Copyright © 2015 Pearson Education, Inc. The Revenue Cycle: Sales to Cash Collections Chapter 12...

40

Copyright © 2015 Pearson Education, Inc. The Revenue Cycle: Sales to Cash Collections Chapter 12 12-1

-

Upload

todd-dorsey -

Category

Documents

-

view

213 -

download

0

Transcript of Copyright © 2015 Pearson Education, Inc. The Revenue Cycle: Sales to Cash Collections Chapter 12...

Copyright © 2015 Pearson Education, Inc.

The Revenue Cycle: Sales to Cash CollectionsChapter 12

12-1

Copyright © 2015 Pearson Education, Inc.

Learning Objectives

•Describe the basic business activities and related information processing operations performed in the revenue cycle.

•Discuss the key decisions that need to be made in the revenue cycle, and identify the information needed to make those decisions.

•Identify major threats in the revenue cycle, and evaluate the adequacy of various control procedures for dealing with those threats.

12-2

Copyright © 2015 Pearson Education, Inc.

INTRODUCTION

•The revenue cycle is a recurring set of business activities and related information processing operations associated with:▫Providing goods and services to customers▫Collecting their cash payments

•The primary external exchange of information is with customers.

Copyright © 2015 Pearson Education, Inc.

Basic Revenue Cycle Activities

•1. Sales order entry•2. Shipping•3. Billing•4. Cash Collections

12-4

Copyright © 2015 Pearson Education, Inc.

1. Sales Order Entry Processing Steps

•Performed by Sales Department (reports to VP of Marketing)

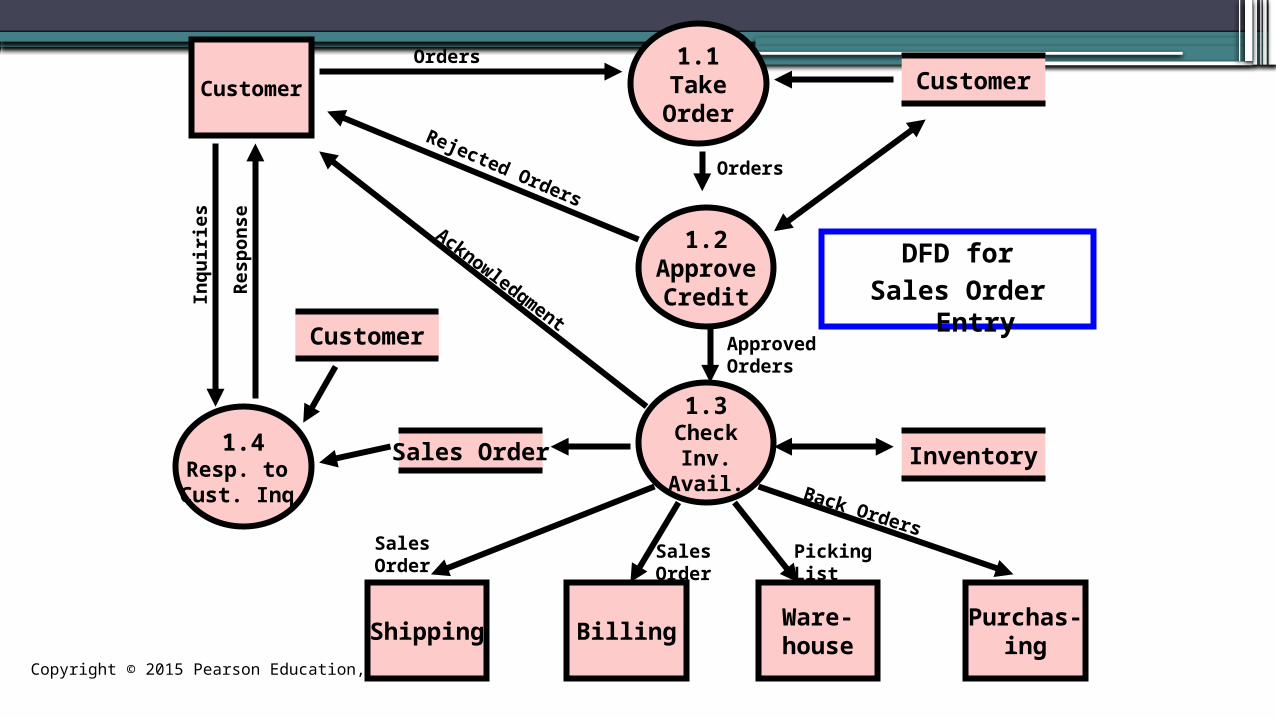

•1.1 Take the customer order •1.2 Approve customer credit•1.3 Check inventory availability•1.4 Respond to customer inquiries

12-5

Copyright © 2015 Pearson Education, Inc.

1.1TakeOrder

Customer

Shipping

1.2Approve

Credit

1.3Check

Inv.Avail.

BillingWare-house

Purchas-ing

1.4Resp. to Cust. Inq.

Customer

Sales Order

Customer

Inventory

Orders

Rejected Orders

Acknowledgment

Orders

ApprovedOrders

Back Orders

PickingList

SalesOrder

SalesOrder

Inq

uir

ies

Res

po

nse

DFD for

Sales Order Entry

Copyright © 2015 Pearson Education, Inc.

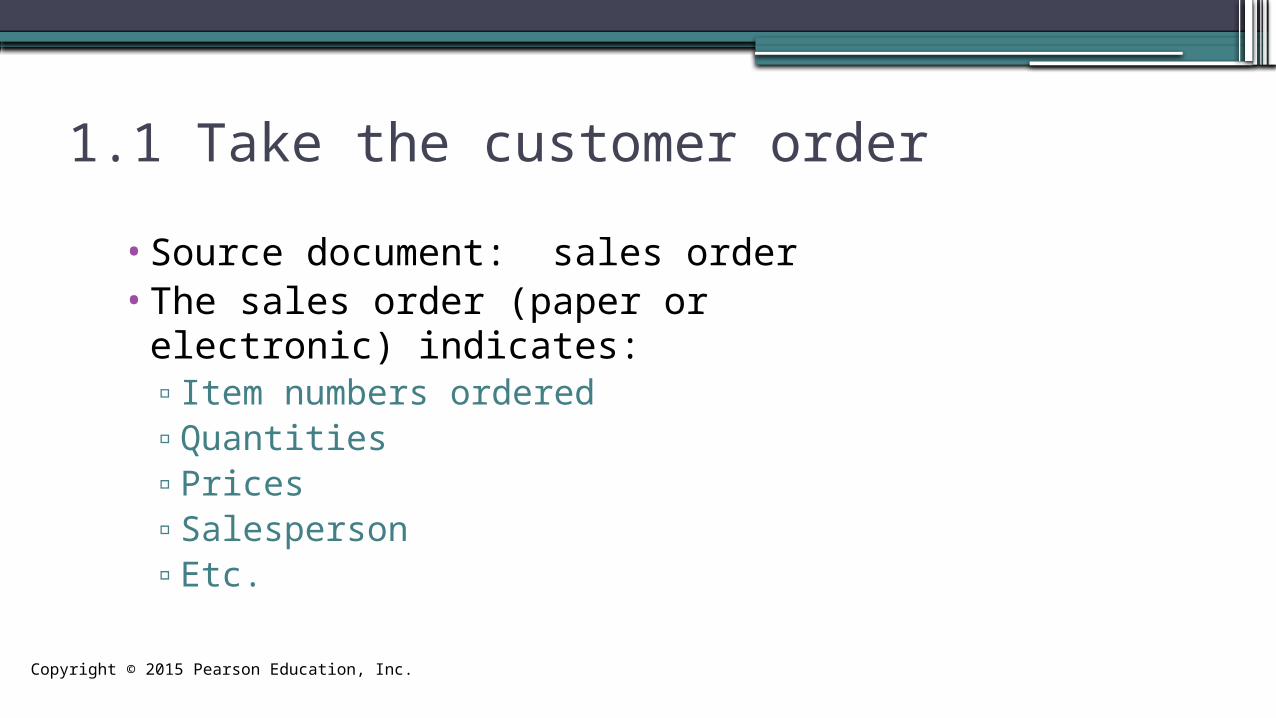

1.1 Take the customer order

•Source document: sales order •The sales order (paper or electronic)

indicates:▫Item numbers ordered▫Quantities▫Prices▫Salesperson▫Etc.

Copyright © 2015 Pearson Education, Inc.

1.1 Take the customer order•How IT can improve efficiency and effectiveness:

▫Have customers enter data themselves (OCR, webpages, etc.)

▫Orders entered online can be routed directly to the warehouse for picking and shipping.

▫Sales history can be used to customize solicitations.▫Choiceboards can be used to customize orders.▫Electronic data interchange (EDI) can be used to link a

company directly with its customers to receive orders or even manage the customer’s inventory.

▫Email and instant messaging are used to notify sales staff of price changes and promotions.

Copyright © 2015 Pearson Education, Inc.

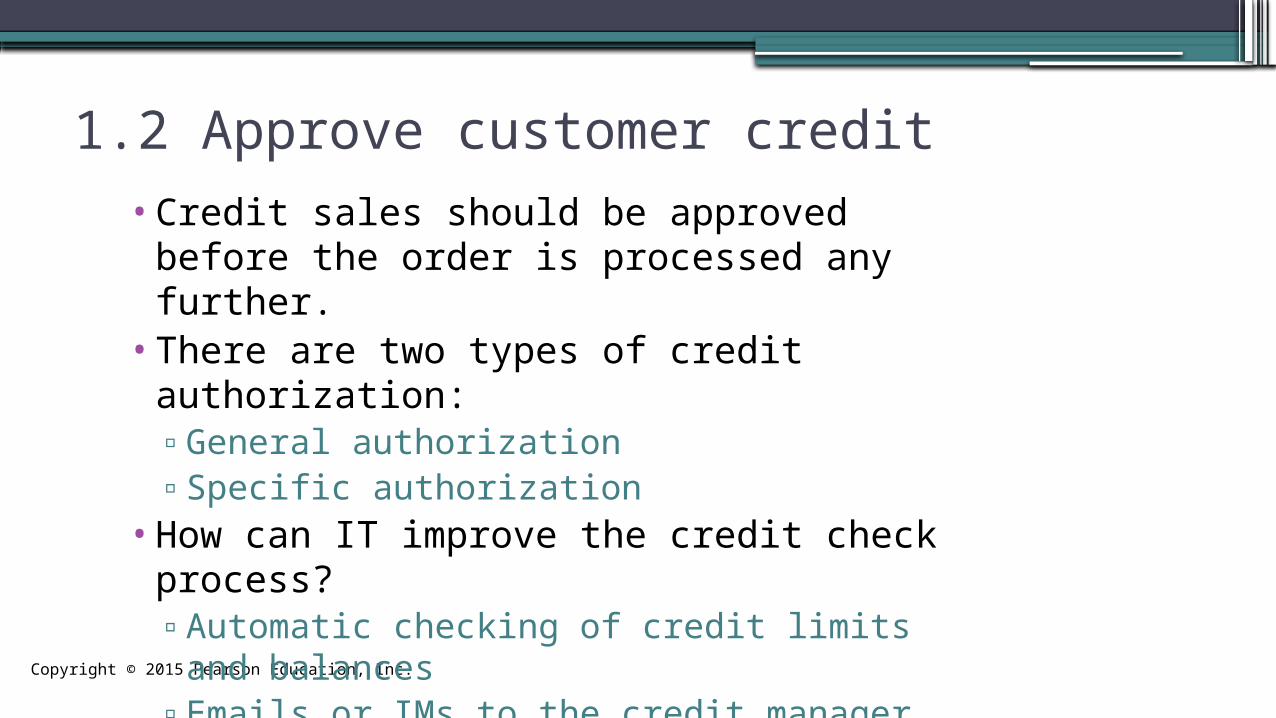

1.2 Approve customer credit•Credit sales should be approved before

the order is processed any further.•There are two types of credit

authorization:▫General authorization▫Specific authorization

•How can IT improve the credit check process?▫Automatic checking of credit limits and

balances▫Emails or IMs to the credit manager for

accounts needing specific authorization

Copyright © 2015 Pearson Education, Inc.

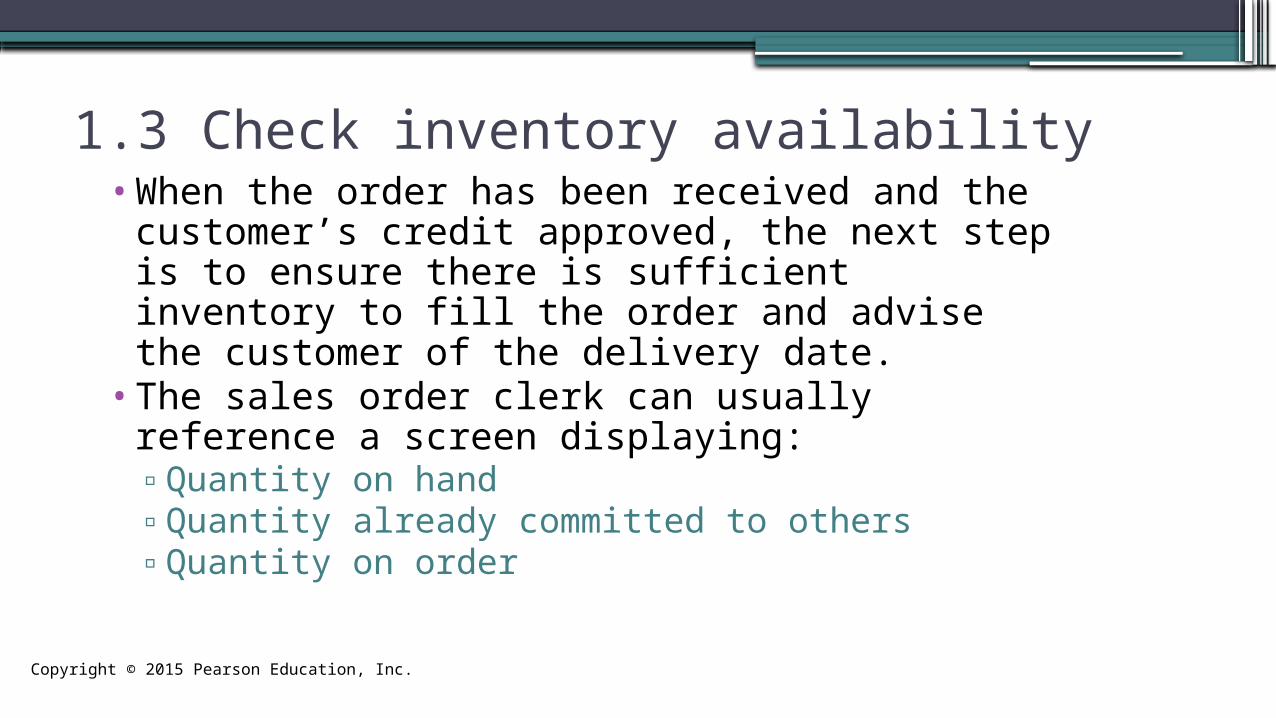

•When the order has been received and the customer’s credit approved, the next step is to ensure there is sufficient inventory to fill the order and advise the customer of the delivery date.

•The sales order clerk can usually reference a screen displaying:▫Quantity on hand▫Quantity already committed to others▫Quantity on order

1.3 Check inventory availability

Copyright © 2015 Pearson Education, Inc.

•If there are enough units to fill the order:▫Complete the sales order▫Update the quantity available field in the inventory

file▫Notify the following departments of the sale:

Inventory (picking ticket) Billing Shipping

▫Send an acknowledgment to the customer

1.3 Check inventory availability

Copyright © 2015 Pearson Education, Inc.

•If there’s not enough to fill the order, initiate a back order.▫For manufacturing companies, notify the

production department that more should be manufactured.

▫For retail companies, notify purchasing that more should be purchased.

1.3 Check inventory availability

Copyright © 2015 Pearson Education, Inc.

•Another step in the sales order entry process is responding to customer inquiries:▫May occur before or after the order is placed▫The quality of this customer service can be critical

to company success•Transaction processing technology can be used to

improve customer relationships:▫POS systems can link to the customer master file▫IT should be used to automate responses to routine

customer requests.▫The effectiveness of a website depends on its design

1.4 Respond to customer inquiries

Copyright © 2015 Pearson Education, Inc.

•Many companies use Customer Relationship Management (CRM) systems to support this process:▫Organizes customer data to facilitate

efficient and personalized service▫Provides data about customer needs and

business practices so they can be contacted proactively about the need to reorder

1.4 Respond to customer inquiries

Copyright © 2015 Pearson Education, Inc.

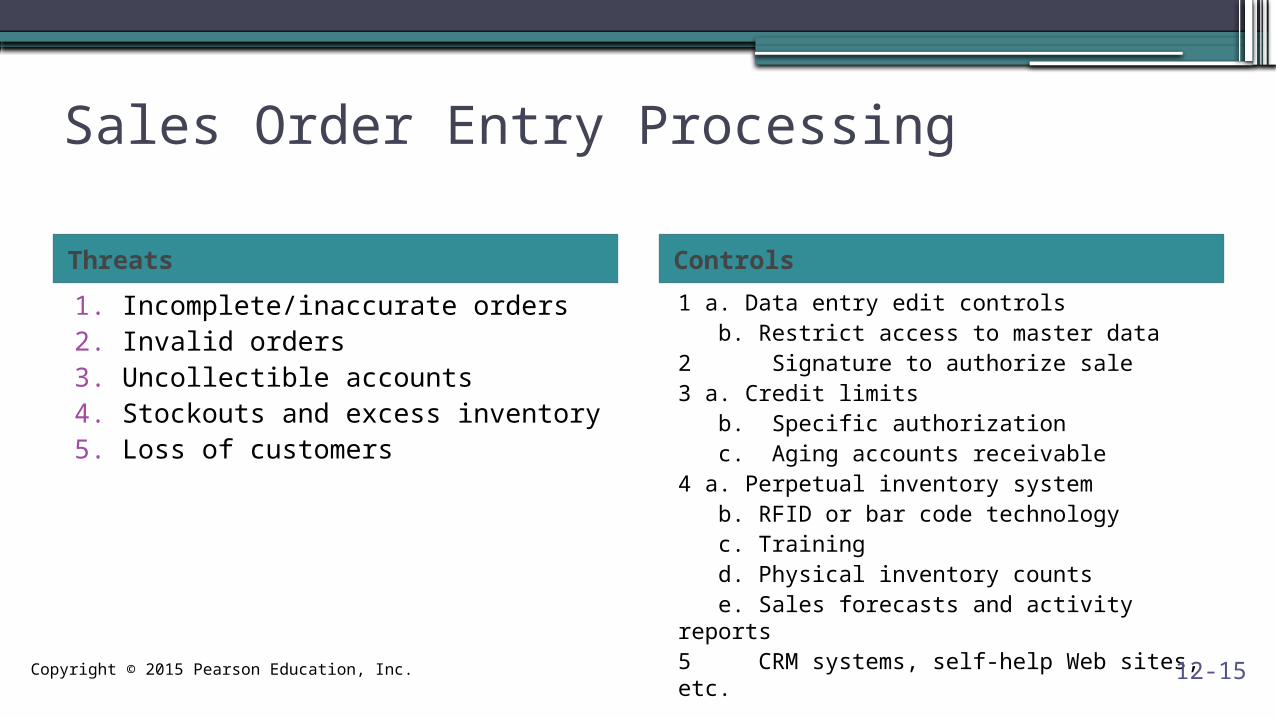

Sales Order Entry Processing

Threats Controls

1. Incomplete/inaccurate orders2. Invalid orders3. Uncollectible accounts4. Stockouts and excess inventory5. Loss of customers

1 a. Data entry edit controls b. Restrict access to master data 2 Signature to authorize sale3 a. Credit limits b. Specific authorization c. Aging accounts receivable4 a. Perpetual inventory system b. RFID or bar code technology c. Training d. Physical inventory counts e. Sales forecasts and activity reports5 CRM systems, self-help Web sites, etc.

12-15

Copyright © 2015 Pearson Education, Inc.

2. SHIPPING• The second basic activity in the revenue cycle is filling

customer orders and shipping the desired merchandise.

• The process consists of two steps▫Picking and packing the order (▫Shipping the order

• The warehouse department typically picks the order• The shipping departments packs and ships the order• Both functions include custody of inventory and

ultimately report to the VP of Manufacturing.Pick and pack the orderShip the order

Copyright © 2015 Pearson Education, Inc.

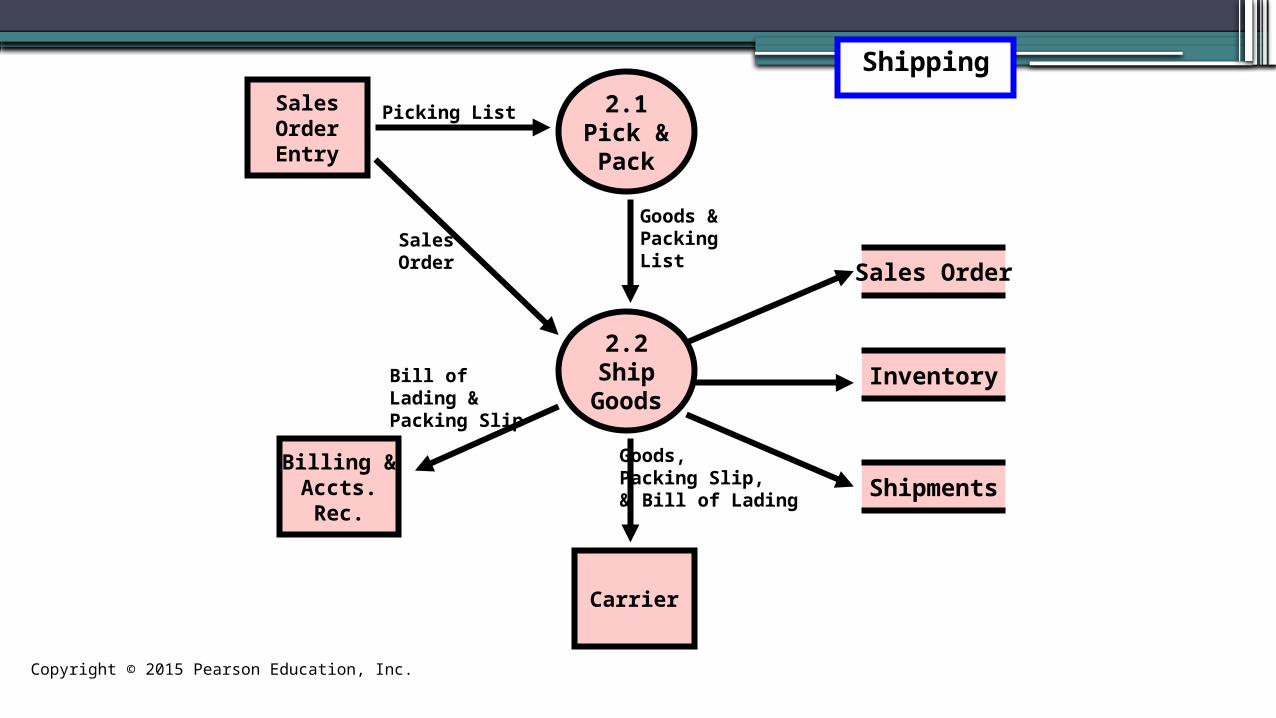

2.1Pick &Pack

Sales Order

2.2Ship

Goods

SalesOrderEntry

Shipping

Carrier

Inventory

ShipmentsBilling &Accts.Rec.

Picking List

Goods &PackingList

Goods,Packing Slip,& Bill of Lading

Bill ofLading &Packing Slip

SalesOrder

Copyright © 2015 Pearson Education, Inc.

2.1 Pick & pack the order•Source documents: picking ticket•A picking ticket is printed by sales order

entry and triggers the pick-and-pack process•The picking ticket identifies:

▫Which products to pick▫What quantity

•Warehouse workers record the quantities picked on the picking ticket, which may be a paper or electronic document.

•The picked inventory is then transferred to the shipping department.

Copyright © 2015 Pearson Education, Inc.

•Technology can speed the movement of inventory and improve the accuracy of perpetual inventory records:▫Bar code scanners▫Conveyer belts▫Wireless technology so workers can receive

instructions without returning to dispatch▫Radio frequency identification (RFID) tags:

Eliminate the need to align goods with scanner Allow inventory to be tracked as it moves through

warehouse Can store up to 128 bytes of data

2.1 Pick & pack the order

Copyright © 2015 Pearson Education, Inc.

•The shipping department compares the following quantities:▫Physical count of inventory▫Quantities indicated on picking ticket▫Quantities on sales order

•Discrepancies can arise if:▫Items weren’t stored in the location indicated▫Perpetual inventory records were inaccurate

•If there are discrepancies, a back order is initiated.

2.2 Ship goods

Copyright © 2015 Pearson Education, Inc.

•Source documents: Packing slip, Bill of lading•The clerk then records :

▫The sales order number▫The item numbers ordered▫The quantities shipped

•This information is used to:▫Update the quantity-on-hand field in the

inventory master file▫Produce a packing slip▫Produce multiple copies of the bill of lading

2.2 Ship goods

Copyright © 2015 Pearson Education, Inc.

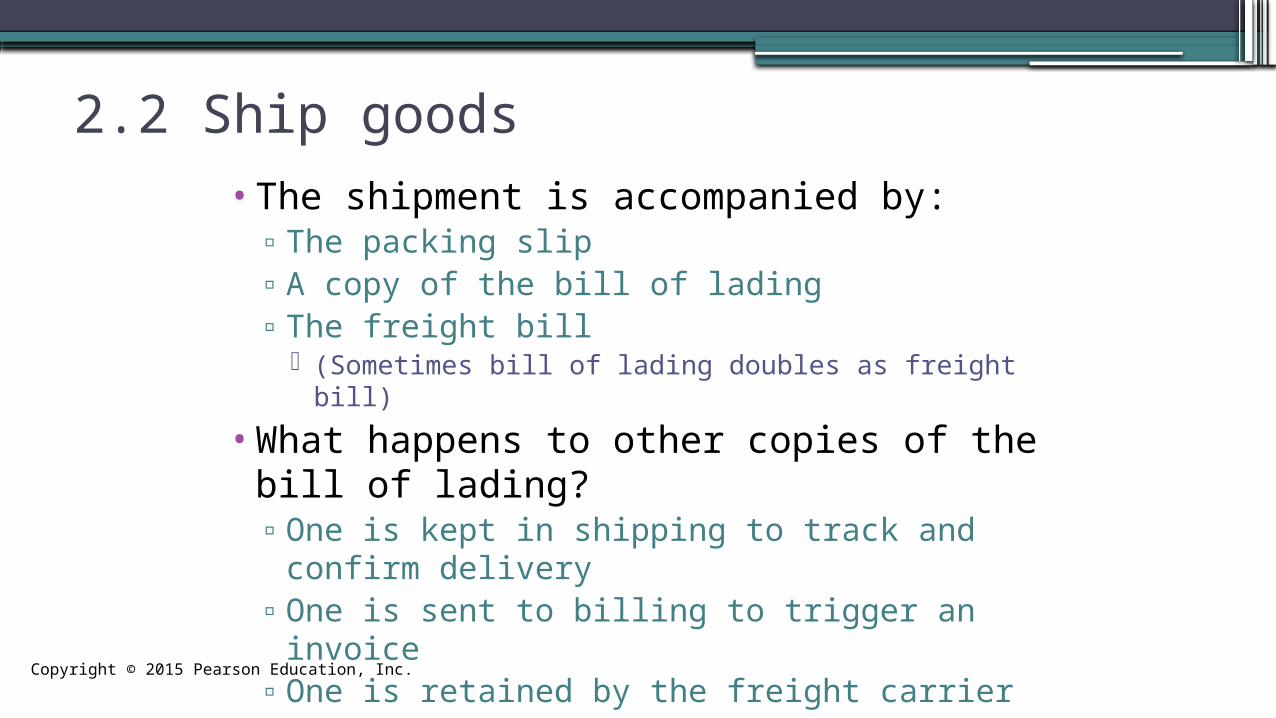

•The shipment is accompanied by:▫The packing slip▫A copy of the bill of lading▫The freight bill

(Sometimes bill of lading doubles as freight bill)

•What happens to other copies of the bill of lading?▫One is kept in shipping to track and confirm

delivery▫One is sent to billing to trigger an invoice▫One is retained by the freight carrier

2.2 Ship goods

Copyright © 2015 Pearson Education, Inc.

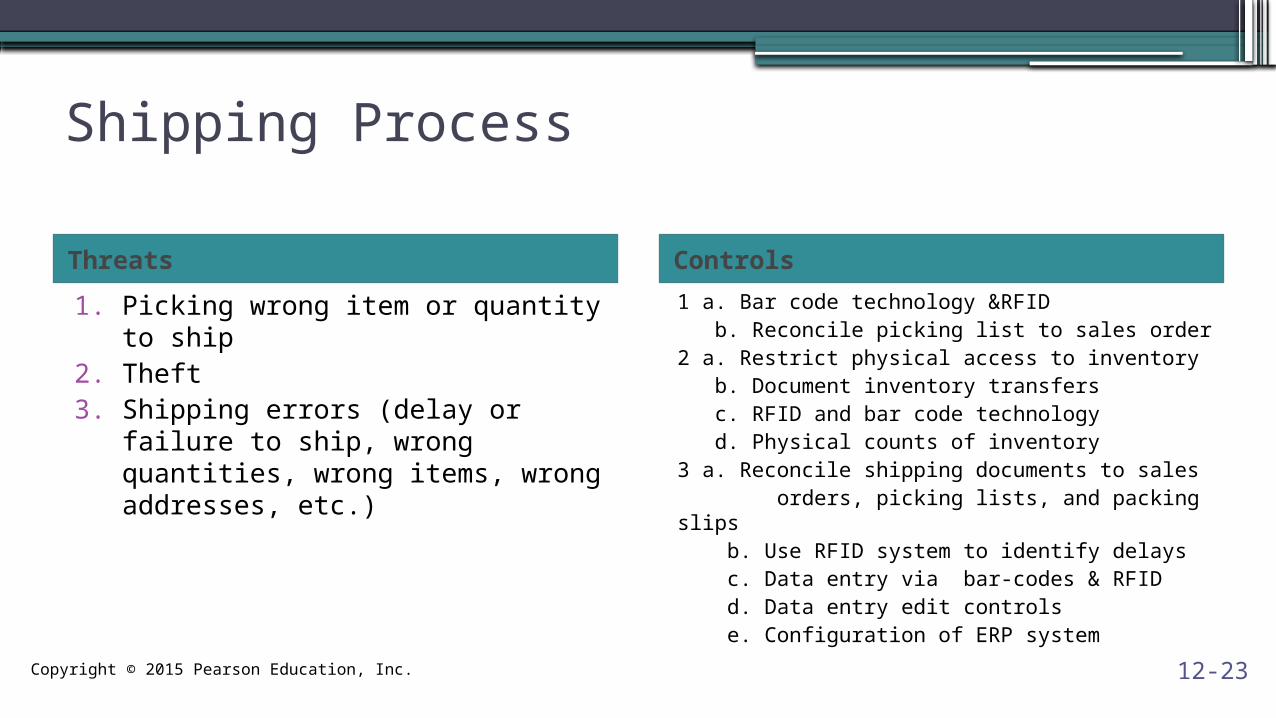

Shipping Process

Threats Controls

1. Picking wrong item or quantity to ship

2. Theft3. Shipping errors (delay or failure to

ship, wrong quantities, wrong items, wrong addresses, etc.)

1 a. Bar code technology &RFID b. Reconcile picking list to sales order2 a. Restrict physical access to inventory b. Document inventory transfers c. RFID and bar code technology d. Physical counts of inventory3 a. Reconcile shipping documents to sales orders, picking lists, and packing slips b. Use RFID system to identify delays c. Data entry via bar-codes & RFID d. Data entry edit controls e. Configuration of ERP system 12-23

Copyright © 2015 Pearson Education, Inc.

3. BILLING•The third revenue cycle activity is

billing customers.•This activity involves two tasks:

▫Invoicing/billing ▫Updating accounts receivable

Copyright © 2015 Pearson Education, Inc.

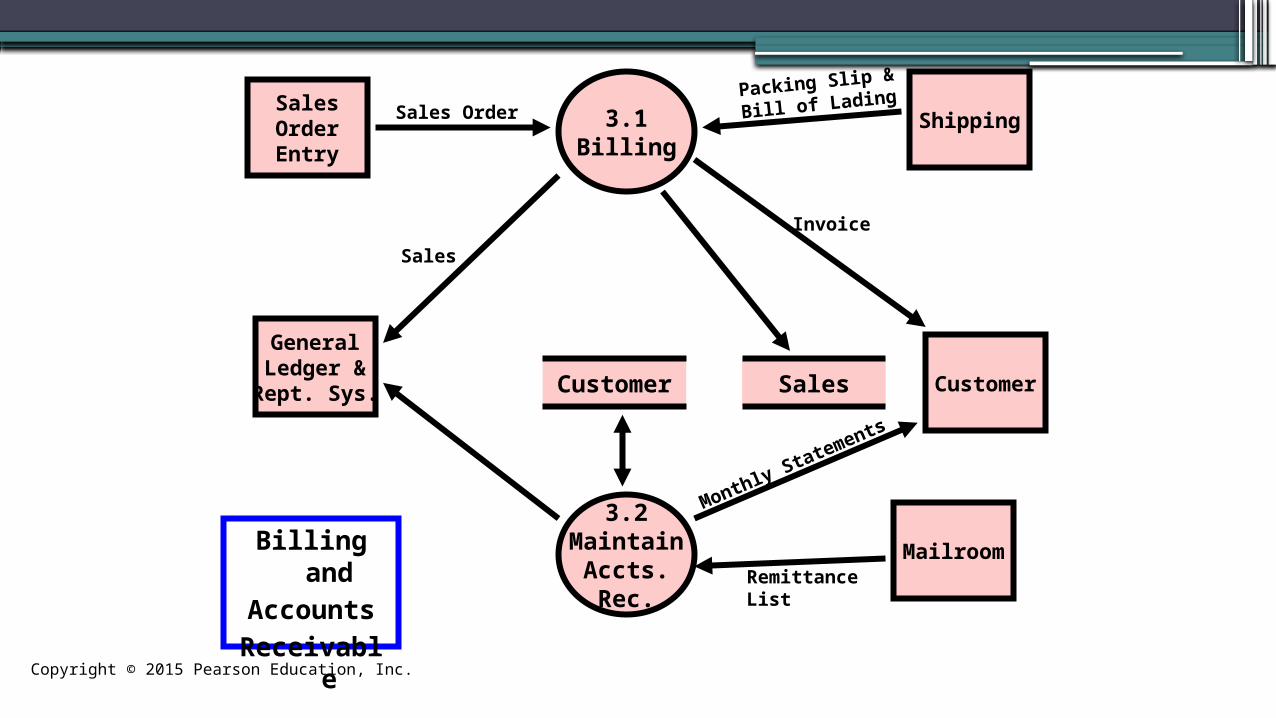

3.1Billing

Customer

3.2MaintainAccts.Rec.

SalesOrderEntry

Billing and

Accounts

Receivable

CustomerSales

GeneralLedger &Rept. Sys.

Shipping

Mailroom

Sales Order

Sales

Packing Slip &

Bill of Lading

Invoice

Monthly Statements

RemittanceList

Copyright © 2015 Pearson Education, Inc.

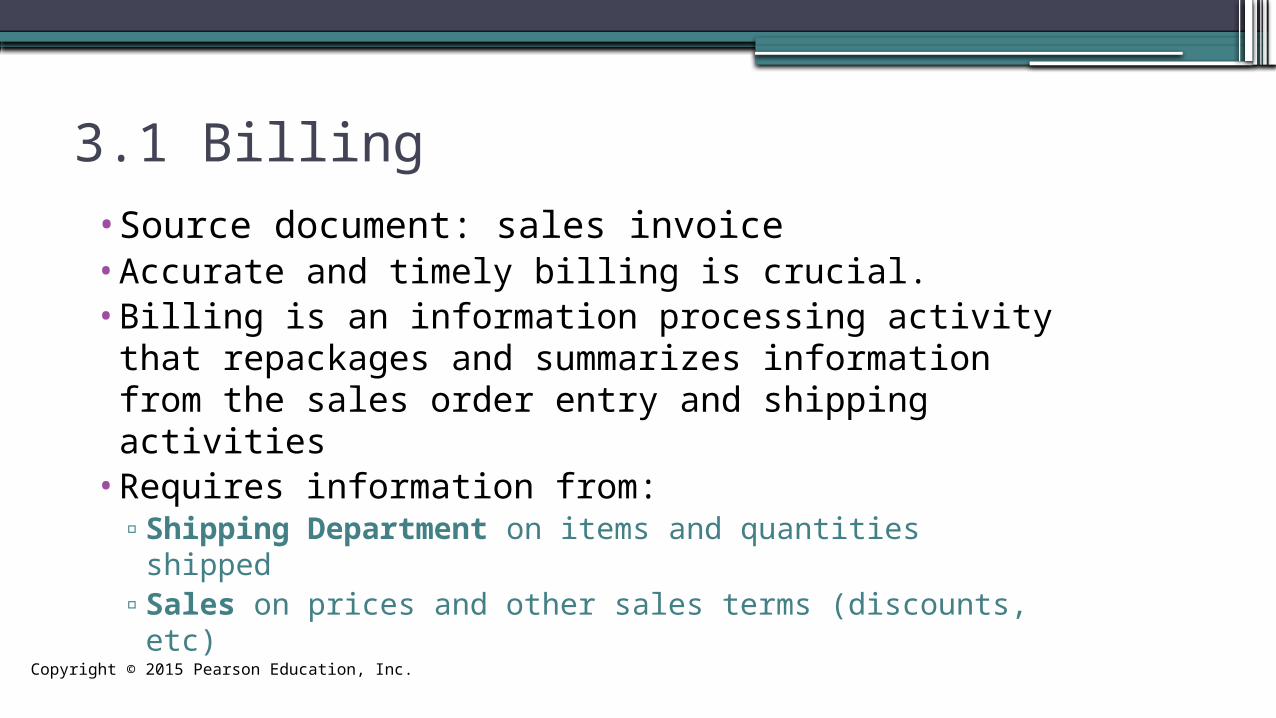

3.1 Billing•Source document: sales invoice•Accurate and timely billing is crucial.•Billing is an information processing activity that

repackages and summarizes information from the sales order entry and shipping activities

•Requires information from:▫Shipping Department on items and quantities

shipped▫Sales on prices and other sales terms (discounts, etc)

Copyright © 2015 Pearson Education, Inc.

•The basic document created is the sales invoice. The invoice notifies the customer of:▫The amount to be paid▫Where to send payment

•Invoices may be sent/received:▫In paper form▫By EDI

Common for larger companies Faster and cheaper than snail mail

3.1 Billing

Copyright © 2015 Pearson Education, Inc.

•When buyer and seller have accurate online systems:▫Invoicing process may be skipped

Seller sends an email when goods are shipped Buyer sends acknowledgment when goods are received Buyer automatically remits payments within a specified

number of days after receiving the goods▫Can produce substantial cost savings

3.1 Billing

Copyright © 2015 Pearson Education, Inc.

•Source document: credit memo and monthly statements

•The accounts receivable function reports to the controller

•This function performs two basic tasks▫Debits customer accounts for the amount the

customer is invoiced▫Credits customer accounts for the amount of

customer payments•Two basic ways to maintain accounts receivable:

▫Open-invoice method▫Balance forward method

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

•OPEN-INVOICE METHOD:▫Customers pay according to each invoice▫Two copies of the invoice are typically sent to the

customer Customer is asked to return one copy with payment This copy is a turnaround document called a remittance

advice▫Advantages of open-invoice method

Conducive to offering early-payment discounts Results in more uniform flow of cash collections

▫Disadvantages of open-invoice method More complex to maintain

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

•BALANCE FORWARD METHOD:▫Customers pay according to amount on their

monthly statement, rather than by invoice▫Monthly statement lists transactions since the

last statement and lists the current balance The tear-off portion includes pre-printed information

with customer name, account number, and balance Customers are asked to return the stub, which serves as

the remittance advice Remittances are applied against the total balance rather

than against a specific invoice

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

•Cycle billing is commonly used with the balance-forward method▫Monthly statements are prepared for subsets of

customers at different times. EXAMPLE: Bill customers according to the following

schedule: 1st week of month—Last names beginning with A-F 2nd week of month—Last names beginning with G-M 3rd week of month—Last names beginning with N-S 4th week of month—Last names beginning with T-Z

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

• Image processing can improve the efficiency and effectiveness of managing customer accounts.▫Digital images of customer remittances and accounts

are stored electronically•Advantages:

▫Fast, easy retrieval▫Copy of document can be instantly transmitted to

customer or others▫Multiple people can view document at once▫Drastically reduces document storage space

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

•EXCEPTION PROCEDURES: ACCOUNT ADJUSTMENTS AND WRITE-OFFS:▫Adjustments to customer accounts may need to be

made for: Returns Allowances for damaged goods Write-offs as uncollectible

▫These adjustments are handled by the credit manager

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

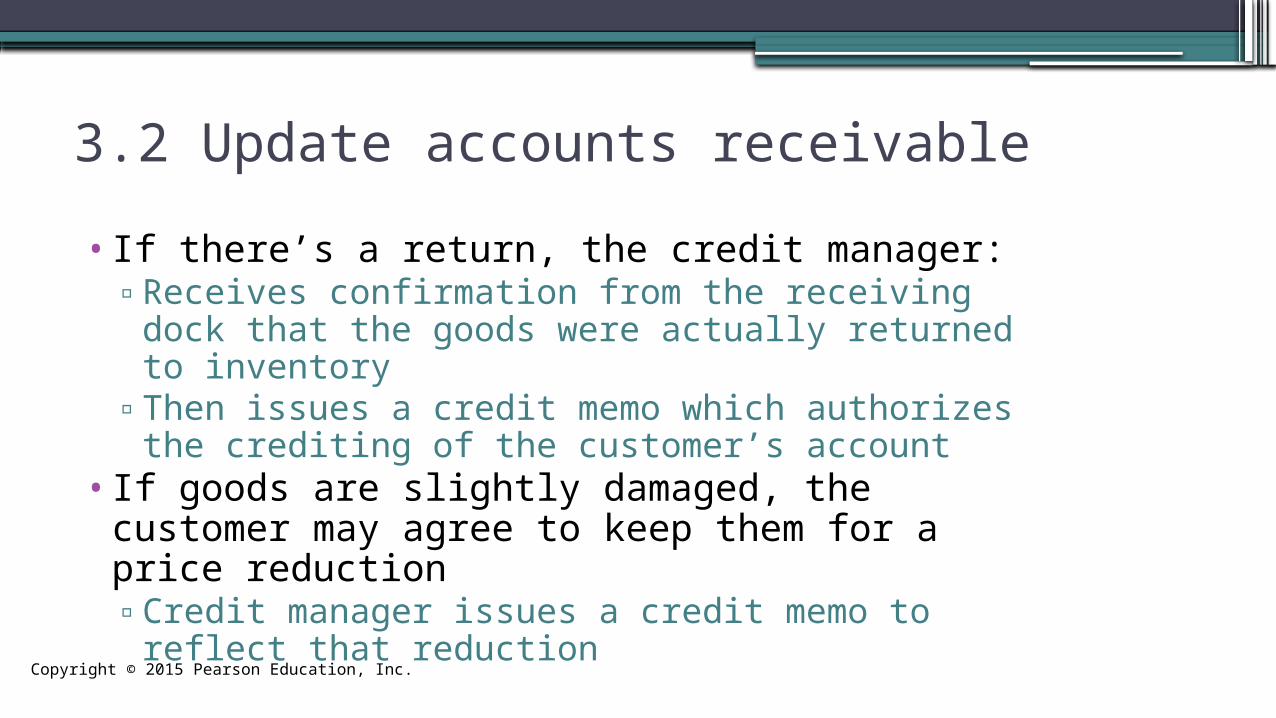

•If there’s a return, the credit manager:▫Receives confirmation from the receiving dock that

the goods were actually returned to inventory▫Then issues a credit memo which authorizes the

crediting of the customer’s account•If goods are slightly damaged, the customer may

agree to keep them for a price reduction▫Credit manager issues a credit memo to reflect that

reduction

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

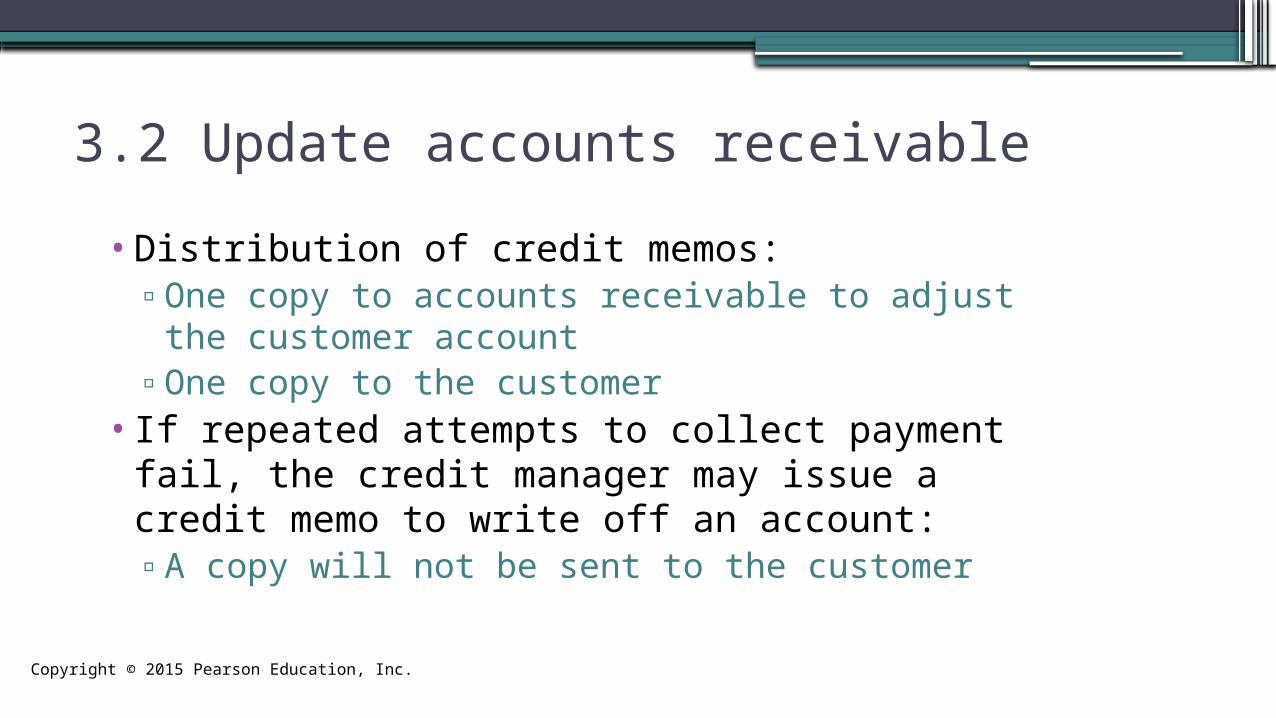

•Distribution of credit memos:▫One copy to accounts receivable to adjust the

customer account▫One copy to the customer

•If repeated attempts to collect payment fail, the credit manager may issue a credit memo to write off an account:▫A copy will not be sent to the customer

3.2 Update accounts receivable

Copyright © 2015 Pearson Education, Inc.

Billing Process

Threats Controls

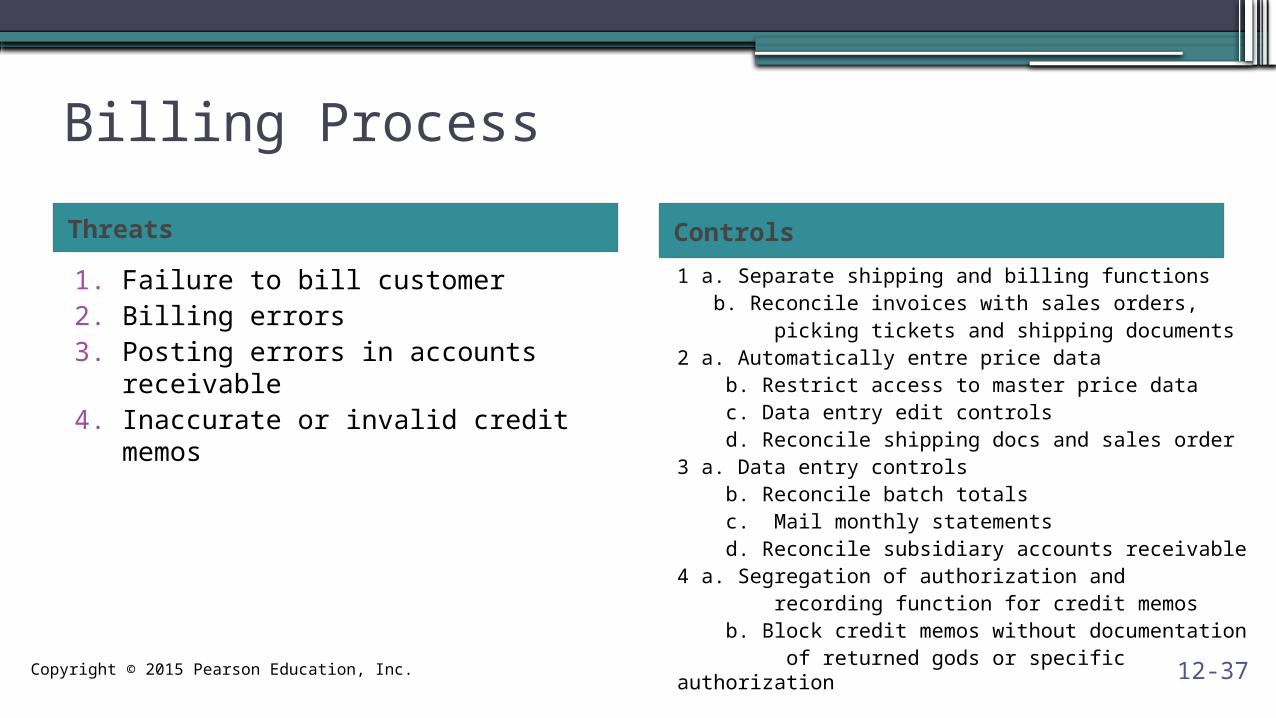

1. Failure to bill customer2. Billing errors3. Posting errors in accounts

receivable4. Inaccurate or invalid credit memos

1 a. Separate shipping and billing functions b. Reconcile invoices with sales orders, picking tickets and shipping documents2 a. Automatically entre price data b. Restrict access to master price data c. Data entry edit controls d. Reconcile shipping docs and sales order3 a. Data entry controls b. Reconcile batch totals c. Mail monthly statements d. Reconcile subsidiary accounts receivable4 a. Segregation of authorization and recording function for credit memos b. Block credit memos without documentation of returned gods or specific authorization

12-37

Copyright © 2015 Pearson Education, Inc.

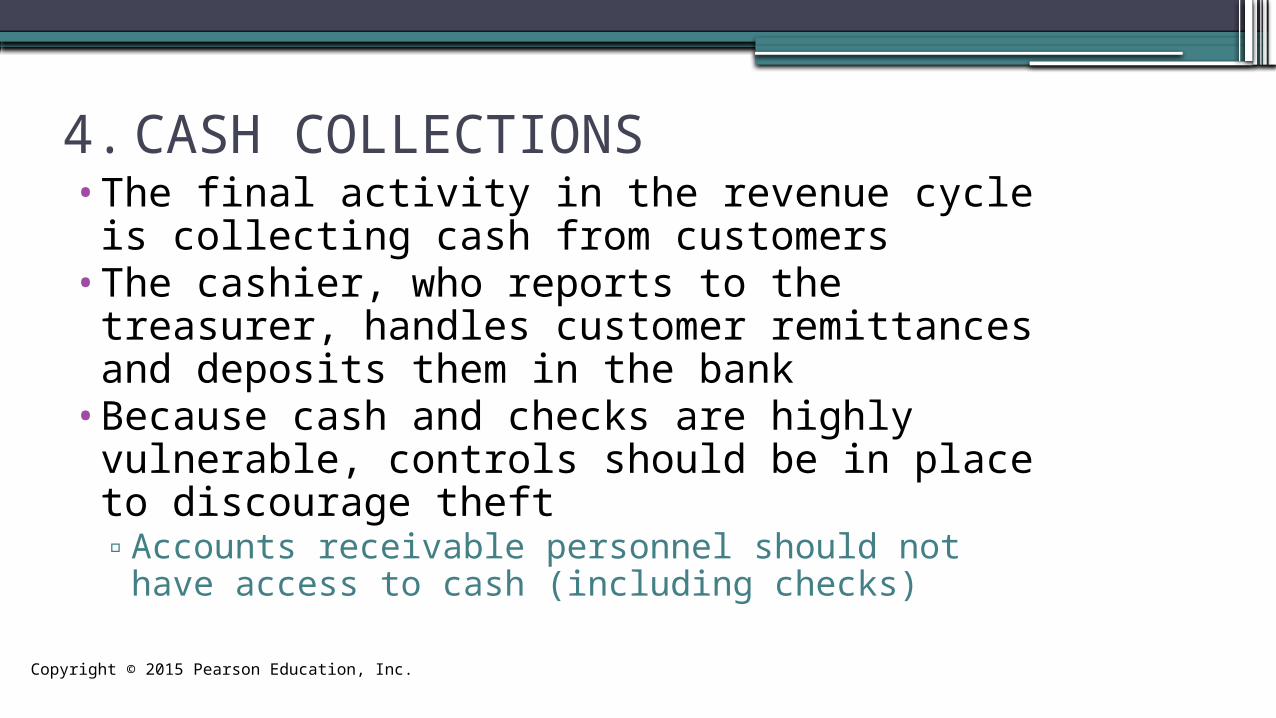

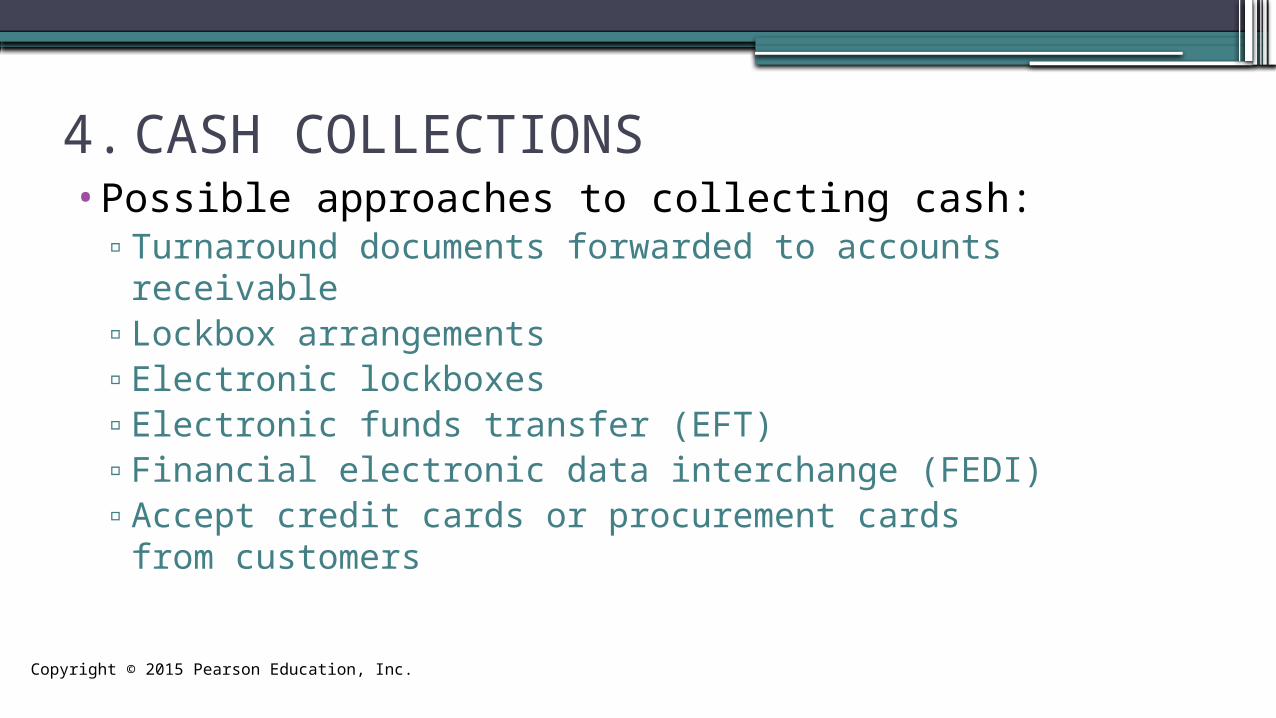

4. CASH COLLECTIONS•The final activity in the revenue cycle is

collecting cash from customers•The cashier, who reports to the treasurer,

handles customer remittances and deposits them in the bank

•Because cash and checks are highly vulnerable, controls should be in place to discourage theft▫Accounts receivable personnel should not have

access to cash (including checks)

Copyright © 2015 Pearson Education, Inc.

•Possible approaches to collecting cash:▫Turnaround documents forwarded to accounts

receivable▫Lockbox arrangements▫Electronic lockboxes▫Electronic funds transfer (EFT)▫Financial electronic data interchange (FEDI)▫Accept credit cards or procurement cards from

customers

4. CASH COLLECTIONS

Copyright © 2015 Pearson Education, Inc.

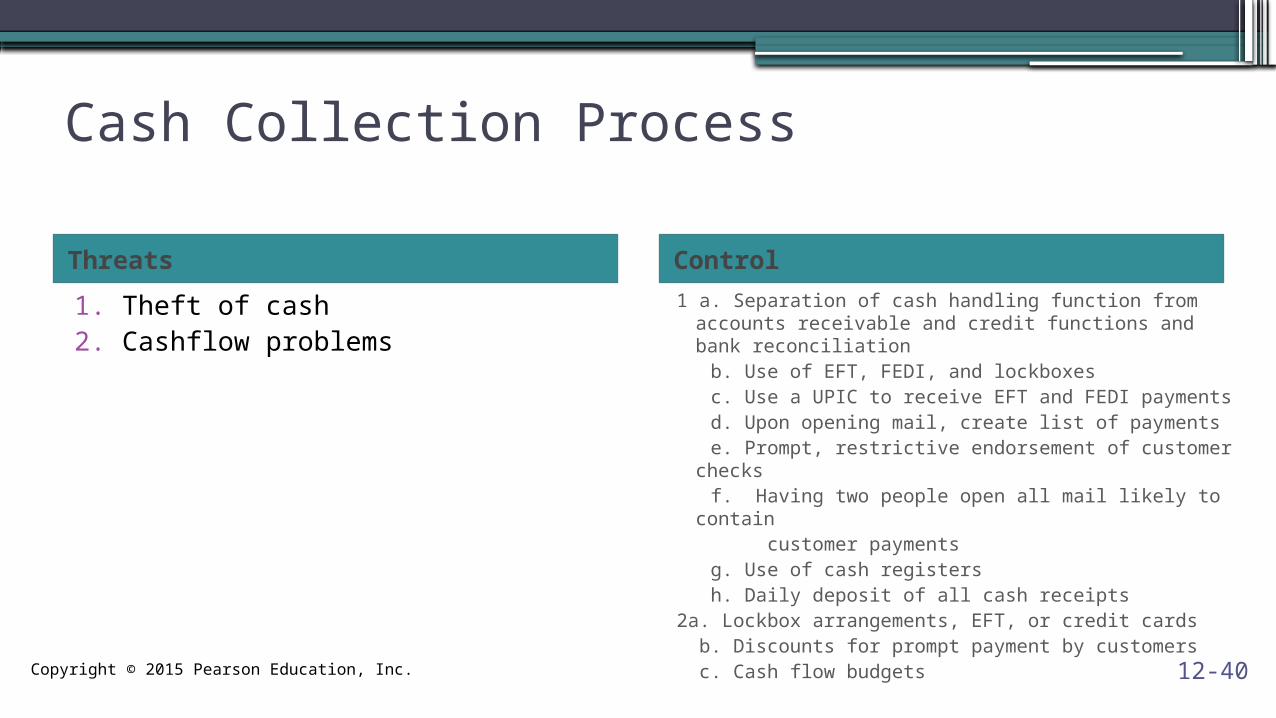

Cash Collection Process

Threats Control

1. Theft of cash2. Cashflow problems

1 a. Separation of cash handling function from accounts receivable and credit functions and bank reconciliation

b. Use of EFT, FEDI, and lockboxes c. Use a UPIC to receive EFT and FEDI payments d. Upon opening mail, create list of payments e. Prompt, restrictive endorsement of customer

checks f. Having two people open all mail likely to contain customer payments g. Use of cash registers h. Daily deposit of all cash receipts2a. Lockbox arrangements, EFT, or credit cards b. Discounts for prompt payment by customers c. Cash flow budgets 12-40