Construction of Jones Lang LaSalle Prime and Secondary Index Nasima Ahmed Senior Analyst EMEA...

19

Construction of Jones Lang LaSalle Prime and Secondary Index Nasima Ahmed Senior Analyst EMEA Capital Market Research 24 th June 2010

-

Upload

joshua-francis -

Category

Documents

-

view

226 -

download

0

Transcript of Construction of Jones Lang LaSalle Prime and Secondary Index Nasima Ahmed Senior Analyst EMEA...

Construction of Jones Lang LaSalle Prime and Secondary Index

Nasima AhmedSenior Analyst EMEA Capital Market Research

24th June 2010

2

Agenda

Why?

Definition

Methodology

Health Warnings

Results

Conclusion

3

Why?

Create the first Jones Lang LaSalle Prime and Secondary Index

Limited work done so far, thus need for more academic work in this field

Address the issues of over representation of certain sectors in the existing Jones Lang LaSalle “Growth” and “Value” Index

4

Definition….

“Prime” asset is one which is located in the best position, is new and well designed, is of a lot size popular with investors and is

freehold with no restrictive covenants and is let to a sound covenant on a long term lease. All these factors are reflected in the yield of the property, thus “Prime” assets are low yielding property because it has the potential of future capital and rental growth

A “Secondary” asset is characterised by high yields, largely reflecting the location, covenant strength and the age of the property

5

Methodology

6

Sample size 913 properties

Sectors – Office, Retail and Industrial

Two approaches:

- Equivalent yield quartiles

- Capital value quartiles

In order to exclude “hybrid properties” the middle quartile was ignored

Only the “super prime” and “super secondary” (properties which remained in the lower and upper quartiles over the period studied 1996 to 2008) assets were included

Methodology

25th percentile

Lower quartile

50th percentile Middle quartile

Upper quartile 75th percentile

7

Methodology

Total Return:

Capital value growth: The compounded increase in quarterly values, net of capital expenditure, expressed as a percentage of the capital employed each quarter.

Income Return: The net income receivable for the quarter expressed as a percentage of the capital employed over the quarter.

Estimated rental value: The increase in the estimated rental value of properties held throughout the measurement period, expressed as a percentage of the rental value at the beginning of the period.

Initial yield: The rent passing (net of ground rent) as a percentage of the capital value at the same date.

Equivalent yield: Estimation of the discount rate which equates the future income flows to the current capital value.

1

1

t

tttt Value

IncomeValueValuer

8

Health Warnings

Data -Lag in valuation

-Issue of serial correlation

-How representative is the sample

Methodology

-Issues concerning management expenses and depreciation

9

Results

10

Source: Jones Lang LaSalle

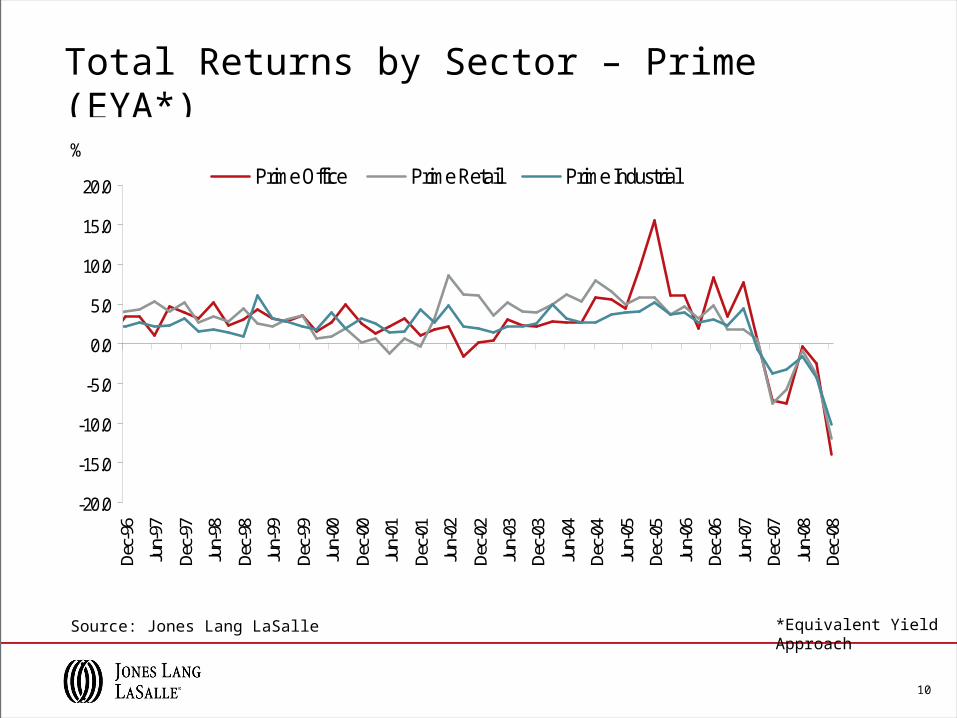

Total Returns by Sector – Prime (EYA*)

*Equivalent Yield Approach

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Dec-

96

Jun-

97

Dec-

97

Jun-

98

Dec-

98

Jun-

99

Dec-

99

Jun-

00

Dec-

00

Jun-

01

Dec-

01

Jun-

02

Dec-

02

Jun-

03

Dec-

03

Jun-

04

Dec-

04

Jun-

05

Dec-

05

Jun-

06

Dec-

06

Jun-

07

Dec-

07

Jun-

08

Dec-

08

%Prime Office Prime Retail Prime Industrial

11

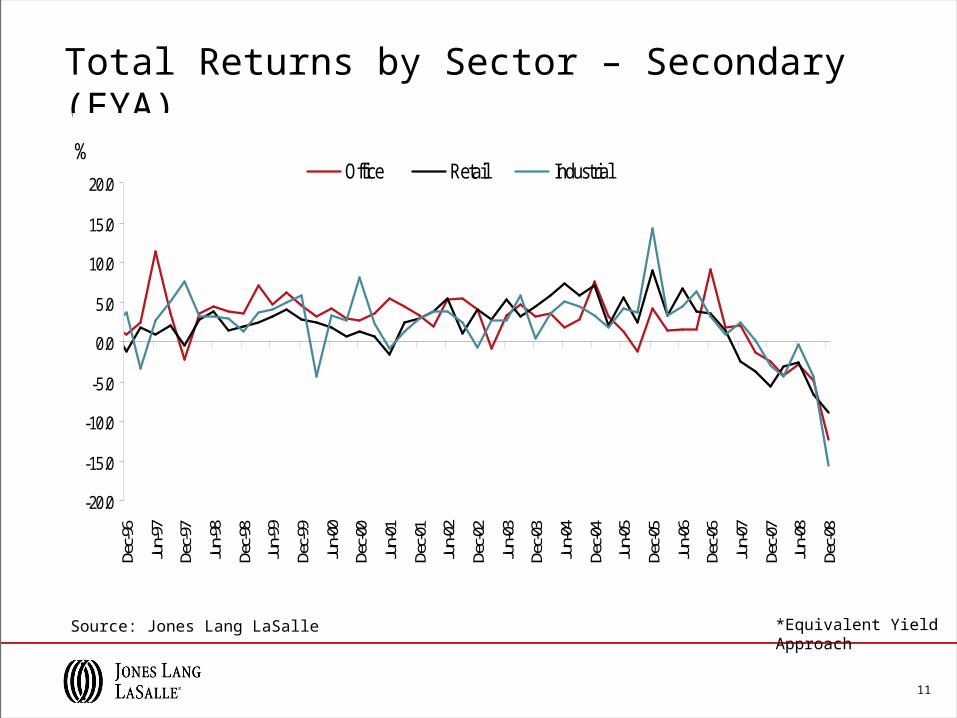

Total Returns by Sector – Secondary (EYA)

Source: Jones Lang LaSalle *Equivalent Yield Approach

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Dec-9

6

Jun-

97

Dec-9

7

Jun-

98

Dec-9

8

Jun-

99

Dec-9

9

Jun-

00

Dec-0

0

Jun-

01

Dec-0

1

Jun-

02

Dec-0

2

Jun-

03

Dec-0

3

Jun-

04

Dec-0

4

Jun-

05

Dec-0

5

Jun-

06

Dec-0

6

Jun-

07

Dec-0

7

Jun-

08

Dec-0

8

%Office Retail Industrial

12

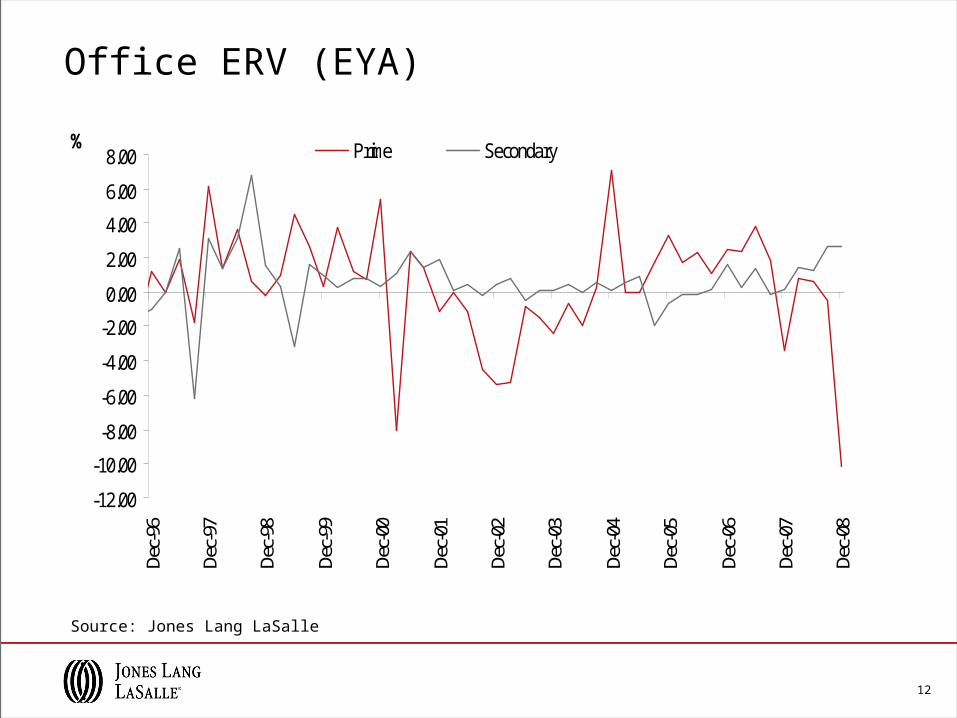

Office ERV (EYA)

Source: Jones Lang LaSalle

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00De

c-96

Dec-

97

Dec-

98

Dec-

99

Dec-

00

Dec-

01

Dec-

02

Dec-

03

Dec-

04

Dec-

05

Dec-

06

Dec-

07

Dec-

08

% Prime Secondary

13

Total Returns by Sector – Prime (CVA)

Source: Jones Lang LaSalle *Capital Value Approach

-15.0

-10.0

-5.0

0.0

5.0

10.0

Dec-

96

Jun-

97De

c-97

Jun-

98

Dec-

98

Jun-

99

Dec-

99Ju

n-00

Dec-

00

Jun-

01

Dec-

01

Jun-

02

Dec-

02Ju

n-03

Dec-

03

Jun-

04

Dec-

04

Jun-

05De

c-05

Jun-

06

Dec-

06

Jun-

07

Dec-

07Ju

n-08

Dec-

08

% Office Retail Industrial

14

Total Returns by Sector – Secondary (CVA)

Source: Jones Lang LaSalle *Capital Value Approach

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

Dec-

96Ju

n-97

Dec-

97Ju

n-98

Dec-

98Ju

n-99

Dec-

99Ju

n-00

Dec-

00Ju

n-01

Dec-

01Ju

n-02

Dec-

02Ju

n-03

Dec-

03Ju

n-04

Dec-

04Ju

n-05

Dec-

05Ju

n-06

Dec-

06Ju

n-07

Dec-

07Ju

n-08

Dec-

08

% Office Retail Industry

15

IPD and JLL Prime and Secondary Index

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Mar-0

1

Mar-0

2

Mar-0

3

Mar-0

4

Mar-0

5

Mar-0

6

Mar-0

7

Mar-0

8

% Prime Secondary IPD Low Yield IPD High Yield

Office Total Returns – (EYA) Office Total Returns – (CVA)

-15.0

-10.0

-5.0

0.0

5.0

10.0

Mar-0

1

Mar-0

2

Mar-0

3

Mar-0

4

Mar-0

5

Mar-0

6

Mar-0

7

Mar-0

8

%Prime Secondary

IPD Low Yield IPD High Yield

Source: Jones Lang LaSalle, IPD

16

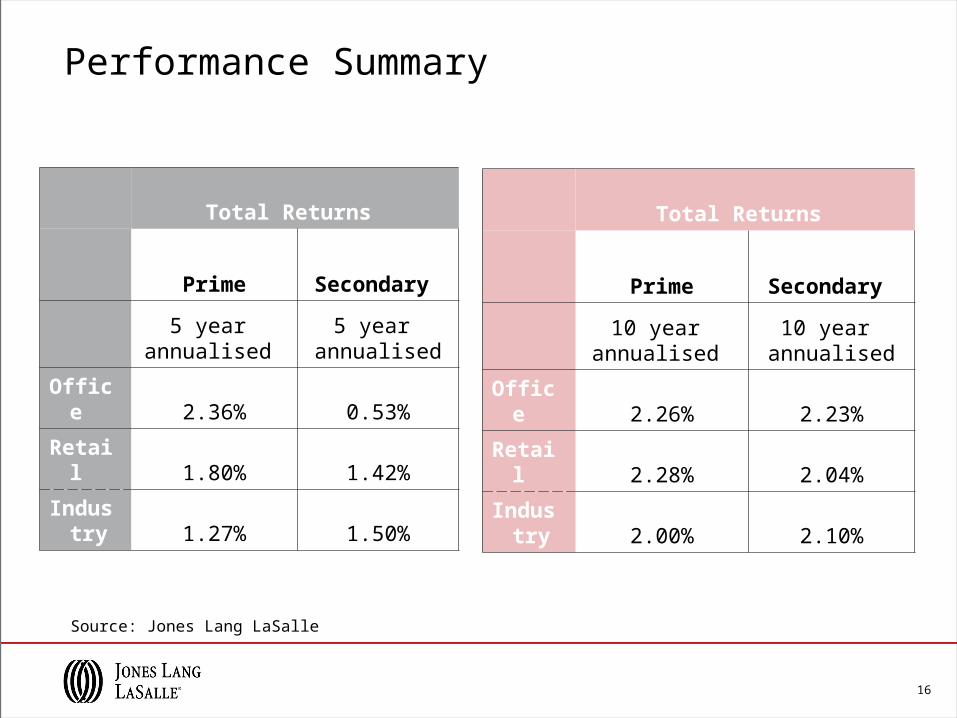

Performance Summary

Total Returns

Prime Secondary

5 year annualised

5 year annualised

Office 2.36% 0.53%

Retail 1.80% 1.42%

Industry 1.27% 1.50%

Total Returns

Prime Secondary

10 year annualised

10 year annualised

Office 2.26% 2.23%

Retail 2.28% 2.04%

Industry 2.00% 2.10%

Source: Jones Lang LaSalle

17

Conclusion

Two approaches :

The equivalent yield approach: More comparable with IPD upper and lower quartile Accurately demonstrated the market cyclical trends across all the sectors

The Capital Value Approach: Limitation given that it is a lot size measure – e.g. a big block of secondary office can be

classified as prime Does not capture the market cyclical trends across all three sectors

Sector Performance: Office sector: Secondary properties outperformed in the boom years and underperform

in down cycle Retail sector: Followed a similar trend to the office sector from 2007 onwards with prime

assets outperforming in boom years and underperforming in down cycle Industrial sector: showed similar trends to the office sector

18

Recommendation

Alternative approaches:

Conduct similar analysis using Initial Yield and Reversionary Yield Split sample by the qualitative property characteristics of prime and

secondary

Methodology : Conduct tests to incorporate some of the “Hybrid” properties to the sample? The assumption to exclude properties showing +50%/-50% was that the best

approach to take? When calculating returns additional costs such as management costs,

depreciation should be included.

19

Thank you

Nasima AhmedSenior AnalystEMEA Capital Market ResearchTel: +44 (0)20 3147 1211 Fax: +44 (0)20 3147 1730 email: [email protected]