Consilium automotive salary survey 2014

20

consilium GROUP consiliumrecruit.com 2014 The Salary Review Automotive

-

Upload

andy-vincent -

Category

Documents

-

view

232 -

download

0

description

Â

Transcript of Consilium automotive salary survey 2014

consiliumGROUP

consiliumrecruit.com

2014

The

Salary Review

Automotive

Russell Tuck - Director, Consilium Group

“

”

The job market for experienced automotive industry professionals has tightened

dramatically. It is therefore vital that companies offer competitive compensation

to attract top talent as well as encourage your best people to stay.

1

Welcome to The Review

Summary of 2013

Demand for Talent 2014

Automotive Technology Trends

The Next 5 Years

Market Insight

Salary Tables

Salary Conversion Guide

Page 2

Page 3

Page 5

Page 6

Page 7

Page 9

Page 10

Page 15

Contents

2

E

UK Automotive - Highlights

stablished in 2001, Consilium has been The automotive industry is the UK’s largest

a trusted recruitment partner to the UK sector in terms of exports, generating around

Automotive industry for over thirteen years. £30bn of annual revenue

This is our annual salary report that presents The sector exports to over 100 countries

the remuneration levels of 125 separate roles worldwide and currently accounts for around

across nine career disciplines, coupled with 11% of total UK exports

recruitment trends anticipated for our sector It also produces trucks, vans, buses, during 2014 and beyond.motorbikes, construction equipment and

The source data is derived from a combination racing cars with eight of the eleven Formula 1

of job seekers disclosure of current salaries, teams based here

advertised vacancy salaries and actual job

offers managed by Consilium over the past 12 The salaries included in this review exclude any

months purely within the Automotive sector. bonuses and benefits packages which can be

found to vary widely, so this publication acts as

a guide to base salaries only.

Consilium operates across a diverse range of

The UK auto industry delivers a £60bn annual automotive organisations throughout the UK;

turnover with a £12bn in net value - added to we are therefore suitably experienced and

the UK economy, contributing 2.3% to GDP qualified to reasonably forecast how

remuneration packages are likely to look in the The sector produced over 1.5 million cars last

coming year.year, the highest level for five years of which

80% were exported The salary guidance is based on the Midlands

region - the heartland of the UK auto industry The UK produces even more engines than

and benchmark for remuneration guidance vehicles - 2.5 million. In fact, a third of all Ford

across the UK.engines worldwide are produced in the UK

However, the salary ranges can be customised 720,000 people employed in the automotive

for each of the UK regions by using the local sector across manufacturing, retail and after

variance calculator - please see simple sales - 140,000 of whom are directly employed

conversion guide on page 15in manufacturing

UK automotive companies currently invest over

£1.5bn a year in R&D combined

Welcome toThe Review

3

T he UK possesses one of the most diverse According to the SMMT, Britain produced 1.51m

and productive automotive sectors in cars in 2013, a 3% rise on 2012 that represents

the world, and on the back of building half a million more than just four years ago. In

more than 1.5m cars last year (the highest line with this resurgence, it is expected that the

production output since 2007), the resurgent UK will overtake France and Spain to become

industry tapped into strong global demand the Europe’s second-largest producer after

and correspondingly increased output, Germany.

investment and ultimately employment levels.The news comes as Nissan, the UK’s biggest

car maker by production announced the

introduction of an additional shift resulting in

round the clock production across the facility

and a resulting increase in headcount to 7,300 -

the largest in the plant’s 28 year history.

Equally, Jaguar Land Rover has also witnessed

a major resurgence, with 2013 proving to be a

record year for production volumes coupled

with year on year headcount growth that has

resulted in over 8,000 new workers appointed

over the past 3 years and set to continue across

all UK facilities in addition to considerable

Only last year the industry attracted £2.5 bn overseas expansion.

of investment and created thousands of

jobs. This is in addition to the considerable However, the recovery across the industry is not

investment made by global vehicle manu- uniform. Nissan and JLR are jointly responsible

facturers over the previous five years. In for 80% of the 200,000 increase in car

2011 alone there was over £4bn of new production between 2001 and 2013, but for

investment announcements in the UK which Toyota, Vauxhall and Honda, the country’s 4th,

supported the creation of 9,900 new jobs 5th and 6th biggest manufacturers are all

and safe- guarded another 12,000 across producing around 30% fewer cars in Britain

vehicle manufacturers and the supply chain. than they were before the financial crisis.

Summaryof 2013

Positioned as the largest sector in terms

of exports by value, the UK automotive

industry is well placed to support efforts

to re-balance the economy towards trade

and investment in line with a government

target to double exports to £1tn by 2020.

4

And while luxury manufacturers Bentley, Just a third of all parts that go into the

JLR have announced more than £2bn worth average British built car come from UK

of investments between them in 2013, fellow based suppliers. That compares with

premium brand Aston Martin declared its around 60% in Germany, and a massive

intensions more recently in 2014 with plans 80% in the Czech Republic, a relative

to invest £500m as part of a longer term newcomer to the big volume car

plan to develop a new range of cars, plus manufacturing game.

extend its manufacturing facility at Gaydon.

To address these major challenges as well as

opportunities faced by the UK auto sector, Unfortunately, the future for Lotus is less

the Automotive Investment Organisation certain after the Hethel based company

(AIO) was formed last year.made a net loss in excess of £167m in

2013 and ultimately breached its banking

Headed by former Ford Chairman Joe covenants. Despite this the company still

Greenwell, it has been well received by invested over £92m in R&D during 2013, a

industry leaders, not only because it is fully figure in excess of its entire revenue stream,

integrated within UK Trade & Investment but hopefully serves as a bold statement

but also a joint creation of the Automotive of intent for the future.

Council resulting in senior buy-in from

industry.

As well as ensuring that the UK automotive

industry maintains its status as a global

leader, the main aims of the AIO are to

increase R&D investment, strengthen

relationships overseas with global

manufacturers and importantly promote

the UK as a great supply chain investment

opportunity

and

Summaryof 2013

By far, the biggest concern for the

automotive industry at present is the

erosion of the supply chain over the

past 30 years.

5

T he UK automotive industry supports a Supply-Chain disciplines, with Manufacturing

complex infrastructure; ranging from and Operations also feeling the strain more

OEM’s & VM’s through to Tier 1 and Tier 2 recently as volumes near capacity levels.

suppliers that produce a multitude of vehicles, It may be that companies who have previously modules and components. Equally there exists been highly selective with their selection criteria a healthy support industry that provides may have to widen their parameters - even primarily consulting, and after market services consider individuals from other manufacturing to this ever burgeoning industry sector.sectors (with FMCG and Aerospace being

The dramatic increase in vehicle production increasingly considered), in order to satisfy

volumes over the past 3-4 years coupled with requirements. This is despite the requirement

relentless new vehicle development has created to provide training as well as period of

a major increase in demand across all discipline adjustment for any new converts.

areas. This is further exacerbated by the gradual In line with these resourcing pressures, we have shortening of launch cycles as OEM’s attempt also witnessed a stronger demand for Contracting to keep their product ranges ‘fresh’.and Interim staff which fortunately can provide

Consequently, this has resulted in a contest for a flexible solution for companies to meet

talent as organisations compete for a limited fluctuations in demand. The downside however

pool of automotive based skill-sets and being that Contractors are all too often exponents

industry specific experience; often resulting in of supply and demand, and can prove costly,

candidates receiving multiple job offers. Indeed, particularly for the higher demand skills-sets.

another prevalent trend is for customer

companies (often OEM’s) to poach staff directly

from their suppliers as a means of plugging

skills gaps; again the knock-on effect

culminating in progressive wage increases. This

combined with the trend for counter offers

means that organisations are increasingly

forced to break budgets & salary parameters in

order to secure their new recruits.

This is a trend that is expected to continue into Clearly this is a positive indication that firms 2014 as the effect of skills scarcity continues to are now tackling the skills shortage within the bite. So far this has been felt particularly within industry, but may be considered too little, too late Engineering (Design, Production, Process and to offer any real benefit in the short-termProject based roles), Quality, and Logistics /

Demandfor Talent 2014

Looking to the future and on a positive note,

the trend particularly among larger organisations

is to either increase or initiate Apprenticeship

and Graduate intake schemes.

6

AutomotiveTechnology

Trends

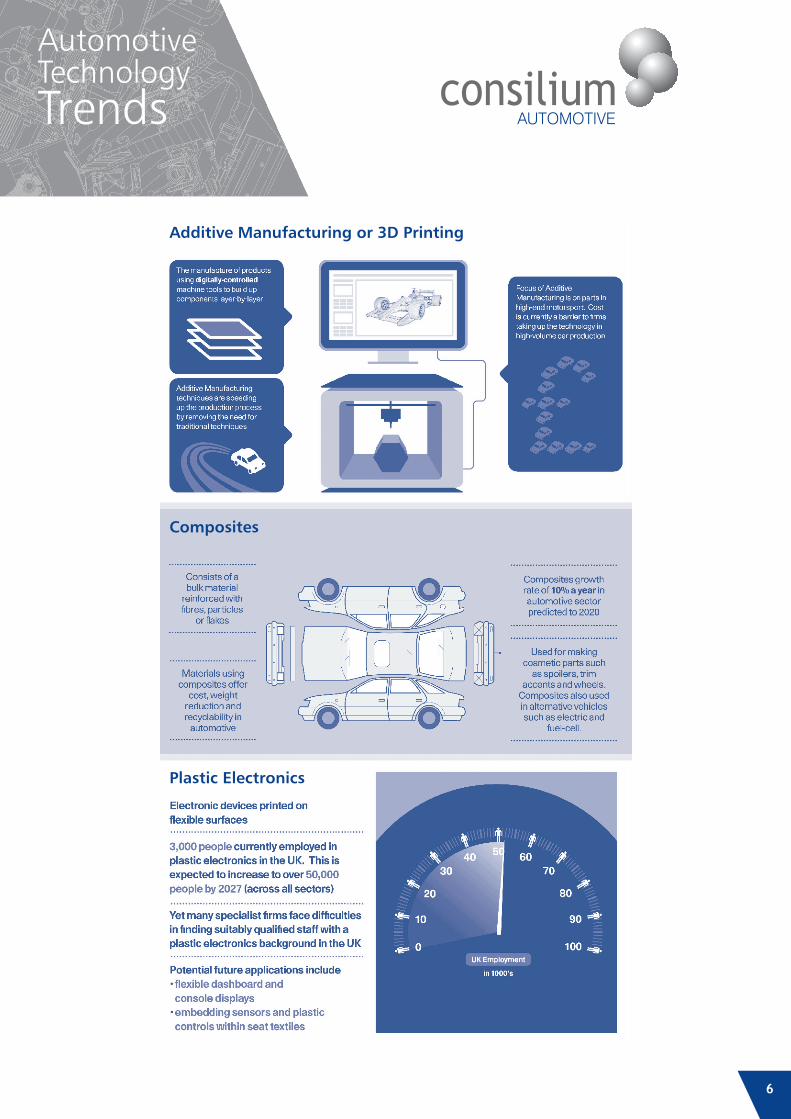

Additive Manufacturing or 3D Printing

Composites

Plastic Electronics

7

A

Research & Development

Export Markets

Supply Chain

s well as being home to some of the business from overseas and become

most productive car plants in Europe, the indispensable partners to global vehicle

UK auto industry also possesses a world-class manufacturers.

reputation for design and innovation. This is Research from the Automotive Council has particularly apparent in the field of low-carbon already shown that 80% of all component vehicle technologies where the UK is positioned types for vehicle assembly could be produced as an industry leader.in the UK if capability gaps are addressed -

With this in mind there are numerous worth approx. £3bn to UK suppliers.

challenges facing the UK automotive sector

which cannot be ignored.

The industry, supported by the UK government

focus on innovation has already identified five

priority technologies to develop in the UK to

ensure the sector strengthens its capabilities

in R&D. This is crucial for encouraging

investment and sustaining long-term

competitiveness in automotive manufacturing.

In particular, there are opportunities presented Global vehicle demand is set to proliferate with

by the global shift to low-carbon technologies the rise of emerging economies. By 2050 there

in automotive vehicle production. is expected to be more than one billion more

passenger vehicles on the road than today. Car Estimates suggest the shift towards a low-

ownership in China alone is estimated to over-carbon economy could see in excess of £150bn

take the US by 2030, and together China and invested in low-carbon vehicle technologies

India are expected to account for a third of all over the next 20 years alone.

global car ownership by 2050.

If the UK were to maintain its share of the

Chinese premium brand sector, then based on The UK automotive sector has already benefited

these growth predictions alone, the value of from considerable investment by global vehicle

exports to China could grow from £2bn in manufacturers over the last five years. These

2011 to £9.3bn by 2020.new investments and expansion plans present

UK suppliers with the opportunity to win back

The Next

5 Years

Developing the UK supply chain is

extremely important and will enhance

the ability of UK automotive companies

to produce more and at a reduced cost.

8

However, the UK spent only 0.02% of GDP on graduates annually from the period 2012-2020

trade support last year - widely criticised as with far too few students graduating from

being insufficient to re-balance the economy university each year to satisfy demand.

towards net exports.

At the moment there is a huge shortage

of engineering capacity, both in terms of

apprenticeships for skilled trades in The present overcapacity in the European manufacturing and at the graduate level, automotive market has been magnified by the particularly in growth areas such as electronics slow down of the major Eurozone economies - and advanced powertrain.Germany, France, Italy and Spain. Low growth

and high unemployment across Europe has

until recently curtailed consumer demand and

increased price competition, forcing automotive Access to finance remains a critical issue for UK firms to control costs in order to sustain automotive companies seeking to invest for competitiveness. growth. Despite government efforts to

influence lenders, their reluctance lies in the

perceived risk involved in an industry where The uncertainty surrounding Europe’s political lead times for new products can often extend future also presents a short-term challenge for to 5-7 years.the sector. The industry currently exports more

than 82% of vehicles manufactured in the UK,

with 49% of total automotive exports going to Manufacturers have invested heavily in energy the 27 EU member states.efficiency measures but the profitability of the

heaviest users is still threatened by high prices

and supply issues.The industry faces significant skill shortages

Since 2002 alone, the industrial price of gas as well as difficulties in attracting young people

has increased by 122%, while individual into careers in engineering and advanced

electricity prices have increased by 94%.manufacturing. It has made some good

progress in increasing the number of The increase in energy prices has wiped

apprenticeship starts, but there are long-term out company efficiency savings for many

supply issues at graduate level. companies, with green tariffs expected to

add another 70% by 2030 if they go ahead For example, recent analysis from the Royal as proposedAcademy of Engineering estimates that the UK

economy will require more than10,000 STEM

Competition

Finance

Europe

Energy Prices

Skills

The Next

5 Years

9

O f the 28 companies whom participated in this survey, representing a cross-section of the

industry (including OEMs, Motorsport, Off-highway, T1&T2 suppliers, plus support companies

involved in the auto industry supply-chain),we were able to gain the following insight:

How do you expect headcount numbers to change during 2015?

Do you expect your company to announce salary increases or bonus payments during 2015?

How does your company normallygo about resourcing?

What is your main tool to ensureemployee retention?

MarketInsight

Increase57%

Remainconstant29%

Decrease14%

Yes52%

No23%

Unsure25%

Flexible Working / Conditions 10%

ImprovedSalary36%

CareerDevelopment23%

EnhancedBenefits19%

Training12%Recruitment

Agency54%

DirectAdvertising23%

Social Media/Networking 18%

Other 5%

10

consiliumGROUP

2014

SalaryTables

11

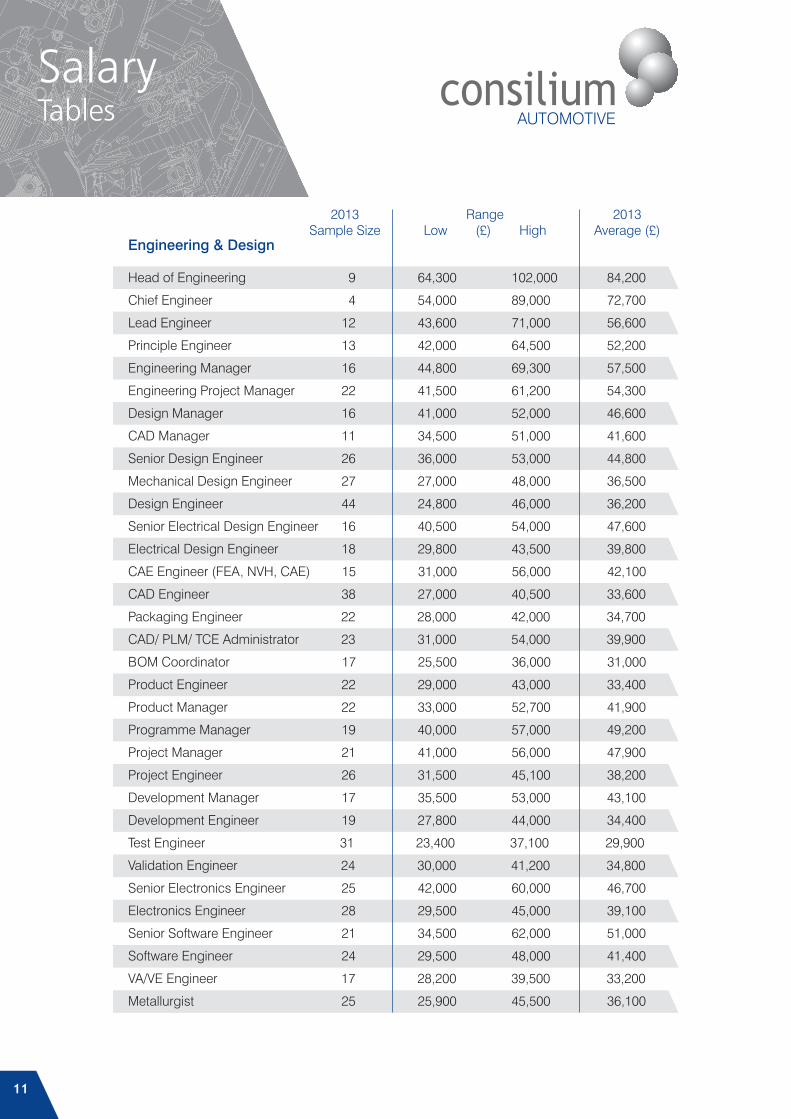

Head of Engineering 9 64,300 102,000 84,200

Chief Engineer 4 54,000 89,000 72,700

Lead Engineer 12 43,600 71,000 56,600

Principle Engineer 13 42,000 64,500 52,200

Engineering Manager 16 44,800 69,300 57,500

Engineering Project Manager 22 41,500 61,200 54,300

Design Manager 16 41,000 52,000 46,600

CAD Manager 11 34,500 51,000 41,600

Senior Design Engineer 26 36,000 53,000 44,800

Mechanical Design Engineer 27 27,000 48,000 36,500

Design Engineer 44 24,800 46,000 36,200

Senior Electrical Design Engineer 16 40,500 54,000 47,600

Electrical Design Engineer 18 29,800 43,500 39,800

CAE Engineer (FEA, NVH, CAE) 15 31,000 56,000 42,100

CAD Engineer 38 27,000 40,500 33,600

Packaging Engineer 22 28,000 42,000 34,700

CAD/ PLM/ TCE Administrator 23 31,000 54,000 39,900

BOM Coordinator 17 25,500 36,000 31,000

Product Engineer 22 29,000 43,000 33,400

Product Manager 22 33,000 52,700 41,900

Programme Manager 19 40,000 57,000 49,200

Project Manager 21 41,000 56,000 47,900

Project Engineer 26 31,500 45,100 38,200

Development Manager 17 35,500 53,000 43,100

Development Engineer 19 27,800 44,000 34,400

Test Engineer 31 23,400 37,100 29,900

Validation Engineer 24 30,000 41,200 34,800

Senior Electronics Engineer 25 42,000 60,000 46,700

Electronics Engineer 28 29,500 45,000 39,100

Senior Software Engineer 21 34,500 62,000 51,000

Software Engineer 24 29,500 48,000 41,400

VA/VE Engineer 17 28,200 39,500 33,200

Metallurgist 25 25,900 45,500 36,100

2013Sample Size

2013Average (£)

RangeLow (£) High

Engineering & Design

SalaryTables

12

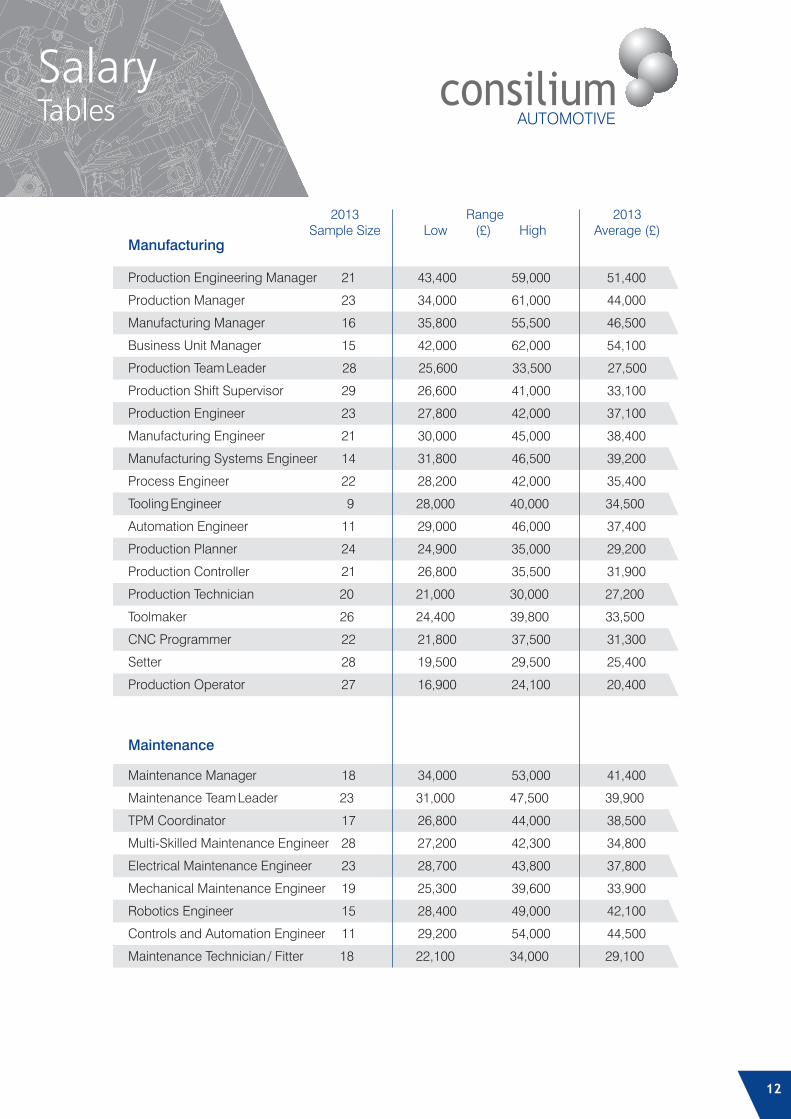

Production Engineering Manager 21 43,400 59,000 51,400

Production Manager 23 34,000 61,000 44,000

Manufacturing Manager 16 35,800 55,500 46,500

Business Unit Manager 15 42,000 62,000 54,100

Production 28 25,600 33,500 27,500Team Leader

Production Shift Supervisor 29 26,600 41,000 33,100

Production Engineer 23 27,800 42,000 37,100

Manufacturing Engineer 21 30,000 45,000 38,400

Manufacturing Systems Engineer 14 31,800 46,500 39,200

Process Engineer 22 28,200 42,000 35,400

Tooling Engineer 9 28,000 40,000 34,500

Automation Engineer 11 29,000 46,000 37,400

Production Planner 24 24,900 35,000 29,200

Production Controller 21 26,800 35,500 31,900

Production 20 21,000 30,000 27,200Technician

Toolmaker 26 24,400 39,800 33,500

CNC Programmer 22 21,800 37,500 31,300

Setter 28 19,500 29,500 25,400

Production Operator 27 16,900 24,100 20,400

Maintenance Manager 18 34,000 53,000 41,400

Maintenance Leader 23 31,000 47,500 39,900Team

TPM Coordinator 17 26,800 44,000 38,500

Multi-Skilled Maintenance Engineer 28 27,200 42,300 34,800

Electrical Maintenance Engineer 23 28,700 43,800 37,800

Mechanical Maintenance Engineer 19 25,300 39,600 33,900

Robotics Engineer 15 28,400 49,000 42,100

Controls and Automation Engineer 11 29,200 54,000 44,500

Maintenance / Fitter 18 22,100 34,000 29,100Technician

2013Sample Size

2013Average (£)

RangeLow (£) High

Manufacturing

Maintenance

SalaryTables

13

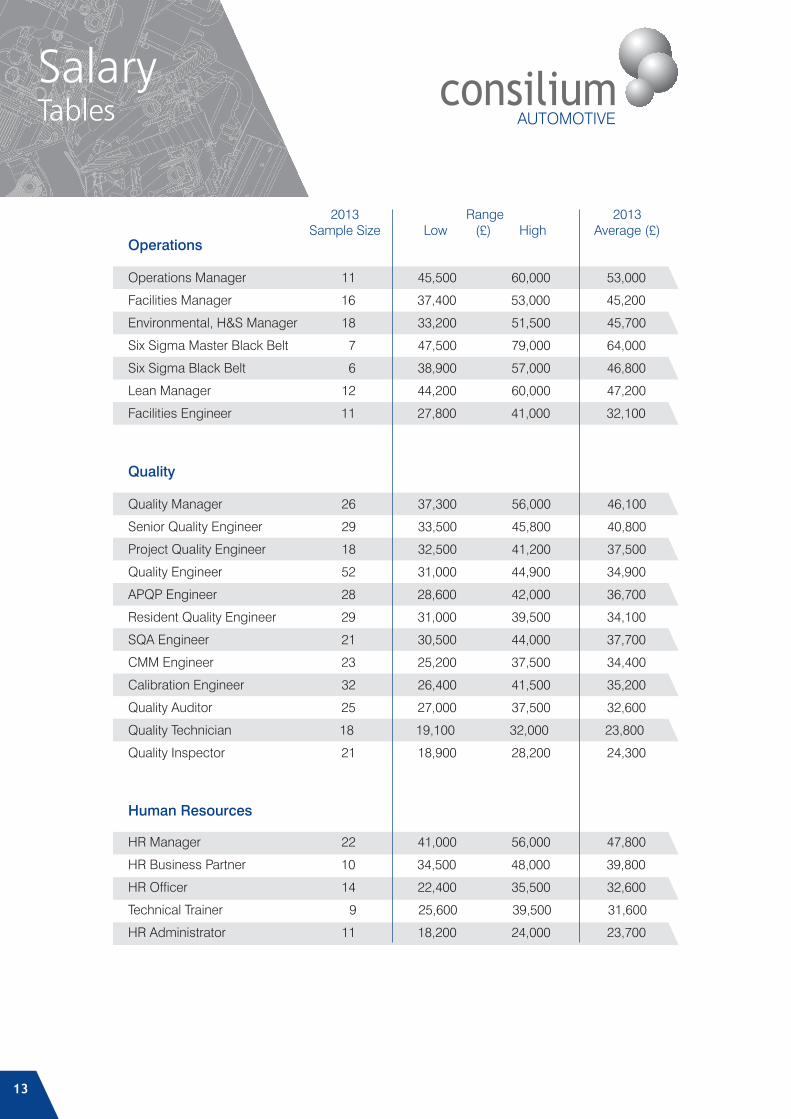

Operations Manager 11 45,500 60,000 53,000

Facilities Manager 16 37,400 53,000 45,200

Environmental, H&S Manager 18 33,200 51,500 45,700

Six Sigma Master Black Belt 7 47,500 79,000 64,000

Six Sigma Black Belt 6 38,900 57,000 46,800

Lean Manager 12 44,200 60,000 47,200

Facilities Engineer 11 27,800 41,000 32,100

2013Sample Size

2013Average (£)

RangeLow (£) High

Operations

Quality Manager 26 37,300 56,000 46,100

Senior Quality Engineer 29 33,500 45,800 40,800

Project Quality Engineer 18 32,500 41,200 37,500

Quality Engineer 52 31,000 44,900 34,900

APQP Engineer 28 28,600 42,000 36,700

Resident Quality Engineer 29 31,000 39,500 34,100

SQA Engineer 21 30,500 44,000 37,700

CMM Engineer 23 25,200 37,500 34,400

Calibration Engineer 32 26,400 41,500 35,200

Quality Auditor 25 27,000 37,500 32,600

Quality 18 19,100 32,000 23,800Technician

Quality Inspector 21 18,900 28,200 24,300

Quality

Human Resources

HR Manager 22 41,000 56,000 47,800

HR Business Partner 10 34,500 48,000 39,800

HR Officer 14 22,400 35,500 32,600

Technical Trainer 9 25,600 39,500 31,600

HR Administrator 11 18,200 24,000 23,700

SalaryTables

14

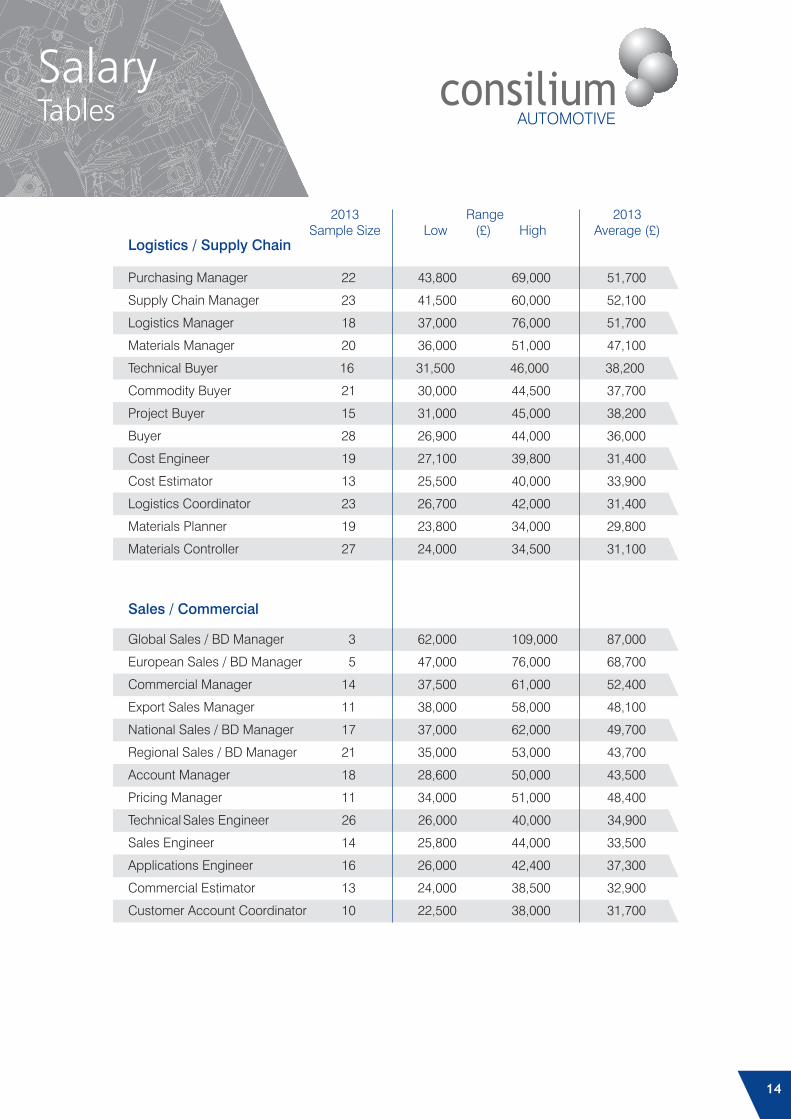

Purchasing Manager 22 43,800 69,000 51,700

Supply Chain Manager 23 41,500 60,000 52,100

Logistics Manager 18 37,000 76,000 51,700

Materials Manager 20 36,000 51,000 47,100

Technical Buyer 16 31,500 46,000 38,200

Commodity Buyer 21 30,000 44,500 37,700

Project Buyer 15 31,000 45,000 38,200

Buyer 28 26,900 44,000 36,000

Cost Engineer 19 27,100 39,800 31,400

Cost Estimator 13 25,500 40,000 33,900

Logistics Coordinator 23 26,700 42,000 31,400

Materials Planner 19 23,800 34,000 29,800

Materials Controller 27 24,000 34,500 31,100

Global Sales / BD Manager 3 62,000 109,000 87,000

European Sales / BD Manager 5 47,000 76,000 68,700

Commercial Manager 14 37,500 61,000 52,400

Export Sales Manager 11 38,000 58,000 48,100

National Sales / BD Manager 17 37,000 62,000 49,700

Regional Sales / BD Manager 21 35,000 53,000 43,700

Account Manager 18 28,600 50,000 43,500

Pricing Manager 11 34,000 51,000 48,400

Technical Sales Engineer 26 26,000 40,000 34,900

Sales Engineer 14 25,800 44,000 33,500

Applications Engineer 16 26,000 42,400 37,300

Commercial Estimator 13 24,000 38,500 32,900

Customer Account Coordinator 10 22,500 38,000 31,700

2013Sample Size

2013Average (£)

RangeLow (£) High

Logistics / Supply Chain

Sales / Commercial

SalaryTables

15

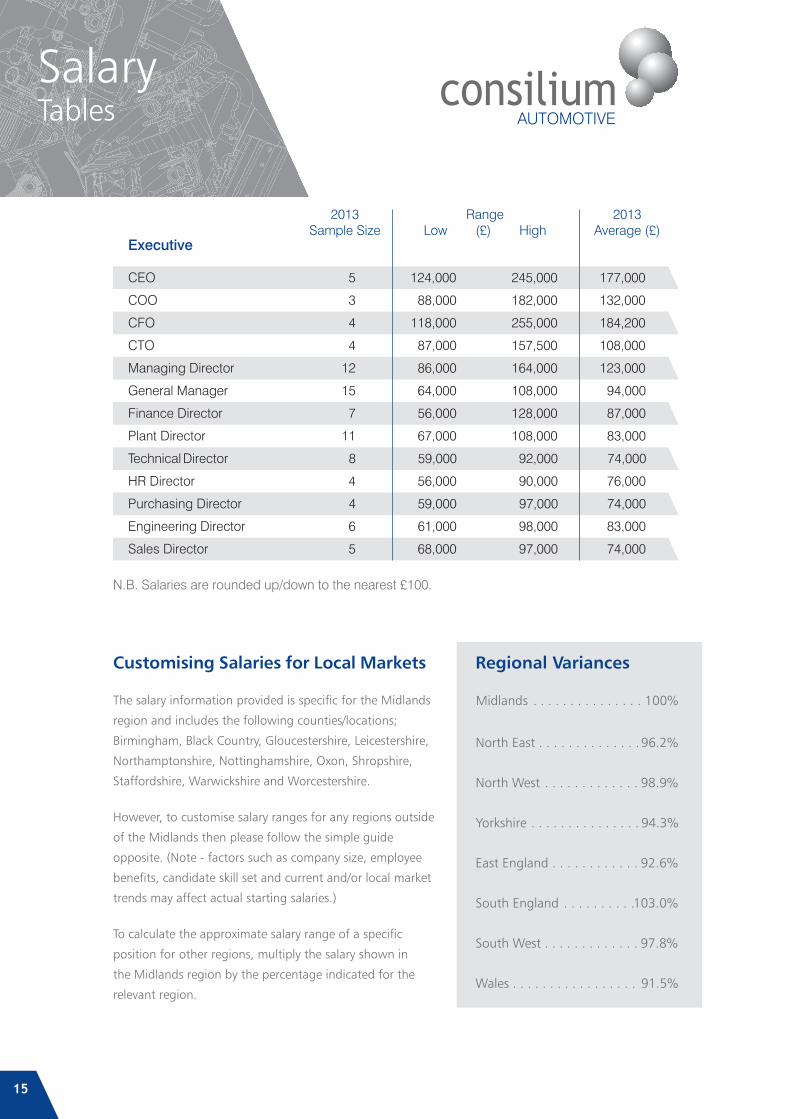

Customising Salaries for Local Markets

The salary information provided is specific for the Midlands

region and includes the following counties/locations;

Birmingham, Black Country, Gloucestershire, Leicestershire,

Northamptonshire, Nottinghamshire, Oxon, Shropshire,

Staffordshire, Warwickshire and Worcestershire.

However, to customise salary ranges for any regions outside

of the Midlands then please follow the simple guide

opposite. (Note - factors such as company size, employee

benefits, candidate skill set and current and/or local market

trends may affect actual starting salaries.)

To calculate the approximate salary range of a specific

position for other regions, multiply the salary shown in

the Midlands region by the percentage indicated for the

relevant region.

Midlands . . . . . . . . . . . . . . .

North East . . . . . . . . . . . . . .

North West . . . . . . . . . . . . .

Yorkshire . . . . . . . . . . . . . . .

East England . . . . . . . . . . . .

South England . . . . . . . . . .

South West . . . . . . . . . . . . .

Wales . . . . . . . . . . . . . . . . .

Regional Variances

100%

96.2%

98.9%

94.3%

92.6%

103.0%

97.8%

91.5%

CEO 5 124,000 245,000 177,000

COO 3 88,000 182,000 132,000

CFO 4 118,000 255,000 184,200

CTO 4 87,000 157,500 108,000

Managing Director 12 86,000 164,000 123,000

General Manager 15 64,000 108,000 94,000

Finance Director 7 56,000 128,000 87,000

Plant Director 11 67,000 108,000 83,000

Technical Director 8 59,000 92,000 74,000

HR Director 4 56,000 90,000 76,000

Purchasing Director 4 59,000 97,000 74,000

Engineering Director 6 61,000 98,000 83,000

Sales Director 5 68,000 97,000 74,000

2013Sample Size

2013Average (£)

RangeLow (£) High

Executive

N.B. Salaries are rounded up/down to the nearest £100.

SalaryTables

consiliumGROUP

Member

Anglo HouseWorcester RoadStourport-on-SevernWorcestershire DY13 9AW

Russell Tuck01299 [email protected]

To discuss any aspect of the automotive recruitment or a more specific and Benefit award levels within your particular marketplace - please contact:

analysis of Compensation

© Consilium Group Ltd - All profile requests are subject to our normal Termsand Conditions of Business for the Introduction of Staff - available on request.

100 COUNTRIES

TO OVER

EXPORT 11%OF TOTAL UK EXPORTS

£55BN ANNUAL

TURNOVER

£12BN

ECONOMY

IN NETVALUETO THE UK

CONTRIBUTION

TO GDP2.3%

£1.5

BN

A YEARIN R&D OF ANNUAL

REVENUE

£30BN

CARS AND COMMERCIALVEHICLES PER YEAR

1.6 MILLION

2.5 MILLION ANNUALLYENGINES

EUROPE’S

MARKETNEW CAR2ND LARGEST

720,000PEOPLE EMPLOYED

IN AUTO UK’S LARGESTEXPORTER