Conference call ye 2012 final

15

1 PRODUCING AND EXPLORING YEAR END CONFERENCE CALL FEBRUARY 20, 2013

-

Upload

terangagold -

Category

Documents

-

view

199 -

download

1

Transcript of Conference call ye 2012 final

1

PRODUCING AND EXPLORING YEAR END CONFERENCE CALL FEBRUARY 20, 2013

2

FORWARD LOOKING STATEMENTS Certain information included in this presentation, including any information as to the Company’s strategy, projects, exploration programs, joint venture ownership positions, plans, future financial or operating performance and other statements that express management’s expectations or estimates of future performance, constitute “forward-looking statements”. The words “believe”, “expect”, “will”, “intend”, ”anticipate”, “project”, ”plan”, “estimate”, “on track” and similar expressions identify forward looking statements. Such forward-looking statements are necessarily based upon a number of estimates, assumptions, opinions and analysis made by management in light of its experience that, while considered reasonable, may turn out to be incorrect and involve known and unknown risks, uncertainties and other factors, in each case that may cause the actual financial results, performance or achievements of the Company to be materially different from the Company’s estimated future results, performance or achievements expressed or implied by those forward-looking statements. Such forward-looking statements are not guarantees of future performance. These assumptions, risks, uncertainties and other factors include, but are not limited to: assumptions regarding general business and economic conditions; conditions in financial markets and the future financial performance of the company; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; the supply and demand for, deliveries of, and the level and volatility of the worldwide price of gold or certain other commodities (such as silver, fuel and electricity); fluctuations in currency markets, including changes in U.S. dollar and CFA Franc interest rates; risks arising from holding derivative instruments; adverse changes in our credit rating; level of indebtedness and liquidity; ability to successfully complete announced transactions and integrate acquired assets; legislative, political or economic developments in the jurisdictions in which the Company carries on business; operating or technical difficulties in connection with mining or development activities; employee relations; availability and costs associated with mining inputs and labour; the speculative nature of exploration and development, including the risks of obtaining necessary licenses and permits and diminishing quantities or grades of reserves; changes in costs and estimates associated with our projects; the accuracy of our reserve estimates (including with respect to size, grade and recoverability) and the geological, operational and price assumptions on which these are based; contests over title to properties, particularly title to undeveloped properties; the risks involved in the exploration, development and mining business, as well as other risks and uncertainties which are more fully described in the Company's prospectus dated November 11, 2010 and in other Company filings with securities and regulatory authorities which are available at www.sedar.com. Accordingly, readers should not place undue reliance on such forward looking statements. Teranga expressly disclaims any intention or obligation to update or revise any forward looking statements, whether as a result of new information, future events or otherwise, except in accordance with applicable securities laws. This presentation is dated as of February 20, 2013. All references to the Company include its subsidiaries unless the context requires otherwise. This presentation contains references to Teranga using the words “we”, “us”, “our” and similar words and the reader is referred to using the words “you”, “your” and similar words.

3

Profit (Loss) • Q4 2012 $48.8M • 2012 $79.9M • 2011 ($16.0M)

Cash Balance

• 2012 (1) $45.0M • 2011 (2) $24.6M

Hedge Balance • Jan. 29, 2013 38,105 oz. • 2012 59,789 oz. • 2011 174,500 oz.

Revenue • 2012 $350.5M • 2011 $236.9M

FINANCIAL RESULTS SUMMARY

(1) As at December 31, 2012. Includes cash and cash equivalents and $5.3M in bullion receivables. (2) As at December 31, 2011. Includes cash and cash equivalents and $17.0M in bullion receivables.

4

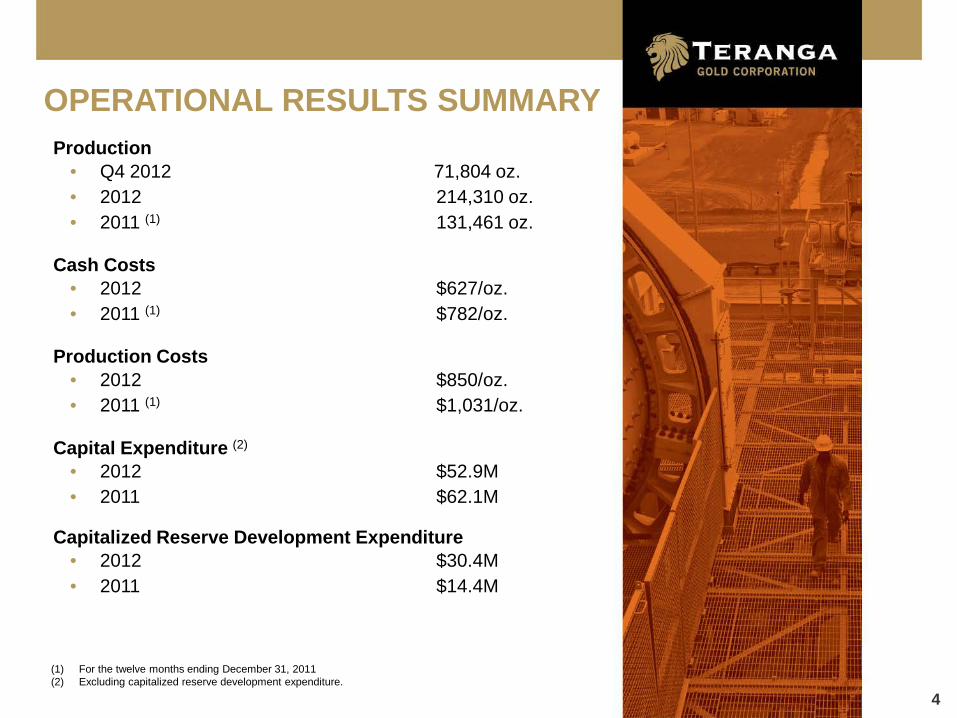

Production • Q4 2012 71,804 oz. • 2012 214,310 oz. • 2011 (1) 131,461 oz.

Cash Costs • 2012 $627/oz. • 2011 (1) $782/oz.

Production Costs • 2012 $850/oz. • 2011 (1) $1,031/oz.

Capital Expenditure (2) • 2012 $52.9M • 2011 $62.1M

Capitalized Reserve Development Expenditure

• 2012 $30.4M • 2011 $14.4M

(1) For the twelve months ending December 31, 2011 (2) Excluding capitalized reserve development expenditure.

OPERATIONAL RESULTS SUMMARY

5

Production Guidance • 190,000 - 210,000oz. at cash costs of $650 - $700/oz.

• Material mined 24% higher than in 2012

• Ore milled 37% higher than in 2012

Costs • Gross costs increasing $30M or 20%

• Unit costs per tonne to decrease

2013 OUTLOOK

6

Tax Assessments • Senegal tax authority has levied $36M in tax assessments

against the Company

• Reviewed with our legal counsel and concluded to have no merit

Contribution Tax • New Senegalese law was passed to impose a 5%

“contribution” on the sale of products from mines and quarries

• Stability provision in place for Sabodala

• Working with the Senegalese authorities in order to find a mutually agreeable solution

FISCAL

7

Mill Expansion Completed in 2012 • Continuing our mill optimization work

• Capacity - 3.5Mtpa of 100% hard ore and 6Mtpa of 100% oxide ore

• Processing ~95% hard ore in 2013

• Expect design capacity by end of Q2

Mill Production • Objective is to produce a base of 200,000oz. from the mine

license alone

• Phase 1 Vision: Increase production to 250,000 – 350,000oz.

• Gora will be additive to our mine license production for an annual total of ~250,000oz.

EXPANSION, RESERVES AND EXPLORATION & DEVELOPMENT

8

Economics • Capital cost est. $45M - $50M • Est. total cash cost to average $675 - $700/oz. • NPV (5%) at $1500/oz. of $105 million • IRR 69%

Open Pit

• 26km from mill • Technical Study and ESIA complete – initiating

permitting Q1’13 • Proven & Probable reserves of 285,000oz. at

4.2gpt. • Estimated 4 year mine life • Stripping ratio of 19:1 • Estimating production to start in 2014

MOST ADVANCED SATELLITE DEPOSIT - GORA

Source – Typical section of Gora looking South West, 2012.

9

RESERVES & RESOURCES(1,2)

Deposit

Proven Probable Proven and Probable Tonne

s Grade Au Tonnes Grade Au Tonne

s Grade Au

(Mt) (g/t) (Moz) (Mt) (g/t) (Moz) (Mt) (g/t) (Moz)

Sabodala 6.55 1.5 0.315 11.07 1.24 0.443 17.62 1.34 0.758 Sutuba - - - 0.37 1.40 0.017 0.37 1.40 0.017 Niakafiri 0.23 1.69 0.013 7.58 1.12 0.274 7.81 1.14 0.287 Gora 0.57 4.07 0.074 1.53 4.27 0.21 2.1 4.22 0.284

Stockpiles 7.32 1.02 0.24 - - - 7.32 1.02 0.24

Total 14.67 1.36 0.642 20.56 1.43 0.944 35.23 1.40 1.586

• Reserves remain similar to that of 2011 net of production

• Focused on growing our reserves and are confident that we will add reserves on the ML

• M&I resources increased 34% to 2.9Moz.

(1) Please see page 15 for Competent Persons Statement relating to this reserves estimate. (2) Based on assays received as of August 2012.

Deposit

Measured Indicated Measured and Indicated

Tonnes Grade Au Tonnes

Grade Au Tonne

s Grad

e Au

(Mt) (g/t) (Moz) (Mt) (g/t) (Moz) (Mt) (g/t) (Moz)

Sabodala 28.06 1.24 1.12 31.47 0.96 0.97 59.53 1.09 2.09 Sutuba - - - 0.50 1.27 0.02 0.50 1.27 0.02 Niakafiri 0.30 1.74 0.02 10.50 1.10 0.37 10.70 1.12 0.39 Gora 0.49 5.27 0.08 1.84 4.93 0.29 2.32 5.00 0.37 Total 28.85 1.32 1.22 44.31 1.16 1.65 73.05 1.22 2.87

10

SABODALA PIT – MAIN FLAT EXTENSION /

LOWER FLAT ZONE

SAMBAYA HILL

DINKOKHONO

• Potential to expand gold inventory on ML with the objective of increasing mine life to the year 2020/25

POTENTIAL TO EXPAND THE ML GOLD MINERALIZATION INVENTORY

NIAKAFIRI / NIAKAFIRI WEST / SOUKHOTO

SUTUBA

33km2

11

EXPLORATION - ML • Drill program for the Sabodala pit to be completed in Q1’13

• Targeting new pit design for mid-year

• Conduct an underground analysis in the second half of the year

• Drilling in 2012 extended the Masato mineralized limits defining approximately 700,000oz. of Inferred Resource

• Expect to begin drilling at Niakafiri by mid-year

12

EXPLORATION – RLP • Currently have 10(1) exploration permits ~1,200 km2 of land

surrounding our 33 km2 ML

• 2012 - Over 100,000m drilled, 25 anomalies, $20M

• Highlights from the 2012 drilling program; • Discovery of a new prospect at Tourokhoto-Marougou • Identification of significant mineralization at Saiensoutou

• 2013 budget - $10-15M • Focus is on five priority targets • Other targets will be followed up in 2014

• Committing a minimum budget of $20M for exploration programs on the ML and RLP

(1) The Company’s 11th exploration permit, Sabodala North West, was not renewed by the Government in June 2012. The Company has since appealed this decision and is awaiting a response from the Government

13

SAIENSOUTOU

NINYENKO / SORETO

DIABOUGOU

TOUROKHOTO (Main and Marougou)

1,200km2

35km from Mill

PROPERTIES IN VARYING STAGES OF ASSESSMENT WITHIN RLP

GOUMBOU GAMBA

GORA

14

FOCUS IS ON CONTINUED GROWTH Focused on Growing Reserves

• To secure a reserve life to year 2020/25 • Growth through exploration • Growth through regional opportunities (JV’s, acquisitions)

Focused on Growing Production

• Phase 1: 250,000 – 350,000oz. annual production by leveraging existing mill and land package

• Phase 2: 400,000 – 500,000oz. annual production, will require another mill expansion

Focused on Building Financial Strength

• Eliminating hedge book • Expanding cash margins • Increasing cash balance • Use free cash flow to self-fund growth strategy • Focusing on the ounces that provide the best returns • Increase earning and cash flow per share (minimize dilution)

15

COMPETENT PERSONS STATEMENT The technical information contained in this Report relating to the mineral reserve estimates within the Sabodala, Sutuba, Niakafiri and Gora deposits and the Stockpiles, is based on information compiled by Julia Martin, P.Eng., MAusIMM (CP), a full time employee with AMC Mining Consultants (Canada) Ltd., is independent of Teranga, is a “qualified person” as defined in NI 43-101 and a “competent person” as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Ms. Martin has sufficient experience relevant to the style of mineralization and type of deposit under consideration and to the activity she is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Ms Martin has reviewed and accepts responsibility for the reserve estimates disclosed above. Ms Martin has consented to the inclusion in the report of the matters based on her information in the form and context in which it appears in this Report. The technical information contained in this Report relating to the mineral resources is based on information compiled by Ms. Patti Nakai-Lajoie, who is a Member of the Association of Professional Geoscientists of Ontario. Ms. Patti Nakai-Lajoie is full time employee of Teranga and is not “independent” within the meaning of National Instrument 43-101. Ms. Patti Nakai-Lajoie has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which she is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Ms. Patti Nakai-Lajoie is a “Qualified Person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects.and she consents to the inclusion in the report of the matters based on her information in the form and context in which it appears in this Report. The technical information contained in this Report relating to exploration results is based on information compiled by Mr. Martin Pawlitschek, who is a Member of the Australian Institute of Geoscientists. Mr. Pawlitschek is a consultant of Teranga and is not “independent” within the meaning of National Instrument 43-101. Mr. Pawlitschek has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Mr. Pawlitschek is a “Qualified Person” in accordance with NI 43-101 and he consents to the inclusion in the report of the matters based on his information in the form and context in which it appears in this Report.