Connecting with "Hyperconnected" Consumers

13

CONNECTING WITH “HYPERCONNECTED” CONSUMERS WOMEN IN RESEARCH JUNE 11, 2015

-

Upload

euromonitor-international -

Category

Business

-

view

3.933 -

download

5

Transcript of Connecting with "Hyperconnected" Consumers

CONNECTING WITH “HYPERCONNECTED” CONSUMERS

WOMEN IN RESEARCH

JUNE 11, 2015

© Euromonitor International

2

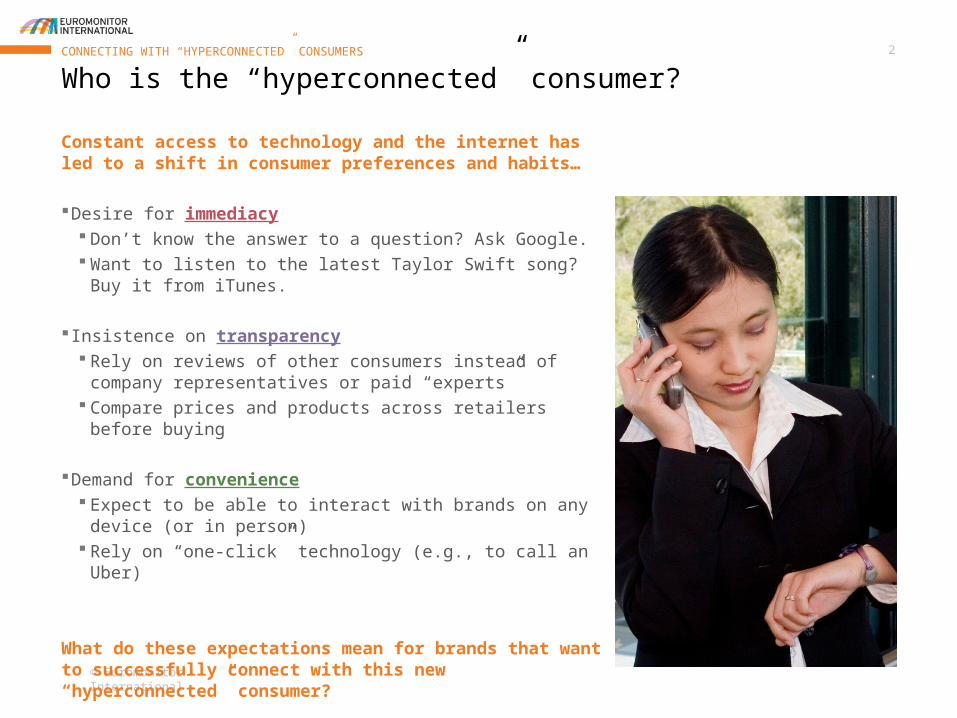

Constant access to technology and the internet has led to a shift in consumer preferences and habits…

Desire for immediacy Don’t know the answer to a question? Ask Google. Want to listen to the latest Taylor Swift song? Buy it from iTunes.

Insistence on transparency Rely on reviews of other consumers instead of company

representatives or paid “experts” Compare prices and products across retailers before buying

Demand for convenience Expect to be able to interact with brands on any device (or in

person) Rely on “one-click” technology (e.g., to call an Uber)

What do these expectations mean for brands that want to successfully connect with this new “hyperconnected” consumer?

Who is the “hyperconnected” consumer?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

CONNECTING WITH HYPERCONNECTED CONSUMERS…

…ONLINE AND IN THE PHYSICAL WORLD

…WHILE SHOPPING

…VIA MOBILE

© Euromonitor International

4

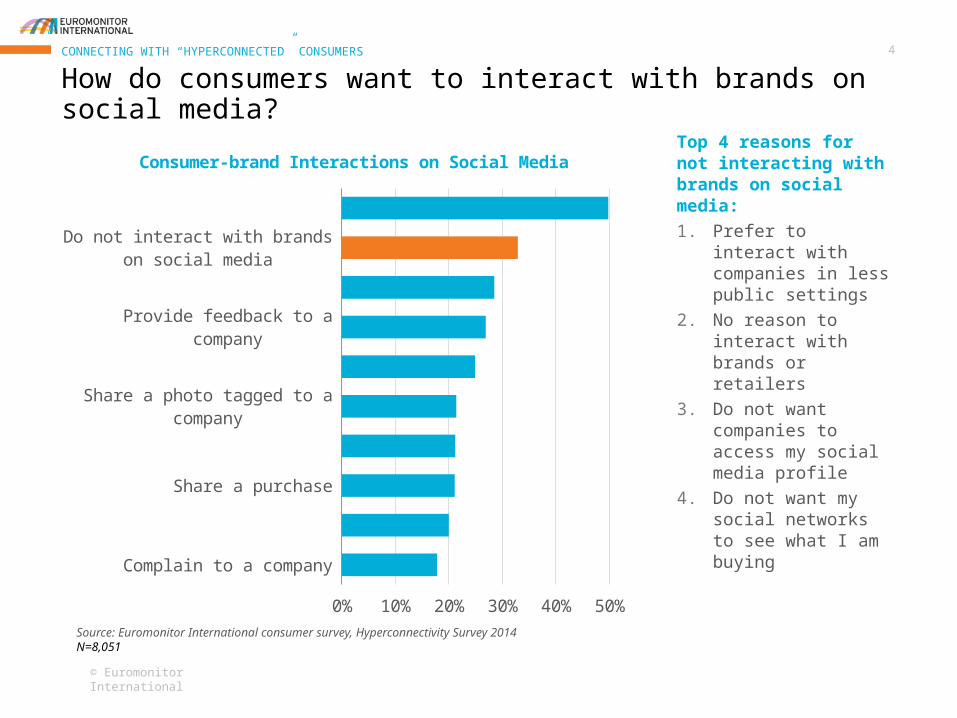

Complain to a company

Share or retweet a product

Share a purchase

Talk to customer service

Share a photo tagged to a company

Buy something via social media

Provide feedback to a company

Share a company’s feed or post

Do not interact with brands on social media

“Follow” or “like” a company

0% 10% 20% 30% 40% 50%

Consumer-brand Interactions on Social MediaTop 4 reasons for not interacting with brands on social media:

1. Prefer to interact with companies in less public settings

2. No reason to interact with brands or retailers

3. Do not want companies to access my social media profile

4. Do not want my social networks to see what I am buying

How do consumers want to interact with brands on social media?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014N=8,051

© Euromonitor International

5

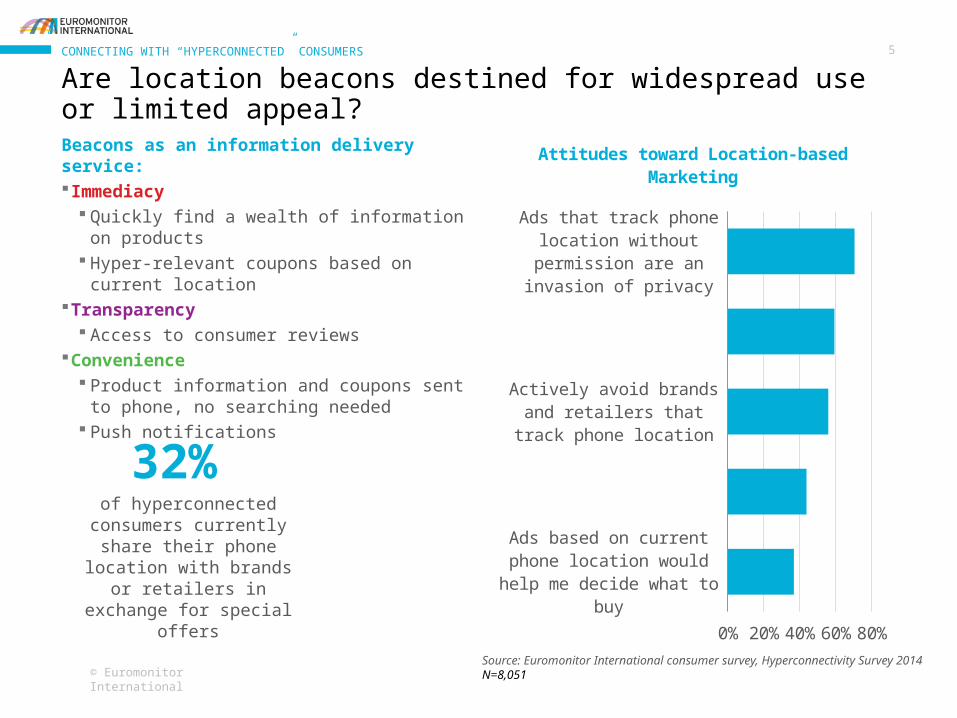

Are location beacons destined for widespread use or limited appeal?

CONNECTING WITH “HYPERCONNECTED” CONSUMERS

32% of hyperconnected consumers

currently share their phone location with brands or

retailers in exchange for special offers

Beacons as an information delivery service: Immediacy

Quickly find a wealth of information on products Hyper-relevant coupons based on current

locationTransparency

Access to consumer reviewsConvenience

Product information and coupons sent to phone, no searching needed

Push notifications

Ads based on current phone location would help me decide what to buy

Willing to share phone location in exchange for discounts

Actively avoid brands and retailers that track phone location

Uncomfortable sharing phone location with brands and retailers

Ads that track phone location without permission are an invasion of privacy

Attitudes toward Location-based Marketing

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014N=8,051

© Euromonitor International

6

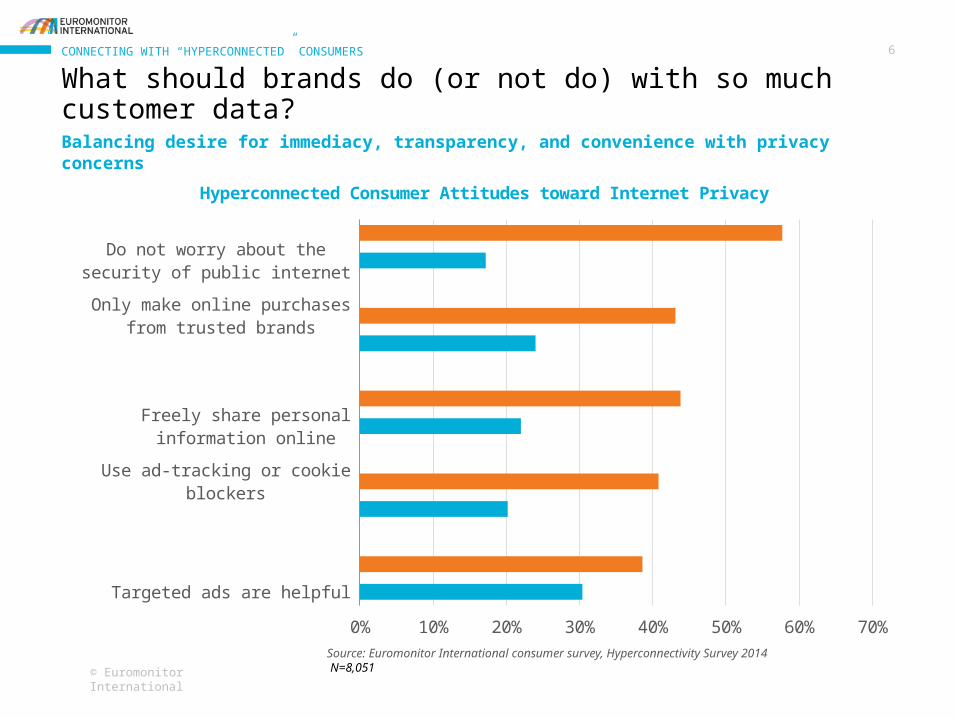

What should brands do (or not do) with so much customer data?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

Balancing desire for immediacy, transparency, and convenience with privacy concerns

Targeted ads are helpful

Use ad-tracking or cookie blockers

Freely share personal information online

Only make online purchases from trusted brands

Do not worry about the security of public internet

0% 10% 20% 30% 40% 50% 60% 70%

Hyperconnected Consumer Attitudes toward Internet Privacy

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014 N=8,051

CONNECTING WITH HYPERCONNECTED CONSUMERS…

…ONLINE AND IN THE PHYSICAL WORLD

…WHILE SHOPPING

…VIA MOBILE

© Euromonitor International

8

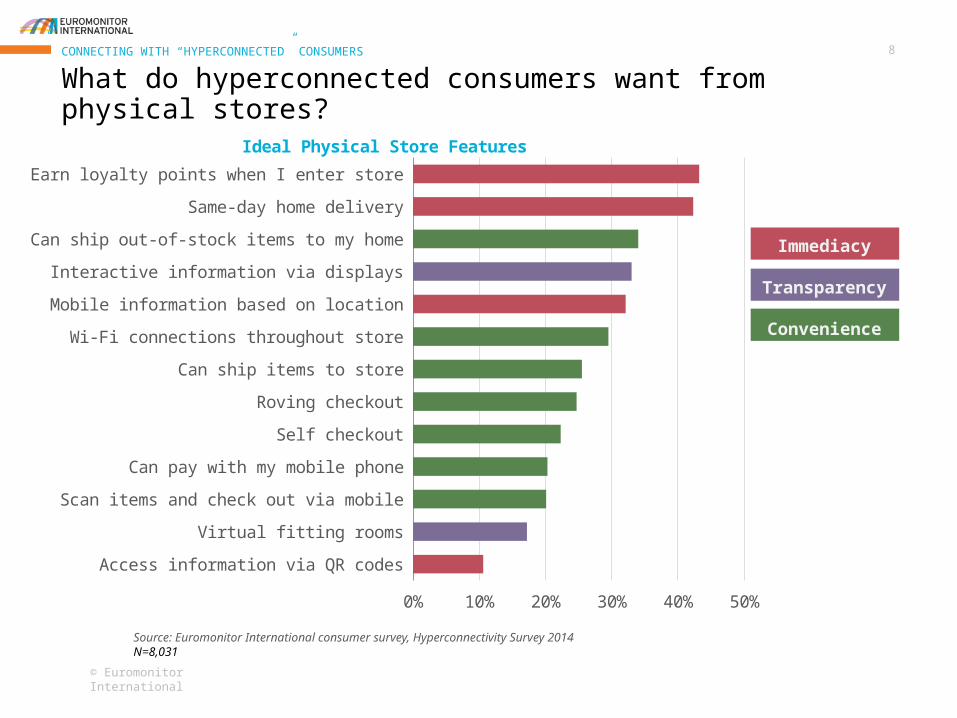

Immediacy

Transparency

Convenience

Access information via QR codes

Virtual fitting rooms

Scan items and check out via mobile

Can pay with my mobile phone

Self checkout

Roving checkout

Can ship items to store

Wi-Fi connections throughout store

Mobile information based on location

Interactive information via displays

Can ship out-of-stock items to my home

Same-day home delivery

Earn loyalty points when I enter store

0% 10% 20% 30% 40% 50%

Ideal Physical Store Features

What do hyperconnected consumers want from physical stores?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014N=8,031

© Euromonitor International

9

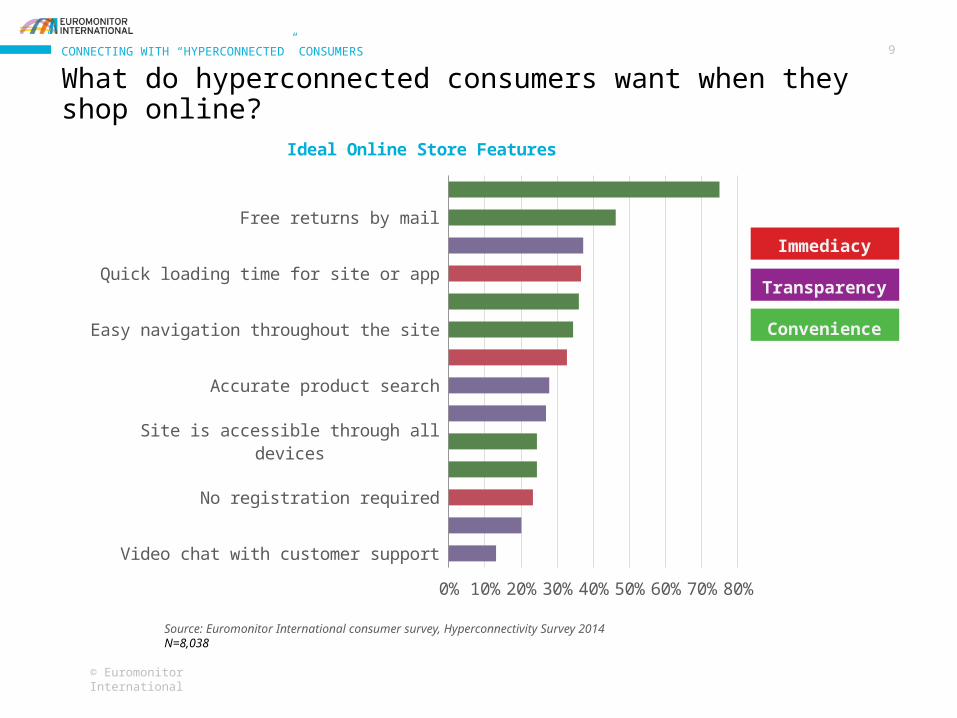

Video chat with customer support

Virtual fitting rooms

No registration required

Product suggestions based on history

Site is accessible through all devices

Videos showcasing product features

Accurate product search

Expedited shipping

Easy navigation throughout the site

Free return to store

Quick loading time for site or app

Feedback from current customers

Free returns by mail

Free shipping

0% 10% 20% 30% 40% 50% 60% 70% 80%

Ideal Online Store Features

What do hyperconnected consumers want when they shop online?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014N=8,038

Immediacy

Transparency

Convenience

© Euromonitor International

10

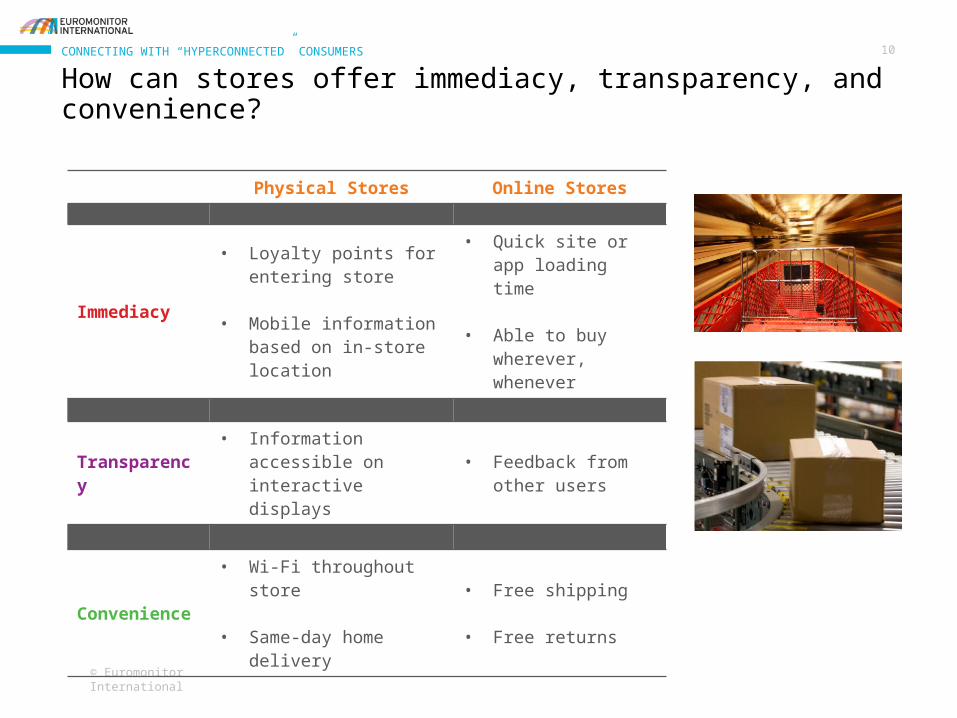

How can stores offer immediacy, transparency, and convenience?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

Physical Stores Online Stores

Immediacy

• Loyalty points for entering store

• Mobile information based on in-store location

• Quick site or app loading time

• Able to buy wherever, whenever

Transparency• Information accessible

on interactive displays• Feedback from other

users

Convenience• Wi-Fi throughout store

• Same-day home delivery

• Free shipping

• Free returns

CONNECTING WITH HYPERCONNECTED CONSUMERS…

…ONLINE AND IN THE PHYSICAL WORLD

…WHILE SHOPPING

…VIA MOBILE

© Euromonitor International

12

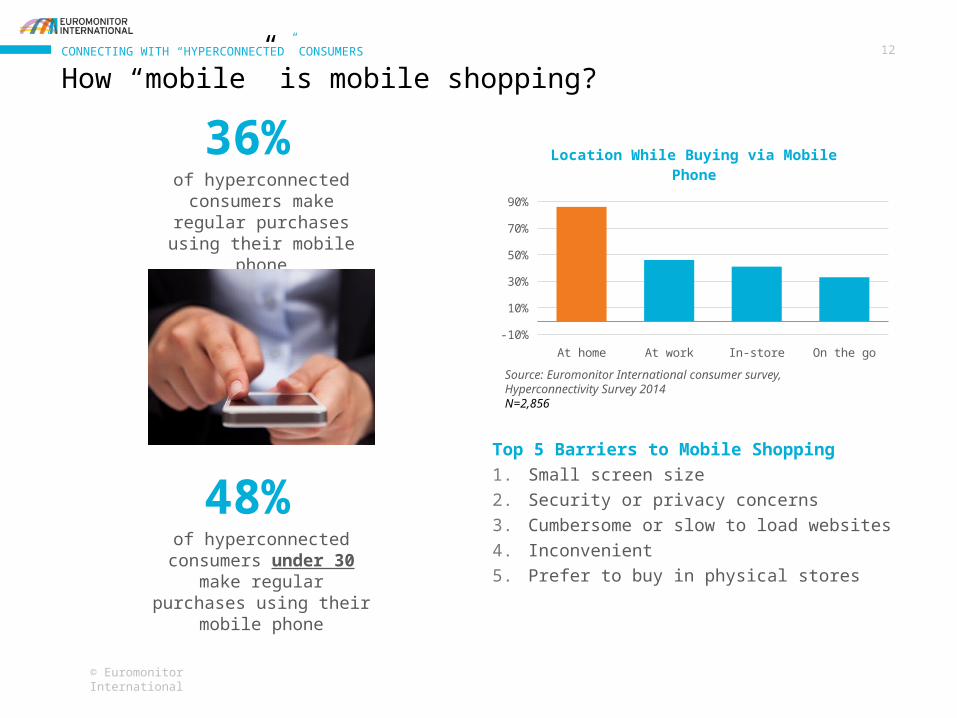

48% of hyperconnected

consumers under 30 make regular purchases using their

mobile phone

36% of hyperconnected

consumers make regular purchases using their mobile

phone

At home At work In-store On the go0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Location While Buying via Mobile Phone

How “mobile” is mobile shopping?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

Top 5 Barriers to Mobile Shopping

1. Small screen size

2. Security or privacy concerns

3. Cumbersome or slow to load websites

4. Inconvenient

5. Prefer to buy in physical stores

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014N=2,856

© Euromonitor International

13

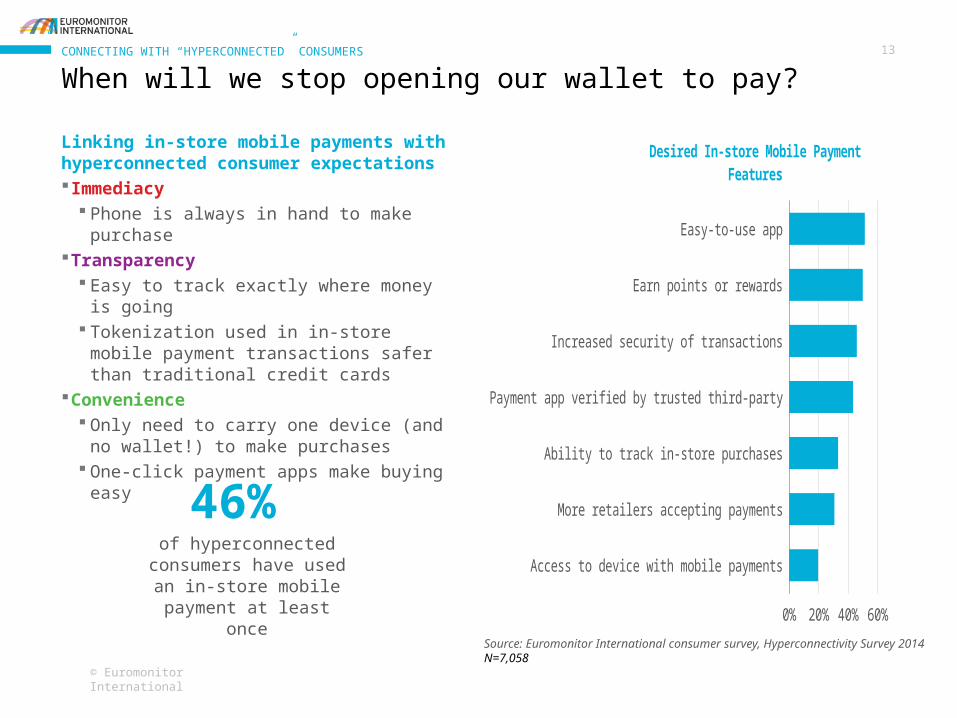

Linking in-store mobile payments with hyperconnected consumer expectations Immediacy

Phone is always in hand to make purchaseTransparency

Easy to track exactly where money is going Tokenization used in in-store mobile payment

transactions safer than traditional credit cardsConvenience

Only need to carry one device (and no wallet!) to make purchases

One-click payment apps make buying easy

Access to device with mobile payments

More retailers accepting payments

Ability to track in-store purchases

Payment app verified by trusted third-party

Increased security of transactions

Earn points or rewards

Easy-to-use app

0% 20% 40% 60%

Desired In-store Mobile Payment Fea-tures

When will we stop opening our wallet to pay?CONNECTING WITH “HYPERCONNECTED” CONSUMERS

46% of hyperconnected

consumers have used an in-store mobile payment at

least once

Source: Euromonitor International consumer survey, Hyperconnectivity Survey 2014N=7,058