Corporate Presentation Corporate Presentation August, 2004.

27

Corporate Presentation www.telemar.com.br/ir August, 2004

-

Upload

lucinda-lawrence -

Category

Documents

-

view

244 -

download

0

Transcript of Corporate Presentation Corporate Presentation August, 2004.

Corporate Presentation

Corporate Presentation

www.telemar.com.br/ir August, 2004

2August 2004August 2004 www.telemar.com.br/ir

Telemar Presentation - Contents

3. Review of Operating Results 12

2. Growth Strategy 3

1. Highlights – 2003/2004 1

4. Financial Overview 20

3August 2004August 2004 www.telemar.com.br/ir

Goal: Building a fully integrated telecom service provider

Change, adaptation and consolidation Market share gains in all lines of

businesses Selective growth (New Services) Consolidation of investments

Growth in highly competitive markets: Long Distance (Nationwide and

International) Data & Corporate (Nationwide) PCS Mobile Services (Region I)

Exploring new opportunities: Broadband Bundling Services New Products (residential/SME) Wi-Fi hotspots

Target: Ensure a sound financial position, with increasing returns to shareholders

Goal: Building a fully integrated telecom service provider

Change, adaptation and consolidation Market share gains in all lines of

businesses Selective growth (New Services) Consolidation of investments

Growth in highly competitive markets: Long Distance (Nationwide and

International) Data & Corporate (Nationwide) PCS Mobile Services (Region I)

Exploring new opportunities: Broadband Bundling Services New Products (residential/SME) Wi-Fi hotspots

Target: Ensure a sound financial position, with increasing returns to shareholders

Highlights – Telemar 2003/2004

Region I

= Concession areafor Wireline services

= Mobile license for Wireless services

Nationwide

= Authorization areafor Long-Distance and Data services

4August 2004August 2004 www.telemar.com.br/ir

3. Review of Operating Results 12

2. Growth Strategy 3

1. Highlights – 2003/2004 1

4. Financial Overview 20

5August 2004August 2004 www.telemar.com.br/ir

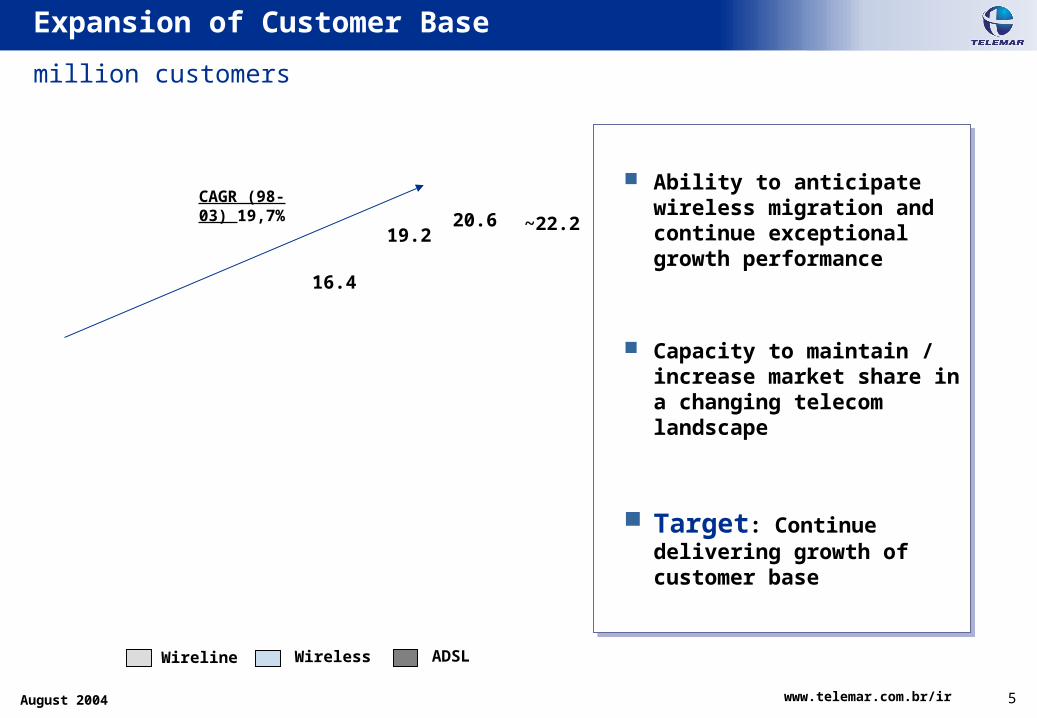

Ability to anticipate wireless migration and continue exceptional growth performance

Capacity to maintain / increase market share in a changing telecom landscape

Target: Continue delivering growth of customer base

Ability to anticipate wireless migration and continue exceptional growth performance

Capacity to maintain / increase market share in a changing telecom landscape

Target: Continue delivering growth of customer base

million customers

*Company’s acquisition

Expansion of Customer Base

CAGR (98-03) 19,7%

19.2

16.4

~22.220.6

Wireline Wireless ADSL

6August 2004August 2004 www.telemar.com.br/ir

Investments for expansion of fixed line network essentially completed

Fully operational digital platform

Mix consists of 78% residential, 18% business, and 4% public phones

Wireline penetration is only ~50% of households in Region I

Obstacle: Increase in wireline penetration subject to GDP growth and regulatory changes

Investments for expansion of fixed line network essentially completed

Fully operational digital platform

Mix consists of 78% residential, 18% business, and 4% public phones

Wireline penetration is only ~50% of households in Region I

Obstacle: Increase in wireline penetration subject to GDP growth and regulatory changes

million lines

Fixed Lines in Service

growth maintenance

7August 2004August 2004 www.telemar.com.br/ir

Wireline / ADSL Market in Brazil

Other

17%

Velox

83%

Velox

18%

Other

18%

Speedy

40%

Turbo

24%

Market Share (Brazil v. Region I) – Dec/03

Market Share (Brazil v. Region I) – Dec/03

PC Penetration (% of households) – Dec/03

PC Penetration (% of households) – Dec/03

*

*Source: Pyramid Research

2003

Velox is already present in 110 cities, more than ten times the availability of broadband alternatives

Broadband penetration is expected to grow to 30% of nationwide internet access in the next five years

Effort to build sales channels to penetrate SME clients together with other bundled services (LD, wireless)

Challenge: Capture and retain premium clients increasing overall ARPU

Velox is already present in 110 cities, more than ten times the availability of broadband alternatives

Broadband penetration is expected to grow to 30% of nationwide internet access in the next five years

Effort to build sales channels to penetrate SME clients together with other bundled services (LD, wireless)

Challenge: Capture and retain premium clients increasing overall ARPU

Brazil Region I

Average

8August 2004August 2004 www.telemar.com.br/ir

Highest ADSL growth in Brazil (+176k lines >37% of 2003 nationwide net adds)

ADSL represents 82% of broadband access in Brazil

Velox revenues increased by 285% yoy in 1H04

Subscribers reached 217K in Dec/03 (18% of total broadband access in Brazil), and 345k in Jun/04

Target: Increase ADSL penetration in Region I from 1.9% of LIS to 5% in 2-3 years

Highest ADSL growth in Brazil (+176k lines >37% of 2003 nationwide net adds)

ADSL represents 82% of broadband access in Brazil

Velox revenues increased by 285% yoy in 1H04

Subscribers reached 217K in Dec/03 (18% of total broadband access in Brazil), and 345k in Jun/04

Target: Increase ADSL penetration in Region I from 1.9% of LIS to 5% in 2-3 years

ADSL Growth

Thousand lines

Gross Revenue

(R$ million)

450

9August 2004August 2004 www.telemar.com.br/ir

Wireless Market in Brazil

^Includes other operators: Nextel, CTBC, SERCOMTEL, Telemig and Tele Norte Celular

** Morgan Stanley estimates.

Market Share (Brazil v. Region I) – Jun/04

Market Share (Brazil v. Region I) – Jun/04

Wireless Penetration (%) – Jun/04Wireless Penetration (%) – Jun/04

*

*Source: Pyramid Research

Even with increased competition, Oi remains a high growth player in its home market (35% net adds in 2Q04)

Oi reached ~21% market share in Jun/04

Wireless penetration in Region I (25%) still offers significant growth potential

Challenge: Grow subs by ~65% in 2004, with positive EBITDA margins

Even with increased competition, Oi remains a high growth player in its home market (35% net adds in 2Q04)

Oi reached ~21% market share in Jun/04

Wireless penetration in Region I (25%) still offers significant growth potential

Challenge: Grow subs by ~65% in 2004, with positive EBITDA margins

Average

Brazil** Region I

Vivo

44%

TIM

19%

Other*

8%

Claro

20%

Oi

9%

10August 2004August 2004 www.telemar.com.br/ir

Most successful GSM launch globally

5 million subs in 24 months

Almost 50% share of all net adds in Region I since launching

Oi´s market share (Jun/04)

Region I: 21%

Brazil: 9%

Most successful GSM launch globally

5 million subs in 24 months

Almost 50% share of all net adds in Region I since launching

Oi´s market share (Jun/04)

Region I: 21%

Brazil: 9%

Wireless Platform

Pre paid Post paid

1,4012,236

3,893

80%20% 80%

20%

83%

17%

35

~6,500

Thousand subscribers

Gross Revenue

(R$ million)

5,093

85%

15%

11August 2004August 2004 www.telemar.com.br/ir

Short Message Service - SMS

Thousand messages

Gross Revenue

(R$ million)

SMS annual revenues achieved a run-rate of over R$ 70 million in the last two quarters

Oi has a team focused on data services, particularly for the corporate market

Oi also launched Wi-Fi hotspots in early 2004

Target: Increase data ARPU and maintain growth of customer base

SMS annual revenues achieved a run-rate of over R$ 70 million in the last two quarters

Oi has a team focused on data services, particularly for the corporate market

Oi also launched Wi-Fi hotspots in early 2004

Target: Increase data ARPU and maintain growth of customer base

12August 2004August 2004 www.telemar.com.br/ir

Focus on profitability: EBITDA positive since inception

62% CAGR in attendant positions, in line with increase in customer base and net revenues (70% CAGR)- Contax currently has 29 customers, including major banks, utilities, insurance, media, telecom, retail

Target: Consolidate #1 position as call center operator in Brazil

Focus on profitability: EBITDA positive since inception

62% CAGR in attendant positions, in line with increase in customer base and net revenues (70% CAGR)- Contax currently has 29 customers, including major banks, utilities, insurance, media, telecom, retail

Target: Consolidate #1 position as call center operator in Brazil

Call Center Services

Attendant Positions

7,3374,947

12,907

Net Revenues

(R$ million)

223

421

146

>15,00014,887

287

13August 2004August 2004 www.telemar.com.br/ir

3. Review of Operating Results 12

2. Growth Strategy 3

1. Highlights – 2003/2004 1

4. Financial Overview 20

14August 2004August 2004 www.telemar.com.br/ir

13%6%

7%

17%

9%8%

40%

Consolidated Gross Revenue Breakdown – 1H04

The Company’s four main lines of business provide a healthy balance between stable cash flow and growth opportunities

Local59%

Inter-Connection

Data

Long Distance(includes VC2/3)

Fixed to Mobile (VC1)

Wireline

Moderate Growth

Long Distance

High Growth

Wireless

High Growth

Data & Corporate

High Growth

Others(*)

(*) – Includes advanced voice, public telephones, additional services and Contact Center.

Mobile

15August 2004August 2004 www.telemar.com.br/ir

Telemar keeps on leadership in LD services in Region I.

Growth in Long Distance Services

LD Gross Revenue - R$ millionLD Gross Revenue - R$ millionLD as a % of Total Revenues

(includes F2M)

LD as a % of Total Revenues (includes F2M)

+31.7%

16August 2004August 2004 www.telemar.com.br/ir

Key corporate and governmental contracts achieved during 2003

Data revenues increased by 31% in 2003 and 15% in 2002

Challenge: Increase market share in data services in Region I and nationwide

Key corporate and governmental contracts achieved during 2003

Data revenues increased by 31% in 2003 and 15% in 2002

Challenge: Increase market share in data services in Region I and nationwide

Focus on Data / Corporate Services

Major Clients won in 2003Major Clients won in 2003

Data Revenues (gross) - R$ millionData Revenues (gross) - R$ million

+31.6%

17August 2004August 2004 www.telemar.com.br/ir

Revenue growth of 69% yoy

Services revenues increased 91% yoy, resulting mainly from subscriptions, outgoing calls & SMS

EBITDA breakeven reached after 18 months of operations

Target: Continue to deliver high revenue growth with positive EBITDA margins

Revenue growth of 69% yoy

Services revenues increased 91% yoy, resulting mainly from subscriptions, outgoing calls & SMS

EBITDA breakeven reached after 18 months of operations

Target: Continue to deliver high revenue growth with positive EBITDA margins

Gross Revenue from Wireless Services

Services

Handsets

R$ million

511 866

1H03 1H04

18August 2004August 2004 www.telemar.com.br/ir

Delivering consistent revenue and EBITDA growth in spite of huge wireline expansion & wireless startup

Recurring margins stable over time, in the mid-40’s EBITDA for 2001 impacted by extraordinary provisions

Target 2004: Consolidated EBITDA margin in mid-40s even with a faster growth of wireless revenues

Delivering consistent revenue and EBITDA growth in spite of huge wireline expansion & wireless startup

Recurring margins stable over time, in the mid-40’s EBITDA for 2001 impacted by extraordinary provisions

Target 2004: Consolidated EBITDA margin in mid-40s even with a faster growth of wireless revenues

R$ million

Consolidated Net Revenues and EBITDA

Net Revenues EBITDA EBITDA Margin

19August 2004August 2004 www.telemar.com.br/ir

Consolidated Net Income

1999 2000 2001 2002 20031998 1H04

R$ million

1H03

20August 2004August 2004 www.telemar.com.br/ir

CAPEX 2003: ~12% of net revenues (v. 17% in 2002)

CAPEX 1H04: R$ 534 million (7.1% of net revenues)

Consolidated CAPEX since 1998: US$10.4 billion

Target: Stabilize CAPEX at ~15% of net revenues to support growth in wireless and other services (broadband, long distance)

CAPEX 2003: ~12% of net revenues (v. 17% in 2002)

CAPEX 1H04: R$ 534 million (7.1% of net revenues)

Consolidated CAPEX since 1998: US$10.4 billion

Target: Stabilize CAPEX at ~15% of net revenues to support growth in wireless and other services (broadband, long distance)

10.1

2.01.7

Wireline

Consolidated CAPEX

Wireless

R$ billion

Anatel TargetsMobile License

(R$1.1 bn)

2.0

1.1

0.9

1.1

2.82.22.5

0.6

60%

40%

2.2

7.9

0.5

21August 2004August 2004 www.telemar.com.br/ir

3. Review of Operating Results 12

2. Growth Strategy 3

1. Highlights – 2003/2004 1

4. Financial Overview 20

22August 2004August 2004 www.telemar.com.br/ir

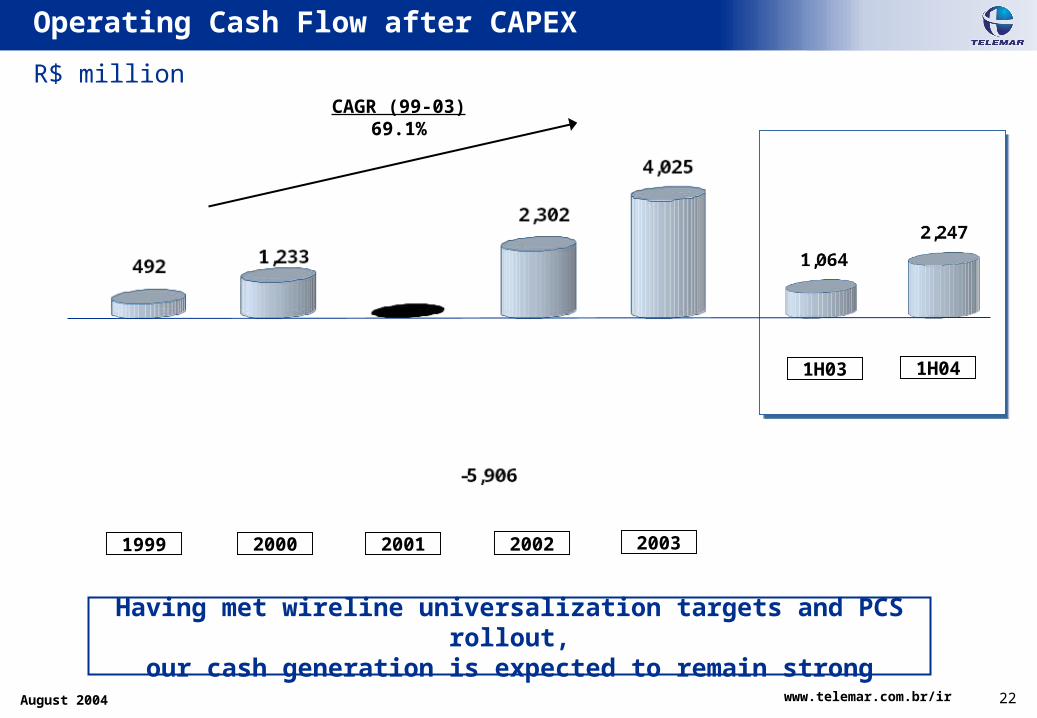

Operating Cash Flow after CAPEX

R$ million

1999 2000 2001 2002 2003

Having met wireline universalization targets and PCS rollout,our cash generation is expected to remain strong

CAGR (99-03)69.1%

1H041H03

23August 2004August 2004 www.telemar.com.br/ir

Dividend Payments - 1999/2003

1999 2000 2001 2002 2003

Dividend yield

Dividend *

US$ million

Our goal is to continue to provide high cash returns to shareholders

* includes JCP (interest on capital)

24August 2004August 2004 www.telemar.com.br/ir

Net Debt Position and Repayment Schedule

R$ million

% of total

12.1 22.6 28.0 11.4 6.4

Net Debt – Jun/04 Net Debt – Jun/04 Gross Debt Repayment Schedule –

Jun/04

Gross Debt Repayment Schedule – Jun/04

Given our strong cash generation, we should reduce net debt to less than 1x EBITDA by year end 2004

19.5

R$ 7,355 million R$ 12,200 million

25August 2004August 2004 www.telemar.com.br/ir

Key Financial Ratios

Net Debt / EBITDANet Debt / EBITDA Amortization*/ EBITDA (%)Amortization*/ EBITDA (%)

Dividends* / EBITDA (%)Dividends* / EBITDA (%)CAPEX / EBITDA (%)CAPEX / EBITDA (%)

* includes JCP (interest on capital)

(*) 12 - Month EBITDA* Principal and interest

26August 2004August 2004 www.telemar.com.br/ir

Key Financial and Valuation Ratios

Enterprise Value / EBITDAEnterprise Value / EBITDA Market Cap / EBITDAMarket Cap / EBITDA

EBITDA / Net Interest ExpenseEBITDA / Net Interest ExpenseEBITDA / Total Debt ServiceEBITDA / Total Debt Service

27August 2004August 2004 www.telemar.com.br/ir

Investor Relations

Rua Humberto de Campos, 425 / 8º andar

Leblon

Rio de Janeiro -RJ

Phone: ( 55 21) 3131-1314/1313/1315/1316

Fax: (55 21) 3131-1155

E-mail: [email protected]

Visit our website:

http://www.telemar.com.br/ir

This presentation contains forward-looking statements. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements and involve inherent risks and uncertainties. These statements are based on current plans, estimates and projections, and therefore you should not place undue reliance on them. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new information or future events

“Safe Harbor” Statement