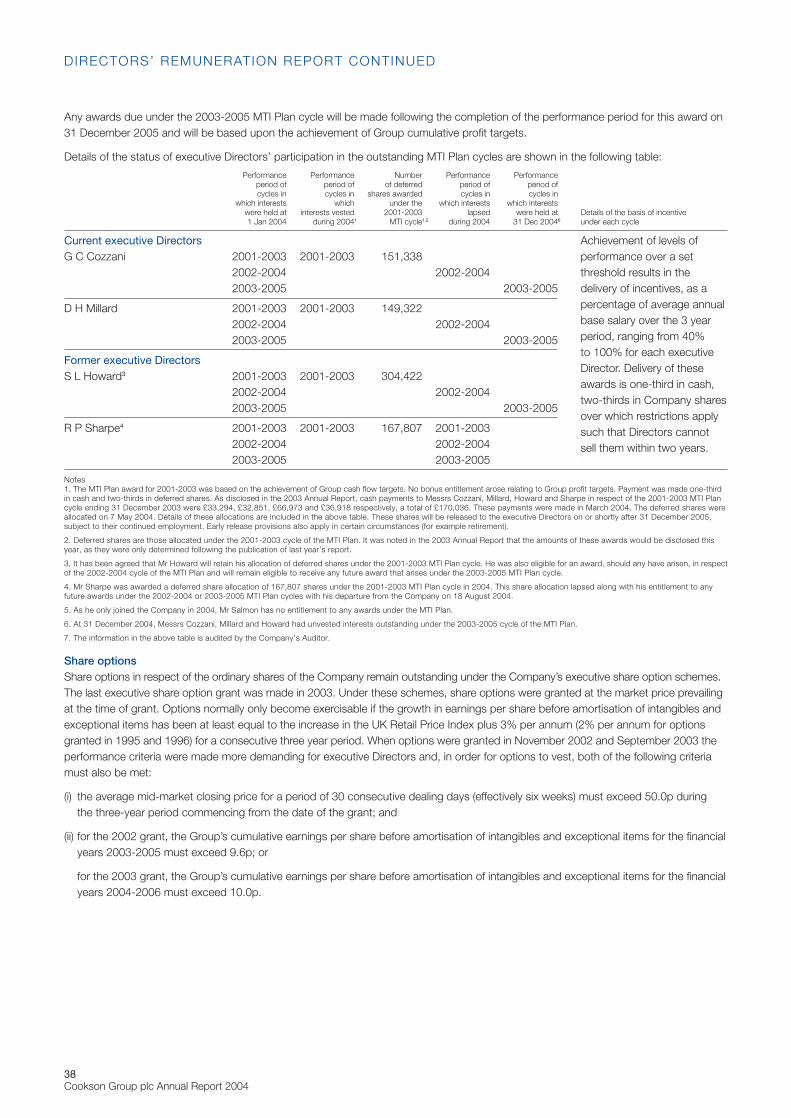

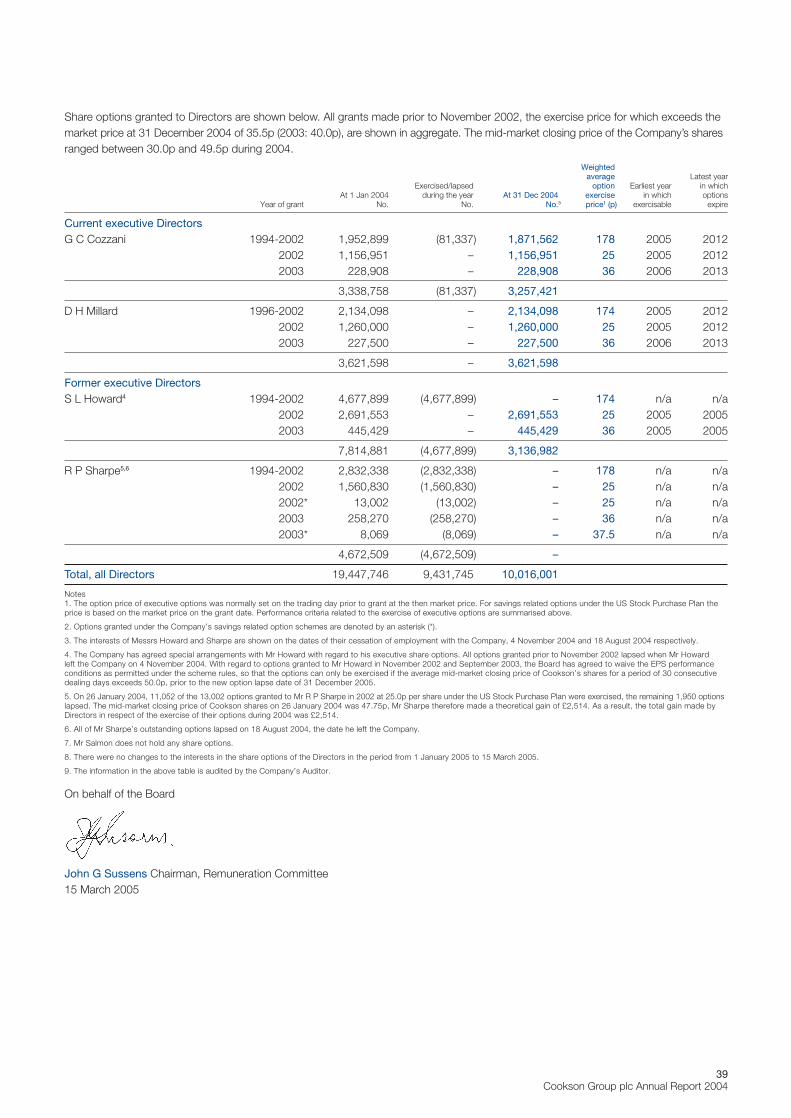

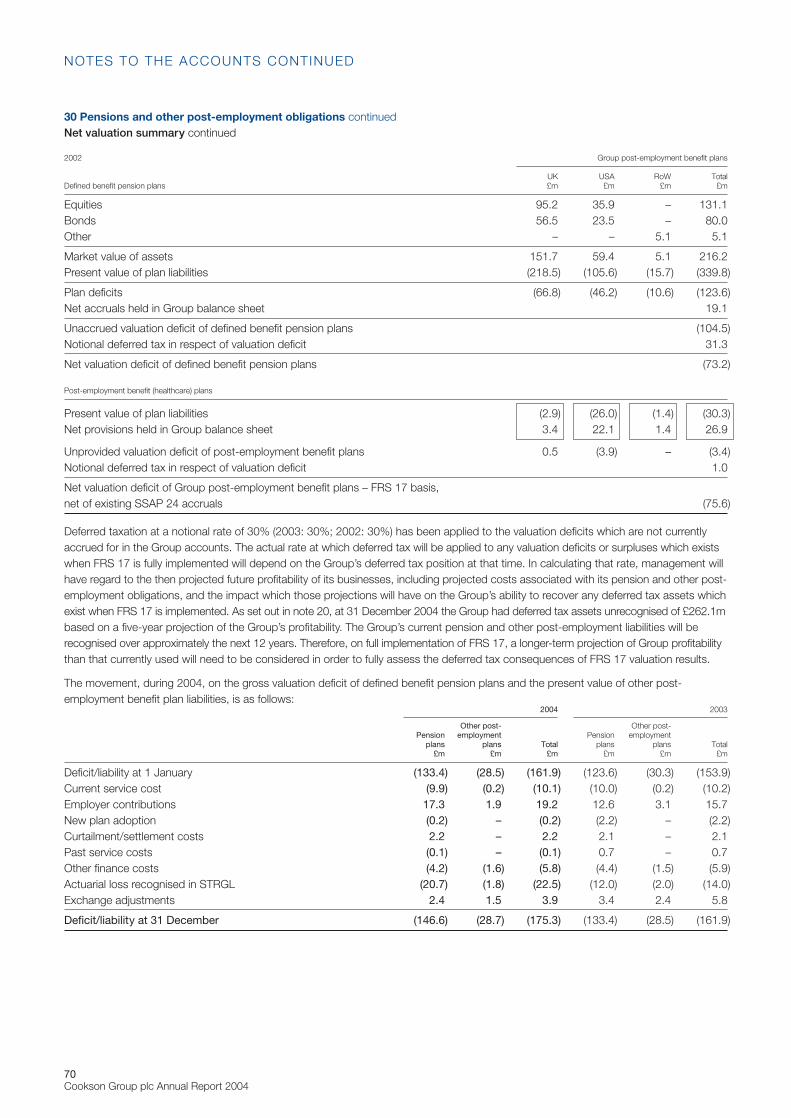

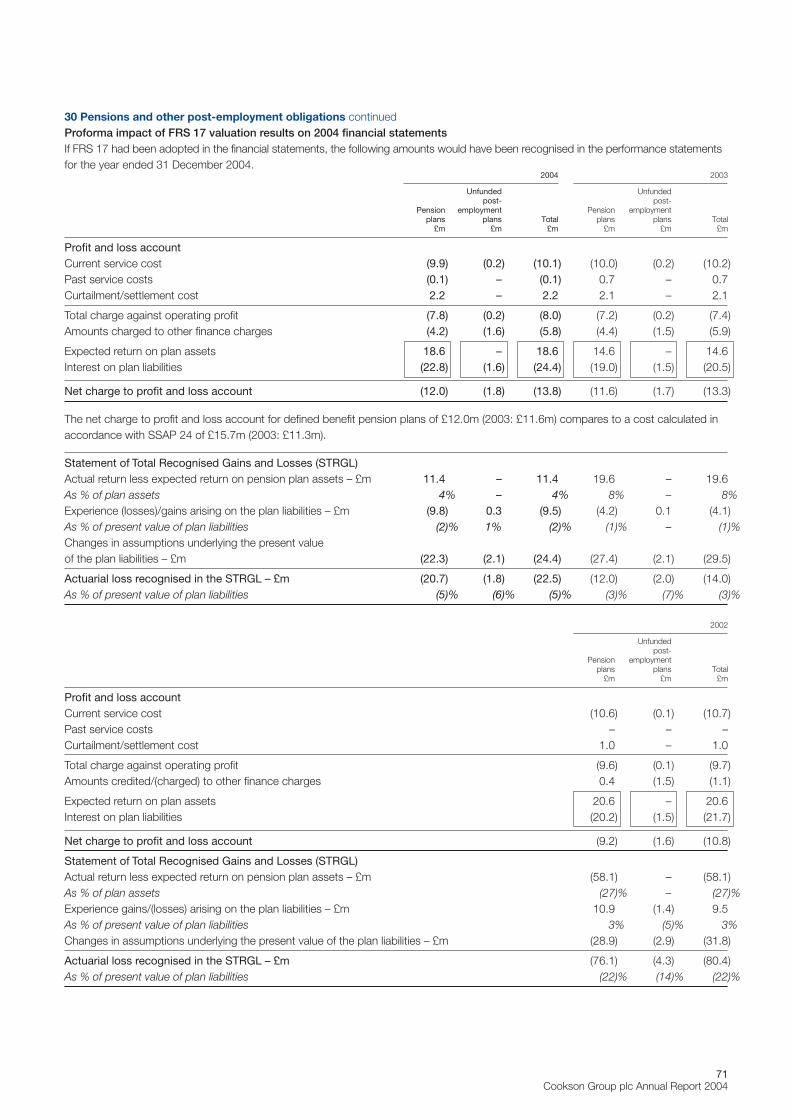

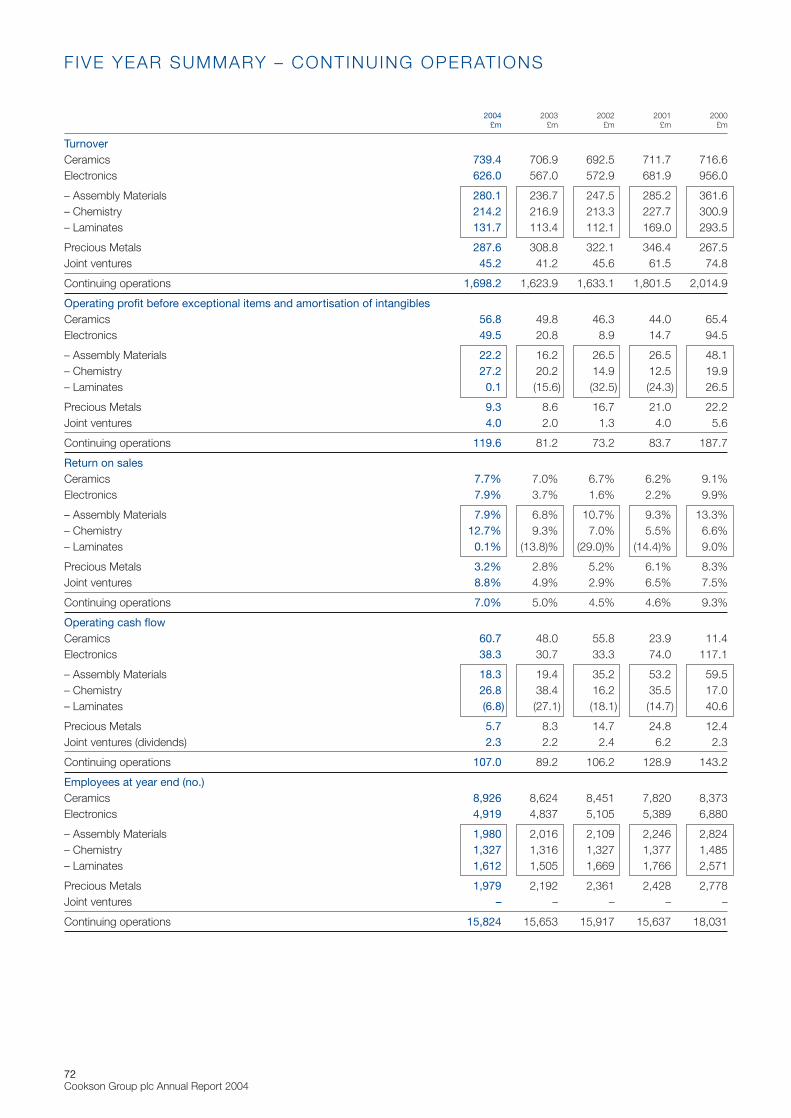

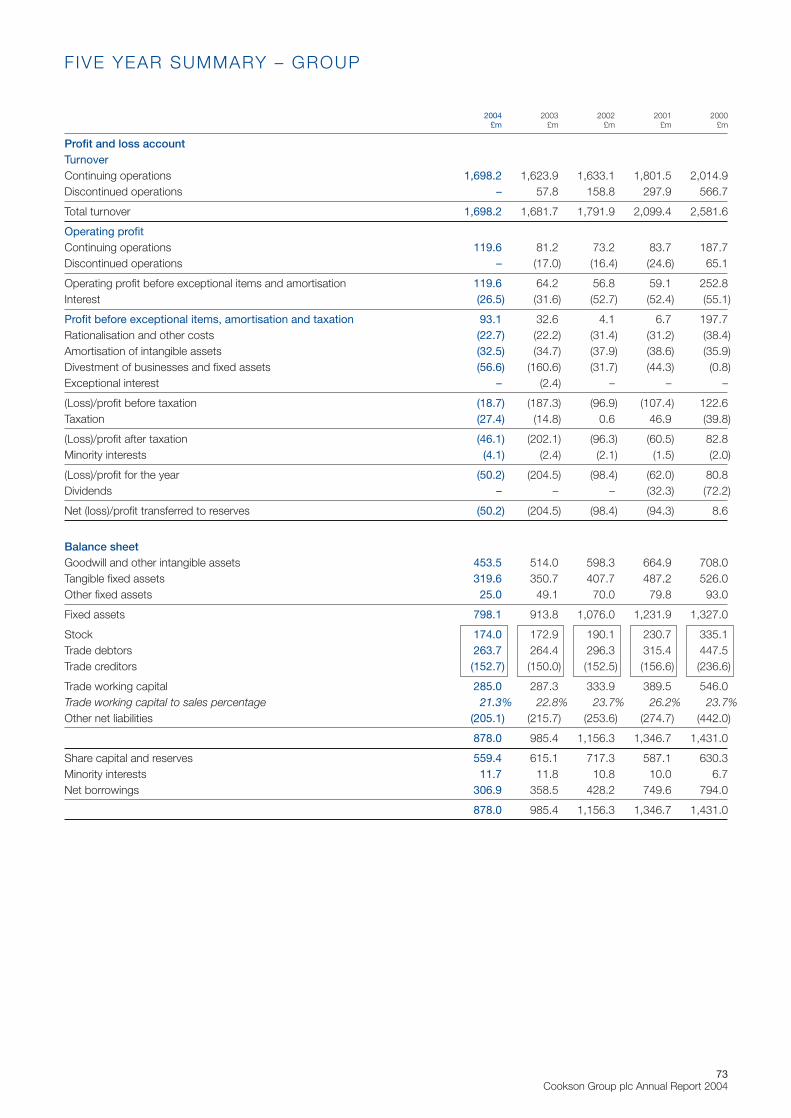

Cookson Group plc Annual Report 2004 - … · futuristic spherical building is constructed from...

86

Cookson Group plc Annual Report 2004 Around your world

Transcript of Cookson Group plc Annual Report 2004 - … · futuristic spherical building is constructed from...

Cookson Group plc Annual Report 2004

Around your world

COOKSON WE ARE A LEADING MATERIALS SCIENCE

COMPANY SUPPLYING PRODUCTS AND

SERVICES TO CUSTOMERS WORLDWIDE.

OUR OPERATIONS ARE FORMED INTO THREE

DIV IS IONS – CERAMICS, ELECTRONICS AND

PRECIOUS METALS.

WE AIM TO ADD VALUE TO OUR CUSTOMERS’

BUSINESSES BY PROVIDING MATERIALS,

PROCESSES AND SERVICES THAT ALLOW

THEM TO INCREASE THE EFFICIENCY, QUALITY

AND PRODUCTIV ITY OF THEIR OPERATIONS.

THROUGHOUT THE WORLD, COOKSON

COMPANIES ARE KNOWN FOR SUPPLYING

PRODUCTS THAT REPRESENT THE BEST

TECHNOLOGY, SUPPORTED BY THE BEST

TECHNICAL SERVICE.

YOU MAY BE SURPRISED WHERE OUR

PRODUCTS ARE FOUND AROUND YOUR WORLD.

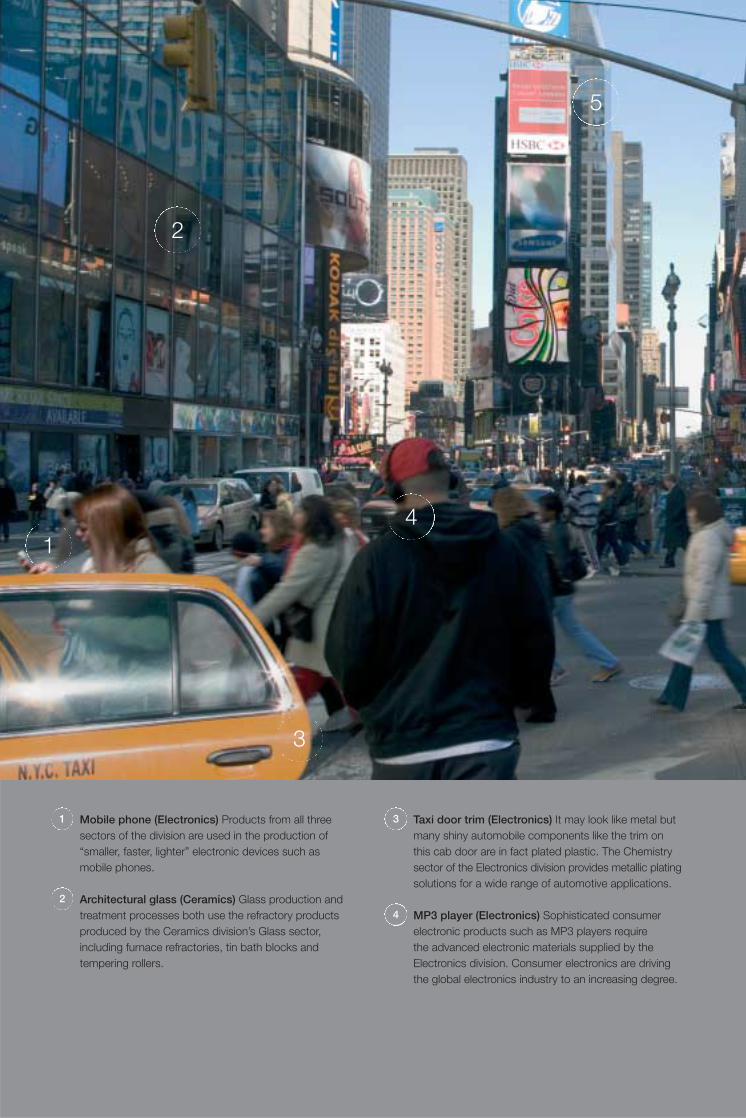

Mobile phone (Electronics) Products from all threesectors of the division are used in the production of“smaller, faster, lighter” electronic devices such asmobile phones.

Architectural glass (Ceramics) Glass production andtreatment processes both use the refractory productsproduced by the Ceramics division’s Glass sector,including furnace refractories, tin bath blocks andtempering rollers.

2

1 Taxi door trim (Electronics) It may look like metal butmany shiny automobile components like the trim onthis cab door are in fact plated plastic. The Chemistrysector of the Electronics division provides metallic platingsolutions for a wide range of automotive applications.

MP3 player (Electronics) Sophisticated consumerelectronic products such as MP3 players require the advanced electronic materials supplied by theElectronics division. Consumer electronics are drivingthe global electronics industry to an increasing degree.

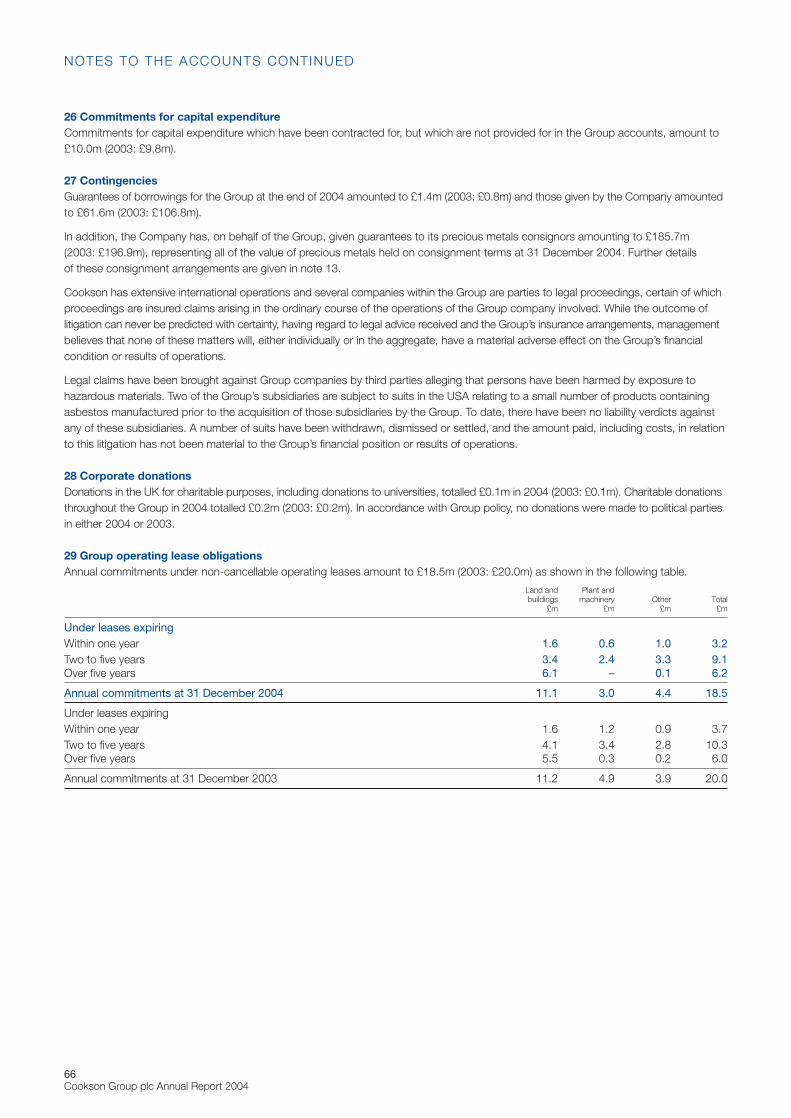

4

3

2

3

1

5

4

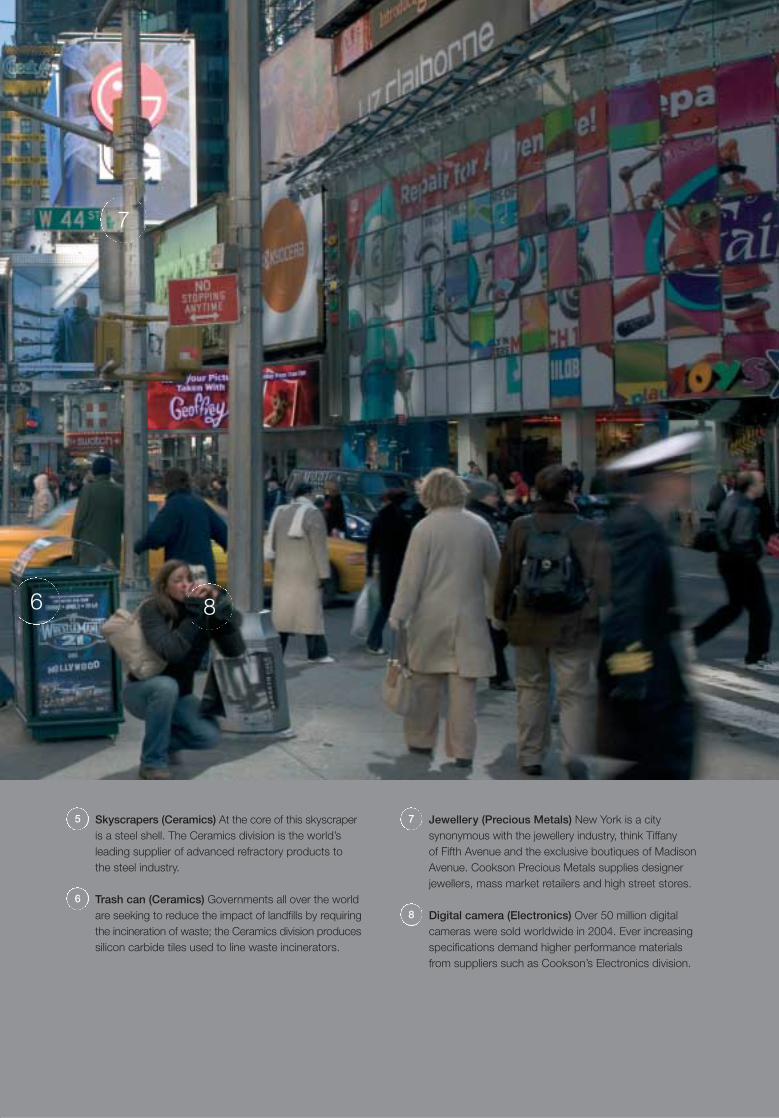

Skyscrapers (Ceramics) At the core of this skyscraperis a steel shell. The Ceramics division is the world’sleading supplier of advanced refractory products to the steel industry.

Trash can (Ceramics) Governments all over the worldare seeking to reduce the impact of landfills by requiringthe incineration of waste; the Ceramics division producessilicon carbide tiles used to line waste incinerators.

6

5 Jewellery (Precious Metals) New York is a citysynonymous with the jewellery industry, think Tiffany of Fifth Avenue and the exclusive boutiques of MadisonAvenue. Cookson Precious Metals supplies designerjewellers, mass market retailers and high street stores.

Digital camera (Electronics) Over 50 million digitalcameras were sold worldwide in 2004. Ever increasingspecifications demand higher performance materialsfrom suppliers such as Cookson’s Electronics division.

8

7

86

7

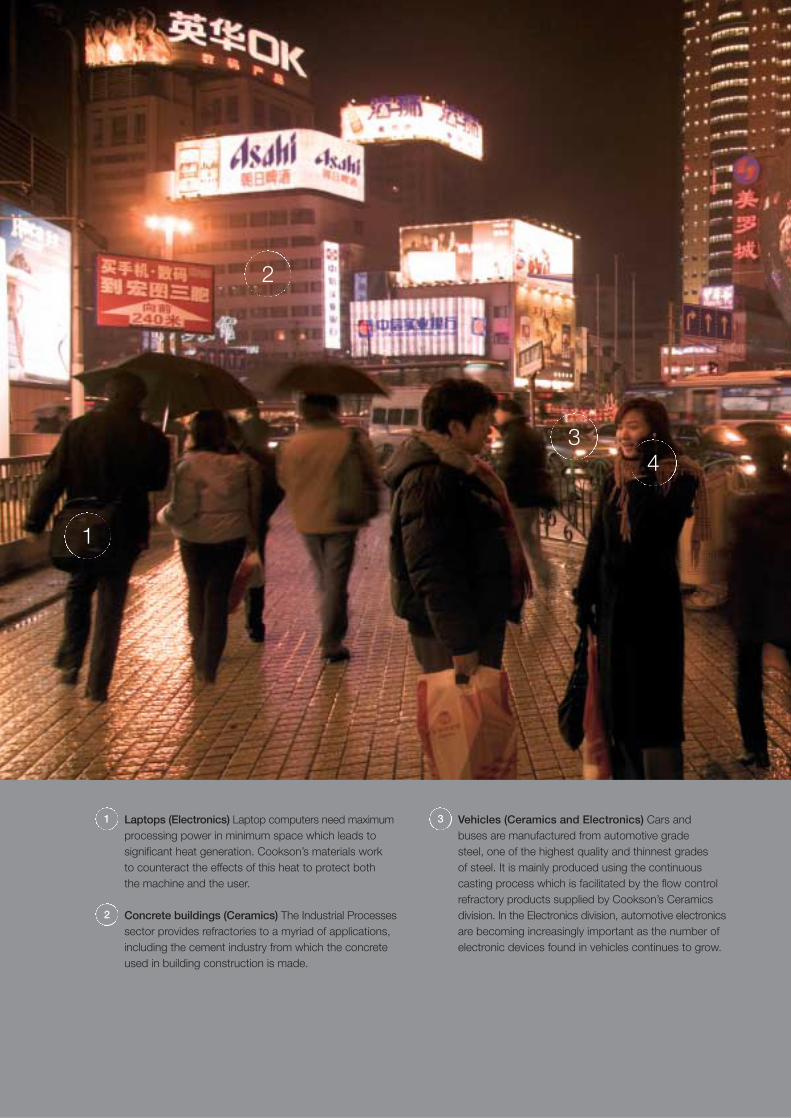

Laptops (Electronics) Laptop computers need maximumprocessing power in minimum space which leads tosignificant heat generation. Cookson’s materials work to counteract the effects of this heat to protect both the machine and the user.

Concrete buildings (Ceramics) The Industrial Processessector provides refractories to a myriad of applications,including the cement industry from which the concreteused in building construction is made.

2

1 Vehicles (Ceramics and Electronics) Cars and buses are manufactured from automotive grade steel, one of the highest quality and thinnest grades of steel. It is mainly produced using the continuouscasting process which is facilitated by the flow controlrefractory products supplied by Cookson’s Ceramicsdivision. In the Electronics division, automotive electronicsare becoming increasingly important as the number ofelectronic devices found in vehicles continues to grow.

3

4

2

1

3

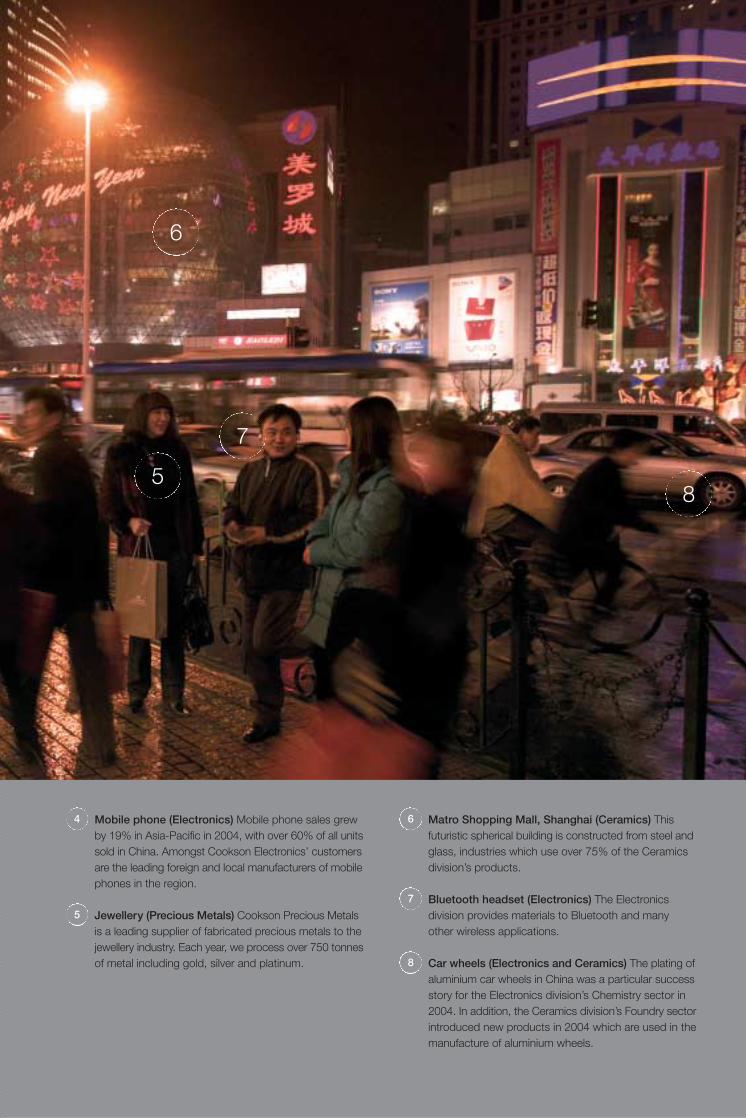

Mobile phone (Electronics) Mobile phone sales grewby 19% in Asia-Pacific in 2004, with over 60% of all unitssold in China. Amongst Cookson Electronics’ customersare the leading foreign and local manufacturers of mobilephones in the region.

Jewellery (Precious Metals) Cookson Precious Metalsis a leading supplier of fabricated precious metals to thejewellery industry. Each year, we process over 750 tonnesof metal including gold, silver and platinum.

5

4 Matro Shopping Mall, Shanghai (Ceramics) Thisfuturistic spherical building is constructed from steel andglass, industries which use over 75% of the Ceramicsdivision’s products.

Bluetooth headset (Electronics) The Electronicsdivision provides materials to Bluetooth and many other wireless applications.

Car wheels (Electronics and Ceramics) The plating ofaluminium car wheels in China was a particular successstory for the Electronics division’s Chemistry sector in2004. In addition, the Ceramics division’s Foundry sectorintroduced new products in 2004 which are used in themanufacture of aluminium wheels.

8

7

6

5

6

7

8

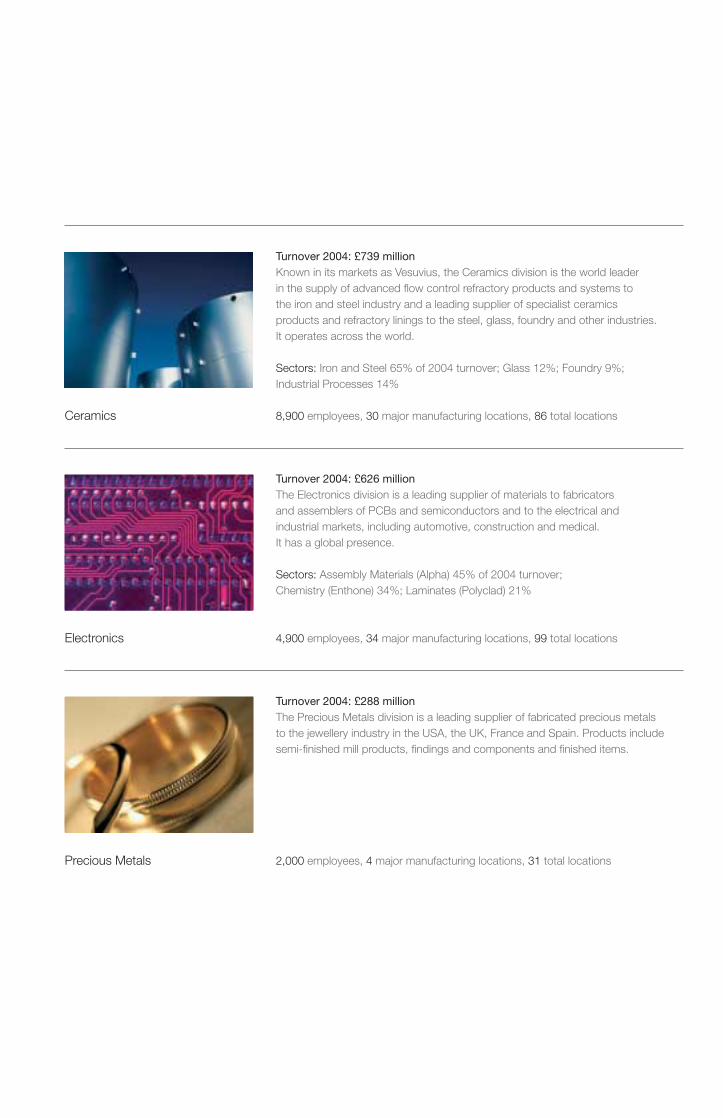

Ceramics

Electronics

Precious Metals

Turnover 2004: £739 millionKnown in its markets as Vesuvius, the Ceramics division is the world leader in the supply of advanced flow control refractory products and systems to the iron and steel industry and a leading supplier of specialist ceramics products and refractory linings to the steel, glass, foundry and other industries. It operates across the world.

Sectors: Iron and Steel 65% of 2004 turnover; Glass 12%; Foundry 9%; Industrial Processes 14%

8,900 employees, 30 major manufacturing locations, 86 total locations

Turnover 2004: £626 millionThe Electronics division is a leading supplier of materials to fabricators and assemblers of PCBs and semiconductors and to the electrical and industrial markets, including automotive, construction and medical. It has a global presence.

Sectors: Assembly Materials (Alpha) 45% of 2004 turnover; Chemistry (Enthone) 34%; Laminates (Polyclad) 21%

4,900 employees, 34 major manufacturing locations, 99 total locations

Turnover 2004: £288 millionThe Precious Metals division is a leading supplier of fabricated precious metalsto the jewellery industry in the USA, the UK, France and Spain. Products includesemi-finished mill products, findings and components and finished items.

2,000 employees, 4 major manufacturing locations, 31 total locations

Highlights 1

Around your world in 2004 2

Corporate social responsibility 6

Chairman’s statement 8

Chief Executive’s statement 9

Operating review 11

Financial review 18

Board of Directors 23

Directors’ report 24

Directors’ remuneration report 31

Corporate responsibility statement 40

Health, safety and environmental report 41

Directors’ responsibility statement 42

Auditor’s report 43

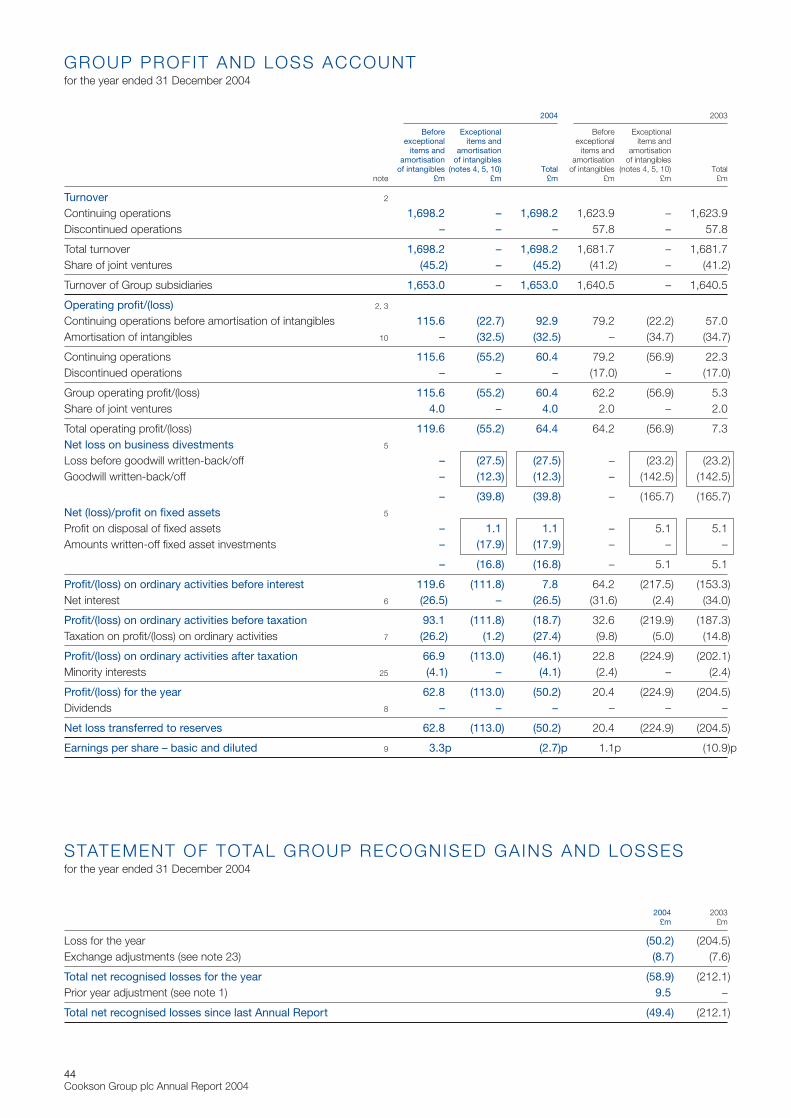

Group profit and loss account 44

Statement of total Group recognised gains and losses 44

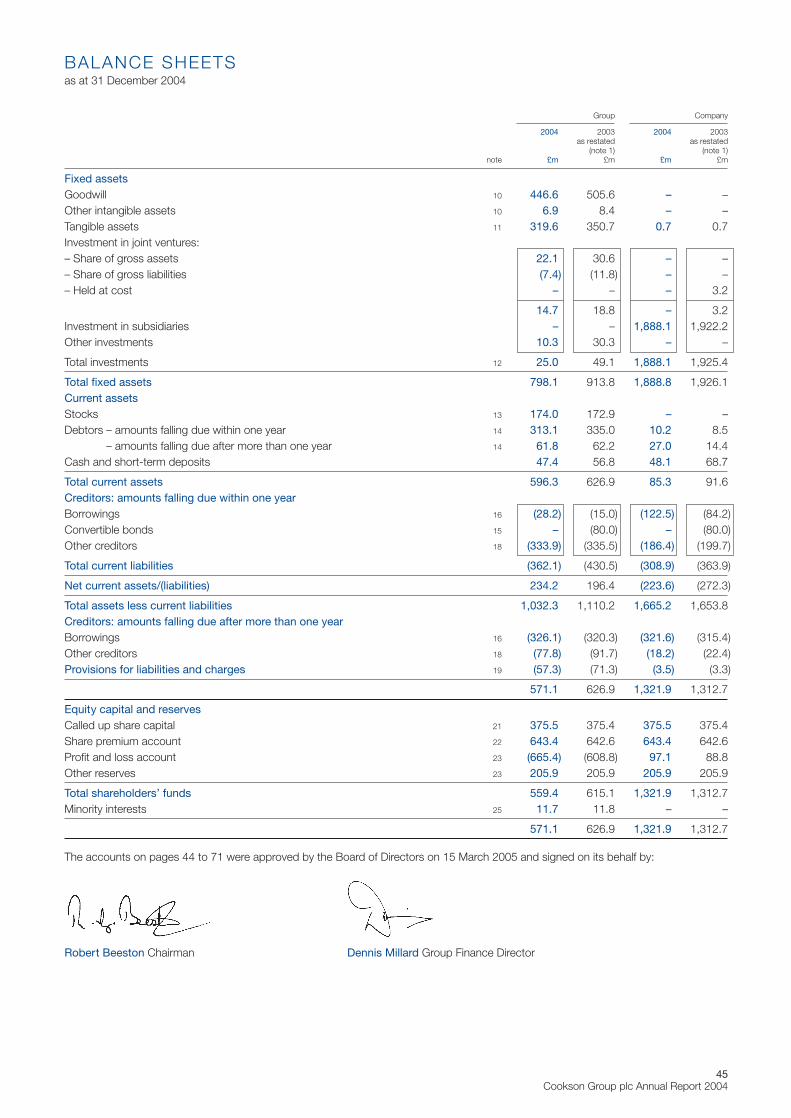

Balance sheets 45

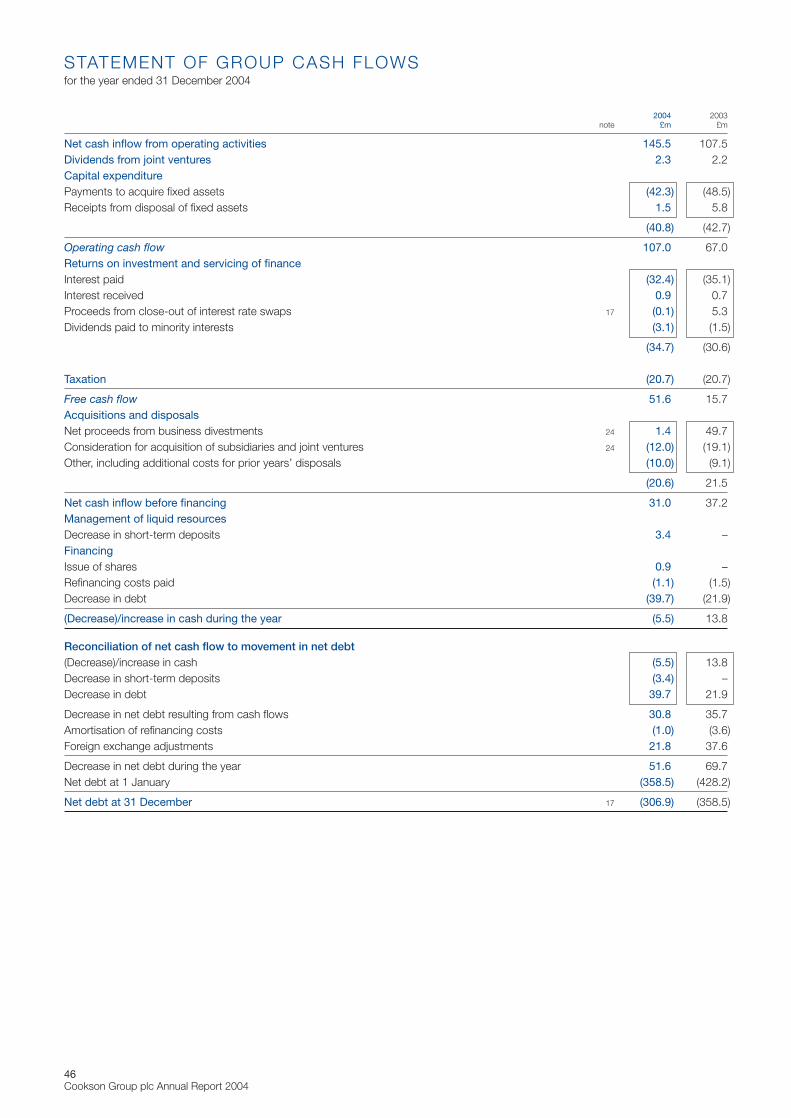

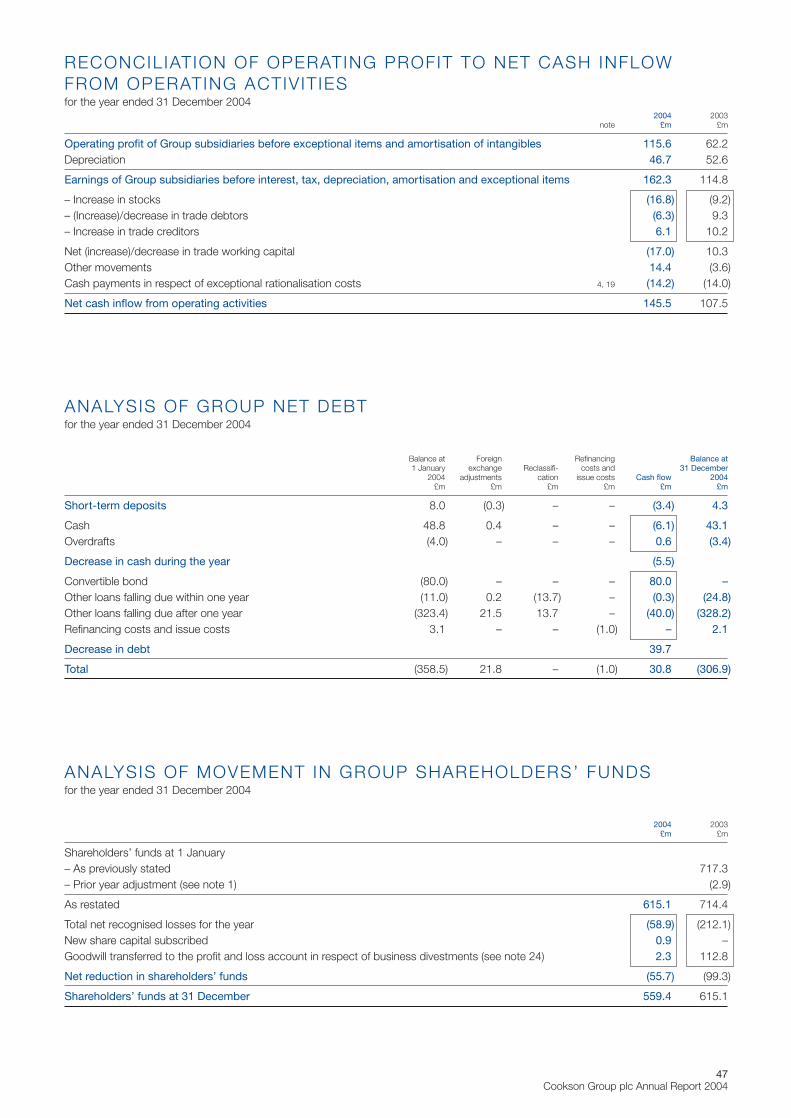

Statement of Group cash flows 46

Reconciliation of operating profit to netcash inflow from operating activities 47

Analysis of Group net debt 47

Analysis of movements in Groupshareholders’ funds 47

Notes to the accounts 48

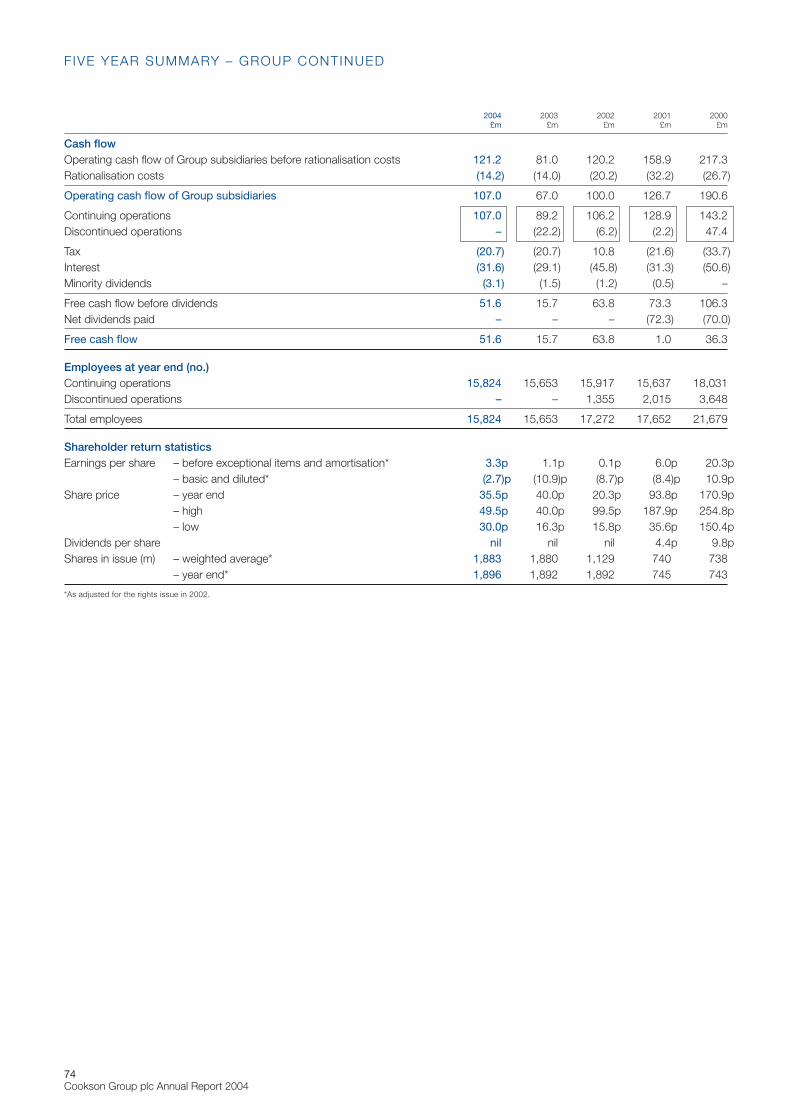

Five year summary – continuing operations 72

Five year summary – Group 73

Shareholder information 75

Glossary of technical and financial terms 76

CONTENTS

1Cookson Group plc Annual Report 2004

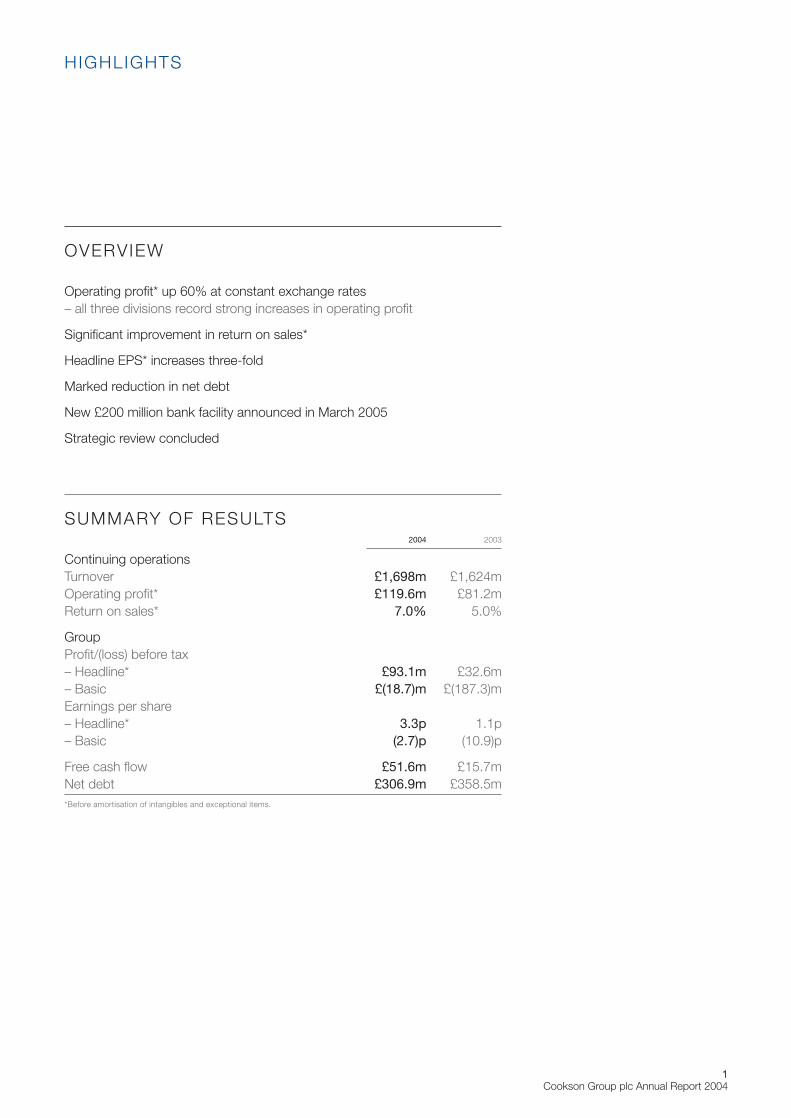

OVERVIEW

Operating profit* up 60% at constant exchange rates– all three divisions record strong increases in operating profit

Significant improvement in return on sales*

Headline EPS* increases three-fold

Marked reduction in net debt

New £200 million bank facility announced in March 2005

Strategic review concluded

SUMMARY OF RESULTS2004 2003

Continuing operationsTurnover £1,698m £1,624mOperating profit* £119.6m £81.2mReturn on sales* 7.0% 5.0%

GroupProfit/(loss) before tax– Headline* £93.1m £32.6m– Basic £(18.7)m £(187.3)mEarnings per share– Headline* 3.3p 1.1p– Basic (2.7)p (10.9)p

Free cash flow £51.6m £15.7mNet debt £306.9m £358.5m*Before amortisation of intangibles and exceptional items.

H IGHLIGHTS

2Cookson Group plc Annual Report 2004

Streamlining for success in Ceramics2004 saw the start of plans to upgrade andmodernise VISO plants in Illinois, USA andMonterrey, Mexico, which are essential tosupport the steel and foundry industries inthe NAFTA region. The Illinois facility is the“master plant” for NAFTA, whilst Monterreycan easily supply the southern part of theNAFTA region. To ensure sustainable long-term success, these two facilities are being upgraded with state-of-the-artmanufacturing and material handlingequipment, due to be completed in thesecond quarter of 2005.

Electronics in the EastIncreased demand across the Electronicsdivision in 2004 led to plans for a newfacility in Shanghai which will enhance ourability to provide local sales, warehousing,technical support and analytical services tothis critically important region. In Shenzhen,the Chemistry sector’s China TechnicalCentre will open in 2005, providingapplications engineering expertise throughadvanced analytical and diagnosticequipment and development personnel.

Upgrading in the USAThe Laminates sector of the Electronicsdivision completed the upgrade of its USfacilities during 2004. In California, a state-of-the-art electronics manufacturing facilityopened in March and in New Hampshireproduction was upgraded and modernised.The introduction of lean manufacturing andadvanced scheduling practices at bothplants will accelerate product delivery speedsand address customers’ inventory issues.

Investing in IndiaVesuvius acquired a crucible plant inMehsana in 2003. Since then, the plant hasundergone considerable reorganisation toimprove operational performance, resultingin improved quality and higher market shares.Modernising the production facilities hastripled capacity and process improvementshave delivered significant productivity gains.Better raw materials management andenergy consumption have also contributedto the plant’s success.

Gearing up for automotiveIn the Electronics division, Chemistryachieved a breakthrough market position in 2004 in aluminium wheel plating in Asia. Approximately 700,000 wheels aremanufactured each year in China using our chemistry. Eastern Europe alsoachieved substantial market growth in this field. As manufacturing of certain auto parts migrates to Eastern Europe and China, we are well positioned to grow this important market segment.

Precious Metals shines in ThailandCookson Precious Metals launched a jointventure in Thailand with the Unique Groupduring 2004, known as PCF Precious ChainFinding and Alloy Co. The new company isthe exclusive agent for Cookson PreciousMetals in Thailand, representing tradenames such as Excell Chain, HallmarkSweet and Stern Leach and promoting a wide range of products including chain,findings, alloys, mill products and beads.

Leading in lead-freeEuropean and Japanese regulations aredriving the need to reduce or eliminate lead,cadmium, chrome and other materials fromproducts used to manufacture electronicassemblies, PCBs, automotive parts andother consumer products. Cookson hasdemonstrated leadership in developinglead-free and other environmentally soundtechnologies, products and services.

Our Assembly Materials sector has developed a complete suite ofenvironmentally friendly, lead-free electronicsassembly materials. Additionally, it has madea commitment to assist the industry bysharing its extensive lead-free technology andanalytical expertise. The sector organisedthe Global Lead-Free Knowledge Networkconsisting of leading suppliers in theelectronics assembly industry. Over 50seminars were conducted in 20 countriesaround the world and attended by over1,700 assembly process engineers. Thisleading industry educational effort willcontinue in 2005.

The Chemistry sector continued itsleadership in lead-free final finishes for PCB fabrication and introduced a systemof hexavalent chrome-free processes andcobalt-free electroless nickel products to meet standards implemented by theworld’s leading automotive producers.

The Laminates sector expanded itsproduct portfolio of lead-free and halogen-free laminate materials.

AROUND YOUR WORLD IN 2004

Driving growth from core markets

3Cookson Group plc Annual Report 2004

1 2 3

5 6

7 8

4

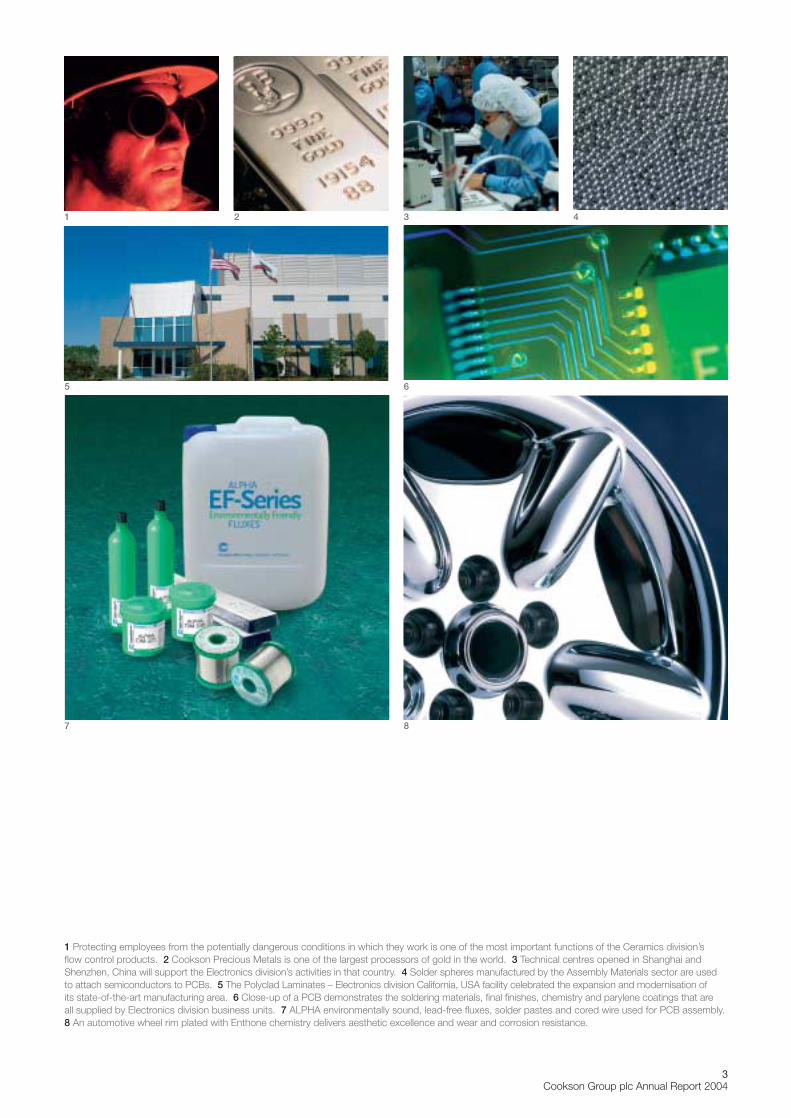

1 Protecting employees from the potentially dangerous conditions in which they work is one of the most important functions of the Ceramics division’s flow control products. 2 Cookson Precious Metals is one of the largest processors of gold in the world. 3 Technical centres opened in Shanghai andShenzhen, China will support the Electronics division’s activities in that country. 4 Solder spheres manufactured by the Assembly Materials sector are used to attach semiconductors to PCBs. 5 The Polyclad Laminates – Electronics division California, USA facility celebrated the expansion and modernisation of its state-of-the-art manufacturing area. 6 Close-up of a PCB demonstrates the soldering materials, final finishes, chemistry and parylene coatings that are all supplied by Electronics division business units. 7 ALPHA environmentally sound, lead-free fluxes, solder pastes and cored wire used for PCB assembly.8 An automotive wheel rim plated with Enthone chemistry delivers aesthetic excellence and wear and corrosion resistance.

4Cookson Group plc Annual Report 2004

Opening up new business opportunitiesRapid growth in Asia-Pacific continuedthroughout 2004 in the Ceramics division,especially in China where crude steelproduction now exceeds the EU and the USA combined, leading to increasingdemand for flow control refractories andthe technical service for which Vesuvius is renowned. A programme started in the fourth quarter will double Chinese VISO capacity by April 2005, making theSuzhou plant one of the Group’s biggest.Elsewhere, it was decided to increase ourshare of the slide gate joint venture withWuhan Iron & Steel from 25% to 50% witheffect from 2005. This plant, managed byVesuvius since March 2003, will install newmixing and pressing equipment to increasecapacity and improve quality.

The fused silica plant in Kua Tang, Chinaopened its second phase in January 2004.This plant is our most modern and, as wellas producing glass tempering rollers, nowmanufactures large diameter ceramic rollers,opening up new business opportunities infloat line furnaces.

Poland – our gateway to Eastern EuropeThe evolution of the global economy in the last ten years has prompted EasternEuropean countries to modernise theirindustrial practices – and hence their usage of refractory products. From its manufacturing platform in Poland,Vesuvius is helping its customers toundertake this transformation. The transferof the division’s monolithics technology toPoland has allowed Vesuvius Poland todouble its monolithics output over the lasttwo years. In 2004, we embarked upon

two major investments to support thegrowth of our flow control business inCentral Eastern Europe: one to extendVISO capacity and the other to modernisean existing line to manufacture latesttechnology slide gate refractories. Bothprojects will be completed during 2005.

Maximising materials managementThe past three years have seen a significantshift in the way Vesuvius has dealt with rawmaterial supply from China, moving awayfrom purchasing through traders to dealingdirectly with the Chinese producers. Directpurchasing enables us to source quality rawmaterials at truly competitive prices and hasalso allowed us to develop direct relationshipswith Chinese producers who, as a result,gave Vesuvius preferred customer statusthrough a period of high demand in 2004.

Many of the raw materials Vesuvius usesare becoming available in China and it is onlyby being based there that new supplies canbe identified at the earliest possible stage.By tightly controlling raw material quality,we are now able to take full advantage of China’s low processing costs and sendprocessed materials to many of our plantsaround the world, with confidence that thequality will be within specification for everybag of material supplied.

No more polishingThrough a collaborative effort with the UK’sMiddlesex University, Cookson PreciousMetals has introduced Argentium™ SterlingSilver, a revolutionary alloy. Argentium™Sterling Silver is highly tarnish resistant,staying bright and beautiful without polishing.It is harder and more durable than standard

sterling silver and can be laser-welded, whichopens up new avenues in application anddesign. Argentium™ Sterling Silver providesopportunities for Cookson Precious Metalsin its core jewellery market as well as otherareas including cutlery and flatware gifts.

Argentium™ Sterling Silver has theadditional benefit of being environmentallyfriendly because it eliminates the need forchemical processes to remove an unwantedsubstance called firescale which developswhen standard sterling silver is heatedduring manufacturing.

Prestigious R&D centre opened in IndiaOctober 2004 saw the opening of theElectronics division’s Indian ResearchCentre in Bangalore. The new facility is a partnership with India’s pre-eminentscientific institution, the Indian Institute of Science, and is located in Bangalore’sprestigious Entrepreneurship Centre. TheCentre is an integral part of the division’sglobal R&D effort, where the focus is on thedevelopment of leading edge technologiesfor a wide range of applications. Thiscommitment to scientific excellence willallow us to continue to meet the technologychallenges of the future cost-effectively andparticularly to serve the rapidly growingAsia-Pacific region.

AROUND YOUR WORLD IN 2004

Building on strongleadership positions

5Cookson Group plc Annual Report 2004

3 4 5

1 2

7 8

6

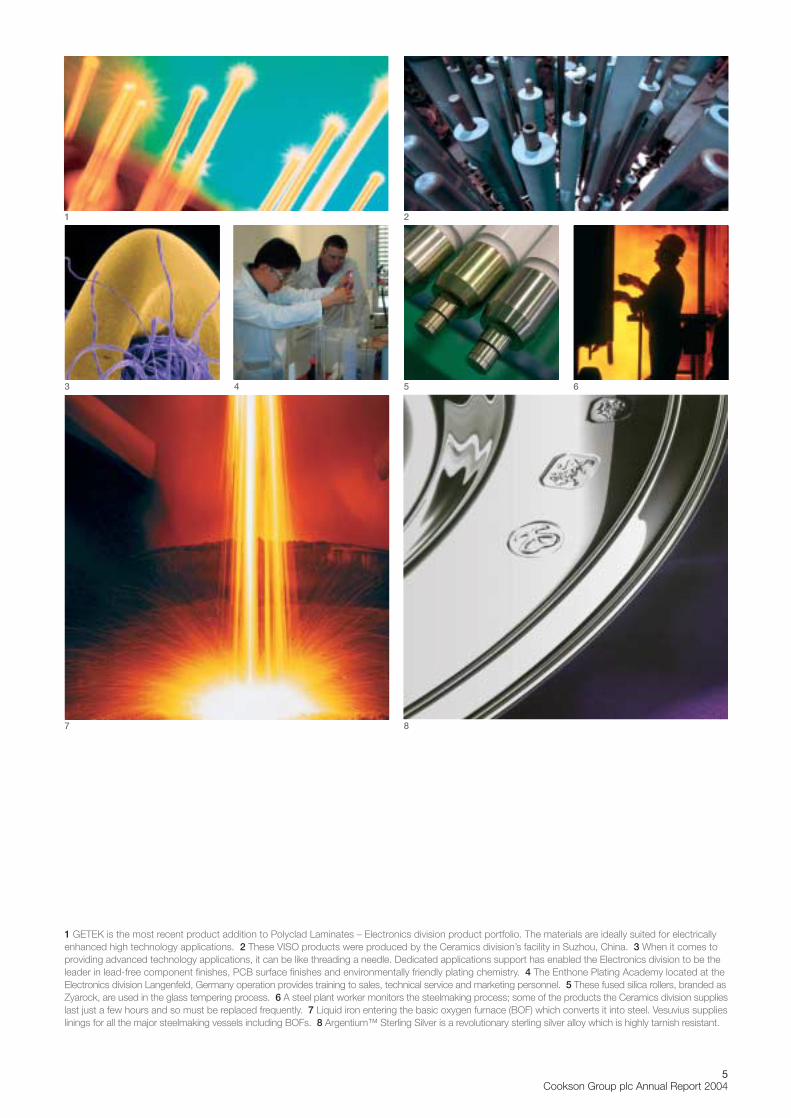

1 GETEK is the most recent product addition to Polyclad Laminates – Electronics division product portfolio. The materials are ideally suited for electricallyenhanced high technology applications. 2 These VISO products were produced by the Ceramics division’s facility in Suzhou, China. 3 When it comes toproviding advanced technology applications, it can be like threading a needle. Dedicated applications support has enabled the Electronics division to be theleader in lead-free component finishes, PCB surface finishes and environmentally friendly plating chemistry. 4 The Enthone Plating Academy located at theElectronics division Langenfeld, Germany operation provides training to sales, technical service and marketing personnel. 5 These fused silica rollers, branded asZyarock, are used in the glass tempering process. 6 A steel plant worker monitors the steelmaking process; some of the products the Ceramics division supplieslast just a few hours and so must be replaced frequently. 7 Liquid iron entering the basic oxygen furnace (BOF) which converts it into steel. Vesuvius supplieslinings for all the major steelmaking vessels including BOFs. 8 Argentium™ Sterling Silver is a revolutionary sterling silver alloy which is highly tarnish resistant.

6Cookson Group plc Annual Report 2004

The workplaceCookson’s success depends very much on retaining the commitment of the peoplewho work within it. We therefore strive toensure our people have a safe environmentin which to work and that our employmentpractices are fair and equitable.

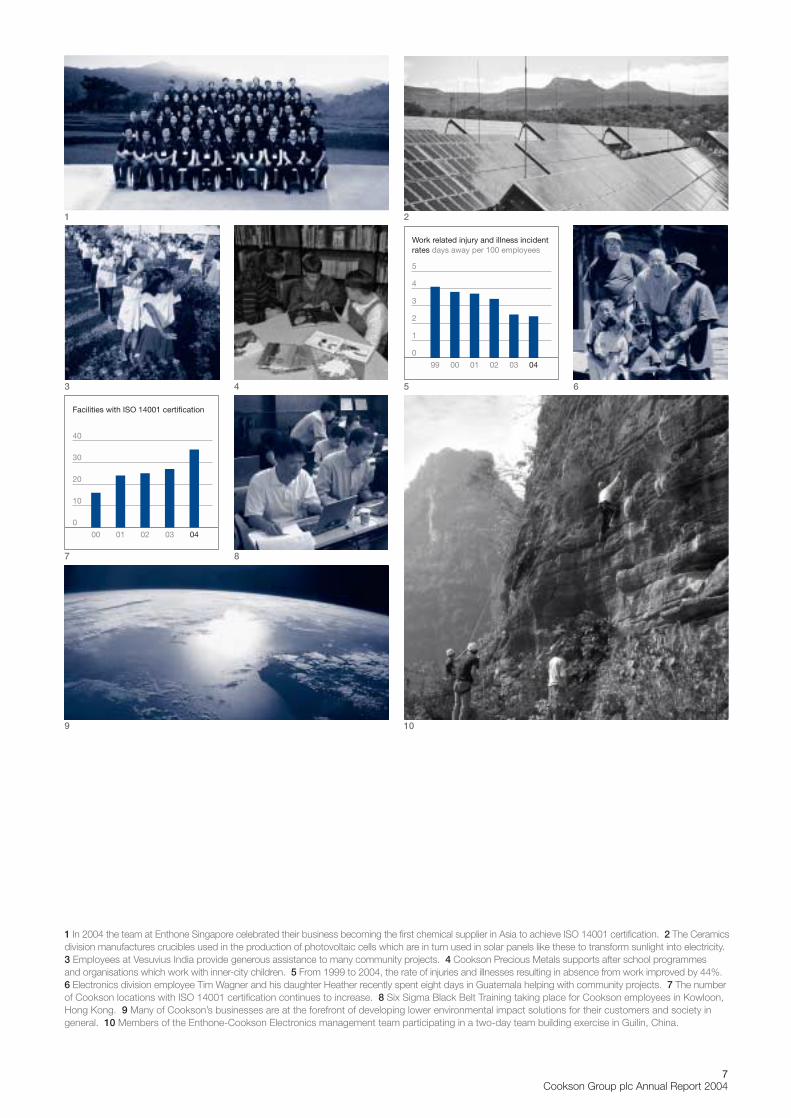

SafetyOur goal is zero work-related injuries andillnesses. To achieve this, we have in placea worldwide initiative to improve safetyperformance. The programme includesminimum standards of performance,targeted assistance to high risk sites and avariety of training and awareness activities.From 1999 to 2004, our rate of injuries and illnesses resulting in absence fromwork improved by 44%. In 2004, 40% ofCookson’s operations around the worldachieved our goal of zero work-relatedillnesses and injuries.

One area on which we have been workinghard is the avoidance of work-related injuriesthrough better application of ergonomicprinciples. The last three years have seenextensive ergonomic training throughoutthe Group and the establishment ofergonomic teams at a number of facilitieswith real results.

Employment practicesCookson believes that wherever in theworld they work employees have the rightto be treated in good faith and on the basisof respect for the dignity of the individual.

We recognise that job satisfaction requiresworking environments that motivate ouremployees to be productive and innovativeand provide opportunities for training and

development so our people can maximisetheir personal potential and develop careerswithin the Group.

The environmentCookson’s policy is to operate in a mannerthat preserves a sound environment.

In 2004, we began a new programme to reduce energy use, including trainingemployees to understand energy use andconservation principles and introducingenergy audits to assist high-use sites inidentifying and implementing conservationmeasures. This programme is alreadyshowing results. At our largest energyconsumption site, initial efforts will reducelighting costs by 70%.

The number of Cookson locationscertified to ISO 14001, the internationalstandard for environmental managementsystems, continues to increase. By the end of 2004, 36 locations had achievedcertification and 15 additional locationswere actively implementing the standard.This growth is an indication of thecommitment of Cookson companies toimproved environmental performance.

The marketplaceMany of Cookson’s businesses are at theforefront of developing lower environmentalimpact solutions for their customers andsociety in general.

The Electronics division’s leadership inthe development of environmentally friendlyproducts for electronic devices is detailedon page 2.

The Ceramics division contributes to thecontrol of climate change by manufacturingcrucibles used in the production of

photovoltaic cells, which convert sunlightinto electricity.

The communityCookson people all around the world areinvolved in community projects. Here arejust a few examples.

Every member of staff at Vesuvius India contributed one day’s salary to help those affected by the December 2004 tsunami disaster. They also providegenerous assistance to a number of Indian organisations working to improvethe health and education of underprivilegedchildren. In addition, they support thedevelopment of young entrepreneurs within their local communities, helpingthem to create small businesses, many of which become suppliers to Vesuvius.

Freezing temperatures and rain did littleto deter Electronics’ employees in Altoona,USA from raising money in the AmericanCancer Society’s Relay for Life campaign.Recognition for their efforts came with theRookie of the Year award in their first yearof participation in the event.

Cookson Precious Metals assistscommunity organisations including YMCA after school programmes and facility development, as well as helpinginner-city children through organisationswhich work with disadvantaged, specialneeds programmes such as the NationalCouncil of Community Justice in New York.

CORPORATE SOCIAL RESPONSIBIL ITY

Acting responsiblyaround your world

7Cookson Group plc Annual Report 2004

3 4

8

5

4

3

2

1

0

040302010099

Work related injury and illness incident rates days away per 100 employees

5

40

30

20

10

0

0403020100

Facilities with ISO 14001 certification

7

2

9 10

6

1 In 2004 the team at Enthone Singapore celebrated their business becoming the first chemical supplier in Asia to achieve ISO 14001 certification. 2 The Ceramicsdivision manufactures crucibles used in the production of photovoltaic cells which are in turn used in solar panels like these to transform sunlight into electricity.3 Employees at Vesuvius India provide generous assistance to many community projects. 4 Cookson Precious Metals supports after school programmes and organisations which work with inner-city children. 5 From 1999 to 2004, the rate of injuries and illnesses resulting in absence from work improved by 44%.6 Electronics division employee Tim Wagner and his daughter Heather recently spent eight days in Guatemala helping with community projects. 7 The numberof Cookson locations with ISO 14001 certification continues to increase. 8 Six Sigma Black Belt Training taking place for Cookson employees in Kowloon,Hong Kong. 9 Many of Cookson’s businesses are at the forefront of developing lower environmental impact solutions for their customers and society ingeneral. 10 Members of the Enthone-Cookson Electronics management team participating in a two-day team building exercise in Guilin, China.

1

8Cookson Group plc Annual Report 2004

CHAIRMAN’S STATEMENT

For Cookson, 2004 was a year of bothchange and progress. I was very pleased to announce the appointment of Nick Salmonwho joined us as Chief Executive in July.Nick brings vast experience to the Group’sBoard which he demonstrated in his first sixmonths as we undertook a wide-rangingstrategic review.

Nick presented the outcome of thisreview in January 2005. The strategyadopted, which the Board wholeheartedlyendorses, recognises that there is stillmuch to do to create maximum value for all our stakeholders and sets out a proactiveprogramme for the immediate future.

Nevertheless, 2004 was a good start. TheGroup’s profit before tax* of £93 million wasalmost three times higher than the previousyear and headline earnings per share*improved to 3.3 pence (2003: 1.1 pence). I am particularly pleased to report thatoperating cash flow was strong, resulting in a considerable reduction in net debt to£307 million (2003: £359 million). We expectto make further progress across our threedivisions in the current year.

The Board is well aware that manyshareholders are keen to see thereinstatement of dividend payments as a sign of confidence in the strength ofCookson’s recovery. It is our intention to return Cookson to the dividend list assoon as possible, with dividends paid on a sustainable basis from free cash flow.

A further indication of the confidenceboth we and our bankers have in Cookson’sfuture is the refinancing of our bank facility,on improved pricing and terms, which wasannounced on 1 March 2005.

In common with many companies, themost recent valuation of our UK pensionscheme showed a sizeable deficit. Followingdiscussions with the scheme’s trustees, the contributions of both the Company andscheme members have been increased.

During the year, we announced theappointment of Jan Oosterveld and JohnSussens as non-executive Directors to replaceTony Alexander and June de Moller whoretired as non-executive Directors in 2004.

Steve Howard stepped down from theBoard in November following a smoothhandover to Nick Salmon. Ray Sharpe,Chief Executive of the Electronics division,resigned in May.

I would like to take this opportunity tothank Steve, Ray, Tony and June for theirvaluable contributions to Cookson over a number of years.

We have also recently announced furtherdirectorate changes. Dennis Millard, GroupFinance Director since 1996, has informedthe Board of his intention to step downfrom the Board and leave Cookson duringthe course of 2005. Dennis has beenGroup Finance Director over a period that has encompassed both significantachievements and considerable challenges,most recently with the arrangement of thenew £200 million bank facility. He was anintegral part of the strategic review and I know that Nick Salmon appreciates thesupport Dennis has given him during hisinitial period with Cookson. The process of recruiting a successor has commencedand Dennis will continue in his role until an appointment has been made and atransition effected.

Finally, I would like to thank KentAtkinson, who steps down as a non-executive Director on 15 April 2005, for his contribution over the past two years.John Sussens has succeeded Kent asSenior Independent Director.

This year’s improved performance was achieved through the efforts andcommitment of the Group’s employeesworldwide. I thank them for raising thestandards of our operations.

Robert Beeston Chairman15 March 2005

*Before exceptional items and amortisation of intangible assets.

“Our strategy recognises that there is still much todo to create maximum value for all our stakeholders.

Nevertheless, 2004 was a good start”Robert Beeston Chairman

9Cookson Group plc Annual Report 2004

CHIEF EXECUTIVE’S STATEMENT

2004 resultsThe Group’s results showed a markedimprovement in 2004, benefiting from bothbetter market conditions and action takento restructure certain businesses and controlcosts. Turnover from continuing operationswas up 5% at reported exchange rates to£1,698 million. Operating profit forcontinuing operations before exceptionalitems and amortisation of intangible assetsrose by 47% to £120 million. Net incomeafter tax, amortisation of intangible assets andexceptional charges improved from a loss of£205 million in 2003 to a loss of £50 millionin 2004. Net debt at 31 December 2004 was£307 million, compared to £359 million at31 December 2003, reflecting an exceptionallystrong fourth quarter improvement.

This much improved performance camefrom a marked pick-up in the global marketsfor our Electronics division, which started in the last quarter of 2003, together withcontinued strong growth in global demandfor steel and glass, the most important end markets for the Ceramics division. ThePrecious Metals division delivered a betterresult than last year despite relatively weakconsumer demand for gold jewellery in thepeak fourth quarter shopping season.

The overall improvement also reflects thebenefits from the disposal of the Electronicsdivision’s loss-making equipment businessSpeedline, which was sold in November2003, and from the ongoing restructuringof that division’s Laminates sector whichhas transformed it from loss-making tobreak-even.

Actions taken during 2004 to addressunderperforming businesses included:

Restructuring of Precious Metals in Europe:We closed two manufacturing sites in Franceduring 2004 and consolidated seven salesoffices into three. European production wasreorganised to focus on gold products in theUK and silver products in Spain. Completionof this programme will take place in thesecond quarter of 2005.

Restructuring of Electronics in the USAand Europe: In the second half of the yearwe initiated a further phase of restructuringin the Laminates sector in the USA andGermany including rationalisation of theUS-based divisional head office. Completionof the US initiatives and implementation ofa social plan in Germany, which has beenagreed with the local unions, are scheduledto take place in the first half of 2005.

Disposals and rationalisation in Ceramics:As part of our strategy to exit low margincommodity activities, in December 2004 wesold two refractory brick making businessesbased in Belgium and Germany for a cashconsideration of £1 million. We alsolaunched a project to rationalise productionin NAFTA and expand our Mexican plant.

These measures, the costs of which arereported in the exceptional charges, will yieldimproved operating results going forward.

Strategic reviewSince my arrival in July 2004, I haveundertaken a thorough review of Cookson’soperations and with the Board haveconducted a complete strategic review, the result of which we presented to thefinancial markets on 18 January 2005. The full presentation is available on ourwebsite, www.cooksongroup.co.uk, and

I highlight the main conclusions from thereview below:– there has been a common misconception

that Cookson is a pure electronicscompany. In reality, since the disposal of Speedline and with the restructuring of Laminates, less than 30% of our salesand profits come from electronics markets;

– all our main businesses command strongmarket share and technology positionsand have production facilities that arewell adapted to their geographic markets.However, more can be done to improveperformance; and

– the Group has adequate financialresources. The new £200 millionunsecured bank facility is a clear andtangible confirmation of our improvedfinancial condition and prospects.

StrategyAs a result of the review, the Group willpursue a strategy which incorporates the following.

Our operational focus will be ondeveloping the performance of our corebusinesses by capitalising on existingstrong market shares and technologicalexpertise and investing further in growingmarkets. Operational improvement plansare being introduced at all businesseswhich are designed to produce markedgains in competitiveness, profitability andcash generation. These plans revolvearound the following principles:

Products and markets: We will focus onhigher technology, higher margin products,maintaining a high R&D spend and exitingcommodity activities.

“We have fundamentally sound positions in our markets, good products and technologies and a great team of committed people

worldwide who are striving to deliver continuous improvements in customer service and returns to our shareholders”

Nick Salmon Chief Executive

Investment and restructuring: We have awell balanced geographic match betweenour production facilities and our customermarkets. That is to say “we make where we sell”, critical because in all our activitieswe need to be a “just-in-time” supplier (see charts below). Today 37% of our sales originate from NAFTA, 36% from the EU and 27% from the Rest of the World,principally Asia-Pacific. We anticipatestrongest market growth in Asia-Pacific andthe Rest of the World. NAFTA is expected toshow continued, albeit modest, growth whilstEurope is expected to decline slowly. We willprogressively adapt our production capacitiesto the evolution of our geographic markets,investing in new production capacity inemerging markets while restructuring asnecessary in mature markets.

Cost reduction: We will simplify ourstructure and take out costs, particularlyoverhead costs. We have already identifiedcentral cost savings of some £3 million. We will continue to focus on improving theeffectiveness of our materials purchasingas nearly 50% of our cost of sales is in raw materials.

Specific examples of how these principlesare being applied in each division can befound in the Operating and Financial Reviewstarting on page 11.

ObjectivesBy focusing on our activities in this way, wewill create the right platform from which wecan develop our higher growth, higher marginbusinesses in order to achieve the margintargets outlined in the strategic review:10% return on sales by 2007 for both theCeramics and Electronics divisions and15% return on net sales value (i.e. excluding

the precious metal content) for the PreciousMetals division.

We also plan to reduce debt significantlyover the next 2-3 years through a combinationof stronger operational cash flow – fromimproved profitability and working capitalmanagement – and a disposal programmewhich aims to raise over £100 million fromthe sale of a number of non-core businessesfrom across all three divisions. The sale ofthe fraternity rings business, from thePrecious Metals division, in December 2004for £3 million was a first step in thisprogramme.

We are also repositioning Cookson fromits historical perception as a highly cyclicalstock and intend to resume a sustainabledividend payment as soon as possible,with dividends funded from free cash flow.

ObservationsThis is my first year in the Group. Sincejoining in July, I have travelled extensivelyaround our global operations, meetingemployees and customers. This experiencehas convinced me that we have fundamentallysound positions in our markets, goodproducts and technologies and a great teamof committed people worldwide who arestriving to deliver continuous improvementsin customer service and returns to ourshareholders. Some senior managementchanges have been necessary and I amvery confident that the internal promotionsof Steve Corbett to Chief Executive of theElectronics division, Rick Richesin to ChiefExecutive of the Laminates sector andHuub van Dunn to Chief Executive of theChemistry sector will bring improvedperformance in their respective businesses.

I have been pleased to see a strong and

sincere commitment to ensuring world classhealth, safety and environmental compliancein all our facilities in all regions. Furthermore,I have been favourably impressed with the Group’s internal controls and overalloperational structure, which combine arelatively lean, decentralised operatingapproach with strong central financial controland governance functions. This year has alsoseen an enormous effort to ensure timelyimplementation of new regulatory standardssuch as IFRS and the Sarbanes-Oxley Act.

OutlookTrading in the early weeks of 2005 suggeststhat the robust market conditions experiencedby the Ceramics division in 2004 arecontinuing. In the Electronics division, therewas evidence in late January and Februarythat customers were de-stocking inventoriesof some higher margin products, althoughmomentum now appears to be returning.The relatively weak retail trading environmentwhich impacted the Precious Metals division throughout the second half of 2004 continues but many jewellery industryobservers remain optimistic of a recovery.

From this position, we are confident thatwe can deliver additional improvements in2005 as we execute our strategy to enhanceoperational performance, strengthen ourbalance sheet further via the disposalprogramme and build on our core businesses.

Nick Salmon Chief Executive15 March 2005

10Cookson Group plc Annual Report 2004

CHIEF EXECUTIVE’S STATEMENT CONTINUED

Group:Turnover by division

Group:Turnover by location of operation

Group:Turnover by customer location

Group:Operating profit by division

44% Ceramics39% Electronics17% Precious Metals

33% USA29% Continental Europe21% Asia-Pacific9% United Kingdom8% Rest of the World

30% USA27% Continental Europe24% Asia-Pacific11% Rest of the World8% United Kingdom

48% Ceramics44% Electronics8% Precious Metals

11Cookson Group plc Annual Report 2004

OPERATING REVIEW

Group performanceTurnover for the Group’s continuingoperations, including joint ventures, was11% higher in 2004 than 2003 at constantexchange rates and 5% higher at reportedexchange rates. In the second half of 2004,turnover increased by 10% at constantexchange rates over the second half of 2003 and fourth quarter turnover of£437 million was 4% higher than the same quarter last year. These growth ratesreflect the fact that Group performance had begun to recover in the second half of 2003, particularly in the fourth quarter.

Higher profits from continuing operationsacross all three divisions resulted in a 60% increase in operating profit in 2004 at constant exchange rates and a 47%increase at reported exchange rates. Fourthquarter operating profit of £35.6 millionwas 18% higher than the same quarter last year at constant exchange rates. Allthree divisions registered improvements in operating profit for the year over 2003:Ceramics increased by £10.6 million (23%),Electronics was £30.0 million (154%) higherand Precious Metals was up £1.7 million(23%). Profits from joint ventures rose by£2.3 million at constant exchange rates to £4.0 million (up £2.0 million at reportedexchange rates).

Return on sales for the Group’scontinuing operations of 7.0% improved by2.1 percentage points in 2004 at constantexchange rates and 2.0 percentage pointsat reported exchange rates. It has risensequentially in each half year since thebeginning of 2003. All divisions recordedyear-on-year rises in return on sales.

The fastest growing and most profitableregion for the Group continued to be Asia-Pacific which accounted for 24% of theGroup’s customer base in 2004 and 47%of operating profit. The USA remained theGroup’s largest region in terms of turnover,representing 30% of the total in 2004. Therewas a major improvement in profitability inthis region where rationalisation initiativesthat had commenced in 2003 and 2004began to bear fruit.

Divisional performanceCeramics divisionKnown in its markets as Vesuvius,Cookson’s Ceramics division is the worldleader in the supply of advanced flowcontrol refractory products to the iron andsteel industry. It is also a leading supplier of refractory linings and speciality refractoryproducts for iron and steelmaking, the glassindustry, ferrous and non-ferrous foundriesand other industrial processes.

Market overviewThe Ceramics division benefited fromimproved market conditions in its majormarkets that began to take hold in thesecond half of 2003 and continuedthroughout 2004.

The division’s largest sector is Iron and Steel, resulting in some two-thirds ofits sales and profits being linked to steelproduction volumes. In 2004 global steelproduction rose by almost 9%, surpassingone billion tonnes for the first time. Chinaconfirmed its position as the world’s leadingsteel producer with year-on-year growth of 23% and accounted for over 25% of the

world’s total production in 2004. ExcludingChina, global production was 4.5% higher in2004 with the USA, the EU, Russia, Ukraineand Brazil each growing by around 5%,whilst Japan and South Korea were some3% higher. Steel prices rose strongly in 2004,strengthening the industry’s financial position.

The steel industry continued to consolidatein 2004. Mittal Steel – formerly LNM – isnow the world’s largest steelmaker withcapacity of some 70 million tonnes across14 countries. The world’s top six producersrepresented 23% of global steel output in2004, up from 19% in the previous year.

The end markets of the Foundry, Glassand Industrial Products sectors are generallylinked to GDP growth and thereforebenefited from a year of overall globaleconomic growth. The most importantmarkets for these sectors are constructionand automotive, both of which experiencedimproving market conditions in 2004.

Divisional performance and initiativesThe Ceramics division recorded a strongoverall performance in 2004 as a result ofthe buoyant global steel industry and stableconditions in its other markets. Turnover for the year of £739 million, excluding joint ventures, was 5% higher than 2003 at reported exchange rates and 11% higherat constant exchange rates. Operatingprofit grew by 14% at reported exchangerates to £56.8 million and was up 23% at constant exchange rates. Return onsales was 7.7%, up from 6.9% at constantexchange rates in the previous year. Thefourth quarter was particularly strong withsales at record levels.

8

6

2

4

0

H204

H104

H203

H103

75

50

25

0

H204

H104

H203

H103

900

600

300

0

H204

H104

H203

H103

2004 2003

First half 842 746Second half 856 778

Year 1,698 1,524

Group – continuing operations: Turnover £m

2004 2003

First half 55.1 29.8Second half 64.5 45.2

Year 119.6 75.0

Group – continuing operations: Operating profit £m

2004 2003

First half 6.5 4.0Second half 7.5 5.8

Year 7.0 4.9

Group – continuing operations: Return on sales %

Refer to the Glossary of Technical and Financial Terms on page 76. All charts and tables at constant exchange rates unless otherwise stated.

The Iron and Steel sector accounted for 65% of turnover for the year, the Glasssector accounted for 12% and the Foundryand Industrial Processes sectors 9% and14% respectively.

Regionally, Europe (including the UK) wasthe division’s largest region, accounting for41% of turnover. The USA contributed 30%of turnover, Asia-Pacific 13% and the Restof the World 16%.

Two plants based in Belgium and Germanywhich made bricks used in glass-makingfurnaces were divested during 2004.

Sector performanceIron and SteelThe Iron and Steel sector principally suppliestwo kinds of products to steelmakers: liningsin the form of either bricks or monolithicswhich are used to line the main steelmakingvessels; and flow control products whichcontrol and protect the stream of moltenmetal as it passes through the steelmakingprocess, particularly during continuouscasting, the most important of which areVISO products and slide gate systems.

Strong industry conditions resulted in a 13% increase in turnover for 2004 atconstant exchange rates, an increase of6% at reported exchange rates. Sales ofthe high technology, higher margin flowcontrol products were some 7% higherthan last year whilst lining and constructionrelated sales increased by 15%.

Regionally, the sector’s performancereflected the trends seen in its served markets.

Steel production in Asia increased by13% from 2003 to 2004. The sector’s sales showed a 42% increase year-on-

year. Chinese production remained strongdespite government attempts to slowgrowth. With its expanding VISO and slidegate plants in Suzhou, Vesuvius is wellpositioned to take advantage of futureopportunities in China in spite of increasinglocal competition. The Indian marketcontinued to grow in line with spending oninfrastructure projects. Thailand outperformedits SE Asian neighbours, which remainedfairly static. The Australian, Japanese,Korean and Taiwanese markets were stable.

The enlarged 25-member EU reported5% growth in steel production in 2004,with Poland, Spain and Italy recording the biggest increases. Outside the EU,Turkey, Russia and Ukraine all increasedtheir production. The division’s sales inEurope remained stable in the maturemarkets and showed a stronger increase in the emerging markets of Central Europe.

2004 was clearly a year of marketrecovery in NAFTA after several disappointingyears, with an overall increase of 5% in steelproduction, led by a 5% increase in the USAand a 10% increase in Mexico. The sector’ssales grew in line with these strongerproduction levels.

2004 saw several price increases in rawmaterials. In addition, there were adverseprice moves in oil, energy and transportation.As a result, Vesuvius has embarked upon amajor price increase programme, with effectfrom January 2005.

The Iron and Steel sector introduced anumber of new products during the year.The introduction of a new range of robust,user-friendly, low maintenance slide gatemechanisms has been completed; the

four new gates cover the full range fromvery small mini mill ladles to very largeintegrated steel shop ladles and replace 28existing models. A new sprayable insulationproduct, known as Thermacoat, has beensuccessfully launched with equivalentproperties to fibre material.

An in-depth review of NAFTA plantsresulted in a decision to upgrade the VISO facilities at Charleston, Illinois andMonterrey, Mexico and to cease operations at the Hillsboro, Texas facility. In China, it was decided to increase the Group’sshare of the slide gate joint venture withWuhan Iron & Steel from 25% to 50% witheffect from 2005 and efficiency improvementmeasures are being implemented. Investmentis also being made to increase VISO capacityat the Suzhou plant.

In Poland, in order to support thegrowing Central European market, VISOproduction capacity is being increased andthe slide gate refractory line modernised to enable Vesuvius Poland to manufacturethe latest slide gate refractory technology.

GlassThe Glass sector supplies a wide range of refractories used in the glass-makingindustry and specialist ceramic productsused in glass processing.

Demand for flat glass is primarily dependentupon conditions in the construction andautomotive industries, as a result of which itis prone to a reasonable degree of cyclicality.After a number of challenging years, the lasttwo years have experienced recovery on a global scale. Despite competition fromplastics and other materials, glass remains

12Cookson Group plc Annual Report 2004

OPERATING REVIEW CONTINUED

10

6

8

2

4

0

H204

H104

H203

H103

35

25

30

15

20

5

10

0

H204

H104

H203

H103

400

300

200

100

0

H204

H104

H203

H103

2004 2003

First half 358 330Second half 381 337

Year 739 667

Ceramics: Turnover £m

2004 2003

First half 25.9 22.4Second half 30.9 23.8

Year 56.8 46.2

Ceramics: Operating profit £m

2004 2003

First half 7.2 6.8Second half 8.1 7.1

Year 7.7 6.9

Ceramics: Return on sales %

13Cookson Group plc Annual Report 2004

the material of choice for glazing and the packaging of many drinks and otherliquids, and the demand for container glasscontinues to be strong.

Turnover for the Glass sector increasedby 18% in 2004 compared with the previousyear at constant exchange rates, up 11%at reported exchange rates. In the hotfurnaces area, our US business Monofrax,which manufactures fused cast productsused in glass-making furnaces, performedstrongly due to expansion in Europe andAsia and the weak US dollar. In the area of glass transforming, all product linesperformed well compared to last year. Themain applications for fused silica (solar andglass transforming) enjoyed market growth.Solar grew by 30% and, despite strongcompetition, Vesuvius has maintained itsmarket share. Technical ceramics alsogrew strongly compared to last year.

Monofrax has developed a new applicationin nuclear waste treatment furnaces and in thin glass applications. Additionally, new metallurgical applications are beingfound for Zyarock rollers in silicon steel andstainless steel annealing and galvanising. Anew generation of tempering rolls is beingdeveloped and jumbo crucibles are beingvalidated by Japanese customers, offeringnew opportunities for growing business.

The fused silica plant in Kua Tang, Chinawas expanded during the past year with theopening of the second phase in January2004. This plant is our most modern and, along with the production of glasstempering rollers, it can now manufacturelarge diameter ceramic rollers, opening up new business opportunities in float

line furnaces which were previously theexclusive domain of steel rollers.

FoundryThe Foundry sector supplies an extensiverange of high performance refractory productsto ferrous and non-ferrous foundries.

The sector recorded turnover for the year which was 10% higher than last yearat constant exchange rates and 3% higherat reported exchange rates.

In NAFTA, market conditions improved inall areas, particularly in investment castingand steel foundries. In Europe, overallmarket conditions remained flat, althoughinvestment casting activities were morerobust as a result of improvements in theaerospace and industrial gas turbine sectors.NAFTA and Europe were both impacted by imported castings from China. In Asia-Pacific, continued strong growth in theChinese foundry sector reflects the generaleconomic acceleration in that region.

A number of new products wereintroduced in 2004 including filters for ironfoundry applications and low pressure stalktubes for the manufacture of automotivecomponents including aluminium wheels.Continued development of monolithics for the full range of foundry applicationssupported growth in this important productsector, particularly for aluminium castingapplications, taking advantage of largeprimary aluminium plant expansion projects in the Middle East. Developmentof customised rotary degassers for use in the purification of molten aluminium alsoresulted in business expansion with majoraluminium manufacturers.

In line with general market trends, keyresources were relocated to China.

Industrial ProcessesThe Industrial Processes sector provides a wide range of refractory products for a diversified range of industries which in general follow GDP trends, includinghydrocarbon processing, petrochemical,cement and incineration. Unlike most of theCeramics division’s activities, the activities ofthe Industrial Processes sector are mainlyproject-based and therefore linked to overallnew investment and renewal projects.

Sales for this sector in 2004 were 1%lower than 2003 at constant exchange ratesand 4% lower at reported exchange rates.

The strongest performing area wasconstruction and installation, driven by a number of major projects. The primaryaluminium industry remained stable overall,although NAFTA was weak.

Several new products were developedfor various industries including new bricksfor anode bake furnaces, chlorinators, gasturbines and coal gasification applications.A new range of basic bricks was introducedfor the cement and lime industry, enablingVesuvius to provide a full lining offering. Inmonolithics, a new range of non-wettingmonolithics has been developed foraluminium casthouses.

31% Continental Europe30% USA16% Rest of the World13% Asia-Pacific10% United Kingdom

Ceramics: Turnover by location of operation

65% Iron and Steel14% Industrial Processes12% Glass9% Foundry

Ceramics: Turnover by sector

28% USA27% Continental Europe19% Rest of the World18% Asia-Pacific8% United Kingdom

Ceramics: Turnover by location of customer

Electronics divisionOverview2004 was a year of change for theElectronics division with importantdevelopments in terms of both leadershipand focus.

Steve Corbett became Chief Executiveof the division in October, succeeding Ray Sharpe who resigned in May. Stevejoined Cookson in 1990 and prior to thisappointment had been Chief Executive of the Chemistry sector since 2002. Steve has initially assumed responsibilityfor the Chemistry and Assembly Materialssectors as well as divisional staff and R&D functions.

Changing customer attitudes towardssuppliers of materials for PCB fabricationand assembly resulted in a realignment ofthe division’s product and service offerings.Customers no longer value the “one stopshop” approach which the division’selectronics materials businesses had pursuedin recent years. Instead, they prefer to retaina competitive market throughout the supplychain. The Electronics division has thereforesought to unbundle its PCB-orientedproducts and services, in particularLaminates and Chemistry. This has enabledthe Chemistry sector to reposition resourcesto its important industrial markets – whichaccount for 50% of its business – andallowed Laminates to focus on returning to and then maintaining profitability.

Market overviewThe improved market conditions thatbecame evident in the last quarter of 2003 continued throughout 2004 for much of the global electronics industry.

Amongst the industry’s end markets, the established market drivers of PCs andmobile handsets grew strongly. WorldwidePC shipments grew by nearly 12% in 2004,accelerated by better performance andwireless accessibility. Mobile handsetvolumes were nearly 30% higher than in 2003 and recorded the highest evershipment level in the fourth quarter of 2004.Hard disk drive unit volumes grew by 24%versus 2003, fuelled by soaring demand for DVD recorders, game consoles andMP3 players. Consumer electronic devicescontinue to drive the electronics industry toan ever-increasing degree.

Regionally, Asia-Pacific experienced thestrongest industry growth in terms of bothproduction and local end market demand.PC shipments, for example, grew by 16%over 2003, driven in particular by growth in China and India. North America alsoexhibited good year-on-year growth whileEurope was more subdued.

The transition to lead-free productsaccelerated in 2004 in line with newregulations in Japan and the EU whichcome into force in 2005-2006. The use oflead-free products is a significant change,not just for the Assembly Materials sectorwhose solder products have traditionallycontained lead. Non-lead solders melt at higher temperatures and so all otherPCB components, including laminates and fabrication chemistries, must also be able to withstand these temperatures.

Divisional performance and initiativesThe Electronics division’s turnover andprofits grew significantly over the previousyear in 2004 as a result of more favourable

market conditions, new productintroductions, market share gains and alower cost base. Turnover of £626 million,excluding joint ventures, increased by 10%at reported exchange rates and by 19% at constant exchange rates. Operating profit excluding joint ventures grew 138% at reported exchange rates to £49.5 million, an increase of 154% at constant exchangerates. The division’s return on sales increasedfrom 3.7% in 2003 to 7.9% in 2004.

Assembly Materials was the division’slargest sector, accounting for 45% of bothturnover and operating profit. Chemistry,the most profitable sector, accounted for34% of turnover and 55% of operatingprofit. Laminates provided 21% of turnoverand made a marginal contribution tooperating profit.

Asia-Pacific continued to be thedivision’s fastest growing region and was responsible for 36% of turnover, an increase of five percentage points over 2003. To support this growth, newproduction and support facilities wereopened in China and India during thecourse of the year. Europe (including theUK) accounted for 31%, the USA 29% and the Rest of the World 4%.

2004 represented the first full year thatall three sectors implemented Six Sigma.Laminates and Chemistry started down the Six Sigma path four years ago andhave reaped many benefits in the form of hard cash savings, improved systemsand processes and – most importantly – alarge population of Black Belts and GreenBelts who systematically solve everydayproblems using Six Sigma methodology.Assembly Materials introduced Six Sigma

14Cookson Group plc Annual Report 2004

OPERATING REVIEW CONTINUED

36% Asia-Pacific29% USA26% Continental Europe5% United Kingdom4% Rest of the World

Electronics: Turnover by location of operation

10

6

8

2

4

0

H204

H104

H203

H103

30

20

10

0

H204

H104

H203

H103

350

200

250

100

150

50

0

300

H204

H104

H203

H103

2004 2003

First half 308 258Second half 318 269

Year 626 527

Electronics: Turnover £m

2004 2003

First half 23.3 6.3Second half 26.2 13.2

Year 49.5 19.5

Electronics: Operating profit £m

2004 2003

First half 7.6 2.4Second half 8.2 4.9

Year 7.9 3.7

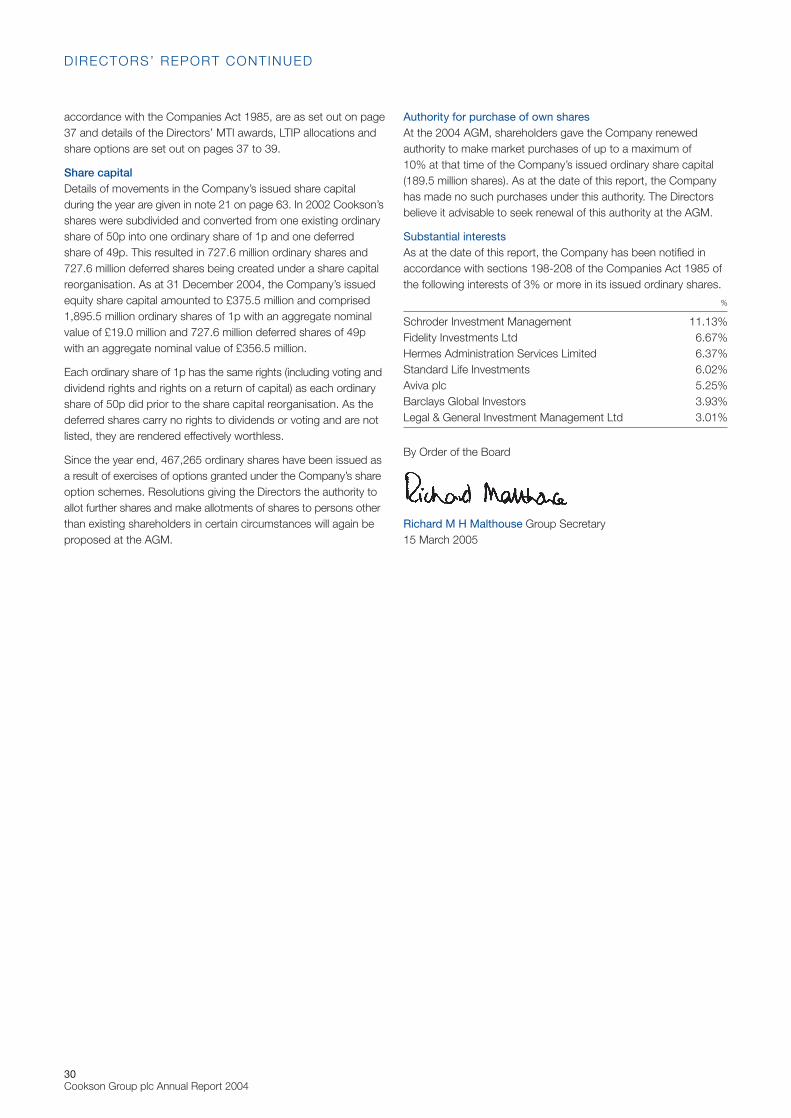

Electronics: Return on sales %

15Cookson Group plc Annual Report 2004

early in 2004 and has already graduated a population of certified Black and GreenBelts. The Six Sigma culture is now firmlyestablished within the Electronics divisionfor the benefit of our own businesses andthose of our suppliers and customers.

Sector performanceAssembly MaterialsThe electronics industry accounts forapproximately 70% of Assembly Materials’turnover, with the remaining 30% going intoa variety of industrial and medical applications.

Turnover in 2004 increased by 18% atreported exchange rates to £280 million, up 28% at constant exchange rates.Approximately two-thirds of this increase wasdirectly related to the price of tin – the sector’smajor raw material – which rose on averageby some 75% and was, in the main, passedon to customers during the course of theyear. Operating profit of £22.2 million was37% higher than last year at reportedexchange rates and 47% higher at constantexchange rates. Return on sales improvedto 7.9%, despite the tin price impact.

Asia-Pacific, the sector’s largest region,accounted for 41% of sales in 2004. TheUSA accounted for 30%, Europe 25% andthe Rest of the World 4%.

The transition to lead-free solder productscontinued to be an important technologydriver for the sector in 2004 with theconversion to these products increasingsignificantly across all product lines. Formetal products (bar and wire), lead-freevolumes doubled over the prior year. Forsolder pastes, lead-free increased by 30%.Lead-free solder sphere volumes increasedfive-fold to 11% of total sphere sales.

Tin is the sector’s single largest rawmaterial with purchases in 2004 amountingto some £90 million. During the last year the price of tin increased significantly which has highlighted the need for effectiveraw materials management, achieved via a global hedging programme and pricingmechanisms which enable higher rawmaterial prices to be passed on to customers.Additionally, maintaining active relationshipswith major tin producers and minersensures continuity of supply.

The Semiconductor Packaging materialsbusiness faced difficult market conditions in2004. Revenues were flat compared to 2003.Epoxy mould compound volumes wereessentially flat versus the prior year. Soldersphere volumes declined, although highermargin lead-free sphere volumes were upsignificantly, resulting in much improvedoverall gross margins. The microelectronicsoldering products and polymers segmentsexperienced solid growth.

Specialty Coating Systems (SCS) had anexcellent year, with growth in the coatingservices and equipment segments of itsbusiness. Medical applications continue to provide growth opportunities for SCS.

In October, a state-of-the-art researchcentre was opened in Bangalore, India,which will focus on developing leadingedge technologies for a wide range ofapplications including electronics assembly,nano-technology and opto-electronics.

ChemistryEnd markets for the Chemistry sector’sproducts are split equally between electronicsand other industries, including automotive,plumbing, furniture and military.

Huub van Dunn succeeded Steve Corbettas Chief Executive of the sector in November.Huub was previously President of theChemistry sector’s European businesses.

Each geographic region of the worlddisplayed subtly different market dynamicsin 2004. The demand for PCB fabricationchemistries was strong in Asia-Pacific with revenues increasing in excess of 20%.In Europe, this product segment grewmarginally; in the Americas, marketcontraction persists as the sector’scustomer base continues to consolidateand moves to Asia. In response to this, adecision was reached during 2004 to closea manufacturing facility located on the WestCoast of the USA, to be completed in 2005.

The microelectronics product lines,including semiconductor copper, wererobust, growing some 30% over the prioryear on a worldwide basis.

Overall, the industrial markets showedgood growth across all regions in 2004,especially the automotive and plumbingsegments. Of particular note, the sectorachieved significant market penetration in aluminium wheel plating in China.

In the second half of the year it wasdecided to withdraw from certain low margin,precious metal decorative product lines. Asa result of the withdrawal from these preciousmetals activities, the Chemistry sector’sturnover of £214 million was essentiallyunchanged year-on-year at reportedexchange rates, with an improvement of 5% recorded at constant exchange rates.Operating profit improved markedly to£27.2 million, up 35% at reported exchangerates and 45% at constant exchange rates.Return on sales rose to 12.7% for the year.

10

6

8

2

4

0

H204

H104

H203

H103

15

10

5

0

H204

H104

H203

H103

150

100

50

0

H204

H104

H203

H103

2004 2003

First half 134 106Second half 146 113

Year 280 219

Assembly Materials: Turnover £m

2004 2003

First half 10.3 7.1Second half 11.9 7.9

Year 22.2 15.0

Assembly Materials: Operating profit £m

2004 2003

First half 7.6 6.8Second half 8.2 7.0

Year 7.9 6.9

Assembly Materials: Return on sales %

125

75

100

50

25

0

H204

H104

H203

H103

2004 2003

First half 107 102Second half 107 101

Year 214 203

Chemistry: Turnover £m

Geographically, the sector’s largest regionwas Europe, which also has the largestproportion of non-electronics activities, and accounted for 42% of the sector’sturnover for 2004. The USA provided 29%of turnover, Asia-Pacific 23% and the Restof the World 6%.

Investment during the course of the yearlargely focused on two areas. Firstly, theunbundling of the Laminates and Chemistrysectors’ offering to PCB fabricators allowedChemistry to reallocate resources to itsimportant non-electronics industrial marketsand products. These include: plating onplastic, an exciting development withparticular use in automotive applications;environmentally friendly products includinghexavalent chromium-free, lead-free andcadmium-free; and improved corrosion and wear resistant coatings.

Secondly, the sector continued to buildits global presence in line with customerneeds. In particular, the business continuesto develop in Asia-Pacific with significantadditions to the region’s technicalsalesforce made during 2004. To supportthis growth, a technical centre was openedin Shenzhen, China and a divisional salesand technical support laboratory wasestablished in Shanghai. Elsewhere,activities in Mexico have been expanded.

During the course of 2004, theChemistry business was challenged by rising raw material costs. In particular,nickel prices increased significantly as didraw materials and packaging materialslinked to petrochemical precursors. Priceincreases were implemented to pass along the increased raw material costswhere possible.

Competition continues to drivecommoditisation in the PCB fabricationmarket, particularly in primary imaging. All major competitors are targeting theexplosive growth in Asia and are investingin facilities and support personnel.

LaminatesLaminates, the only one of the division’sthree sectors whose products are soldexclusively into the electronics industry,continued to recover in 2004 from thethree-year industry downturn it hadexperienced since 2001. In October, the sector’s Chief Operating Officer Rick Richesin replaced Joe Santolucito as Chief Executive.

General market conditions improvedsignificantly during 2004, with demand forproducts related to high reliability serverapplications and lead-free assembly fuellinggrowth. Markets for specialised substratesin automotive and high-frequency applicationswere also strong.

Sector turnover increased by 16% overthe previous year at reported exchangerates to £132 million, an increase of 26% at constant exchange rates. Laminatesoperated at around break-even in 2004, aconsiderable improvement on the loss of£15.6 million recorded in 2003 at reportedexchange rates (£14.3 million at constantexchange rates).

The regional split showed the ongoingimportance of Asia-Pacific which accountedfor 46% of the sector’s turnover in 2004.The USA provided 28% of turnover andEurope 26%. Year-on-year turnover growthin Asia-Pacific was 61%, whilst the USA andEurope grew by 12% and 3% respectively.

Despite lower growth in the USA and Europe,management believes that a presence inboth regions is required; although massPCB production has largely relocated toAsia-Pacific, much of the specification andqualification process continues to takeplace in the West, as does production ofhigh-performance PCBs. The just-in-timenature of the electronics supply chainrequires local production facilities to meetthe very short lead times of 24 to 48 hours.

High-performance laminates havebecome the sector’s main focus during thecourse of the year. These products, whichinclude high-reliability epoxy products usedin lead-free PCBs and enhanced electricallaminates such as GETEK, currentlyaccount for some two-thirds of the sector’ssales and it is management’s intention toincrease this further at the expense ofstandard performance laminates which are becoming commoditised and largelythe domain of low-cost Asian producers.

2004 saw further restructuring in order to meet changing customer requirementsand to reduce costs. Investment continuedin Asia-Pacific. New production capacity for GETEK products was installed andcommissioned mid-year in Taiwan and inthe fourth quarter additional capacity forboth laminate and prepreg was added at the Huizhou facility in Southern China.Restructuring also continued in the USA withthe closure of the sector’s head office andthe installation of fully automated productionlines at both US plants during the course of the year. In Europe, a plan has beenannounced that will reduce capacity inGermany by 75% and thereby focus Europeanproduction at one major plant in Sweden.

16Cookson Group plc Annual Report 2004

OPERATING REVIEW CONTINUED

5

0

–10

–5

–15

H204

H104

H203

H103

75

50

25

0

H204

H104

H203

H103

2004 2003

First half 66 50Second half 66 55

Year 132 105

Laminates: Turnover £m

2004 2003

First half 0.6 (10.0)Second half (0.5) (4.3)

Year 0.1 (14.3)

Laminates: Operating profit £m

15

10

5

0

H204

H104

H203

H103

2004 2003

First half 12.5 9.1Second half 14.7 9.7

Year 27.2 18.8

Chemistry: Operating profit £m

2004 2003

First half 11.6 8.9Second half 13.8 9.7

Year 12.7 9.3

Chemistry: Return on sales %

15

10

5

0

H204

H104

H203

H103

17Cookson Group plc Annual Report 2004

Raw material costs increased sharply for two of the sector’s main commodities,copper foil and woven glass cloth. Epoxyresin prices also increased, driven byescalating oil prices. Shortages of bothcopper and glass cloth were evident duringthe first half of 2004 as suppliers restrictedcapacity in order to drive up prices. Thesecosts were passed on to customers throughprogrammed price increases during thefirst three quarters of the year.

Significant market share increases wereachieved in both the USA and Asia. Newmulti-year supply agreements with threemajor PCB manufacturers were successfullycompleted, owing to our advanced productportfolio and global geographic presence.

Precious Metals divisionMarket overviewIn 2004, the Precious Metals division facedchallenges in both its leading markets, theUSA and Europe. Demand for finishedjewellery products is influenced to a largeextent by both consumer confidence andconsumer preferences. The fourth quarteris the most important for many retailbusinesses and consumer confidence was depressed in the USA and Europethroughout much of this period. This wasreflected in the experience of retailers in general in these regions where thenormal Christmas shopping season began later and was shorter in durationthan anticipated, leading to disappointingresults across the retail sector.

The preference of buyers and wearers of jewellery for white metals and gemstonejewellery rather than yellow gold items, whichhad been noted in 2003, continued in 2004.

The price of precious metals – particularlygold – also has an impact on jewellerydemand as retailers are reluctant to holdinventory when prices are high. Goldtraded in a range from $375/ounce to$455/ounce during the year, reaching itspeak in early December. The price of silverreached a high for the year of $8.22 in earlyApril before falling to its low point of $5.44in mid-May.

The major destocking programme, ledby US giant Wal-Mart, which took place in the first half of 2003, was not repeatedduring 2004.

Divisional performance and initiativesThe division’s turnover of £288 million was 7% lower than last year at reportedexchange rates and 1% lower at constantexchange rates. Net sales, which excludethe precious metal content, of £116 millionwere also 7% lower than 2003 at reportedexchange rates and 1% lower at constantexchange rates. Despite lower turnover,operating profit for 2004 increased by 8%at reported exchange rates to £9.3 million,a rise of 22% at constant exchange rates.Return on net sales was 8.0%, up on lastyear’s figure of 6.9%.

Turnover for the division’s US operationsincreased by 9% at constant exchange ratesas a result of the return to more normaltrading conditions and the non-recurrenceof the major destocking programme seenin 2003. In Europe, however, turnoverdecreased by 10% as a result of theFrench rationalisation programme and the closure of some retail outlets in Spain.

As a result of higher consumer demandfor silver jewellery items, in 2004 and in

early 2005 measures were taken to increaseboth silver capacity and margins earnedfrom silver production.

During 2004, the European businessunderwent significant restructuring in orderto improve profitability. Following agreementwith local unions in May, production wasdiscontinued in France, with the closure of two manufacturing and four distributionfacilities and the relocation of the Frenchsalesforce. Restructuring in activitieselsewhere in Europe has resulted in goldproduction now being focused in the UKand silver production in Spain. These actionshave allowed the European businesses tomake the most efficient use of their resourcesby maximising the use of capacity in orderto address the fast-moving jewellery industryin that region.

In December, the division sold its non-coreUS fraternity rings activities for £3 million.This business had sales of £3 million in 2004and the disposal realised a small net gain.

Joint Ventures (JVs)Joint venture turnover of £45.2 million wasup 16% on 2003 at constant exchangerates. Operating profit from joint ventureswas £4.0 million, a 135% increase atconstant exchange rates. The majority ofJV results related to the Chemistry sector’sJV in Japan. This business performed well,with turnover of £39.6 million up 36% atconstant exchange rates and operatingprofit increasing by £1.6 million at constantexchange rates to £3.5 million. TheLaminates sector’s loss-making JV withFukuda was wound up during 2004 afterrecording sales of £1 million and anoperating loss of £0.4 million in the year.

75

50

25

0

H204

H104

H203

H103

8

4

6

2

0

H204

H104

H203

H103

15

5

10

0

H204

H104

H203

H103

2004 2003

First half 60 56Second half 56 61

Year 116 117

Precious Metals: Net sales value £m

2004 2003

First half 3.3 0.4Second half 6.0 7.2

Year 9.3 7.6

Precious Metals: Operating profit £m

2004 2003

First half 5.5 0.7Second half 10.6 11.8

Year 8.0 6.9

Precious Metals: Return on net sales value %

50% USA32% Continental Europe18% United Kingdom

Precious Metals: Turnover by location of operation

18Cookson Group plc Annual Report 2004

Group profit and loss Profit before tax, exceptional items and amortisation of intangiblesGroup profit before tax, exceptional items and amortisation of intangibles was £93.1 million for 2004, which was£60.5 million higher than 2003. This increasearose as follows: – £44.6 million (60%) increase in operating

profit from continuing operations atconstant exchange rates;

– eradication of losses of £17.0 million that were incurred by operationsdiscontinued in 2003, predominantlySpeedline;

– £5.1 million decrease in interest; and– £6.2 million adverse exchange rate

translation variance for operating profit of continuing operations.

The adverse exchange rate translationeffect arose mainly as a consequence of the weakness of the US dollar and its “tracking” currencies versus sterling.

The decrease in interest in 2004 from£31.6 million to £26.5 million arose primarilyfrom a lower charge for the amortisation ofrefinancing fees and a favourable exchangerate impact of £2.8 million. The averageinterest rate on drawn borrowings, excluding

the amortisation of refinancing fees and thedeferred income from interest rate swaps,was 6.8%, similar to that of 2003. Themargins on the new bank facility arrangedin March 2005 are at a lower level than theprevious facilities.

Exceptional items and amortisation of intangibles Operating exceptional itemsIn 2004, operating exceptional charges of £22.7 million (2003: £22.2 million) arose,consisting of £7.9 million of asset write-offsand £14.8 million of cash-related costs. Ofthe total charge for 2004:– £2.9 million arose in the Ceramics

division for the rationalisation of threemanufacturing facilities in the USA;

– £9.9 million related to programmes tooptimise the manufacturing capacity andproduct offering of the Laminates sectorof the Electronics division in the USA andEurope and to reorganise the divisionaland sector management structures; and

– £9.9 million arose in respect of theprogramme to reorganise the PreciousMetals division’s European operations.

An exceptional interest charge of £2.4 millionarose in 2003; no charge arose in 2004.

Net loss on disposal of operationsA net loss on disposal of operations of £39.8 million arose in 2004 (2003:£165.7 million), consisting of a net lossbefore goodwill of £27.5 million and awrite-back/off of goodwill of £12.3 million,primarily from the following:– sale of two brickmaking plants in

Europe in the Ceramics division (£33.2 million); and

– winding up of the Cookson Fukuda joint venture in the UK in which theGroup had a 50% share (£7.4 million).

The net loss in 2003 of £165.7 million wasmainly in respect of the sale of Speedlineand the Precision Products businesses.

Net (loss)/profit on fixed assetsA net loss of £16.8 million in 2004 (2003: £5.1 million profit) was due primarily to a £17.9 million write-down in the value of the Group’s investment in a revenue sharing arrangement put in place in 1998 with ELI Inc. over a fibre optic cable network in the USA.

F INANCIAL REVIEW

Dennis Millard Group Finance Director

2004 2003

Continuing operations 119.6 81.2– Ceramics 56.8 49.8– Electronics 49.5 20.8– Precious Metals 9.3 8.6– Joint ventures 4.0 2.0Discontinued operations – (17.0)

Group operating profit 119.6 64.2Interest (26.5) (31.6)

Profit before tax 93.1 32.6

Group: Profit before tax £m

2004 2003

First half 42.0 5.5Second half 51.1 27.1

Year 93.1 32.6

Group: Profit before tax £m

60

40

20

0

H204

H104

H203

H103

200

150

100

50

0

0403020100

Group: Profit before tax £m 2000-2004

All charts and tables at constant exchange rates unless otherwise stated.

19Cookson Group plc Annual Report 2004