Cost estimating in these times of austerity

44

06/06/2014 1 UNCLASSIFIED QinetiQ Proprietary © Copyright QinetiQ Limited 2014 QINETIQ/TIS/S&AS/PUB1401673 Abstract • The presentation will review the maturity of risk management and cost estimating in organisations and the effect this can have upon financial decisions made by project managers. • This presentation will briefly discuss the three methods of estimating; analytical, analogous and parametric before studying parametric cost and schedule estimating in more depth. It will consider the benefits of generating parametric estimates early in the project life cycle and other applications of parametric estimating when little information is available to the Project Manager. • Finally, the presentation will explore means of making the project more cost effective using cost estimating relationships (CER) to explore cost saving measures suitable for these years of austerity. © Copyright QinetiQ Limited 2014 UNCLASSIFIED QinetiQ Proprietary QINETIQ/TIS/S&AS/PUB1401673 Cost estimating in these times of austerity Association of Project Managers (APM) South Wales and West of England Branch 4 th June 2014 Dale Shermon QinetiQ Fellow / Head of Profession Cost Engineering

-

Upload

association-for-project-management -

Category

Business

-

view

946 -

download

1

Transcript of Cost estimating in these times of austerity

06/06/2014

1

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Abstract

• The presentation will review the maturity of risk management and cost

estimating in organisations and the effect this can have upon financial

decisions made by project managers.

• This presentation will briefly discuss the three methods of estimating;

analytical, analogous and parametric before studying parametric cost

and schedule estimating in more depth. It will consider the benefits of

generating parametric estimates early in the project life cycle and other

applications of parametric estimating when little information is

available to the Project Manager.

• Finally, the presentation will explore means of making the project more

cost effective using cost estimating relationships (CER) to explore cost

saving measures suitable for these years of austerity.

© Copyright QinetiQ Limited 2014

UNCLASSIFIED

QinetiQ Proprietary

QINETIQ/TIS/S&AS/PUB1401673

Cost estimating in these times of austerity

Association of Project Managers (APM)

South Wales and West of England Branch

4th June 2014

Dale Shermon QinetiQ Fellow / Head of Profession Cost Engineering

06/06/2014

2

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Contents

1. Introduction

2. Cost and Risk Maturity

assessments

3. Methods of cost estimating

4. FACET Parametric estimating

5. Austerity – project cost saving

measures

6. Summary

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

1.

Introduction

06/06/2014

3

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Dale Shermon BA, ACCA CDip (A&F)

• Rolls-Royce, British Aerospace,

Matra Marconi Space, UK MOD /

SPS & PFG, PRICE Systems;

• QinetiQ Fellow and Head of

Profession Cost Engineer;

Council member and Fellow

ACostE (FACostE)

Member of APM (MAPM)

Life member and Certified

Parametric Practitioner (CPP) of

ICEAA

Chairman and member of SCAF

• Parametrician of the Year 2013

• Frieman award 2009 for

“outstanding lifetime contribution

to cost estimating”

• ISPA St. Louis, Best Hardware

paper, 2006, “TrueConcepts a

methodology not a model”

• ISPA Florida, Best Applications

paper, 2003, “If a little knowledge

is dangerous… what is a lot of

knowledge?”

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

SCAF

06/06/2014

4

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

QinetiQ Procurement Advisory Service (QPAS)

Advice Services

Evaluation Services

QPAS

AWARD - QinetiQ Commerce Decisions Ltd

Co

st E

ng

ine

erin

g

Pro

gra

mm

e &

Pro

ject

Man

ag

em

en

t

Req

uire

men

ts

Accep

tan

ce

Th

rou

gh

Life

Serv

ices

Ris

k M

an

ag

em

en

t

Bu

sin

ess A

naly

sis

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Knowledge Based Estimating (KBE)

06/06/2014

5

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

2.

Cost and Risk Maturity

assessments

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Why Conduct a Maturity Assessment?

Assess the quality and consistency of cost and risk management

implementation

Understand cost and risks and their impacts across the enterprise

Improve cost and risk management to inform decision-making across the

organisation portfolio

Realise tangible benefits in capability acquisition and support

Reduce duplication of effort, across organisations

Improve communications, where common issues are identified

Improve coherency and alignment, and share good practice

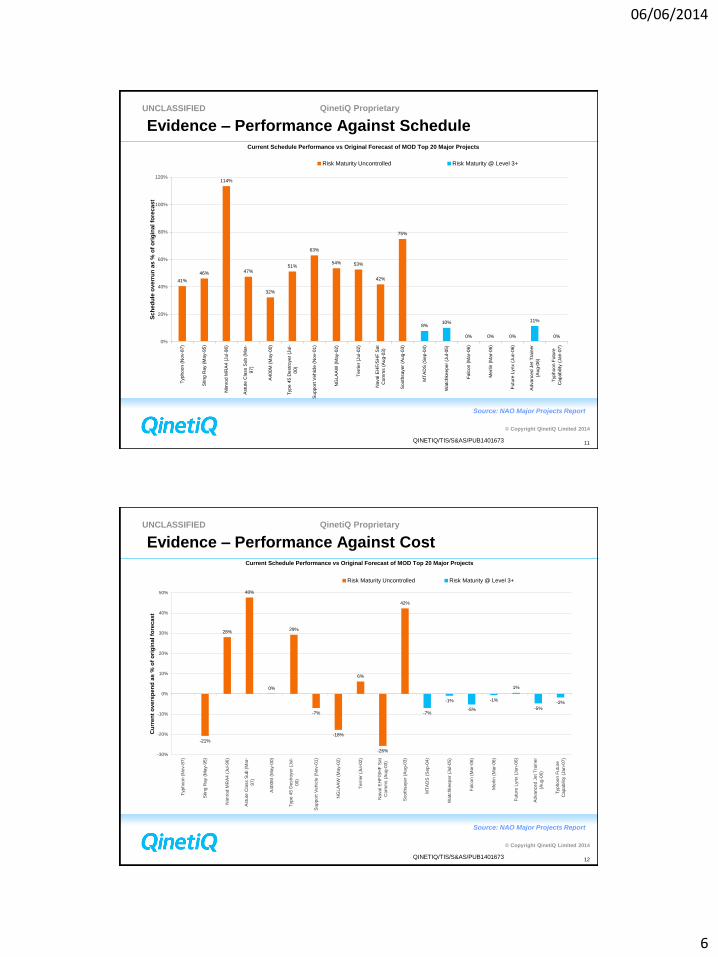

“Major projects that have used the QinetiQ benchmarking tool and subsequently improved their risk maturity have reduced forecast overspend by an average of 20% of

project value and forecast schedule overrun by 41 months”

Source: NAO Major Projects Report

10

06/06/2014

6

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Evidence – Performance Against Schedule

11

Current Schedule Performance vs Original Forecast of MOD Top 20 Major Projects

41%

46%

114%

47%

32%

51%

63%

54% 53%

42%

75%

8%10%

0% 0% 0%

11%

0%0%

20%

40%

60%

80%

100%

120%T

yphoon (

Nov-8

7)

Stin

g R

ay (

Ma

y-9

5)

Nim

rod M

RA

4 (

Jul-96)

Astu

te C

lass S

ub (

Ma

r-

97)

A400M

(M

ay-0

0)

Type 4

5 D

estr

oyer

(Jul-

00)

Support

Vehic

le (

Nov-0

1)

NG

LA

AW

(M

ay-0

2)

Te

rrie

r (J

ul-02)

Naval E

HF

/SH

F S

at

Com

ms (

Aug-0

3)

Sooth

sayer

(Aug-0

3)

MT

AD

S (

Sep-0

4)

Watc

hkeeper

(Jul-05)

Fa

lcon (

Ma

r-06)

Me

rlin

(M

ar-

06)

Fu

ture

Lynx (

Jun-0

6)

Advanced J

et

Tra

iner

(Aug-0

6)

Typhoon F

utu

re

Capabili

ty (

Jan-0

7)

Sch

ed

ule

overr

un

as %

of

ori

gin

al fo

recast

Risk Maturity Uncontrolled Risk Maturity @ Level 3+

Source: NAO Major Projects Report

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Evidence – Performance Against Cost

12

Current Schedule Performance vs Original Forecast of MOD Top 20 Major Projects

-21%

28%

48%

0%

29%

-7%

-18%

6%

-26%

42%

-7%

-1%

-5%

-1%

1%

-5%

-2%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Typhoon (

Nov-8

7)

Sting R

ay (

May-9

5)

Nim

rod M

RA

4 (

Jul-96)

Astu

te C

lass S

ub (

Mar-

97)

A400M

(M

ay-0

0)

Type 4

5 D

estr

oyer

(Jul-

00)

Support

Vehic

le (

Nov-0

1)

NG

LA

AW

(M

ay-0

2)

Terr

ier

(Jul-02)

Naval E

HF

/SH

F S

at

Com

ms (

Aug-0

3)

Sooth

sayer

(Aug-0

3)

MT

AD

S (

Sep-0

4)

Watc

hkeeper

(Jul-05)

Falc

on (

Mar-

06)

Merlin

(M

ar-

06)

Futu

re L

ynx (

Jun-0

6)

Advanced J

et

Tra

iner

(Aug-0

6)

Typhoon F

utu

re

Capabili

ty (

Jan-0

7)

Cu

rren

t o

vers

pen

d a

s %

of

ori

gin

al fo

recast

Risk Maturity Uncontrolled Risk Maturity @ Level 3+

Source: NAO Major Projects Report

06/06/2014

7

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673 13

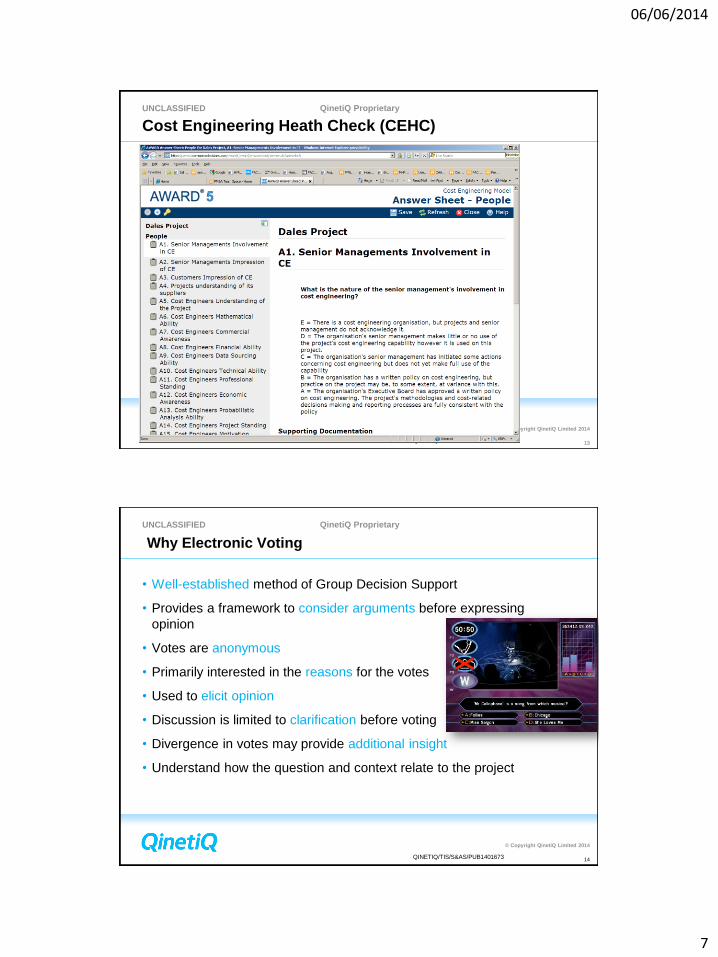

Cost Engineering Heath Check (CEHC)

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Why Electronic Voting

• Well-established method of Group Decision Support

• Provides a framework to consider arguments before expressing

opinion

• Votes are anonymous

• Primarily interested in the reasons for the votes

• Used to elicit opinion

• Discussion is limited to clarification before voting

• Divergence in votes may provide additional insight

• Understand how the question and context relate to the project

14

06/06/2014

8

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

What’s The Process? – Delphi Technique

1. Question is posed

2. Think!

3. Consider the question and context

4. Vote

5. Facilitated discussion

6. Voting results presented

7. Salient points recorded for analysis/reporting

8. Record the consensus view

9. Re-vote (as necessary)

10. Record the consensus view

15

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Case Study - Cumulative result of SCAF assessment

16

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5

A1

A5

B1

B3

C4

C16

C15

C5

D3

D13

D6

A15

1. Schedule risk

analysis tools

2. Technical

data storage

3. Software

estimating tools

4. Planning and

communication

Weak Excellent

06/06/2014

9

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Case study - UK MOD Assessment of Cost Maturity

0.00

1.00

2.00

3.00

4.00

5.00

SCAF

EACE

MOD

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

3.

Methods of Cost Estimating

06/06/2014

10

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Cost Engineering

• Estimating techniques include:

1. Analytical

2. Analogy

3. Parametric

• Selecting appropriate methodology

© Copyright QinetiQ Limited 2014

UNCLASSIFIED

QinetiQ Proprietary

QINETIQ/TIS/S&AS/PUB1401673

Analytical

06/06/2014

11

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Analytical / Detailed Estimating

• Traditional approach and understanding of ‘estimating’

Also known as “Bottom-Up”

• Most common technique in cost proposals

• Complete for each functional labour category against a breakdown

structure:

Engineering

Manufacturing

Program Management

Quality

Tooling and Test

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Equipment or Produce Breakdown Structure (PBS)

Helicopter

Airframe Propulsion

Engine Engine Control Engine Control

software

AV Application

software

Product Breakdown

Structure (PBS)

Work Breakdown Structure

(WBS)

Organisation

Breakdown Structure

(OBS)

Focus on what is deliverable!

06/06/2014

12

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Work Breakdown Structure (WBS)

PBS

Project

Management Engineering

Manufacture,

Assembly,

Integration and Test

Product Breakdown

Structure (PBS)

Work Breakdown Structure

(WBS)

Organisation

Breakdown Structure

(OBS)

Usually accompanied by a Work Package Description:

• Inputs

• Output

• Activities

• Assumption / Dependencies

• Duration / Effort

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Organisation Breakdown Structure (OBS)

PBS

WBS

Project Manager

Project Control

Cost Engineering

Configuration Control

Travel and Subsistence

costs

Product Breakdown

Structure (PBS)

Work Breakdown Structure

(WBS)

Organisation

Breakdown Structure

(OBS)

06/06/2014

13

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Helicopter

Airframe Propulsion

Engine Gear box Engine Control

Project Management Engineering MAIT

Project Manager

Project Control

Cost Engineering

Configuration Control

Requirements

analysis

Systems Eng.

Electronic Eng.

Mechanical Eng.

Travel and

Subsistence costs Computing costs

Material cost

Fabrication labour

Machining labour

Sub-contractor costs

AV Application software

Engine control s/w

Product Breakdown

Structure (PBS)

Work Breakdown Structure

(WBS)

Organisation

Breakdown Structure

(OBS)

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Detailed Build Up (Cont…)

• Estimated Labour – the Direct (booked) effort for a person;

Clearly identify all categories (functions) of labour required to complete the

Work Package activities

For example, Project Management time

Calculated in hours for example;

7.5 hours per day

37 hours per week

06/06/2014

14

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Detailed Build Up (Cont…)

• Estimated Non-labour – the direct (billable) cost expenditure;

Can be material, services, sub-contract costs or other direct costs

For example, travel and subsistence

Clearly identify all categories (test facilities, computer facilities, test

equipment, sub-contract support) of non-labour required to complete the

Work Package activities

Calculated in single monetary units (£1,000), not thousands(£1k), millions (£1m),

etc.

Identify the currency used, Pounds, Dollars, Euro

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Detailed Build Up (Cont…)

Excluded

• Overheads – the Indirect effort and costs that are not booked or

billable directly to the project

For example, Security staff, Executive staff

06/06/2014

15

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Detailed Build Up (Cont…)

• When estimating resources or time consider the activity as a functions of size, complexity and productivity relative to previous activities that you have completed.

• Resource (or time) = f (size, complexity, productivity)

Size = volume, weight, quantity, lines of code, surface area, power, thrust – the magnitude of the problem

Complexity = technology, materials, manufacturing process, design difficulty, novelty, number of interfaces, number of requirements, customer – level of difficulty

Productivity = tools, staff skills, scope of design, communications, language, access – achievement of the activity

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

# of Drawings x Drawing factor x Hours per Drawing

Case Study - Detailed Hour Build Up

• Estimated Number of Drawings = 100

• Drawing factor

Detailed drawing = 1.0

General Assembly = 1.5

• Engineering Dept. Standard = 40 Hours per Drawing

• Engineering basis of bid is then submitted to Cost Engineering function

for conversion to currency

Resource (or time) = f (size, complexity, productivity)

06/06/2014

16

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Disadvantages

Advantages

• Time and resource intensive

• Omissions and duplications likely

• Often subjective and can contain distortions

• Changes can be time consuming

• Detailed specifications are required

• MS Excel spreadsheets can become complicated

• Very Detailed

• Well accepted methodology

• High level of detail gives a perceived view of

‘accuracy’

• MS Excel usual choice of tool

Detailed Build Up (Cont…)

© Copyright QinetiQ Limited 2014

UNCLASSIFIED

QinetiQ Proprietary

QINETIQ/TIS/S&AS/PUB1401673

Analogy

06/06/2014

17

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Analogy

• A comparison between two systems or efforts

Based on a relative scaling of a data point

Determination of how much more or less the new system will be relative to

the historical data point

• Commonly used for ROMs and as cross-checks

• Subjective complexity factors are used many times to adjust analogous

system cost to new system

• Requires minimal time and cost

• Normally completed at the system or sub-system level

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Case study - Estimating by analogy

Performance

(Mach Speed)

Unit Production

Cost (UPC)

(UK £)

Old analogous system: Mach 1.5 £30 Million

• New system speed is 2x old system

• Cost of new system is therefore =

2 x £30m = £60m

• Analogy normally assumes a Linear

Relationship

06/06/2014

18

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Disadvantages

Advantages

• Can be subjective

• Assumes a linear relationship between cost, time

and technology

• Can be difficult to obtain detailed level of

information

• Can be used early in a project with minimum data

• Ideal for conceptual level estimating

Analogy (Cont…)

© Copyright QinetiQ Limited 2014

UNCLASSIFIED

QinetiQ Proprietary

QINETIQ/TIS/S&AS/PUB1401673

Parametric

06/06/2014

19

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Parametric Cost Model

• Commercially available cost models, for example:

FACET

SEER

TruePlanning

• Cost Estimating Relationships (CER) is also considered a Parametric

Cost Model

• Parametric Cost Model

Is a mathematical relationship:

Cost to Cost

Performance to Cost

Statistical inferences

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Parametric Cost Modelling

© PRICE Systems 2006 All

rights reserved

Historical

Project

Normalised

Independent

- Design

- Performance

Dependent

- Cost

- Schedule

- Performance

Cost Estimating Relationship (CER)

06/06/2014

20

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Filling the gaps - International Data

Non UK Vehicles

BMP - 3 Pandur

Tracked

Wheeled 2004 2006 2007?

FV432 Scorpion Striker Spartan Warrior

1963 1972 1975 1978 1986

Shortland APC

1965

Fox

1973

Saxon

1976

(PV)

Current UK Army vehicles

Future UK Vehicle

requirements

Non UK Vehicles

BMP - 3 Pandur

Tracked

Wheeled

Stingray

1988 1990

CV 9040

1993 1995

Pizarro

1998

Centuaro

1991

Simba

1993

Stingray CV 9040 Pizarro

1998

Centuaro Simba

2004 2006 2007?

1960 1970 1980 1990 2000 2010 1960 1970 1980 1990 2000

FV432 Scorpion Striker Spartan Warrior

1963 1972 1975 1978 1986

Shortland APC

1965

Fox

1973

Saxon

1976

(PV)

Current UK Army vehicles

Future UK Vehicle

requirements

FRES

MRAV, Tracer, ABSV

Indicative sample only from

QinetiQ database which covers

72 types of AFV in current

production and / or service

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

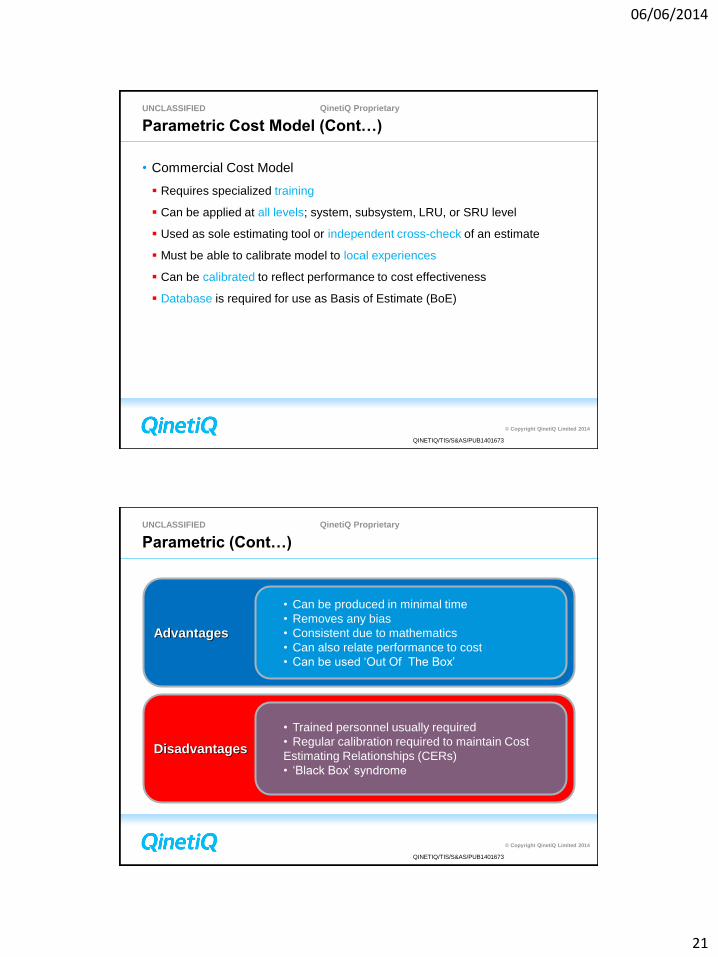

Parametric Cost Model (Cont…)

• Commonly used for:

ROMs

Proposal Costs

Trade Studies

Budgetary Estimates

• Requires more time than Analogy, but considerably less time and cost

than a Detailed Build Up

06/06/2014

21

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Parametric Cost Model (Cont…)

• Commercial Cost Model

Requires specialized training

Can be applied at all levels; system, subsystem, LRU, or SRU level

Used as sole estimating tool or independent cross-check of an estimate

Must be able to calibrate model to local experiences

Can be calibrated to reflect performance to cost effectiveness

Database is required for use as Basis of Estimate (BoE)

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Disadvantages

Advantages

• Trained personnel usually required

• Regular calibration required to maintain Cost

Estimating Relationships (CERs)

• ‘Black Box’ syndrome

• Can be produced in minimal time

• Removes any bias

• Consistent due to mathematics

• Can also relate performance to cost

• Can be used ‘Out Of The Box’

Parametric (Cont…)

06/06/2014

22

© Copyright QinetiQ Limited 2014

UNCLASSIFIED

QinetiQ Proprietary

QINETIQ/TIS/S&AS/PUB1401673

Selecting the Most Appropriate Methodology

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

General Selection Criteria

• The “most appropriate” methodology or methodologies is generally

based on considerations such as:

Program phase

Program requirements stability/maturity

Availability of relevant historical data

Type of estimate required

Customer requirements and/or preferences

Time and/or manpower to complete estimate

06/06/2014

23

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Programme Life Cycle

Selecting the Most Appropriate Methodology

Concept & Assessment Development / Demonstration

Manufacture & Entry Into Service

In Service Operation & Support

Parametrics

Analogy

Engineering / Bottom Up

Extrapolation From Actuals

Gross Estimate Detailed Estimate

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Parametric

Analytical Analogous

Little Confidence

Cost Cost

Time

Parametric

Analytical Analogous

More Confidence

Cost

Time

Multiple estimating methods provide confidence

06/06/2014

24

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

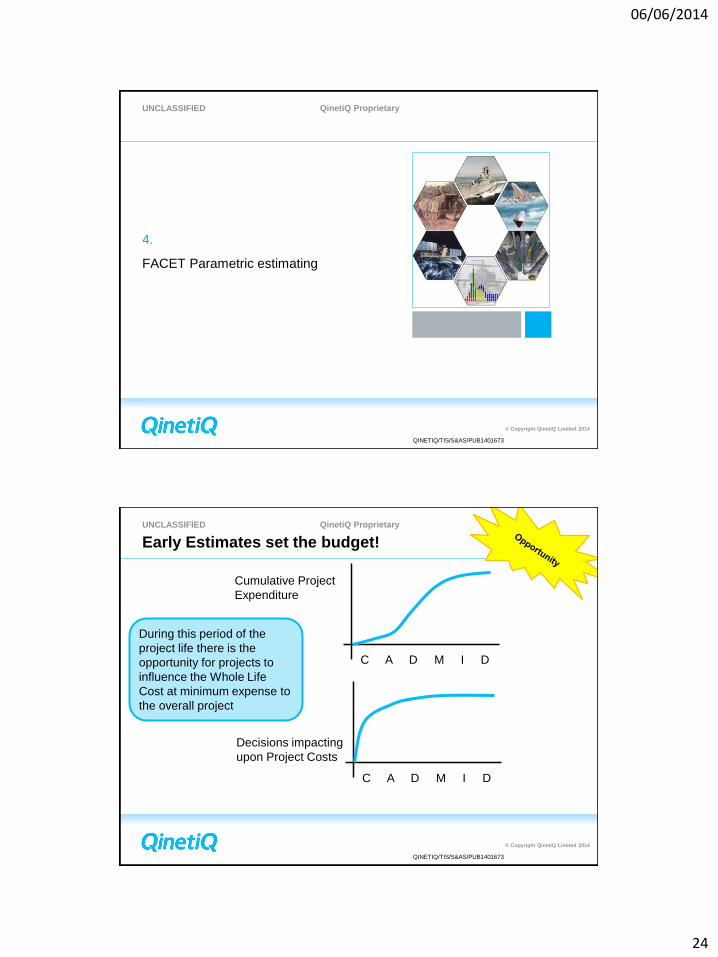

4.

FACET Parametric estimating

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Early Estimates set the budget!

C A D M I D

C A D M I D

Cumulative Project

Expenditure

Decisions impacting

upon Project Costs

During this period of the

project life there is the

opportunity for projects to

influence the Whole Life

Cost at minimum expense to

the overall project

06/06/2014

25

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Operational

Analysis

• Identify Acquisition cost

• Identification of In-service cost

• Top level trade off

• Performance

• Design

• Programme issues.

• Down selection of options

• Multiple platform solutions.

Key Decision made at the very beginning of a project

need to be based on sound information such as;

Cost Estimating aims

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Combining Performance and Design

06/06/2014

26

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

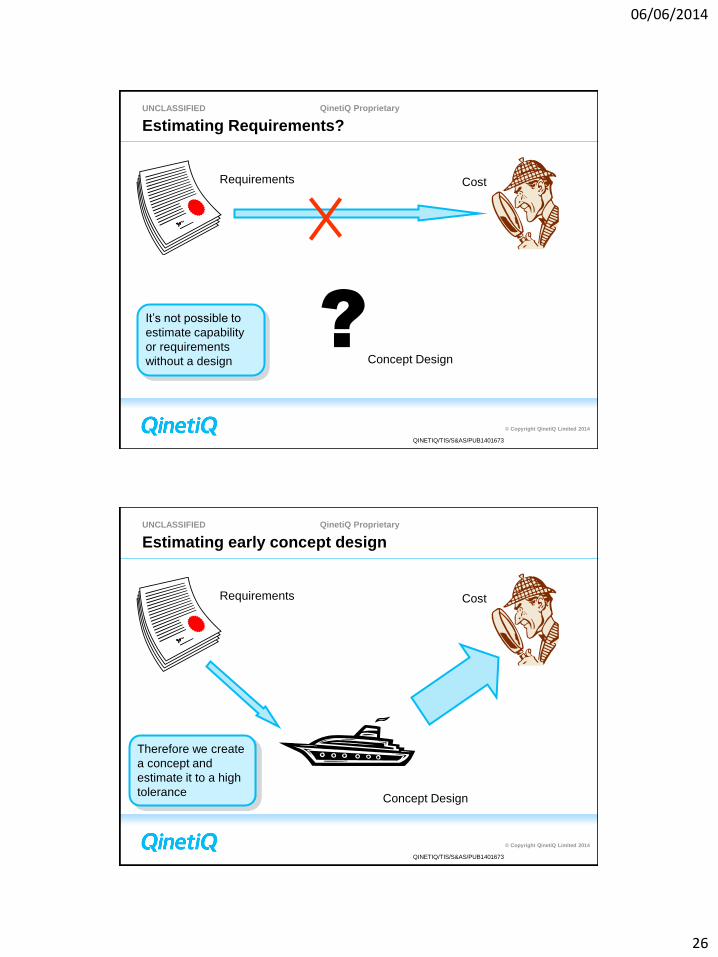

Estimating Requirements?

Requirements Cost

Concept Design

? It’s not possible to

estimate capability

or requirements

without a design

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Estimating early concept design

Requirements Cost

Concept Design

Therefore we create

a concept and

estimate it to a high

tolerance

06/06/2014

27

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

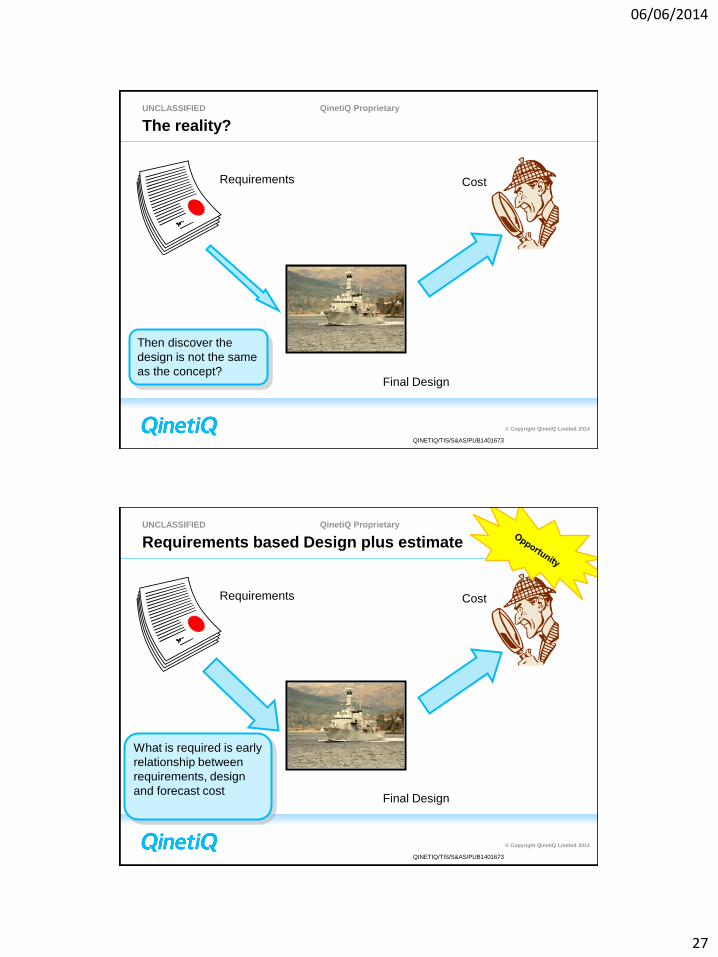

The reality?

Requirements Cost

Final Design

Then discover the

design is not the same

as the concept?

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Requirements based Design plus estimate

Requirements Cost

Final Design

What is required is early

relationship between

requirements, design

and forecast cost

06/06/2014

28

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Deterministic prediction for X

In-service

date

Cost p

er

un

it m

ass

Prediction

X

Y

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Recognising the uncertainty in the input

In-service

date

Cost p

er

un

it m

ass

Prediction

X

Distribution Y

06/06/2014

29

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Recognising the compound error of CER and input

In-service

date

Cost p

er

un

it m

ass

Prediction

X

Distribution Y

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Case studies

06/06/2014

30

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

0

5

10

15

20

25

1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Date

Pro

gra

mm

e C

os

ts F

Fr

Bn

Case study - Charles De Gaulle; Programme Costs

Programme authorised

First steel cut

First block

Official Launch

Start of sea trials

Commissioned

FFr 15.6 Bn First

published estimate of

the Programme cost

April 1992

FFr 17.2Bn

FFr 18.8Bn

FFr 20 Bn Last

Programme cost

estimate Sept 2000

FFr 20.38 Bn Estimated

Programme cost. Using

FACET and only technical

data available in 1992

28% cost growth between first and last

official programme costs

Less than 2% difference between

FACET and last official programme cost

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

0

2

4

6

8

10

12

14

16

18

20

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Date

Pro

gra

mm

e C

os

ts E

uro

Bn

Case study - Eurofighter Development Costs

Less benefit of EAP

demonstrator

FACET

Official

Feasibility study

French withdraw

Start Project Definition

Development start

Production start

110% cost growth between first and last

official programme costs

Less than 8% difference between

FACET and last official programme cost

06/06/2014

31

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

£0M £100M £200M £300M £400M £500M £600M

Option 3

Option 2

Option1

MoD Indicative Design

Commercial Design

(risk to performance from under sizing)

(Size well matched to

MoD requirements)

281 397

366 486

437 519

470 550

492 563

Bands show spread of ± standard error about

estimate

Programme cost (1994 prices)

Key

LCU EH-01 Spot

Flag Capability

Reduced Cost Options

Case study - Balance of Investment (BOI)

• Buying a new ship

with a limited

budget:

Identify alternative

options;

Estimates quickly

with tolerances on

the estimates;

Analyse what is

afforable;

Consider cost-

effectivness.

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

FACET Model

06/06/2014

32

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

FACET WLC Models : Input Screen

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

FACET WLC Models : Input Screen

1,000 kg

reduction

06/06/2014

33

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

FACET WLC Models : Results Screen

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

FACET Cost Context Model Output

The context model provide a rapid

evaluation capability of quotation and

internal estimates

06/06/2014

34

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

5.

Austerity – project cost saving

measures

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Non-recurring cost

• Non-recurring costs are defined

as those which only happen

once in a project.

• Non-recurring costs can be

either;

• duration-related, for example

project management, or

• task-related, for example

conducting a stress analysis.

06/06/2014

35

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

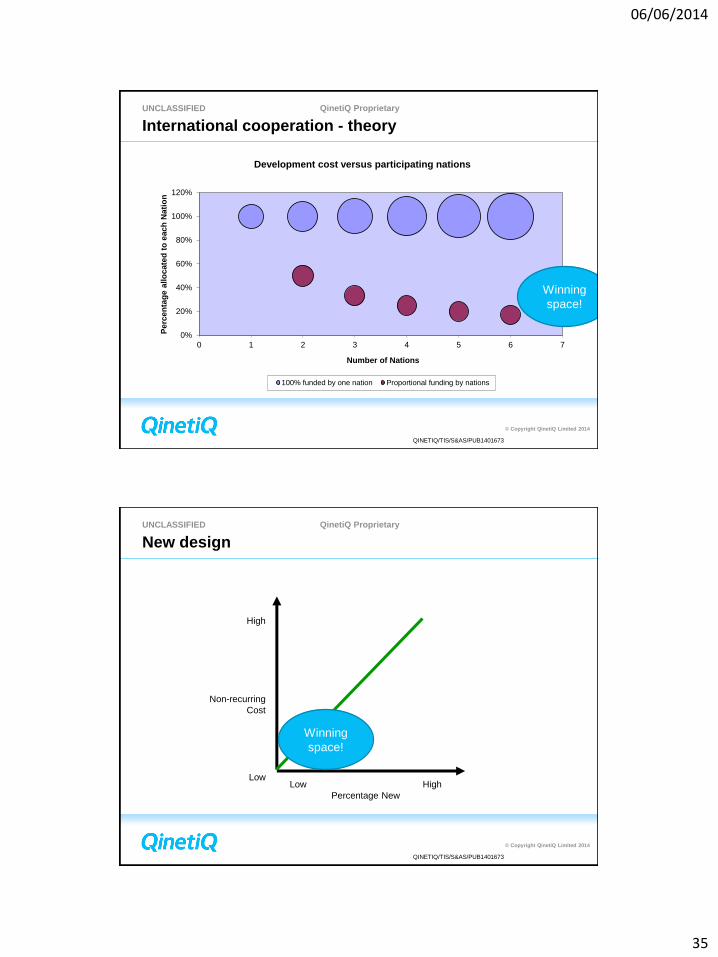

0%

20%

40%

60%

80%

100%

120%

0 1 2 3 4 5 6 7

Perc

en

tag

e a

llo

cate

d t

o e

ac

h N

ati

on

Number of Nations

Development cost versus participating nations

100% funded by one nation Proportional funding by nations

International cooperation - theory

Winning

space!

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

New design

High

Non-recurring

Cost

Low Low High

Percentage New

Winning

space!

06/06/2014

36

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Commonality / modularity in development

High

Non-recurring

Cost

Low

Low High

Design Repeat

Winning

space!

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

New

Adapted

Deleted

Translated

0% Test

0% Code

0% Design

Auto Generation

?% Design

?% Code

?% Test

Reused

100% Test

100% Code

100% Design

Software development is a non-recurring activity

Winning

space!

06/06/2014

37

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

1 2 3 4 5 5 6 7 8 9 1011121314151617181920

Cap

ab

ility

Years in-service

Incremental Traditional

Incremental development versus ‘big bang’

Winning

space!

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Time

Cost Lower complexity Higher complexity

Time Now

Cheaper but less capable technology

Not desirable for Defence

Market forces = technology maturity

06/06/2014

38

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Recurring cost

• Recurring costs are defined as

those which occur repeatedly in

a project.

• Recurring costs tend to be task-

related (rather than duration-

related), for example

manufacturing components.

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Overlapping schedule

Development

Production

Delayed schedule

Development

Production

Optimisation of the schedule

Optimised schedule

Development

Production

Winning

space!

06/06/2014

39

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

100 off

50 off

UPC50

UPC100

Learning or Cost improvement curve

Assumes:

• Low turnover of staff;

• Consistent manufacturing

process;

• Single shift pattern;

• Single facility;

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

100 off

50 off x UPC100

Learning or Cost improvement curve

Acquire 50 off items from a total batch of 100 off

Assumes:

• that you only pay for the items you require

• you take evenly over the period

• there is a customer for the other 50 off

06/06/2014

40

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

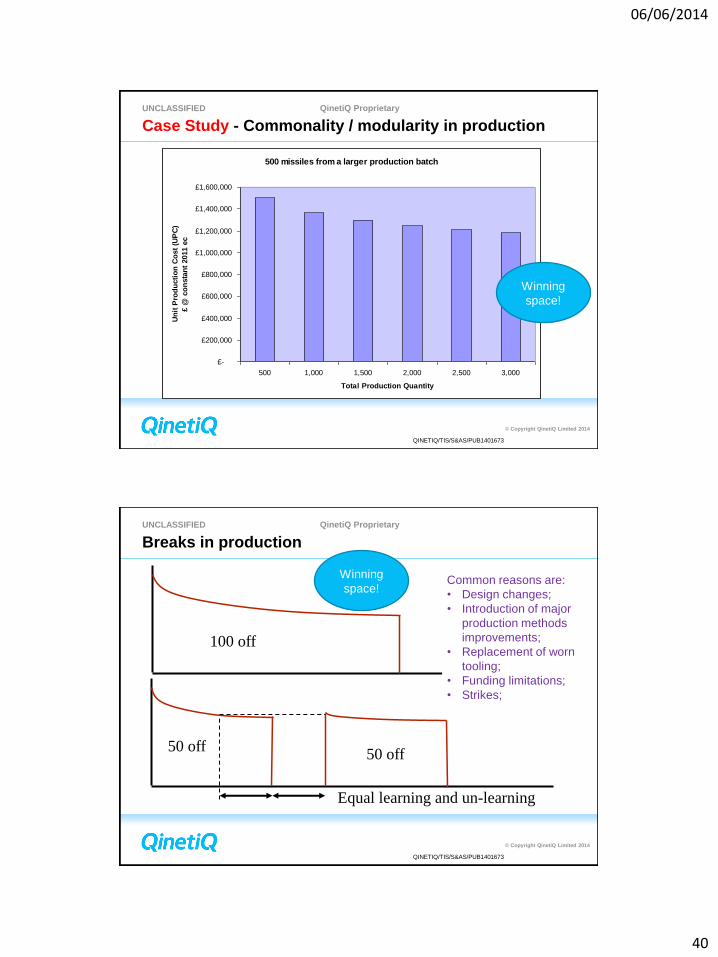

500 missiles from a larger production batch

£-

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

500 1,000 1,500 2,000 2,500 3,000

Total Production Quantity

Un

it P

rod

ucti

on

Co

st

(UP

C)

£ @

co

nsta

nt

2011 e

c

Case Study - Commonality / modularity in production

Winning

space!

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

100 off

50 off 50 off

Equal learning and un-learning

Breaks in production

Winning

space! Common reasons are:

• Design changes;

• Introduction of major

production methods

improvements;

• Replacement of worn

tooling;

• Funding limitations;

• Strikes;

06/06/2014

41

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

In-service cost

• In-service costs are defined as

costs which occur following the

manufacture of the platform,

system or service.

• As such they have a tendency

to be event based, such as

failures or maintenance

opportunities.

• In-service cost can be duration-

related or task-related, but the

tasks will have a rhythm or

periodicity.

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

In-service costs

Reliability

Infant

mortality

Wear out

System Life (Years)

Number of failures

Reduce optimise in-service cost:

• Anticipate obsolescence / regulatory requirements;

• Monitor fleet failures rates;

• Reduce usage through synthetic training;

06/06/2014

42

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

In-service costs

Reliability

Midlife

update

System Life (Years)

Number of failures

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

In-service costs

• Reduce Required Spares Holdings

Improve repair pipeline times

Improve/optimise spares holdings

Pool key assets between Nations

Optimise storage and transportation

• Reduce Repair Costs

Cost optimise repair capabilities, national vs international

Improve utilisation of maintenance and fault data to improve maintenance

policies and anticipate

Challenge industrial cost base

Design out cost drivers

06/06/2014

43

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

6.

Summary

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Summary

• Reviewed cost and risk maturity

assessment – How good are your

numbers?

• Consider three estimating

methodologies to add confidence to

your cost predictions;

• Utilise parametrics cost modelling as a

source of independent cost estimating

(ICE) and prompt areas of cost saving;

• Identified some Austerity measures that

can be deployed to reduce potential

costs.

06/06/2014

44

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

Any questions?

QinetiQ

Building 240

The Close

Bristol Business Park

Coldharbour Lane

Bristol BS16 1FJ

United Kingdom

Tel +44 (0)117 953 8455

Mobile +44 (0)7785 522 847

www.QinetiQ.com/als

Dale Shermon

QinetiQ Fellow /

Head of Profession Cost Engineering

QinetiQ

Building 240

The Close

Bristol Business Park

Coldharbour Lane

Bristol BS16 1FJ

United Kingdom

Tel +44 (0)117 953 8455

Mobile +44 (0)7785 522 847

dshermon@QinetiQ

.com

www.QinetiQ.com/als

Dale Shermon

QinetiQ Fellow /

Principal C

onsultant

UNCLASSIFIED QinetiQ Proprietary

© Copyright QinetiQ Limited 2014

QINETIQ/TIS/S&AS/PUB1401673

www.QinetiQ.com