Corporate governance

28

Corporate Governance

-

Upload

deborah-sharon -

Category

Education

-

view

106 -

download

0

Transcript of Corporate governance

Corporate Governance

Corporate Governance• It is a system by which business corporations are

directed and controlled• Specifies the distribution of rights and

responsibilities among different participants in the corporation

• Also specifies the rules and procedures for making decisions on corporate affairs

• Provides the structure through which the company objectives are set and the means of attaining those objectives and monitoring performance

Corporate Governance• It can be defined narrowly as the relationship of

a company with its stakeholders or more broadly, its relationship with society

• It is about promoting corporate fairness, transparency and accountability

• It is a system and a process, consistent with principles and practices which are used by corporate firms of a free and open society

• It assigns final authority and full responsibility of managing the firm to the Board of Directors of the firm

Corporate Governance Concepts

• Milton Friedman, ‘Corporate Governance is to conduct the business in accordance with owner or shareholders’ desires, which generally will be to make as much money as possible, while conforming to the basic rules of the society embodied in law and local customs’.

Corporate Governance Concepts

• J.Wolfensohn, President, World Bank, ‘Corporate Governance is about promoting corporate fairness, transparency and accountability’

Corporate Governance Concepts• Is a set of process or set of systems and process

to ensure that the company is managed to suit the best interests of all stakeholders

• Internal Stakeholders : Promoters, Employees, Workmen and Executives

• External Stakeholders : Shareholders, Customers, Suppliers, Financial Institutions, Dealers, Vendors, Bankers, Community, Trade Bodies, Government, Regulators and Fauna and Flora of the area

Corporate Governance Concepts

• Voluntary Ethical Code of Business• Transparency, Integrity and Accountability of

the Management• Deals with laws, procedures, practices and

implicit rules that determine a company’s ability to take correct managerial decisions for its stakeholders

Need for Corporate Governance

• Market driven economy• Globalization and Liberalization • Severe and chaotic competition (Efficiency

and Effectiveness are now the critical success factor)

• High and consistent standards for reporting• Changing ownership structure

Parties to Corporate Governance

• Primary social stakeholders– Customers– Suppliers– Investors– Managers and

Employees– Local Communities– Business Partners– Global citizens

• Secondary social stakeholders– Government – Society– Unions– Media and

Communicators– Trade bodies– Competitors

Parties to Corporate Governance

• Primary non-social stakeholders– Natural Environment– Non-human species– Future Generations

• Secondary non-social stakeholders– Environmental

pressure groups– Animal welfare

pressure groups

Principles of Corporate Governance

• Rights and Equitable treatment of shareholders

• Accountability• Disclosure and transparency• Integrity and ethical behavior• Interest of other stakeholders• Role and responsibilities of the Board• Transparency

Issues involving Corporate Governance Principles

• Mechanisms and Controls (designed to reduce the inefficiencies that arise)

• Internal Corporate Governance controls• Monitoring by the Board of Directors

(safeguard invested capital)• Remuneration (Performance based

remuneration)

Appointment of Directors

• Four Types of Directors in a limited company– Working Directors– Non-Working Directors but from the entrepreneurs’

family– Outside directors inducted for their expertise in some

area connected with the firm’s business eg. advocates, chartered accountants and technical consultants

– Directors nominated by lending financial institutions and banks

Steps to be taken in Governing Corporations

• Forward looking reporting (Reports to be strategic)

• Score-card approach (should give the salient features of the report at a glance)

• Measurements and controls (develop forms with digital approach to make measurement possible)

• Responsibility and Accountability (to stakeholders is the foremost interest)

Steps to be taken in Governing Corporations

• Transparency of Operations (especially with the stakeholders)

• Trust with teams• Fairness (sense of justice in all its dealings)

Ethical Business

Ideas behind Corporate Governance• Adequate information to stake holders• Focused approach• Stream-lined delegation• Professional management

• This would result in maximizing the shareholder value and in protecting the interest of other stakeholders

Corporate Governance in India

• Main issues in the area of Corporate Governance in India

• Role of Board of Directors (independent and effective board)

• Composition of the Board• Audit Committee (>5 crore paid-up capital must

establish audit committee; may include non-executive directors, auditors, the company secretary or any senior manager)

Corporate Governance in India

• Shareholders Committee (SEBI’s code provides for constitution of shareholders’ committee under the chairmanship of non-executive director - to ensure that grievances of shareholders)

SEBI Code of Corporate Governance

• Issued by SEBI dated 21.2.2000• SEBI constituted a committee on Corporate

Governance under chairmanship of Kumar Mangalam Birla

• To promote and raise the standard of Corporate Governance in respect of Listed companies

SEBI Code of Corporate Governance

Board of Directors• Optimum combination of executive and non-

executive directors (not less than 50%)• All pecuniary relationship or transactions of

non-executive directors to be disclosed in Annual Report

SEBI Code of Corporate Governance

Audit Committee• To meet 3 times a year• Shall have powers – To investigate any activity within the terms of

reference– To seek info from any employee– To obtain outside legal and other professional

advice

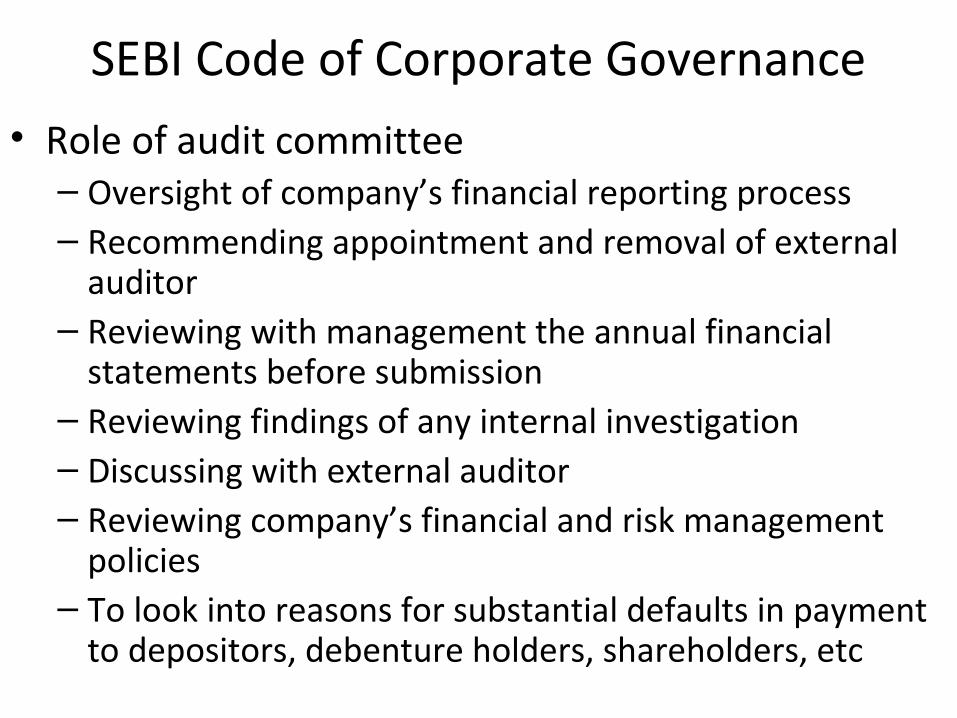

SEBI Code of Corporate Governance• Role of audit committee– Oversight of company’s financial reporting process– Recommending appointment and removal of external

auditor– Reviewing with management the annual financial

statements before submission – Reviewing findings of any internal investigation– Discussing with external auditor– Reviewing company’s financial and risk management

policies– To look into reasons for substantial defaults in payment

to depositors, debenture holders, shareholders, etc

SEBI Code of Corporate Governance

Remuneration of Directors• Remuneration of non-executive directors to

be fixed by Board of Directors• Remuneration to be disclosed in the

Corporate Governance section of the annual report

SEBI Code of Corporate Governance

Board Procedure• Board meeting to be held at least 4 times a

year• Maximum time gap between any 2 meetings

is 4 months• A director shall not be a member in more than

10 committees in which companies he is director

SEBI Code of Corporate Governance

Management • Directors’ Report or Management Discussion

and Analysis Report should form part of the annual report

• All transactions where the Board’s personal interest, that has potential conflict with interest of the company must be disclosed

SEBI Code of Corporate Governance

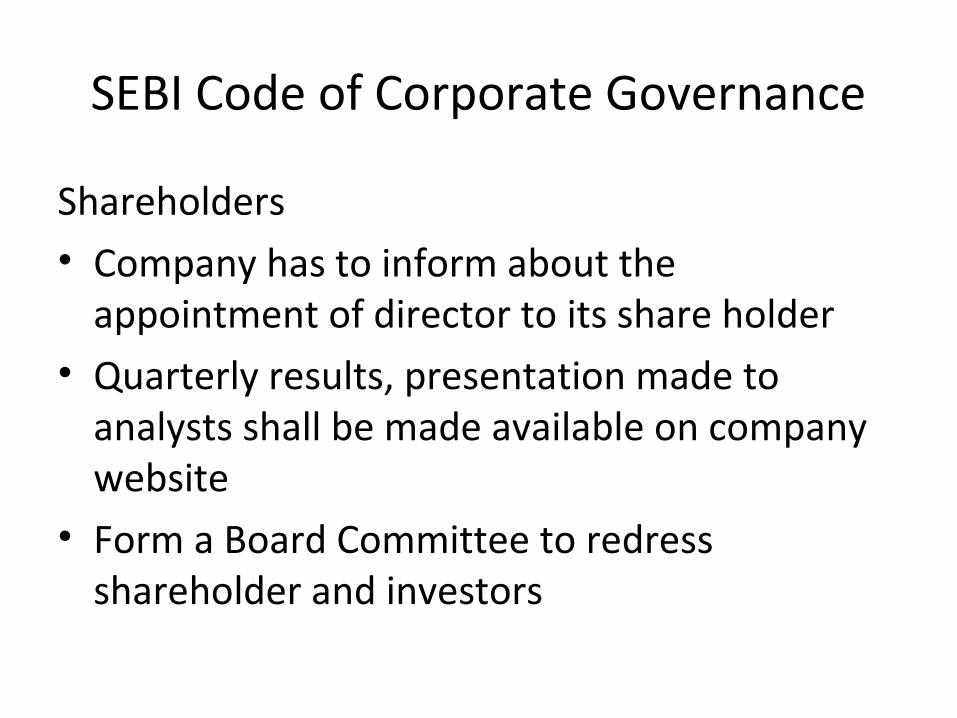

Shareholders• Company has to inform about the

appointment of director to its share holder• Quarterly results, presentation made to

analysts shall be made available on company website

• Form a Board Committee to redress shareholder and investors

SEBI Code of Corporate Governance

Report on Corporate Governance• Separate section on Corporate Governance in

the Annual Report with detailed Compliance Report on Corporate Governance

SEBI Code of Corporate Governance

Compliance• Obtain a Certificate from Auditors of the

Company regarding compliance of conditions of corporate Governance

• Annex such certificate with the Directors Report which is sent annually to all shareholders of the Company

• Sent to Stock Exchanges along with annual returns filed by the Company

![Corporate Governance Manualpaisalo.in/pdf/corporate-governance-en.pdf · [ 1 ] DEFINITIONS Corporate Governance Corporate Governance is the system of internal controls and procedures](https://static.fdocuments.us/doc/165x107/60457b037dc32d128b177c66/corporate-governance-1-definitions-corporate-governance-corporate-governance.jpg)