Corporate Presentation Second Quarter Results...

19

Second Quarter Results 2014 Corporate Presentation

Transcript of Corporate Presentation Second Quarter Results...

Second QuarterResults 2014

Corporate Presentation

The information contained herein has been prepared by Cencosud S.A. (“Cencosud”) solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities and should not be treated as giving investment or other advice. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein. Any opinions expressed in this presentation are subject to change without notice and Cencosud is under no obligation to update or keep current the information contained herein. The information contained herein does not purport to be complete and is qualified in its entirety by reference to more detailed information included in the preliminary offering memorandum. Cencosud and its respective affiliates, agents, directors, partners and employees accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this material.

This presentation may contain statements that are forward‐looking subject to risks and uncertainties and factors, which are based on current expectations and projections about future events and trends that may affect Cencosud’s business. You are cautioned that any such forward‐looking statements are not guarantees of future performance. Several factors may adversely affect the estimates and assumptions on which these forward‐looking statements are based, many of which are beyond our control.

2Second Quarter www.cencosud.com

3www.cencosud.com

2Q14

Highlights

•Cencosud Announces Deal with Scotiabank for Financial Services in Chile

• Positive Supermarket SSS Trends Boosted by the Easter Week Effect & Promotions

• SG&A Margin Improvements Despite Macro Headwinds

•5 Net Openings in the Quarter to Total 1,101 Stores & 48 Shopping Centers

•Adjusted EBITDA Grew 1.7% YoY, Adjusted EBITDA Margin Decreased to 6.1%

•Net Profit Increased 196.2% YoY

Second Quarter

4www.cencosud.com

Revenue by Country (CLP mm)Revenue Evolution (CLP mm)

• Revenue gains in all Business Units, Positive SSS in SupermarketsPushed Revenue up 6% in the Division.

• Negative World Cup Effect in Brazil

• Devaluation of 27.8% of the ARS Curbed Further Revenue Gains

• Positive SSS in Department Stores Despite slower discretionaryspending

Second Quarter

www.cencosud.com 5

EBITDA & SG&A

Performan

ce

•Home Improvement EBITDA Jumped 56.1% After Better Results in all Markets

•Home Improvement Proved Successful SG&A Control in Chile & Argentina

• Supermarkets Posted Adj. EBITDA Growth in all Markets but Brazil

• Brazil Operations Posted a One‐off Labor Related Provision Related Tied to Litigation Against the Govt. of Brazil of CLP 7,264 million

•Excluding the Brazil Labor Related Provision, SG&A Margin Decreased from 24.1% to 23.7% in 2Q14

•Peru Supermarkets SG&A Expanded Only 1% Following Expense Control Initiatives

Second Quarter

6www.cencosud.com

EBITDA by Country (CLP mm)Adjusted EBITDA Evolution (CLP mm)

• Adjusted EBITDA growth was driven by Home Improvement,Shopping Centers & Financial Services

• Peru supermarkets posted higher results on SG&A control, revenuegrowth

• All supermarket operations posted positive EBITDA expansionexcept Brazil

• Labor related provision of CLP 7,264 million negatively impactedAdj. EBITDA

Second Quarter

77Second Quarter

SupermarketsRevenue evolution (CLP mm) Adjusted EBITDA evolution (CLP mm)SSS evolution by country in local currency

8www.cencosud.com

• Revenue was boosted by higher revenues in Chile, Brazil and Colombia & Peru.

• Easter effect provided a boost for revenue & SSS

• 31 net openings in the region since 2Q13

• Continued sequential narrowing of negative SSS in Colombia

• Brazil posted a weak EBITDA generation due to operational issuesat Prezunic and one‐off provision

• Excluding Brazilian operations Adj. EBITDA in the supermarketdivision jumped 29% while posting margin improvement of 115bps to 6.4%.

Second Quarter

Revenue evolution (CLP mm) Adjusted EBITDA evolution (CLP mm)SSS evolution by country in local currency

9

Home Improvement

www.cencosud.com

• Stronger sales across all markets

• ARS depreciation curbed revenue expansion for Argentine operations

• Colombia revenues jumped 53% on the back of 4 new stores

• Argentina was the highlight of the operation withSG&A expanding only 0.3% on the back of maturinginitiatives in logistics and efficiencies.

• SG&A in Chile continued to dilute with marginnarrowing to 20.5%

Second Quarter

Revenue evolution (CLP mm) Adjusted EBITDA evolution (CLP mm)

11

Shopping Centers

www.cencosud.com

• Revenue expansion in the division was curbed by an 8.3% decrease in revenues fromArgentina

• Sales at Portal Ñuñoa in Chile were affected by the opening of a competingdevelopment.

• Chile posted a significant SG&A drop as a result of a reclassification of expenses to the“Others” segment.

• Lower SG&A over sales in Chile and Peru fueled better Adj. EBITDA performance, alsoboosted by an improved performance in our development in the city of Arequipa.

Second Quarter

• On September 4th the company received authorization forthe opening of 15,000 m2 of GLA at its Costanera Centeroffice tower project.

• Cencosud will begin the process of leasing out office spaceat the tower.

12

Financial Services

www.cencosud.com

• Portfolio expansion in the period pushed revenue upward.

• EBITDA growth was pushed downward by lower operating income in Chile as a result of costs associated with the launch of Cencosud´s newopen credit card.

• Risk stemming from our Peruvian portfolio is lower due to a more mature portfolio

Second Quarter

7,3%

Banco ParisCAT

CLP PENARS

Revenue evolution (CLP mm) Adjusted EBITDA evolution (CLP mm)2014 SSS evolution in local currency

10

Department Store

www.cencosud.com

• Paris Peru stores boosted revenue with theopening of 3 new locations since 2Q13

• Chile posted SSS of 3.4% with higher trafficcoming from Paris promotional events and moremoderate SSS at Johnson

Second Quarter

• EBITDA generation dropped as a consequence ofmore promotional activities & product mix inChile in combination with higher losses fromPeru

• SG&A over sales improved further to 25.3% from25.4% in 1Q13

13

Financial Ratios

www.cencosud.com

Net debt evolution (US$ bn) Net leverage (net debt/EBITDA)

Breakdown by Issuer Breakdown by Currency(after CCS)

Breakdown by Rate(after CCS)

Second Quarter

14

Amortization Schedule

www.cencosud.com

• This chart incorporates debt amortizations as of 2Q14.

• This chart does not incorporate any pay down of debt with funds to be received from the announced JV in financial services in Chile

FIN

AN

CIA

L D

EBT

USD

MM

Second Quarter

16

Financial Services

Update

www.cencosud.comSecond Quarter 15

Corporate Presentation www.cencosud.com 16

Announcement Bondholder Approval-

Bank WaiversClosing

Around 90 days

June 30th Sept 4th 4Q14

Reception of Regulator approval

Timeline for Closing

Request For SBIF* Approval

Aug 13th

• *: SBIF stands for “Superintendencia de Bancos e Instituiciones Financieras”. This is a Chilean government agencycharged with the supervising of commercial banks and other financial institutions, safeguard depositors and or creditorsand the public interest.

17

Bondholder Meeting

www.cencosud.comSecond Quarter

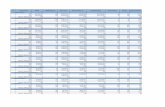

Issuance Series Currency Issued Amount (000's)

MaturityYears

Outstanding Amount(000's)

Rate at Issuance Last Yield Spread Duration Rating Callable

since

443 A U.F. 4.000 21 4.000 4,25% 4,02% 2,25% 6,31 AA- 2011443 C U.F. 4.500 21 4.500 4,10% 4,09% 2,30% 8,17 AA- 2011443 D U.F. 1.500 21 1.500 4,00% 4,00% 2,02% 8,86 AA- 2012530 E U.F. 6.500 20 2.000 3,50% 3,00% 1,33% 3,64 AA- 2013530 F U.F. 6.500 10 4.500 4,00% 3,98% 1,81% 10,76 AA- 2013

• The company secured approval from bondholders of issuance 530 on September 4th bondholder meeting

• Issuance 443 is callable at par and the company is at this time assessing whether to call a second meeting or to call the issuance

18

Conclusion

www.cencosud.com

• Strong performance in Chile / Peru / Argentina in 1H14

• These markets represented around 70% of our revenue in the period• SSS accelerated in Supermarkets • SG&A delivers 8.6% adj. EBITDA growth in 1H14• EBITDA margins expanding

• Colombia

• Colombian operations on track• Favorable macro environment pushing consumption• Expecting break‐even in SSS in 3Q14• Traction with loyalty program & private labels

• Brazil• Navigating challenges in Brazil following SAP implementation• Clear strategy in place to handle turn around with focus on inventory management • SSS comparisons specially hurt by Prezunic performance

Second Quarter

19