Lets Talk Trash Abigail Dahlberg [email protected] @thegreenerword.

Upload

angelica-conleyCategory

view

217download

4

Coop Trends In EuropeHans Dahlberg

National Conference on Cooperative Development in IndiaNew Dehli

December 2007

The list…

• Revenue almost 1 trillion USD

• Compared to last year (11% real growth ignoring currency fluctuations)

• Largely confirms total in first ranking

• Need a variety of ways of showcasing co-operative performance and achievements

(G10)The 10 Biggest Economies in the World

9831,124 1,106

1,7191,910

2,1132,197

4,672

2,800

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

USA Japan Germany UK France China Italy Spain Canada Global300

12,452

South America0.4%

Asia - Pacific21%

Europe62%

North America17%

Global 300 by Region

Insurance23% Consumer

26%

Food & Agri 30%

Banks16%

All Others5%

Global 300 by Sector

Cooperatives & mutuals are sustainable businesses…

Name Coun-try

Sector Year of establishment

Unive NL Insurance 1794Alte Leipziger Hallesche DE Insurance 1819Gothaer DE Insurance 1820Mobiliar CH Insurance 1826AGIS NL Insurance 1827MMA FR Insurance 1828Suedzucker DE Food & Agri 1837Liverpool Victoria UK Insurance 1843East Of England UK Consumer 1844Nationwide Building Society UK Banks 1848

… But …

# Cooperative Orig Sector Structure

Turnover (€)

Date Share Price (€m)

Initiative Deal motivation

1 Cebeco Group NL Sup&Mark Fed 3,911>623 Nov97 34/16% 68 Coop C: Injection need2 Sodiaal: Yoplait FR Dairy Fed 824 May02 50% 175? Coop C: Injection need3 Pro-Fac: Agrilink USA Fruit Prim 712 Aug02 56% 814 Coop C: Debt4 Nilza BR Dairy Fed 60 Nov04 55% ? Coop C: Debts5 Golden Circle AU Fruit Prim 220 Mar05 20% 27 Coop C: Debts6 Capsa ES Dairy Prim 686 Jan06 57% 300 PE-fund PE: Profitable?7 Fonterra NZ Dairy Prim 6,462 Sep06 0.4% 12 PE-fund PE: Profitable8 Aveve: Q-Bakeries BE Supply Prim 56 Oct06 100% ? Coop? C: Cash?9 SanCor AR Dairy Fed 404 Dec06 62.5% 91 PE-fund C: Debts

10 SWS IR Rural serv. Fed 31 Dec06 100% 110 PE-fund C: Cashing11 SunBeam AU Fruit Prim 132 Mar07 100% 64 PE-fund C: Cashing12 Tnuva IL Dairy Fed 1,023 Mar07 ±75% 769 CEO C: Cashing13 Ag Processing USA Arable Fed 1,840 Aug07 100% 662+42 PE-fund PE: Profitable14 Reox (DG): Breeo IR Dairy Prim 358 Sep07 100%? 150? PE-fund? PE: Profitable

Source: Onno van Bekkum (NICE), www.nyenrode.nl/nice

… Private equity has started the hunt!

Global 300 Further analysis

G300 - % Of Turnover By Country

15% 15%

13%

6%

4% 4% 4%

3% 3% 3% 2% 2%2% 2%

1% 1% 1% 1% 0.5%0.4%0.3%0.2%0.2%0.2%0.1%0.1%

18%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%F

ranc

e

Japa

n

US

A

Ger

man

y

Net

herla

nds

Ital

y

UK

Sw

itzer

land

Kor

ea

Fin

land

Sw

eden

Spa

in

Can

ada

Den

mar

k

New

Zea

land

Nor

way

Bel

gium

Aus

tria

Irel

and

Indi

a

Bra

zil

Chi

na

Aus

tral

ia

Sin

gapo

re

Tai

wan

, C

hina

Isra

el

Por

tuga

l

G300 - Number of Coops By Country

67

55

32

2319

14149887765

33333222111110

10

20

30

40

50

60

70

80

US

A

Fra

nce

Ger

man

y

Ital

y

Net

her

lan

ds

Jap

anUK

Fin

lan

d

Can

ada

Sw

itze

rlan

d

Sw

eden

Sp

ain

New

Zea

lan

d

No

rway

Irel

and

Bel

giu

m

Den

mar

k

Ind

ia

Bra

zil

Au

stra

lia

Ko

rea

Sin

gap

ore

Isra

el

Au

stri

a

Ch

ina

Po

rtu

gal

Tai

wan

, C

hin

a

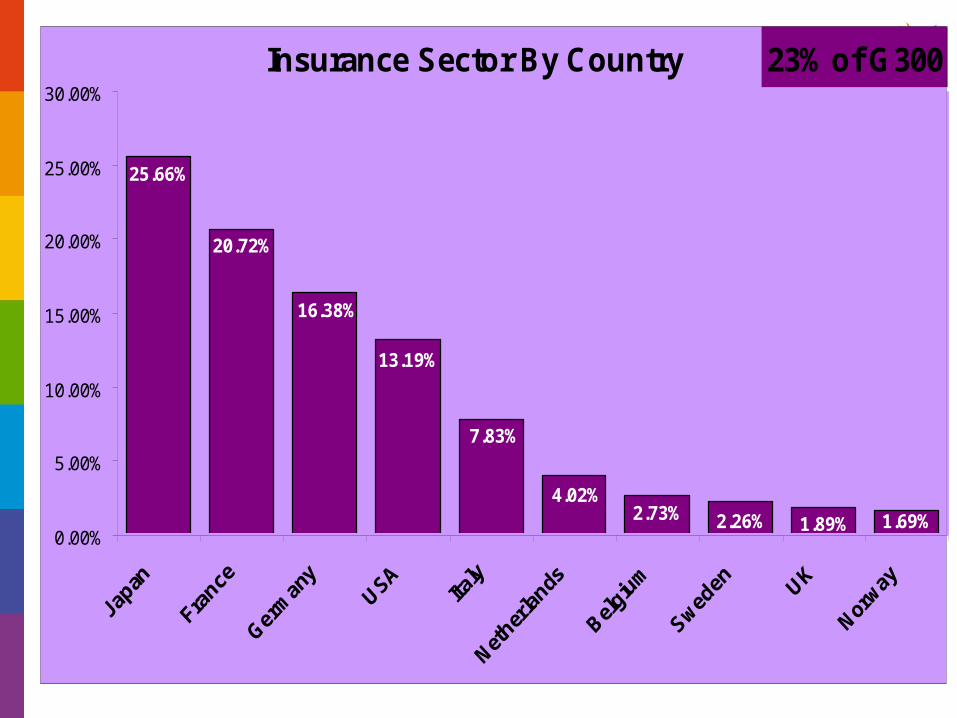

Insurance Sector By Country

1.69%1.89%2.26%2.73%4.02%

7.83%

13.19%

16.38%

20.72%

25.66%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

23% of G300

% Of Turnover : GDP14%

14%

10% 10%

8%

7% 7%

6%

5% 5%

4%

3% 2% 2% 2% 2% 2% 2% 2%1% 1%

3%3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

New Z

eala

nd

Finl

and

Switzer

land

Nether

land

s

Fran

ce

Sweden

Denm

ark

Indi

a

Taiw

an, C

hina

Germ

any

Korea

Norway

Japan

Irela

nd Italy

Belgi

umSpa

in

Canad

a

Austri

a

Singa

pore UK

USA

Isra

el

Consumer Sector By Country

2.38%3.00%3.05%

4.80%

7.77%

10.91%11.49%

13.14%13.21%

19.42%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

Germ

any

USA

Franc

e UK

Switzer

land Ita

ly

Japa

n

Finla

nd

Nethe

rlands

Canad

a

26% of G300

Top 20

Ranking Name of the Coop Country Turnover %1 Edeka Zentrale AG Germany 15,660 6.21%2 Migros Switzerland 15,475 6.14%3 The Co-operative Group UK 12,726 5.05%4 Coop Swiss Switzerland 10,729 4.26%5 Coop Norden S&N&D 10,307 4.09%6 John Lewis Partnership PLC UK 9,172 3.64%7 ReWe Group (Zentral-AktiengesellschaFU)Germany 7,662 3.04%8 Wakefern Food Corp. USA 7,239 2.87%9 Edeka Minden eG Germany 5,688 2.26%

10 Edeka Südwest eG Germany 5,607 2.22%11 SOK Corporation Finland 5,027 1.99%12 Superunie Netherlands 4,944 1.96%13 Associated Wholesale Grocers USA 4,918 1.95%14 Système U Centrale Regionale Ouest France 4,506 1.79%15 Federated Co-operatives Limited Canada 4,070 1.61%16 Cooppérative d'Exploitation et de Répartition Pharmacieutiques de RouensFrance 3,916 1.55%17 Cooperativa Farmaceutica Española Spain 3,795 1.51%18 United Co-operatives Ltd UK 3,547 1.41%19 Edeka Nordbayern-Sachsen-Thüringen eGGermany 3,489 1.38%20 Ace Hardware USA 3,466 1.37%

Top 20 141,942 56%Total Sector 252,136

Global 300 - National 100 • Use Global 300 methodology to create national lists

• So far…..

– USA – a pioneer!

– The UK recently published their UK 100

– Netherlands has issued a provisional NL 100

– France will shortly release their first French 100

– The following countries/sectors have given in-principle support:

• Canada

• Singapore

• Australia

• ICMIF

• ICBA

• This represents approximately 60% of global list so far…..

• How to Do It Workshop on Tuesday 16th October…..

• Since, this workshop a global data group has met on Wednesday and started work on mapping existing databases and methodologies

CSR – methodologyfrom principles to practice…

• Development of draft measure of Corporate (Co-operative) Social Responsibility

• Reviewed existing CSR criteria

• CSR and annual reports

• The co-operative difference

CSR – some reflections

• CSR is increasingly being embraced by our corporate competitors

• Co-op principles in particular the ICA’s Statement of Co-operative Identity are the basis of most co-op operation throughout the world

• Co-ops driven by their values have in many ways been pioneers of socially responsible business

• However, the movement has not done all it could in measuring the co-operative difference

• It has allowed others to claim credit for “inventing “CSR”

CSR – some reflections

• Some of the best examples of CSR are to be found among the Global 300

• However, our preliminary research shows that co-ops are not reporting in a consistent way

• If anything, many are simply following the usual approach of their investor competitors

• This has led us to develop a “draft” CSR methodology

ICA’s Global 300 (draft) CSR approach

We are attempting to developed a measure which incorporates the best aspects of mainstream CSR reporting while taking account of the co-op difference

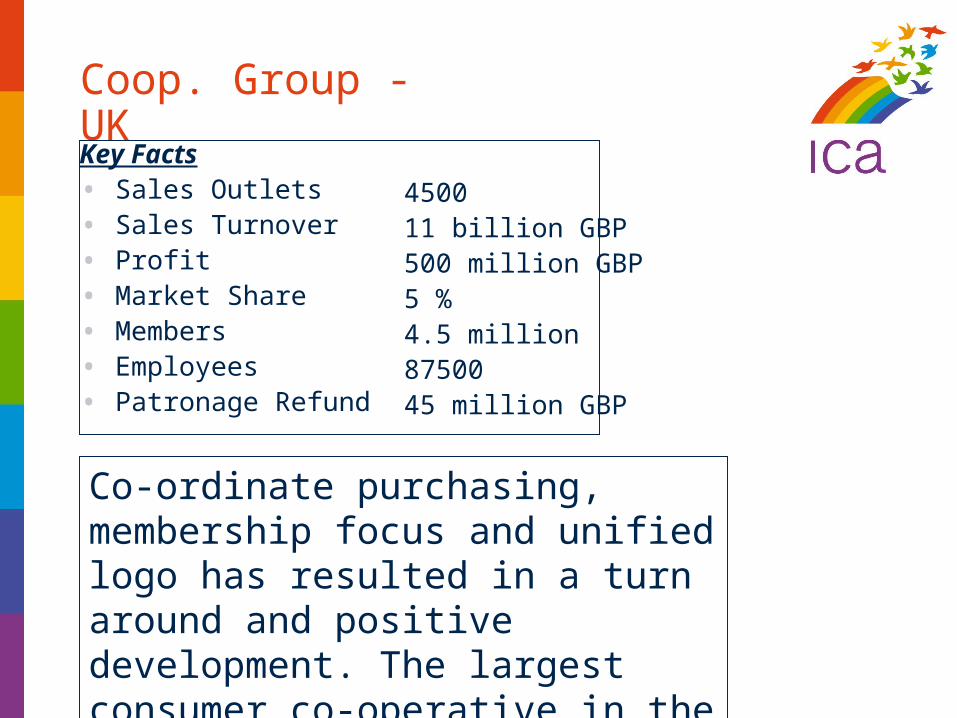

Coop. Group - UK

Key Facts• Sales Outlets• Sales Turnover• Profit• Market Share• Members• Employees• Patronage Refund

450011 billion GBP500 million GBP5 %4.5 million8750045 million GBP

Co-ordinate purchasing, membership focus and unified logo has resulted in a turn around and positive development. The largest consumer co-operative in the world created.

Coop Schweiz

Key Facts• Sales Outlets• Sales Turnover• Profit• Market Share

– Food– Non-food

• Members• Employees

15006.5 billion GBP138 million GBP

21 %10 %2.5 million45 500

Progressive top-down revolution created a one national consumer co-operative with a strong environmental profile.

S-group Finland

Key Facts• Sales Outlets• Sales Turnover• Profit• Market Share

– Food– Restaurants– Petrol & Oil

• Members• Employees• Patronage Refund

14007 billion GBP240 million GBP

35 %25 %18 %1.6 million34 000153 million GBP

Your own shop – a centrally managed retail chain with regional adjustment and a cost effective growth strategy.

Sistema Coop Italy

Key Facts• Sales Outlets• Sales Turnover• Profit• Market Share• Members• Employees

All 140 societies13008 billion GBP200 million GBP18 %6.2 million53 000

Top leading retail chain caring about: People, Society, Environment, Italian culture and Italian production... in order to cultivate an Italian model as an answer to the global challenges.

9 largest8607.3 billion GBP - -5.7 million46 000

Coop Sweden

Key Facts• Sales Outlets• Sales Turnover• Profit• Market Share• Members• Employees

15125.1 billion GBP53 million GBP21 %3 million17 000

Top leading retail chain with a vision to serve members in there endeavor for a sustainable life in a sustainable society.

A natural step

Demand, what is the member asking for ?

What can we deliver – our

ability & capacity

What position can and do we wish to have

Strategic Profile

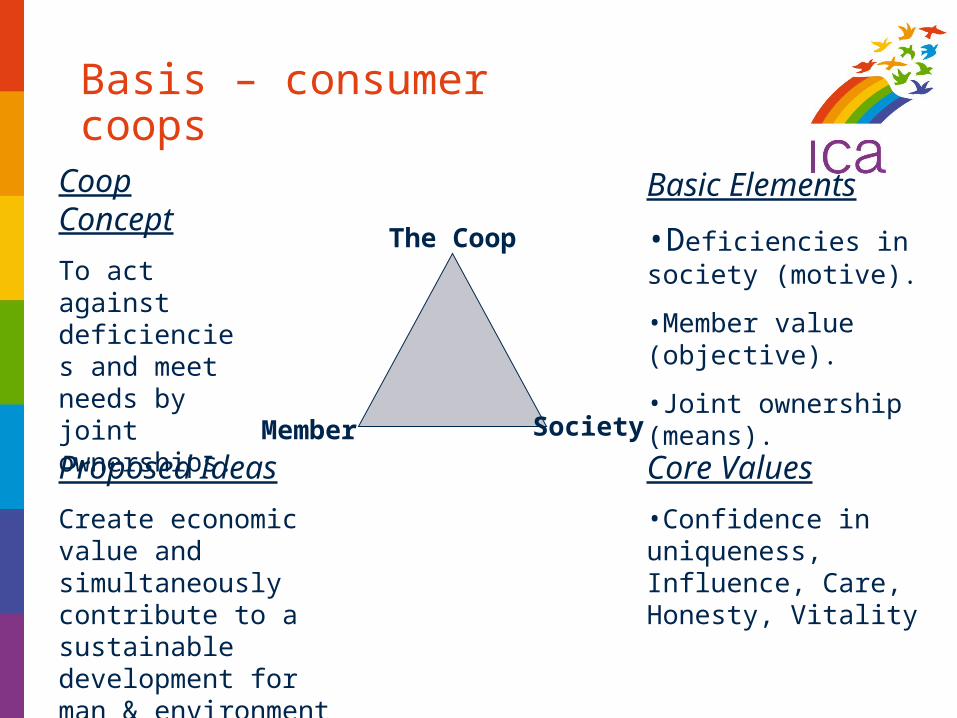

Basis – consumer coops

The Coop

Member Society

Coop Concept

To act against deficiencies and meet needs by joint ownerships.

Basic Elements

•Deficiencies in society (motive).

•Member value (objective).

•Joint ownership (means).

Core Values

•Confidence in uniqueness, Influence, Care, Honesty, Vitality

Proposed Ideas

Create economic value and simultaneously contribute to a sustainable development for man & environment

Possible Status? 3 – 5 years

Profitable and value based retailing

Priceworthy sustainable products and services

Contribute to a sustainable development

Business & Financial Requirements

Member needs and usefulness

Community needs