Contribution of the Golf Industry to the Arizona Economy ...

Contribution of the Golf Industry to the Arizona Economy in 2014

Dari Duval Ashley Kerna George Frisvold Kai Umeda Runfeng Li

COLLEGE OF AGRICULTURE & LIFE SCIENCES

CooperativeExtension

Contribution of the Golf Industry to the Arizona Economy in 2014Dari Duval Economic Impact Analyst

Ashley Kerna Economic Impact Analyst

George Frisvold Professor and Extension Specialist

Kai Umeda Extension Specialist

Runfeng Li Graduate Research Assistant

December 2016

COLLEGE OF AGRICULTURE & LIFE SCIENCES

CooperativeExtension

© 2016 The Department of Agricultural and Resource Economics, The University of Arizona.Any products, services or organizations that are mentioned, shown or indirectly implied in this publication do not imply endorsement by The University of Arizona.Issued in furtherance of Cooperative Extension work, acts of May 8 and June 30, 1914, in cooperation with the U.S. Department of Agriculture, Jeffrey C. Silvertooth, Associate Dean & Director, Extension & Economic Development, College of Agriculture Life Sciences, The University of Arizona.The University of Arizona is an equal opportunity, affirmative action institution. The University does not discriminate on the basis of race, color, religion, sex, national origin, age, disability, veteran status, or sexual orientation in its programs and activities.

Contribution of the Golf Industry to the Arizona Economy iii

ContentsAcknowledgments viExecutive Summary 7Introduction 10

Overview 10Motivation 10Economic and Industry Context 10

Methods and Data 14Arizona Golf Facility Survey 14Statistical Methodology and Expansion Factor 15Golf-Related Tourism 15Golf-Related Businesses 15Economic Contribution Analysis 15Residential Real Estate Premiums 16Golf Environmental Analysis 16

Arizona Golf Facilities 17Population and Distribution by Facility Characteristics 17Golf Play 19Facility Revenues 20Facility Expenses 21Facility Employment 22Capital Investment and Renovations 23Charitable Contributions 23

Golf Tourism 24Golf Travelers 24

Out-of-State and Foreign Golfers 24Reason for Visit 24Expenditure Pattern 24

Professional Tournament Spectators 25Estimated Direct Impact of Golf Tourism in Arizona 25

Golf-Related Businesses 26Economic Contribution Analysis 27

Golf Facility Operations Economic Contribution Analysis 28Golf Tourism Economic Impact Analysis 28Golf-Related Businesses Contribution Analysis 29Total Economic Contribution 30

Residential Real Estate Premiums 31Water and Conservation Practices 34

Acreage 34Irrigation Water Used 34

US Geological Survey 35Arizona Department of Water Resources 38

Irrigation Methods 43Management Strategies 44Irrigation Audits 45

Contribution of the Golf Industry to the Arizona Economyiv

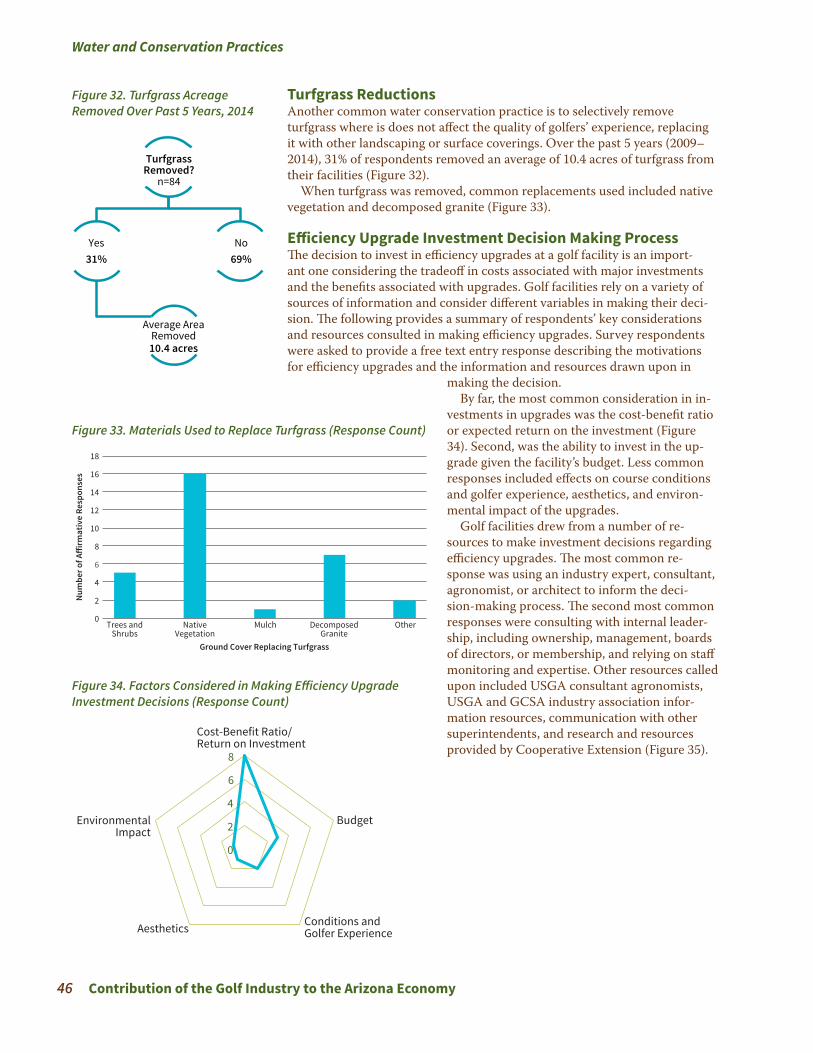

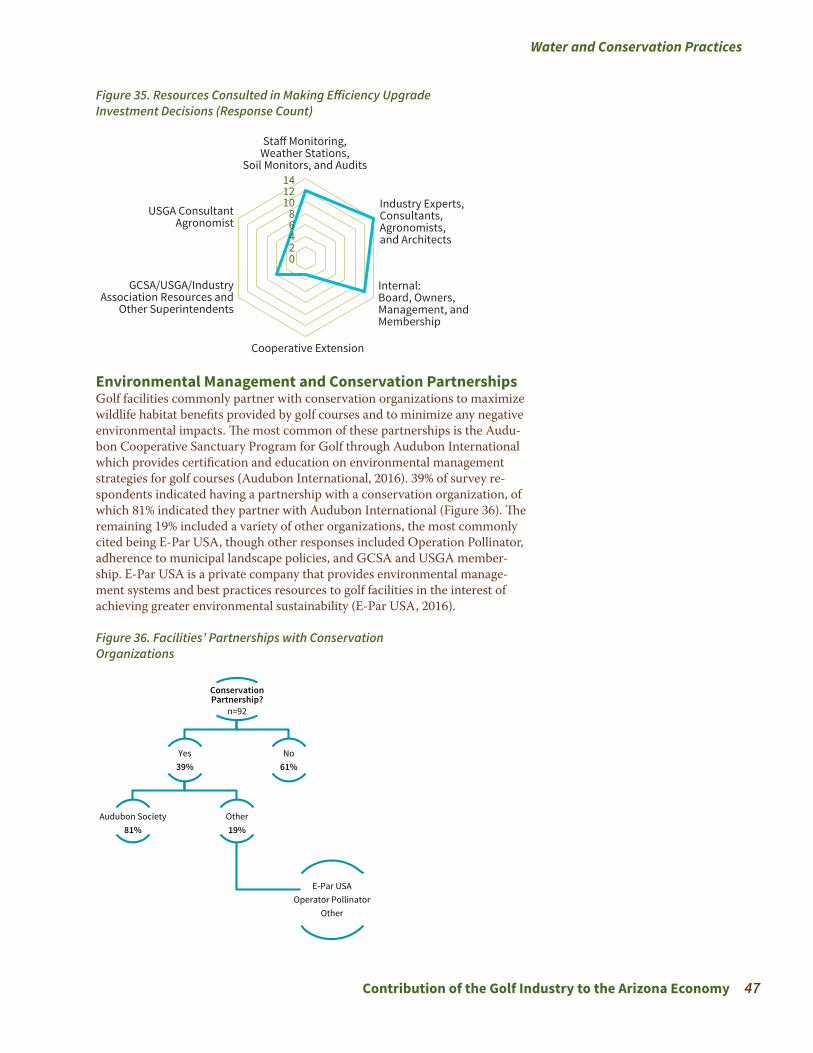

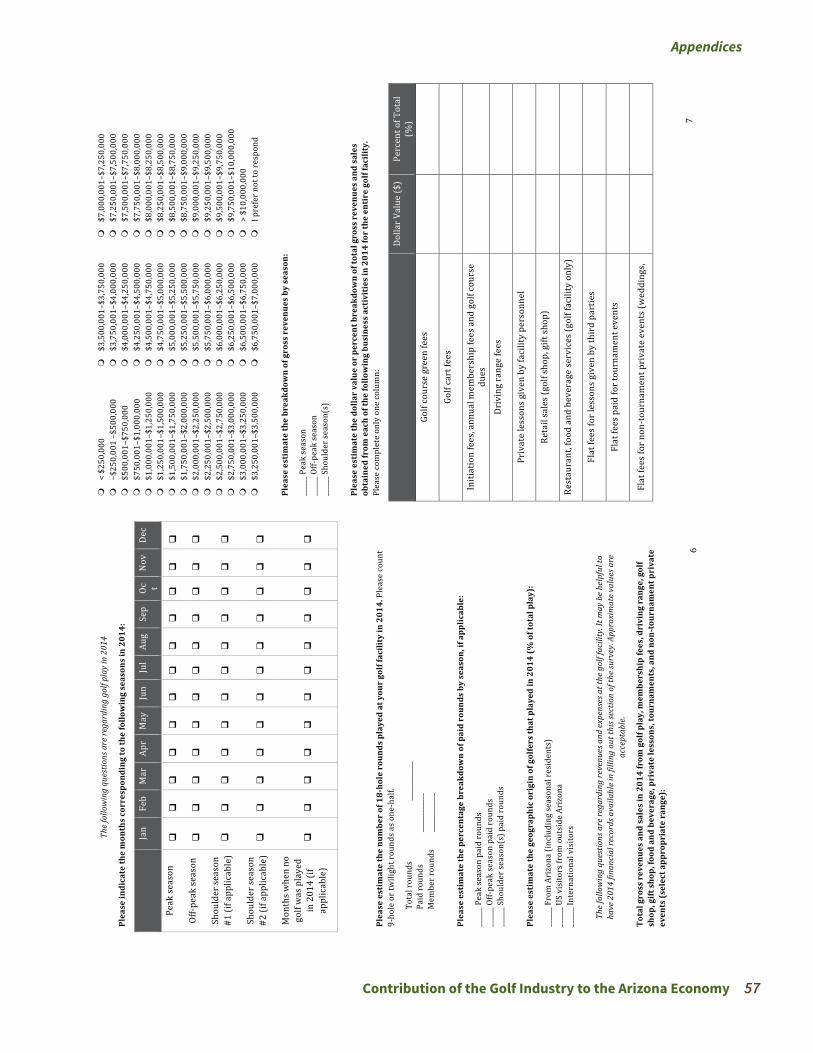

Turfgrass Reductions 46Efficiency Upgrade Investment Decision Making Process 46Environmental Management and Conservation Partnerships 47

Summary and Conclusions 48References 50Glossary and Acronyms 53 Appendices 54

Appendix A: Survey Instrument 54Appendix B: Survey Invitation Letter 62Appendix C: Scaling and Expansion Method 63Appendix D: Economic Contribution Analysis Methods 64Appendix E: IMPLAN Industry Assignments for Spending Patterns 65

FiguresFigure 1. Arizona Gross State Product and US Gross Domestic Product 2004–2014, in Millions, Adjusted to

2014 Dollars 11Figure 2. Total Revenues for Golf Courses and Country Clubs, United States, 2004–2014 11Figure 3. Gross State Product of Arizona Amusements, Gambling and Recreation Industries, 2004–2014, Adjusted to

2014 Dollars 12Figure 4. Arizona Per Capita Disposable Personal Income 2004–2014, Adjusted to 2014 Dollars 12Figure 5. National Golf Course Closures (18-Hole Equivalents), 2001–2014 13Figure 6. Date of Course Opening, Survey Responses vs. Full Database 19Figure 7. Percentage of Respondents Identifying a Given Month as Peak Season, Off-Peak Season, Shoulder Season,

or No Golf Played 19Figure 8. Pro Shop Services Provided (Response Count) 21Figure 9. Golf Course Maintenance Expenditure Breakdown 22Figure 10. Golf Course Renovations by Type (Response Count), 2014 23Figure 11. Illustration of Relationship between Economic Metrics 27Figure 12. Top 10 Industries Impacted by Component of Economic Contribution Analysis 29Figure 13. Case Shiller Home Price Index for Phoenix, 2002–2014 33Figure 14. Golf Freshwater Withdrawals Compared to Withdrawals for All Other Uses, Arizona 2010 35Figure 15. Total Freshwater Withdrawals by County, Golf vs. All Other Withdrawals, Arizona 2010 36Figure 16. Groundater Withdrawals by County, Golf vs. All Other Withdrawals, Arizona 2010 36Figure 17. Total Surface Water Withdrawals by County, Golf vs. All Other Uses, Arizona 2010 37Figure 18. Golf Course Use of Reclaimed Wastewater by County, Arizona, 2010 38Figure 19. Golf Water Use (Including Effluent) as a Percentage of Total AMA Water Use by AMA, 2014 39Figure 20. Golf Water Use by AMA, 2004–2015 (in Acre-Feet) 39Figure 21. AMA Golf Water Use by Source, 2004–2015 (in Acre-Feet) 40Figure 22. Golf Groundwater Use by AMA, 2004–2015 (in Acre-Feet) 40Figure 23. Golf Surface Water Use by AMA, 2004–2015 (in Acre-Feet) 41Figure 24. Golf Spillwater Water Use by AMA, 2004–2015 (in Acre-Feet) 41Figure 25. Golf CAP Water Use by AMA, 2004–2015 (in Acre-Feet) 42Figure 26. Golf Effluent Use by AMA, 2004–2015 (in Acre-Feet) 42Figure 27. AMA Golf Water Use by Type, 2014 43Figure 28. Use of Turfgrass Management Strategies (Response Count), 2014 44Figure 29. Average Acreage Overseeded in 2009 and 2014 45

Contribution of the Golf Industry to the Arizona Economy v

Figure 30. Overseeding Practices (Response Count) 45Figure 31. Irrigation Audit Performed in Past 5 Years and Resulting Water Savings, 2014 45Figure 32. Turfgrass Acreage Removed Over Past 5 Years, 2014 46Figure 33. Materials Used to Replace Turfgrass (Response Count) 46Figure 34. Factors Considered in Making Efficiency Upgrade Investment Decisions (Response Count) 46Figure 35. Resources Consulted in Making Efficiency Upgrade Investment Decisions (Response Count) 47Figure 36. Facilities’ Partnerships with Conservation Organizations 47

TablesTable 1. Survey Response Rates by Role of Survey Respondent 17Table 2. Survey Responses by Number of Holes at Golf Facility and Role of Survey Respondent 17Table 3. Survey Responses by Type of Facility and Role of Survey Respondent 18Table 4. Survey Responses by Location of Facility and Role of Survey Respondent 18Table 5. Survey Responses by Area of State and Role of Survey Respondent 18Table 6. Percentage of Rounds Played in 2014 by Geographic Origin of Golfer 20Table 7. Estimate of Statewide Golf Facility Revenues by Category, 2014 20Table 8. Estimate of Statewide Golf Facility Expenses by Category, 2014 21Table 9. Estimate of Statewide Golf Facility Full- and Part-Time Employment, 2014 22Table 10. Estimate of Statewide Golf Facility Capital Investment and Amount Purchased In-State, 2014 23Table 11. Geographic Origin of Golfers in Arizona, by Percentage of Total Play, 2014 24Table 12. Golf Traveler Spending Pattern 25Table 13. Major Professional Golf Tournaments in Arizona, 2014 25Table 14. Estimate of Statewide Golf-Related Business Sales (Retailers and Service Providers), 2014 26Table 15. Economic Contribution Summary for Golf Facility Operations, 2014 28Table 16. Estimate of Statewide Golf Facility State and Local Taxes, 2014 28Table 17. Economic Contribution Summary for Golf Tourism, 2014 29Table 18. Economic Contribution Summary for Golf-Related Businesses, 2014 30Table 19. Economic Contribution Summary, Total, 2014 30Table 20. Selected Hedonic Study Estimates of Home Price Premiums for Proximity to Golf Courses 31Table 21. Estimated of Statewide Golf Facility Acreage, 2014 34Table 22. Freshwater Withdrawals for Golf Course Irrigation as a Percentage of Total County Withdrawals for All Uses,

2010 35Table 23. Number of Golf Facilities by AMA in 2014 38Table 24. Number of Facilities Using Water Source by AMA, 2014 38Table 25. Irrigation Method for Arizona Golf Facilities, 2014 (Survey Results) 43

Contribution of the Golf Industry to the Arizona Economyvi

AcknowledgmentsThis study was coordinated by Cactus & Pine GCSA, a member of the Golf Course Superintendent Association of America, with the cooperation of the Club Managers Association of America and Southwest Section PGA. Cactus & Pine GCSA would like to thank the following contributors for their support and generosity in funding the study:

Cactus & Pine, GCSA $6,000 Arizona Golf Association $5,000 CMAA $5,000 Desert Mountain Club, Inc. $5,000 Southwest Section PGA $5,000 The Thunderbirds $5,000 Troon Golf L.L.C. $5,000 Arizona Country Club $2,500 OB Sports Golf Management $2,500 The Antigua Group Inc. $2,500 The Country Club at DC Ranch $2,000 Arizona Women’s Golf Association $1,500 Blue Star Resort & Golf $1,000 Grayhawk Golf Club $1,000 The Golf Club @ Johnson Ranch $1,000 The Estancia Club $1,000 The Mirabel Club $1,000 Apache Sun Golf Club $500 Arizona NGCOA $500 Communication Links $500 Paradise Valley Country Club $500

Executive Summary

Contribution of the Golf Industry to the Arizona Economy 7

Executive SummaryWhat Is the Issue?Golf is an important part of Arizona’s economy and a defining component of the physical landscape of many of its cities and towns. Golf facilities support jobs and income for the state economy, indirectly support other Arizona busi-nesses that serve and supply the facilities, drive tourist spending by attracting visitors from outside the state, and support sales by retailers offering golf equipment and merchandise to Arizona golfers. Additionally, golf facilities exert a positive effect on the value of residential real estate in their proximity. Meanwhile, golf courses require inputs year-round to maintain playable and attractive conditions for golfers on the facility’s turfgrass and other landscape surfaces. Major inputs include irrigation water, fertilizer, and other agricul-tural chemicals. Conservation efforts at golf facilities aim to balance the use of natural resources with the economic viability of the courses.

This study provides an estimate of the economic contribution of the golf industry to Arizona’s economy in 2014, examining the following components:• Golf facility operations (operations spending, jobs, and other contribu-

tions)• Golf-related tourist spending• Golf-related business revenues

This report uses a variety of metrics to describe the golf industry’s con-tribution to the Arizona economy. These include sales (output), value added (GDP), labor income (employee compensation and proprietor income), jobs, and state and local taxes. It’s important to note that many of these economic metrics are interconnected and, therefore, cannot be added together. Fur-thermore, while sales (output) is an easily-interpreted measure of economic activity, value added (also known as gross state product) is the best reflection of an industry’s contribution to the state economy.

The contribution of the golf industry to Arizona’s economy goes beyond the direct effects of facility revenues, tourist spending, and golf-related business sales. The businesses providing those goods and services also require inputs of goods and services in order to operate, many of which are supplied by in-state suppliers. Those local businesses in turn require their own production inputs. These rounds of business-to-business transactions of providing inputs are known as indirect effects. Additionally, incomes (wages, salaries, and profits) generated for individuals employed directly by the golf industry are used to pur-chase household needs, such as rent or mortgages, doctor visits, and groceries. This spending produces rounds of household-to-business transactions, known as induced effects. Because of these indirect and induced multiplier effects, the economic contribution of the golf industry in Arizona is considerably greater than indicated by direct sales and tourist spending.

Other effects of the golf industry are not best measured using regional economic contribution analysis. These effects include the influence of golf courses on residential real estate values and natural resource use and con-servation. The study provides an update to a 2004 estimate of residential real estate premiums attributable to frontage on and proximity to golf courses, and provides a snapshot of golf water use and conservation and management practices at Arizona golf facilities in 2014.

What Did the Study Find?Arizona’s golf industry had a total estimated economic contribution of $3.9 billion in sales (output) to the state economy in 2014. This includes the direct,

Executive Summary

8 Contribution of the Golf Industry to the Arizona Economy

indirect, and induced effects of golf course operations ($2.5 billion), golf tour-ism ($1.1 billion), and golf-related businesses ($347 million).

Economic Contribution• Golf facility operations generated a direct contribution of $1.1 billion

in sales to the state economy in 2014, directly supporting an estimated 18,695 full- and part-time jobs. Including multiplier effects, the total contribution was $2.5 billion in sales, $1.4 billion in value added (gross state product), and approximately 29,500 full- and part-time jobs. An estimated $72 million in state and local taxes was directly supported, including $39 million in direct state and local sales tax revenues. An esti-mated 11.6 million rounds of golf were played in Arizona in 2014.

• Golf tourism, both golf travelers and golf spectators, attracted an esti-mated $598 million in spending from out-of-state visitors in 2014, for a total estimated impact of $1.1 billion in sales and approximately 10,500 jobs. Direct sales tax impacts were estimated at $32 million in 2014. Roughly a third of rounds played in Arizona in 2014 were by out-of-state and out-of-country visitors.

• Golf-related businesses, such as equipment and apparel retailers, practice ranges, and golf cart dealers, had estimated annual sales of $270 million, for a total estimated contribution of $347 million in sales, approximately 1,800 jobs, and directly-supported sales tax revenues of $6.5 million.

Residential Real Estate Premiums• Hedonic studies have shown that frontage on and proximity to golf

courses is associated with a sales price premium for residential real estate.

• Residential real estate premiums associated with all homes ever built in golf course communities in Arizona were estimated to be nearly $2.1 billion.

Water Use• Survey Results• Statewide use—According to survey results, Arizona golf facilities

used an estimated 167,397 acre-feet (AF) of irrigation water in 2014, occupying a total of 45,000 acres for the golf courses, of which 32,000 acres was turfgrass.

• Use of effluent—Statewide, according to survey results from this study, an estimated 35% of golf water use was effluent in 2014. This percent-age from the survey is somewhat higher than estimates from water resource agencies (see below).

• USGS Statewide Data (2010)• Statewide use—In 2010, 130,116 AF of self-supplied freshwater was

used to irrigate golf courses, accounting for 1.9% of Arizona’s total freshwater withdrawals. This figure includes groundwater and surface water, but excludes effluent.

• Use of effluent—Statewide, 49,488 AF of reclaimed wastewater was used for golf course irrigation in 2010, accounting for 28% of golf ’s total statewide water use.

• Share of statewide use by source—In 2010, golf irrigation accounted for 3% of state groundwater withdrawals and 1.1% of state surface wa-ter withdrawals, but 34% of state reclaimed water use for irrigation.

Executive Summary

Contribution of the Golf Industry to the Arizona Economy 9

• ADWR Active Management Area (AMA) Data• Share of statewide AMA use—According to Arizona Department of

Water Resources (ADWR) data, golf water use represented 3.5% of total AMA water use in Arizona in 2014.

• Breakdown of golf AMA use by source—In 2014, groundwater repre-sented 48.1% of AMA golf water use, surface water, 10.9%, CAP, 14.6%, and effluent, 26.3%. Whereas some AMAs rely on a varied mix of wa-ter sources, others rely heavily on one or two sources, such as effluent or groundwater.

• Use of effluent—Use of effluent by golf facilities in AMAs was 33,977 AF in 2014, an increase of 27% since 2004.

• 10-year trend—Between 2004 and 2014, ADWR reported a net increase of 24,736 AF of golf facility water use in Arizona’s AMAs, with all types of water use increasing. During that time, the number of facilities in Arizona’s AMAs also increased, from 239 facilities to 252 facilities.

Conservation Practices• 51% of respondents reported performing irrigation audits for their golf

course irrigation systems, and among respondents conducting irrigation audits, 95% made adjustments to their irrigation systems, for an average irrigation water savings of 19.5 AF of water per facility per year.

• 31% of respondents reported having removed turfgrass in the past 5 years. Another 39% reported having a partnership with conservation organizations, the most common of which was Audubon International.

How was the study conducted?This study relies on the results of a statewide survey of golf facilities per-formed between April and August of 2016. In order to capture all compo-nents of golf facility operations, the survey was directed at three key staff positions at each facility: General Manager/Director of Club Operations, Head Golf Professional/Director of Golf, and Golf Course Superintendent/Director of Agronomy. The survey response rate was 44% for General Man-agers, 26% for Golf Professionals, and 45% for Superintendents. With some unusable responses having been submitted, the useable response rate was 42% for General Managers, 25% for Golf Professionals, and 39% for Superin-tendents. Unbiased estimates were calculated from the survey response data using scaling and an expansion factor. Survey data were complemented with secondary data on golf business establishments, golf tourism, real estate, and golf water use from a variety of sources. The economic multiplier effects of the golf industry were estimated using IMPLAN 3.1, the premier input-out-put model used for regional economic impact analysis.

Introduction

10 Contribution of the Golf Industry to the Arizona Economy

IntroductionOverviewGolf is an important part of Arizona’s economy and a defining component of the physical landscape of many of its cities and towns. The golf industry supports jobs and incomes for the state economy, indirectly supports other Arizona businesses that serve and supply the facilities, drives tourist spending by attracting visitors from outside the state, and supports sales by retailers offering golf equipment and merchandise. Additionally, golf facilities exert a positive effect on the value of residential real estate in their proximity. Meanwhile, golf courses require inputs year-round to maintain playable and attractive conditions for golfers on the facility’s turfgrass and other landscape surfaces. Major inputs include irrigation water, fertilizer, and other agricul-tural chemicals. Conservation efforts at golf facilities aim to balance the use of natural resources with the economic viability of the courses.

This study provides an estimate of the economic contribution of golf to Arizona’s economy in 2014, examining the following components:

• Golf facility operations (spending, jobs, and other contributions)• Golf-related tourist spending• Golf-related businesses.

This estimate includes direct, indirect, and induced multiplier effects and is measured in terms of sales (output), value added (GDP), labor income (em-ployee compensation and proprietor income), jobs, and state and local taxes.

Furthermore, the study provides an updated estimate of residential real estate price premiums attributable to proximity to golf courses. Finally, this study provides a snapshot of golf water use and conservation and manage-ment practices at Arizona golf facilities in 2014.

MotivationThis study provides an update to a 2006 study of the economic contribution of golf to the Arizona economy in 2004, “Economic and Environmental Impact of Golf” (Schmitz, 2006). It relies on primary data collected from Arizona golf facilities state-wide through a survey, as well as secondary data from a variety of sources. A survey was necessary because government statistics do not capture golf facilities in one single industry. Businesses are typically captured in government statistics according to the industry that represents the majority of their sales. Therefore, golf facilities that are part of resort hotels are often categorized as hotels (NAICS1 721110). Golf facilities not associated with resorts are most typically classified as golf courses and country clubs (NAICS 713910). To rely only on statistics for golf courses and coun-try clubs would significantly underrepresent the extent of the industry in the state, considering that many golf courses in Arizona are attached to resort properties. In addition to filling the gaps in government data, the survey provides an opportunity to better understand golf facility revenues and expenses, employment, and conser-vation and management practices used on the golf courses.

Economic and Industry ContextSince 2004, the date of the most recent analysis, the state and national econ-omies have weathered great challenges as a result of the Great Recession.

1 North American Industry Classification System (NAICS) codes are 2 to 6 digit codes used for purposes of classifying business entities by their primary industry in government statistics (US Census Bureau, 2016).

Introduction

Contribution of the Golf Industry to the Arizona Economy 11

Arizona was hit especially hard by the downturn, and golf, an activity linked closely with both disposable personal income as well as real estate, suffered heavily as a result. The state and national economies both experienced signif-icant contractions between 2008 and 2009, as evidenced by gross domestic product and gross state product (Figure 1).

$0$2,000,000$4,000,000$6,000,000$8,000,000

$10,000,000$12,000,000$14,000,000$16,000,000$18,000,000$20,000,000

Natio

nal G

DP—

Mill

ions

201

4 US

D

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

National Arizona

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Ariz

ona

GDP—

Mill

ions

201

4 US

D

Figure 1. Arizona Gross State Product and US Gross Domestic Product 2004–2014, in Millions, Adjusted to 2014 Dollars

Source: Bureau of Economic Analysis, Bureau of Labor Statistics

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 201417,000

17,500

18,000

18,500

19,000

19,500

20,000

20,500

21,000

21,500

22,000

MIll

ions

of D

olla

rs

Total Revenue for Golf Courses and Country Clubs, All Establishments, Employer Firms* Brown bar denotes period of economic recession.

Figure 2. Total Revenues for Golf Courses and Country Clubs, United States, 2004–2014

Source: US Census Bureau

At the national level, golf courses and country clubs saw a significant de-cline in revenues between 2007 and 2010 (Figure 2).

Amusements, gambling, and recreation industries’ direct contribution to Arizona’s gross state product, which includes golf courses and country clubs,

Introduction

12 Contribution of the Golf Industry to the Arizona Economy

experienced a considerable slump starting in 2007, but has since resumed growth since 2011 (Figure 3).

The economic downturn’s effect on households in Arizona is evidenced by trends in per capita disposable income (Figure 4). After increasing to a sharp peak in 2007, Arizona per capita disposable personal income declined, bot-toming out in 2011, and has gradually increased since that time.

In recent years, the national supply of golf courses has been decreasing in what is considered a market correction after significant increases in golf course construction during the 1990s (Hueber & Worzala, 2010). Golf course closures in the U.S. began to increase in the early 2000s and have averaged

$800

$900

$1,000

$1,100

$1,200

$1,300

$1,400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Gros

s Sta

te P

rodu

ct (M

illio

n, 2

014

USD)

Figure 3. Gross State Product of Arizona Amusements, Gambling and Recreation Industries, 2004–2014, Adjusted to 2014 Dollars

Source: Bureau of Economic Analysis; Bureau of Labor Statistics

$31,500

$32,000

$32,500

$33,000

$33,500

$34,000

$34,500

$35,000

$35,500

$36,000

$36,500

$37,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Per C

apita

Dis

posa

ble

Pers

onal

Inco

me

(201

4 Do

llars

)

Figure 4. Arizona Per Capita Disposable Personal Income 2004–2014, Adjusted to 2014 Dollars

Source: Bureau of Economic Analysis, Bureau of Labor Statistics

Introduction

Contribution of the Golf Industry to the Arizona Economy 13

0

20

40

60

80

100

120

140

160

180

200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Golf

Cour

se C

losu

res (

18-H

ole

Equi

vale

nts)

Figure 5. National Golf Course Closures (18-Hole Equivalents), 2001–2014

Source: National Golf Foundation

140 closures per year between 2006 and 2014 (Figure 5). This, coupled with relatively low levels of new construction since that time, have led to a net re-duction in the number of 18-hole equivalent courses in the U.S. The National Golf Foundation projects golf course openings in the U.S. to average 20 or fewer annually in the near future (NGF, 2013).

In Arizona, a similar trend has emerged with 17 facilities closing during that same period. Yet, an estimated 19 new golf facilities have opened be-tween 2004 and 2014, resulting in a net increase of two facilities. This is not including facilities that have undergone significant renovations, closed and reopened, or transferred ownership since that time. Another important trend includes the privatization of public municipal courses. In recent years, such courses have struggled to remain financially solvent, prompting municipal-ities to sell to or partner with third-party management companies (Keegan, 2010). This trend has affected municipal courses in Arizona.

Methods and Data

14 Contribution of the Golf Industry to the Arizona Economy

Methods and DataArizona Golf Facility SurveyThis economic contribution analysis relies on the results of an online survey of golf facilities in Arizona. The survey collected information on the oper-ations of Arizona golf facilities in calendar year 2014 with focused sections directed to three key staff positions at each facility:

• General Manager / Director of Club Operations (referred to herein as General Manager);

• Head Golf Professional / Director of Golf (referred to herein as Golf Professional);

• Golf Course Superintendent / Director of Agronomy (referred to herein as Superintendent).

The section answered by the General Manager concentrated on overall golf facility operations with questions pertaining to facility finances, investment, and employment. The section answered by the Golf Professional focused on tournaments and pro shop finances and purchasing. The section answered by the Superintendent included information on golf course maintenance ex-penses and practices, and in particular focused on turfgrass management and water conservation strategies. Finally, all three staff roles completed an initial survey section regarding general facility characteristics, including number of holes, county location, facility type, and other similar general characteristics.The survey was distributed by two means: an online survey distributed via email using the Qualtrics platform (Appendix A), as well as a hard-copy invitation letter mailed to facilities and addressed to the General Manager (Appendix B). The online survey was distributed via email invitations to a database of golf facility contacts whose emails were available through golf industry associations, as well as from facility websites. The survey invitation letter was sent via US Mail to all golf facilities in the state and included a URL for survey participants to follow where they could enter a password to access the survey.

The full database of Arizona golf facilities was compiled through a com-bination of sources, primarily the Arizona Golf Association and Golflink. The lists of facilities were combined, removing duplicates, and the informa-tion was validated, removing facilities that were no longer in operation, and compiling contact information. The database includes 313 separate facility listings. This survey and study were conducted at the facility level, with facilities varying in size and many having more than one golf course at the establishment.

The online survey was first activated and distributed on April 20, 2016 and remained open until August 5, 2016. The hard copy letter was mailed on April 20, 2016. A follow-up letter was mailed on May 18, 2016. Email reminders were sent periodically during the open period to those facilities that email contacts were available for. Survey invitations were also sent by Cactus and Pine Golf Course Superintendent (GCSA), the Southwest Section Professional Golf Association (PGA), and the Club Managers Association of America (CMAA) to their respective memberships. A survey incentive was coordinated through Cactus and Pine GCSA to drive participation in the first weeks of the survey. Participants were eligible for an optional raffle drawing if they participated before May 31, 2016.

Settings in Qualtrics were configured to remove any connection between a respondent’s email and their survey response. The system provided an

Methods and Data

Contribution of the Golf Industry to the Arizona Economy 15

anonymized unique identifier for each response. Similarly, the optional raffle was a separate survey with no connection to golf facility survey responses and raffle responses to preserve the anonymity of responses. The survey was reviewed by the University of Arizona’s Human Subjects Protection Program and was determined not to constitute human research. Best practices were followed with regards to survey design, allowing respondents to opt out of any question, either by including questions where no response was required, or by including the option of “I prefer not to respond.” After the survey closed, anonymized results data were downloaded and analyzed according to methods described in subsequent sections.

Statistical Methodology and Expansion FactorThe golf survey was divided into four sections. The first section asked all respondents to provide general characteristics of their facility. The other three sections were directed towards each role at the facility. The survey presented a combination of qualitative and quantitative responses.

Questions that presented yes-no options or asked respondents to select among multiple options were analyzed using a simple count method. These are questions where the response is not a number and therefore should not vary depending upon the size of the facility.

For those questions where respondents were asked to provide a number (revenues, rounds of golf, etc.), a scaling and expansion method was used to obtain an unbiased estimate of statewide values based on the survey sample, assuming that numerical responses (revenues, costs, acreage, etc.) are propor-tional to the size of the facility in terms of number of holes. For a full descrip-tion of the scaling and expansion method, please consult Appendix C.

Golf-Related TourismData from the survey regarding the percent of annual rounds played by geo-graphic origin on the golfer were coupled with golf tourist expenditure and travel behavior data from two separate research reports to account for the contribution of golf tourists, as well as professional golf tournament specta-tors to the state economy.

Golf-Related BusinessesThe golf-related businesses section of this study relies on a variety of second-ary data sources, including ReferenceUSA, MelissaData, and Census Industry Snapshots. These data are used to produce an establishment count, as well as an estimate of annual revenues for those golf-related businesses whose eco-nomic activity is not captured through the survey response.

Economic Contribution AnalysisIntegrating results from previous sections, the indirect and induced multiplier effects of golf facility operations, golf-related tourism, and golf-related busi-nesses, were calculated using the IMPLAN 3.1 model and software in order to obtain a total economic contribution estimate. IMPLAN is an input-output model that captures the linkages between economic sectors through local buyer-supplier relationships, whereby purchases of goods and services from local providers across the supply chain create additional rounds of transac-tions in the economy, supporting additional sales, incomes, and jobs. Both business-to-business (indirect effects) as well as business-to-household (in-duced effects) transactions were captured using this model.

Methods and Data

16 Contribution of the Golf Industry to the Arizona Economy

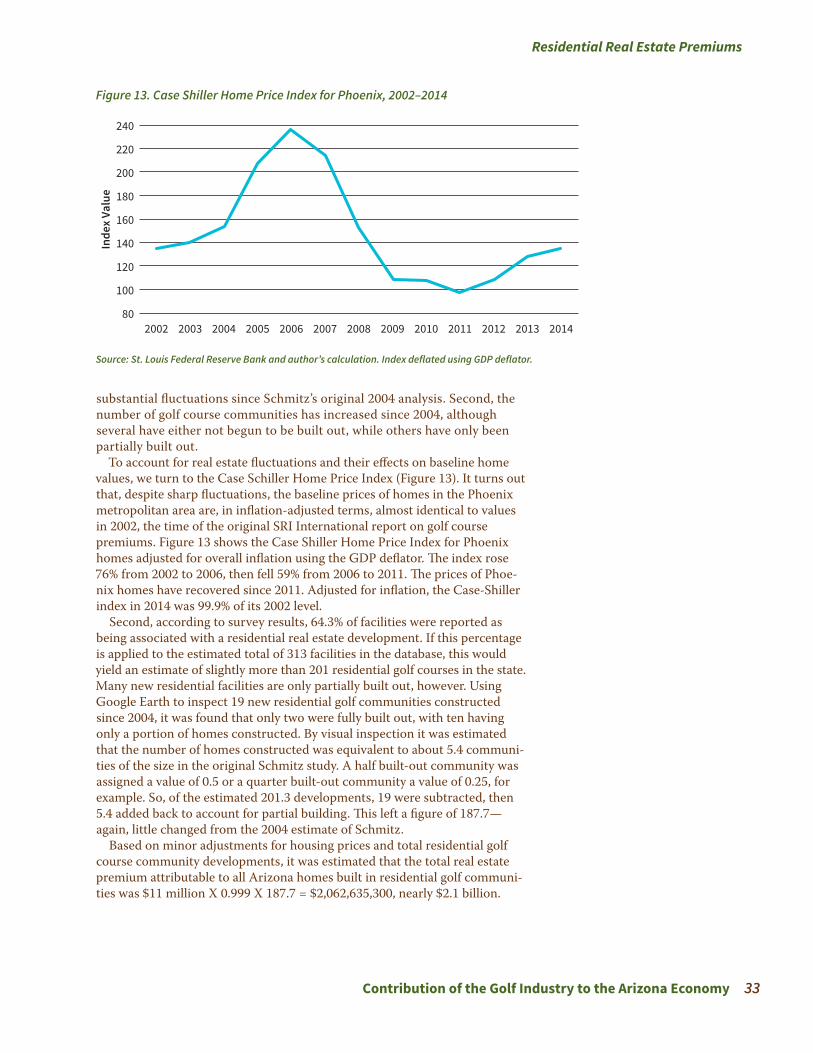

Residential Real Estate PremiumsFor the current study, Schmitz’s 2006 estimates of the total statewide resi-dential real estate premiums attributable to frontage on or proximity to golf courses were updated. Schmitz estimated per-community residential real es-tate premiums for golf course communities, applying the estimated per-com-munity premium to the total estimated number of golf course communities in the state. The estimate was updated by calculating a premium proportional to the underlying value of the home versus a fixed value per house, and ac-counting for underlying real estate value fluctuations between 2004 and 2014 using data from the Case Schiller Home Price Index for Phoenix. Finally, the estimate was adjusted to account for changes in the number of golf course communities in the state since the previous study.

Golf Environmental AnalysisThis final section of this study focuses on golf facility irrigation water use and conservation practices, relying on both primary and secondary data. Survey results were used to derive statewide estimates of water use, turfgrass man-agement practices, and conservation activities. That information was sup-plemented with US Geological Survey (USGS) and Arizona Department of Water Resources (ADWR) data for a higher level picture of golf water use in Arizona.

Arizona Golf Facilities

Contribution of the Golf Industry to the Arizona Economy 17

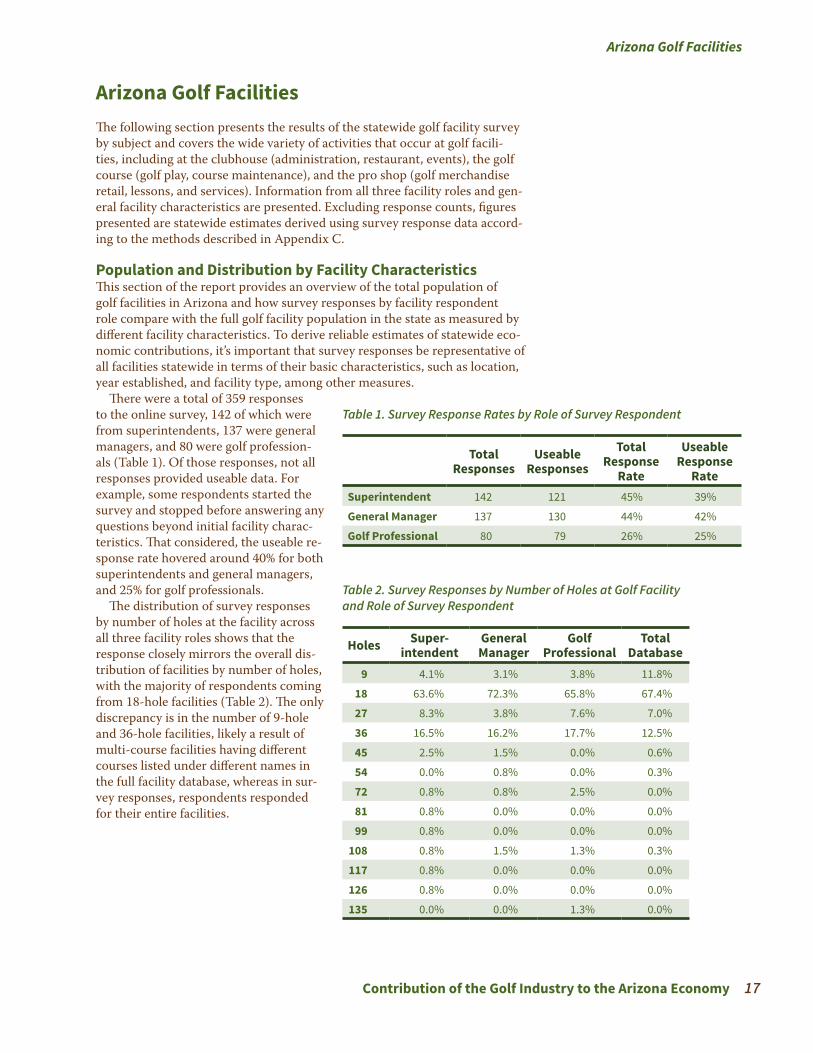

Arizona Golf FacilitiesThe following section presents the results of the statewide golf facility survey by subject and covers the wide variety of activities that occur at golf facili-ties, including at the clubhouse (administration, restaurant, events), the golf course (golf play, course maintenance), and the pro shop (golf merchandise retail, lessons, and services). Information from all three facility roles and gen-eral facility characteristics are presented. Excluding response counts, figures presented are statewide estimates derived using survey response data accord-ing to the methods described in Appendix C.

Table 1. Survey Response Rates by Role of Survey Respondent

Total Responses

Useable Responses

Total Response

Rate

Useable Response

RateSuperintendent 142 121 45% 39%

General Manager 137 130 44% 42%

Golf Professional 80 79 26% 25%

Table 2. Survey Responses by Number of Holes at Golf Facility and Role of Survey Respondent

Holes Super- intendent

General Manager

Golf Professional

Total Database

9 4.1% 3.1% 3.8% 11.8%

18 63.6% 72.3% 65.8% 67.4%

27 8.3% 3.8% 7.6% 7.0%

36 16.5% 16.2% 17.7% 12.5%

45 2.5% 1.5% 0.0% 0.6%

54 0.0% 0.8% 0.0% 0.3%

72 0.8% 0.8% 2.5% 0.0%

81 0.8% 0.0% 0.0% 0.0%

99 0.8% 0.0% 0.0% 0.0%

108 0.8% 1.5% 1.3% 0.3%

117 0.8% 0.0% 0.0% 0.0%

126 0.8% 0.0% 0.0% 0.0%

135 0.0% 0.0% 1.3% 0.0%

Population and Distribution by Facility CharacteristicsThis section of the report provides an overview of the total population of golf facilities in Arizona and how survey responses by facility respondent role compare with the full golf facility population in the state as measured by different facility characteristics. To derive reliable estimates of statewide eco-nomic contributions, it’s important that survey responses be representative of all facilities statewide in terms of their basic characteristics, such as location, year established, and facility type, among other measures.

There were a total of 359 responses to the online survey, 142 of which were from superintendents, 137 were general managers, and 80 were golf profession-als (Table 1). Of those responses, not all responses provided useable data. For example, some respondents started the survey and stopped before answering any questions beyond initial facility charac-teristics. That considered, the useable re-sponse rate hovered around 40% for both superintendents and general managers, and 25% for golf professionals.

The distribution of survey responses by number of holes at the facility across all three facility roles shows that the response closely mirrors the overall dis-tribution of facilities by number of holes, with the majority of respondents coming from 18-hole facilities (Table 2). The only discrepancy is in the number of 9-hole and 36-hole facilities, likely a result of multi-course facilities having different courses listed under different names in the full facility database, whereas in sur-vey responses, respondents responded for their entire facilities.

Arizona Golf Facilities

18 Contribution of the Golf Industry to the Arizona Economy

Similarly, response by role according to the type of golf facility reflects the general golf facility population with the highest proportion of facilities being public, followed by private, and then semi-private (Table 3).

Most facilities were located in either residen-tial real estate developments or in resorts (Table 4). Columns may not sum to 100% as facilities can be located in more than one type of location, or in none. A comparison with the full course population is not provided because the location definitions in the database differ from those op-tions provided in the survey.

Survey response by geographic location of the

Location Super- intendent

General Manager

Golf Professional

A residential real estate development (including retirement communities or any housing development)

68.6% 66.2% 58.2%

A resort 13.2% 6.2% 12.7%

A park or recreation area (municipal, county, etc.) 5.0% 6.2% 5.1%

A military installation 1.7% 1.5% 1.3%

Tribal land 5.0% 1.5% 6.3%

Other 9.1% 10.0% 12.7%

Table 4. Survey Responses by Location of Facility and Role of Survey Respondent

Table 3. Survey Responses by Type of Facility and Role of Survey Respondent

Type Superintendent General Manager Golf Professional Total DatabasePublic 48.8% 47.7% 50.6% 61.3%

Semi-private 24.0% 17.7% 17.7% 15.3%

Private 27.3% 33.1% 30.4% 23.3%

Other 0.0% 1.5% 1.3% 0.0%

Area Super- intendent

General Manager

Golf Professional

Total Database

Phoenix and Central

69% 67% 66% 63%

Tucson and Southern

12% 16% 19% 17%

Northern 13% 12% 13% 12%

Western 5% 5% 3% 8%

Table 5. Survey Responses by Area of State and Role of Survey Respondent

facility also closely resembles the full facility population in the state (Table 5). Roughly two-thirds of golf facilities are located in the metro Phoenix area, a little less than a fifth are located in Tucson and Southern Arizona, and the remaining fifth are located in Northern and Western Arizona.

In regard to the year that the golf facility was first established, survey re-sponses closely resemble the pattern observed in the full database of facilities in the state. As can be seen in Figure 6, most facilities were first established between the mid-1980s and the mid-2000s. Since 2004, it is estimated that 17 golf facilities have closed and 19 new golf facilities have opened in Arizona, resulting in a net increase of 2 facilities.

Arizona Golf Facilities

Contribution of the Golf Industry to the Arizona Economy 19

Golf PlayAn estimated 11,573,579 rounds of golf were played in Arizona in 2014.2 Of total rounds, 7,678,120 were rounds played by members of private or semi-private facilities. 60.8% of total rounds were played during peak season, 19.6% during off-peak season, and 19.6% during shoulder seasons.Respondents were asked to indicate the months corresponding to peak sea-son, off-peak season, shoulder seasons, and times when no golf was played at their facilities. A clear trend emerges, showing peak season beginning around November and peaking in March (Figure 7). Off-season begins in June and ends by October. Shoulder seasons were clustered around May and Octo-ber. Months when no golf was played were spaced fairly consistently across

01020304050607080

0

10

20

30

40

50

60

70

1900–1909

1950–1959

1960–1969

1970–1979

2000–2009

2010–2014

Cour

ses b

y Ye

ar O

pene

d

Resp

onse

s by

Year

Ope

ned

Database Golf Course Superintendent General Manager Head Golf Professional

1910–1919

1920–1929

1930–1939

1940–1949

1980–1989

1990–1999

Figure 6. Date of Course Opening, Survey Responses vs. Full Database

Figure 7. Percentage of Respondents Identifying a Given Month as Peak Season, Off-Peak Season, Shoulder Season, or No Golf Played

0%10%20%30%40%50%60%70%80%90%

100%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Perc

enta

ge o

f Res

pons

es

Peak O�-Peak Shoulder No Golf

2 This estimate was corroborated using independent estimates of number of rounds played and matches closely with national estimates of average rounds per 18-hole equivalent course (Reit-man, 2014) and numbers published by the Arizona Office of Tourism (2013).

Arizona Golf Facilities

20 Contribution of the Golf Industry to the Arizona Economy

the year. Statewide seasonal trends are reflective of the concentration of courses in Phoenix and Central Arizona where winter months are peak season and summer months are off-peak season. For example, 79% of respondents consider August as off-peak season, 9% consider it peak season, 7% consider it as shoulder season, and 4% report no golf being played during the month of August.

Survey respondents were also asked to provide a breakdown of the geographic origin of golfers in terms

Source: Authors’ estimates from survey

Table 6. Percentage of Rounds Played in 2014 by Geographic Origin of Golfer

From Arizona (including seasonal

residents)US Visitors from Outside Arizona

International Visitors

67.7% 24.3% 8.0%

Table 7. Estimate of Statewide Golf Facility Revenues by Category, 2014

Source: Authors’ estimates from survey

Revenue Category Statewide EstimateInitiation fees, annual membership fees and golf course dues $386,325,091

Golf course green fees $337,693,953

Restaurant, food and beverage services (golf facility only) $201,517,614

Retail sales (golf shop, gift shop) $86,805,260

Golf cart fees $38,872,021

Flat fees paid for tournament events $17,529,592

Driving range fees $17,254,931

Flat fees for non-tournament private events (weddings, etc.) $10,768,954

Private lessons given by facility personnel $8,062,260

Flat fees for lessons given by third parties $753,849

Other $41,783,270

TOTAL $1,147,366,795

of the percent of total play. Results indicate that roughly two-thirds of rounds are played by Arizona golfers, including seasonal residents. Roughly a quarter are played by visitors from other states, and the remainder (8%) are played by international visitors (Table 6).

Facility RevenuesRespondents were asked to provide a breakdown of facility revenue by cate-gory. This was done in one of two methods—either providing exact values by category or by providing a range of total revenues and a percentage break-down by category. In the case that a range and percentages were provided, those percentages were applied to the range midpoint to yield estimated category values and were folded into the overall weighted average estimate. Total Arizona golf facility revenues were estimated to be $1.1 billion in 2014 (Table 7).

While most golf facility revenue is generated by golf play, a significant amount of golf revenue is generated through golf pro shops. Golf pro shops are located at golf facilities, are staffed by golf professionals, and provide a variety of services and goods to golfers, including lessons, sales of hard and soft goods, and cart and equipment rental. About 88% of responding golf pro-fessionals indicated they are directly employed by the golf facility, 5% own and operate the pro shop on behalf of the facility, and another 5% work for a third-party management company. Of pro shop services provided, the most com-mon responses (with 76 in all) were equipment and apparel sales and equip-

Arizona Golf Facilities

Contribution of the Golf Industry to the Arizona Economy 21

Figure 8. Pro Shop Services Provided (Response Count)

0 10 20 30 40 50 60 70 80

Equipment andApparel Sales

Equipment Rental

Equipment Repair

Lessons

Locker Rental

Pro

Shop

Ser

vice

s

ment rental. Based on survey responses, 17% of golf pro shop merchandise was purchased from in-state manufacturers of golf equipment and goods, such as Ping and AM&E. The second most common response was providing lessons (74 respondents). In fact, in 2014, golf professionals provided an estimated 150,545 half-hour lessons statewide, generating an estimated $8 million in revenue for Arizona golf facilities. Less common responses were equip-ment repair (57 respondents) and locker rental (32 respon-dents) (Figure 8).

Table 8. Estimate of Statewide Golf Facility Expenses by Category, 2014

Source: Authors’ estimates from survey

Expense Category Statewide EstimateClubhouse payroll (employees whose work is based in the clubhouse or golf shop, including fringe benefits)

$200,165,974

Golf course maintenance payroll $155,658,825

Utilities (water, electric, gas, etc.) $95,841,042

Golf course maintenance supplies and services $94,628,735

General administrative expenses (excluding utilities, payroll, and advertising)

$82,826,999

Cost of food and beverage $76,510,958

Golf shop merchandise $48,981,076

Lease expenses (both operating and capital) $27,063,231

Payments on debt $16,207,130

Advertising / Marketing / Promotion $13,704,628

Facility insurance $12,786,030

Cash contributions to charities $1,196,438

Other expenses $54,198,163

TOTAL $879,769,229

Facility ExpensesSimilar to revenues, respondents were asked to provide estimates of facility expenses by category, either providing exact values by category or by pro-viding a total expense range and percentage breakdown by category (Table 8). Once again, in the case of a range and percentages, the percentages were applied to the midpoint of the expense range provided. Total Arizona golf facility expenses were estimated to be $880 million in 2014 (Table 8). This implies that net of operating expenses, golf facilities retained an estimated $268 million in profits in 2014.

Arizona Golf Facilities

22 Contribution of the Golf Industry to the Arizona Economy

Employment Full-Time Part-Time Total % of TotalCourse Maintenance

5,016 555 5,571 29.8%

Golf Shop 1,783 2,810 4,593 24.6%

Food and Beverage

2,324 3,115 5,439 29.1%

Administra-tive

835 207 1,042 5.6%

Other 1,076 973 2,050 11.0%

TOTAL 11,035 7,660 18,695

Table 9. Estimate of Statewide Golf Facility Full- and Part-Time Employment, 2014

Source: Authors’ estimates from survey

As would be expected, payroll is the primary expense for golf facilities. Approximately 40% of total golf facility expenses are dedicated to clubhouse and golf course mainte-nance payroll (Table 8). Other major expenses are related to maintaining the courses.

Golf course maintenance staff works year round to maintain playable and attractive conditions on golf courses in Arizona. This requires a variety of in-puts. Survey responses by superintendents suggest that spending on golf course maintenance is dominated by spending on payroll, which represented roughly half of all maintenance expenditures. The second highest expense category is irrigation water at roughly 13%, followed by chemicals (fertilizers, herbicides, and pesticides) at 5.3% of expenditures (Figure 9).

Figure 9. Golf Course Maintenance Expenditure Breakdown

Chemicals5.3%

Irrigationwater12.7%

Lease expenses(Both operating

and capital)3.8%

Purchase ofcapital equipment(tractors, mowers,

aerifiers, etc.)2.4%

Utilities:electric4.6%

Fuel: dieseland gasoline

3.3%

Other maintenancesupplies and expenses

11.7%

Plant material0.4%

Seed4.1%

Sand and soil1.4%

Maintenance payroll(including all fringe benefits

paid by the facility)50.3%

Facility EmploymentAn estimated 18,700 full-time and part-time jobs were directly linked to golf facilities in 2014 (Table 9). Total jobs were fairly evenly split between course maintenance, pro shop, and food and beverage service. Administrative and other jobs accounted for the smallest portion of total direct jobs.

Arizona Golf Facilities

Contribution of the Golf Industry to the Arizona Economy 23

Table 10. Estimate of Statewide Golf Facility Capital Investment and Amount Purchased In-State, 2014

Source: Authors’ estimates from survey

Total Purchased in AZFurniture $17,812,758 $10,465,807

Equipment $30,856,655 $18,273,506

Buildings $36,511,494 $32,014,841

Other $2,227,001 $2,102,121

Golf Course $86,823,095 $37,791,883

TOTAL $174,231,003 $100,648,158

Capital Investment and RenovationsGolf facility capital investment occurs on an annual basis in order to maintain buildings, equipment, furnishings, and golf courses. Survey respondents were asked to provide a breakdown of capital investments by category as well as the portion of the investment that was spent in-state. Based upon those responses, Arizona golf facilities spent an estimated $174 million on capital investment in 2014, of which $101 million was spent in Arizona (Table 10).

This investment in assets such as buildings, furnishings, and equipment adds to the overall value of assets owned by golf facili-ties, expanding the state and local tax base. As of December 2014, the assessed value of total owned assets of Arizona golf facilities was an estimated $3.7 billion.

In addition to annual capital investments in 2014, a review of publically available documents and news articles suggests that there were several Arizona golf facilities that underwent significant reno-vations in 2014. Facilities were reported as completing bunker renovations, adding tee boxes, relocating and resurfacing greens, replacing cart paths, re-landscaping desert areas, and even installing new irrigation systems. Survey respondents also reported course renovations, particularly bunker

Figure 10. Golf Course Renovations by Type (Response Count), 2014

02468

10121416

New Greens

Bunker Renovatio

n

Cart Paths

Revegetation

Re-sodding or R

esurfa

cing

Irrigatio

n System Renovatio

n

Irrigatio

n Computer Syste

m

New Tees

Drainage

Practice Facilty

Expansion

Num

ber o

f Res

pons

es

and cart path renovations (Figure 10).

In total, it is estimated that more than $20 million was spent on golf facility renovations in 2014. How-ever, because capital invest-ments and renovations can be funded through facility revenues, these values are not included in the total economic contribution analysis so as to avoid double-counting.

Charitable ContributionsAnother major contribution of golf facilities is their generation of revenue for charitable causes. This occurs through a variety of channels. Many local golf tournaments serve as fundraisers for charitable organizations. Accord-ing to survey results, roughly 32% of tournaments in 2014 in Arizona were hosted by a group whose purpose was to raise money for a charitable cause. Golf facilities also provide in-kind contribution of rounds of golf, lessons, and other goods and services for fundraising purposes. Finally, golf facilities make cash contributions to support charitable organizations. Statewide, an estimated $3.9 million in in-kind contributions were donated to charitable causes in 2014. Cash contributions totaled an estimated $1.2 million. Those cash contributions represent income for charitable organizations, supporting staff and programs.

Golf Tourism

24 Contribution of the Golf Industry to the Arizona Economy

Golf TourismThis section presents an estimate of the money that is brought into the state from golf tourism. Two types of golf tourism are examined: travelers who visit Arizona for the primary purpose of playing golf, either recreationally, or in amateur tournaments, and travelers who visit Arizona to spectate at major professional tournaments. The calculations incorporate survey data on num-ber of rounds played by visitor origin, information on golf traveler expendi-tures and visitation habits from a July 2016 study focusing on the Tucson and Phoenix/Scottsdale markets (Sports & Leisure Research Group, 2016), data from a 2012 study on the economic impact of the 2012 Waste Management Phoenix Open (Mokwa, et al, 2012), and reported attendance at major profes-sional tournaments from local news media.

Golf Travelers

Out-of-State and Foreign GolfersAs presented in the previous section on golf play, roughly two-thirds of golf play in Arizona was by Arizona residents (Table 11). The remaining third was by out-of-state and foreign visitors. Based upon the estimated 11.6 million rounds played in 2014, 3.7 million rounds were played by out-of-state and for-eign golfers. Those visitors create an impact on the state economy by bringing money from out of state and spending it on golf, lodging, restaurants, enter-tainment, and other local expenditures (Sports & Leisure Research Group, 2016).

Reason for VisitWhile many travelers play golf while on vacation or business, not all of those trips can be attributed to golf. For example, travelers may take a trip to a destination in order to visit friends or family or see specific attractions, and during the trip go golfing. In order to estimate tourist spending attributable to golf, it’s necessary to have information on the proportion of golf travel for which the primary motivation for the trip was to play golf versus other activities. Recall that 3.7 million rounds of golf were played by out-of-state and foreign golfers. According to the 2016 Sports & Leisure Research Group study, the median number of annual golf trips taken per golf traveler is 6 trips per year, 3 for which golf was the primary motivation (either a golf vacation or travel to participate in an amateur golf tournament). Therefore, for the pur-poses of this study, 50% of travel rounds (1.9 million rounds) will be consid-ered as attributable to golf. The same study reported an average of 6.1 rounds of golf played per trip. Dividing the estimated travel rounds attributable to golf by the average number of rounds per trip yields an estimate of 306,415 unique visits attributable to golf in 2014.

Expenditure PatternWhile some of the expenditures of out-of-state and foreign golfers are captured in the golf facility survey, such as rounds of golf played, revenues from greens fees and cart rentals, and total revenues from food and beverage purchases at the golf facility, other expenditures that happen outside the golf facility are not captured by the survey. These expenditures constitute an eco-nomic impact attributable to golf and therefore need to be estimated based upon golf traveler expenditure patterns. In the case of food and beverages purchased during travel, it can be assumed that some of these purchases occurred at the golf facility, while others occurred elsewhere. The estimated

Table 11. Geographic Origin of Golfers in Arizona, by Percentage of Total Play, 2014

Origin Percentage of Total Play

From Arizona (including sea-sonal residents)

67.7%

US visitors from outside Arizona

24.3%

International visitors

8.0%

Golf Tourism

Contribution of the Golf Industry to the Arizona Economy 25

spending on food and beverage is split half-and-half between the golf facility and outside the golf facility to exclude traveler spending at the golf facility that would be captured in survey data. Expenditures on airfare and fuel costs driving to the destination were assumed to have occurred out-of-state and therefore were excluded.

For this report, we use a golf traveler expenditure pattern from the 2016 Sports & Leisure Research Group report (Table 12).

Using the above spending pattern and the calculated number of trips attributable to golf tourists coming to play in Arizona, the estimated direct economic impact of golf travel to the Arizona economy in 2014 was $539,465,000.3

3 Were all golf trips attributable to golf as the primary reason for the travel, the estimated direct contribution would be $1,078,931,000.

Table 12. Golf Traveler Spending Pattern

Source: 2016 Sports & Leisure Research Group “Visit Tucson” Report, Adjusted to 2014 Dollars

Item Amount per Trip Include or ExcludeAirfare $439 Exclude

Car Rental $209 Include

Fuel Cost $153 Exclude

Golf $448 Exclude

Lodging/accommodations $609 Include

Local Transportation $129 Include

Food/Dining/Beverage $407 Include half

Entertainment/attractions $255 Include

Shopping & other retails sales

$356 Include

Total $3,004 $1,761

Professional Tournament SpectatorsTourists come to Arizona from outside the state not only to play golf, they also come to watch golf. Professional tournaments are a major attraction for out-of-state visitors. Furthermore, large professional tournaments require support staff and vendors who travel from out of state to support professional golf-ers, provide media coverage, and sell goods and ser-vices. Four of the largest professional tournaments in Arizona were included in this analysis (Table 13), estimating the number of unique out-of-town visi-tors based upon reported attendance in 2014.

A 2012 economic impact study of the Waste Management Phoenix Open estimated that there

Table 13. Major Professional Golf Tournaments in Arizona, 2014

* Attendance not known, estimated at 40,000.Sources: Arizona Republic (2016); Davis (2014a); Davis (2014b)

Tournament 2014 Attendance HostWaste Management Phoenix Open

563,008 TPC Scottsdale

Charles Schwab Cup Championship

40,000 Desert Mountain

Accenture Match Play 40,000* Dove Mountain

LPGA JTBC Founders Cup 56,250 Desert Ridge

were 67,320 unique visitors to the metropolitan Phoenix region attending the event. With a conservative assumption that half of those visitors were from out-of-state, this equates to unique out-of-state visitors representing 6.5% of reported attendance. That rate was applied to the attendance estimates for the other three tournaments (Table 13). In addition, the 2012 report provides an estimate of the number of support professionals attending the tourna-ment, estimated at 234 individuals. That same number was used for the other three tournaments as well. All tournaments were either 4 or 5 days in length, therefore the average stay of 4.4 days used in the 2012 study was used for all 4 tournaments. Applying the spending pattern provided in the 2012 study, adjusted to 2014 dollars and excluding spending on airfare, an estimated $58 million in out-of-state visitor direct spending can be attributed to major professional golf tournaments.

Estimated Direct Impact of Golf Tourism in ArizonaCombining golf travelers and professional golf tournament spectators, the total direct impact of golf tourism to Arizona’s economy in 2014 was an estimated $598,300,000.

Golf-Related Businesses

26 Contribution of the Golf Industry to the Arizona Economy

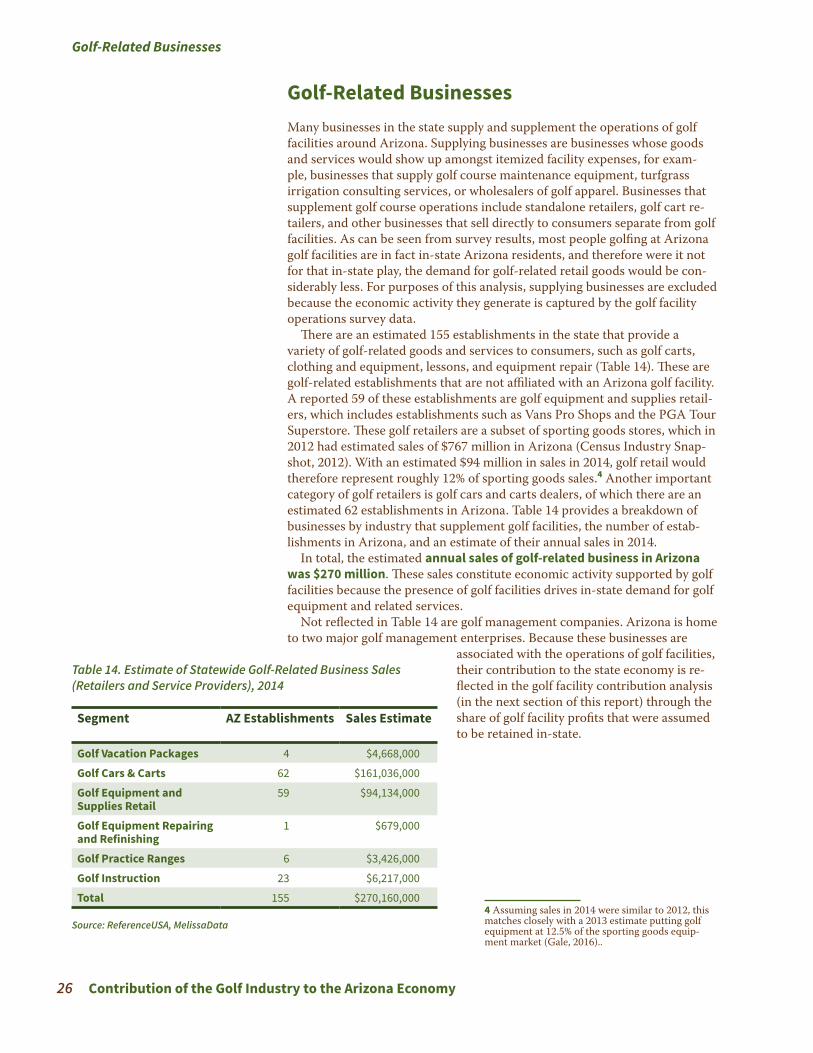

Golf-Related BusinessesMany businesses in the state supply and supplement the operations of golf facilities around Arizona. Supplying businesses are businesses whose goods and services would show up amongst itemized facility expenses, for exam-ple, businesses that supply golf course maintenance equipment, turfgrass irrigation consulting services, or wholesalers of golf apparel. Businesses that supplement golf course operations include standalone retailers, golf cart re-tailers, and other businesses that sell directly to consumers separate from golf facilities. As can be seen from survey results, most people golfing at Arizona golf facilities are in fact in-state Arizona residents, and therefore were it not for that in-state play, the demand for golf-related retail goods would be con-siderably less. For purposes of this analysis, supplying businesses are excluded because the economic activity they generate is captured by the golf facility operations survey data.

There are an estimated 155 establishments in the state that provide a variety of golf-related goods and services to consumers, such as golf carts, clothing and equipment, lessons, and equipment repair (Table 14). These are golf-related establishments that are not affiliated with an Arizona golf facility. A reported 59 of these establishments are golf equipment and supplies retail-ers, which includes establishments such as Vans Pro Shops and the PGA Tour Superstore. These golf retailers are a subset of sporting goods stores, which in 2012 had estimated sales of $767 million in Arizona (Census Industry Snap-shot, 2012). With an estimated $94 million in sales in 2014, golf retail would therefore represent roughly 12% of sporting goods sales.4 Another important category of golf retailers is golf cars and carts dealers, of which there are an estimated 62 establishments in Arizona. Table 14 provides a breakdown of businesses by industry that supplement golf facilities, the number of estab-lishments in Arizona, and an estimate of their annual sales in 2014.

In total, the estimated annual sales of golf-related business in Arizona was $270 million. These sales constitute economic activity supported by golf facilities because the presence of golf facilities drives in-state demand for golf equipment and related services.

Not reflected in Table 14 are golf management companies. Arizona is home to two major golf management enterprises. Because these businesses are

Table 14. Estimate of Statewide Golf-Related Business Sales (Retailers and Service Providers), 2014

Source: ReferenceUSA, MelissaData

Segment AZ Establishments Sales Estimate

Golf Vacation Packages 4 $4,668,000

Golf Cars & Carts 62 $161,036,000

Golf Equipment and Supplies Retail

59 $94,134,000

Golf Equipment Repairing and Refinishing

1 $679,000

Golf Practice Ranges 6 $3,426,000

Golf Instruction 23 $6,217,000

Total 155 $270,160,000

associated with the operations of golf facilities, their contribution to the state economy is re-flected in the golf facility contribution analysis (in the next section of this report) through the share of golf facility profits that were assumed to be retained in-state.

4 Assuming sales in 2014 were similar to 2012, this matches closely with a 2013 estimate putting golf equipment at 12.5% of the sporting goods equip-ment market (Gale, 2016)..

Economic Contribution Analysis

Contribution of the Golf Industry to the Arizona Economy 27

Economic Contribution AnalysisThe following section presents economic contribution analyses for the three major components examined in this analysis—golf facility operations, golf tourism, and golf-related businesses. These contribution analyses utilize input-output modeling techniques and the IMPLAN 3.1 software, a regional economic model used to estimate the linkages between local industries.

The contribution of the golf industry to Arizona’s economy goes beyond the revenues of golf facilities, golf tourist spending, and the sales of golf-re-lated businesses, known as direct effects. Providing those goods and services requires inputs of other goods and services, including machinery, fertilizers, water, wholesale goods, and labor. Many of those goods and services are sup-plied by local businesses that themselves require inputs to operate and pro-duce, and so on. Each additional round of transactions eventually dissipates as money leaks out of the state economy. These rounds of business-to-business transactions providing inputs to production are known as indirect effects. Another critical component of economic activity supported by the golf industry is the set of effects resulting from salaries and wages paid to people employed by the golf industry and its supplying industries. When these em-ployees spend their paychecks on household expenses such as rent or mort-gages, visits to the doctor, or groceries, more rounds of household-to-busi-ness transactions take place, known as induced effects. The total economic contribution of an industry is the sum of these three types of effects. For a detailed explanation of the methods used to calculate the economic contribu-tion analysis, please see Appendices D and E.

A variety of economic metrics are used to describe the golf industry’s con-tribution to the Arizona economy. These include sales (output), value added (GDP), labor income (employee compensation and proprietor income), jobs, and state and local taxes. It’s important to note that many of these economic metrics are interconnected and, therefore, cannot be added together. Figure 11 demonstrates the relationship between sales, value added, and income.

Sales, or output, measures the total final value of goods and services pro-duced by an industry. Sales is a gross measure of economic activity as it includes the value of economic activity generated in the industry (value added) as well as the costs of inputs. While sales is the easiest metric to understand,

LaborIncome

SalesValueAdded

Wages, Salaries, and Benefits of Employees

ProprietorIncome

Other Property Type Income

Profits

TaxesInput Costs

Value AddedLabor Income

Figure 11. Illustration of Relationship between Economic Metrics

Economic Contribution Analysis

28 Contribution of the Golf Industry to the Arizona Economy

the most precise metric to measure an industry’s contribution to the Arizona economy is value added. Value added is the net incremental change in value from the last stage of production. It measures the additional gain in economic activity that can be attributed a particular industry. This metric is synonymous to the official measure of gross domestic product (GDP), the measure that is most often used to measure the size of an economy. Value added is comprised of the incomes paid to workers, the profits of the industry, and the taxes paid to the government (IMPLAN Group, LLC). Finally, labor income measures the total personal income supported by the industry. It includes the wages, salaries, and benefits of employees as well as the income of proprietors.

The following section of the report summarizes the results of the eco-nomic contribution analyses for golf facility operations, golf-tourism, and other golf-related businesses. Additionally, Figure 12 demonstrates the other industries in Arizona that are most affected through the multiplier effects generated by the golf industry.

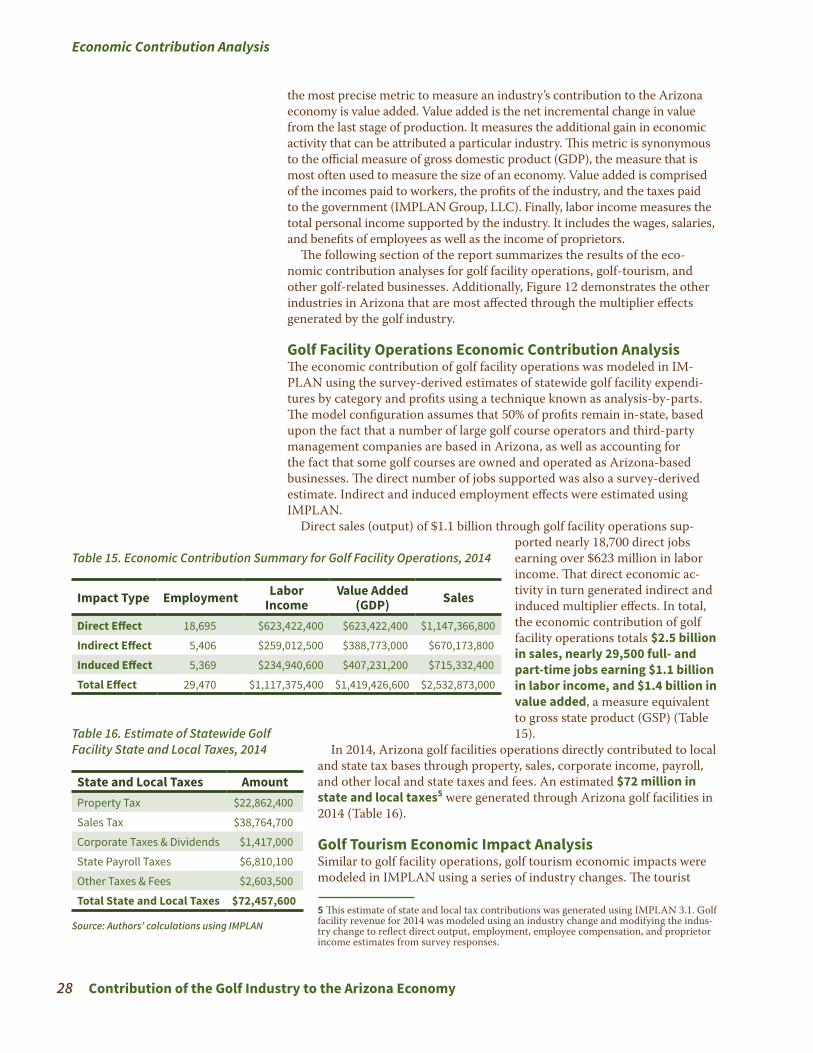

Golf Facility Operations Economic Contribution AnalysisThe economic contribution of golf facility operations was modeled in IM-PLAN using the survey-derived estimates of statewide golf facility expendi-tures by category and profits using a technique known as analysis-by-parts. The model configuration assumes that 50% of profits remain in-state, based upon the fact that a number of large golf course operators and third-party management companies are based in Arizona, as well as accounting for the fact that some golf courses are owned and operated as Arizona-based businesses. The direct number of jobs supported was also a survey-derived estimate. Indirect and induced employment effects were estimated using IMPLAN.

Direct sales (output) of $1.1 billion through golf facility operations sup-

Table 15. Economic Contribution Summary for Golf Facility Operations, 2014

Impact Type Employment Labor Income

Value Added (GDP) Sales

Direct Effect 18,695 $623,422,400 $623,422,400 $1,147,366,800

Indirect Effect 5,406 $259,012,500 $388,773,000 $670,173,800

Induced Effect 5,369 $234,940,600 $407,231,200 $715,332,400

Total Effect 29,470 $1,117,375,400 $1,419,426,600 $2,532,873,000

ported nearly 18,700 direct jobs earning over $623 million in labor income. That direct economic ac-tivity in turn generated indirect and induced multiplier effects. In total, the economic contribution of golf facility operations totals $2.5 billion in sales, nearly 29,500 full- and part-time jobs earning $1.1 billion in labor income, and $1.4 billion in value added, a measure equivalent to gross state product (GSP) (Table 15).Table 16. Estimate of Statewide Golf

Facility State and Local Taxes, 2014

Source: Authors’ calculations using IMPLAN

State and Local Taxes AmountProperty Tax $22,862,400

Sales Tax $38,764,700

Corporate Taxes & Dividends $1,417,000

State Payroll Taxes $6,810,100

Other Taxes & Fees $2,603,500

Total State and Local Taxes $72,457,600

In 2014, Arizona golf facilities operations directly contributed to local and state tax bases through property, sales, corporate income, payroll, and other local and state taxes and fees. An estimated $72 million in state and local taxes5 were generated through Arizona golf facilities in 2014 (Table 16).

Golf Tourism Economic Impact AnalysisSimilar to golf facility operations, golf tourism economic impacts were modeled in IMPLAN using a series of industry changes. The tourist

5 This estimate of state and local tax contributions was generated using IMPLAN 3.1. Golf facility revenue for 2014 was modeled using an industry change and modifying the indus-try change to reflect direct output, employment, employee compensation, and proprietor income estimates from survey responses.

Economic Contribution Analysis

Contribution of the Golf Industry to the Arizona Economy 29

spending pattern provided in previous sections was used to simulate eco-nomic activity in the hotel and restaurant industries and other industries where golf tourists would spend their moneys. Retail margins were applied to retail industries for purposes of calculating indirect and induced effects, while maintaining direct output as gross sales figures. Direct employment, labor income, and value added were calculated using IMPLAN.

As reported in previous sections, out-of-state tourist spending attributable to golf had an estimated direct sales impact of $598 million in 2014. Those sales, including indirect and induced multiplier effects, supported $1.1 bil-lion in sales, $576 million in value added, and nearly 10,500 jobs earning $343 million in labor income (Table 17). Because this spending is by out-of-state visitors, it represents money coming into Arizona from outside the state. This represents exogenously demanded goods and services and therefore can be considered an economic impact (versus an economic contribution).

Table 17. Economic Contribution Summary for Golf Tourism, 2014

Impact Type Employment Labor Income Value Added Sales

Direct Effect 7,102 $192,571,900 $320,162,700 $598,300,200

Indirect Effect 1,478 $68,497,100 $113,541,400 $208,667,400

Induced Effect 1,875 $82,044,400 $142,217,800 $249,836,200

Total Effect 10,455 $343,113,500 $575,921,800 $1,056,803,800

Golf Facility Operations Golf-Related Businesses Golf Tourism

• Other amusement and recreation industries

• Wholesale trade• Real estate• Office administrative

services• Owner-occupied

dwellings• Other local government

enterprises• Electric power transmis-

sion and distribution• Landscape and

horticultural services• Insurance carriers• Hospitals

• Hotels and motels, including casino hotels

• Full-service restaurants• Automotive equipment

rental and leasing• Retail: Clothing and

clothing accessories stores

• Retail: Miscellaneous store retailers

• Other amusement and recreation industries

• Amusement parks and arcades

• Real estate• Transit and ground

passenger transportation• Owner-occupied

dwellings

• Retail: Motor vehicle and parts dealers

• Retail: Sporting goods, hobby, musical instru-ment, and book stores

• Real estate• Other educational

services• Owner-occupied

dwellings• Travel arrangement and

reservation services• Other amusement and

recreation industries• Wholesale trade• Insurance carriers• Hospitals

Figure 12. Top 10 Industries Impacted by Component of Economic Contribution Analysis

Top industries impacted by golf tourism include hotels and motels ($199 million total sales impact), restaurants ($88 million total sales impact), and car rental ($68 million total sales impact), closely mirroring the tourist spending pattern (Figure 12). Hotel and motel sales supported by golf tourism support an estimated 1,960 full- and part-time jobs in that industry. Golf tourism directly generated an estimated $32 million in state and local sales tax revenues.

Economic Contribution Analysis

30 Contribution of the Golf Industry to the Arizona Economy

Table 19. Economic Contribution Summary, Total, 2014

Impact Type Employment Labor Income Value Added Sales

Direct Effect 27,013 $855,173,300 $1,002,200,900 $2,015,827,000

Indirect Effect 7,101 $337,132,100 $519,041,200 $909,074,400

Induced Effect 7,595 $332,317,900 $576,027,200 $1,011,858,200

Total Effect 41,708 $1,524,623,300 $2,097,269,200 $3,936,759,600

Golf-Related Businesses Contribution AnalysisEstimates of sales from golf-related businesses were modeled in IMPLAN as a series of industry changes according to their corresponding IMPLAN in-dustries (Appendix E). Direct employment effects were estimated using IM-PLAN, as were indirect and induced effects. Retail margins were applied to all retail industries in order to calculate indirect and induced effects, while the direct effects were measured as gross sales. This can be observed in the results (Table 18) in the relatively small indirect effects across employment, labor income, value added, and sales.

Table 18. Economic Contribution Summary for Golf-Related Businesses, 2014

Impact Type Employment Labor Income Value Added Sales

Direct Effect 1,216 $39,179,000 $58,615,800 $270,160,000

Indirect Effect 217 $9,622,600 $16,726,800 $30,233,100

Induced Effect 350 $15,332,900 $26,578,200 $46,689,600

Total Effect 1,784 $64,134,400 $101,920,800 $347,082,800

In total, including multiplier effects, golf-related business direct sales of $270 million supported a total of $347 million in sales, $102 million in value added, $64 million in labor income, and nearly 1,800 full- and part-time jobs.

Similar to the case of golf facilities, the top industries affected by spending at golf-related businesses includes those same golf-related businesses (direct effects), but also industries affected when individuals employed by supporting industries go out and spend their incomes on household expenditures such as rent or mortgage or medical care (Figure 12). Golf-related businesses gener-ated an estimated $6.5 million in direct sales tax revenues for local and state governments.

Total Economic ContributionThe total contribution of the golf industry in 2014, including golf facility operations, golf tourism, and golf-related businesses, totaled $3.9 billion in direct, indirect, and induced sales (Table 19). Nearly 42,000 jobs were supported, both directly and through multiplier effects, earning $1.5 billion in labor income. The golf industry contributed $2.1 billion to gross state product (value added) through direct and multiplier effects.

Residential Real Estate Premiums

Contribution of the Golf Industry to the Arizona Economy 31

Residential Real Estate PremiumsThe hedonic price method is a common method used in real estate and environmental economics to estimate the economic value of attributes of a neighborhood such as quality of schools, environmental goods (such as proximity to parks or open space), or environmental risks (such as proximity to Superfund sites). The basic idea behind this approach is that a house can be characterized as a bundle of attributes. Some of these attributes are spe-cific to the house (square footage, lot size, whether it has a swimming pool), while others are attributes of the neighborhood where the house is located. Multivariate regression analysis is used to estimate the value of a home as a function of its various attributes. Several studies have included proximity to golf courses as one variable for analysis, either as a main factor of interest or simply as a control variable.