Constructing HRA: Blueprints for Solid Administration

45

-

Upload

benefitexpress -

Category

Recruiting & HR

-

view

481 -

download

0

Transcript of Constructing HRA: Blueprints for Solid Administration

Constructing HRA:Blueprints for Solid Administration

Larry Grudzien

Attorney at Law

3

The following important features will discussed:

• Which employees may participate?

• What expenses can be reimbursed?

• What ERISA requirements apply?

• What types of contributions are possible?

• What amount of contributions are possible?

• When are withdrawals possible?

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Agenda

4

• Provided in Rev. Ruling 2002-41 and IRS Notice 2002-45

• Considered an employer sponsored self-funded health and welfare plan subject to Code §105(h) and ERISA

• Financed by the employer’s (no pre-tax salary reduction contributions) contributions

• Allowed to carry over any unused balances

• Passage of ACA affected what items could be reimbursed after 2013

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What is an HRA?

5

• Employer controls what medical expenses are reimbursed

• Employer controls the amount of the reimbursement each year

• HRAs can be used to provide retiree medical benefits

• Employer can reimburse premiums or just expenses

• Employees can lose right to receive reimbursement once they leave employment unless they elect COBRA

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Why would an employer consider establishing an HRA?

6

• Plan Document

• Enrollment form

• Summary Plan Description (SPD)

• Expense Reimbursement Form

• Form 5500, if required

• Summary of Benefits and Coverage

• Summary Annual Report (if required to file Form 5500)

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What documents are needed to establish them?

7

• To reimburse medial expenses or premiums, the HRA must be integrated with a group health plan an insured health plan.

• An employer can designate which expenses it will reimburse under the HRA.

• No group health plans is needed for reimbursing dental, vision and retiree expenses or premiums.

• Two integration methods are provided: First method is with a group health plan that does not provide

minimum value

Second method is with group health plan that provides minimum value

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Does an HRA have to be used with a group health plan?

8

• For expenses or premiums to be reimbursed, dependents must be covered by group health plan of the employer or spouse’s employer.

• Employees (and former employees) must be offered the opportunity to permanently opt-out of and waive future reimbursements from the HRA at least annually.

• On termination of employment, the HRA must either be forfeited, or it must allow the employee to permanently opt out and waive future reimbursements.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Does an HRA have to be used with a group health plan?

9

• The employer determines which employees will participate in the plan.

• An employer may exclude any employee as long as the plan passes the nondiscrimination tests of Code §105(h).

• Self-employed individuals, partners and more than 2% shareholders of a S Corporation may not participate.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Who is eligible to make or receive contributions?

10

Yes. HRAs are considered a self-funded welfare plan and must meet all of the ERISA requirements:

• Written plan requirement

• Trust requirement, if HRA is funded

• Claims procedures

• Reporting and Disclosure

• Fiduciary requirements

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Must the ERISA requirements be met?

11

It is possible, provided:

• FSA and HRA cannot reimburse the same medical expense

• If expense can be covered by both, plan must specify that FSA must be exhausted first

• If plan does not specify, HRA must be exhausted first

• Employer may designate only certain expenses can be reimbursed by HRA

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Can an employee participate in a Health FSA in the same month?

12

• No, because HRAs contain only employer contributions.

• Use-it- or-lose rule does not apply.

• Uniform coverage rules does not apply.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Do the Health FSA rules apply to HRAs?

13

• Reimburse participants for medical premiums or expenses up to a maximum dollar amount specified by the employer for any plan year

• Reimburse participants for all eligible medical expenses or only those specified by the employer

• Any contributions to HRA deductible by the employer, and any reimbursements for expenses are not taxable to the employees

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What contributions are permitted & how are they treated for tax purposes?

14

• The Plan can reimburse medical expenses and/or premiums

• Employer can reimburse any medical expense under Code § 213(d) or just those expenses it specifies in the plan

• Can include dental, vision, prescription drug and preventive care expenses

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What expenses can be reimbursed?

15

• No. HRAs are prohibited after 2013

• HRAs of small employers given relief until the end of 2016

• Certain small employers will be allowed under a qualified small employer HRA

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Can HRAs reimburse premiums for individual coverage?

16

• Yes, an employer may allow carryover, but is not required to do so

• Employer may specify the carryover amount and period

• Any amount allowed to be carried over will be considered an expense on the employer’s balance sheet

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Can unused amounts be carried to future years?

17

• Yes, an employer can specify an amount that it will provide for each year of service.

• An employer is not required to fund this amount.• An employee can lose any amount if he or she

leaves before the designated retirement date.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Can HRAs be used to fund retiree medical amounts?

18

• Yes, an employer may specify events in which the employee loses the right to continue to use any amounts set aside in an HRA.

• Employer can provide that amounts will be available after termination of employment or death

• Employee can continue to use HRA if he or she elects COBRA

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Once contributions are made, can they be forfeited?

19

No. The DOL has not required employers to fund contributions that are promised.

They can be paid from the employer’s general assets.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Must benefits be funded?

20

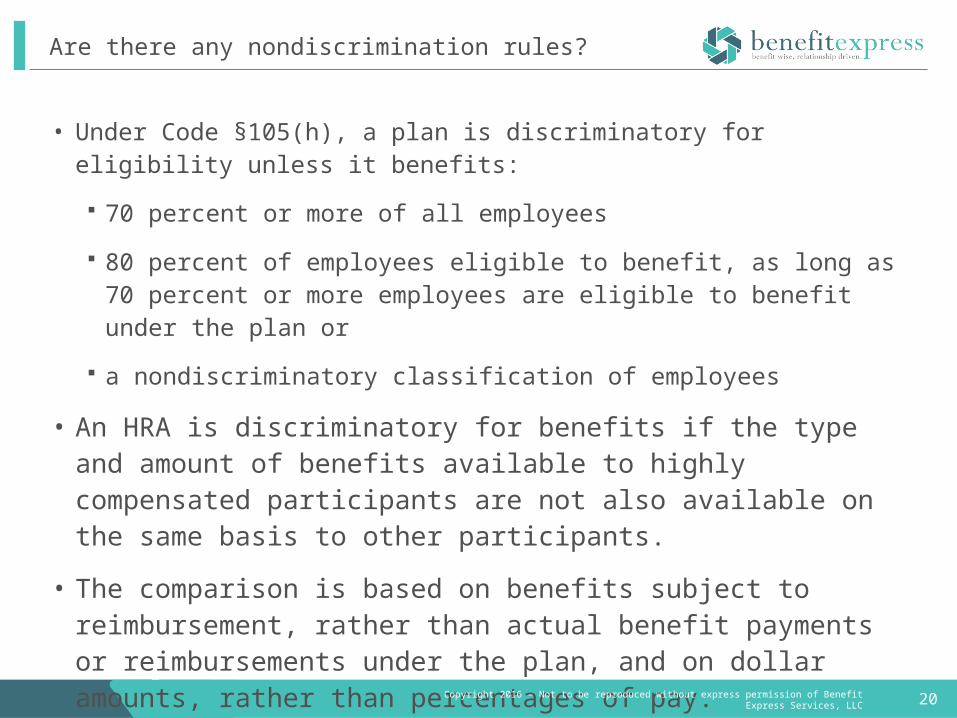

• Under Code §105(h), a plan is discriminatory for eligibility unless it benefits:

70 percent or more of all employees

80 percent of employees eligible to benefit, as long as 70 percent or more employees are eligible to benefit under the plan or

a nondiscriminatory classification of employees

• An HRA is discriminatory for benefits if the type and amount of benefits available to highly compensated participants are not also available on the same basis to other participants.

• The comparison is based on benefits subject to reimbursement, rather than actual benefit payments or reimbursements under the plan, and on dollar amounts, rather than percentages of pay.

• These nondiscrimination rules do not apply to retiree benefits if certain conditions are met.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Are there any nondiscrimination rules?

21

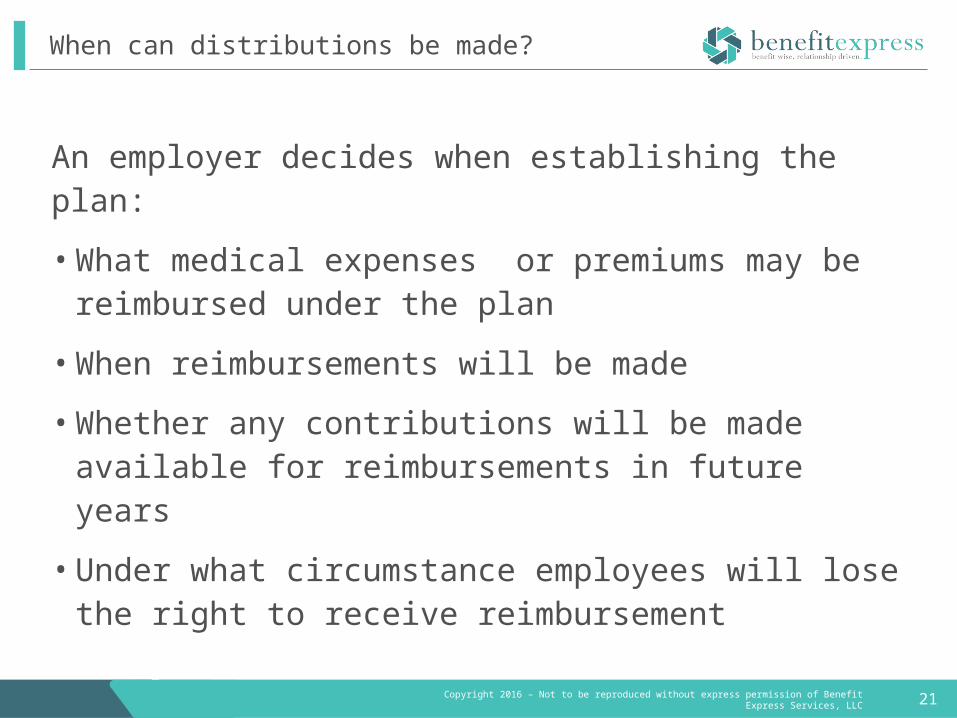

An employer decides when establishing the plan:

• What medical expenses or premiums may be reimbursed under the plan

• When reimbursements will be made

• Whether any contributions will be made available for reimbursements in future years

• Under what circumstance employees will lose the right to receive reimbursement

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

When can distributions be made?

22

The employee submits claims to the employer or to a TPA selected by the employer.

Procedures for submitting claims are similar to procedures under a Health FSA.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Who substantiates if paid for medical expenses?

23

The employer may design a plan to allow a deceased employee’s spouse and other dependents to continue participation in the plan without electing COBRA.

If not, COBRA will be available to spouse and other dependents.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What happens to an individual’s HRA upon his or her death?

24

Yes. An employer may place restrictions on what expenses will be reimbursed, the amount of the reimbursement and when the reimbursement will be made.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

May the employer place any restrictions on withdrawals?

25

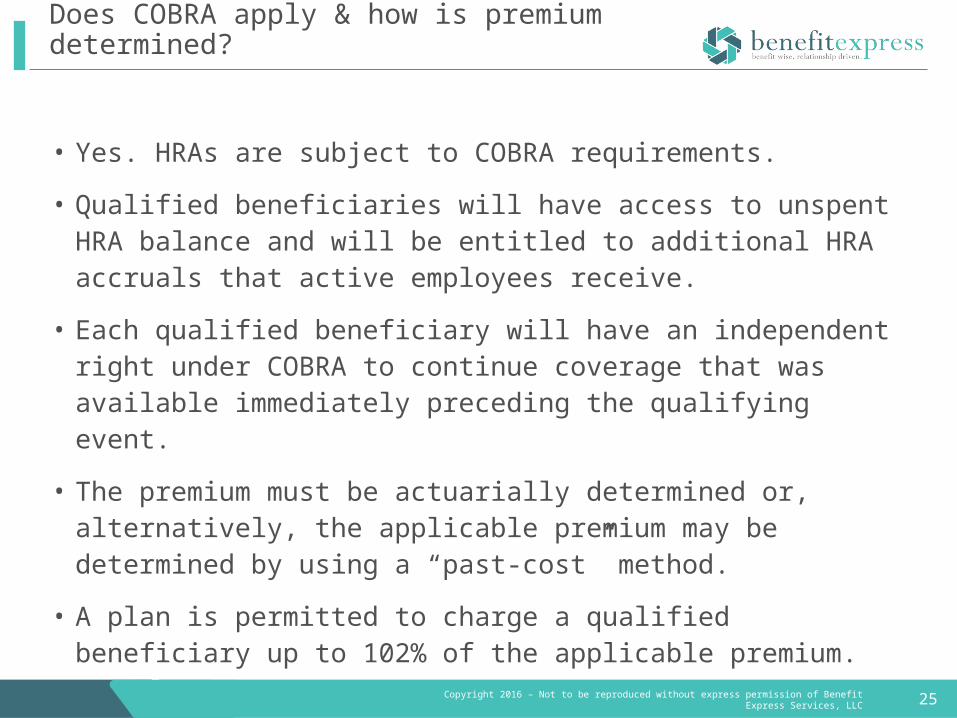

• Yes. HRAs are subject to COBRA requirements.

• Qualified beneficiaries will have access to unspent HRA balance and will be entitled to additional HRA accruals that active employees receive.

• Each qualified beneficiary will have an independent right under COBRA to continue coverage that was available immediately preceding the qualifying event.

• The premium must be actuarially determined or, alternatively, the applicable premium may be determined by using a “past-cost” method.

• A plan is permitted to charge a qualified beneficiary up to 102% of the applicable premium.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Does COBRA apply & how is premium determined?

26

It will depend on whether an employee has to participate in the HRA to participate in the group health plan.

An employer can provide a separate election.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

When electing COBRA, must the employer give a separate election?

27

• An HRA generally will be a group health plan under HIPAA’s portability and administrative simplification rules.

• HRAs generally will be subject to HIPAA’s portability requirements (special enrollment rights, nondiscrimination requirements, and certificate of creditable coverage requirements) and administrative simplification rules (covering privacy, security, and electronic data interchange (EDI)).

• A health plan with fewer than 50 participants that is administered by the employer that established and maintains the plan is excluded from the definition of group health plan.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Does HIPAA apply?

28

• Subject to the ERISA reporting requirements

• Subject Form 5500 requirements- exempt if unfunded and have under 100 participants

• Must provide and Form 1095-C if plan is not integrated with a group health plan of the employer

• Section 111 Reporting -$5,000 or more

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What reporting is required?

29

• Separate SPD

• Separate SBC

• Employees (and former employees) must be offered the opportunity to permanently opt-out of and waive future reimbursements from the HRA at least annually.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

What disclosures are required to participants?

30

• An employer has complete control over: what medical expenses will be reimbursed

what unused amounts will be carried over

for what period of time unused amounts will be carried over

• An employer can decide from year to year what amounts they will contribute.

• HRAs can work with Health FSAs.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Why would an employer participate in an HRA?

31

• ERISA requirements will still apply

• Nondiscrimination requirements apply

• Claim substantiation is still required

• Possible funding issues

• May reduce savings in going to higher deductible health plan

• COBRA application

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Why would an employer not participate in an HRA?

Qualified Small Employer HRA (“QSEHRA”)

Employers may adopt this HRA plan design starting with plan years that begin on or after January 1, 2017.

Effective Date

34

For an employer to qualify to offer this plan design, an employer must:

• Employ less than 50 full time employees and full time equivalent employees (determined in the previous calendar year)

• Not offer a group health plan

• Offer the HRA on the same terms to all eligible employees

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Eligible Employers

35

Employers may design this plan to exclude certain employees from participating.

They are:

• Employees who have not completed 90 days of service

• Part-time (less than 35 hours) and seasonal employees (work less than 9 months)

• Employees under age 25

• Union employees

• Certain non resident aliensCopyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Excludible Employees

36

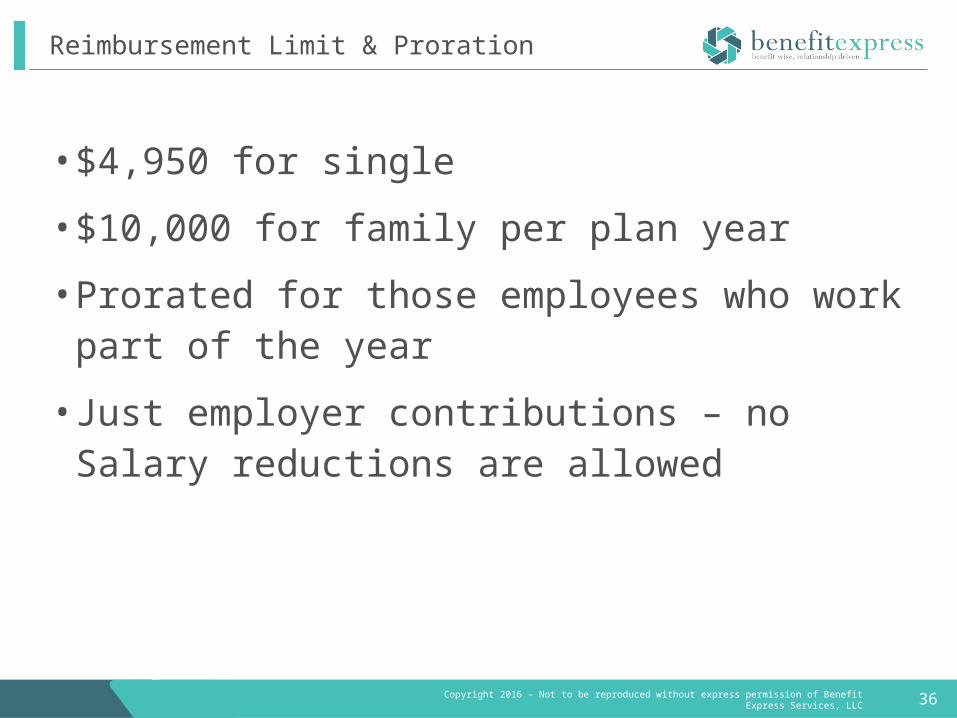

• $4,950 for single

• $10,000 for family per plan year

• Prorated for those employees who work part of the year

• Just employer contributions – no Salary reductions are allowed

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Reimbursement Limit & Proration

37

• The employer can vary the amount of reimbursements available under the arrangement based on age of the eligible employee (and family members if the arrangement covers family members) or the number of family members of the employee covered under the arrangement.

• Any such variation must be made in accordance with the variation in price of an insurance policy in the relevant individual health insurance market.

• For this purpose, any variation must be determined by reference to the same insurance policy with respect to all eligible employees.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Reimbursement Limit & Proration

38

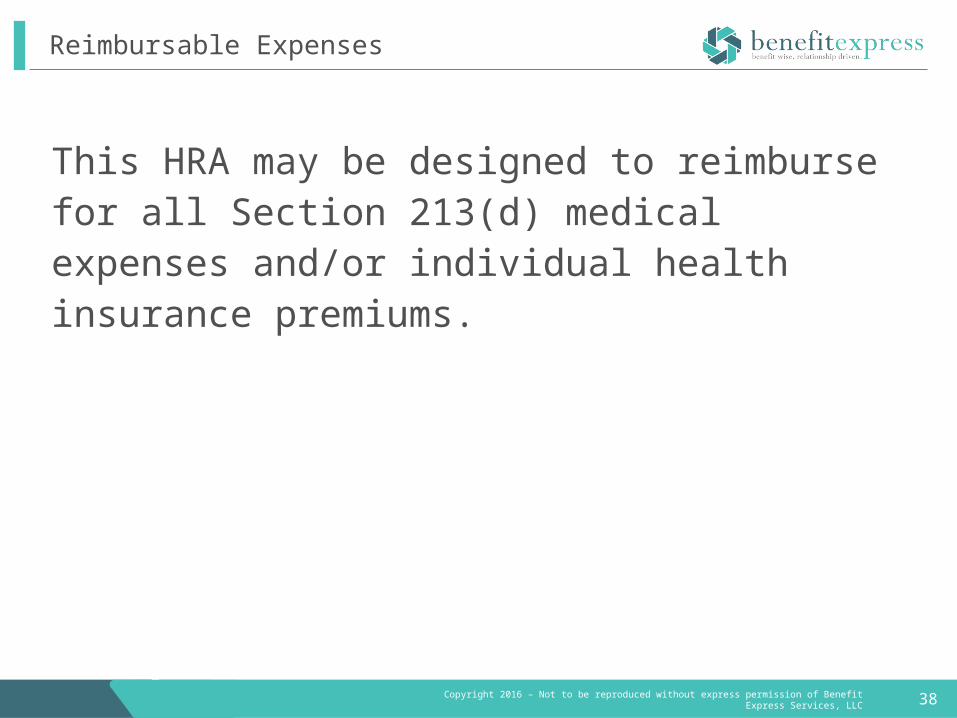

This HRA may be designed to reimburse for all Section 213(d) medical expenses and/or individual health insurance premiums.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Reimbursable Expenses

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC 39

• An employee must show proof that they are covered under a minimum essential health plan when enrolling.

• After enrollment, the employee must provide the following as proof of continued coverage in order to receive tax-free reimbursement: Explanation of Benefits (EOB) for §213(d) medical expenses

Monthly Premium bill for Individual health insurance premium expenses

• Participants may be taxed on their reimbursements if the participant is not covered by their minimum essential coverage for any month during the plan year.

Condition to receive tax-free reimbursements

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC 40

• An employer must provide an annual written notice 90 days in advance of the plan year or the employee’s initial eligibility date.

• This notice must be provided to all eligible employees.

• The notice must:

Contain the amount of HRA benefit available

Instruct employees to provide the amount of HRA benefit available to the public exchange if the employee is applying for a premium tax credit

Warn employees that their reimbursements may be taxable if the employee does not have minimum essential coverage for any month

• Failure to provide this notice can trigger a penalty of $50 per employee, up to $2,500 per year.

Notice Requirement

41

• An employee who is provided this HRA is not eligible for a premium tax credit if this HRA is “affordable.”

• Affordability for this purpose is computed in a manner similar for other employer coverage.

• This HRA is considered affordable for a month if excess of the self-only premium under the second lowest cost silver plan offered in the relevant individual health insurance market over 1/12 of the employee’s permitted benefit under this HRA does not exceed 1/12 of 9.69 percent of the employee’s household income.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Coordination with Premium Tax Credits

42

This HRA’s benefit amount must be reported on the employee’s W-2.

• This HRA is not subject to COBRA.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Other Matters

43

• The requirement that his HRAs be funded by the employer (with no salary reduction contributions), the nondiscrimination rules, and the proof of coverage provision are all part of the definition of this HRA.

• An arrangement that does not satisfy these requirements is not this HRA and will be subject to the ACA market reforms and other requirements applicable to group health plans.

• Thus, an employer that fails to meet the applicable requirements could be subject to the $100 per person per day excise tax or penalty (as applicable).

• Employers adopting this HRA may also be subject to penalties for failing to meet applicable reporting requirements.

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Consequences of Failing Requirements

Questions?

45

Larry GrudzienAttorney at Law

(708) [email protected]

Copyright 2016 – Not to be reproduced without express permission of Benefit Express Services, LLC

Contact Information