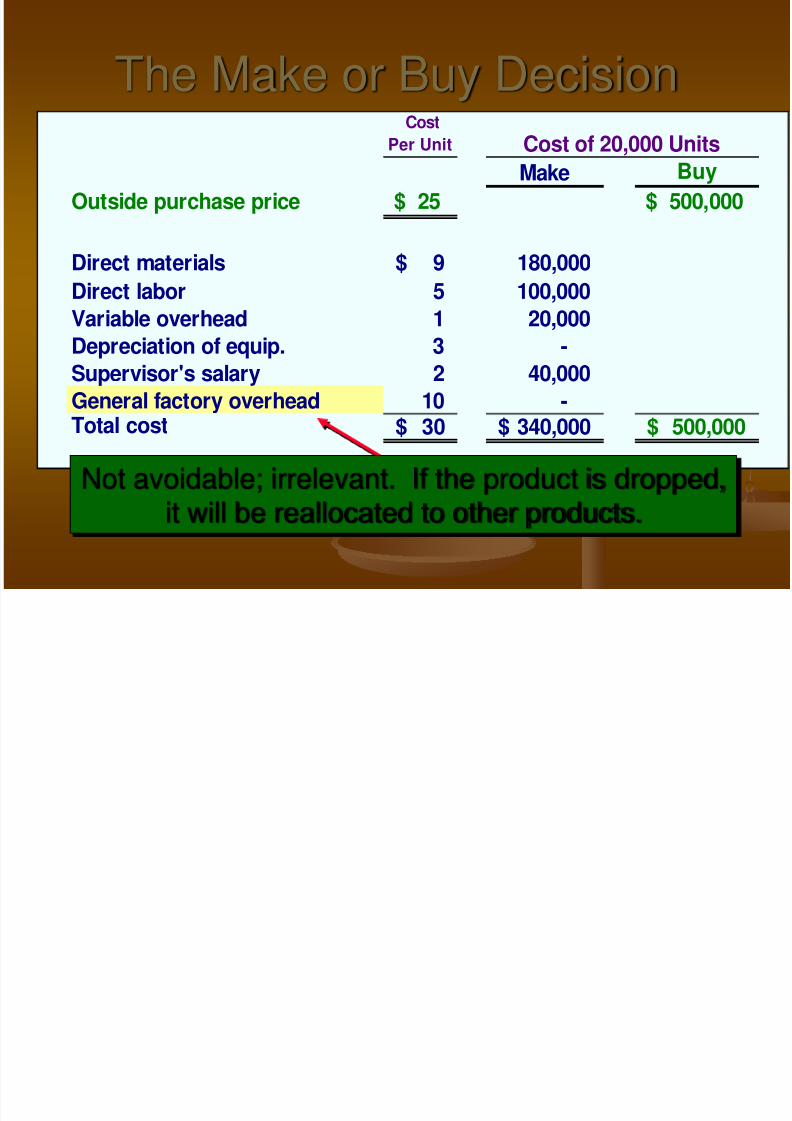

Cost

Per Unit Cost of 20,000 UnitsMake Buy

Outside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000

Direct labor 5 100,000

Variable overhead 1 20,000

Depreciation of equip. 3 -

Supervisor's salary 2 40,000

General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

The Make or Buy Decision

20,000 × $9 per unit = $180,000

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 9/35

Cost

Per Unit Cost of 20,000 UnitsMake Buy

Outside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000

Direct labor 5 100,000

Variable overhead 1 20,000

Depreciation of equip. 3 -

Supervisor's salary 2 40,000

General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

The Make or Buy Decision

The special equipment has no resalevalue and is a sunk cost.

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 10/35

Cost

Per Unit Cost of 20,000 UnitsMake Buy

Outside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000

Direct labor 5 100,000

Variable overhead 1 20,000

Depreciation of equip. 3 -

Supervisor's salary 2 40,000

General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

The Make or Buy Decision

Not avoidable; irrelevant. If the product is dropped,it will be reallocated to other products.

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 11/35

The Make or Buy Decision

Should we make or buy part 4A?

Cost

Per Unit Cost of 20,000 UnitsMake Buy

Outside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000

Direct labor 5 100,000

Variable overhead 1 20,000

Depreciation of equip. 3 -

Supervisor's salary 2 40,000

General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 12/35

The Make or Buy Decision

DECISION RULE

In deciding whether to accept the outsidesupplier’s offer, Astech isolated the relevant

costs of making the part by eliminating: The sunk costs.

The future costs that will not differ betweenmaking or buying the parts.

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 13/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 14/35

Impact of JIT Inventory Methods

In a JIT inventory system . . .

Productiontends to equalsales . . .

So, the difference between variable andabsorption income tends to disappear.

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 15/35

Techniques

The Make or Buy Decision

Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 16/35

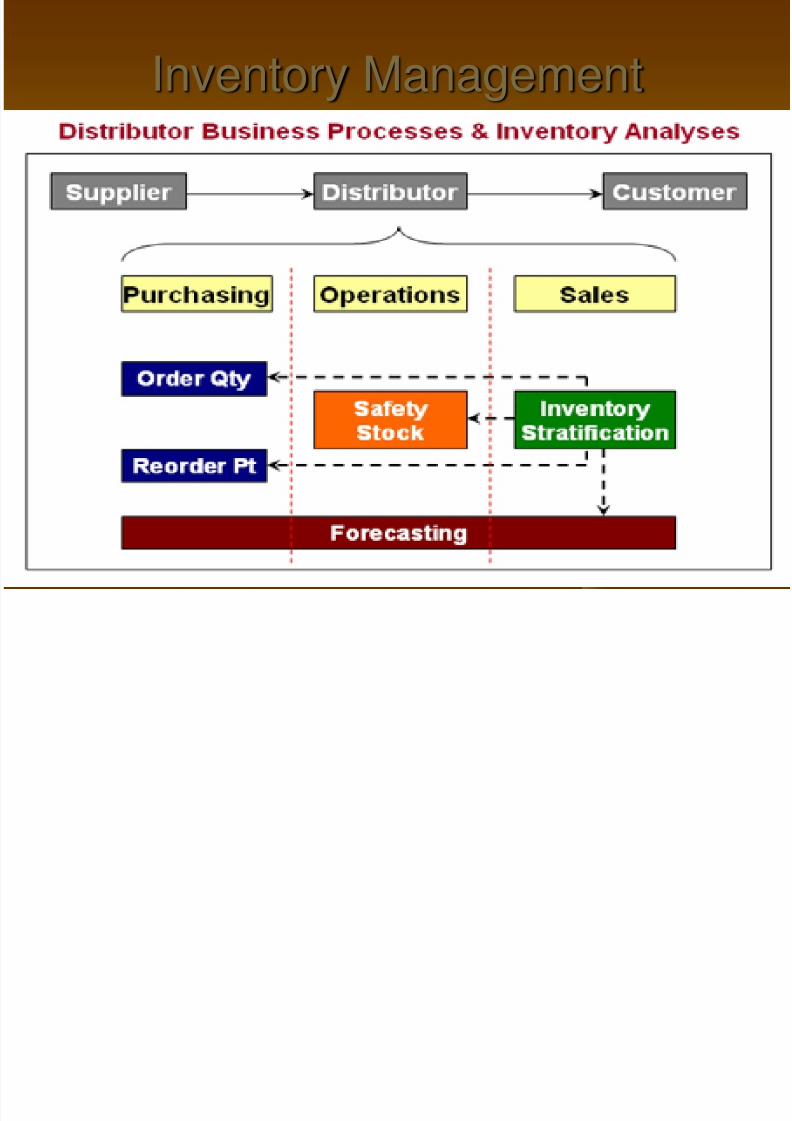

Inventory Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 17/35

Qunatity Discounts

Avoid DisturbanceReduce number of ordering / setupHedge against inflationMeet Unexpected Demands

Quantity Discounts

When to order

How much to orderBuffer Stock Maximum InventoryHow often to review stock

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 18/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 19/35

Budgeting

Define goaland objectives

Uncover potentialbottlenecks

Coordinateactivities

Communicatingplans

Think about andplan for the future

Means of allocatingresources

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 20/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming Investment Decision

Robust Decision

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 21/35

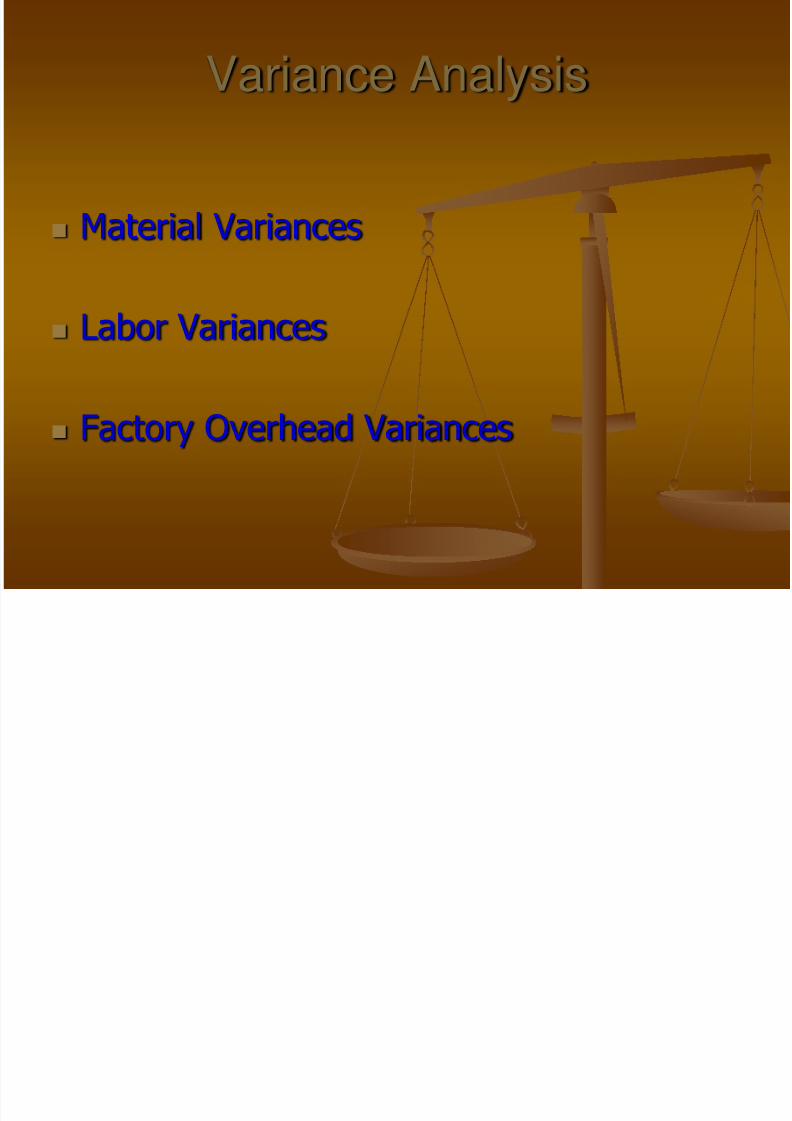

Variance Analysis

Material Variances

Labor Variances

Factory Overhead Variances

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 22/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming Investment Decision

Robust Decision

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 23/35

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

- 100 200 300 400 500 600 700 800

CVP Graph

Fixed expenses

Units

Total Expenses

Total Sales

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 24/35

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

- 100 200 300 400 500 600 700 800

Units

CVP Graph

Break-even point

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 25/35

Equation Method

Profits = Sales – (Variable expenses + Fixed expenses)

Sales = Variable expenses + Fixed expenses + Profits

OR

At the break-even point

profits equal zero.

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 26/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming Investment Decision

Robust Decision

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 27/35

Activity Based Costing (ABC)

ABC is designed toprovide managers

with cost informationfor strategic and

other decisions thatpotentially affect

capacity andtherefore “fixed”

costs.

ABC is agood supplement to our traditional

cost system

I agree!

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 28/35

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 29/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming Investment Decision

Robust Decision

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 30/35

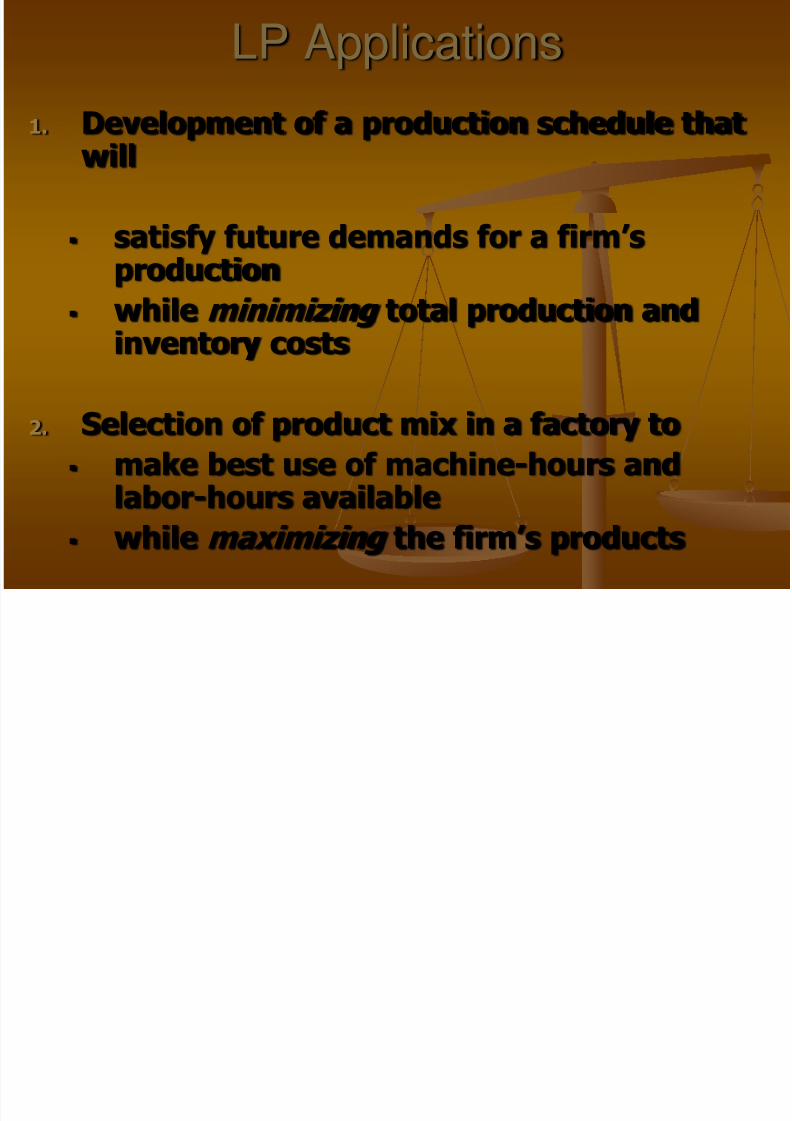

LP Applications

1. Development of a production schedule thatwill

satisfy future demands for a firm’s

production while minimizing total production and

inventory costs

2. Selection of product mix in a factory to make best use of machine-hours and

labor-hours available

while maximizing the firm’s products

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 31/35

LP Applications

3.

Determination of grades of petroleumproducts to yield the maximum profit

4. Selection of different blends of raw

materials to feed mills to produce finishedfeed combinations at minimum cost

5. Determination of a distribution systemthat will minimize total shipping cost fromseveral warehouses to various marketlocations

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 32/35

Techniques

The Make or Buy Decision Just-In-Time

Inventory Management

Budgeting

Variance Analysis

Const-Volume-Profit Analysis

Activity Based Costing

Linear Programming

Enterprise Cost Management

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 33/35

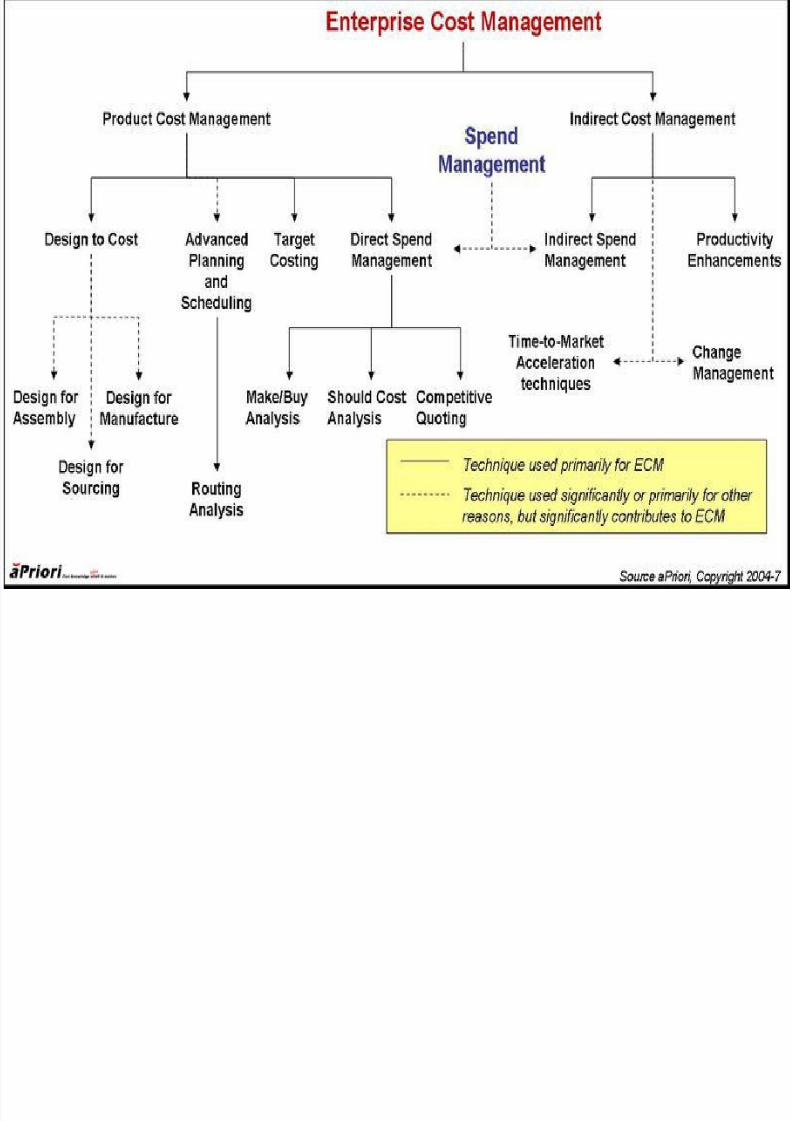

ECM

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 34/35

7/31/2019 Cost Management Accounting Techniques 1204758241780170 2

http://slidepdf.com/reader/full/cost-management-accounting-techniques-1204758241780170-2 35/35

CONCLUSION

Corporate Decision-Makers Rely on

Cost & Management Accountants

Thank you.