Corporate Rescue and the New Financial Rehabilitation and ...€¦ · DIME & EVIOTA LAW FIRM 2010...

32

DIME & EVIOTA LAW FIRM 2010 Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010 [A DLDTE LAW CLIENT PAPER] Ronald B. Dime 2/F M IDWAY COURT BLDG ., 241 EDSA MAND . CITY , PHILS .

Transcript of Corporate Rescue and the New Financial Rehabilitation and ...€¦ · DIME & EVIOTA LAW FIRM 2010...

DIME & EVIOTA LAW FIRM

2010

Corporate Rescue and the

New Financial

Rehabilitation and

Insolvency Act of 2010 [A DLDTE LAW CLIENT PAPER]

Ronald B. Dime

2 / F M I D W A Y C O U R T B L D G . , 2 4 1 E D S A M A N D . C I T Y , P H I L S .

2

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

I. INTRODUCTION: A BRIEF HISTORY For a long time, a distressed corporation in the Philippines had no other

real recourse than to commit legal seppuku, whether or not its financial

condition was due to the fundamental unsoundness of its business or merely a

temporary run in with bad luck.

This lack of any real corporate rescue vehicle characterized the legal

environment that prevailed under the regime of Act No. 1956 (otherwise known

as the “Insolvency Law”) from the time of its enactment on 20 May 1909 until the

early 1980s1.

Act 1956 by itself introduced major changes to corporate law and removed

the distinction in the Spanish system between “insolvency”

and “bankruptcy.” Nonetheless, the Insolvency Law’s approach to corporate

rescue was simply to provide a “solvent but illiquid” debtor temporary relief from

payment of its debts while an “insolvent” corporation was forced to undertake a

gradual and organized liquidation process2.

1 The Insolvency Law of the Philippines is in fact a derivative of even

older laws from other jurisdictions, such as the California Insolvency

Law of 1895 and the American bankruptcy Act of 1867 [See Sun Life

Assurance Co. of Canada v. Frank B Ingersoll, et. al.; GR No. 164758

(November 1921)]

2 The three main remedies under Act 1956 are:

a) Petitions for the suspension of payments by an individual, sociedad

or corporation under Section 2 of the Insolvency Law:

Section 2. The debtor who, possessing sufficient property

to cover all his debts, be it an individual person, be it a

sociedad or corporation, foresees the impossibility of

meeting them when they respectively fall due, may petition

that he be declared in the state of suspension of payments

by the court, or the judge thereof in vacation, of the

province or of the city in which he has resided for six

months next preceding the filing of his petition.

b) Petitions for Voluntary dissolution under Section 14:

Section 14. An insolvent debtor, owing debts exceeding in

amount the sum of one thousand pesos, may apply to be

discharged from his debts and liabilities by petition to

the Court of First Instance of the province or city in

3

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

In 1981, then President Marcos issued Presidential Decree (P.D.) No. 1758

which amended P.D. No. 902-A. For the first time, the concept of “corporate

rehabilitation” was introduced. This is contained in an addendum to the powers

formerly granted to the Securities and Exchange Commission (SEC)3 under

Section 5 of PD No. 902-A, to wit:

“Section 5. In addition to the regulatory and adjudicative functions of the Securities and Exchange commission over corporations, partnerships and other forms of association registered with it expressly granted under existing laws and decrees, it shall have original and exclusive jurisdiction to hear and decide cases involving:

x x x

“d) Petitions of corporations, partnerships or associations to be declared in the state of suspension of payments in cases where the corporation, partnership or association possesses sufficient property to cover all its debts but foresees the impossibility of meeting them when they respectively fall due or in cases where the corporation,

which he has resided for six months next preceding the

filing of such petition. In his petition he shall set forth

his place of residence, the period of his residence therein

immediately prior to filing said petition, his inability to

pay all his debts in full, his willingness to surrender all

his property, estate, and effects not exempt from execution

for the benefit of his creditors, and an application to be

adjudged an insolvent. He shall annex to his petition a

schedule and inventory in the form hereinafter provided.

the filing of such petition shall be an act of insolvency.

c) Petitions for Involuntary Insolvency:

Section 20. An adjudication of insolvency may be made on

the petition of three or more creditors, residents of the

Philippine islands, whose credits or demands accrued in the

Philippine Islands, and the amount of which credits or

demands are in the aggregate of not less than one thousand

pesos; Provided, that none of said creditors has become a

creditor by assignment, however made, within thirty days

prior to the filing of said petition. Such petition must be

filed in the Court of first Instance of the province or

city in which the debtor resides or has his principal place

of business, and must be verified by at least three of the

petitioner. the following shall be considered acts of

insolvency, and the petition shall set forth one or more of

such acts: xxx

3 Jurisdiction has since been transferred to the Regional Trial Court.

4

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

partnership or association has no sufficient assets to cover its liabilities, but is under the management of a Rehabilitation Receiver or Management Committee created pursuant to this Decree.”

[as amended by P.D. 1758]

One of the innovations created by PD 1758 is that while an insolvent

corporation (i.e. one that does not have sufficient assets to cover its debts) was

limited to a Petition for Insolvency resulting in liquidation of assets under Act

1956; a corporation, which is technically “insolvent,” was given the authority to

prove that it can be rehabilitated with court supervision. As explained by the

Supreme Court:

“Section 5, par. (d) should be construed as vesting upon the SEC original and exclusive jurisdiction only over petitions to be declared in a state of suspension of payments, which may either be: (a) a simple petition for suspension for payments based on the provisions of the Insolvency Law, or (b) a similar petition accompanied by a prayer for the creation/ appointment of a management committee and/ or rehabilitation receiver based on the provision of P.D. No. 902-A. Said provision cannot be stretched to include petitions for insolvency. The reason is that under said Section 5, par. (d) above-quoted, the jurisdiction of the SEC over cases where the corporation, partnership or association has no sufficient assets to cover its liabilities, and therefore insolvent, is qualified by the conjunctive phrase "but is under the management of a Rehabilitation Receiver or Management Committee created pursuant to this Decree." This qualification effectively circumscribes the jurisdiction of the SEC over insolvent corporations, partnerships and associations and consequently, over proceedings or the declaration of insolvency. It demonstrates beyond doubt that jurisdiction over insolvency proceedings pertains neither in the first instance nor exclusively to the SEC, but only in continuation of or as incident to the exercise of its jurisdiction over petitions to be declared in a state of suspension of payments wherein the petitioning corporation, partnership or association had previously been placed under a rehabilitation receiver or management committee by the SEC itself.

“Viewed differently, where the petition filed is one for

5

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

declaration of a state of suspension of payments due to a recognition of the inability to pay one's debts and liabilities, and where the petitioning corporation either : (a) has sufficient property to cover all its debts but foresees the impossibility of meeting them as they fall due (solvent but illiquid) or (b) has no sufficient property (insolvent) but is under the management of a rehabilitation receiver or a management committee, the applicable law is P.D. No. 902-A pursuant to Sec. 5, par. (d) thereof. However, if the petitioning corporation has no sufficient assets to cover its liabilities and is not under a rehabilitation receiver or a management committee created under P.D. 902-A, and does not seek merely to have the payments of its debts suspended, but seeks a declaration of insolvency, as in this case, the applicable law is Act 1956 on voluntary insolvency, specifically section 14 therefor, which states:

“x x x”

[Land Bank of the Philippines vs. Capistrano, et al. G.R. No 73123, 2 September 1991]

It may be convenient to mention at this juncture that by the “Law” on

corporate rehabilitation, is meant that body of rules that govern: (i) formal and

substantive requirements of rehabilitation, (ii) effects of rehabilitation, (iii)

procedural rules as well as (iv) liquidation and disposition of assets. For the most

part, this body of rules was developed over time by the courts4. Thus, aside from

jurisprudence, the chief tomes of rehabilitation practice are Administrative

Matter (A.M.) No. 00-8-10-SC, otherwise known as the “Rules of Procedure on

Corporate Rehabilitation5 of 2008” (hereinafter, the “2008 Rules”) which took

the place of the 2000 Interim Rules on Corporate Rehabilitation (hereinafter,

the “Interim Rules”) as well as some related provisions of A.M. No. 01-2-04 SC or

the “Interim Rules of Procedure for Intra-Corporate Controversies” (circa

2001).

4 Thus, in a sense, mimicking Common Law.

5 Which amended the 2000 Interim Rules on Corporate Rehabilitation.

6

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

While the current corporate rehabilitation rules are a marked

improvement over the antiquated Insolvency Law, certain gaps in the law have

prevented it from being a definitive corporate rescue vehicle.

II. THE FRIA

The Lower House approved House Bill (HB) 7090, its version of the

Financial Rehabilitation and Insolvency Act of 2010 (the “FRIA”), on 02

February 2010 or just before the end of its 14th Session6.

Off the bat, it would be accurate to conclude that the FRIA7 is not a simple

codification of the existing rules on corporate rehabilitation but a veritable

system overhaul. Broadly speaking, the FRIA integrates rehabilitation and

restructuring along with insolvency law. Furthermore, it moves from the debtor

controlled process of the older system to a framework where the creditors take

the fore in determining the future of the distressed corporation.

What follows below are some of the key features of the new FRIA

pertaining to rehabilitation of corporate debtors.

Meaning of “insolvent”

The old Insolvency Law of 1909 made a distinction between a debtor who

was “insolvent” and one which was solvent but “illiquid.” Given that prior to the

passage of the Securities Regulation Code (Republic Act 8799) the jurisdiction

over Petitions to Declare Suspension of Payments and/or for the appointment of

a Rehabilitation Receiver was given to the Securities and Exchange Commission

6 As of this writing, HB 7090 is to be consolidated with its counterpart

Senate Bill (SB) 61 and thereafter transmitted to the President for

approval.

7 The author uses FRIA and HB 2070 interchangeably as a practical

convention.

7

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

(SEC) while Petitions for Insolvency had to be heard by the Regional Trial Court

(RTC), some confusion resulted which eventually required some clarification by

the Supreme Court8.

On the other hand, both the 2000 Interim Rules on Corporate

Rehabilitation as well as the 2008 Rules on Corporate Rehabilitation made

rehabilitation available to any debtor “who foresees the impossibility of meeting

its debts when they respectively fall due.”

The FRIA avoids the trap entirely by providing for a broad definition of the

term “insolvent,” as follows:

“Section 4. Definition of Terms. – As used in this Act, the term:

xxx

“(p) Insolvent shall refer to the financial condition of a debtor that is generally unable to pay its or his liabilities as they fall due in the ordinary course of business or has liabilities that are greater than its or his assets.”

xxx

Three ways to rescue a corporation; Out-of-Court Rehabilitation

While the old rehabilitation regime did not expressly provide for

8 For instance, see Rubberworld v. NLRC, GR No. 126773.

See also: Union Bank v. Concepion, GR No. 160272 where the Supreme

Court declared that the SEC retained jurisdiction over a Petition for

the declaration of suspension of payments and rehabilitation even if

the debtor became insolvent during the course of the proceedings.

Finally, see Philippine National Bank v. CA [GR No. 165571, 20 January

2009] where one of the issues raised was whether or not a “technically

insolvent corporation” (i.e. one which foresees its inability to pay

its obligations for more than one year) can file a Petition for

Rehabilitation with the SEC despite not having filed a prior petition

for Suspension of Payments. The Supreme Court ruled that the SEC Rules

on Corporate Recovery allowed rehabilitation without “[r]equiring a

previous filing of a petition for suspension of payments.”

8

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

rehabilitation without court intervention, it did not specifically disallow it either.

Thus, a rehabilitation plan entered into by the debtor and its creditors partakes of

the nature of a contract and should not be invalidated simply on the ground that

it was done without court approval. Following the general rule however, non-

parties cannot be bound by the terms of the negotiated rehabilitation plan.

The FRIA takes it a step further by expressly providing rules to govern

extrajudicial rehabilitation. More specifically, there are three (3) processes to

resuscitate a financially distressed corporation under the FRIA, namely: (i) court

supervised rehabilitation, (ii) pre-negotiated rehabilitation and/or (iii) out-of-

court restructuring agreements. The choice largely depends on whether or not

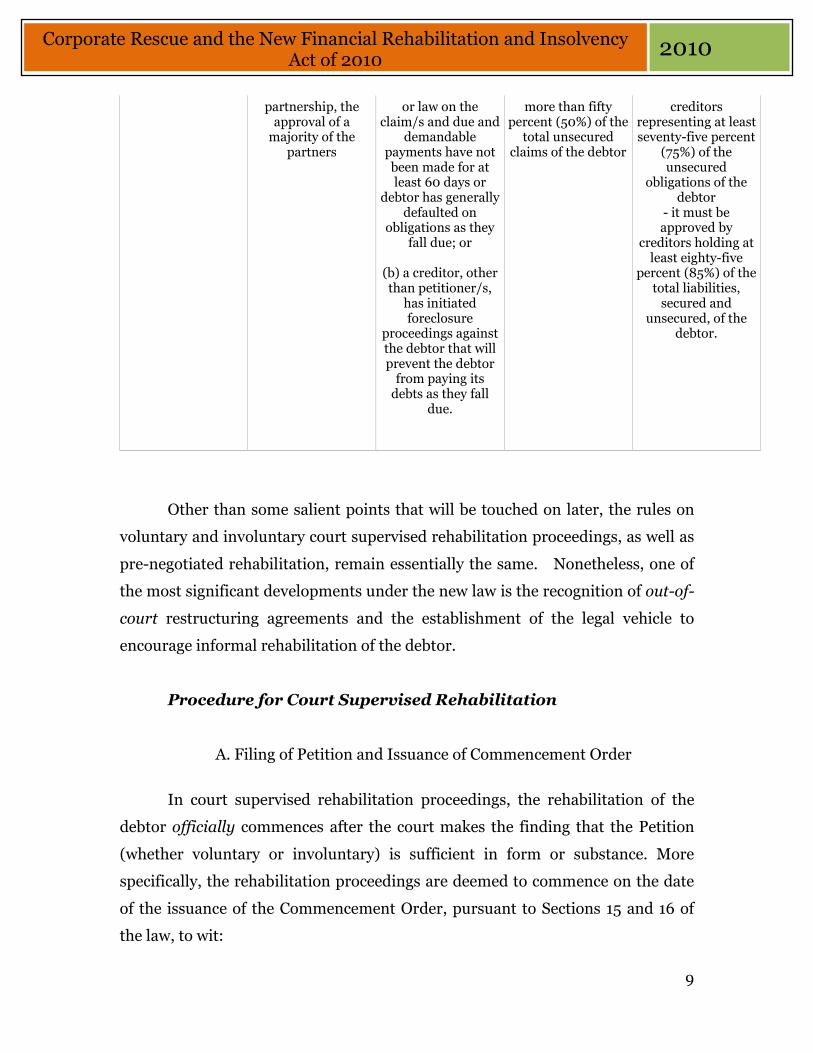

the initiating party can accumulate the necessary number of votes, to wit:

Voluntary Rehabilitation

(Debtor Initiated Court

Supervised)

Involuntary. Rehabilitation

(Creditor Initiated Court Supervised)

Pre-Negotiated Rehabilitation

Informal Rehabilitation

Provision

Section 12

Section 13

Section 76

Section 83

Petitioner

Debtor

Creditors

Debtor who may be joined by any of its

creditors

None

General

Conditions

- in case of a

corporation, by a majority vote of the board of directors or

trustees and authorized by a vote of the stockholders representing at least two-thirds (2/3) of the outstanding capital stock, or in case of a non-stock corporation, by the vote of at least two-thirds (2/3) of the

members - in case of a

- creditors must

have an aggregate claim

of PhP1,000,000.00 or at least 25 % of the subscribed

capital stock or partner's

contributions, whichever is

higher provided that:

(a) there is no

genuine issue of fact

- Pre-negotiated

Rehabilitation Plan which has been endorsed or approved by

creditors holding at least two-thirds (2/3) of the total liabilities of the debtor, including secured creditors holding more than fifty percent (50%) of the total secured claims of the debtor and unsecured creditors holding

- debtor must agree to the out-of-court

or informal restructuring/

workout agreement or Rehabilitation

Plan - it must be approved by creditors

representing at least sixty-seven percent (67%) of the secured obligations of the

debtor - it must be approved by

9

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

partnership, the approval of a majority of the

partners

or law on the claim/s and due and

demandable payments have not been made for at least 60 days or

debtor has generally defaulted on

obligations as they fall due; or

(b) a creditor, other than petitioner/s, has initiated foreclosure

proceedings against the debtor that will prevent the debtor from paying its debts as they fall

due.

more than fifty percent (50%) of the total unsecured

claims of the debtor

creditors representing at least seventy-five percent

(75%) of the unsecured

obligations of the debtor

- it must be approved by

creditors holding at least eighty-five

percent (85%) of the total liabilities, secured and

unsecured, of the debtor.

Other than some salient points that will be touched on later, the rules on

voluntary and involuntary court supervised rehabilitation proceedings, as well as

pre-negotiated rehabilitation, remain essentially the same. Nonetheless, one of

the most significant developments under the new law is the recognition of out-of-

court restructuring agreements and the establishment of the legal vehicle to

encourage informal rehabilitation of the debtor.

Procedure for Court Supervised Rehabilitation

A. Filing of Petition and Issuance of Commencement Order

In court supervised rehabilitation proceedings, the rehabilitation of the

debtor officially commences after the court makes the finding that the Petition

(whether voluntary or involuntary) is sufficient in form or substance. More

specifically, the rehabilitation proceedings are deemed to commence on the date

of the issuance of the Commencement Order, pursuant to Sections 15 and 16 of

the law, to wit:

10

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

“Section 15. Action on the Petition. – If the Court finds the petition for rehabilitation to be sufficient in form and substance, it shall, within five (5) working days from the filing of the petition, issue a Commencement Order. If within the same period, the court finds the petition deficient in form and substance, the court may, in its discretion, give the petitioner/s a reasonable time within which to amend or supplement the petition, or to submit such documents as may be necessary or proper to put the petition in proper order. In such case, the five (5) working days provided above for the issuance of the Commencement Order shall be reckoned from the date of the filing of the amended or supplemental petition or the submission of such documents.

Section 16. Commencement of Proceedings and Issuance of a Commencement Order. – The rehabilitation proceedings shall commence upon the issuance of the Commencement Order, which shall:

xxx

Under the same Section 16, the “Commencement Order” shall, among

others: (i) declare that the debtor is under rehabilitation9, (ii) direct publication

of the Order and notice to creditors10, (iii) appoint a rehabilitation receiver11, (iv)

set the date of the initial hearing for the determination of whether or not the

debtor can be rehabilitated12, (v) direct all creditors to file their claims at least

five (5) days from initial hearing13 and (vi) direct the government, through the

Bureau of Internal Revenue (BIR) to either file its Comment to the Petition for

Rehabilitation or present its claims against the debtor.

Suspension or Stay Order

9 Subparagraph (e)

10 Subparagraphs (f) and (g)

11 Subparagraph (h)

12 Subparagraph (m)

13 Subparagraph (i)

11

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

In addition, the Commencement Order shall include a Suspension or Stay

Order prohibiting the sale or disposition of assets of the debtor and ordering the

suspension of all actions against the debtor and/or the debtor’s estate. The

scope and/or coverage of the stay order under the FRIA remain as broad as

before. However, certain cases are allowed to proceed until the execution stage14.

These and other exceptions are enumerated in Section 18 of the law, to wit:

“Section 18. Exceptions to the Stay or Suspension Order. – The Stay or Suspension Order shall not apply:

“(a) to cases already pending appeal in the Supreme Court as of commencement date: Provided, That any final and executory judgment arising from such appeal shall be referred to the court for appropriate action;

“(b) subject to the discretion of the court, to cases pending or filed at a specialized court or quasi-judicial agency which, upon determination by the court, is capable of resolving the claim more quickly, fairly and efficiently than the court: Provided, That any final and executory judgment of such court or agency shall be referred to the court and shall be treated as a non-disputed claim;

“(c) to the enforcement of claims against sureties and other persons solidarily liable with the debtor, and third party or accommodation mortgagors as well as issuers of letters of credit, unless the property subject of the third party or accommodation mortgage is necessary for the rehabilitation of the debtor as determined by the court upon recommendation by the rehabilitation receiver;

“(d) to any form of action of customers or clients of a securities market participant to recover or otherwise claim moneys or securities entrusted to the latter in the ordinary course of the latter’s business as well as any action of such securities market participant or the appropriate regulatory agency or self-regulating organization to pay of settle such claims or liabilities;

“(e) to the actions of a licensed broker or dealer to sell pledged securities of a debtor pursuant to a securities pledge

14 In Philippine Airlines v. Court of Appeals [GR No. 150592, 20 January

2009], it was held that the stay order suspends the proceedings and not

just the enforcement of the claim. However, the 2008 Rules allow the

commencement of actions to prevent prescription of actions.

12

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

or margin agreement for the settlement of securities transactions in accordance with the provisions of the Securities Regulation Code and its implementing rules and regulations;

“(f) the clearing and settlement of financial transactions through the facilities of a clearing agency or similar entities duly authorized, registered and/or recognized by the appropriate regulatory agency like the Bangko Sentral ng Pilipinas (BSP) and the SEC as well as any form of actions of such agencies or entities to reimburse themselves for any transactions settled for the debtor; and

“(g) Any criminal action against the individual debtor or owner, partner, director or officer of a debtor shall not be affected by any proceeding commenced under this Act.”

Note that pursuant to sub-paragraph (c) above, the suspension order does

not cover the enforcement of claims against “persons solidarily liable with the

debtor” including “issuers of letters of credit.” This follows the rule in MWSS vs.

Daway [GR No. 160732, 21 June 2004] which held that a letter of credit is

excluded from the jurisdiction of the rehabilitation court, thus:

“Secondly, Sec. 6 (b) of Rule 4 of the Interim Rules does not enjoin the enforcement of all claims against guarantors and sureties, but only those claims against guarantors and sureties who are not solidarily liable with the debtor. Respondent Maynilad’s claim that the banks are not solidarily liable with the debtor does not find support in jurisprudence.

“We held in Feati Bank & Trust Company v. Court of Appeals that the concept of guarantee vis-à-vis the concept of an irrevocable letter of credit are inconsistent with each other. The guarantee theory destroys the independence of the bank’s responsibility from the contract upon which it was opened and the nature of both contracts is mutually in conflict with each other. In contracts of guarantee, the guarantor’s obligation is merely collateral and it arises only upon the default of the person primarily liable. On the other hand, in an irrevocable letter of credit, the bank undertakes a primary obligation. We have also defined a letter of credit as an engagement by a bank or other person made at the

13

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

request of a customer that the issuer shall honor drafts or other demands of payment upon compliance with the conditions specified in the credit.

“Letters of credit were developed for the purpose of insuring to a seller payment of a definite amount upon the presentation of documents and is thus a commitment by the issuer that the party in whose favor it is issued and who can collect upon it will have his credit against the applicant of the letter, duly paid in the amount specified in the letter. They are in effect absolute undertakings to pay the money advanced or the amount for which credit is given on the faith of the instrument. They are primary obligations and not accessory contracts and while they are security arrangements, they are not converted thereby into contracts of guaranty. What distinguishes letters of credit from other accessory contracts, is the engagement of the issuing bank to pay the seller once the draft and other required shipping documents are presented to it. They are definite undertakings to pay at sight once the documents stipulated therein are presented.

“Letters of Credits have long been and are still governed by the provisions of the Uniform Customs and Practice for Documentary Credits of the International Chamber of Commerce. In the 1993 Revision it provides in Art. 2 that “the expressions Documentary Credit(s) and Standby Letter(s) of Credit mean any arrangement, however made or described, whereby a bank acting at the request and on instructions of a customer or on its own behalf is to make payment against stipulated document(s)” and Art. 9 thereof defines the liability of the issuing banks on an irrevocable letter of credit as a “definite undertaking of the issuing bank, provided that the stipulated documents are presented to the nominated bank or the issuing bank and the terms and conditions of the Credit are complied with, to pay at sight if the Credit provides for sight payment.”

“We have accepted, in Feati Bank and Trust Company v. Court of Appeals and Bank of America NT & SA v. Court of Appeals, to the extent that they are pertinent, the application in our jurisdiction of the international credit regulatory set of rules known as the Uniform Customs and Practice for Documentary Credits (U.C.P) issued by the International Chamber of Commerce, which we said in Bank of the Philippine Islands v. Nery was justified under Art. 2 of the Code of Commerce, which states:

14

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

`Acts of commerce, whether those who execute them be merchants or not, and whether specified in this Code or not should be governed by the provisions contained in it; in their absence, by the usages of commerce generally observed in each place; and in the absence of both rules, by those of the civil law.’

“The prohibition under Sec 6 (b) of Rule 4 of the Interim Rules does not apply to herein petitioner as the prohibition is on the enforcement of claims against guarantors or sureties of the debtors whose obligations are not solidary with the debtor. The participating banks’ obligation are solidary with respondent Maynilad in that it is a primary, direct, definite and an absolute undertaking to pay and is not conditioned on the prior exhaustion of the debtor’s assets. These are the same characteristics of a surety or solidary obligor.

“Being solidary, the claims against them can be pursued separately from and independently of the rehabilitation case, as held in Traders Royal Bank v. Court of Appeals and reiterated in Philippine Blooming Mills, Inc. v. Court of Appeals, where we said that property of the surety cannot be taken into custody by the rehabilitation receiver (SEC) and said surety can be sued separately to enforce his liability as surety for the debts or obligations of the debtor. The debts or obligations for which a surety may be liable include future debts, an amount which may not be known at the time the surety is given.

“The terms of the Irrevocable Standby Letter of Credit do not show that the obligations of the banks are not solidary with those of respondent Maynilad. On the contrary, it is issued at the request of and for the account of Maynilad Water Services, Inc., in favor of the Metropolitan Waterworks and Sewerage System, as a bond for the full and prompt performance of the obligations by the concessionaire under the Concession Agreement and herein petitioner is authorized by the banks to draw on it by the simple act of delivering to the agent a written certification substantially in the form Annex “B” of the Letter of Credit. It provides further in Sec. 6, that for as long as the Standby Letter of Credit is valid and subsisting, the Banks shall honor any written Certification made by MWSS in accordance with Sec. 2, of the Standby Letter of Credit regardless of the date on which the event giving rise to such Written Certification arose.

15

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

“Taking into consideration our own rulings on the nature of letters of credit and the customs and usage developed over the years in the banking and commercial practice of letters of credit, we hold that except when a letter of credit specifically stipulates otherwise, the obligation of the banks issuing letters of credit are solidary with that of the person or entity requesting for its issuance, the same being a direct, primary, absolute and definite undertaking to pay the beneficiary upon the presentation of the set of documents required therein.

“The public respondent, therefore, exceeded his jurisdiction, in holding that he was competent to act on the obligation of the banks under the Letter of Credit under the argument that this was not a solidary obligation with that of the debtor. Being a solidary obligation, the letter of credit is excluded from the jurisdiction of the rehabilitation court and therefore in enjoining petitioner from proceeding against the Standby Letters of Credit to which it had a clear right under the law and the terms of said Standby Letter of Credit, public respondent acted in excess of his jurisdiction.”

On the other hand, the Stay or Suspension Order applies with equal force

to the enforcement of both secured and unsecured claims except that under

Section 60 of the FRIA, the issuance of the Stay or Suspension Order “shall not

be deemed in any way to diminish or impair the security or lien of a secured

creditor, or the value of his lien or security, except that his right to enforce said

security or lien may be suspended during the term of the Stay Order.” Again,

this paraphrases the “equality in equity” principle the effects of which were

explained in the case of Tsuneishi Heavy Industries (Cebu), Inc. v. Negros

Navigation Co., Inc. et. al. [GR 166845, 10 December 2008], thus:

“PD 902-A mandates that upon appointment of a management committee, rehabilitation receiver, board or body, all actions for claims against corporations, partnerships or associations under management or receivership pending before any court, tribunal, board or body shall be suspended. PD 902-A does not make any distinction as to what claims are covered by the suspension of actions for claims against corporations under

16

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

rehabilitation. No exception is made therein in favor of maritime claims. Thus, since the law does not make any exemptions or distinctions, neither should we. Ubi lex non distinguit nec nos distinguere debemos. “The justification for the suspension of actions or claims, without distinction, pending rehabilitation proceedings is to enable the management committee or rehabilitation receiver to effectively exercise its/his powers free from any judicial or extra-judicial interference that might unduly hinder or prevent the "rescue" of the debtor company. To allow such other actions to continue would only add to the burden of the management committee or rehabilitation receiver, whose time, effort and resources would be wasted in defending claims against the corporation instead of being directed toward its restructuring and rehabilitation. “It is undisputed that THI holds a preferred maritime lien over NNC’s assets by virtue of THI’s unpaid services. The issuance of the stay order by the rehabilitation court does not impair or in any way diminish THI’s preferred status as a creditor of NNC. The enforcement of its claim through court action was merely suspended to give way to the speedy and effective rehabilitation of the distressed shipping company. Upon termination of the rehabilitation proceedings or in the event of the bankruptcy and consequent dissolution of the company, THI can still enforce its preferred claim upon NNC. “PD 902-A was designed not only to salvage an ailing corporation but also to protect the interest of investors, creditors and the general public. Section 6 (d) of PD 902-A provides: "the management committee or rehabilitation receiver, board or body shall have the power to take custody of, and control over, all the existing assets and property of such entities under management; to evaluate the existing assets and liabilities, earnings and operations of such corporations, partnerships or other associations; to determine the best way to salvage and protect the interest of the investors and creditors; to study, review and evaluate the feasibility of continuing operations and restructure and rehabilitate such entities if determined to be feasible by the [court]. It shall report and be responsible to the [court] until dissolved by order of the [court]: Provided, however, That the [court] may, on the basis of the findings and recommendation of the management committee, or

17

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

rehabilitation receiver, board or body, or on its own findings, determine that the continuance in business of such corporation or entity would not be feasible or profitable nor work to the best interest of the stockholders, parties-litigants, creditors, or the general public, order the dissolution of such corporation entity and its remaining assets liquidated accordingly. The management committee or rehabilitation receiver, board or body may overrule or revoke the actions of the previous management and board of directors of the entity or entities under management notwithstanding any provision of law, articles of incorporation or by-laws to the contrary." “When a distressed company is placed under rehabilitation, the appointment of a management committee follows to avoid collusion between the previous management and creditors it might favor, to the prejudice of the other creditors. The stay order is effective on all creditors of the corporation without distinction, whether secured or unsecured. All assets of a corporation under rehabilitation receivership are held in trust for the equal benefit of all creditors to preclude one from obtaining an advantage or preference over another by the expediency of attachment, execution or otherwise. As between the creditors, the key phrase is equality in equity. Once the corporation threatened by bankruptcy is taken over by a receiver, all the creditors ought to stand on equal footing. Not any one of them should be paid ahead of the others. This is precisely the reason for suspending all pending claims against the corporation under receivership. “Rizal Commercial Banking Corporation v. Intermediate Appellate Court [GR No. 74851, 9 December 1999], promulgated by the Court en banc before the effectivity of the Interim Rules on Corporate Rehabilitation, is still valid case law up to the present. It enumerates the guidelines in the treatment of claims involving corporations undergoing rehabilitation, viz.: “1. All claims against corporations, partnerships, or

associations that are pending before any court, tribunal, or board, without distinction as to whether or not a creditor is secured or unsecured, shall be suspended effective upon the appointment of a management committee, rehabilitation receiver, board, or body in accordance with the provisions of Presidential Decree No. 902-A.

18

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

“2. Secured creditors retain their preference over

unsecured creditors, but enforcement of such preference is equally suspended upon the appointment of a management committee, rehabilitation receiver, board, or body.

“In the event that the assets of the corporation, partnership, or association are finally liquidated, however, secured and preferred credits under the applicable provisions of the Civil Code will definitely have preference over unsecured ones.”

B. Other effects of Commencement

Continuous Supply of Goods and Services

To ensure continuous delivery of goods and services necessary for the

debtor’s business, the FRIA adopts the provision under the 2008 Rules granting

the rehabilitation court authority to include in the Commencement Order a

prohibition enjoining the debtor’s suppliers from withholding supply of essential

goods and services15, to wit:

“Section 16. Commencement of Proceedings and Issuance of a Commencement Order. – The rehabilitation proceedings shall commence upon the issuance of the Commencement Order, which shall:

xxx

“(k) prohibit the debtor’s suppliers of goods or services from withholding the supply of goods and services

15 Presumably, the authority of the court under this section applies

only to valid and subsisting contracts for continuous supply of goods

or services, as opposed to supply contracts on a per order basis. In

other words, it would be one thing to require the supplier to fulfill

the terms of an existing supply contract by continuing to supply the

debtor. It would be a different matter to compel the supplier to

continue supplying the debtor where each order is covered by a separate

contract as this would be tantamount to requiring the supplier to

contract with the debtor.

19

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

in the ordinary course of business for as long as the debtor makes payments for the services or goods supplied after the issuance of the commencement order;”

xxx

[Italics ours]

Waiver of Taxes

Section 19 of the law provides that from the time of the issuance of the

Commencement Order until the approval of the Rehabilitation Plan or dismissal

of the petition, the imposition of all taxes shall be waived, thus:

“Section 19. Waiver of Taxes and Fees Due to the National Government and to Local Government Units. – Upon issuance of the Commencement Order by the court, and until the approval of the Rehabilitation Plan or dismissal of the Petition, which is earlier, the imposition of all taxes and fees, including penalties interests and charges thereof, due to the national government or to LGUs shall be considered waived, in furtherance of the objectives of rehabilitation.”

C. Duration of the Commencement Order and Modification of the Suspension Order

The Commencement Order shall be effective for the entire duration of the

rehabilitation proceedings and “for as long as there is a substantial likelihood

that the debtor will be successfully rehabilitated16.” The determination of this

fact will be based primarily on a report (by the Rehabilitation Receiver] either

that the Rehabilitation Plan is “realistic, feasible and reasonable” or even if the

Rehabilitation Plan is not feasible, there still exists “a substantial likelihood for

the debtor to be rehabilitated.”

16 Section 21

20

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

As in the old Rules, the FRIA allows the court to modify the terms of the

suspension order or relieve a claim from its coverage if a creditor does not have

adequate protection over the security, thus:

“Section 61. Lack of Adequate Protection. – The court, on motion or motu proprio, may terminate, modify or set conditions for the continuance of suspension of payment, or relieve a claim from the coverage thereof, upon showing that: (a) a creditor does not have adequate protection over property securing its claim; or (b) the value of a claim secured by a lien on property which is not necessary for the rehabilitation of the debtor exceeds the fair market value of the said property.

“For purposes of this section, a creditor shall be deemed to lack adequate protection if it can be shown that:

“(a) the debtor fails or refuses to honor a pre-existing agreement with the creditor to keep the property insured;

“(b) the debtor fails or refuses to take commercially reasonable steps to maintain the property;

“(c) the property has depreciated to an extent that the creditor is under secured.

“Upon showing of lack of protection, the court shall order the debtor or rehabilitation receiver to make arrangements to provide for the insurance or maintenance of the property; or to make payments or otherwise provide additional or replacement security such that the obligation is fully secured. If such arrangements are not feasible, the court may modify the Stay Order to allow the secured creditor lacking adequate protection to enforce its security claim against the debtor: Provided, however, That the court may deny the creditor the remedies in this paragraph if the property subject of the enforcement is required for the rehabilitation of the debtor.”

D. Use, Treatment and Disposition of Assets

As a general rule, funds or property of the debtor cannot be used except in

the ordinary course of business or unless necessary to pay off the administrative

21

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

expenses during the rehabilitation proceedings17. These include court-approved

pre-commencement loans, as discussed above18 and compensation of employees

necessary to carry on the debtor’s business19.

Nonetheless, the court may, upon application by the rehabilitation

receiver, allow the disposition of the debtors’ encumbered property subject to the

general requirement that the disposition is necessary for the continued operation

of the business. However, the debtor must make an arrangement with the

secured creditor for a substitute lien20. This applies to the sale of property

covered by a trust receipt or consignment agreement, in which case the law

provides that the disposition shall “not give rise to any criminal liability under

applicable laws.”

E. Treatment of Contracts

Confirmation of Cancellation of Existing Contracts

Likewise, the issuance of the Commencement Order marks the start of a

cleanup period which requires the debtor and the rehabilitation receiver to chop

out those contractual commitments which are not necessary for the continued

existence of the business and/or the rehabilitation of the debtor.

Section 57 of the law grants the debtor the power to confirm or cancel

pre-existing contracts within ninety (90) days from the issuance of the

Commencement Order in order to weed out extremely onerous contracts that

may have been the cause of the debtor’s predicament. Those not confirmed

17 Section 48

18 Section 55

19 Section 56

20 Section 50.

22

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

expressly by the debtor shall be deemed terminated but the party whose contract

is not confirmed will be allowed to pursue a claim for damages on account of the

debtor’s election, which claim shall be considered a demand existing prior to the

filing of the Petition for Rehabilitation, to wit:

“Section 57. Treatment of Contracts. – Unless cancelled by virtue of a final judgment of a court of competent jurisdiction issued prior to the issuance of the Commencement Order, or at anytime thereafter by the court before which the rehabilitation proceedings are pending, all valid and subsisting contracts of the debtor with creditors and other third parties as at the commencement date shall continue in force: Provided, That within ninety (90) days following the commencement of proceedings, the debtor, with the consent of the rehabilitation receiver, shall notify each contractual counterparty of whether it is confirming the particular contract. Contractual obligations arising or performed during this period, and afterwards for confirmed contracts, shall be considered administrative expenses. Contracts not confirmed within the required deadline shall be considered terminated. Claims for actual damages, if any, arising as a result of the election to terminate a contract shall be considered a pre-commencement claim against the debtor. Nothing contained herein shall prevent the cancellation or termination of any contract of the debtor for any ground provided by law.

New Money

Stay Order notwithstanding, the FRIA allows the debtor to incur post-

commencement loans and/or other obligations subject to the approval of the

court21. This has a similar import as the “New Money” clause under the 2008

Rules. Debt payments falling under this provision will be considered as

administrative expenses during the pendency of the proceedings.

F. The Rehabilitation Receiver

21 Section 55

23

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

The initial appointment of the Rehabilitation Receiver (as one of the

elements of the Commencement Order under Section 16) is subject to the

discretion of the court, which may retain the original appointee or choose another

from the petitioners’ nominees. However, this discretion is limited in the

following circumstances:

(a) In case the debtor is a securities market participant, in which case the

court shall give priority to the nominee of the appropriate securities or

investor protection fund; or

(b) If the qualified natural or juridical person is nominated by more than

50% of secured creditors and general unsecured creditors, in which case

the court “shall appoint the creditors’ nominee22.”

As a rule, the Rehabilitation Receiver will not supplant the existing

management of the debtor corporation unless otherwise ordered by the court on

motion of any interested party, thus:

“Section 36. Displacement of Existing Management by the Rehabilitation Receiver or Management Committee. -- Upon motion of any interested party, the court may appoint and direct the rehabilitation receiver to assume the powers of management of the debtor, or appoint a management committee that will undertake the management of the debtor, upon clear and convincing evidence of any of the following circumstances:

“(a) Actual or imminent danger of dissipation, loss, wastage or destruction of the debtor’s assets or other properties;

“(b) Paralyzation of the business operations of the debtor; or

22 Section 30

24

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

“(c) Gross mismanagement of the debtor, or fraud or other wrongful conduct on the part of, or gross or willful violation of this Act by, existing management of the debtor or the owner, partner, director, officer or representative/s in management of the debtor.

“In case the court appoints the rehabilitation receiver to assume the powers of management of the debtor, the court may:

“(1) require the rehabilitation receiver to post an additional bond;

“(2) authorize him to engage the services or employ persons or entities to assist him in the discharge of his managerial functions; and

“(3) authorize a commensurate increase in his compensation.”

F. Actions by the Rehabilitation Receiver

As part of its functions, the Rehabilitation Receiver retains the authority to

file an action to annul certain pre-commencement transactions intended to

defraud the creditors. Indeed, this power can be traced back to the basic

authority of the receiver to undertake measures to preserve property under

receivership under the Rules of Court23.

Should the receiver refuse to institute proceedings, any creditor may take

up the cudgels of the corporation with leave of court. If successful, Section 59 of

the law provides that the fruits of the case will redound to the pro-active creditor

to the extent of the value of its credit plus costs, thus:

“Section 59. Actions for Rescission or Nullity. – (a) The rehabilitation receiver or, with his conformity, any creditor may initiate and prosecute any action to rescind, or declare null and void any transaction described in Section 58 hereof. If the rehabilitation receiver does not consent to the

23 Salientes v. IAC [GR 66211, 4 July 1995]

25

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

filing or the prosecution of such action, any creditor may seek leave of the court to commence said action.

“(b) If leave of court is granted under subsection (a), the rehabilitation receiver shall assign and transfer to the creditor all rights, title and interest in the chose in action or subject matter of the proceeding, including any document in support thereof;

“(c) Any benefit derived from a proceeding taken pursuant to subsection (a), to the extent of his claim and the costs, belongs exclusively to the creditor instituting the proceeding, and the surplus, if any, belongs to the estate.

“(d) Where before an order is made under subsection (a), the rehabilitation receiver (or liquidator) signifies to the court his readiness to institute the proceeding for the benefit of the creditors, the order shall fix the time within which he shall do so and, in that case, the benefit derived from the proceeding, if instituted within the time limits so fixed, belongs to the estate.”

H. Administration of Proceedings

Within forty (40) days from the issuance of the Commencement Order, the

court shall set the case for Initial Hearing to determine whether or not there is

substantial likelihood that the debtor can be rehabilitated and undertake the

following:

(a) determine the creditors who have made timely and proper filing

of their notice of claims;

(b) hear and determine any objection to the qualifications or the

appointment of the rehabilitation receiver and if necessary, appoint a new

one;

(c) direct the creditor to comment on the petition and the

Rehabilitation Plan, and to submit the same to the court and to the

rehabilitation receiver within a period not exceeding twenty (20) days;

(d) direct the rehabilitation receiver to evaluate the financial

condition of the debtor and to prepare and submit his report to the court24.

24 Section 22

26

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

Within forty (40) days from the Initial Hearing, the Rehabilitation

Receiver is required to submit his written Report to the court, which will include

a determination of (a) whether or not there is substantial likelihood for the

debtor to be successfully rehabilitated or in the alternative (b) whether the

debtor should be dissolved or liquidated25. After submission of report, the Court

shall act on the petition by: (i) giving due course to the petition, (ii) dismissing

the petition or (iii) converting the proceedings into one for liquidation26.

In the event the court gives due course to the petition, the court will

require the Rehabilitation Receiver to review the Rehabilitation Plan, taking into

consideration the views of the debtor and all creditor classes. While the

consultation is a necessary procedure, the Receiver is not bound by the objections

of the parties27.

Among others, Section 62 of the FRIA provides that Rehabilitation Plan

must include provisions establishing classes and subclasses of voting creditors28.

After identifying the appropriate creditor classes and sub-classes, the Plan must

“specify the treatment of each class or subclass29” and “provide for equal

treatment for all claims within the same class30.” Similar to the 2008 Rules,

Section 62 grants additional protection to secured creditors by requiring the Plan

to “maintain the security interest of secured creditors and preserve the

liquidation value of the security.”

25 Section 24

26 Section 25

27 Section 63

28 Sub-paragraph (d) and (e)

29 Sub-paragraph (g)

30 Sub-paragraph (h)

27

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

Once satisfied with the version of the Rehabilitation Plan, the receiver

must convene the creditors and present the plan to them for approval. Unlike the

old procedure however31, the vote of the debtor is not required for the approval of

the plan, thus:

“Section 64. Creditor Approval of the Rehabilitation Plan. – The rehabilitation receiver shall notify the creditors and stakeholders that the Plan is ready for their examination. Within twenty (20) days from the said notification, the rehabilitation receiver shall convene the creditors, either as a whole or per class, for purposes of voting on the approval of the Plan. The Plan shall be deemed rejected unless approved by all classes of creditors whose rights are adversely modified or affected by the Plan. For purposes of this section, the Plan is deemed to have been approved by a class of creditors if members of the said class holding more than fifty per cent (50%) of the total claims of the said class vote in favor of the Plan. The votes of the creditors shall be based solely on the amount of their respective claims based on the registry of claims submitted by the rehabilitation receiver pursuant to Section 44 hereof.

Notwithstanding the rejection of the Rehabilitation Plan, the court may confirm the Rehabilitation Plan if all of the following circumstances are present:

“(a) the Rehabilitation Plan complies with all the requirements specified in this Act;

“(b) the rehabilitation receiver recommends the confirmation of the Rehabilitation Plan;

“(c) The shareholders, owners or partners of the juridical debtor lose at least their controlling interest as a result of the Rehabilitation Plan; and

“(d) The Rehabilitation Plan would likely provide the objecting class of creditors with compensation which has a net present value greater than that which they would have received if the debtor were under liquidation.”

31 See Section 8 of the Rules of Procedure on Corporate Rehabilitation

(2008)

28

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

Note that under the foregoing provision, separate arrangements can be

made with different classes of creditors subject to approval of 50% of the affected

creditors or 80% of all creditors. This grants flexibility in dealing with varying

needs of each class32.

Even if the Rehabilitation Plan is not approved by the creditors, the court

may still confirm the Plan if it can be shown that objecting class of creditors shall

receive a “net present value greater than that they would have received if the

debtor were under liquidation.” Under the Interim Rules, the debtor can force

court approval of a Rehabilitation Plan over the objection of creditors by merely

showing that “[t]he plan would likely provide the objecting class of creditors with

compensation greater than that which they would have received if the assets of

the debtor were sold by a liquidator within a three-month period.” The 2008

Rules33 changed the basis to “present value projected in the plan”. Requiring

that the computation be based on “net present value” is intended to prevent

debtors from railroading a rehabilitation plan disadvantageous to the creditors by

the simple expedient of stretching the repayment schedule without regard to the

costs of borrowing.

Finally, creditors who take a haircut under the plan will not be taxed for

any amount of debt which is reduced or forgiven under Section 71 of the law.

H. Termination

After creditor approval of the Rehabilitation Plan as provided above, it

must be submitted to the court for confirmation. Creditors shall have the right to

make an Objection but on limited grounds, to wit:

(a) The creditors’ support was induced by fraud;

32 See also Section 42 on the formation of Creditors’ Committee.

33 Specifically, Rule IV, Section 11

29

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

(b) The documents or data relied upon in the Rehabilitation Plan are

materially false or misleading; or

(c) The Rehabilitation Plan is in fact not supported by the voting

creditors34

If, upon due hearing, the court finds merit in the objection, it may order

the receiver or the debtor to cure the defect whenever possible. On the other

hand, it shall order the proceedings to be turned into liquidation if the debtor

acted in bad faith or if the defect is incurable35.

However, in case (a) there are no objections to the Rehabilitation Plan, (b)

the objections are found to be without merit or (c) any defect in the

Rehabilitation Plan has been cured; the court shall issue an order confirming the

plan even over and above the objections of the owners, partners or stockholders

of the insolvent debtor36

To prevent the debtor (or any interested party) from dragging out the

proceedings in the hopes of obtaining a settlement on the basis of attrition, the

law fixes a maximum period of one year (from the time of the filing of the

petition) within which the plan must be confirmed. Otherwise, the proceedings

will turn into one of liquidation. This should force the parties to negotiate in

earnest.

Pre-Negotiated Rehabilitation

The concept of a pre-negotiated rehabilitation was introduced and is

currently available under the 2008 Rules, which the FRIA adopts without

substantial modification. Thus, the debtor, by itself or jointly with the creditors,

34 Section 66

35 Section 67

36 Section 68

30

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

may file a petition for the approval of a pre-negotiated rehabilitation plan

provided that it has been endorsed by creditors holding at least 2/3 of the total

liabilities of the debtor, including secured creditors holding more than 50 percent

of the total secured claims and unsecured creditors holding more than 50 percent

of the total unsecured claims. However, while the 2008 Rules mandated the

appointment of a Rehabilitation Receiver either by election of the parties or by

order of the court, the FRIA gives the parties the freedom to undertake the

proceedings without a receiver.

The Order under Section 77 of the law which directs interested parties to

file their objections to the Pre-Negotiated Rehabilitation Plan also requires

publication and personal delivery of a copy of the Petition to each creditor who is

not a petitioner but who holds at least 10%37 of the total liabilities of the debtor.

The FRIA enumerates grounds to object to the Rehabilitation Plan in

addition to those originally provided under the 2008 Rules. Thus, under Section

79:

“Section 79. Objection to the Petition or Rehabilitation Plan. – Any creditor or other interested party may submit to the court a verified objection to the petition or the Rehabilitation Plan not later than eight (8) days from the date of the second publication of the Order mentioned in Section 77 hereof. The objection shall be limited to the following:

“(a) The allegations in the petition or the Rehabilitation Plan, or the attachments thereto are materially false or misleading;

“(b) The majority of any class of the creditors do not in fact support the Rehabilitation Plan;

“(c) The Rehabilitation Plan fails to accurately account for a claim against the debtor and the claim is not categorically declared as a contested claim; or

“(d) The support of the creditors, or any of them, was

37 5% under the 2008 Rules.

31

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

induced by fraud.

“Copies of the objection to the petition or the Rehabilitation Plan shall be served on the debtor, the rehabilitation receiver (if applicable), the secured creditor with the largest claim and who supports the Rehabilitation Plan, and the unsecured creditor with the largest claim and who supports the Rehabilitation Plan.”

If, after due hearing, the courts finds merit to the objection, it will order

the debtor to cure the defect. On the other hand, if it finds that the petitioners

acted in bad faith or that the defect is incurable, it may order the conversion of

proceedings into one for liquidation38. As in the 2008 Rules, the Rehabilitation

Plan will be deemed approved if the court fails to act within a period of 120

days39.

Informal Rehabilitation

As mentioned previously, one of the most important and potentially far

reaching innovations under the FRIA is the recognition of out-of-court

restructuring/workout agreements. Pursuant to Section 89 of the Act, “[t]he

insolvent debtor and creditor may seek court assistance for the execution or

implementation” of the Rehabilitation Plan, provided that it meets the minimum

requirements of the law. Ultimately, this type of cooperative endeavor may offer

the best chances of rehabilitation as it theoretically provides the least amount of

disruption to the operations of an already beleaguered company.

Furthermore, to allow the parties to negotiate a feasible workout plan, the

debtor and creditors holding more than 50% of the debt may agree on a standstill

period pending the completion of the plan for up to 120 days40, provided in

38 Section 80.

39 Section 81.

40 Section 85

32

Corporate Rescue and the New Financial Rehabilitation and Insolvency Act of 2010

2010

addition that notice to all creditors is published in a newspaper of general

circulation once a week for two consecutive weeks. The said notice must invite

the creditors to participate in the negotiation of the plan and inform them that

the plan will be binding on all creditors if the required votes are obtained41.

An out-of-court Rehabilitation Plan approved by at least 67% of secured

creditors, 75% of unsecured creditors, and 85% of all creditors42 will be

“crammed down” all creditors pursuant to Section 86 of the law, to wit:

“Section 86. Cram Down Effect. – A restructuring/workout agreement or Rehabilitation Plan that is approved pursuant to an informal workout framework referred to in this chapter shall have the same legal effect as confirmation of a Plan under Section 69 hereof. The notice of the Rehabilitation Plan or restructuring agreement or Plan shall be published once a week for at least three (3) consecutive weeks in a newspaper of general circulation in the Philippines. The Rehabilitation Plan or restructuring agreement shall take effect upon the lapse of fifteen (15) days from the date of the last publication of the notice thereof.”

Quick Notes on Insolvency and Liquidation: Cross Border Insolvency

By virtue of Section 139 of the FRIA, the Philippines is now deemed to

adopt the provisions of the UNCITRAL Model Law on Cross Border Insolvency

(1997) subject to procedural rules to be promulgated by the Supreme Court.

Essentially, the law provides a framework for the recognition of foreign

insolvency proceedings and grants certain parties in such proceedings access to

Philippine courts for purposes of obtaining some form of affirmative or other

relief.

41 Ibid.

42 Section 84