Corporate Valuation and Financing

26

Corporate Valuation and Financing IPOs Prof H. Pirotte

-

Upload

cruz-raymond -

Category

Documents

-

view

29 -

download

1

description

Corporate Valuation and Financing. IPOs. Initial Capital Very early stage “Family, Friends and Fools”, notion of Angel Investors Venture capital firms=> specialized in raising capital for young firms => often diversification benefits =>possibility to benefit from expertise - PowerPoint PPT Presentation

Transcript of Corporate Valuation and Financing

Corporate Valuation and FinancingIPOsProf H. Pirotte

Introduction

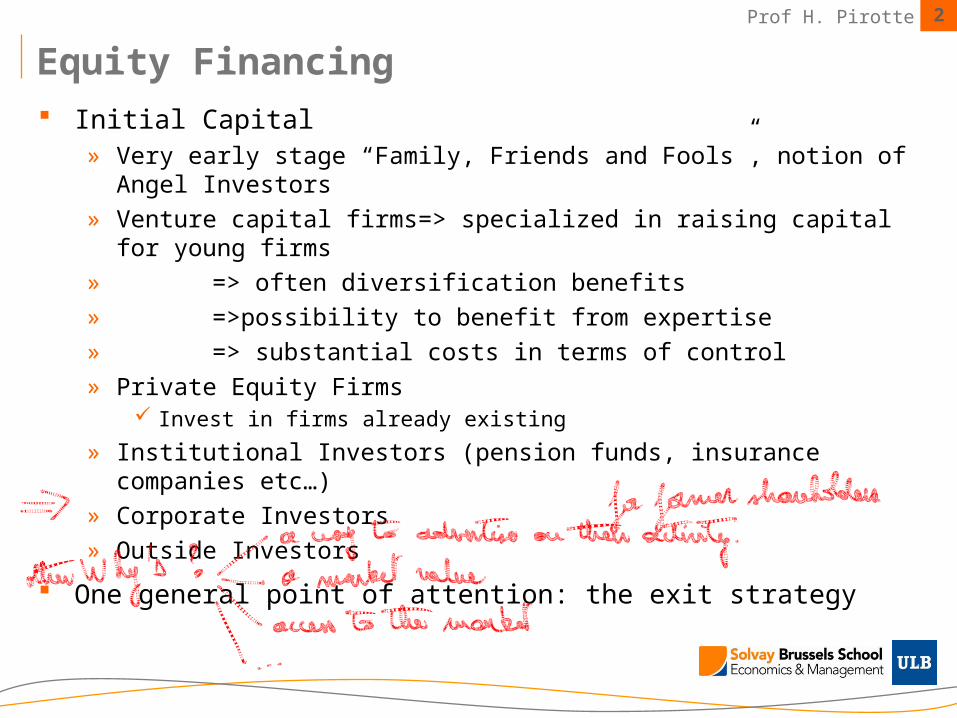

Equity Financing Initial Capital

» Very early stage “Family, Friends and Fools”, notion of Angel Investors» Venture capital firms=> specialized in raising capital for young firms» => often diversification benefits» =>possibility to benefit from expertise» => substantial costs in terms of control» Private Equity Firms

Invest in firms already existing» Institutional Investors (pension funds, insurance companies etc…)» Corporate Investors» Outside Investors

One general point of attention: the exit strategy

Prof H. Pirotte 2

Introduction

Introduction The natural evolution of firm’s capital

» Association of founders» Incorporation (shares owned by founders, key-employees and some early

investors)» Bank and private loans» Going public, mainly through an IPO a strategic decision

Steps» Awareness and preparation

Cleansing Manage as a public firm Change marketing strategy Develop key contacts

» The offer» The new corporate life

Primary vs. secondary issues

Going public Prof H. Pirotte 3

Introduction

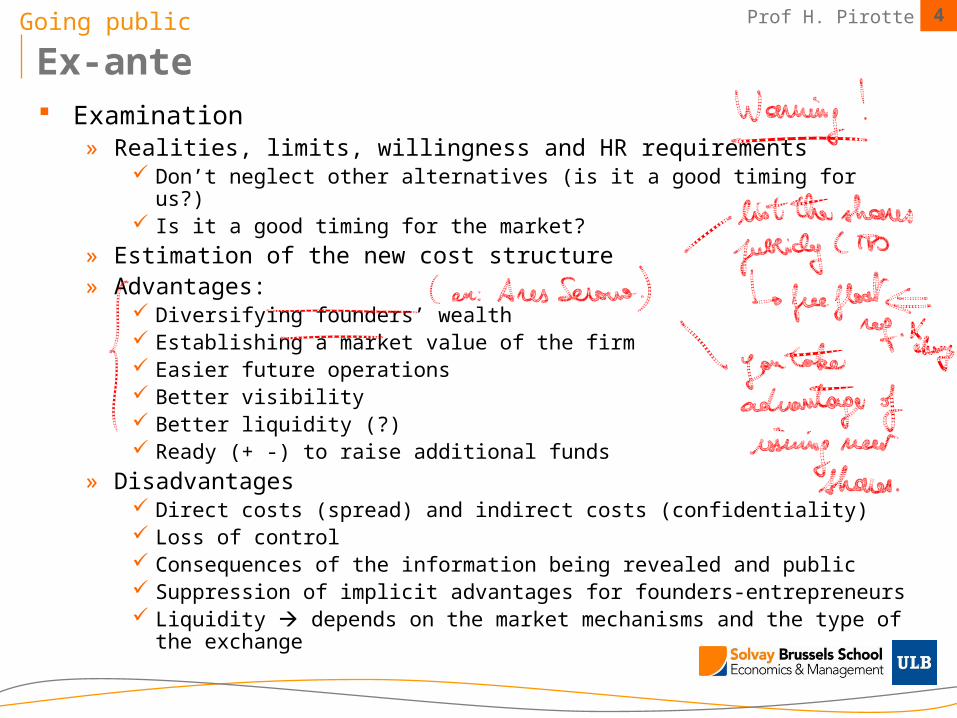

Ex-ante Examination

» Realities, limits, willingness and HR requirements Don’t neglect other alternatives (is it a good timing for us?) Is it a good timing for the market?

» Estimation of the new cost structure» Advantages:

Diversifying founders’ wealth Establishing a market value of the firm Easier future operations Better visibility Better liquidity (?) Ready (+ -) to raise additional funds

» Disadvantages Direct costs (spread) and indirect costs (confidentiality) Loss of control Consequences of the information being revealed and public Suppression of implicit advantages for founders-entrepreneurs Liquidity depends on the market mechanisms and the type of the exchange

Going public Prof H. Pirotte 4

Introduction

Ex-post Evidence

» Any decision will be judged by the market» Rumours, internal and external events will have an impact» Never neglect your shareholders» You must keep the contact with the market» The management activity must be more structured, ready to justify any decision» Keep enough breath to guarantee the continuity of the strengths of the firm

Going public Prof H. Pirotte 5

Introduction

The Market It is highly dependent on the state of the economy and it generally concerns

» Firms of “new economies” and birth of “new markets”» Firms deciding to go public» Privatisations» Spin-offs

In Switzerland

IPO process

IPO en Suisse

0

5

10

15

20

25

30

1997 1998 1999 2000 2001 2002 2003

Le marché des IPO en Suisse

24%

24%13%9%

6%

5%

19%CSFB

UBS Warburg

Bank Vontobel

ZKB

Bank J ulius Bär

ABN Amro

Autres

Prof H. Pirotte 6

Introduction

The Market In Europe

Source:ECMI Paper,n°2, August 2006

IPO process Prof H. Pirotte 7

Introduction

Process Preliminary phase

» After approval of the Board of Directors, the managers ask for an “underwriter”. Role:

Advisory / Pricing / Sale of shares / Syndication» Selection of the investment banker: “competitive bid” or “negotiated offer”» Appraisal of fundamental data of the firm

Long-term planning and future opportunities» The firm uses the services of lawyers and expert accountants (via the investment

banker) to write the preliminary prospectus (“red herring”). Due diligence

» Follow-up of market conditions» Pre-marketing: analysis of attractiveness, price sensitivity, feedback

Final phase» Roadshow: presentation of the “equity story”» Once the corrections made following the comments of the regulatory commission,

the final prospectus is issued. “Tombstones” are used before and after the issuance (marketing the IPO)

» Bookbuilding and the book

IPO process Prof H. Pirotte 8

Introduction

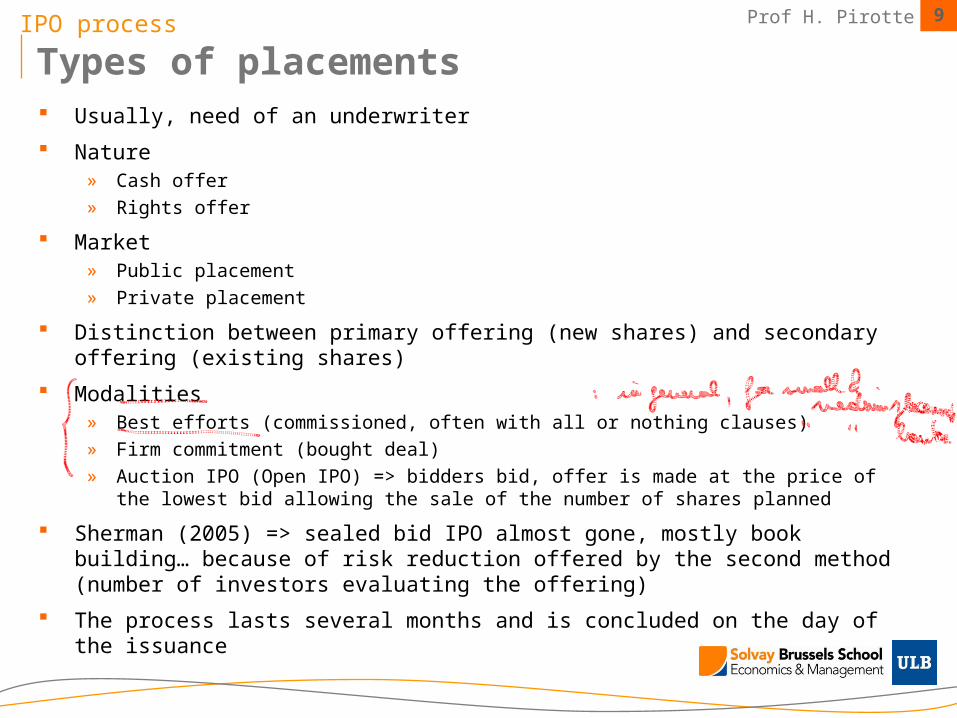

Types of placements Usually, need of an underwriter

Nature» Cash offer» Rights offer

Market» Public placement» Private placement

Distinction between primary offering (new shares) and secondary offering (existing shares)

Modalities» Best efforts (commissioned, often with all or nothing clauses)» Firm commitment (bought deal)» Auction IPO (Open IPO) => bidders bid, offer is made at the price of the lowest bid allowing the sale of the

number of shares planned

Sherman (2005) => sealed bid IPO almost gone, mostly book building… because of risk reduction offered by the second method (number of investors evaluating the offering)

The process lasts several months and is concluded on the day of the issuance

IPO process Prof H. Pirotte 9

Introduction

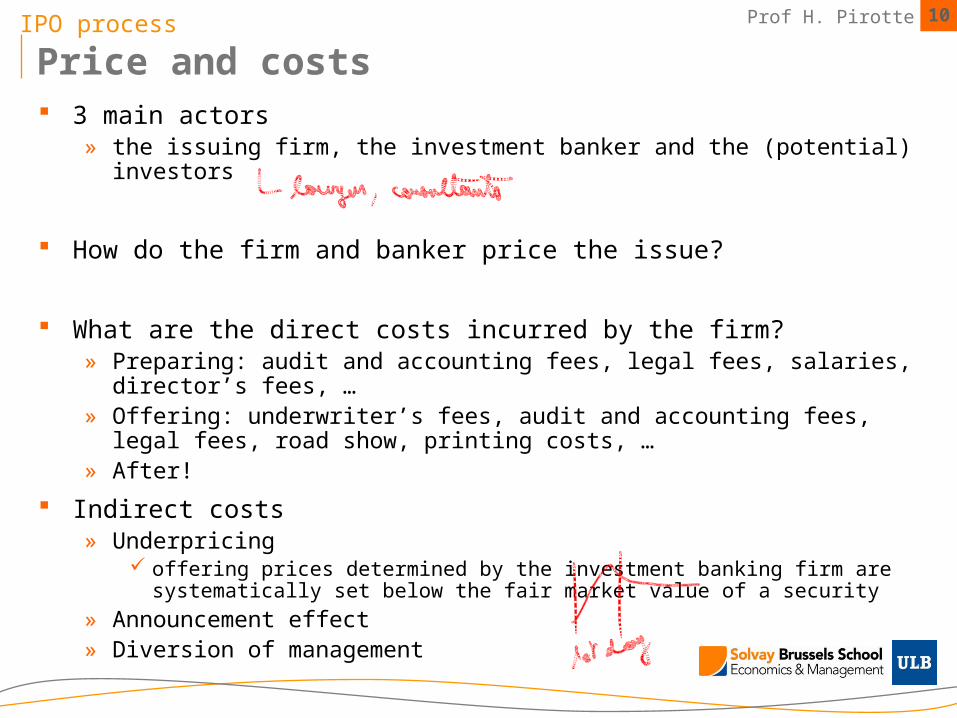

Price and costs 3 main actors

» the issuing firm, the investment banker and the (potential) investors

How do the firm and banker price the issue?

What are the direct costs incurred by the firm?» Preparing: audit and accounting fees, legal fees, salaries, director’s fees, …» Offering: underwriter’s fees, audit and accounting fees, legal fees, road show,

printing costs, …» After!

Indirect costs» Underpricing

offering prices determined by the investment banking firm are systematically set below the fair market value of a security

» Announcement effect» Diversion of management

IPO process Prof H. Pirotte 10

Introduction

Types of mechanisms

Source:ECMI Paper,n°2, August 2006

IPO process Prof H. Pirotte 11

Introduction

Short-term performance (underpricing)

Krigam, Shaw and Womack (1999), The Persistence of IPO Mispricing and the Predictive Power of Flipping, Journal of Finance.

IPO underpricing Prof H. Pirotte 12

Introduction

Short-term performance (underpricing)

Krigam, Shaw and Womack (1999), The Persistence of IPO Mispricing and the Predictive Power of Flipping, Journal of Finance.

IPO underpricing Prof H. Pirotte 13

Introduction

Short-term performance (underpricing)

Ritter & Welch (2002), A REVIEW OF IPO ACTIVITY, PRICING AND ALLOCATIONS, Yale Working Paper

IPO underpricing Prof H. Pirotte 14

Introduction

Short-term performance (underpricing)

Source: ECMI Paper, n°2, August 2006

IPO underpricing Prof H. Pirotte 15

Introduction

Short-term performance (underpricing)

Source: ECMI Paper, n°2, August 2006

IPO underpricing Prof H. Pirotte 16

Introduction

Short-term performance (underpricing)

Source: ECMI Paper, n°2, August 2006

IPO underpricing Prof H. Pirotte 17

Introduction

Short-term performance (underpricing) Various studies

Paper Period Abnormal Return (1st month)

Ibbotson [1975] 60-69 11.4 %

Ibbotson & Jaffe [1974] 60-70 16.8 %

Ritter [1984] 77-82 Firm commitment 14.8 %Best efforts 42.8 %

Paper Conclusion

Loughran & Ritter [1995] 5y 30% underperformance against benchmark

Brav and Gompers [1997]

Even with benchmark

Fama [1998] IPOs are typically small high-growth stocks and they all have low returns in the post-1963 period.

IPO underpricing Prof H. Pirotte 18

Introduction

But in the long-run… While all studies show a positive average of 19% abnormal return at the end of

the first trading day based on unadjusted returns, they show a negative abnormal performance in the long-run, underperforming the market by 23% over the next 3 years, or underperforming a benchmark portfolio of similar size and book-to-market ratio by 5%.(Copeland, Weston and Shastri 2005)

Puzzle?

Paper Conclusion

Loughran & Ritter [1995] 5y 30% underperformance against benchmark

Brav and Gompers [1997]

Even with benchmark

Fama [1998] IPOs are typically small high-growth stocks and they all have low returns in the post-1963 period.

IPO underpricing Prof H. Pirotte 19

Introduction

Evidence…

Paper Conclusion

Hickman [1953], Marsh [1982], Taggart [1977]

Fluctuations of outside finance raised via equity.

Firms issue equity after their own stock has risen relative to the market

Choe, Masulis & Nanda [1989] Negative reaction to announcement of an equity issue is smaller when volume of all equity issues is high.

Krigam, Shaw and Womack [1999]

First day winners continue to be winners over the first year.First day dogs continue to be relative dogs.Exception for extra-hot IPOs that provide the worst future perf.Large “informed” traders “flip” IPOs that perform the worst in the future. IPOs with low flipping perform well during the first 6 months. Flipping is predictable and underwriters pricing errors are intentional.1988-1995: 1’232 large-capitalization IPOs12%: +30% or more on the first trading day25%: closed at or below the offer price

IPO underpricing Prof H. Pirotte 20

Introduction

Evidence… (2)

Krigam, Shaw and Womack (1999), The Persistence of IPO Mispricing and the Predictive Power of Flipping, Journal of Finance.

IPO underpricing Prof H. Pirotte 21

Introduction

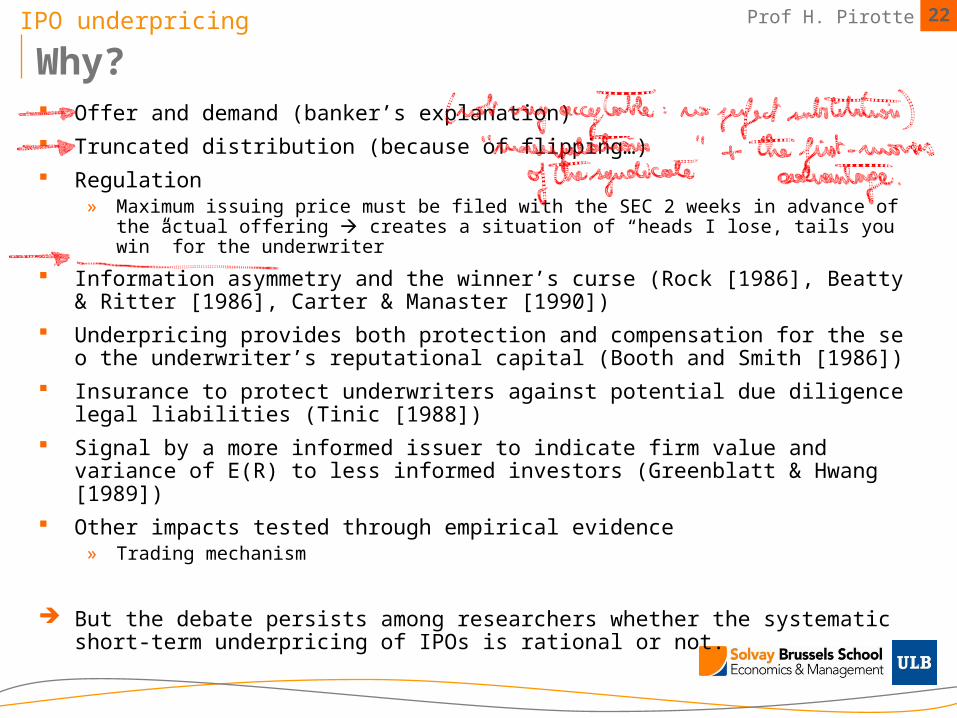

Why? Offer and demand (banker’s explanation) Truncated distribution (because of flipping…) Regulation

» Maximum issuing price must be filed with the SEC 2 weeks in advance of the actual offering creates a situation of “heads I lose, tails you win” for the underwriter

Information asymmetry and the winner’s curse (Rock [1986], Beatty & Ritter [1986], Carter & Manaster [1990])

Underpricing provides both protection and compensation for the se o the underwriter’s reputational capital (Booth and Smith [1986])

Insurance to protect underwriters against potential due diligence legal liabilities (Tinic [1988]) Signal by a more informed issuer to indicate firm value and variance of E(R) to less informed

investors (Greenblatt & Hwang [1989]) Other impacts tested through empirical evidence

» Trading mechanism

But the debate persists among researchers whether the systematic short-term underpricing of IPOs is rational or not.

IPO underpricing Prof H. Pirotte 22

Introduction

The winner’s curse The Medium guy and the Smart guy…

» Since prices tend to rise during the first hour of trading, Medium invests an equivalent amount in all IPOs. Can Medium obtain an abnormal return?

» Example Smart can take 1’000 shares

Medium can take 1’000 shares, and invests 100 shares by IPO A is an undervalued firm: Smart asks for 1’000 shares, Medium asks for 100 shares

But only 110 shares are issued: 100 for Smart and 10 for Medium. B is an overvalued firm: Medium asks for 100, Smart for 0.

» To avoid this phenomenon, issuing prices are understated by 30-40% to ensure a minimum riskfree rate to Medium.

IPO underpricing Prof H. Pirotte 23

Introduction

Rock (1986) Assumptions

» Prices and volumes are fixed» If demand > offer rationing» The firm wants to issue N shares» Each share has a value v (random variable, know probability density function f )» 2 types of investors

Uninformed: U investors owning 1€ each, don’t know v. Informed: total wealth of I, they know v.

» The firm doesn’t know v, but chooses p, the issuing price.» I < N E(v) the firm must attract uninformed investors» The demand of the uninformed investors depends on p, not on v.» Demand of informed investors

I if v > p 0 if v p

IPO underpricing Prof H. Pirotte 24

Introduction

Rock (1986) - 2 Model

» The profit of uninformed investors, if they invest is given by

» Uninformed investors receive more shares when v < p winner’s curse» To attract uninformed investors, the company must choose a price lower than E(v)

such that E(U) = 0

where

( ) ( - ) ( ) ( - ) ( )U

v p v p

UE v p f v dv v p f v dv

I U

max U such that E( ) 0 ( ) ( ) ( ) 0v p

p E V p v p f v dv

UI

I

IPO underpricing Prof H. Pirotte 25

Introduction

Rock (1986) - 3 Example

» Hypothesis: f (v) is uniform on the following interval

» The condition can be written

» Typical cases = 0

2

1v,

2

1v

dp

d 0

dp

d 0

v p v p

2

1

20

2

IPO underpricing Prof H. Pirotte 26