Coolidge Grp02

12

COOLIDGE BANK & TRUST COMPANY By: Group No. 02 Abhijeet Nayak (10P002) Amar Rajagopal (10P007) Nipun Goyal (10P035) Pratyaksh Mehra (10P039) Saksham Agarwal (10P047)

-

Upload

abhijeetnayak -

Category

Documents

-

view

379 -

download

5

Transcript of Coolidge Grp02

COOLIDGE BANK & TRUST COMPANY

By: Group No. 02Abhijeet Nayak (10P002)Amar Rajagopal (10P007)Nipun Goyal (10P035)Pratyaksh Mehra (10P039)Saksham Agarwal (10P047)

About the Company• Established in Dec 1960 by 12 merchants &

businessmen• Headed by Mr. Milton Adess with no prior

financial exposure - who considered money to be a product which has to be sold at the lowest possible price and the best possible quality

• At end of 4 yrs their total deposits - $10.2 mn & after “No Service Charge” scheme it grew manifolds to $61.2 mn by 1970

Innovations @ Coolidge

We Close Sundays

X’Mas Interest

We give business a

break

We’re Loners

F N S C P C AWe pick up & Deliver

No money down

We love MBA’s

What’s the new Gen coming to

Coolidge bank comes to Kendall

We give you credit for

being successful

Growth Gaurantee

Case Analysis• Coolidge Bank is a young and innovative

commercial bank in the Boston area• Debating introduction of NOW accounts

offered by both thrift banks & commercial banks

• With a substantial number of thrift banks offering NOW accounts and the concept starting to grow among commercial banks in Massachusetts, Coolidge Bank has to decide its strategy

Introduction to ‘NOW’ Account• Withdrawal by negotiable instrument, i.e. Check• Interest received @ 5%• Per transaction cost to the bank approx 10cents• 100% deposits can be re-invested• No overdraft facility available• Any number of transactions possible• Offered by commercial banks & other NBFC’s

Note: Keeping a NOW account will not improve ourprofits but not keeping a NOW account shall onlylead to huge losses.

Reasons to introduce NOW accountGains

• Prevent migration of our present accounts to competitor’s ‘NOW’ accounts

• Earn interest on 15% more deposits in hand• Greater ease of usage. Can be traded• No cap on number of transactions

Loss• Interest out-flow on deposits• Substantial operating costs

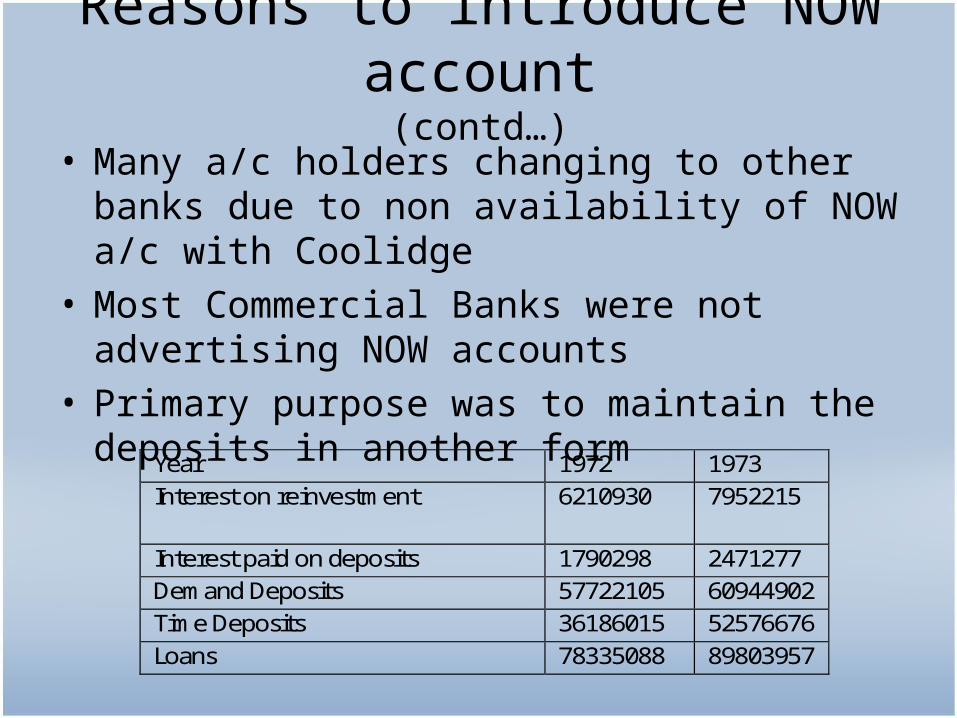

Reasons to introduce NOW account(contd…)

• Many a/c holders changing to other banks due to non availability of NOW a/c with Coolidge

• Most Commercial Banks were not advertising NOW accounts

• Primary purpose was to maintain the deposits in another form

Year 1972 1973 Interest on reinvestment 6210930 7952215

Interest paid on deposits 1790298 2471277 Demand Deposits 57722105 60944902 Time Deposits 36186015 52576676 Loans 78335088 89803957

Product offered• Interest Provided 5%

• No charges up to 10 transactions per month

• Transaction Charges as per following details:– Balance less than 500 : 20cents– Balance more than 500 : 10 cents for first 10 nos 15 cents for further nos

Cost Analysis (contd…)

% of changing Balance %of changing Balance20.00 0-250$ 10.00 0-250$40.00 250-1000$ 25.00 250-1000$60.00 >1000$ 50.00 >1000$

% of changing Balance Deposits Deposits transferred interest to be paid % of changing Balance Deposits20.00 0-250$ 4191216.62 838243.32 42974.64 10.00 0-250$ 4191216.6240.00 250-1000$ 9356448.37 3742579.35 191872.67 25.00 250-1000$ 9356448.3760.00 >1000$ 15967945.01 9580767.01 491181.94 50.00 >1000$ 15967945.01

Total 726029.25

% of changing Balance Deposits Deposits transferred interest income foregone% of changing Balance Deposits20.00 0-250$ 4191216.62 838243.32 83193.62 10.00 0-250$ 4191216.6240.00 250-1000$ 9356448.37 3742579.35 371441.96 25.00 250-1000$ 9356448.3760.00 >1000$ 15967945.01 9580767.01 950867.98 50.00 >1000$ 15967945.01

Total 1405503.56

% of changing Balance Deposits Deposits transferred interest income foregone% of changing Balance Deposits20.00 0-250$ 272451.78 54490.36 5408.04 10.00 0-250$ 272451.7840.00 250-1000$ 18145288.55 7258115.42 720350.42 25.00 250-1000$ 18145288.5560.00 >1000$ 8827437.67 5296462.60 525661.12 50.00 >1000$ 8827437.67

Total 1251419.57

Checking Account Balance Situation-1 (If funds migrated to NOW Account) Checking Balance Situation Case-2 (If funds migratedto NOW account)

% of changing Balance Deposits Deposits transferred Extra funds avlbl for reinvestmentextra interest income % of changing Balance Deposits20.00 0-250$ 4191216.62 838243.32 125736.50 12479.04 10.00 0-250$ 4191216.6240.00 250-1000$ 9356448.37 3742579.35 561386.90 55716.29 25.00 250-1000$ 9356448.3760.00 >1000$ 15967945.01 9580767.01 1437115.05 142630.20 50.00 >1000$ 15967945.01

Total 1405503.56Grand Total 4062426.70

Net Gain 3336397.45

Checking Account Balance Situation-1 (Cost Incurred due to Interest Outflow) Checking Account Checking Account Balance Situation-2 (Cost Incurred due to Interest Outflow) Checking Account

Savings Account Balance Situation-1 (Cost Incurred due to Interest Outflow) Savings Account Savings Account Balance Situation-2 (Cost Incurred due to Interest Outflow) Savings Account

Savings Account Balance Situation-1 (If funds migrated to other banks) Savings Account Savings Balance Situation Case-2 (If funds migratedto other banks) Savings Account

Checking Account Balance Situation-1 (If funds migrated to other banks) Checking Account Checking Balance Situation Case-2 (If funds migratedto other banks) Checking Account

Competitor Analysis Coolidge Bank Offering Commerci

al Banks Mutual Savings Banks

Savings & Loans Co-op Banks

Interest Rate paid 5% (=) (=) (=)

Basis of calculation of interest rates

Day of Deposit to Withdrawal (=) (=) (=)

Frequency of compounding Daily (+) (+) (+)

Charge per Draft

20 Cents ($500 or less accounts)

10 Cents for <= 10

Drafts($1000 or more accounts)

15 Cents for > 10 Drafts

($1000 or more accounts)

(-)

(+)

(=)

(-)

(+)

(-)

(-)

(+)

(-)

Frequency of Compounding

Interest

Quarterly (Effective Interest

Rate)

Monthly (Effective Interest Rate)

Daily(Effective Interest Rate)

4% 1.0406 1.0407 1.408 5% 1.05109 1.05116 1.0512

Trends• Data suggests mass switching to NOW a/c in future• Operational costs for NOW a/c transactions to fall

gradually due to restructuring• More than 95% of Check-in a/c holders have savings

a/c as well• As people are not averse to having more than one

type of a/c they will shift to NOW as well• Major reason for a/c shifting prior to NOW was

convenience• Customers moving towards companies offering

more convenience & flexibility

Thank You!!!