CONFIDENTIAL Global Competition – How can Korean Companies Prosper and Grow in a Hostile Climate...

33

CONFIDENTIAL Global Competition – How can Korean Companies Prosper and Grow in a Hostile Climate Stephen Bear, McKinsey & Company July 19, 2005 This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organization without prior written approval from McKinsey & Company. This material was used by McKinsey & Company during an oral presentation; it is not a complete record of the discussion.

-

Upload

ginger-collins -

Category

Documents

-

view

216 -

download

0

Transcript of CONFIDENTIAL Global Competition – How can Korean Companies Prosper and Grow in a Hostile Climate...

CONFIDENTIAL

Global Competition – How can Korean Companies Prosper and Grow in a Hostile Climate

Global Competition – How can Korean Companies Prosper and Grow in a Hostile Climate

Stephen Bear, McKinsey & Company

July 19, 2005

This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organization without prior written approval from McKinsey & Company. This material was used by McKinsey & Company during an oral presentation; it is not a complete record of the discussion.

2

KEY MESSAGES

1. Despite challenging conditions, Korean companies have performed quite well – but their “health” raises concerns about sustainability

2. To prosper and grow in this hostile environment, Korean companies can look at the rise of other global champions for lessons to emulate

3. Without a concerted effort by companies, government and labor, Korea will not shake itself out of the current malaise

3

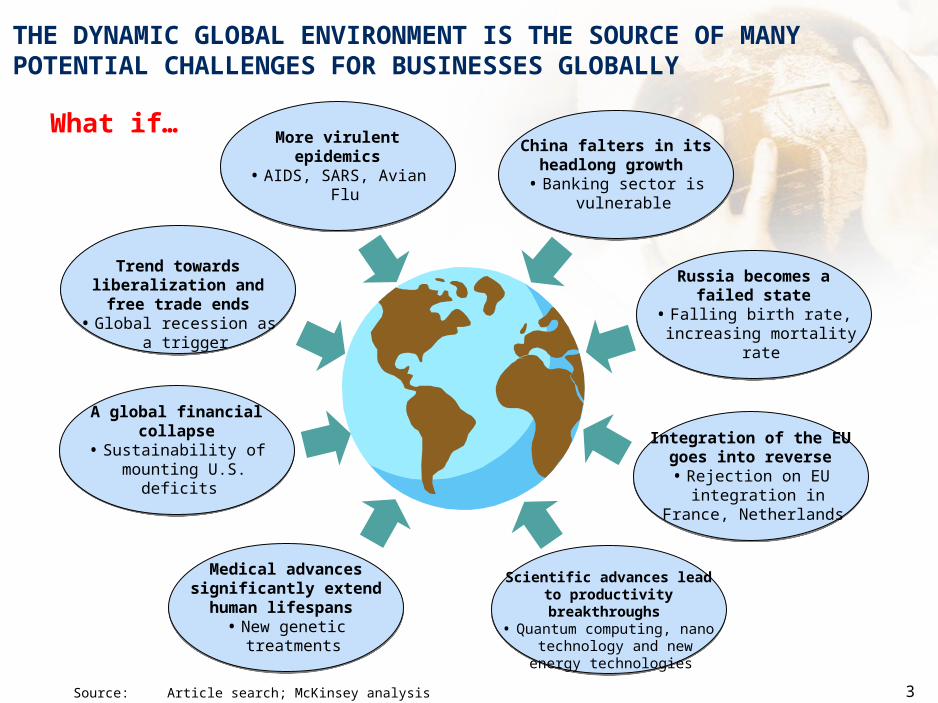

THE DYNAMIC GLOBAL ENVIRONMENT IS THE SOURCE OF MANY POTENTIAL CHALLENGES FOR BUSINESSES GLOBALLY

More virulent epidemics• AIDS, SARS, Avian Flu

China falters in its headlong growth

• Banking sector is vulnerable

Russia becomes a failed state

• Falling birth rate, increasing mortality rate

Integration of the EU goes into reverse

• Rejection on EU integration in France, Netherlands

Scientific advances lead to productivity breakthroughs • Quantum computing, nano

technology and new energy technologies

Medical advances significantly extend human

lifespans • New genetic treatments

A global financial collapse• Sustainability of mounting

U.S. deficits

Trend towards liberalization and free trade ends

• Global recession as a trigger

Source:Article search; McKinsey analysis

What if…

4

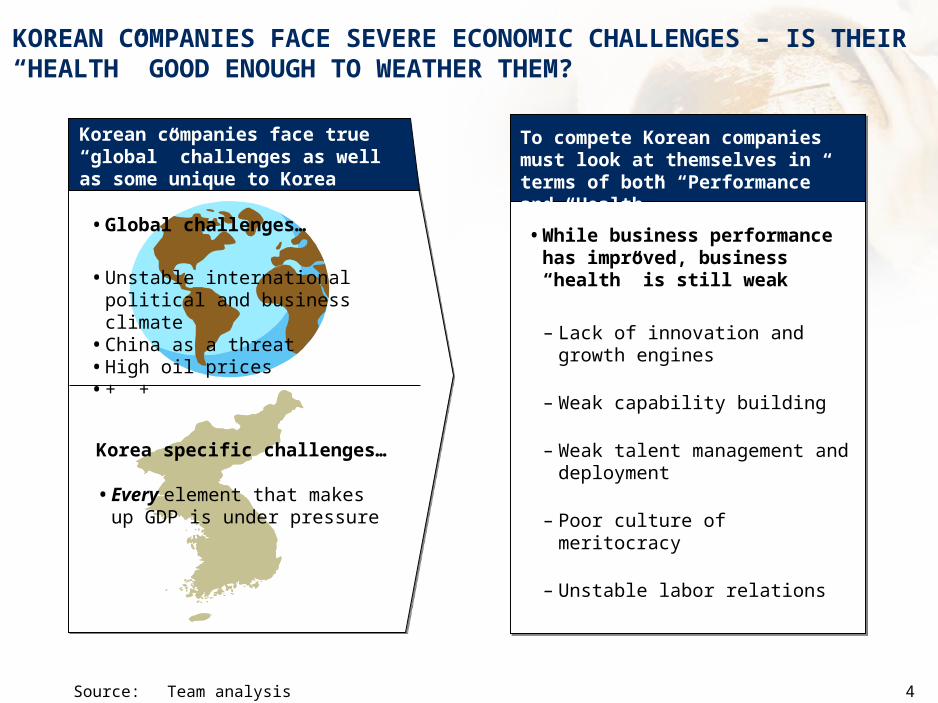

KOREAN COMPANIES FACE SEVERE ECONOMIC CHALLENGES – IS THEIR “HEALTH” GOOD ENOUGH TO WEATHER THEM?

Source:Team analysis

Korean companies face true “global” challenges as well as some unique to Korea

Korea specific challenges…

• Every element that makes up GDP is under pressure

• Global challenges…

• Unstable international political and business climate

• China as a threat• High oil prices• + +

• While business performance has improved, business “health” is still weak

– Lack of innovation and growth engines

– Weak capability building

– Weak talent management and deployment

– Poor culture of meritocracy

– Unstable labor relations

To compete Korean companies must look at themselves in terms of both “Performance” and “Health”

5

• Increasing pressure given growing government debt and increasing social burden

5• Low corporate investment (despite accumulation of cash)

• Fierce competition for FDI (especially from China)

• Negative capital market’s view on Korea

2

3

4

GIVEN DOMESTIC AND INTERNATIONAL CLIMATE THERE WILL BE ON-GOING PRESSURE ON GDP GOING FORWARD

GDP C I G NX

• Continued suppressed domestic spending

• Korea’s export led economy concentrated on both a sector and destination basis1

6

Source:Team analysis

Sluggish GDP

growth expected

6

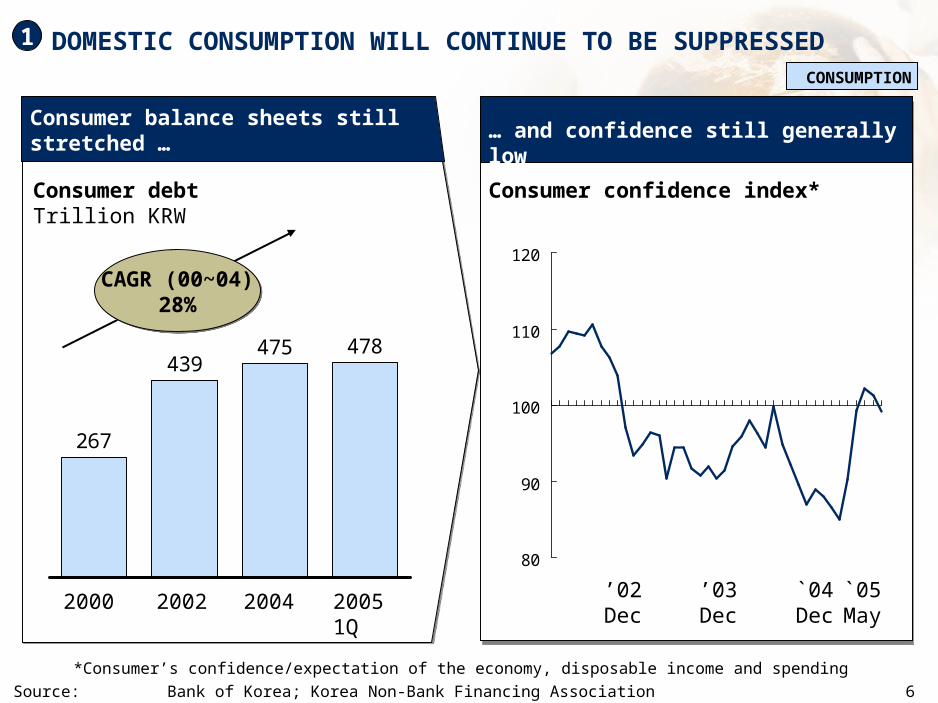

DOMESTIC CONSUMPTION WILL CONTINUE TO BE SUPPRESSEDCONSUMPTION

1

소비자 기대지수 ** … and confidence still generally low

Consumer confidence index*

80

90

100

110

120

’02 Dec

’03 Dec

`04 Dec

`05 May

267

439475 478

20022000 2004 20051Q

CAGR (00~04)28%

CAGR (00~04)28%

Consumer balance sheets still stretched …

Consumer debtTrillion KRW

*Consumer’s confidence/expectation of the economy, disposable income and spending

Source: Bank of Korea; Korea Non-Bank Financing Association

7

KOREAN COMPANIES ARE NOT FINDING ATTRACTIVE OPPORTUNITIES TO INVEST

INVESTMENT

… companies’ investments have been weak

Despite increase in cash reserves… due to negative economic outlook…

Annual growth rate of cash reserve of Korea’s top 50 companies*Percent, growth rate

22%7%

40%52%

2%

2003 20042000 20022001

Business confidence index

60

80

100

120

-9.8

6.8

-1.5

3.8 3.1

Investment growth rate (YOY)Percent

2001 2003 2005.1Q(E)

20042003 2005

* Based on top 50 manufacturing companies which are listed in KOSPI by revenue

Source: KIS-Value; National Statistics Office; Korea development bank; Bank of Korea

20042002

2

8

KOREA’S COMPETITIVENESS TO ATTRACT FDI IS ONE OF THE LOWEST IN ASIA

Source: IMD world competitiveness yearbook (2004); Korea chamber of commerce & industry

On the scale of 10 (figures in brackets show ranking among 60 countries surveyed), 2004

Labor related restriction

Risks from political uncertainty

Investment incentives

U.S.

Taiwan

China

Japan

Korea

Singapore 7.14

8.72

6.13

4.67

8.15

3.75 5.29

4.77

6.58

6.94

6.83

8.29

3.17

5.62

6.14

6.69

6.37

7.76

(55) (41)(44)

(20) (16)(10)

(54) (23)(12)

(47) (13)(8)

(27) (44)(17)

(13) (1)(2)

INVESTMENT

3

9

AS A RESULT, FDI AS A PERCENT OF GDP REMAINS LOW Percent INVESTMENT

*2004(E)

Source:EIU country data, Viewswire

China

Singapore

Ireland

0

5

10

15

20

25

1996 1997 1998 1999 2000 2001 2002 2003 2004

Korea*

Foreign direct investment as percent of GDP

3

10

4 KOREAN VALUATIONS ARE LOWER THAN OTHER MARKETS DUE TO THE CAPITAL MARKET’S NEGATIVE VIEW ON KOREA

Aggregate Market-to-Book ratio

Source: Datastream; McKinsey

INVESTMENT

S&P 500

DJ Euro Stocks

0

1

2

3

4

5

6

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

China - DS

KOSPI - Korea

HSI – Hong Kong

11

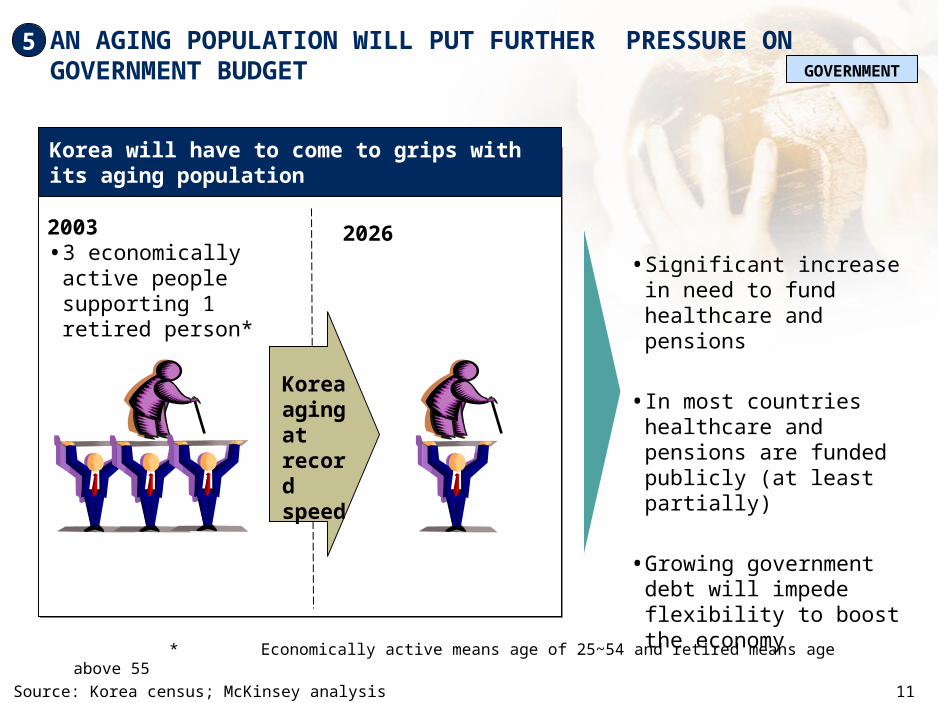

AN AGING POPULATION WILL PUT FURTHER PRESSURE ON GOVERNMENT BUDGET

Korea will have to come to grips with its aging population

2026

5GOVERNMENT

2003• 3 economically active

people supporting 1 retired person*

Korea aging at record speed

• Significant increase in need to fund healthcare and pensions

• In most countries healthcare and pensions are funded publicly (at least partially)

• Growing government debt will impede flexibility to boost the economy

*Economically active means age of 25~54 and retired means age above 55

Source: Korea census; McKinsey analysis

12

6 EXPORTS, THE ONLY PILLAR PROPPING UP KOREA’S ECONOMIC GROWTH HAS BEEN LOSING ITS MOMENTUM USD billion, YoY growth rate

Source: KITA; Bank of Korea

EXPORT

43.046.1 47.8

56.959.3

64.0 62.0

69.0 67.0

21%

14%16%

26%

29%

21%

13%

39%38%

1Q 2Q 3Q 4Q 1Q 2Q

2003 2004

3Q 4Q 1Q

2005

Growth rate

Total export amount

13

6 KOREAN EXPORTS ARE INCREASINGLY HIGHLY CONCENTRATED

Source: KITA; literature review

USD Billions, Percent EXPORT

Export concentration

risk

100% =

Semiconductor

2001 2004

Wireless telecom. device

Auto

Computer

Shipbuilding

Others

9%

7%

9%

7%

7%

61%

10%

10%

11%

7%

6%

56%

253.8150.4

39%44%

Share of items in total exports

14

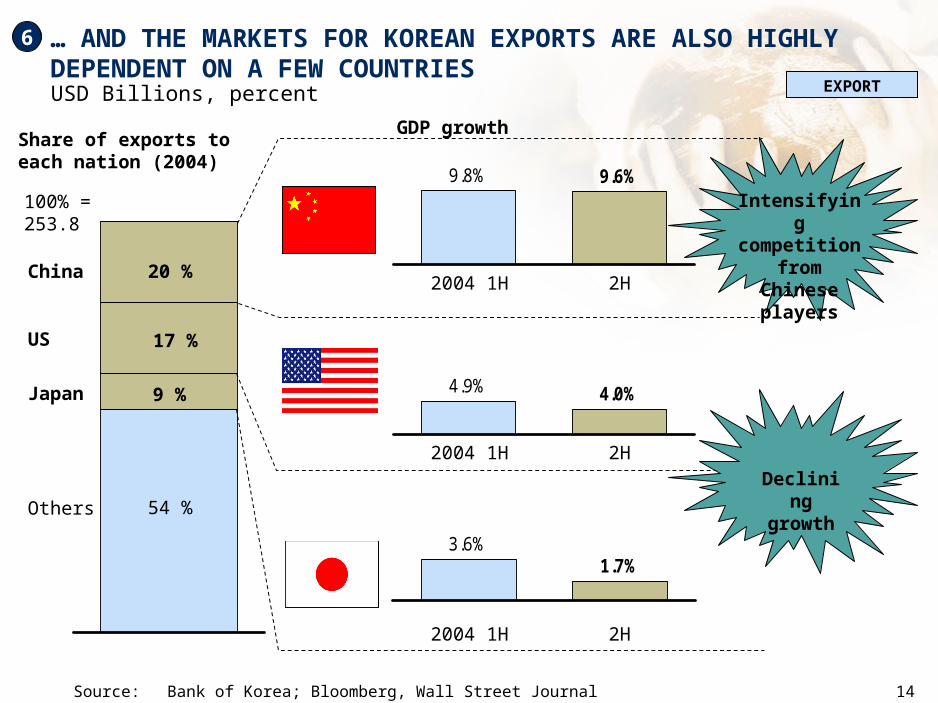

… AND THE MARKETS FOR KOREAN EXPORTS ARE ALSO HIGHLY DEPENDENT ON A FEW COUNTRIESUSD Billions, percent

Source:Bank of Korea; Bloomberg, Wall Street Journal

EXPORT

20 %China

Share of exports to each nation (2004)

100% = 253.8

US

Japan

Others

17 %

9 %

54 %

GDP growth

9.8% 9.6%

2004 1H 2H

4.9% 4.0%

2004 1H 2H

2004 1H 2H

3.6%1.7%

6

Intensifying competition

from Chinese players

Declining growth

15

BASED ON ITS COMPETITIVE WAGES AND GROWING CAPABILITIES, CHINA IS BECOMING A FORMIDABLE COMPETITOR

1.04

9.44

KoreaChina

*Hourly wages of workers in manufacturing sector**Number of years China can close the gap between Korea, assessed and forecasted by KDB

Source: EIU Country Data, KDB

Labor* cost comparison

US$, 2004

China’s competitiveness gap with Korea **

Gap in terms of number of years2004

6

1.8

2.3

2.5

3.8

4.5

7.0Shipbuilding

Automobile

Semiconductor

Computer

Telecom device

Consumer Electronics

16

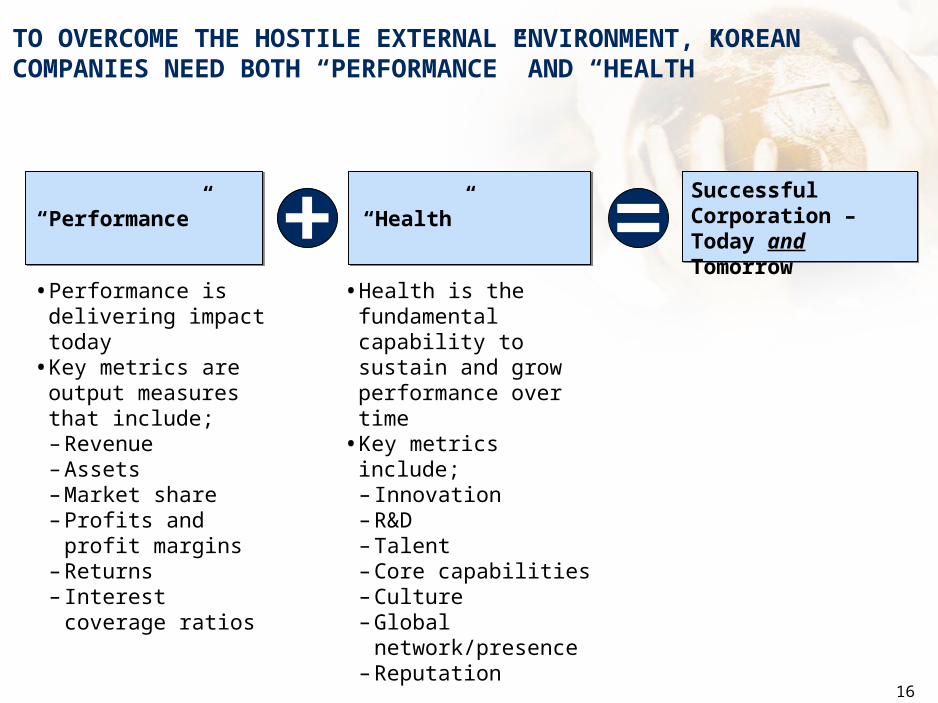

TO OVERCOME THE HOSTILE EXTERNAL ENVIRONMENT, KOREAN COMPANIES NEED BOTH “PERFORMANCE” AND “HEALTH”

“Performance”

• Performance is delivering impact today

• Key metrics are output measures that include;– Revenue– Assets– Market share– Profits and profit

margins– Returns– Interest coverage

ratios

“Health”

• Health is the fundamental capability to sustain and grow performance over time

• Key metrics include;– Innovation – R&D– Talent – Core capabilities– Culture– Global

network/presence– Reputation

Successful Corporation – Today and Tomorrow

17

WHILE KOREAN BUSINESS PERFORMANCE HAS IMPROVED…

Revenue

158284

490576

1998 2000 2002 2004

KRW Trillions

Asset

240372

520592

1998 2000 2002 2004

KRW Trillions

Operating margin

Number of companies, percent

Net profit margin

Number of companies, percent

20 11 10 11

53 66 66 69

25 20 20 162 4 5 4

1998 2000 2002 2004

Over 20%10%~20%

0%~10%

Below 0%

100%= 500 500 500 500

38 27 19 14

62 73 81 86

1998 2000 2002 2004

Positive net profit

Negative net profit

100%= 500 500 500 500

Source:Kis-value

Top 500 listed companies on KSE by revenue

18

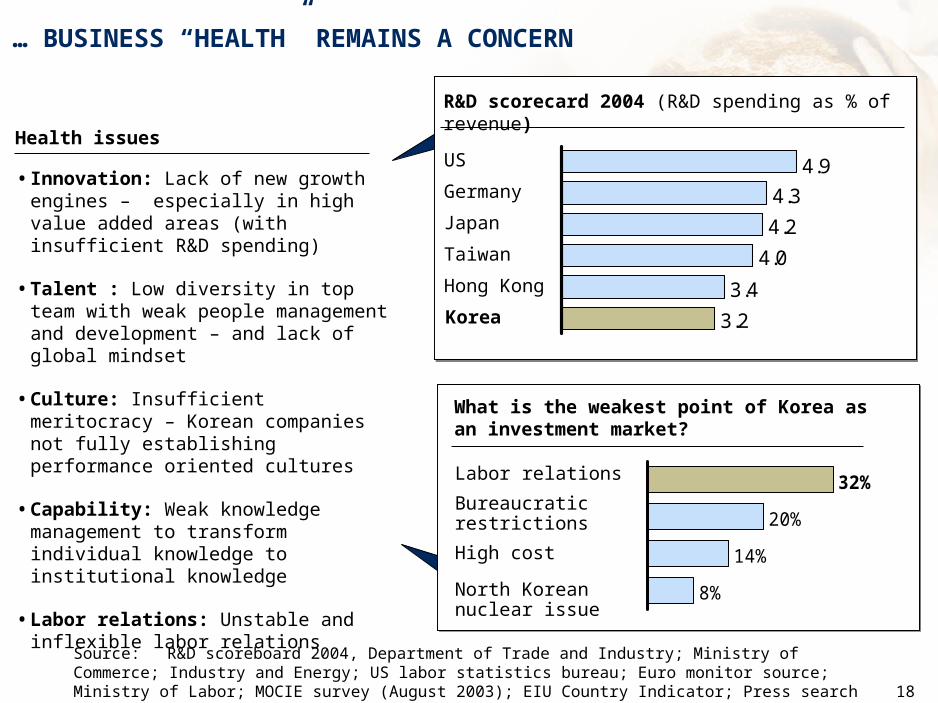

… BUSINESS “HEALTH” REMAINS A CONCERN

Source:R&D scoreboard 2004, Department of Trade and Industry; Ministry of Commerce; Industry and Energy; US labor statistics bureau; Euro monitor source; Ministry of Labor; MOCIE survey (August 2003); EIU Country Indicator; Press search

Health issues

• Innovation: Lack of new growth engines – especially in high value added areas (with insufficient R&D spending)

• Talent : Low diversity in top team with weak people management and development – and lack of global mindset

• Culture: Insufficient meritocracy – Korean companies not fully establishing performance oriented cultures

• Capability: Weak knowledge management to transform individual knowledge to institutional knowledge

• Labor relations: Unstable and inflexible labor relations

What is the weakest point of Korea as an investment market?

20%

14%

8%

32%Bureaucratic restrictions

High cost

North Korean nuclear issue

Labor relations

3.2

3.4

4.0

4.2

4.3

4.9

R&D scorecard 2004 (R&D spending as % of revenue)

US

Germany

Japan

Taiwan

Hong Kong

Korea

19

KEY MESSAGES

1. Despite challenging conditions, Korean companies have performed quite well – but their “health” raises concerns about sustainability

2. To prosper and grow in this hostile environment, Korean companies can look at the rise of other global champions for lessons to emulate

3. Without a concerted effort by companies, government and labor, Korea will not shake itself out of the current malaise

20

Global Champions are …

… the world’s most resilient companies competing successfully across geographies and businesses and well positioned to succeed in all types of economic environments

THE JOURNEY TO GLOBAL CHAMPION IS LONG (AND RISKY) AND REQUIRES FUNDAMENTAL ‘HEALTH’ OF COMPANIES

Source: Team analysis

• Journey is long & risky

– Companies have taken anywhere from 5 to 15 years to achieve global success

– For each company that achieves success, there are many others that fall by the wayside

• Successful journey requires both performance and ‘health’

– Capability to sustain and evolve performance over time

Journey to global champion

Local leader

Global leader

Global champion

21

Examples• Microsoft• Citigroup• Dell• Samsung• Johnson &

Johnson• Walmart• Fortis

40

23

38

6117

Number of companiesMANY COMPANIES FALL BY THE WAYSIDE

Note:The churn is not directly computable because 1997 list of GCs was developed using 5-year data (1992-97), whereas the 2002 GC list was developed using 10-year data

Source: Research Insight (Compustat and Global); Bloomberg; G2000 database

1997 Global champions

Drop-outs

Stay-ins New entrants

2002 Global champions

Examples• Honeywell• HSBC• Morgan Stanley• Pfizer• Cisco• Wyeth• Sun

Microsystems• Accenture

BACK UP

Examples• Akzo Nobel• Motorola• Pepsi• Fiat• Nestle• Hanson• Merck• Gillette

22

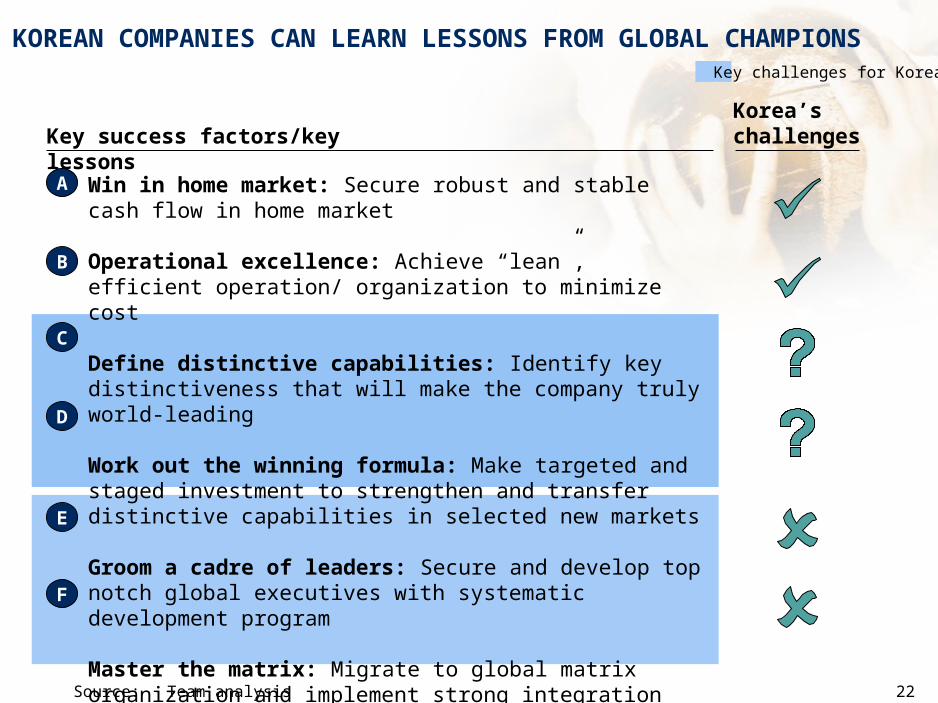

KOREAN COMPANIES CAN LEARN LESSONS FROM GLOBAL CHAMPIONS

Source:Team analysis

Key success factors/key lessons

Win in home market: Secure robust and stable cash flow in home market

Operational excellence: Achieve “lean”, efficient operation/ organization to minimize cost

Define distinctive capabilities: Identify key distinctiveness that will make the company truly world-leading

Work out the winning formula: Make targeted and staged investment to strengthen and transfer distinctive capabilities in selected new markets

Groom a cadre of leaders: Secure and develop top notch global executives with systematic development program

Master the matrix: Migrate to global matrix organization and implement strong integration processes with effective corporate center

A

B

C

D

E

F

Korea’s challenges

Key challenges for Korea

23

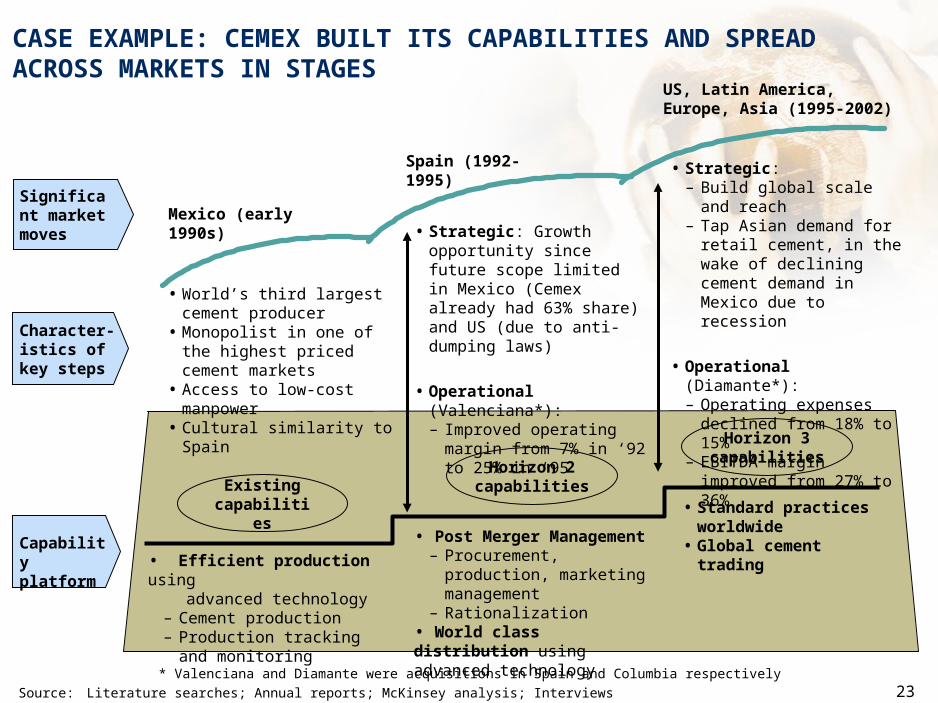

CASE EXAMPLE: CEMEX BUILT ITS CAPABILITIES AND SPREAD ACROSS MARKETS IN STAGES

Capability platform

Mexico (early 1990s)

Spain (1992-1995)

US, Latin America, Europe, Asia (1995-2002)

Existing capabilities

Horizon 2capabilities

Horizon 3capabilities

• Efficient production using advanced technology

– Cement production– Production tracking and

monitoring

• Post Merger Management – Procurement, production,

marketing management– Rationalization

• World class distribution using advanced technology

• Standard practices worldwide

• Global cement trading

• Strategic: Growth opportunity since future scope limited in Mexico (Cemex already had 63% share) and US (due to anti-dumping laws)

• Operational (Valenciana*): – Improved operating margin

from 7% in ‘92 to 25% in ‘95

• Strategic: – Build global scale and reach– Tap Asian demand for retail

cement, in the wake of declining cement demand in Mexico due to recession

• Operational (Diamante*): – Operating expenses declined

from 18% to 15%– EBITDA margin improved

from 27% to 36%

Character-istics of key steps

Significant market moves

• World’s third largest cement producer

• Monopolist in one of the highest priced cement markets

• Access to low-cost manpower• Cultural similarity to Spain

* Valenciana and Diamante were acquisitions in Spain and Columbia respectively

Source: Literature searches; Annual reports; McKinsey analysis; Interviews

24

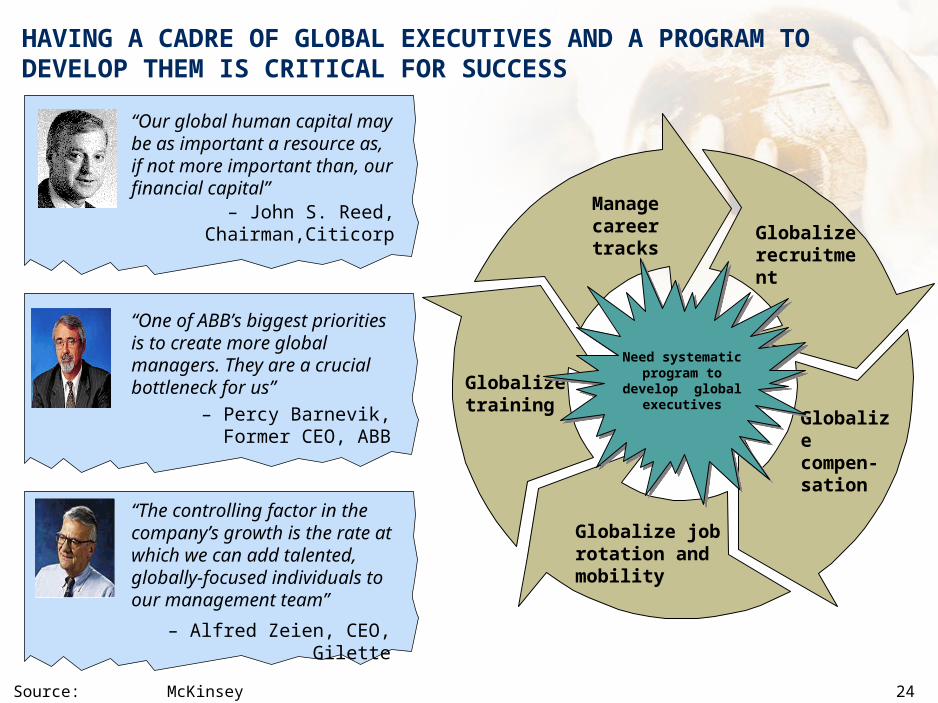

HAVING A CADRE OF GLOBAL EXECUTIVES AND A PROGRAM TO DEVELOP THEM IS CRITICAL FOR SUCCESS

Source: McKinsey

“Our global human capital may be as important a resource as, if not more important than, our financial capital”

– John S. Reed, Chairman,Citicorp

“One of ABB’s biggest priorities is to create more global managers. They are a crucial bottleneck for us”

– Percy Barnevik, Former CEO, ABB

“The controlling factor in the company’s growth is the rate at which we can add talented, globally-focused individuals to our management team”

– Alfred Zeien, CEO, Gilette

Globalize training

Manage career tracks Globalize

recruitment

Globalize compen-sation

Globalize job rotation and mobility

Need systematic program to develop global executives

25

MASTERING THE MATRIX ORGANIZATION REQUIRES THREE IMPORTANT ACTIONS

Source: Team analysis

Global matrix organization Processes

Set up the global matrix organization based on strategic priorities and allocate decision rights to each group – Don’t try to make all your global decisions locally or at home!

Build strong coordination mechanisms to bind various groups together

Set up ‘soft’ processes for fostering collaborative culture

1

2

3

1

3

Coordination

2

26

KEY MESSAGES

1. Despite challenging conditions, Korean companies have performed quite well – but their “health” raises concerns about sustainability

2. To prosper and grow in this hostile environment, Korean companies can look at the rise of other global champions for lessons to emulate

3. Without a concerted effort by companies, government and labor, Korea will not shake itself out of the current malaise

27

DESPITE SEVERE CHALLENGES, WITH THE RIGHT CHANGES, MORE KOREAN COMPANIES CAN BECOME GLOBAL CHAMPIONS

Korea is located in the center of the most dynamic economic area

Source: DRI-WEFA; Global 2000 database; Global Insights; McKinsey analysis

Some Asian companies, including Korean companies, are emerging rapidly

CHINA

BEIJING

SEOUL

TOKYO

NORTH-KOREA

SOUTH-KOREA

SHANGHAI

JAPANFUNSHUN

KUMAMOTO

CHIBAFUNABASHI

YOKOHHAMAHAMAMATSU

KAWASAKI

KYOTO

NAGOYAOSAKAI

KOBEOKKAYAMA

HIROSHIMA

KITAKYUSHU

FUKUOKA

KUMAMOTOJINAN

ZIBOXINGTAI

SHIJIAZHUANG

TIANJIN

TANGSHAN

TAZHANGJIKOU

FUXIN

JINZHOU ANSHAN

BENXISHENYANG

PYUNGYANGNAMPO

INCHONSUWON

TAEJON TAEGU

PUSAN

ULSAN

KWANJU

• 19% of world GDP• >0.5 billion people• ~200 cities with population of >1 million

Number of Asian (excluding Japanese) companies in the Global 1000

4.8%

4.4%

2.5%

1.0%

6.2%

5.6%

3.5%

3.0%

Top 100

Top 200

Top 500

Top 1000

1997

2002

New Asian global

champions

HSBC

28

FOR “KOREA INC.” TO PROSPER AND GROW, THERE MUST BE A CONCERTED EFFORT BY EACH KEY PARTIES

Source:Team analysis

Government Labor

Globally competitive “Korea Inc.”

None of the 3 can do it

alone!

Corporations

29

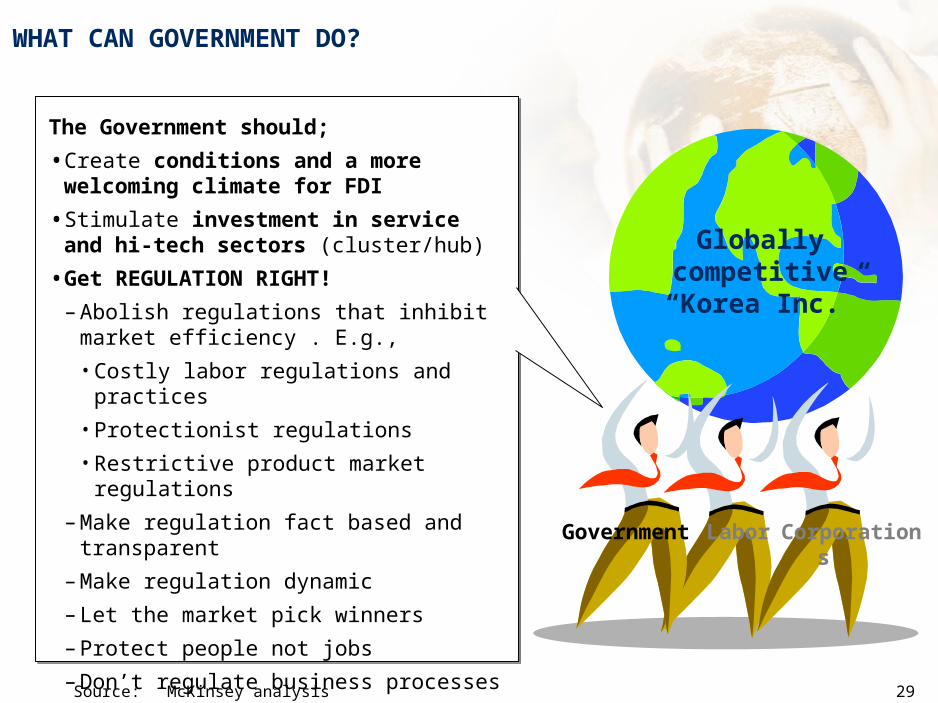

WHAT CAN GOVERNMENT DO?

Source:McKinsey analysis

The Government should;

• Create conditions and a more welcoming climate for FDI

• Stimulate investment in service and hi-tech sectors (cluster/hub)

• Get REGULATION RIGHT!

– Abolish regulations that inhibit market efficiency . E.g.,

• Costly labor regulations and practices

• Protectionist regulations

• Restrictive product market regulations

– Make regulation fact based and transparent

– Make regulation dynamic

– Let the market pick winners

– Protect people not jobs

– Don’t regulate business processes

– Make natural-monopoly trade-offs explicit

Government Labor Corporations

Globally competitive “Korea Inc.”

30

WHAT CAN LABOR DO?

Source: McKinsey analysis

Labor should;

• Recognize it HAS to change – or it will whither together with Korean competitiveness

• Recognize impact of negative reputation on Korea

• Get creative about win-win solutions

• Recognize the need for increased productivity to fund increased incomesGovernment Labor Corporations

Globally competitive “Korea Inc.”

31

WHAT CAN CORPORATIONS DO?

Source:McKinsey analysis

Corporations should;

• Focus as much on “Health” as “Performance”

• Significantly improve how they work as an organization

• Innovate and take risks to create a healthy and balanced portfolio of initiatives

… And to go Global;

• Create a true global organization that makes decisions where they need to be made

• Ramp up focus on global network/presence – global business is much more than exporting

• Ramp up focus on global talent – mindset shift of executives to truly think and act global

Government Labor Corporations

Globally competitive “Korea Inc.”

32

BUT… MORE IMPORTANT THAN ANYTHING – IT IS UP TO THE LEADERS IN THIS ROOM TO TAKE LEADERSHIP AND DRIVE CHANGE

• Many of these recommendations have been known for years…

• …but, why is there no change?

• It is up to the business leaders in Korea to be the catalyst that gets Korea Inc. out of the slump and drive prosperity in what will continue to be a hostile climate

IS A “CRISIS”

REQUIRED TO PRECIPITATE

CHANGE?

33

EOD