COST MANAGEMENT Accounting & Control Hansen▪Mowen▪Guan COPYRIGHT © 2009 South-Western...

39

COST MANAGEMENT COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning. Cengage Learning and South-Western are trademarks used herein under license. 1 Accounting & Control Hansen▪Mowen▪Guan Chapter 5 Product and Service Costing: Job-Order System

-

Upload

daniella-white -

Category

Documents

-

view

231 -

download

2

Transcript of COST MANAGEMENT Accounting & Control Hansen▪Mowen▪Guan COPYRIGHT © 2009 South-Western...

COST MANAGEMENT

COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning.Cengage Learning and South-Western are trademarks used herein under license.

1

Accounting & ControlHansen▪Mowen▪Guan

Chapter 5Product and Service

Costing:Job-Order System

2

Study Objectives1. Differentiate the cost accounting systems of service and

manufacturing firms and of unique and standardized products.2. Discuss the interrelationship of cost accumulation, cost

measurement, and cost assignment.3. Explain the difference between job-order and process costing,

and identify the source documents used in job-order costing.4. Describe the cost flows associated with job-order costing, and

prepare the journal entries.5. Explain why multiple overhead rates may be preferred to a

single, plantwide rate.6. Explain how spoilage is treated in a job-order costing system.

3

Manufacturing Firmsversus Service Firms

• Manufacturing involves joining together direct materials, direct labor, and overhead to produce a new product. The product is tangible and can be inventoried.

• A service is intangible. It cannot be separated from the customer and cannot be inventoried.

• Managers must be able to track the costs of services rendered just as precisely as they must track the costs of goods manufactured.

4

Unique versus Standardized Products and Services

• Firms that produce unique products in small batches that incur different product costs must track the costs of each product or batch separately. This is a…

• Job-order costing system– Examples: Cabinet makers, home builders,

dental and medical services

5

Unique versus Standardized Products and Services

• Some firms produce identical units of the same product. The costs of each unit are also the same. This is a…

• Process-costing costing system– Examples: Food, cement, petroleum and

chemicals

6

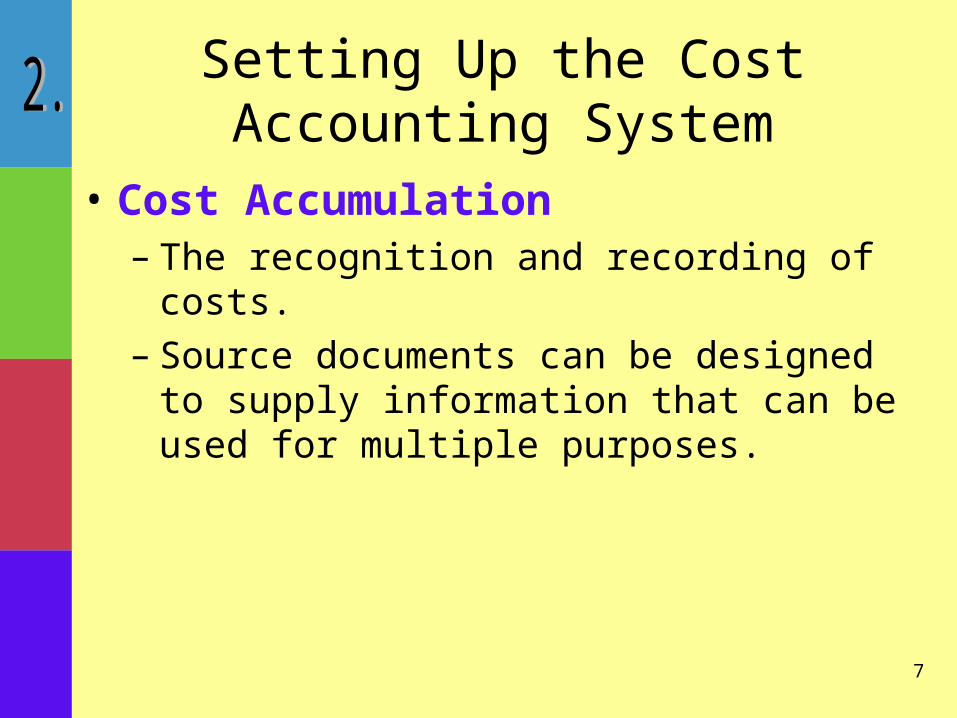

Setting Up the CostAccounting System

7

Setting Up the CostAccounting System

• Cost Accumulation– The recognition and recording of costs.– Source documents can be designed to supply

information that can be used for multiple purposes.

8

Setting Up the CostAccounting System

• Cost Measurement– Classifying the costs and determining the

dollar amounts for direct materials, direct labor and overhead.

– Methods of measurement• Actual costing: uses actual costs for direct

materials, direct labor, and overhead• Normal costing: uses actual costs for direct

materials and direct labor but measures overhead costs on a predetermined basis

9

Setting Up the CostAccounting System

• Cost Assignment– Occurs after costs have been accumulated

and measured.– Total product costs associated with the units

is divided by the number of units produced to determine unit cost.

10

Setting Up the CostAccounting System

• Unit Cost– Used in manufacturing firms to

• Value inventory• Determine income• Inform decision making

– Used in nonmanufacturing firms to• Determine profitability• Determine feasibility of new services

11

Setting Up the CostAccounting System

• Unit cost is made up of– Direct materials– Direct labor– Overhead

Traced directly to units

12

Setting Up the CostAccounting System

• Overhead is applied using a predetermined rate based on budgeted overhead costs and budgeted amount of driver.

• Commonly used drivers include– Units produced– Direct labor hours– Direct labor dollars– Machine hours– Direct materials dollars or cost

13

Setting Up the CostAccounting System

• Activity level– Must be predicted for the coming year to

calculate the predetermined overhead rate.

• Predicting activity– Reflective of consumer demand

• Normal activity level• Expected activity level

– Reflective of production capabilities• Theoretical activity level• Practical activity level

14

Job-Order Costing: Overview

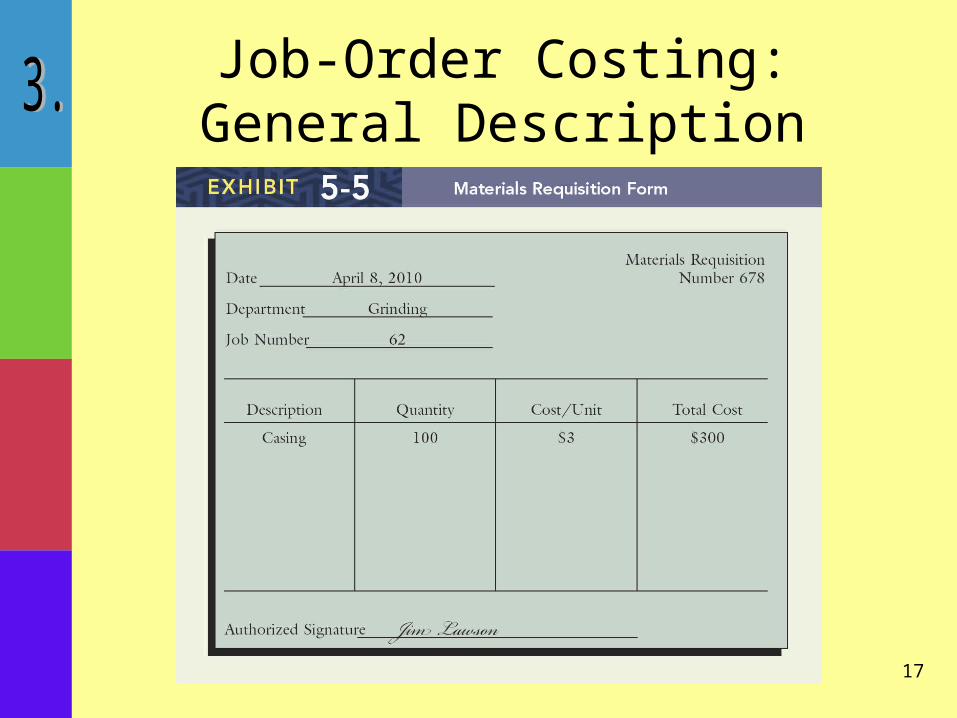

• Job-order industries produce a wide variety of products or jobs that are distinct.

• Costs are accumulated by job in a job-order costing system.

• Each job is documented on a job-order cost sheet.

15

Job-Order Costing: Overview

• Total manufacturing costs for the job are divided by the number of units produced to determine unit cost.

• The work-in-process inventory is the collection of all job-order cost sheets.

16

Job-Order Costing:General Description

17

Job-Order Costing:General Description

18

Job-Order Costing:General Description

19

Overhead is assigned to jobs using a predetermined overhead rate. The actual amount of the driver used as a base must be collected and recorded.

Job-Order Costing:General Description

20

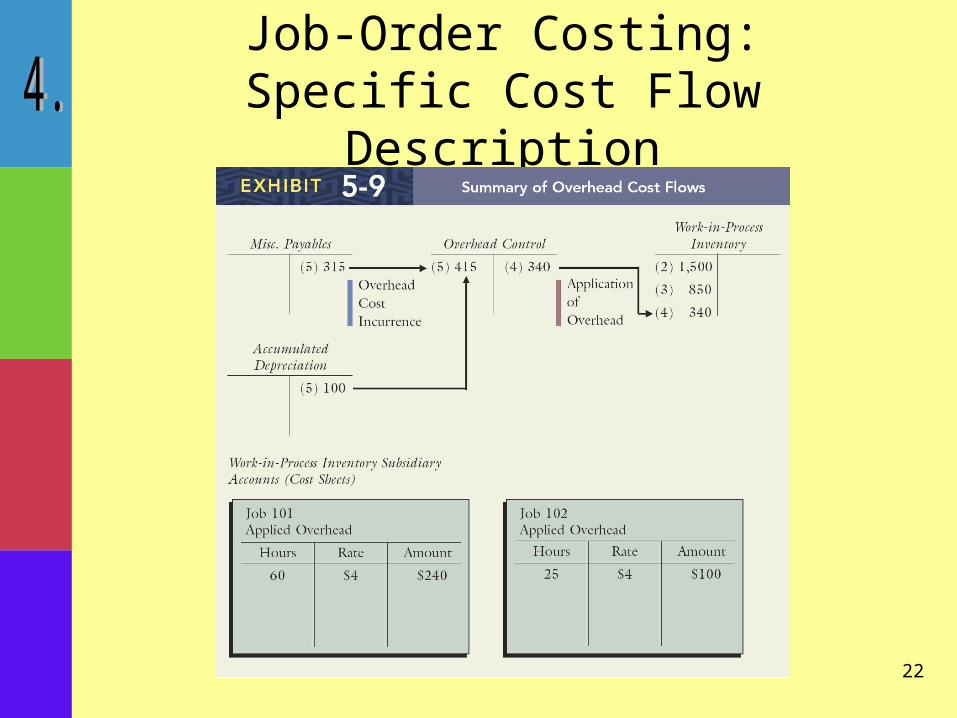

Job-Order Costing:Specific Cost Flow Description

21

Job-Order Costing:Specific Cost Flow Description

22

Job-Order Costing:Specific Cost Flow Description

23

Job-Order Costing:Specific Cost Flow Description

24

Job-Order Costing:Specific Cost Flow Description

25

Statement of Cost of Goods Manufactured

Direct materials:Beginning direct materials inventory -$ Add: purchases of direct materials 2,500 Total direct materials available 2,500$ Less: Ending direct materials 1,000

Direct materials used 1,500$

All Signs CompanyStatement of Cost of Goods Manufactured

For the Month Ended January 31, 2010

26

Statement of Cost of Goods Manufactured

Direct materials:Beginning direct materials inventory -$ Add: purchases of direct materials 2,500 Total direct materials available 2,500$ Less: Ending direct materials 1,000

Direct materials used 1,500$ Direct labor 850

All Signs CompanyStatement of Cost of Goods Manufactured

For the Month Ended January 31, 2010

27

Statement of Cost of Goods Manufactured

Direct materials:Beginning direct materials inventory -$ Add: purchases of direct materials 2,500 Total direct materials available 2,500$ Less: Ending direct materials 1,000

Direct materials used 1,500$ Direct labor 850 Manufacturing overhead:

Lease 200$ Utilities 50 Depreciation 100 Indirect labor 65

415

All Signs CompanyStatement of Cost of Goods Manufactured

For the Month Ended January 31, 2010

28

Statement of Cost of Goods Manufactured

Direct materials:Beginning direct materials inventory -$ Add: purchases of direct materials 2,500 Total direct materials available 2,500$ Less: Ending direct materials 1,000

Direct materials used 1,500$ Direct labor 850 Manufacturing overhead:

Lease 200$ Utilities 50 Depreciation 100 Indirect labor 65

415 Less: Underapplied overhead 75

Overhead applied 340

All Signs CompanyStatement of Cost of Goods Manufactured

For the Month Ended January 31, 2010

29

Statement of Cost of Goods Manufactured

Direct materials:Beginning direct materials inventory -$ Add: purchases of direct materials 2,500 Total direct materials available 2,500$ Less: Ending direct materials 1,000

Direct materials used 1,500$ Direct labor 850 Manufacturing overhead:

Lease 200$ Utilities 50 Depreciation 100 Indirect labor 65

415 Less: Underapplied overhead 75

Overhead applied 340 Current manufacturing costs 2,690$ Add: Beginning work-in-process inventory - Less: Ending work-in-process inventory (850) Cost of goods manufactured 1,840$

All Signs CompanyStatement of Cost of Goods Manufactured

For the Month Ended January 31, 2010

30

Statement of Cost of Goods Sold

Beginning finished goods inventory -$ Cost of goods manufactured 1,840 Goods available for sale 1,840$ Less: ending finished goods inventory - Normal cost of goods sold 1,840$ Add: underapplied overhead 75 Adjusted cost of goods sold 1,915$

All Signs CompanyStatement of Cost of Goods Sold

For the Month Ended January 31, 2010

31

Summary ofManufacturing Cost Flows

32

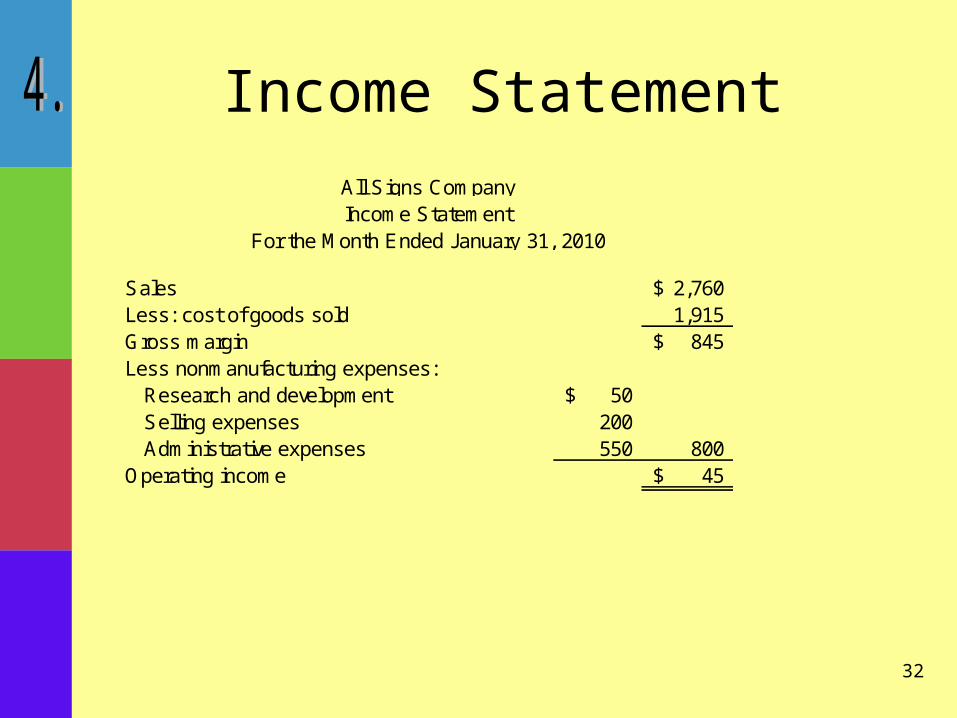

Income Statement

Sales 2,760$ Less: cost of goods sold 1,915 Gross margin 845$ Less nonmanufacturing expenses:

Research and development 50$ Selling expenses 200 Administrative expenses 550 800

Operating income 45$

All Signs CompanyIncome Statement

For the Month Ended January 31, 2010

33

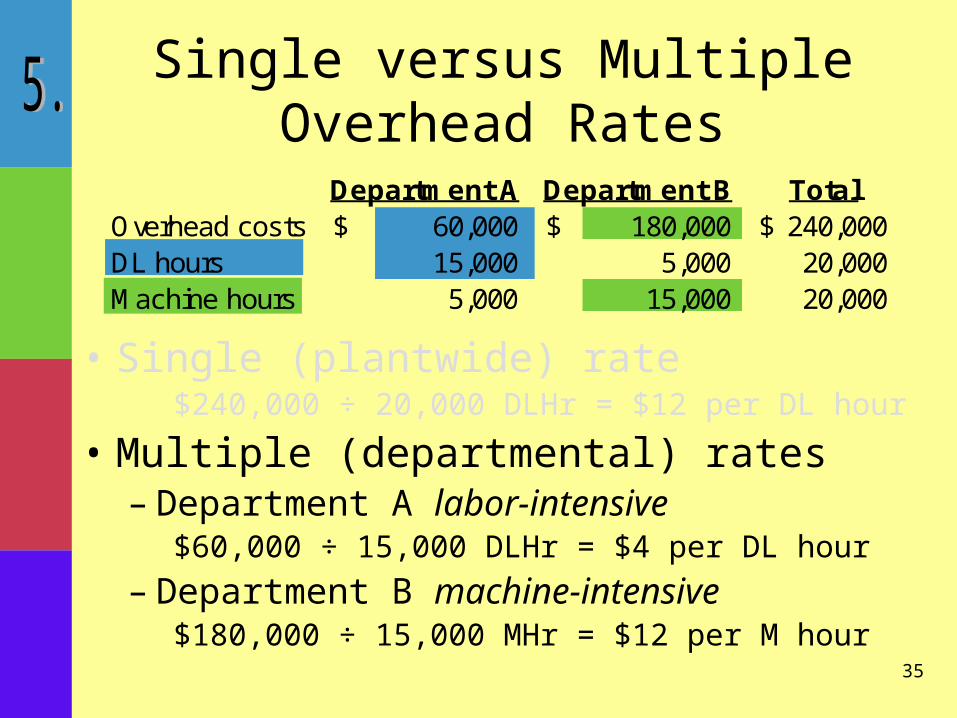

Single versus MultipleOverhead Rates

• Single (plantwide) rate$240,000 ÷ 20,000 DLHr = $12 per DL hour

• Multiple (departmental) rates– Department A labor-intensive

$60,000 ÷ 15,000 DLHr = $4 per DL hour

– Department B machine-intensive$180,000 ÷ 15,000 MHr = $12 per M hour

Department A Department B TotalOverhead costs 60,000$ 180,000$ 240,000$ DL hours 15,000 5,000 20,000 Machine hours 5,000 15,000 20,000

34

Single versus MultipleOverhead Rates

Using single overhead application rate:

Prime Costs 5,000$ 5,000$ Applied overhead:

DL hours 500 1 Single rate 12.00$ 6,000 12.00$ 12

Total costs 11,000$ 5,012$ Units produced 1,000 1,000 Unit cost 11.000$ 5.012$

Job #23 Job #24

35

Single versus MultipleOverhead Rates

• Single (plantwide) rate$240,000 ÷ 20,000 DLHr = $12 per DL hour

• Multiple (departmental) rates– Department A labor-intensive

$60,000 ÷ 15,000 DLHr = $4 per DL hour

– Department B machine-intensive$180,000 ÷ 15,000 MHr = $12 per M hour

Department A Department B TotalOverhead costs 60,000$ 180,000$ 240,000$ DL hours 15,000 5,000 20,000 Machine hours 5,000 15,000 20,000

36

Single versus MultipleOverhead Rates

Using multiple overhead application rates:

37

Single versus MultipleOverhead Rates

Using multiple overhead application rates:

Prime Costs 5,000$ 5,000$ Applied overhead:

Dept A:DL Hours 500 - Rate 4.00$ 2,000 4.00$ -

Dept B:Machine hours - 500 Rate 12.00$ - 12.00$ 6,000

Total costs 7,000$ 11,000$ Units produced 1,000 1,000 Unit cost 7.000$ 11.000$

Job #23 Job #24

38

Single versus MultipleOverhead Rates

Comparison of Overhead Assigned:

Job 23 Job 24

Single rate 500 DLH @ $12 = $6,000

1 DLH @$12 = $12

Multiple rates 500 DLH @ $4 = $2,000

500 MH @$12 = $6,000

COST MANAGEMENT

COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning.Cengage Learning and South-Western are trademarks used herein under license.

39

Accounting & ControlHansen▪Mowen▪Guan

End Chapter 5