Content at Glance :- - Welcome To AP Institute of...

30

Transcript of Content at Glance :- - Welcome To AP Institute of...

AP Institute For Training and Learning Pvt Ltd 1

Content at Glance :-

1.0 Articles

1. Analysis of case - SARAL WIRE CRAFT PVT LTD vs. Commissioner

Customs, Central Excise and Service Tax, and ORS by CA Avinash

Poddar

2. An Article on “Levy of Service Tax on Salami or Premium” by CA

Avinash Poddar and CA Aishwarya Agarwal

3. An Article on “Detailed Manual Scrutiny of Service Tax Returns” by CA

Avinash Poddar and CA Aishwarya Agarwal

4. GST – Whether really a Game Changer by CA Avinash Poddar

2.0 News & Updates

1. New GST can remove a lot of wastage: Kaushik Basu, chief economist of

World Bank

2. Open to amendments in future once GST bill is passed: Rajnath

3. Gujarat High Court refers judges' plot allotment PIL to larger bench

4. Govt makes last-ditch attempt to clear Bill on GST in monsoon session

5. SC stays HC order upholding tax on legal services to firms

6. SC stays Gujarat HC order on judges' plot allotment PIL

3.0 Case Laws

1. M/S Habasit Lakoka Pvt Ltd Vs Commissioner Of Central Excise,

Coimbatore

2. Mirc Electronics Ltd. Vs. Commissioner Of Central Excise, Thane-I

3. Commissioner Of Central Excise, Aurangabad Vs. Rudra Galaxy Channel

Ltd.

4. Reliance Communications Ltd Vs. Union Of India And Ors

5. Eagle Corporation Pvt Ltd And 1 Vs. Union Of India And 4

6. Union Of India And Ors Vs M/S Karvy Stock Broking Ltd

7. M/S Khicha Industries Vs Commissioner Of Central Excise -Jaipur-II

8. Akme Projects Ltd Vs Commissioner Of Service Tax, Bangalore

9. Nrb Bearing Ltd Vs Commissioner Of Central Excise, Mumbai

10. Commissioner Of Central Excise-Ahmedabad-Iii Vs M/S Nirma Ltd

11. M/S. India Switch Company Pvt. Ltd. Vs.Cst, Chennai

12. Durgapur Diesel Sales & Service Vs. Superintendent (Service Tax) Central

Excise, Durgapur

AP Institute For Training and Learning Pvt Ltd 2

13. V.N.K. Menon & Co. Vs. Customs, Excise & Service Tax Appellate

Tribunal

14. Commissioner Of Customs (Import) Vs. N.T. Rama Rao

15. Rgl Converters Vs. Commissioner Of Central Excise, Delhi-I

16. 1) M/S Ssf Plastics India Pvt Ltd, 2) Mr Ramesh Chugh Vs. 1) The Union

Of India Ministry Of Finance Law And Justice Aayakar Bhavan, New

Marine Lines Mumbai, 2) The Commissioner Of Central Excise Customs

And Service Tax, Daman Commissionerate, 4th Floor, Adarshdham

Building, Vapi-Daman Road,Vapi

17. Commissioner Of Central Excise, Thane-Ii Vs United Shippers Ltd

18. Mr Xavier Thomas Vs The Union Of India

19. M/S City Travels Vs Commissioner Of Central Excise, Coimbatore

20. M/S Coral Crest Builders Vs Commissioner Of Central Excise, Coimbatore

21. M/S. Bombay Market Art Silk Co Op. Ltd Vs.Commissioner, Central

Excise & Service Tax, Surat I

22. Allied Transport Vs.Commissioner Of Central Excise, Customs, Service

Tax, Mumbai

23. Geojit Bnp Paribas Financial Services Ltd. Vs. Commissioner Of Central

Excise, Customs & Service Tax

24. Secretary To Government Department Of Agriculture Vs. Union Of India

25. Fifth Avenue Sourcing (P.) Ltd. Vs. Commissioner Of Service Tax, Chennai

26. Garden Silk Mills Ltd. (Pfy Division) & 1 Vs. Union Of India & 2

27. M/S The India Cements Ltd Vs. Commissioner Of Central Excise,

Tirunelveli

28. Standard Auto Agencies Vs Commissioner Of Central Excise And Service

Tax-Bhopal

29. M/S Allspheres Entertainment Pvt Ltd Vs Commissioner Of Central

Excise, Meerut

30. M/S Tilaknagar Industries Ltd Vs Commissioner Of Central Excise,

Aurangabad

31. Cst, Delhi Vs.M/S. Bagai Construction

32. Ismt Ltd. Vs. Commissioner Of Central Excise, Pune

33. C.M.G. Ductiles Ltd. Vs. Commissioner Of Central Excise, Kolkata-Iv

34. Sanco Trans Ltd. Vs. Commissioner Of Customs

35. Commissioner Of Central Excise Vs. Federal Mogul Tpr India Ltd.

36. Fun Multiplex (P.) Ltd. Vs. Union Of India

37. M/S Tata Chemicals Ltd Vs. Collector Of Central Excise, Ahmedabad

AP Institute For Training and Learning Pvt Ltd 3

38. M/S Jayaswal Neco Ltd Vs. Commissioner Of Central Excise, Raipur

39. M/S Ganpati Zilha Krishi Audyogik Sarva Seva Sahakari Society Ltd Vs.

Commissioner Of Central Excise, Kolhapur

40. Mr Haresh Goradia, Mr Hemant J Patel, Mr Manohar V Date Vs.

Commissioner Of Central Excise, Raigad

41. Amogh Broadband Services Pvt Ltd Vs Commissioner Of Central Excise,

Bangalore-I

42. M/S G E T Engineering Constructions Pvt Ltd Vs Commissioner Of

Service Tax, Chennai

43. M/S Afcons Infrastructure Ltd Vs Commissioner Of Central Excise And

Service Tax, Daman

44. Commissioner Of Customs Delhi Iii Vs.M/S. Mark Exhaust Systems Ltd.

45. Commissioner Of Central Excise & Customs Aurangabad Vs.Nagar

Taluka Shramik Seva Sangh

46. Powerage Industries Ltd. Vs. Commissioner Of Central Excise & Service-

Tax, Jaipur-I

47. Samsung India Electronics (P.) Ltd. Vs. Commissioner Of Central Excise

And Service Tax

48. Ganesh Yadav Vs. Union Of India

49. Gilco Exports Ltd. Vs. Union Of India

50. Centre For Development Of Advance Computing Vs. Commissioner Of

Central Excise, Pune

51. Surlux Diagnostic Ltd. Vs. Assistant Commissioner Of Customs

52. Sangita Sajjan Jindal Vs. Union Of India And Ors

53. Tec Paper Pvt Ltd Vs. Union Of India & 1

54. Commissioner Of Central Excise, Pune-I Vs. M/S Ganesh Enterprises

55. Anurag Kashyap Vs. Union Of India & Ors

56. M/S Vodafone South Ltd Vs Commissioner Of Central Excise And Service

Tax - Chandigarh - II

57. Commissioner Of Customs And Central Excise Vs M/S Grip Engineers

Pvt Ltd

AP Institute For Training and Learning Pvt Ltd 4

1.0 Articles

1. Analysis of case - SARAL WIRE CRAFT PVT LTD vs. Commissioner Customs, Central Excise and Service Tax, and ORS by CA Avinash Poddar

SARAL WIRE CRAFT PVT LTD vs.

Commissioner Customs, Central Excise and

Service Tax, and ORS

Issue: Service of Adjudication Order

Authored by CA Avinash Poddar, Managing

Partner, A A P & Co.

Issue: Service of Adjudication Order

Supreme Court of India has set aside the

impugned orders of High Court of Uttarakhand

where the honorable high court has pronounced

that an Appeal is a creature of the statute and

therefore it being filed beyond the permitted time

limit under the statute is a futile exercise.

In Favour of: Assessee

Facts of the Case

Appellant has sought to take advantage of a

Notification granting exemption from payment of

Central Excise Duty as well as Additional Duty of

Excise for a period of ten years.

Dispute was whether the exemption would be

available to the appellant means whether the

location where the Appellant’s factory/unit is

located covered under the exemption notification.

Issue was raised and revenue was of the view that

the exemption is not applicable to the Appellant

and hence the Show Cause Notice dated 25.03.2011

was issued.

Assistant Commissioner concluded the proceedings

and hearings in respect of SCN on 28.07.2011 but

issued the order holding that the appellant is not

eligible for exemption on 30.03.2012.

Appellant contended that he got aware for the first

time, regarding the fact that the order was passed

by the Assistant Commissioner holding that the

Appellant is not eligible for the exemptions, on

26.07.2012 when the recovery proceedings was

initiated by the department.

As per the details with the department the

Adjudication order was served on an employee of

the Appellant, named Sanjay.

As per the Appellant Sanjay was a ‘kitchen boy’

employed on daily wages and he was not all

allowed to deal with the communication to and

from the Appellant. Sanjay has affixed the stamp

/seal of the Appellant, on 03.04.2012, for which he

was unauthorized.

Once the Appellant become aware of the order

passed by the officer he filed an appeal on

22.08.2012 but the said appeal was held not

maintainable by the Commissioner (Appeals) as the

same was filed beyond 60 days prescribed period.

Hence case was not considered on merits at all.

Thereafter CESTAT and High Court of Uttarakhand

both has upheld the same and rejected the appeal

and have not considered on merits.

Matter in Question (No. 1) – Whether serving of

the order to Kitchen Boy is correct way of serving.

Before discussing on this let us first try to

understand what the statute provides. Section 37C

of the Central Excise Act is reproduced as under:

(1) Any decision or order passed or any summons or notices issued under this Act or the rules made thereunder, shall be served, -

(a) by tendering the decision, order, summons or notice, or sending it by registered post with acknowledgment due [or by speed post with proof of delivery or by courier approved by the Central Board of Excise and Customs constituted under the Central Boards of Revenue Act, 1963 (54 of 1963)] to the person for whom it is intended or his authorised agent, if any;

(b) if the decision, order, summons or notice cannot be served in the manner provided in clause (a), by affixing a copy thereof to some conspicuous part of the factory or warehouse or other place of business or usual place of residence of the person for whom such decision, order, summons or notice, as the case may be, is intended;

(c) if the decision, order, summons or notice cannot be served in the manner provided in clauses (a) and (b), by affixing a copy thereof on the notice board of the officer or

AP Institute For Training and Learning Pvt Ltd 5

authority who or which passed such decision or order or issued such summons or notice.

As per the above provisions it is clear that every

efforts shall be made to serve the order to the

affected party so that he not only has the knowledge

about the order but also he can make himself enable

to initiate any further action such as appeal, etc.

Honorable Supreme Court observed that the

inspector of the department should have

meticulously followed and obeyed the mandate of

the statute and tendered the Adjudication order

either or the party on whom it is was intended or

on its authorized agent.

Hence as per the Honourable Supreme Court

serving of the order on the Kitchen boy is not

proper and hence the case shall be admitted by the

Commissioner (Appeals) since the appeal was

filed on 22.08.2012 is within 60 days from the date

the assessee got awareness of the order i.e. on

26.07.2012.

Relevant Extract of the Supreme Court Order

It is an anathema in law to decide a matter without due notice to the concerned party. Every effort must be taken to meaningfully and realistically serve the affected party so as not merely to ensure that he has knowledge thereof but also to enable him to initiate any permissible action. The Appellant justifiably submits that it was statutorily impermissible for the Respondents to serve the Adjudication Order on a "kitchen boy", who is not even a middle level officer and certainly not an authorized agent of the Appellant.

The version of the Appellant that it learnt of the passing of the Adjudication Order dated 30.3.2012 only when, in the course of the recovery proceedings, the Department's officials had visited its unit, is certainly believable. The fact that, firstly, the Order had not been passed in the presence of the Appellant, so as to render its subsequent service a formality, and secondly, that the Order came to be passed after an inordinate period of eight months should not have been ignored. This fact should not have been lost sight of by the Authorities below as it has inevitably led to a miscarriage of justice. The Inspector of the Department should have meticulously followed and obeyed the mandate of the statute and tendered the Adjudication Order either on the party on whom it was intended or on its authorized agent and on one else.

It is not the Respondents' case that Shri Sanjay was the authorized agent. Even before us, despite several opportunities given, the Respondents have failed to file their response to the Special Leave Petitions so as to controvert the asseveration of the Appellant that Shri Sanjay on whom the decision was tendered was a mere daily wager 'kitchen boy' and that the Appellant had no knowledge of the passing of the Adjudication Order. We are also informed that the recoveries envisaged in the Adjudication Order have already been effected. It is in these circumstances that we are of the clear conclusion that a miscarriage of justice has taken place, in that the Authorities/Courts below have failed to notice the specific language of Section 37C(a) of the Act which requires that an Order must be tendered on the concerned person or his authorized agent, in other words, on no other person, to ensure efficaciousness.

We must immediately recall the decision in Taylor vs. Taylor (1875) 1 Ch. D 426, rendered venerable by virtue of its jural acceptance and applicable for over a century. It was approved by the Privy Council in Nazir Ahmad v. King Emperor (1935-36) 63 IA 372 and was subsequently applied in Rao Shiv Bahadur Singh v. State of Vindhya Pradesh AIR 1954 SC 322, State of UP v. Singhara Singh AIR 1964 SC 358, Babu Verghese v. Bar Council of Kerala (1999) 3 SCC 422 and more recently in Hussein Ghadially v. State of Gujarat (2014) 8 SCC 425.

As observed by this Court in Babu Verghese, "it is the basic principle of law long settled that if the manner of doing a particular act is prescribed under any statute, the act must be done in that manner or not at all." The Inspector who ostensibly served the copy of the Order should have known the requirements of the statute and therefore should have insisted on an acknowledgement either by the Appellant or by its authorized agent. The Inspector had a statutory function to fulfil, not a mere perfunctory one.

The Appeals are accordingly allowed and the impugned Orders are set aside. In the facts obtaining before us, the computation of the period would commence at least from the date on which the Appellant asserts knowledge of its existence, i.e. on 26.7.2012. So computed, the Appeal filed before the Commissioner (Appeals) on 22.8.2012 would be within the prescribed period of 60 days and should, therefore, have been entertained on merits. It is ordered accordingly. The Appellant shall appear before the Commissioner (Appeals) on the forenoon of 3.8.2015. The Appeal shall then be taken up and heard on its merits.

AP Institute For Training and Learning Pvt Ltd 6

Conclusion

Adjudication order has to be served properly by the

department as per the provisions of Section 37C of

the Central Excise Act 1944. And it is their

responsibility to make sure that the order is

properly conveyed to the person to whom it is

intended to be served and he shall be enable to

decide his further course of action i.e. filing appeal.

2. Levy of Service Tax on Salami or Premium

Over the period of time it has been observed that levy of service tax on renting of immovable property has undergone several changes and witnessed various disputes involving constitutional as well as legal questions.

Renting of immovable property was brought into tax netin 2007 for the very first time vide section 65(90a) read with section 65(105)(zzzz) of the Finance Act, 1994. Since then, taxability on renting of immovable property is challenged under various courts and petitions are filed with regards to its constitutional validity before various high courts. The Hon’ble delhi High Court in Home Solutions Retails (India) Limited v. Union of India, - 2011-TIOL-610-HC-DEL-ST-LB, upheld the validity of this levy against which the appeal is still pending before the Hon’ble Supreme Court. While the said appeal is pending before the Apex Court various new emerging issues with huge revenue stakes have cropped up regarding this “Renting of Immovable Property” category of service.

In this article we are trying to bring light on the issue pertaining to the Long-term lease where one time payment in name of salami/ premium as well as the other periodical payments in form of rent charged by the property owner for such immovable property. Issue mainly arises as to whether service tax extends to such salami/premium charged by owner of the property or whether it is only limited to the periodical rent collected.

Service tax has gone through various amendments. Prior to July,2012 service tax has different perspective to charge service tax on various services which changed with the introduction of negative list after July,2012. Prior to July, 2012 renting of immovable property service includes leasing as per section 65(90a) of the Finance Act, 1994. However, the term “leasing” or “lease” has not been defined in the act. In ordinary legal sense lease means demise or transfer of a right to enjoy the property for a fixed term or for perpetuity for a consideration

of a price paid or promised or services or other things of a value to be rendered periodically or on a specific occasions to the lesser /transferor. A leasehold estate is an ownership of a temporary right to hold land or property in which a lessee or a tenant holds rights of real property by some form of title from a lessor orlandlord. In other words, lease agreement can be entered into for any period/ duration. Normally, long term lease are entered into for a period say for 90 years, 99 years, 100 years, etc.

Now, it is very much important for us to first understand the difference between lease and ownership. Lease is only transferring a right to enjoyment to a property while the ownership denotes complete and total control over the property and not only the right to enjoyment. The lessee is only the tenant.Though, he may be entitled to transfer his interest in the property but the right to transfer the property only vests with the owner of the property. Tenancy cannot be said to permanent ownership even when the tenant has incurred capital cost for structures/ construction of such property.

The right of ownership of property cannot be decided by the duration of the lease. Thus, long term lease even if it is for a period of 99 years does not confer the tenant/ lessee ownership, unless thereis specific transfer of the said property under lease but in that case it will no more be a lease. It is settled law that the lease period is not an indication to decide the ownership of the property.

This lease arrangement involves a premium which is paid for such grant of lease to enjoy the property’s use (such one-time premium is paid to acquire leasehold rights and is popularly called salami), particularly when the lease is being taken from a Government Authority, such as an Industrial Development Corporation or a Regional Development Authority. In addition to the premium, periodical amount may also be charged commonly known as rent, which at times may be a nominal amount. The payment of such a salami/premium has been the subject matter of several controversies, under the tax laws, including the liability of the payer to deduct tax at source u/s 194-I and his eligibility to claim deduction for such payment in computing his total income, taxability of such onetime payment i.e. premium/ salami under service tax laws.

The question in matter is for taxability of such salami/ premium under service tax. For the period prior to July 2012, Service Tax was imposed only on taxable services specified in Section 65(105), one of which was renting of immovable property service.

AP Institute For Training and Learning Pvt Ltd 7

The taxable event, thus, under Section 66 of the Act was renting of immovable property service, i.e. continuous enjoyment of the property and in this regard tribunal in the case of Greater Noida Industrial Development Authority vs. CCE (2014) TIOL 1741, has held that the service tax under section 65(105)(zzzz) read with section 65(90a) cannot be charged on the premium or the salami paid by the lessee to the lesser for the transfer of the interest in the property from the lesser to the lessee as this amount is not for continuous enjoyment of the property leased. Also it was further observed that the levy of Service Tax is on renting of immovable property and not on transfer of interest in property from lesser to lessee.

Thus, as regards the provisions existing for the period prior to July 2012, the decision standsclear that salami or premium will not be chargeable to Service Tax under the category of renting of immovable property services. However, it would depend on the facts and circumstances of each case so as to see whether it is actually a payment for parting of interest or not.

As regards the legal provisions prevailing on date, Section 66B read with Section 65B(44) of the Finance Act 1994,provides for charge of Service Tax on all activities undertaken by one person for another for consideration. The definition of 'service' under Section 65B(44) includes declared services as specified in Section 66E and Renting of immovable property is one of the declared services and thus, it constitutes 'service'. The definition of 'service' further excludes a transfer of title in goods or immovable property, by way of sale, gift or in any other manner. The question nowin relation to the new legal provisions arises as to whether the salami/ premium is chargeable to Service Tax or not.

As already discussed earlier, salami/ premium is paidas onetime payment towards transfer of or parting with the right of the lesser in the immovable property. Though there is transfer of such right but it does not result in transfer of ownership thereof. And the fact still remains that there is a transfer of some right in the immovable property. Only exclusion from the definition of 'service' is only transfer of title in immovable property, whether it is by way of sale, gift or in any other manner. Thus, the transfer of title in immovable property is necessary and not the manner in which the transfer is made.

Mere transfer of custody or possession over goods or immovable property, where ownership is not

transferred, does not amount to transfer of title. Circular No.334/1/2012-TRU, dated 16.03.2012.

Section 65B(44) of the Finance Act 1994which defines “service” has certain exclusions which includes the transfer of title in immovable property. In other words, the title in the immovable property itself has to be transferred, i.e. the ownership thereof has to be transferred so as to be covered under the scope of the exclusion clause. By payment of salami/ premium, the lessee does not get any title of ownership in the immovable property. In such a case, the payment of salami/ premium will not be excluded from the definition of 'service'. Though salami/ premium is paid towards transfer of right or interest of the lessor in the property to the lessee but such transfer of right does not result into transfer of title in immovable property in reality. Also, in New Okhla Industrial Development Authority v/s CCE (2014) 45 GST 187 = 44 taxmann.com 287 (CESTAT) (order dated 11-12-2013), it has been held that even a long term lease of 99 years is renting & subject to service tax.

It can now be said that under the new legal provisions, even salami/ premium may get included within the scope of levy of Service Tax. The scope of charge of Service Tax under Section 66B extends to all activities undertaken by one person for another for consideration and it is not restricted to renting only. The taxable event in case of declared services of renting of immovable property continues to be the right to enjoyment of the property. Accordingly, if the activity undertaken against receipt of salami is not excluded from the definition of 'service', the same will become chargeable to Service Tax.

3. Detailed Manual Scrutiny of Service Tax Returns

Ques. 1 What type of return scrutiny was

envisaged under Circular No 185/4/2015 –ST (F.No.137/314/2012 - Service Tax)?

what was the purpose and how is it different from Service Tax Audit prevailing till date?

Ans. 1 In order to put strong return scrutiny system, a two-part system of return scrutiny was envisaged. One is preliminary scrutiny which would be online covering all the returns, and secondly, a detailed manual scrutiny of selected returns which will be identified by the Division/ Range officers on the basis of risk parameters. This system has been incorporated to ensure the correctness of the assessments made by the assessee so as to check the

AP Institute For Training and Learning Pvt Ltd 8

taxability, value of taxable service, payment of service tax, etc.

A detailed scrutiny programme typically supplements the audit programme.

The detailed manual scrutiny programme must replicate some of the best practices in audit. A Return Scrutiny Cell should be created in the Commissionerate's Headquarters. The Return Scrutiny Cell shall maintain the records of the assessees and the returns which are selected for detailed scrutiny and also the results thereof.

The scope of audit is to inspect the financial records of a company for a complete financial year in order to identify non-compliance issues and to evaluate the assessee's internal control system. The two processes of audit and scrutiny are, in fact, complementary to each other.

Ques. 2 How returns are selected for the manual scrutiny?

Ans. 2 The focus of detailed manual scrutiny of the returns would be on the returns of those assessees which are not being audited. The detailed return scrutiny would be conducted in respect of such assessees whose total tax paid (Cash + CENVAT) for the FY 2014-15 is below Rs 50 lakhs. Each Commissionerate has to select equal number of assessees for carrying out return scrutiny.

For these scrutiny, following three total tax paid bands (whether paid in cash or using CENVAT) has been created for the financial year 2014-15.

1. Tax Paid- UptoRs. 10 Lakh 2. Tax Paid- From Rs. 10 Lakh to Rs. 25

lakhs 3. Tax Paid- From Rs. 25 Lakh to Rs. 50

lakhs Ques. 3 What will be the process followed by the

department for such detailed manual scrutiny ?

Ans. 3 The risk parameters and the risk tools which would govern the selection of the returns for detailed manual scrutiny have been developed. The risk scores for the Service Tax returns for the financial year 2014-15 will be calculated and then the data will be segregated on the basis of Zone/Commissionerate/Division/Range. The data resides with DGS&DM which will be shared with the Service Tax & Central Excise field formations through secure data exchange in the following manner:

• The risk score files will be placed on a server. Chief Commissioners of Service Tax

& Central Excise Zones are required to nominate a `Zonal Nodal Officer' who shall access these data and distribute the same to the Zonal Commissionerates dealing with Service Tax. The said officer should preferably be of the rank of Additional/Joint Commissioner and should necessarily have an official email id (ICEGATE or MC email).

• The nomination of Zonal Nodal Officers should be informed to the Service Tax Wing,CBEC by email alongwith attaching a scanned copy ofthe nomination letter. The said communication should contain the nomination by the ChiefCommissioner along with the designation, email id, telephone numbers (mobile & land line numbers) of the nominated Nodal Officer.

• An email will be sent by DGS&DM to the Zonal Nodal Officer. These Zonal Nodal Officers would need to copy and paste on the internet browser the 'weblink' of the page hosting the folders. They would need to login using the username and password which would be shared with them through a separate email sent on their official email id. They would then need to click on the folder bearing the respective Zone name (available on the left panel) to access the files placed there.

• The Return Scrutiny Cell, through an officer authorized by the Commissioner, shall collect the Risk Score data for the Commissionerate from the Zonal Nodal Officer.

• The list of returns to be taken up for detailed scrutiny would be finalized by the Additional/Joint Commissioner in-charge of Division (or in his absence by the Commissioner) as per the risk score in conjunction with the total tax paid by the assessee, local risk parameters (including sensitive and evasion prone sectors), past compliance record of the assessee and manpower availability.

• The list of the assessees selected will be sent to the respective Divisions.

NOTE: (1) The assessees who have been selected for

audit or have been audited recently (in the past three years) should not be taken up for detailed scrutiny. However, the Chief Commissioner, may direct detailed manual scrutiny of an assessee's return who has paid service tax (Cash + CENVAT) more than Rs 50 lakhs in certain specific cases.

(2) In no event should an assessee be subjected to both audit and detailed manual scrutiny.

AP Institute For Training and Learning Pvt Ltd 9

(3) All the officers should maintain strict confidentiality regarding the Risk Score data including the original score, further selection by the Commissionerate, etc. Under no circumstances it is to be shared with the assessee or any other authority since this is information available in a fiduciary relationship, pertaining to a third party, and which may entail further investigation.

Ques. 4 Methodology adopted for the detailed

manual scrutiny? Ans. 4 Detailed scrutiny of returns must be

conducted by the Service Tax Range headed by theSuperintendent and is assisted by a complement of Inspectors. However, the Divisional DC/AC shall be responsible for the overall supervision of this business process in respect of his/her division.

Before return scrutiny is initiated, the assessee must be given prior intimation of at least 15 days and the purpose of the exercise must be spelt out in an Intimation Letter in a format given as Annexure I. Once an assessee's returns are taken up for detailed scrutiny, the Range should compile the Assessee Master Information to facilitate trend analysis in a format given as Annexure II. Since this information is based on the returns, it can be obtained from the returns filed in ACES without making any reference to the assessee.

Returns scrutiny must be done for a complete financial year by looking at two half-yearly returns in conjunction. Before scrutinizing the return for evaluating the correctness of assessment, the information available in the assessee master should be carefully studied by the Divisional DC/AC and must be discussed with his officers, much like Desk Review in Audit.

To begin with, the returns for the financial year 2013-2014 should be taken up for detailedscrutiny. One of the important objectives of return scrutiny is to ensure validation of the information furnished in the self-assessed ST-3 return. The validation exercise would require reconciling information furnished in the ST-3 return with ITR Form Nos. 4, 5, 6 and 26AS and any third party information made available.

In addition to this, the scrutiny exercise mustalso look at the correctness of self-assessment with respect to taxability, admissibility ofabatement and eligibility

for exemption, valuation and CENVAT credit availed/utilized.

A Checklist has been prepared for carrying out detailed manual scrutiny of selected ST-3 returns (Annexure III). For achieving the stated objectives, the checks have been categorized as follows:

• Reconciliation for validation of the information furnished in the ST-3 return;

• Taxability in respect of services which may have escaped assessment;

• Classification (for the purposes of due availment of abatement/exemption benefit);

• Valuation; and • Cenvat credit availment/utilization.

In case any additional details are required, the same may be obtained from the assessee through requisition rather than through a visit. Calling of such additional documents must be done with the approval of the jurisdictional DC/AC so as to obviate the complaint of administrative intrusion.

Based on the experience of some Zonal Commissionerates, it is seen that in a month an Inspector will be able to perform detailed manual scrutiny of a minimum of three assessees. While in some cases, it may take time.

NOTE: (1) The scrutiny process of an assessee

should be completed in aperiod not exceeding three months.

Ques. 5 How findings of the scrutiny should be documented?

Ans. 5 In order to ensure transparency of the scrutiny process, it is important to document thefindings flowing from the scrutiny effort. For this purpose, an Observation Sheet should be prepared. The format of the observation sheet, enclosed as Annexure IV, bears a one-to-one co-relation with the checklist.

The scrutiny officer must record his findings under each of the subject of the checklist namely reconciliation, taxability, classification, valuation and CENVAT credit. Under each of these heads, the officer should record any action that needs to be taken by the Range.

The findings should clearly outline the process of scrutiny that led to the outcome. It is also possible that the officer may come across some issues which may have to be referred to audit or anti-evasion. These should also be noted in the relevant column given in the observation sheet.

AP Institute For Training and Learning Pvt Ltd

In cases where detailed scrutiny of returns results in detection of defaults in service tax payment and it appears that the proviso to section 73(1) of the Finance Act, 1994 is invokable, the ST-3 returns of the past periods should also be verified and results of such verification should be recorded.

All scrutiny findings in a month must be discussed in a Monthly Scrutiny Monitoring Committee Meeting headed by the Additional/Joint Commissioner incharge of the Division (or in his absence by the Commissioner) where each Range should present their scrutiny findings in the form of a `Scrutiny Report' given as Annexure V. The meeting should be attended by all the Range Inspectors, Superintendents and DC/ACs of the Divisions whose supervisory control is with the said ADC/JC. This would provide an opportunity to the officers from other Ranges to respond to the findings and also share best practices.

The views of the committee on the return scrutiny findings must be documented and follow up action taken. Imay be put up to the Commissioner for information. The minutes of the meeting and the decisions including detection and recovery of service tax dues should be properly recorded and maintained by the Scrutiny Cell of the Commissionerate.

Zonal Chief Commissioners are requested to submit monthly reports in the formatgiven in Annexure VI toGeneral of Service Tax till facilities are developed to enable the Commissionerates to upload the data in the MIS of CBEC.

Based on the past experiences in performing detailed manual scrutiny, a few Templates/Case studies have been prepared and are enclosed as Annexures VII and VIII. These Case Studies will help and guide the officersconversant with the process ofScrutiny.

The timelines to be followed for starting detailed manual scrutiny as per the abovedetailed process are as below:

AP Institute For Training and Learning Pvt Ltd

In cases where detailed scrutiny of returns results in detection of defaults in service tax payment and it appears that the proviso to section 73(1) of the Finance Act, 1994 is

3 returns of the past periods should also be verified and the results of such verification should be

All scrutiny findings in a month must be discussed in a Monthly Scrutiny

Committee Meeting headed by the Additional/Joint Commissioner in-charge of the Division (or in his absence by

missioner) where each Range should present their scrutiny findings in the form of a `Scrutiny Report' given as

The meeting should be attended by all the Range Inspectors, Superintendents and DC/ACs of the Divisions whose supervisory control is with the said ADC/JC. This would provide an opportunity to the officers from other Ranges to respond to the findings and also

The views of the committee on the return scrutiny findings must be documented and follow up action taken. Important issues may be put up to the Commissioner for information. The minutes of the meeting and the decisions including detection and recovery of service tax dues should be properly recorded and maintained by the Scrutiny Cell of the Commissionerate.

nal Chief Commissioners are requested to submit monthly reports in the format

in Annexure VI to the Directorate General of Service Tax till facilities are developed to enable the Commissionerates to upload the data in the MIS of CBEC. Based on the past experiences in performing detailed manual scrutiny, a few Templates/Case studies have been prepared and are enclosed as Annexures VII and VIII. These Case Studies will help and guide the officers who are not

e process of Detailed

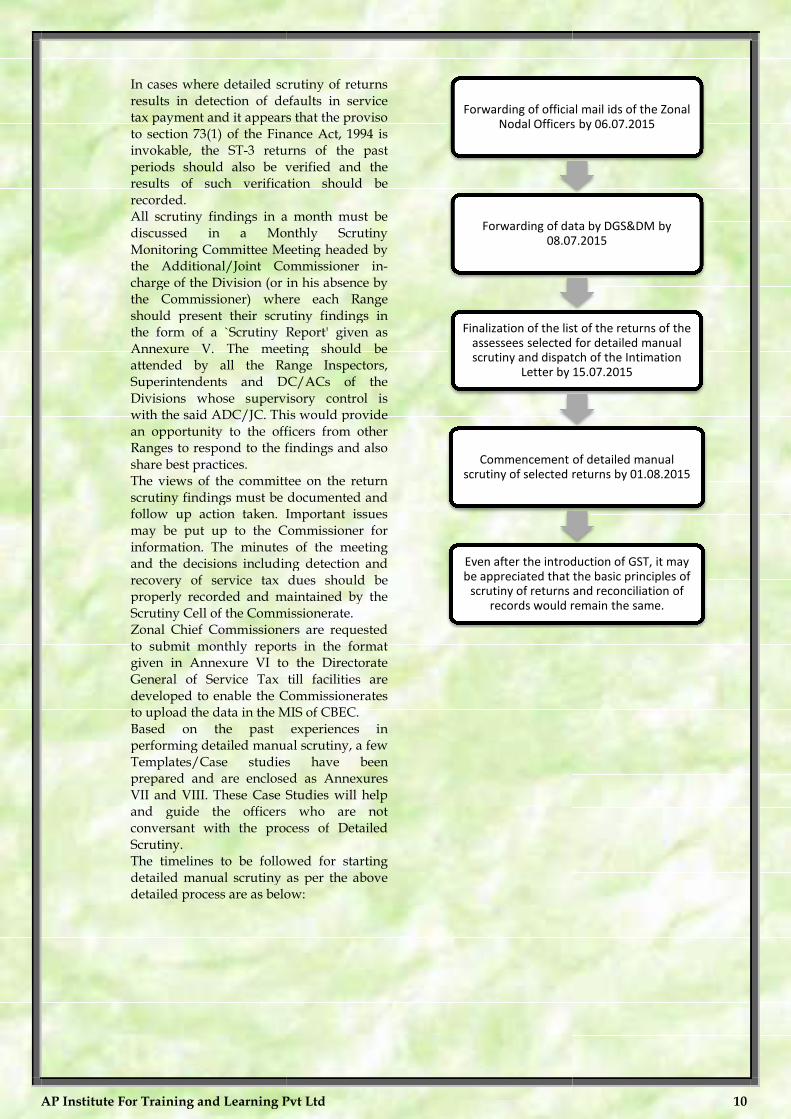

The timelines to be followed for starting detailed manual scrutiny as per the above detailed process are as below:

Forwarding of official mail ids of the Zonal

Nodal Officers by 06.07.2015

Forwarding of data by DGS&DM by

08.07.2015

Finalization of the list of the returns of the

assessees selected for detailed manual

scrutiny and dispatch of the Intimation

Letter by 15.07.2015

Commencement of detailed manual

scrutiny of selected returns by 01.08.2015

Even after the introduction of GST, it may

be appreciated that the basic principles of

scrutiny of returns and reconciliation of

records would remain the same.

10

Forwarding of official mail ids of the Zonal

Nodal Officers by 06.07.2015

Forwarding of data by DGS&DM by

08.07.2015

Finalization of the list of the returns of the

assessees selected for detailed manual

scrutiny and dispatch of the Intimation

Letter by 15.07.2015

Commencement of detailed manual

scrutiny of selected returns by 01.08.2015

Even after the introduction of GST, it may

be appreciated that the basic principles of

scrutiny of returns and reconciliation of

records would remain the same.

AP Institute For Training and Learning Pvt Ltd 11

Ques. 6 What are the appendices prescribed in this relevant notification?

Ans. 6 Following are the Annexures prescribed in this notification which are as follows:

Annexure Particulars Purpose Who will file?

Annexure-I Intimation Letter

To intimate assessee regarding their selection for manual scrutiny under this notification

Department will issue intimation letter to the assessee

Annexure-II Assessee Master Information

To facilitate trend analysis from the service tax returns filed in by the assessee

This annexure is to be filled in by the department

Annexure-III Checklist To reconcile ST-3 return, taxability, Classification, valuation, utilisation of CENVAT credit

This annexure is to be filled in by the department

Annexure-IV Observation Sheet

To document thefindings flowing from the scrutiny effort

This annexure is to be filled in by the department (Superintendent)

Annexure-V Scrutiny Report All scrutiny findings in a month should be presented their scrutiny findings

This annexure is to be filled in by the department (Range Officers)

Annexure-VI Monthly Report (MIS)

To upload the data in the MIS of CBEC

This annexure is to be filled in by the department (Zonal Chief Commissioners)

Annexure-VII Specific Observation Sheet (for the period 2011-12 to 2013-14)

To document thefindings flowing from the scrutiny effort. (Business model-Partnership Services Provided- Renting of Immovable Property Service)

This annexure is to be filled in by the department (Superintendent)

Annexure-VIII Draft Scrutiny Report

Finalisation of scrutiny report This annexure is to be filled in by the department

AP Institute For Training and Learning Pvt Ltd 12

4. GST – Whether really a Game Changer

Since almost a decade we are debating on the Biggest Tax Reform under indirect taxes in the form of Goods and Service Tax (GST). Now it seems to be a reality.

In order to introduce GST in India the very first step to be followed is amendment in the Constitution which shall enable both Centre and the State to levy tax on goods and services. Step towards the same has been taken by honorable Finance Minister, Shri Arun Jaitley by presenting the Constitution (122nd) Amendment Bill, 2014 in Lok Sabha. The bill contains the enabling provisions for the introduction of GST in the country. The said bill got cleared from Lok Sabha on 6th May 2015 and now the said bill in placed in the Rajya Sabha from where on 12th May 2015 it has been given to Select Committee and the said committee is required to submit its report in the monsoon session.

This bill is required to be passed by both the houses with 2/3rd majority and has to be further ratified by at least 15 State Legislatures. Thus once the constitution amendment bill gets cleared, the GST Act, Rules and Notifications can be issued by the authorities.

As per the statement of Honorable Finance Minister Shri Arun Jaitley, the date of introduction of GST in India is 1st April 2016. As per him the entire back end is ready and unless some unforeseen circumstance arises, GST will be implemented from the said date i.e. 1st April 2016.The most relevant and importance reason of introducing GST is to make India competitive with the outside world since due to cascading effect of taxes because of multiplicity of taxes our cost is high and this prevents us to be competitive. Thus the introduction of GST is expected to bring down the cost of the Indian Products by eliminating the cascading effect of taxes.

Let us check the main bullet points of the Constitution (Amendment) Bill, 2014 :.

First Question:

WHAT IS GOODS AND SERVICE TAX?

Goods and Services Tax means a tax on supply of goods or services, or both, except taxes on supply of alcoholic liquor for human consumption [proposed Article 366(12A) of Constitution of India]

Here it is to be noted that the word used is 'supply' and not 'sale'. Therefore it could be said that all supplies of goods and services are liable for tax under the proposed GST regime. Hence the stock transfers, branch transfers since will be covered in the supply and hence will also be covered under GST net.

The term service is defined as; 'Services' means anything other than goods [proposed Article 366(26A) of Constitution of India]

The proposed definition of service is very broad. It includes anything other than goods and therefore even an immovable property can be included.

Second Question:

GST - Tax Incidence ?

Unlike the present tax system which is origin based, GST is consumption based, i.e. tax will become payable at the place or the State in which goods and services are being consumed.

DUAL GST

As originally suggested by Mr Vijay Kelkar there shall be Unified GST in India but looking to the structure of the Country most probably it is going to be Dual GST i.e. where both the State and the Centre will levy tax on similar transaction.

Thus it is expected that there will be dual GST in India viz. State GST (SGST) and Central GST (CGST) [proposed Article 246A of Constitution of India]

Third Question:

What will be the Rate at which GST will be charged?

This is another most debatable issue. Purpose of GST is to reduce the tax burden by avoiding the cascading effect of taxes. Presently if we see both State and Central Levy on a particular transaction we will find that the average rate of tax comes to be between 24 to 28%. Hence the rate at which GST shall be charged is one of the most crucial questions to answer. Unfortunately this issue is still unanswered. But at the same time there are various rates being discussed.

As per me the rates of GST shall be between 16-18% and in case the rates are decided to be kept higher than this the expected outcome of GST will not come.

CGST rates will be common all over India but the SGST rates on the other hand shall be decided by each State and will vary from State to State.

Under the GST regime the Concept of 'declared goods' is expected to be abolished.

INTEGRATED GST FOR INTER-STATE TRANSACTIONS

In case of Inter-State supply of goods and services, there will be integrated GST (IGST) imposed by Government of India [proposed Article 269A(1) of Constitution of India]

AP Institute For Training and Learning Pvt Ltd 13

IGST will also be imposed on imports [proposed Explanation to Article 269A(1) of Constitution of India]

The IGST Rate is expected to be sum total of SGST rate and CGST rate. IGST rate will be same all across the country.

Revenue from IGST will be apportioned among Union and States by Parliament on basis of recommendation of Goods and Service Tax Council [proposed Article 269A(2) and Article 270(1A) of Constitution of India]

Important point to be noted here is mode of taxing under GST is going to be supply of goods and services. Therefore in case of stock transfers, branch transfers and even when goods are dispatched inter-State for job work and return, the IGST shall be payable. And such liability of GST on the stock transfers etc. will lead to blockage of funds and interest burden will also increase.

What about the Excise duty on petroleum and tobacco products?

It is proposed that the excise duty will continue on petroleum products and tobacco products [Entry 84 of List I (Union List) of Seventh Schedule to Constitution of India]

But in case of Tobacco products both will be levied i.e. Excise duty and also GST.

It is further proposed that the petroleum products will be covered in GST network at a later stage.

Further the states will have powers to impose sales tax on sale within the State of petroleum products and alcoholic liquor for human consumption [proposed Entry 54 of List II (State List) of Seventh Schedule to Constitution of India]

ADDITIONAL TAX @ 1% ON INTER-STATE SUPPLY OF GOODS PROPOSED FOR INITIAL TWO YEARS

As per the proposed clause 18(1) of Constitution (Amendment) Bill, 2014, 1% tax will be imposed on inter-State supply of goods for two years or such period as may be recommended by GST Council –.

This 1% is being demanded by the States against the Central Sales Tax. Now under proposed GST regime the word used is 'supply' and not 'sale'. Therefore even the stock transfers, branch transfer and free supplies will also get covered under this levy.

FOLLOWING WILL BE SUBSUMED IN GST

At present excise duty (except on the petroleum products), service tax, duties of excise on medical and toilet preparations, State Vat, Central Sales Tax, octroi, Entry Tax, Entertainment Tax, CVD and

Special CVD on imported goods will be subsumed in GST.

Besides the above basic customs duty on imports will continue And also the stamp duties will also continue.

GOODS AND SERVICE TAXES COUNCIL

'Goods and Service Taxes Council' is constituted with the purpose of proper monitoring and implementation of the GST in the country.

The Union Finance Minister will be Chairperson of the GST Council. And the following will be its members – (a) Union Minister of State for Revenue or Finance (b) Minister of Finance or any other Minister nominated by each State.

Amongst the members of the GST Council, Vice Chairperson will be elected.

The GST Council is mainly a recommendatory body on various issues relating to GST. This is the body that is going to recommend most of the changes in GST implementation from time to time.

It will have statutory powers only in following situations – (a) When petroleum products should be brought in the GST net (b) Distribution of revenue of IGST and CGST among Union and States (c) Continuation of 1% tax on supply of goods inter-State (d) Compensation to States for loss of revenue for period upto five years.

Decision in GST Council be taken with at least 75% of weighted average voting in favour of the decision. Union Government will have 33.33% voting power and States will have 66.67% voting power. Hence it can be said that for any decision to be taken by GST Council the consent of Union Government is must.

EXEMPTION LIMIT – IF ANY?

It is expected that manufacturers with turnover less than Rs. 150 lakhs per annum will be exempted from CGST and IGST (on optional basis).

Dealers with turnover up to 10 lakhs per annum will be exempted from all three i.e. SGST, CGST and IGST.

FINAL REMARKS

Although the proposed GST is not a perfect GST but considering the present situation of the country and the multiple limitations, the proposed GST structure can be said to be best designed.

One thing is sure that the proposed GST regime of

taxation is surely going to be much better than the

current mode of taxation. Most important is,

proposed GST is expected to reduce the cascading

effect of taxes and this will in turn make us more

competent in the global business world.

AP Institute For Training and Learning Pvt Ltd 14

2.0 News & Updates

New GST can remove a lot of wastage: Kaushik Basu, chief economist of World Bank

Kaushik Basu, senior vice president and chief economist of the World Bank, has first-hand experience working in North Block having served as India's chief economic advisor from 2009 to 2012. His forthcoming book, An Economist in the Real World, is based on a ringside view of those India days. As the bank's chief economist, Basu closely follows Indian economic policies, ET interviewed him in Washington.

What do you think of India's new GDP figures? Do you find them believable?

Contrary to what some critics have said, India's new GDP figures are better and more reliable. They capture the value added in the manufacturing sector more comprehensively than in the past and, as such, provide better data. This is not to deny that, as with all macroeconomic indices, there is a margin of error. But data collection and collation in India is a sufficiently transparent exercise that makes deliberate data manipulation extremely unlikely.

The Modi government is concerned about India's ranking (142nd among 189 countries) in the World Bank's Ease of Doing Business index. It claims the examples used by the bank are skewed against India. What is your response?

The World Bank's Doing Business indicator uses the same yardstick to evaluate 189 countries. Using the same yardstick is the fair thing to do, but it also creates a straightjacket. This is unavoidable in multi-country studies. What is important is that it does give useful information about the business ethos of a nation. Anyone who knows India knows of the large transactions costs for doing business. Hence, there is no surprise that India does poorly on this ranking. It is good to see the Indian government wanting to change this. Cutting down bureaucratic costs is one measure that can singlehandedly boost India's growth. I should emphasise that no modern economy can run efficiently without regulation. Hence, a good business ethos does not mean an absence of regulation but a regulatory system that is transparent and quick.

Are the rankings based on surveys of actual businessmen? Also, is the bank randomising the information?

The data for Doing Business are not collected through statistical samples or randomisation methods. This in itself is not a problem because the bulk of it pertains to the actual law. What are the de jure requirements to start a business, have a contract enforced, get electricity connection and so on? There are limitations to this method and we are trying to make improvements. We instituted several changes last year and there is more to come. The data used to be collected from one city in each country. We have now added a second city for all countries with more than 100 million population. I would love to expand this further, but data collection is a very expensive activity. In valuing the ease of getting electricity, the focus used to be entirely on the cumbersomeness of getting a connection for a small new enterprise. We now also look at the regularity and dependability of the supply.

Do you think this ranking is a powerful tool, which encourages countries to improve, or does it end up being an exercise in naming and shaming?

It is a powerful tool, with the risk that countries at times try to game the system and make changes only in the areas tracked by Doing Business. To a certain extent this is unavoidable. American universities do the same to improve their rankings. But the right thing to do is to take the spirit of this exercise and use it to improve the efficiency of government bureaucracy, whether that improves your rank.

In your opinion what are the three or four top reforms India needs most urgently?

Governments need to focus attention on providing better infrastructure and basic welfare — food, health services, education — to the poor. For both these, attention has to be paid to the details of fiscal policy. India's tax GDP ratio is too low. Even a two or three percentage point increase in this can do wonders in terms of better roads, better toilet facilities, electricity connectivity for all and the provision of basic services to the poor. On the economic policy front, if these can be delivered, the rest will follow automatically. There is enough enterprise and creativity in India. It is good to see government taking initiatives on many of these fronts. The last Budget saw some important moves for which the finance minister deserves credit. Take the proposed Goods and Services Tax (GST). Our analysis shows that when freight moves by truck from one Indian city to another, 60% of the time is spent stationary, and the bulk of this occurs at check posts to pay various taxes and do paperwork. This

AP Institute For Training and Learning Pvt Ltd 15

is a shocking waste. The new GST can remove a lot of such wastage.

There are other initiatives which go beyond economic policy but are important. There must, for instance, be an effort to share prosperity and make India a more inclusive society, where people of different castes and religions, and minority groups and people of different orientations all feel a part of society and sense of belonging to India. This is not just the morally right thing to do; it is something that can nurture creativity and promote development.

Purely in terms of growth, India has done well over the last decade. Earlier this year, the World Bank, for the first time, predicted that India would actually be leading the growth chart among all major economies in the world, including China. The forecast, while based on large data analysis, was nevertheless made with some trepidation. In the first quarter of this year, India did actually grow faster than China, and the forecast seems headed to being right. China has done phenomenally well for three decades. With reforms and inclusive policies, India could do the same.

Which of the programmes that India is implementing to reduce poverty is the most efficient? In this context, will Aadhaar help?

It is the government's responsibility to provide certain basic amenities, such as healthcare, education and essential food to the disadvantaged. Aadhaar can be a game-changer. It facilitates delivery of benefits to the poor directly, often by simply enhancing their buying power. It will also mean that you don't have to remain in your village to get the benefits you are entitled to. Wherever you go you can establish your identity and be fully functional. This can empower workers and help make India a more dynamic economy.

How can India cushion itself from disruption resulting from advanced countries exiting quantitative easing?

This is a risk that all emerging economies face. It is a part of globalisation. I am not suggesting we should resist globalisation. Indeed, I believe globalisation provides huge opportunities. India should welcome it and at the same time build resilience. It is a testimony to India's growing economic might that it has overall weathered global turbulence well. But it needs to do more. One mistake India made, in retrospect, was not to build larger foreign exchange

reserves over the last few years. The reserves rose sharply from 1993 to around 2008 but then flattened out. This was a mistake. India should try to build reserves, at least as long as other countries do. This will boost exports and make the economy more resilient to global shocks. The Reserve Bank has made some deft moves along these lines in recent times and that is welcome.

How does the World Bank look at the BRICS Bank and the resultant competition in mediating global capital to developing country infrastructure?

The World Bank has grown since 1944 but global financial needs have grown much more. Hence, the arrival of the new banks is welcome. They should join us in providing more resources to where they are needed.

How should India deal with the two looming trade pacts led by the US neither of which includes India? These two pacts are both geopolitical and economic moves. India says these are protectionist.

I have studied the Trans-Pacific Partnership and believe that, on balance, it is a good initiative, even though it has recently run into heavy weather. It is not meant to be a move to build trade barriers against other countries but an attempt to remove trade barriers among the 12 or so nations involved. If this strengthens these nations and boosts their demand, that will be good for India. This is not to deny that there are some matters of detail which are of concern, such as the effort to put up barriers against generic drugs. This can hurt India, and hurt ordinary citizens of the nations in the Partnership even more. Such clauses should be resisted. But, overall, the agreement is not a matter of concern for India.

Open to amendments in future once GST bill is passed: Rajnath

With the Congress and Left opposing the Goods and Services Tax constitutional amendment, Home Minister Rajnath Singh on Sunday appealed to all parties to lend support to the proposed legislation for its passage in Parliament, saying the government will be open to amendments.

Singh added the government was trying its best to pass the Bill but due to continuous disruption of the House by the opposition, the effort was not successful.

The Bill was passed by the Lok Sabha but the Rajya Sabha is yet to pass it due to opposition from the

AP Institute For Training and Learning Pvt Ltd 16

Congress, Left parties and AIADMK, which want changes. Terming retail traders the backbone of the economy, Singh said the government would not allow their interests to be affected by globalisation.

“We were, are and will always be business-friendly.” he said, adding the economies of India and China were providing impetus to the world economy.

That it does not happen,” he said, adding the economies of India and China were providing impetus to the world economy and the NDA government is doing its best to further improve the country's economy. “There was double digit inflation, fiscal deficit, current account deficit. But with your blessings, we can proudly claim that ever since Modi government took over we have managed to rein in all. Our international trade is now 2 trillion dollars. In five years, our trade will reach 5 trillion dollars. We will be successful in making India an economic super power,” he added.

Gujarat High Court refers judges' plot allotment PIL to larger bench

AHMEDABAD: The row over allotment of plots in a posh locality escalated today with the Gujarat High Court referring the matter to a larger bench after framing a set of questions related to its suo motu PIL on the issue.

In an unprecedented move, the High Court had on Monday issued notices to the 27 sitting as well as former judges, including that of the Supreme Court, over allotment of residential plots to these judges by the Gujarat government in Neetibaug Co-operative Housing Society in Sola area here.

The PIL was heard today by the division bench of acting Chief Justice V M Sahai and Justice Mohinder Pal based on letters written by two former High Court judges (K R Vyas and B J Sethna) which were converted into a public interest litigation(PIL).

The letters questioned the manner in which the plots were alloted, citing alleged breach of norms and lack of transparency.

While hearing the PIL today, the judges framed questions on which further hearing would take place by the larger bench.

Some of the key questions raised by the bench are - who among the judges are not alloted plot in the society? whether the allotment is done after the

formation of the co-operative housing society and how can judges be given land on individual basis when a co-operative society is formed ?

Further, the bench asked whether any falsity is done in giving land at such premium places and whether any advertisement is given in media for the sale of such land ?

Other questions include - whether a judge alloted the plot in the society is having his own house within 8 kms periphery and if it amounts to breach of any law.

The bench also asked whether the sale deed of the society has incurred loss to the state ex-chequer or not ?

During the hearing today, Advocate General Kamal Trivedi and several lawyers of the respondents raised strong objection to High Court's stand on the matter. They pleaded that when the division bench has already decided to refer the matter to the larger bench, then there is no need to enlist these questions.

Govt makes last-ditch attempt to clear Bill on GST in monsoon session

In a move replete with political implications, the National Democratic Alliance (NDA) government late on Monday listed the Goods and Services Tax (GST) Constitutional Amendment Bill, 2014, for consideration and passing in the Rajya Sabha on Tuesday. The Congress, however, stuck to its position that it would not let the House transact any business, except supplementary demand for grants, till External Affairs Minister Sushma Swaraj and two chief ministers resigned.

Earlier on Monday, stock market investors turned jittery over progress on key reform legislation, including GST. The BSE benchmark Sensex declined 135 points from its previous close to end the day at 28,101.72, amid fears that key reform Bills might not get cleared in the ongoing monsoon session of Parliament.

With only three days before the monsoon session ends, the Bharatiya Janata Party (BJP) indicated its seriousness towards the Bill by issuing a whip to all its Rajya Sabha members to be present in the House on Tuesday. The Congress, meanwhile, dropped no hint that it might relent on its "no resignation, no House" stand and allow the Bill to be discussed and passed.

AP Institute For Training and Learning Pvt Ltd 17

However, the government appeared to have been emboldened on Monday, with the Congress, whose protests in the past two weeks have led to a near-washout of the session, receiving a tongue-lashing from Samajwadi Party chief Mulayam Singh Yadav in the Lok Sabha.

Yadav asked the Congress to spell out its stand clearly.

Similarly, Janata Dal (United) chief Sharad Yadav and SP MPs in the Rajya Sabha broke ranks with the Congress, and blamed Finance Minister Arun Jaitley of not working hard enough to break the parliamentary impasse.

Some ministers in the government saw the silver lining in these developments and put in place the plan to push the GST Bill.

Both in the Rajya Sabha and outside, Jaitley said the two Houses were not functioning because of the "obstinacy" of "two leaders" of the Congress. He said Swaraj was willing to again make a statement on the Lalit Modi issue, but alleged the Congress' demand for her resignation was a "pretext"; the "real motive" was to stall the GST Bill.

Also, Environment & Forests Minister Prakash Javadekar held a media briefing at BJP headquarters. He asked the Congress if it also considered the allegations made by former Indian Premier League commissioner Lalit Modi against Congress President Sonia Gandhi, Vice-President Rahul Gandhi and his sister Priyanka Gandhi Vadra.

Meanwhile, Congress senior leader and whip in the Rajya Sabha, Satyavrat Chaturvedi, told Business Standard: "We have made it clear to the government that we can allow only formal financial business, such as supplementary grants, to be taken up in the House. Apart from that, there is no question of any other legislative business, including the GST Bill, being taken up."

Ghulam Nabi Azad, as well as other Congress leaders, clearly said on the floor of the Rajya Sabha that the government could not blame the Opposition for the impasse. "There has been no serious effort from the government to resolve the impasse; it has rather been arrogant," Azad said.

The government's move to list the GST Bill on Monday could potentially put the Congress on the mat. If the latter chooses to continue obstructing functioning of the House, it could be labelled opposing the government's reformist agenda. However, implementation of GST requires constitutional amendment, so the members of Parliament will have to vote by pressing buttons under an electronic system - a complicated method difficult to execute if the House is not in order.

At present, the Congress has 68 MPs; the Left parties, which support the Congress, have 10; and the All-India Anna Dravida Kazhagam (AIADMK), which is opposed to GST, has 11. Last week, Prime Minister Narendra Modi had visited Tamil Nadu Chief Minister and AIADMK chief J Jayalalithaa to win her support for the Bill. If the Congress, the Left parties and AIADMK vote against the Bill, the legislation would fall by seven votes in the House of 245 members. A constitutional amendment needs two-thirds of votes in favour, in a House that has the attendance of at least half the members.

The government has also mooted the idea of calling a special Parliament session to pass the GST Bill. Earlier, after the Lok Sabha passed the Bill, the Rajya Sabha sent it to a select committee. Now, if the Rajya Sabha passes it, with the select committee's recommendations, the Bill will need to be sent back to the Lok Sabha for passage.

After several deadlines were missed during the previous government's term, the current is hoping to implement the indirect tax reform from April 1, 2016. K M Mani, chairman of the empowered committee of states finance ministers on GST, remains hopeful that the present deadline will be met. "Most states are on board for the GST rollout," he said. On the sidelines of an event, Revenue Secretary Shaktikanta Das also said on Monday: "We are taking all measures required to implement GST from April 1, 2016."

SC stays HC order upholding tax on legal services to firms

The Supreme Court on Monday stayed the Bombay High Court’s judgment that upheld the levy of service tax on services provided by lawyers and law firms to business clients with turnover of Rs 10 lakh and more.

A bench headed by Chief Justice HL Dattu while issuing notice to the ministry of finance, the Director General of Service Tax, Central Board of Excise and Customs, and others stayed the HC

AP Institute For Training and Learning Pvt Ltd 18

judgment on the petition filed by the Bombay Bar Association challenging the levy of service tax on lawyers, which was imposed with effect from May 1, 2011, and was changed to reverse charge (obligation was shifted to business entities from July 1, 2012). The issue pertains to the 14-month period between May 1, 2011, and July 1, 2012.

Business entities with a turnover of Rs 10 lakh or more were asked to pay service tax and also deposit the same against the legal fees paid to individual lawyers or law firms. Smaller business entities and individuals did not have to pay service tax when they hire lawyers or law firms. The current rate of service tax is 14%. Various other HCs had stayed the levy of tax on services provided by lawyers and law firms to business clients.

The association in its petition before the SC stated that such levy will impede the ability of litigants to have access to the system of administration and delivery of justice. “The relationship between an advocate and a litigant before the court of law is not that of a service provider and service recipient but that of a representative of a litigant,” it said, adding that the tax provision is unconstitutional because it discriminates between services provided to an individual (where there is no service tax imposition) and to a large business entity which has to bear the service tax burden.

The HC while dismissing petitions filed by the Bombay Bar Association, Advocates Association of Western India and a few lawyers had referred to the changing role of the legal profession and held that it is no longer limited to appearing before the court.

The HC observed that the legislature in introducing service tax on the legal profession had noted the commercialisation of the practice of law which has expanded in scope and sphere post liberalisation and globalization. “Rather by a rational and intelligible differentiation the Parliament has proceeded to levy and impose service tax on legal services rendered to business entities by an individual advocate or law firm,” the HC stated in its December 15 judgment last year.

SC stays Gujarat HC order on judges' plot allotment PIL

The Supreme Court today stayed the Gujarat High Court order issuing notices to its sitting and former judges and also a sitting apex court judge over the allotment of residential plots to them by the state government in a posh locality in Sola area in Ahmedabad.

"The high court was in mortal hurry. This should not have happened. Let the order be stayed. Let us see what can be done," a Bench headed by Chief Justice H L Dattu said.

The high court had yesterday also referred the matter to a larger Bench after framing a set of questions related to its suo motu PIL on the issue.

The apex court Bench also comprising Justices P C Ghose and C Nagappan issued notices to the Gujarat government, judges cooperative society and Registrar of the High Court, seeking their response within four weeks on a petition challenging the high court order.

The apex court also allowed deletion of names of sitting and former judges who were made respondents in the PIL and were issued notices.

The petition challenging the high court order was filed by one of the retired high court judges for whom senior advocate Harish Salve appeared and sought urgent intervention.

Salve questioned the hurry shown by the high court in entertaining a letter by turning it into PIL over allotment of plots which was made several years ago.

"It is not good," said Salve while assailing the high court order.

The apex court also allowed Gujarat High Court Bar Association to be impleaded as party in a petition before it.

AP Institute For Training and Learning Pvt Ltd 19

3.0 Case Laws 1. M/s HABASIT LAKOKA PVT LTD Vs COMMISSIONER OF CENTRAL EXCISE, COIMBATORE

2015-TIOL-1655-CESTAT-MAD Central Excise - CENVAT credit - Appellants are manufacturers of ‘Transmission & Conveyor Belts', having Unit-I and Unit-II located in the same town and availing cenvat credit on inputs and on capital goods - interest demand on the credit amount availed and reversed on the inputs cleared as such to Unit-I during the material period was raised on Unit-II - recovery of interest with penalty under Rules 14 & 15 of CCR 2004 adjudicated, upheld by Commissioner (Appeals), and agitated herein. Held: The impugned clearance of inputs amounts to inter-unit transfer of inputs and it is not the case of the department that appellant's Unit-II has utilized the credit - The Principal Bench rulings in the case of Kesarwani Zarda Bhandar and Sona Koyo Steering Systems are squarely applicable to the facts of the present case - High Court of Delhi in the case of Kwality Ice Cream Company also held that demand of interest raised after three years is hit by limitation - appellants are not liable for demand of interest and penalty; impugned order set aside. 2. Mirc Electronics Ltd. vs. Commissioner of Central Excise, Thane-I

[2015] 59 taxmann.com 360 (Mumbai - CESTAT) Goods imported for trading couldn't be treated as exempted goods for reversal of credit under rule 6(3). Exempted goods have to be excisable goods; hence, imported goods, which are traded, cannot be considered as exempted goods and rule 6 of CENVAT Credit rules, 2004 would not apply thereto 3. Commissioner of Central Excise, Aurangabad vs. Rudra Galaxy Channel Ltd.

[2015] 59 taxmann.com 255 (Mumbai - CESTAT) Cum-tax benefit can be granted only if assessee shows that receipts are cum-tax. In absence of documentary evidence to show that amount received by assessee was cum-tax, cum-tax benefit cannot be granted. Discretion is available to authority to levy penalty only within minimum value and maximum value specified in law; there is no discretion to reduce penalty below minimum specified in law 4. RELIANCE COMMUNICATIONS LTD Vs. UNION OF INDIA AND ORS

2015-TIOL-1750-HC-MUM-CUS When Court issues directions to authority to decide petitioner's application by particular date, it expects authority to take a decision - DGFT to pay costs of Rs ONE lakh: HC.

5. EAGLE CORPORATION PVT LTD AND 1 Vs. UNION OF INDIA AND 4

2015-TIOL-1743-HC-AHM-ST Order of Settlement Commission challenged on ground that main contractor had paid Service Tax - Settlement Commission has rightly held that petitioner cannot be said to be subcontractor - Petition dismissed 6. UNION OF INDIA AND ORS Vs M/s KARVY STOCK BROKING LTD

2015-TIOL-170-SC-ST Service Tax - Business Auxilary Services - Quashing of Board Circular upheld : Board's Circular dated 5.11.2003 clarified that the commission received by the distributor on mutual fund distribution is liable to service tax under the category of Business Auxiliary services and exemption under notification is not available - High Court held Circular to be illegal and contrary to the proviso to Section 37B (a) of the Central Excise Act, 1994 since it takes away the benefit given by an exemption notification - The circular was quashed. Held : This circular dated 05.11.2003 has been set aside by the High Court in the impugned judgment on the ground that it amounts to foreclosing discretion or judgment that may be exercised by the quasi judicial authority while deciding a particular lis under particular circumstances. The High Court referred to the proviso to Section 37B of the Central Excise Act, 1944, which categorically states that such kind of circulars cannot be issued. No error in the impugned judgment. 7. M/s KHICHA INDUSTRIES Vs COMMISSIONER OF CENTRAL EXCISE -JAIPUR-II

2015-TIOL-1606-CESTAT-DEL Assessee engaged in grinding of rock phosphate - "subject" of contract is "contract for grinding of rock phosphate from which it is evident that contract was not for cargo handling and work other than grinding of rock phosphate was incidental or ancillary to main work of grinding - Payment rates were composite rates not amenable to identification as to what rate/amount was paid to those components of services which were arguably in nature of cargo handling service - When quantification is not possible, the levy fails - From 10.09.2004, assessee has been paying ST on entire consideration received under BAS on account of fact that "production of goods on behalf of the client" was added to definition of BAS from said date - Entire demand pertains to period beyond normal period of one year from date of SCN - Adjudicating Authority himself has recorded that case involved interpretation of law and on that ground extending benefit of Section 80 ibid did not impose any

AP Institute For Training and Learning Pvt Ltd 20

penalties at all - Impugned demand is set aside on merit as well as on ground of time-bar 8. AKME PROJECTS LTD Vs COMMISSIONER OF SERVICE TAX, BANGALORE

2015-TIOL-1605-CESTAT-BANG Service Tax - Construction of flats - Service tax collected but not paid to government alleged - Original adjudicating authority dropped the demand and rendered a detailed analysis and concluded on basis of documentary evidence that there was no correlation between the service tax amount shown in the price list given to prospective customers and actual cost of the flat - Further more concluded that the appellant had neither charged service tax nor collected the same but merely obtained indemnity letters from purchasers undertaking to reimburse the service tax - Commissioner (A) without adverting to any discussion mechanically upheld the demand based on price list - Impugned order deserves to be set aside - Appeal allowed with consequential relief. 9 NRB BEARING LTD Vs COMMISSIONER OF CENTRAL EXCISE, MUMBAI

2015-TIOL-1610-CESTAT-MUM s.35F, s.35C(2A) of CEA, 1944 - Any stay order passed by the Tribunal, if it is in force beyond 07.08.2014, it would continue till the disposal of the appeal and there is no need for filing any further applications for extension - Tribunal decision inVenketeshwara Filaments - 2014-TIOL-2388-CESTAT-AHM followed - Application allowed: 10. COMMISSIONER OF CENTRAL EXCISE-AHMEDABAD-III Vs M/s NIRMA LTD