Concurrent (India) Infrastructure Limitedim.sify.com/sifycmsimg/jan2010/Finance/14928324... · ·...

20

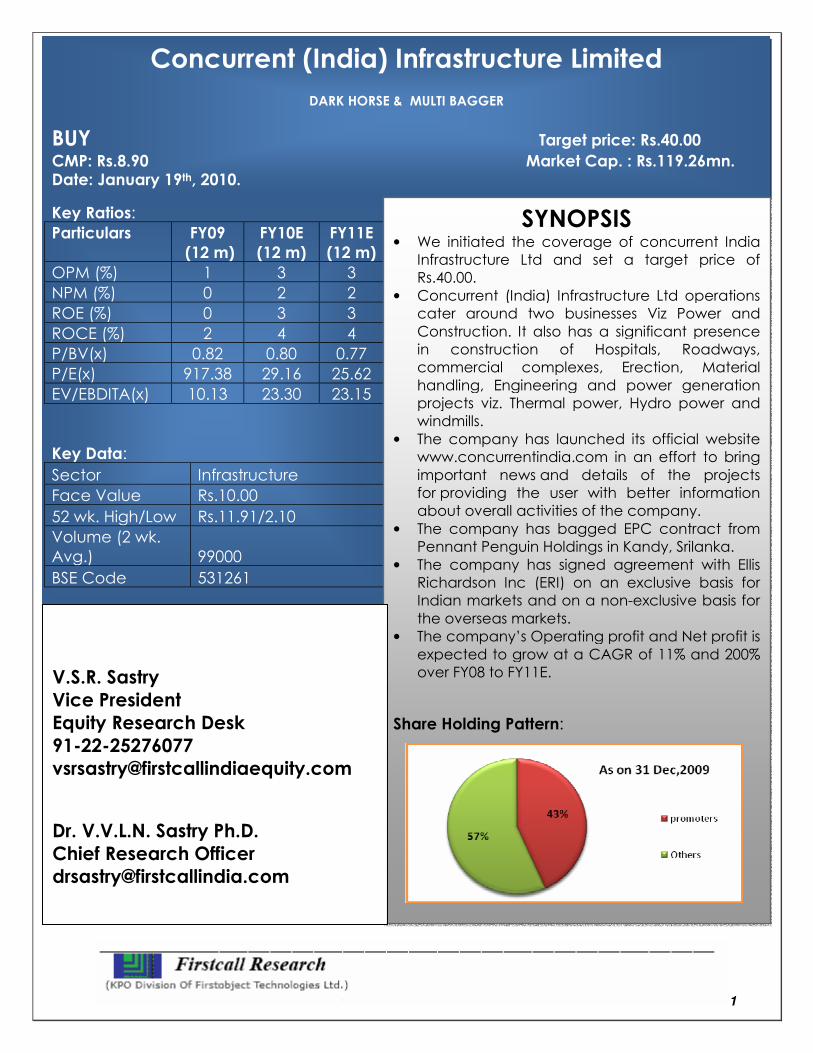

1 Concurrent (India) Infrastructure Limited DARK HORSE & MULTI BAGGER BUY Target price: Rs.40.00 CMP: Rs.8.90 Market Cap. : Rs.119.26mn. Date: January 19 th , 2010. Key Ratios: Particulars FY09 (12 m) FY10E (12 m) FY11E (12 m) OPM (%) 1 3 3 NPM (%) 0 2 2 ROE (%) 0 3 3 ROCE (%) 2 4 4 P/BV(x) 0.82 0.80 0.77 P/E(x) 917.38 29.16 25.62 EV/EBDITA(x) 10.13 23.30 23.15 Key Data: Sector Infrastructure Face Value Rs.10.00 52 wk. High/Low Rs.11.91/2.10 Volume (2 wk. Avg.) 99000 BSE Code 531261 SYNOPSIS • We initiated the coverage of concurrent India Infrastructure Ltd and set a target price of Rs.40.00. • Concurrent (India) Infrastructure Ltd operations cater around two businesses Viz Power and Construction. It also has a significant presence in construction of Hospitals, Roadways, commercial complexes, Erection, Material handling, Engineering and power generation projects viz. Thermal power, Hydro power and windmills. • The company has launched its official website www.concurrentindia.com in an effort to bring important news and details of the projects for providing the user with better information about overall activities of the company. • The company has bagged EPC contract from Pennant Penguin Holdings in Kandy, Srilanka. • The company has signed agreement with Ellis Richardson Inc (ERI) on an exclusive basis for Indian markets and on a non-exclusive basis for the overseas markets. • The company’s Operating profit and Net profit is expected to grow at a CAGR of 11% and 200% over FY08 to FY11E. Share Holding Pattern: V.S.R. Sastry Vice President Equity Research Desk 91-22-25276077 [email protected] Dr. V.V.L.N. Sastry Ph.D. Chief Research Officer [email protected]

Transcript of Concurrent (India) Infrastructure Limitedim.sify.com/sifycmsimg/jan2010/Finance/14928324... · ·...

1

Concurrent (India) Infrastructure Limited

DARK HORSE & MULTI BAGGER

BUY Target price: Rs.40.00 CMP: Rs.8.90 Market Cap. : Rs.119.26mn. Date: January 19th, 2010.

Key Ratios:

Particulars FY09 (12 m)

FY10E (12 m)

FY11E (12 m)

OPM (%) 1 3 3

NPM (%) 0 2 2

ROE (%) 0 3 3

ROCE (%) 2 4 4

P/BV(x) 0.82 0.80 0.77

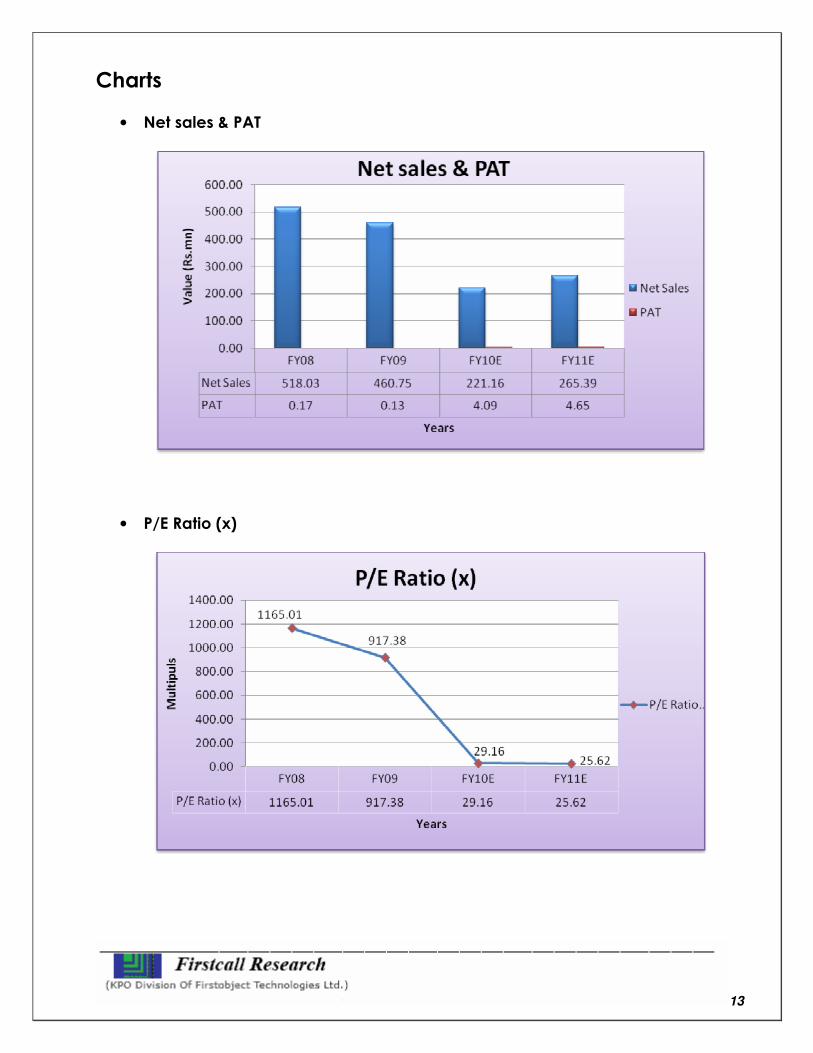

P/E(x) 917.38 29.16 25.62

EV/EBDITA(x) 10.13 23.30 23.15

Key Data:

Sector Infrastructure

Face Value Rs.10.00

52 wk. High/Low Rs.11.91/2.10

Volume (2 wk.

Avg.) 99000

BSE Code 531261

SYNOPSIS • We initiated the coverage of concurrent India

Infrastructure Ltd and set a target price of Rs.40.00.

• Concurrent (India) Infrastructure Ltd operations cater around two businesses Viz Power and

Construction. It also has a significant presence in construction of Hospitals, Roadways, commercial complexes, Erection, Material

handling, Engineering and power generation projects viz. Thermal power, Hydro power and windmills.

• The company has launched its official website www.concurrentindia.com in an effort to bring

important news and details of the projects for providing the user with better information about overall activities of the company.

• The company has bagged EPC contract from Pennant Penguin Holdings in Kandy, Srilanka.

• The company has signed agreement with Ellis Richardson Inc (ERI) on an exclusive basis for Indian markets and on a non-exclusive basis for

the overseas markets. • The company’s Operating profit and Net profit is

expected to grow at a CAGR of 11% and 200% over FY08 to FY11E.

Share Holding Pattern:

V.S.R. Sastry Vice President Equity Research Desk 91-22-25276077 [email protected]

Dr. V.V.L.N. Sastry Ph.D. Chief Research Officer [email protected]

2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Company Profile 07

3. Company products 07

4. Peer Group Comparison 09

5. Key Concerns 09

6. Financials 10

7. Charts & Graph 12

8. Outlook and Conclusion 14

9. Industry Overview 15

3

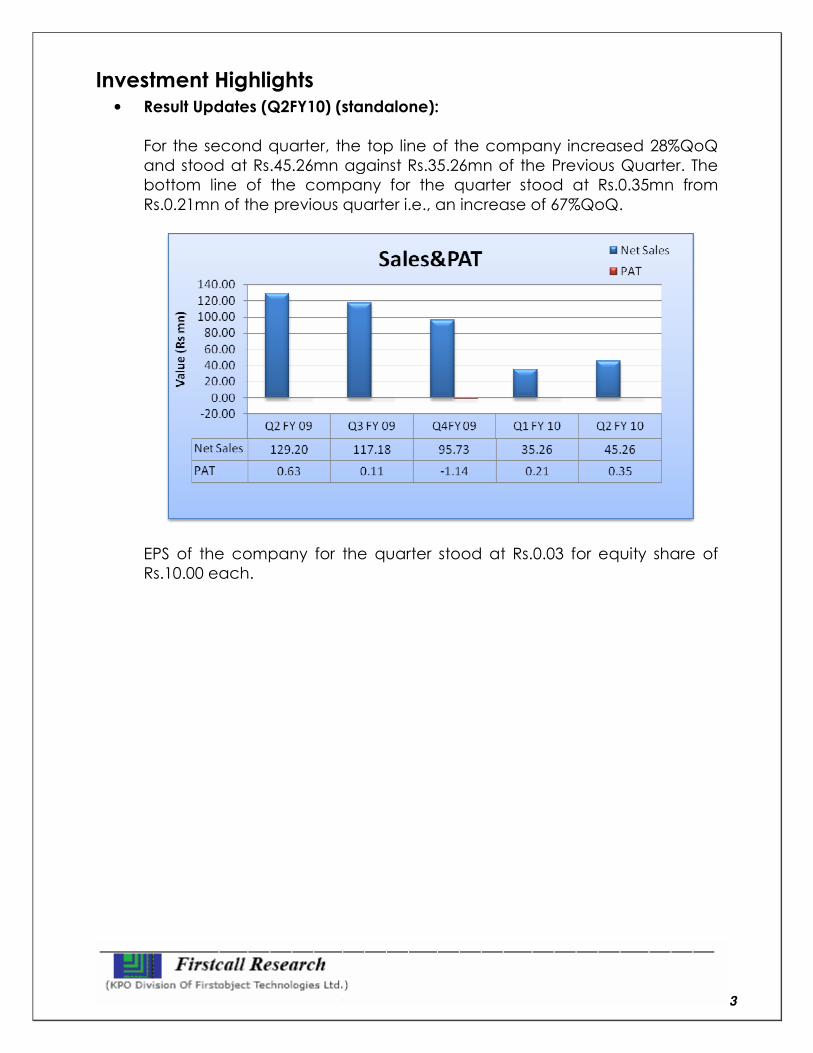

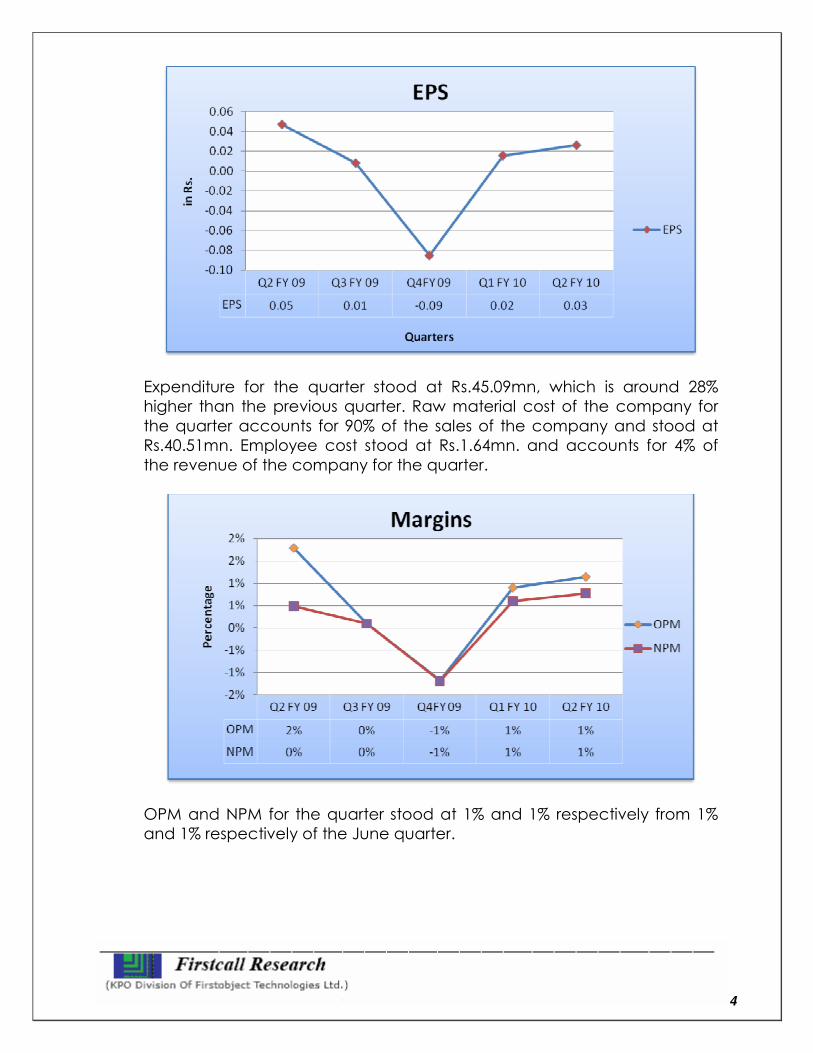

Investment Highlights • Result Updates (Q2FY10) (standalone):

For the second quarter, the top line of the company increased 28%QoQ

and stood at Rs.45.26mn against Rs.35.26mn of the Previous Quarter. The bottom line of the company for the quarter stood at Rs.0.35mn from

Rs.0.21mn of the previous quarter i.e., an increase of 67%QoQ.

EPS of the company for the quarter stood at Rs.0.03 for equity share of

Rs.10.00 each.

4

Expenditure for the quarter stood at Rs.45.09mn, which is around 28%

higher than the previous quarter. Raw material cost of the company for

the quarter accounts for 90% of the sales of the company and stood at Rs.40.51mn. Employee cost stood at Rs.1.64mn. and accounts for 4% of

the revenue of the company for the quarter.

OPM and NPM for the quarter stood at 1% and 1% respectively from 1%

and 1% respectively of the June quarter.

5

• Concurrent India launches its official website

The company has launched its official website www.concurrentindia.com

in an effort to bring important news and details of the projects

for providing the user with better information about overall activities of the

company.

With the help of this website, the company is planning to widen its reach

to its shareholders and create awareness among them.

• Concurrent India receives EPC contract from Pennant Penguin Holding

The company has bagged EPC contract from Pennant Penguin Holdings

in Kandy, Srilanka. The contract involves setting up of 30 MW power

project which is expected to be executed in over a span of 24 months.

• Concurrent India plans to float a preferential issue

The company is looking to float a preferential issue at Rs 15 per share for

the purpose of acquisition of land for logistics business. The company has

identified land of 25 acres near Hyderabad City for the purpose of setting

up logistics supply chain.

• Concurrent India bags Rs. 22crore worth order from Sreenidhi Constructions

The company has bagged a sub-contract worth Rs 22crore from Sreenidhi

Constructions, Belgaum, Karnataka. The contract involves execution of

modernization of distributaries and lateral lining and rehabilitation of

structures coming under Davangere branch canal (30 kilometer). The

project is expected to be completed in 12 months.

• Concurrent India ties up with ERI

The company has signed agreement with Ellis Richardson Inc (ERI) on an

exclusive basis for Indian markets and on a non-exclusive basis for the overseas markets.

Under this collaboration ERI will transfer and impart technical know-how

for turnkey implementation of power plant to Concurrent. ERI will also offer

6

technical and commercial assistance in initial phase of this collaboration.

The agreement is for the duration of three years and also has scope to be

extended for further period.

• Concurrent India plans to acquire 4.15 MW power project

The company has submitted its bid for acquisition of 4.15 MW power

project in the state of Andhra Pradesh. The project is a Mini Hydro Electric

Power Plant. The cost of the project is Rs. 23crore.

• Concurrent India looking to acquire 320 perches land in Sri Lanka

Concurrent (India) Infrastructure (earlier Kushagra Software) is looking to

acquire 320 perches land in Sri Jayewardenepura Kotte, Colombo, Sri

Lanka.

The company has entered into a transaction with Sino-Lanka, a local

entity, for the said acquisition. Further, Sino-Lanka has agreed to transfer

the rights of the land to the company and has also agreed to co-operate

in the necessary documentation and expressed its willingness to assist with

the government authorities namely UDA and BOI.

• Concurrent India receives project from Sreenidhi Constructions

Concurrent (India) Infrastructure (earlier Kushagra Software) has bagged

a deal worth Rs 20crore for waterways works from Sreenidhi Constructions.

The contract involves designing, supply, erection, testing, commissioning

and construction of canal works of Gddada Mallapur UN-Irrigation

scheme in Bydagi Taluq in Haven district of Karnataka. The contract is

expected to be completed within 12 months.

• Concurrent India bags work order worth $3.5 million

Concurrent (India) Infrastructure (earlier Kushagra Software) has bagged

a power project works order worth $3.5 million. The order is scheduled for

completion over a period of next 12 months.

• Kushagra Software pilot power project in Sri Lanka meets with success

7

Concurrent (India) Infrastructure (formerly known as Kushagra Software),

which launched a pilot project for power generation in the Negombo

beach region of Sri Lanka, has announced that the pilot was successful.

As per the technology used, one wind wheel is capable of illuminating

fifty/sixty watt bulbs. In the case of domestic needs, one wind wheel is

capable of supplying electricity needs of two bedroom rural houses. The

technology used by Concurrent is environmental friendly as there is no

pollution involved in it. Also, a distinct feature of this technology used by

Concurrent is that power could be generated with low speed winds unlike

in the usual wind power generation technology where high speed winds

are needed to generate power.

• Kushagra Softwar receives court’s nod for merger

Kushagra Software has received the Bombay High Court’s approval for

merger of Concurrent Infrastructure -- a private limited company -- with

Concurrent (India) Infrastructure.

Concurrent (India) Infrastructure was formerly known as Kushagra

Software. This merger will bring into the fold of the company, the order

book pipeline for infrastructure projects and developmental rights. The

company received a letter of intent for doing a pilot project for area

Negombo Beach Project from the Ministry of Road Development, Housing

& Construction of Western Provincial Council, Sri Lanka

Company profile Concurrent (India) Infrastructure Ltd operations cater around two businesses Viz

Power and Construction. Concurrent is a diversified business entity with a

predominant focus on urban infrastructure projects. It also has a significant

presence in construction of Hospitals, Roadways, commercial complexes,

Erection, Material handling, Engineering and power generation projects viz. Thermal power, Hydro power and windmills. Concurrent was incorporated in the

year 1994, it started as a real estate developer and majority diversified into

infrastructure in the year 2007. The company, formerly known as Kushagra

Software Limited, is based in Navi Mumbai, India.

Business Areas

8

• WindMill

• Hydeo Power

• Engineering

• Real Estate

Power Hydropower

Concurrent has established a leadership position in the Hydro Power sector.

Concurrent diversified its construction capabilities to build and serve the entire

segment viz. Dams, Barrages, Tunnels, Underground Power Stations, Surface

Power Stations along with Water conductor Systems like Surge Shafts, Pressure

Shafts and Penstocks are all now part of the Concurrent repertoire.

Concurrent has unrivalled expertise in large power production, where precision

of the work is a vital factor along with the quality of concrete used. With its

thorough knowledge and commitment to quality Concurrent undertakes such

projects on Engineering Procurement and Construction (EPC) basis as well.

Windmill

The Wind energy industry is currently characterized by growing demand, limited

by a restricted supply. With the windmills steadily increasing their stake in the

energy sector, coupled with hike in electricity tariffs and escalating energy

consumption, the market of customized small-windmill makers for households

9

has approximate 30 per cent annual growth, and is likely to throw a huge

market across the country.

Concurrent explores new grounds and taps into this developing segment.

Concurrent’s turnkey services range from complex front-end engineering design,

construction, installation and commissioning to long-term operations and

maintenance as well as the length breadth and depth of customer

requirements across the wind energy value chain. Prior to chat Concurrent

performs Viability Study on location, geographical condition and feasibility of

the project. The key difference lies in having both strong front-end engineering

and the benefit of local experience, interface management and construction

know how.

Construction Concurrent undertakes turnkey projects of Design and Construction of

commercial complexes, Centres like Shopping Malls and Retail outlets and large

residential & commercial complexes. Its capability encompasses design and

construction. Concurrent takes pride in its structural framework including finishing

and interior works and electro-mechanical services. Concurrent offers

Engineering, Procurement and Construction (EPC) Services include terminal

buildings, visitor’s lounges, etc. Concurrent specializes in building all types of

bridges in various span ranges, using innovative and sophisticated construction

techniques.

Which include: • Incremental Launching

• Segment construction • Cables stayed

• Pre-cast, pre-stressed

• Steel, concrete composite construction

Engineering: The Engineering Procuring and Construction market in India has undergone

significant changes and it has affected both government agencies and private

investment projects. Concurrent will continue to grow its successful construction

operations profitably whilst expanding its EPC capabilities and acquitting/

executing in an increasing number. These projects will come from the key

sectors currently addressed by Concurrent including Hydro, Water, Nuclear and

Thermal as well as Transport and Integrated Infrastructure projects. These EPC

10

skills and capabilities will also be utilized to support Concurrent’s own investment

projects on Build, Operate & Transfer (BOT) basis.

A Key feature of large and complex EPC projects is the requirement to integrate

the right partners to tackle the engineering, equipment and material supply and

specialized construction subcontractors to meet the project objective.

Commercially this may feature joint ventures or consortia but the key is for the

Concurrent project management team to integrate with the partners to tackle

the challenges of shorter schedules and tighter budgets along with the key

requisites of safety, quality and sound environmental practice as well as

increased interface management.

Peer Group Comparison Name of the company

CMP(Rs.) (As on January 19th,2010)

Market Cap.

(Rs. Mn.)

EPS (Rs.)

P/E (x)

P/BV (x)

Dividend (%)

Concurrent

infrastructure Ltd 8.90 119.26 0.01 - 0.86 0.00

GMR Infrastructures Ltd 67.65 247913.2 0.13 520.00 4.34 0.00

Unitech Ltd 87.30 208900.7 1.22 71.88 6.93 5.00

Era Infra Engineering Ltd 210.70 37655.9 16.70 12.62 4.30 20.00

Key Concerns

� Heightened competition

� Increasing cost of the product

11

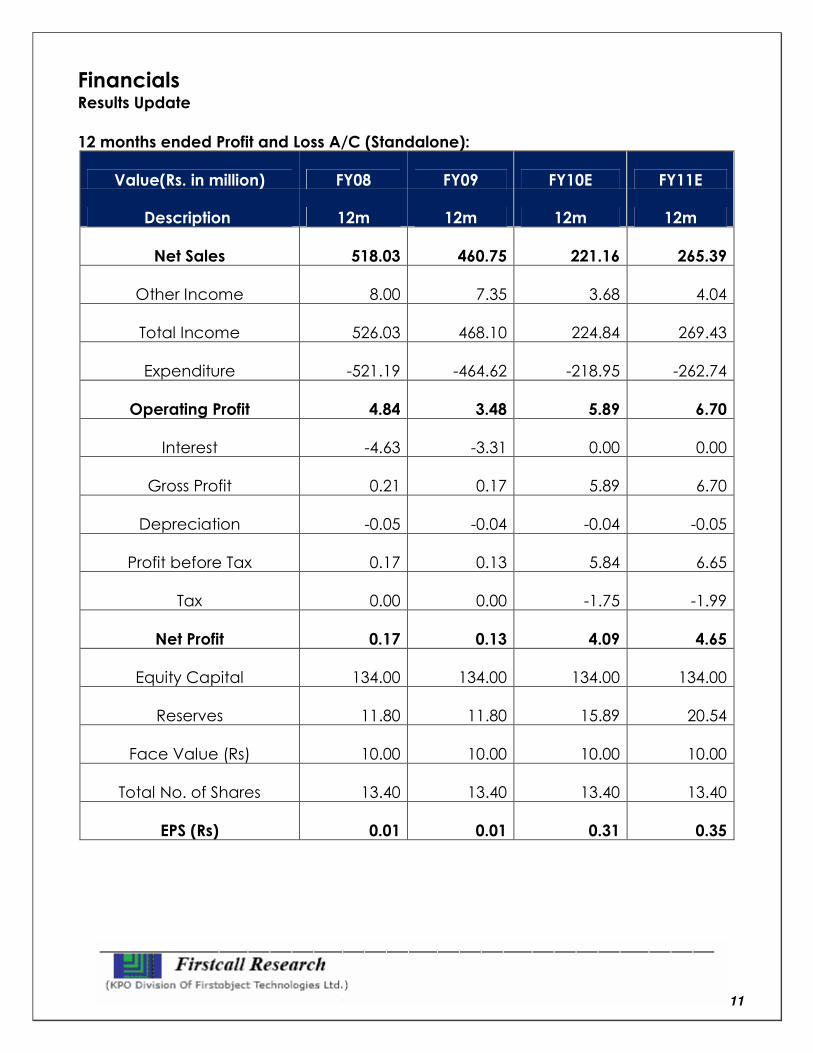

Financials Results Update 12 months ended Profit and Loss A/C (Standalone):

Value(Rs. in million) FY08 FY09 FY10E FY11E

Description 12m 12m 12m 12m

Net Sales 518.03 460.75 221.16 265.39

Other Income 8.00 7.35 3.68 4.04

Total Income 526.03 468.10 224.84 269.43

Expenditure -521.19 -464.62 -218.95 -262.74

Operating Profit 4.84 3.48 5.89 6.70

Interest -4.63 -3.31 0.00 0.00

Gross Profit 0.21 0.17 5.89 6.70

Depreciation -0.05 -0.04 -0.04 -0.05

Profit before Tax 0.17 0.13 5.84 6.65

Tax 0.00 0.00 -1.75 -1.99

Net Profit 0.17 0.13 4.09 4.65

Equity Capital 134.00 134.00 134.00 134.00

Reserves 11.80 11.80 15.89 20.54

Face Value (Rs) 10.00 10.00 10.00 10.00

Total No. of Shares 13.40 13.40 13.40 13.40

EPS (Rs) 0.01 0.01 0.31 0.35

12

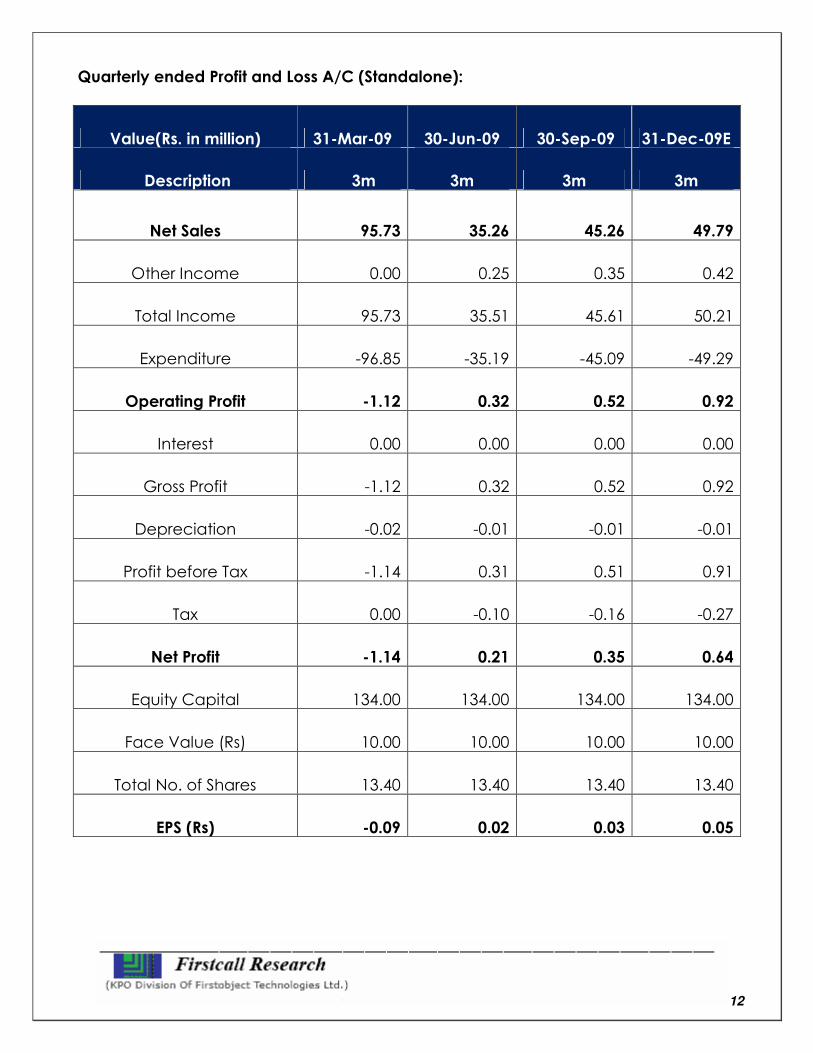

Quarterly ended Profit and Loss A/C (Standalone):

Value(Rs. in million) 31-Mar-09 30-Jun-09 30-Sep-09 31-Dec-09E

Description 3m 3m 3m 3m

Net Sales 95.73 35.26 45.26 49.79

Other Income 0.00 0.25 0.35 0.42

Total Income 95.73 35.51 45.61 50.21

Expenditure -96.85 -35.19 -45.09 -49.29

Operating Profit -1.12 0.32 0.52 0.92

Interest 0.00 0.00 0.00 0.00

Gross Profit -1.12 0.32 0.52 0.92

Depreciation -0.02 -0.01 -0.01 -0.01

Profit before Tax -1.14 0.31 0.51 0.91

Tax 0.00 -0.10 -0.16 -0.27

Net Profit -1.14 0.21 0.35 0.64

Equity Capital 134.00 134.00 134.00 134.00

Face Value (Rs) 10.00 10.00 10.00 10.00

Total No. of Shares 13.40 13.40 13.40 13.40

EPS (Rs) -0.09 0.02 0.03 0.05

13

Charts

• Net sales & PAT

• P/E Ratio (x)

14

• P/BV (X)

• EV/EBITDA(X)

1 Year Comparative Graph

15

Outlook and Conclusion

• At the market price of Rs.8.90, the stock is trading at 29.16 x and 25.62 x for

FY10E and FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 23.30 x for FY10E and 23.15 x

for FY11E.

• Price to book value of the company is expected to be at 0.80 x for FY10E

and 0.77 x for FY11E respectively.

• EPS of the company is expected to be at Rs.0.31 and Rs.0.34 for the

earnings of FY10E and FY11E respectively.

• The company’s Operating profit and Net profit is expected to grow at a

CAGR of 11% and 200% over FY08 to FY11E.

• The company has launched its official website www.concurrentindia.com

in an effort to bring important news and details of the projects

Concurrent India Ltd BSE SENSEX

16

for providing the user with better information about overall activities of the

company.

• The company has bagged EPC contract from Pennant Penguin Holdings

in Kandy, Srilanka. The contract involves setting up of 30 MW power

project which is expected to be executed in over a span of 24 months.

• The company is looking to float a preferential issue at Rs 15 per share for

the purpose of acquisition of land for logistics business. The company has

identified land of 25 acres near Hyderabad City for the purpose of setting

up logistics supply chain.

• The company has bagged a sub-contract worth Rs 22crore from Sreenidhi

Constructions, Belgaum, Karnataka.

• The company has signed agreement with Ellis Richardson Inc (ERI) on an

exclusive basis for Indian markets and on a non-exclusive basis for the

overseas markets.

• The company has submitted its bid for acquisition of 4.15 MW power

project in the state of Andhra Pradesh. The project is a Mini Hydro Electric

Power Plant. The cost of the project is Rs. 23crore.

• The company is looking to acquire 320 perches land in Sri

Jayewardenepura Kotte, Colombo, Sri Lanka.

• The company launched a pilot project for power generation in the

Negombo beach region of Sri Lanka, has announced that the pilot was

successful.

• We recommend ‘BUY’ with a target price of Rs.40.00 for long term.

Industry overview The Indian real estate sector plays a significant role in the country’s economy.

The real estate sector is second only to agriculture in terms of employment

generation and contributes heavily towards the gross domestic product (GDP).

Almost five per cent of the country's GDP is contributed to by the housing sector.

17

In the next five years, this contribution to the GDP is expected to rise to 6 per

cent.

According to Jones Lang LaSalle, faster economic growth in Brazil, Russia, India

and China (BRIC) could result in the property markets of those nations

recovering at a faster rate than the UK and US real estate markets. It has also

been suggested that India's property sector could begin to improve from late

2009 and may attract up to US$ 12.11 billion in real estate investment over a five-

year period.

The information technology (IT) and IT-enabled services (ITES) sector alone is

estimated to require 150 million sq ft of office space across urban India by 2010.

Organized retail is also responsible for the growth in commercial office space

requirement. The organized retail industry is likely to require an additional 220

million sq ft by 2010. Moreover, growth is not restricted to a few towns and cities

but is pan-India, covering nearly all Tier-I and Tier-II cities.

Almost 80 per cent of real estate developed in India is residential space, the rest

comprises of offices, shopping malls, hotels and hospitals. According to the

Tenth Five Year Plan, there is a shortage of 22.4 million dwelling units. Thus, over

the next 10 to 15 years, 80 to 90 million housing dwelling units will have to be

constructed with a majority of them catering to middle- and lower-income

groups. Moreover, India leads the pack of top real estate investment markets in

Asia for 2010, according to a study by PricewaterhouseCoopers (PwC) and

Urban Land Institute, a global non-profit education and research institute.

The report, which provides an outlook on Asia-Pacific real estate investment and

development trends, points out that India, particularly Mumbai and Delhi, are

good destinations. Residential properties are viewed as more promising than

other sectors and Mumbai, Delhi and Bangalore top the pack in the hotel ‘buy'

prospects as well. The study is based on the opinions of over 270 international

real estate professionals, including investors, developers, property company

representatives, lenders, brokers and consultants. Apart from the huge demand,

India also scores on the construction front. A McKinsey report reveals that the

average profit from construction in India is 18 per cent, which is double the

profitability for a construction project undertaken in the US.

The real estate sector is also likely to get a boost from Real Estate Mutual Funds

(REMFs) and Real Estate Investment Trusts (REITs). In fact, according to a CRISIL

paper, the REITs would have the potential to hold at least 5 per cent share of the

total global real estate market by 2010, the size of which would reach US$ 1,400

18

billion in the next three years. The paper titled, ‘Indian REITs; Are We Prepared',

says that by 2010, REITs alone would hold a market size of US$ 70 billion of the

total real estate market as its concept is gaining ground in countries like India

and other developing nations.

According to the Federation of Indian Chambers of Commerce and Industry

(FICCI), the Indian real estate sector is likely to experience consolidation wherein

bigger players may opt for outright buy of smaller firms or forge joint ventures or

business alliances with them.

Foreign direct investment (FDI) into India in the real estate sector for the fiscal

year 2008-09 has been US$ 12.62 billion approximately, according to the latest

data given by the Department of Policy and Promotion (DIPP). Moreover,

buoyed by positive market sentiment and demand revival in housing, four real

estate companies—Emaar MGF Land, Lodha Developers, Sahara Prime City and

Ambience Ltd—are looking to mop-up over US$ 2.35 billion through public

offerings.

New Projects

• Zuri Group Global is planning to invest about US$ 247.5 million towards

setting up five-star business hotels and luxury residential properties over the

next three years.

• Accor Hospitality, the largest hotel chain in Europe, with 4,000 hotels in 90

countries will invest US$ 130 million to come up with 50 hotels in India by

2012.

• An investment of US$ 627.3 million will be made by industries in the

Aeropsace and Precision Engineering Special Economic Zone at Adibatla,

Andhra Pradesh.

• Shriram Properties, part of Chennai-headquartered diversified Shriram

Group, is planning to invest around US$ 1.02 billion in various residential

and commercial projects.

• Unitech will invest US$ 853.42 million in construction of up to 30 million sq ft

of residential and commercial spaces to be launched by next year.

Government Initiatives

19

The government has introduced many progressive reform measures to unlock

the potential of the sector and also meet increasing demand levels. The stimulus

package announced by the government, coupled with the Reserve Bank of

India's (RBI) move allowing banks to provide special treatment to the real estate

sector, is likely to impact the Indian real estate sector in a positive way. RBI has

decided to extend exceptional concessional treatment to the commercial real

estate exposure which are restructured, up to June 30, 2009.

• 100 per cent FDI allowed in realty projects through the automatic route.

• In case of integrated townships, the minimum area to be developed has

been brought down to 25 acres from 100 acres.

• Urban Land (Ceiling and Regulation) Act, 1976 (ULCRA) repealed by

increasingly larger number of states.

• Minimum capital investment for wholly-owned subsidiaries and joint

ventures stands at US$ 10 million and US$ 5 million, respectively.

• Full repatriation of original investment after three years.

• 51 per cent FDI allowed in single-brand retail outlets and 100 per cent in

cash-and-carry through the automatic route.

The 2009-10 budget has also given sops to the realty sector. Developers of

affordable housing projects (units of 1,000-1,500 sq ft) have been granted a tax

holiday on profits from projects initiated in the financial year 2007-08. Such

projects would have to be completed before March 1, 2012.

At the same time, the finance minister allocated US$ 207 million to grant a 1 per

cent interest subsidy on home loans up to US$ 20,691, provided the cost of the

home is not more than US$ 41,382. This subsidy is expected to give a further

boost to the housing sector. ___________________________________________________________ Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but we do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

20

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

Other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com