Copyright © 2003 McGraw Hill Ryerson Limited 20-1 prepared by: Carol Edwards BA, MBA, CFA...

41

copyright © 2003 McGraw Hill Ryerson Limited 20-1 prepared by: Carol Edwards BA, MBA, CFA Instructor, Finance British Columbia Institute of Technology Fundamentals of Corporate Finance Second Canadian Edition

-

Upload

dominick-hubbard -

Category

Documents

-

view

213 -

download

0

Transcript of Copyright © 2003 McGraw Hill Ryerson Limited 20-1 prepared by: Carol Edwards BA, MBA, CFA...

copyright © 2003 McGraw Hill Ryerson Limited

20-120-1

prepared by:Carol EdwardsBA, MBA, CFA

Instructor, FinanceBritish Columbia Institute of Technology

Fundamentals

of Corporate

Finance

Second Canadian Edition

copyright © 2003 McGraw Hill Ryerson Limited

20-220-2

Chapter 20Cash and Inventory Management

Chapter Outline Cash Collection, Disbursement and Float Canada’s Payment System Managing Float Inventories and Cash Management

copyright © 2003 McGraw Hill Ryerson Limited

20-320-3

Collection, Disbursement & Float• Float

Time exists between the moment a check is written and the moment funds are deposited in the recipient’s account.

This time spread is called the float.Payment float occurs because a firm has

written a cheque, but it has not yet cleared the bank.

Availability float occurs because a firm has deposited cheques to its account, but they have not yet been cleared.

Net Float is the difference between the payment float and the availability float.

copyright © 2003 McGraw Hill Ryerson Limited

20-420-4

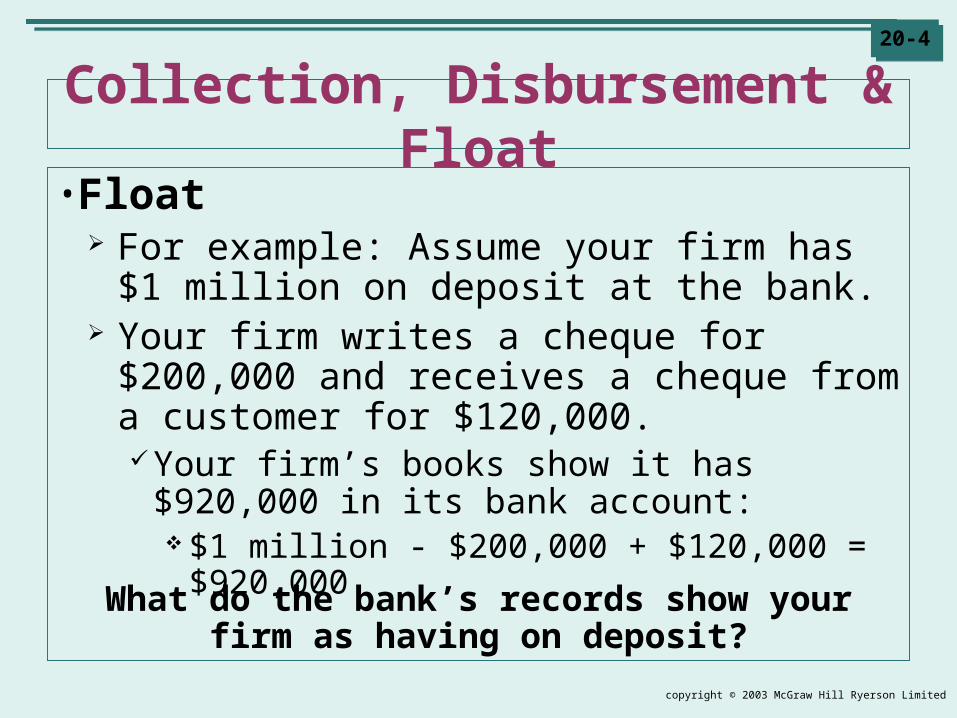

Collection, Disbursement & Float• Float

For example: Assume your firm has $1 million on deposit at the bank.

Your firm writes a cheque for $200,000 and receives a cheque from a customer for $120,000.Your firm’s books show it has $920,000 in its

bank account: $1 million - $200,000 + $120,000 = $920,000

What do the bank’s records show yourfirm as having on deposit?

copyright © 2003 McGraw Hill Ryerson Limited

20-520-5

Collection, Disbursement & Float•Float

Your bank is unaware of either cheque. The cheque your firm wrote has not

cleared its account.The cheque your firm received has not

cleared its account either. Thus, the bank shows your account as

having $1 million.

copyright © 2003 McGraw Hill Ryerson Limited

20-620-6

Collection, Disbursement & Float•Float

The difference between the balance on your books and the balance at the bank is $80,000 in your firm’s favour.That is, your firm actually should have a

balance of $920,000 in its account.But because of time delays in processing

paper cheques, your firm actually gets the use of $1 million.

copyright © 2003 McGraw Hill Ryerson Limited

20-720-7

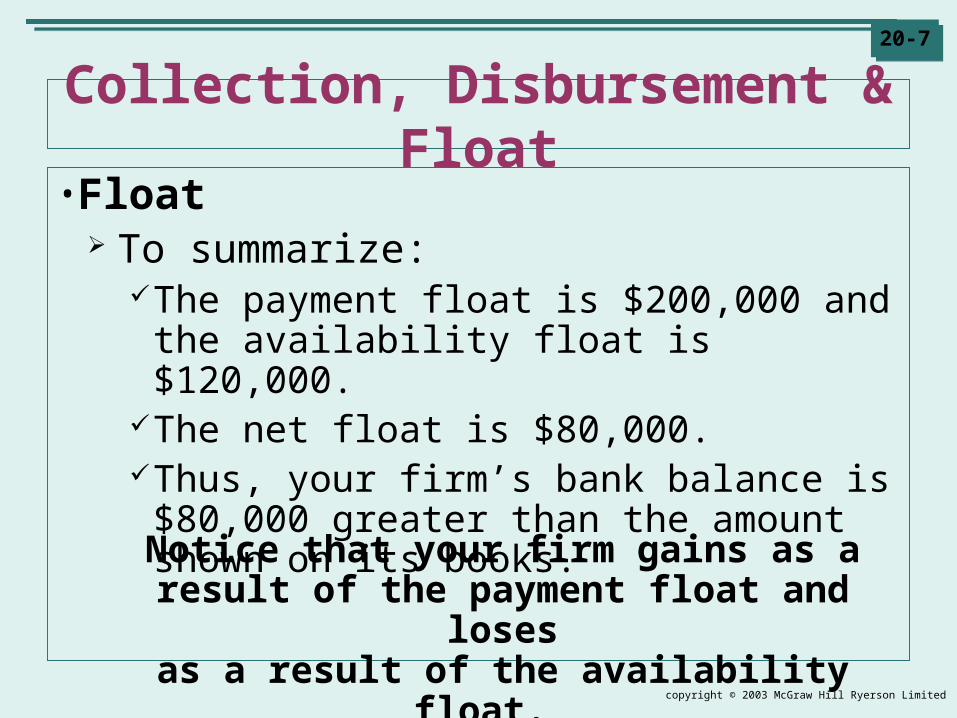

Collection, Disbursement & Float• Float

To summarize:The payment float is $200,000 and the

availability float is $120,000.The net float is $80,000.Thus, your firm’s bank balance is $80,000

greater than the amount shown on its books.

Notice that your firm gains as aresult of the payment float and losesas a result of the availability float.

copyright © 2003 McGraw Hill Ryerson Limited

20-820-8

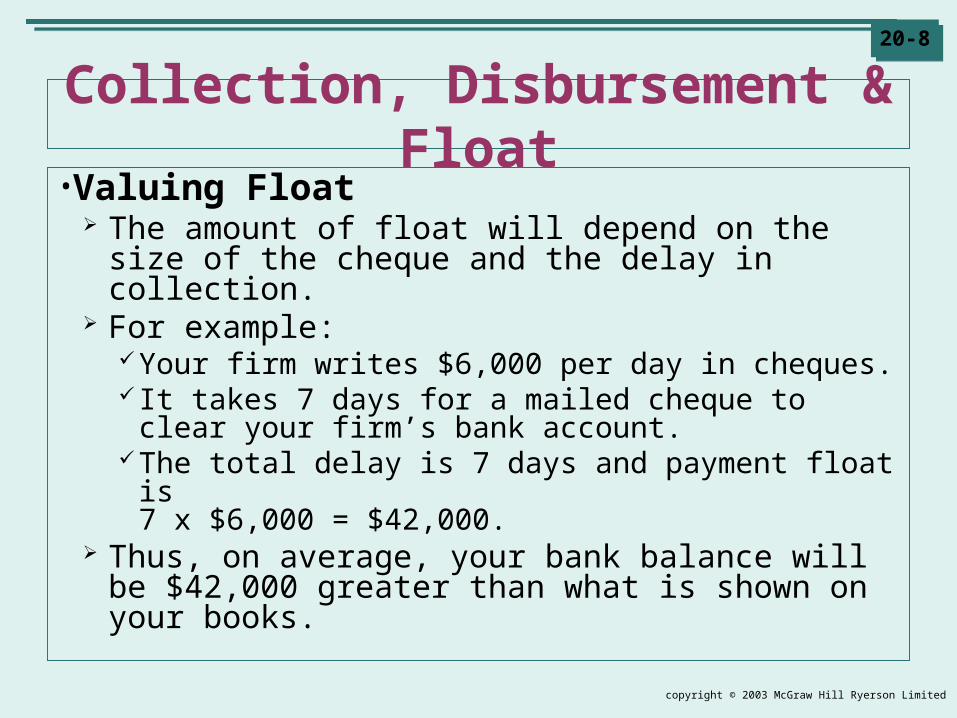

Collection, Disbursement & Float• Valuing Float

The amount of float will depend on the size of the cheque and the delay in collection.

For example:Your firm writes $6,000 per day in cheques. It takes 7 days for a mailed cheque to clear your

firm’s bank account.The total delay is 7 days and payment float is

7 x $6,000 = $42,000. Thus, on average, your bank balance will be

$42,000 greater than what is shown on your books.

copyright © 2003 McGraw Hill Ryerson Limited

20-920-9

Collection, Disbursement & Float•Valuing Float

As a financial manager, you would like to increase the payment float available to your firm and decrease the availability float. For example, if you know it will take a

week to process cheques to suppliers, your firm can get by on a smaller cash balance.

The smaller the cash balance, the more funds your firm can hold in interest paying investments.

copyright © 2003 McGraw Hill Ryerson Limited

20-1020-10

Collection, Disbursement & Float• Playing the Float

Playing the float is the process of accelerating your deposits and delaying your payments so as to generate more float.

But be careful!Playing the float too aggressively and writing

cheques on your account for the sole purpose of creating float and earning interest is illegal.

This behaviour is known as cheque kiting.

copyright © 2003 McGraw Hill Ryerson Limited

20-1120-11

Canada’s Payments System• How Cheques are Cleared

Every day, Canadians use banking machines, cheques, debit cards and preauthorized payments to make payments totalling $127 billion.

Canada’s payments system lays down the rules and procedures which guide the clearing, exchange and settling of all types of payments.

The system is run by the Canada Payments Association (CPA), a non-profit organization.

Its members are financial institutions that take cheques and offer deposit facilities.

copyright © 2003 McGraw Hill Ryerson Limited

20-1220-12

Canada’s Payments System•How Cheques are Cleared

The CPA runs the Automated Clearing Settlement System (ACSS) and the Large Value Transfer System (LVTS).ACSS handles cheques and certain types

of automated payments.LVTS, introduced in 1999, is an electronic

wire transfer system.

copyright © 2003 McGraw Hill Ryerson Limited

20-1320-13

Canada’s Payments System• How Payments are Cleared

There are three steps in the process of clearing and settling payments:1. Payment by cheque, debit card, direct deposit,

or other means.2. Clearing, or the daily process by which the

CPA members exchange deposited payment items and then determine the net amounts due each other.

3. Settlement, or the procedure by which CPA members use funds on deposit at the Bank of Canada to meet their net payment obligations to other member institutions.

copyright © 2003 McGraw Hill Ryerson Limited

20-1420-14

Canada’s Payments System• How Cheques are Cleared

Canadians usually receive credit immediately for the cheques they deposit, even if the cheque is from the other side of the country.

This is not so in the US and other countries, where it can take several days before a bank will clear a cheque through the client’s account.

As a consequence, Canadian financial managers have significantly fewer opportunities to manage their firm’s float than US managers do!

copyright © 2003 McGraw Hill Ryerson Limited

20-1520-15

Managing Float• Creating and Managing Float

Payers attempt to create delays in the check clearing process so that they can use their cash for longer.

Recipients attempt to remove delays in the check clearing process to get available cash sooner.

Note that delays which help the payer, hurt the recipient.

copyright © 2003 McGraw Hill Ryerson Limited

20-1620-16

Managing Float• Creating and Managing Float

There are three sources of float which a company can manage to increase (decrease) the time it takes a cheque to clear the system:Mail Float – the time it takes to mail a cheque.Processing Float – the time it takes the

company to process the cheque upon receipt.Clearing Float – the time it takes the bank to

clear the cheque and adjust the firm’s account. The sum of these three sources of delay is the

collection time.

copyright © 2003 McGraw Hill Ryerson Limited

20-1720-17

Managing Float• Speeding Up Collections

There are a number of methods your firm can institute for speeding up its collections:Concentration Banking is a system whereby

customers, instead of sending cheques to the company, send them to a regional collection centre. This centre transfers funds to the firm’s bank.

Lock Box System is a system whereby customers send payments to a post office box. A local bank collects and processes the cheques

for your firm.

copyright © 2003 McGraw Hill Ryerson Limited

20-1820-18

Managing Float•Speeding Up Collections

Zero-Balance Accounts are regional bank accounts to which just enough funds are transferred daily to pay each day’s bills.

Note that there are costs and benefits of implementing any of the above systems.Thus, the firm’s financial manager must

perform an analysis to determine if the benefits of implementing offset the costs.

copyright © 2003 McGraw Hill Ryerson Limited

20-1920-19

Managing Float•Electronic Payments and Receipts

More firms are giving up paper and conducting their business electronically.

Electronic Funds Transfer (EFT) is payments made electronically instead of using paper-based cheques.

Electronic Data Interchange (EDI) involves direct electronic information exchange between enterprises, eliminating the mailing and handling of paper invoices.

copyright © 2003 McGraw Hill Ryerson Limited

20-2020-20

Managing Float•Electronic Payments and Receipts

Debit Cards involve an ATM card (automated-teller-machine card) which allows retail customers to transfer funds directly from their bank accounts to the retailer’s account.

Preauthorized Payments or Preauthorized Debits (PADs) involve a customer authorizing a bank to pay his/her bills automatically, instead of the customer writing a cheque.

copyright © 2003 McGraw Hill Ryerson Limited

20-2120-21

Managing Float•Electronic Payments and Receipts

There are several advantages of conducting business electronically:Record keeping and routine transactions

are easily automated, reducing time and processing costs.

The cost of such transactions is very low.Money moves instantly, and so float is

drastically reduced, which can generate considerable savings.

copyright © 2003 McGraw Hill Ryerson Limited

20-2220-22

Inventories and Cash Balances• How Much Cash Should a Firm Hold?

You now know some of the tricks of managing your firm’s cash inflows and outflows.

However, how much cash should your firm keep on hand?Remember, cash pays no interest, so holding

cash will be a drag on your firm’s performance.However, investing all your firm’s cash in

securities, while it generates a return for the firm, also involves a cost: If the firm has to pay a bill, it must liquidate a

security and incur transactions costs.

copyright © 2003 McGraw Hill Ryerson Limited

20-2320-23

Inventories and Cash Balances• How Much Cash Should a Firm Hold?

The art of cash management involves balancing the costs and benefits.

Financial managers long ago recognized that holding an “inventory of cash” is like holding an inventory of materials.That is, cash is just another material used in the

production process.Thus, it involves similar costs and benefits.

Holding excess inventory (or cash) is costly; conversely, holding too little is also costly.

The key question, then is, “What is the right amount of inventory (or cash) to hold?”

copyright © 2003 McGraw Hill Ryerson Limited

20-2420-24

Inventories and Cash Balances•Managing Inventories

There are two costs associated with inventory:Order costs – administrative and delivery

charges associated with ordering inventory.Carrying Cost – costs associated with

holding and storing inventory: The cost of space, insurance, losses due to

theft or spoilage and the opportunity cost of the capital tied up in inventory which could have been invested elsewhere.

copyright © 2003 McGraw Hill Ryerson Limited

20-2520-25

Inventories and Cash Balances

•Managing Inventories The inventory problem comes down to

balancing these two costs:As the firm increases its order size, the number of orders falls and therefore the order costs decline.

However, larger orders means an increased inventory size and higher carrying costs.

copyright © 2003 McGraw Hill Ryerson Limited

20-2620-26

Inventories and Cash Balances

•Managing Inventories If you look at Table 20.2 on page 616

of your text, you will see this trade-off numerically depicted for a sample company.

Look at the carrying costs and the order costs.

What is the optimal ordersize for this firm?

copyright © 2003 McGraw Hill Ryerson Limited

20-2720-27

Inventories and Cash Balances•Managing Inventories

The optimal order size for this firm is 60,000 bricks.At this order size, the total costs (order

costs plus carrying costs) are minimized at $3,000.

However, creating a table like Table 20.2 to find the minimum total costs is a slow way to calculate the optimal order size.

Is there an easier way?

copyright © 2003 McGraw Hill Ryerson Limited

20-2820-28

Inventories and Cash Balances•Managing Inventories

You can calculate the Economic Order Quantity (EOQ) using the formula below:

EOQ = 2 x Annual Sales x Cost per Order

Carrying Cost The EOQ is the order size which minimizes

the total inventory costs.

copyright © 2003 McGraw Hill Ryerson Limited

20-2920-29

Inventories and Cash Balances• Managing Inventories

For our example, sales are 1 million bricks, order costs are $90, carrying costs are $0.05 per brick.

EOQ = 2 x Annual Sales x Cost per Order

Carrying Cost

Note this is the same answer as from Table 20.2.

= 2 x 1 million x $90

0.05 = 60,000 bricks

copyright © 2003 McGraw Hill Ryerson Limited

20-3020-30

Inventories and Cash Balances•Managing Inventories

The EOQ model you have been presented with is much simplified.There are numerous refinements which

could be made to make it more accurate.

However, these refinements should not hide the important message that the firm needs to balance its carrying costs and order costs.

copyright © 2003 McGraw Hill Ryerson Limited

20-3120-31

Inventories and Cash Balances

•Managing Inventories Carrying costs include the costs of

storing the goods and the cost of the capital tied up in inventory.

So when storage costs or interest rates are high, inventory levels should be kept low.

When the costs of restocking are high, then inventory should also be high.

copyright © 2003 McGraw Hill Ryerson Limited

20-3220-32

Inventories and Cash Balances•Managing Inventories of Cash

This inventory model can also be applied to the management of cash balances.

That is, the cash management problem is just like the inventory problem, but with a redefinition of the variables:Instead of order costs, the firm has

transactions costs when it sells securities to raise cash.

Interest rates replace carrying costs.Total cash outflows takes the place of annual

sales.

copyright © 2003 McGraw Hill Ryerson Limited

20-3320-33

Inventories and Cash Balances•Managing Inventories of Cash

You can calculate the Initial Cash Balance using the formula below:

Initial Cash Balance =

2 x Annual Cash Outflows x Cost per Sale of Security

Interest Rate

copyright © 2003 McGraw Hill Ryerson Limited

20-3420-34

Inventories and Cash Balances

•Managing Inventories of Cash Thus, the initial cash balance will be

higher if annual cash outflows are large and when the cost of selling a security is high.

Conversely, it will be lower when interest rates are high.

copyright © 2003 McGraw Hill Ryerson Limited

20-3520-35

Inventories and Cash Balances•Managing Inventories of Cash

Like the EOQ model, this model is much simplified.

Other more elaborate and realistic models have been developed which will allow a firm to more accurately manage its cash balances.

Bear in mind that it would be very inefficient to try to manage all of a firm’s cash flows. It would use up too much of management’s time

for the benefits received.

copyright © 2003 McGraw Hill Ryerson Limited

20-3620-36

Inventories and Cash Balances•Managing Inventories of Cash

Thus, you want to think of cash management rules and models as helping you to understand the problems of cash management.

Generally, though, they are not used for day-to-day management.

Such rules probably could not yield the savings resulting from a manager’s good judgment.Providing, that is, that the manager understands

the trade-offs which have been discussed.

copyright © 2003 McGraw Hill Ryerson Limited

20-3720-37

Investing Idle Cash• The Money Market

The money market is the market for short-term securities.

Firms use the money market to invest temporary idle cash balances, so as to earn a safe return on them.

These markets offer securities withShort maturities.Low risk.High liquidity.

copyright © 2003 McGraw Hill Ryerson Limited

20-3820-38

Investing Idle Cash• The Money Market

Some of the securities available in the money market are:Treasury bills.Commercial paper.Certificates of Deposit (CD’s).Repurchase Agreements (Repos or buybacks).

copyright © 2003 McGraw Hill Ryerson Limited

20-3920-39

Summary of Chapter 20 The cash balance on your firm’s books will not

match the balance in its bank account. When your firm writes a cheque, it takes time for

your balance to be adjusted downward.This is called payment float.

Conversely, when your firm receives a cheque, it takes time for its balance to be adjusted upward.

This is called availability float. The net float is the difference between the

payment float and the availability float.

copyright © 2003 McGraw Hill Ryerson Limited

20-4020-40

Summary of Chapter 20 If you can play the float, your firm can hold

smaller cash balances and earn interest on the extra cash it can invest.

There are a number of methods firms can use to manage their float, including concentration banking, lock-box banking and zero-balance accounts.

There are costs and benefits of having inventory.

The costs include carrying costs and ordering costs.

copyright © 2003 McGraw Hill Ryerson Limited

20-4120-41

Summary of Chapter 20 The EOQ model allows you to find the order

size of inventory which minimizes the costs of having inventory.

Cash, like inventory, can be managed so as to minimize the costs associated with holding it.

If a firm has temporary idle balances of cash, it may invest them in the money market.

The money market offers short-term, low risk and highly liquid securities.

This makes them ideal investments in which to invest funds for short periods of time before cash is needed.