Corporate Presentation - November 2012 - Newswireextras.newswire.ca/sepac/Nov2012/Hyperion Corporate...

15

Corporate Presentation - November 2012 www.hyperionexploration.com TSX-V: HYX

Transcript of Corporate Presentation - November 2012 - Newswireextras.newswire.ca/sepac/Nov2012/Hyperion Corporate...

Corporate Presentation - November 2012

www.hyperionexploration.com

TSX-V: HYX

Forward Looking Statements

2

This document may include forward-looking statements including opinions, assumptions, estimates and expectations of future production, cash flow and earnings. When used in this document, the words "anticipate," "believe," "estimate," "expect," "intend," "may," "project," "plan", "will", "should" and similar expressions are intended to be among the statements that identify forward-looking statements. Forward-looking statements are subject to a wide range of risks and uncertainties, and although the Company believes that the expectations represented by such forward-looking statements are reasonable, there can be no assurance that such expectations will be realized. Any number of important factors could cause actual results to differ materially from those in the forward-looking statements including, but not limited to, the volatility of oil and gas prices, the ability to implement corporate strategies, the state of domestic capital markets, the ability to obtain financing, changes in oil and gas acquisition and drilling programs, operating risks, production rates, reserve estimates, changes in general economic conditions and other factors more fully described from time to time in the reports and filings made by the Company with securities regulatory authorities. BOEs may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Niton /McLeod, AB

Pembina, AB

Buck Lake, AB

Garrington, AB

Focused Resource Player

3

Land Summary Acres

Net Land ~ 80,000

Net Undeveloped Land ~ 66,000

Net Undeveloped Cardium Land (including Farm In Land)

~ 37,000

Background:

Started in July 2010 with a recapitalization of a public shell

Early focus: acquisitions, gaining scale and resource drilling repeatability in Cardium light oil

Current focus: share price appreciation through cash flow, production and reserves per share growth.

Strategy:

Acquire and exploit underdeveloped light oil resource plays which lead to lower risk, scalable and repeatable development projects.

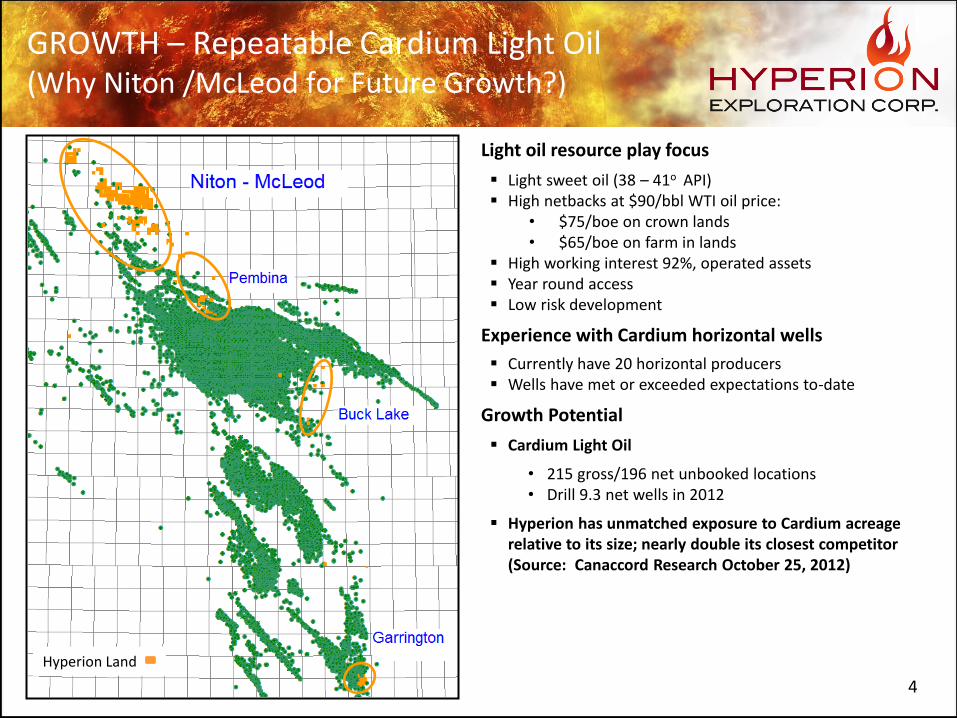

Light oil resource play focus

Light sweet oil (38 – 41o API) High netbacks at $90/bbl WTI oil price:

• $75/boe on crown lands • $65/boe on farm in lands

High working interest 92%, operated assets Year round access Low risk development

Experience with Cardium horizontal wells

Currently have 20 horizontal producers Wells have met or exceeded expectations to-date

Growth Potential

Cardium Light Oil

• 215 gross/196 net unbooked locations • Drill 9.3 net wells in 2012

Hyperion has unmatched exposure to Cardium acreage relative to its size; nearly double its closest competitor (Source: Canaccord Research October 25, 2012)

GROWTH – Repeatable Cardium Light Oil (Why Niton /McLeod for Future Growth?)

4

Hyperion Land

VALUE - Net Asset Value Build Up

5

NAV Build-Up – Pro Forma September, 2012

$1.25 $1.74

• $0.95/share base producing NAV Includes no booked or unbooked locations, net of debt.

• $1.10/share base 2P NAV

Includes only booked locations intended to be drilled within 2012 timeframe, net of debt.

2011 Year End McDaniel Reserve Summary: Proved Plus Probable Reserve Value (BT NPV 10%) …$76.0 million Proved Plus Probable Reserve …………………….……………5.5 MMboe (56 % Oil + NGL’s)

$4.75+/share un-booked

*risked* drilling upside

$5.85

$11.15

2011 Year End McDaniel Property Summary: Garrington Proved Plus Probable Reserve Value (BT NPV 10%) ….…$37.0 million Pembina Proved Plus Probable Reserve Value (BT NPV 10%) ………..$16.2million Other Proved Plus Probable Reserve Value (BT NPV 10%) ……….……$22.8 million

Niton / McLeod “Potential Company Maker Asset”

6

31 3631 3631 3631 3631 3636

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

6

31

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

6

31

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

616161616161

31 3631 3631 3631 3631 3636

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

6

31

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

6

31

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

616161616161

31 3631 3631 3631 3631 3636

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

6

31

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

6

31

16

31 36

16

31 36

16

31 36

16

31 36

16

31 36

1

36

616161616161

T53

T54

T55

T56

T57

T53

T54

T55

T56

T57

R11W5R12R13R14R15R16

R10W5R11R12R13R14R15R16

File: Niton-McLeod Hyperion Land (Al Datum: NAD27 Projection: Stereographic Center: N53.77840 W115.86764 Created in AccuMap™, a product of IHS

Cardium rights - Crown

Deep rights only

Legend

Cardium rights – Crown with farm-in

Gross Net

Land Capture (acres) 35,680 32,508

Tier 1 Tier 1 & 2

Estimated Well Locations (wells) 129 gross/114 net 191 gross/172 net

Estimated Oil in place (Mbbl) 110,500 171,000

Potential Recoverable Oil with primary recovery at 11.7% (Mbbl)

12,900 20,000

Niton/McLeod - Cardium Type Curve Generation

7

Cardium Light Oil Economics

8

Niton / McLeod Risked case Technically Supported Case

Targeted Well Capital ($M) $3,000 $3,000

IP 30 day (boe/d) 161 (92% oil) 225 (92% oi)

Reserves (mboe) 146 (88% oil) 178 (88% oil)

Primary Oil Recovery Factor (%) 11.7% 15.9%

Unbooked Hz Well Location’s 191 Gross / 172 Net 191 Gross / 172 Net

NPV BT10% ($M) $2,000 $4,100

ROR (%) 41% 98%

Payout (Years) 2.0 1.2

Production Efficiency ($/boe/d) $19,000 $13,500

Reserve Cost ($/boe) $20.54 $16.90

Field Netback ($/boe) $67.46 $69.48

Recycle Ratio 3.3 4.1

* Commodity Pricing – McDaniel & Associates July 2012 forecast; WTI US$90.00

0

50

100

150

200

250

1 3 5 7 9 11 13 15 17 19 21 23

Oil

Rat

e (

bb

l/d

ay)

Months On Production

Niton / McLeod Model - Cardium Hz Type Well

Risked Case Technically Supported Case

Development vs Exploration? Definitely Development!

9

A New Cardium Oil Fairway (Why was this asset available to Hyperion?)

10

Financial & Production Performance

11/23/2012 11

Accelerating cash flow(1) and cash flow per share growth since recap in July 2010

(1) “Cash Flow” refers to cash flow from operations excluding changes in working capital

Continued quarter over quarter oil focused production growth Long term production increases through opportunistic/accretive acquisitions and continuous development of corporate lands.

36%

52%

12%

Q4 2011 to Q1 2012 cash flow decrease primarily caused by realized pricing issues between Edmonton Par and WTI benchmarks.

Corporate Profile

Volumes Hedged

Weighted Average Floors and Ceilings

$111.86 $111.86 $112.26 $108.00 $108.00 $108.00

12

Other hedges include: • 425 bbls/day differential hedge Edmonton Light to WTI U.S. for the production period October 1, 2012 to December 31,2012 at PAR • Fixed/floating interest rate swap for $20 million for the borrowing period May 30, 2012 to May 29, 2015 at 1.5% • 1095 mcf/day hedge on Alberta natural gas benchmark for the production period May 1, 2012 to December 31, 2012 at a floor of $1.58 and a ceiling of $2.31

Ticker Symbol: HYX on TSX.V

Shares Outstanding:

Basic (MM): 54.2

Warrants (MM): 12.9

Options (MM): 4.8

Total Fully Diluted (MM): 71.9

Management, employees and directors ownership all sources (%): 12%

Current bank line limit – to be reviewed by lender in November 2012 $40

Current acquisition line limit – to be reviewed by lender in November 2012 $10

Management and Directors

13

Executive History

Trevor Spagrud President, CEO and Director

President, CEO & Director, Titan Exploration Ltd. VP Engineering, Enterra Energy; VP Operations, Big Horn Resources

Larry Hammond Chief Operating Officer

VP Canadian Operations, Enerplus Team Lead EnCana, PanCanadian; Lead Petroleum Engineer, Hibernia

Doug Bailey Chief Financial Officer

Energy Restructuring Consultant CFO Canadian Phoenix, interim CFO various restructured companies, founder private E&P

Tim Gee Vice President, Engineering

Manager Engineering, Berkana Energy (Quatro Resources) Engineering Team Lead, NAL Oil & Gas Trust, Ocelot

Ryan Heath Vice President Land & Business Development

VP Land & Business Development, Severo Energy Corp. Senior Land Negotiator, Paramount; NCE Petrofund

Steve Horth Manager, Exploration

Senior Geologist, Titan Exploration Ltd. Starpoint, Cougar, Dominion, Marathon, Tarragon, Opinac

Director History

Rod Maxwell, Chairman Managing Director, Stonebridge Merchant Capital

Director of a number of publically traded oil and gas companies and energy related service companies. CA & CBV.

Dan O’Neil President, CEO and Director Surge Energy Inc.

Director of a number of publically traded oil and gas companies and energy related service companies; former President and CEO Breaker Energy Ltd.

Greg Turnbull Regional Managing Partner, McCarthy Tetrault LLP

Director of a number of publically traded oil and gas companies including Crescent Point

Greg Bay Founding Partner, Cypress Capital Management

Director of a number of publically traded oil and gas companies and energy related service companies

Titan Exploration (2004-2007): • Founder, 0 - 2,800 boe/d in 3 years • 150 net, hz light oil drilling locations in inventory • Stock value increased from approx. $1.50/sh (IPO) to ~$7.50/sh. • Sold to PennWest (Dec/07) at ~ $3.00/sh (market was depressed at the time

due to recent market events: Elimination of royalty trust structure and punitive changes to Alberta crown royalties)

Enterra Energy / Big Horn Resources (1997-2003): • Started as second employee with 50 boe/d of production • Grew company to 6,500 boe/d by 2003 • Growth from repeatable Doe Creek light oil drilling • Stock value appreciated from $0.70 to $25.00 in this period • Was asked to be CEO of Enterra Trust, but left to found Titan Enerplus (2005-2008): • Led a team of 400 people and production base of 80,000 boe/d (capex of

$400M/yr). Left to found Hyperion EnCana (2000-2005): • Led a team of 40 people and production base of 15,000 boe/d (capex of $40

million/yr) • Responsible for increasing opportunities which resulted in annual capital

expenditures increasing in area from $10M to $40M Hibernia Management Company (1997-2000): • Lead petroleum engineer responsible for offshore well completion and

operations engineering • Managed production of 150k boe/d (well capital cost of ~$50MM each)

Restructuring Consultant (2004-2010): • Worked with lenders, portfolio managers and other stakeholders in the

restructuring of distressed junior oil and gas companies • 15 engagements: involved corrective actions such as: sale of assets, raising

equity, satisfaction of flow thru spending obligations and corporate mergers • Raised $230M of debt and equity as part of restructuring initiatives • Developed enhanced budgeting and modelling skills. Left to found

Hyperion SCGC Inc. (2002-2004): • Responsible for Calgary based, Korean backed, junior oil and gas start up • Helped managed growth thru acquisitions and drilling

Banker: National Bank of Canada

Auditor: KPMG

Legal Counsel: McCarthy Tétrault LLP

Evaluation Engineers: McDaniel & Associates

Registrar & Transfer Agent: Alliance Trust Company

Research Coverage:

GMP Securities Dundee Capital Markets

Canaccord Genuity Paradigm Capital

Desjardins Securities Casimir Capital

Stonecap Securities National Bank Financial

Contact Information

14

Advisors

Hyperion Exploration Corp.

Trevor Spagrud, P.Eng.

President & Chief Executive Officer

(403) 930-0701

Hyperion Exploration Corp.

Doug Bailey, CGA

Chief Financial Officer

(403) 930-0703

Notice to Residents of Ontario

Subscribers (“Subscribers”) resident in Ontario who purchase the securities (the “Shares”) described in this document (the “Offering Memorandum”), and any amendment thereto, during the period of distribution will have a statutory right of action for damages, or, while still the owner of the Shares, for rescission, against Hyperion in the event that the Offering Memorandum, or any amendment thereto, contains an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make any statement not misleading in light of the circumstances in which it was made (hereinafter referred to as a “misrepresentation”) without regard to whether the purchaser relied on the misrepresentation. This statutory right of action is subject to, among other things, the following:

a) if a purchaser elects to exercise the right of action for rescission, the purchaser will have no right of action for damages against Hyperion;

b) no action may be commenced to enforce a right of action for rescission 180 days after the date on which payment for the Shares is made by the purchaser;

c) no action may be commenced to enforce a right of action for damages after the earlier of (i) 180 days after the Subscriber of the Shares first had knowledge of the facts giving rise to the cause of action and (ii) three years after the date on which payment for the Shares is made by the Subscriber;

d) Hyperion will not be liable if it proves that the Subscriber purchased Shares of Hyperion with knowledge of the misrepresentation;

e) in the case of an action for damages, Hyperion will not be liable for all or any portion of the damages that it proves do not represent the depreciation in value of the Shares as a result of the misrepresentations relied upon; and

f) in no case will the amount recoverable in such action exceed the price at which the Shares were sold to the Subscriber.

The statutory right of action described above is in addition to and without derogation from any other right or remedy that the Subscriber might have at law.

15