Corporate asset recovery – Practical considerations for ...

16

Prepared for National Association of Division Order Analysts (NADOA) Annual Conference September 8 - 10, 2021 Corporate Asset Recovery – Practical Considerations for Oil and Gas Companies

Transcript of Corporate asset recovery – Practical considerations for ...

Prepared for National Association of Division Order Analysts (NADOA) Annual ConferenceSeptember 8 - 10, 2021

Corporate Asset Recovery – Practical Considerations for Oil and Gas Companies

2© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

KPMG disclaimer

The following information is not intended to be “written advice concerning one or more Federal tax matters” subject to the requirements of section 10.37(a)(2) of Treasury Department Circular 230.The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.KPMG LLP does not provide legal services

3© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Contents

Unclaimed property – why are we here?— Asset Recovery

- Benefits- Potential cons

— Before pursuing claims- Internal compliance checks- Policies and procedures- Compliance gaps resolution- Reducing unclaimed assets, pre-escheat consideration

— Preparing claims, searches- How to gain efficiencies, when to search- Preparing claim documents- What administrators look out for

— The Claims submission process- Garnering trust- Responding to questions- Other considerations, fraud concerns, providers, benefits, cost

— Questions and contact info

4© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Benefits to asset recovery

Cash is king— Almost $50 billion in unclaimed funds

- Texas > $3 Billion- Florida > $2 Billion- California > $9 Billion

— Can add to department/company budgets

— Think about the direct, measurable value that you can add to your company's bottom line

— Re-occurring, unexpected income stream

— Wide range of claim values— Stimulus = incentive

Corporate asset recovery

Getting started

6© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Before pursuing claims

— Ask the questions:- is my company filing?- What property types have we reported?- To which state?- For how long?- Are we covering all of our product types and

revenue streams?- Have we accounted for subsidiaries?

Acquisitions?

— As part of your compliance review, you may want to conduct a self-audit of policies and procedures:- Are they formal and written?- If so, are the P&P followed?- Have roles been assigned?- Definitions, timelines, and matrices

Internal compliance checks Policies and procedures

7© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Before pursuing claims

— Consider VDAs or First time filings— VDAs offer several benefits (compared

to audits)- Shortened look back period- Waiver of interest and/or penalties- Increased control over the process by

holders - Allows holders to determine “in-scope”

entities and property types- Allows holders time to reduce exposure prior

to remittance— Even holders that previously completed VDAs

with, or audits by, the states may allow companies to periodically complete VDA programs to cover subsequent acquisitions

— DE domiciled companies

— USE YOUR NETWORKS— A surprising amount of fortune 500 companies

report unclaimed assets of other fortune 500 companies

— Respond to letters— Send your own “outreach” letters:

- Working interests, JIB- Complex entity structure- Recent turnover, change of responsibilities

— What to include:- Provide a name, direct line, listing of entities- Don’t request or provide to much info- Remember purpose of outreach

Resolve compliance gaps Reduce unclaimed assets

8© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

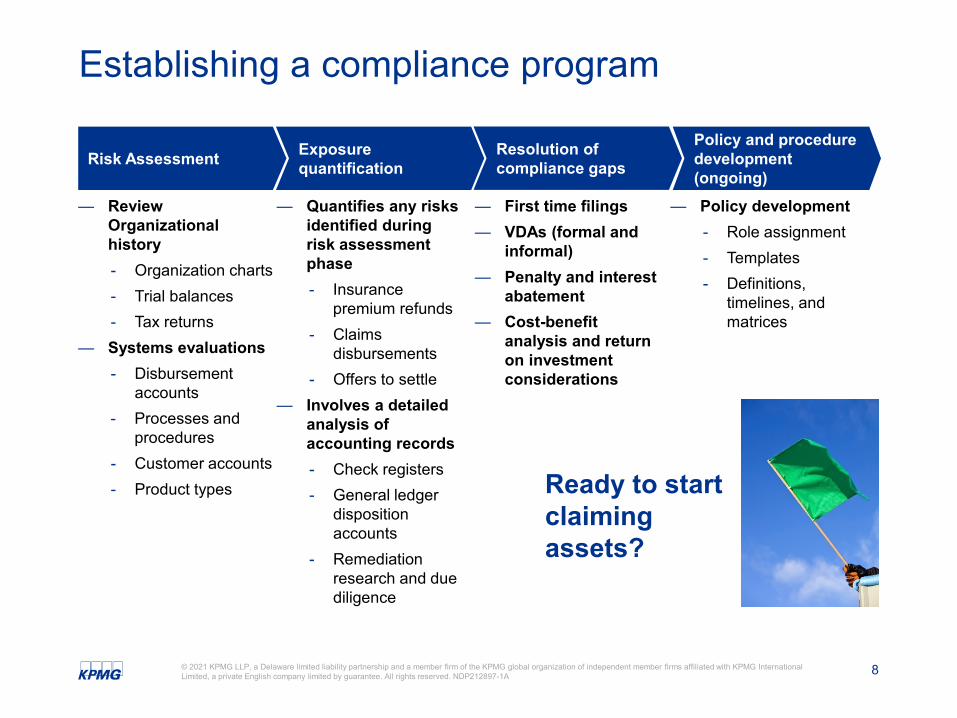

Establishing a compliance program

— Review Organizational history- Organization charts- Trial balances- Tax returns

— Systems evaluations- Disbursement

accounts- Processes and

procedures- Customer accounts- Product types

— Quantifies any risks identified during risk assessment phase- Insurance

premium refunds- Claims

disbursements- Offers to settle

— Involves a detailed analysis of accounting records- Check registers- General ledger

disposition accounts

- Remediation research and due diligence

— First time filings — VDAs (formal and

informal)— Penalty and interest

abatement— Cost-benefit

analysis and return on investment considerations

— Policy development- Role assignment- Templates- Definitions,

timelines, and matrices

Risk Assessment Exposurequantification

Resolution of compliance gaps

Policy and procedure development (ongoing)

Ready to start claiming assets?

Conducting searches, preparing claims

10© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Claims process and submission overviewConducting searches, preparing claims

Claim monitoring and performance

reports

Phase 1 –Feasibility

review

Phase 2 –Property

identification

Phase 3 –Claims

submission

Phase 4 –Ongoing property

identification

11© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

How to gain efficiencies, when to searchConducting searches, preparing claims

Phase 1:Gain efficiencies: — Use the aggregation websites to your advantage— Missingmoney.com – 42 states— Findmyfunds.com – 26 states (includes, WA, OR, WY, DE, CT, NJ)

- Total coverage of almost all 50 states— Consider searching remaining websites independently (e.g. CA)— Identify, save, expand, repeat

- Common nicknames, misspellings, abbreviations, subsidiaries - Identify office locations, PO Box locations, counties

— Delegate to a limited number of people

Phase 2:When to search:— State Databases are typically updated annually— Other’s may be more frequent. Take note of local jurisdictions policies, consider other sources— May also include pending claims— Come up with a frequency that works best for you, it may be staggered— Take note of each states reporting deadline— Slow times, off seasons

12© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Preparing claims packages

Phase 3:— Review and document individual state processes, each are different— Make sure to thoroughly review requirements, especially if you are preparing a large claim. — Example requirements:

- Driver's license- Delegation of authority- Address listings- Organization charts- Notary- Merger documents, PSAs- Yellow print cover pages- W-9

— It’s the little things…— Other things to consider

- Prioritizing claims— Some states don’t list dollar values or ranges upfront

- Is your company the rightful owner? Could there be co-owners?- Is there a reason that the funds haven’t been claimed?- Is your company currently undergoing an unclaimed property audit?

Conducting searches, preparing claims

13© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Garnering trust, responding to questionsThe claims submissions process

Phase 3:Confirm state submission requirements— Electronic vs. mail— Try to avoid omitting required documents— If PII is a concern, request an alternative upfrontGarnering trust:— Start with the easy ones first — Establish a relationship – delegate a point person for each state— Mind your Ps and Qs, be respectful of state delays— It is OK to make multiple submissions— Remember it is a Treasurer's job and duty to return these fundsResponding to questions:— Focus on education— Think about the why— Don’t forget to check the status online and follow upPhase 4:Repeat— Establish process as part of your go forward policies

and procedures

14© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

Other considerations

— What about all of those letters I get?- Provider – Pros and Cons

— Be wary of fraud- Things to look out for

Closing Remarks

Corporate asset recovery

kpmg.com/socialmedia

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.

© 2021 KPMG LLP, a Delaware limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. NDP212897-1A

The KPMG name and logo are trademarks used under license by the independent member firms of the KPMG global organization.

Some or all of the services described herein may not be permissible for KPMG audit clients and their affiliates or related entities.