Conceptual framework. Academic Resource Center Conceptual framework Page 2 Executive summary ► The...

47

Conceptual framework

-

Upload

vivien-logan -

Category

Documents

-

view

225 -

download

0

Transcript of Conceptual framework. Academic Resource Center Conceptual framework Page 2 Executive summary ► The...

Conceptual framework

Academic Resource Center

Conceptual framework Page 2

Executive summary

► The development of the Conceptual Framework is one of the most critical aspects in the convergence of US GAAP and IFRS as converged and new standards become more principles based and less prescriptive in nature. A sound conceptual framework becomes essential to ensuring that standard setters agree on the underlying concepts and definitions before developing converged standards.

► In September 2010, both the FASB and the IASB issued converged chapters dealing with the objectives of financial reporting and the qualitative characteristics of useful financial information. The chapters, which supersede the FASB Financial Accounting Concept Statements (SFACs) No. 1 and No. 2 and paragraphs 1 through 22 and 24 through 46 in the IASB Framework, are identical.

► The objective of financial reporting is to provide useful financial information to the primary users of financial statements (investors, lenders and creditors). The qualitative characteristics of useful financial information identify fundamental characteristics, enhancing characteristics and pervasive constraint. These characteristics are essentially unchanged from the previous concept statement and framework, but are presented in a more straightforward and condensed manner.

Academic Resource Center

Conceptual framework Page 3

Executive summary

► The Convergence Project continues to progress with the final version of a new chapter on Reporting Entity expected in the first quarter of 2011. Phase B – Elements and Recognition, and Phase C – Measurement, are continuing, with an ED on Phase C – Measurement, expected in the latter half of 2011. Phases E through H have not yet been started.

► SFACs No. 5, 6 and 7 and the IASB Framework, paragraphs 23 and 47 through 110, now a part of Chapter 4 of the Conceptual Framework for Financial Reporting, are still applicable and, accordingly, they are presented in the latter half of this module.

► The FASB Conceptual Framework is not a part of the US GAAP hierarchy and is thus not authoritative at this time. The FASB may deliberate this issue in the future. The IASB Conceptual Framework is a third level of accounting to be followed in the IFRS hierarchy.

Academic Resource Center

Conceptual framework Page 4

Primary pronouncements

US GAAP► SFAC No. 5, Recognition and

Measurement in Financial Statements of Business Enterprises

► SFAC No. 6, Elements of Financial Statements

► SFAC No. 7, Using Cash Flow Information and Present Value in Accounting Measure

► SFAC No. 8, Conceptual Framework for Financial Reporting, Chapters 1 and 3

IFRS► IASB, Conceptual Framework for

Financial Reporting (September 2010)► IAS 8, Accounting Policies, Changes in

Accounting Estimates and Errors

Academic Resource Center

Conceptual framework Page 5

FASB► The Conceptual Framework was developed

between 1974 and 2000 and included six separate Concept Statements addressing Objectives of Financial Reporting, Qualitative Characteristics of Accounting Information, Elements of Financial Statements, Recognition and Measurement in Financial Statements of Business Enterprises, Objectives of Financial Reporting by Non-business Organizations and Using Cash Flow Information and Present Value in Accounting Measure.

IASB► The Framework for the Preparation and

Presentation of Financial Statements was issued in 1989 and dealt with substantively the same issues as the FASB Concept Statements, with some differences in Qualitative Characteristics, Elements and Recognition and Measurement.

OverviewPrior to September 2010

Academic Resource Center

Conceptual framework Page 6

► In 2002 the FASB and the IASB agreed to make their accounting standards compatible, including the Conceptual Framework as spelled out in the Norwalk Agreement.

► The Conceptual Framework convergence project was broken into eight phases as follows:► Phase A – Objectives and Qualitative Characteristics► Phase B – Elements and Recognition► Phase C – Measurement► Phase D – Reporting Entity Concept► Phase E – Presentation and Disclosure► Phase F – Framework Purpose and Status in US GAAP► Phase G – Applicability to the Not-for-Profit Sector► Phase H – Remaining Issues

OverviewPrior to September 2010

Academic Resource Center

Conceptual framework Page 7

► In September 2010, the FASB issued SFAC No. 8, Conceptual Framework for Financial Reporting. This concept statement includes two chapters, Chapter 1, “The Objective of General Purpose Financial Reporting,” and Chapter 3, “Qualitative Characteristics of Useful Financial Information.” SFAC No. 8 supersedes SFAC No. 1 and SFAC No. 2.

► Simultaneously, in September 2010, the IASB issued Chapter 1, “The Objective of General Purpose Financial Reporting” and Chapter 3, “Qualitative Characteristics of Useful Financial Information,” which replace the Preface and Introduction as well as paragraphs 1 through 22 and 24 through 46 in the IASB’s Framework for the Preparation and Presentation of Financial Statements. The remaining text of the Framework is included as Chapter 4, “The Framework (1989): the remaining text” in the new IASB Conceptual Framework for Financial Reporting. ► Chapters 1 and 3 are identical in FASB SFAC No. 8, Conceptual Framework for Financial

Reporting, and in the IASB’s Conceptual Framework for Financial Reporting.

OverviewSubsequent to September 2010 (convergence)

Academic Resource Center

Conceptual framework Page 8

► As additional phases of the Conceptual Framework convergence project are completed, additional chapters will be added to the FASB’s SFAC No. 8 and the previous Concept Statements superseded. Additional paragraphs and chapters will also be added to the IASB’s Conceptual Framework replacing the remaining text of the Framework.

► The Boards are continuing to work on Phases B, C and D (Elements and Recognition, Measurement and Reporting Entity, respectively). A final chapter of Phase D is expected in the first quarter of 2011 and an ED for Phase C is expected in the latter half of 2011. Phase B is still in progress and Phases E to H are yet to be started.

OverviewSubsequent to September 2010 (convergence)

Academic Resource Center

Conceptual framework Page 9

► The FASB has stated that, “The concept statements are intended to set forth objectives and fundamental concepts that will be the basis for development of financial accounting and reporting guidelines. The objectives identify the goals and purposes of financial reporting. The fundamentals are the underlying concepts of financial accounting, concepts that guide the selection of transactions and other events and conditions to be accounted for; their recognition and measurement; and the means of summarizing and communicating them to intended parties.”1

► The FASB has also stated that, “The Conceptual Framework is a coherent system of interrelated objectives and fundamental concepts that prescribe the nature, function, and limits of financial accounting and reporting and that is expected to lead to consistent guidance.”2

1SFAC No. 8, Conceptual Framework for Financial Reporting, introduction, paragraph 2.2Ibid, introduction, paragraph 3.

Purpose of the concept statements

Academic Resource Center

Conceptual framework Page 10

► “The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders, and creditors (‘primary users’) in making decisions about providing resources to the entity. Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans and other forms of credit.”3 ► Consequently, primary users need information to help them assess the prospects of future net cash

inflows to an entity.► To assess an entity’s prospects for future cash inflows, primary users need information about the

resources of the entity, claims against the entity and how efficiently and effectively the entity’s management and governing board have discharged the responsibilities to use the entity’s resources. Many primary users cannot require reporting entities to provide information directly to them and thus must rely on general purpose financial statements for much of the financial information they need.

► General purpose financial reports do not and cannot provide all the information that primary users need, therefore, pertinent information from other sources needs to be considered, such as general economic conditions, political events and climate and industry outlook.

3SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 1, “The Objective of General Purpose Financial Reporting,” OB2.

Overview of Chapter 1, “The Objective of General Purpose Financial Reporting”

Academic Resource Center

Conceptual framework Page 11

► Continued:► General purpose financial statements are not designed to show the value of the reporting entity, are not

designed for the sole use of management and are not directed towards regulators or other parties that are not primary users.

► Individual primary users have different and possibly conflicting information needs and desires. Therefore, the preparation of financial reporting standards will seek to provide the information set that will meet the needs of the maximum number of primary users.

► “To a large extent, financial reports are based on estimates, judgments, and models rather than exact depictions. The Conceptual Framework establishes the concepts that underlie those estimates, judgments, and models.”4

4SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 1, “The Objective of General Purpose Financial Reporting,” OB11.

Overview of Chapter 1, “The Objective of General Purpose Financial Reporting”

Academic Resource Center

Conceptual framework Page 12

► Information about a reporting entity’s economic resources, claims and changes in resources and claims:► “General purpose financial reports provide information about the financial position of a reporting entity, which is

information about the entity’s economic resources and claims against the reporting entity. Financial reports also provide information about the effects of transactions and other events that change a reporting entity’s economic resources and claims.”5

► Economic resources and claims:► Information about the nature and amounts of a reporting entity’s economic resources and claims can help users to identify the

reporting entity’s financial strength, weaknesses, liquidity, solvency, needs for additional financing and future cash flows.► Changes in economic resources and claims

► “Changes in economic resources and claims result from an entity’s financial performance and from other events or transactions, such as issuing debt or equity instruments.” 6

► Information about a reporting entity’s financial performance: ► Helps users understand the return that the entity has produced on its economic resources. ► Helps users understand how well management has discharged its responsibilities.► Provides information about variability and components of return. ► Is a predictor of an entity’s future returns on its economic resources.

5SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 1, “The Objective of General Purpose Financial Reporting,” OB12.6Ibid, OB15.

Overview of Chapter 1, “The Objective of General Purpose Financial Reporting”

Academic Resource Center

Conceptual framework Page 13

► Financial performance reflected by accrual accounting:► Accrual accounting provides a better basis than cash receipts and payments for assessing a reporting

entity’s economic resources and claims and changes in economic resources and claims during a period.► “Information about a reporting entity’s financial performance during a period, reflected by changes in its

economic resources and claims, other than by obtaining additional resources directly from investors and creditors, is useful in assessing the entity’s past and future ability to generate net cash from its operations.”7

► Information about a reporting entity’s financial performance during a period may also indicate the extent to which events such as changes in market prices or interest rates have increased or decreased the entity’s economic resources and claims, which would affect net cash flows.

► Financial performance reflected by past cash flows:► Information about a reporting entity’s cash flows during a period also helps users to assess:

► The entity’s ability to generate future net cash inflows. ► The ability to obtain and spend cash, including borrowings and repayment of debt, cash dividends

and distributions to investors and other factors that affect liquidity or solvency.7SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 1, “The Objective of General Purpose Financial Reporting,” OB18.

Overview of Chapter 1, “The Objective of General Purpose Financial Reporting”

Academic Resource Center

Conceptual framework Page 14

► Changes in economic resources and claims not resulting from financial performance:► “Economic resources and claims may also change for reasons other than financial performance, such

as issuing additional ownership shares.”8

► “Information about this type of change is necessary to give users a complete understanding of why the reporting entity’s economic resources and claims changed and their implications on future financial performance.”9

8SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 1, “The Objective of General Purpose Financial Reporting,” OB21.9Ibid.

Overview of Chapter 1, “The Objective of General Purpose Financial Reporting”

Academic Resource Center

Conceptual framework Page 15

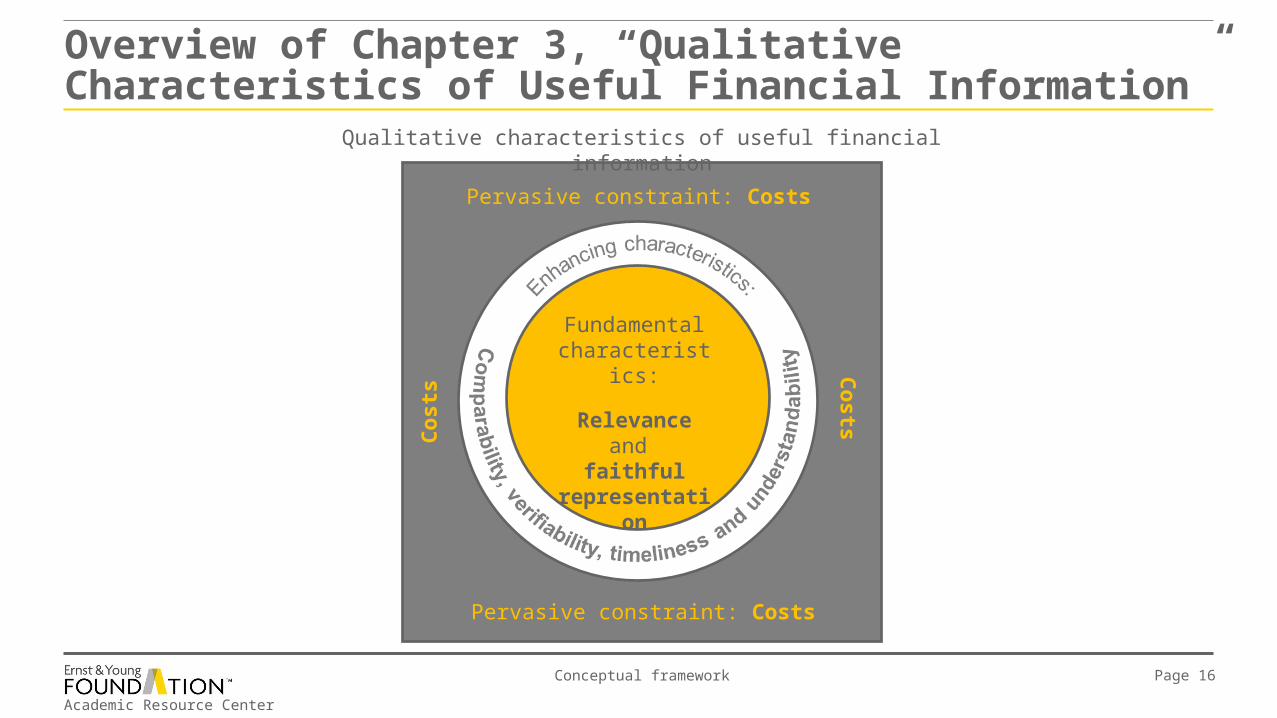

► Introduction:► “The qualitative characteristics of useful financial information identify the types of information that are

likely to be most useful to the existing and potential investors, lenders, and other creditors for making decisions about the reporting entity on the basis of information in its financial reports.”10

► “Financial reports provide information about the reporting entity’s economic resources, claims against the reporting entity, and the effects of transactions and other events and conditions that change those resources and claims. This is referred to in the Conceptual Framework as information about economic phenomena.”11

► “The qualitative characteristics of useful financial information apply to financial information provided in financial statements, as well as to financial information provided in other ways.”12

► “To be useful, financial information must be relevant and faithfully represent what it purports to represent. Financial information is enhanced if it is comparable, verifiable, timely and understandable.”13

► Cost, which is a pervasive constraint on the reporting entity’s ability to provide useful financial information, is applied similarly.

10SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 3, “Qualitative Characteristics of Useful Financial Information,” QC1.11Ibid, QC2.12Ibid, QC3.13Ibid.

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Academic Resource Center

Conceptual framework Page 16

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Pervasive constraint: Costs

Fundamental characteristics:

Relevance and

faithful representation

Qualitative characteristics of useful financial information

Co

sts

Co

sts

Pervasive constraint: Costs

Academic Resource Center

Conceptual framework Page 17

► Qualitative characteristics of useful financial information:► Fundamental qualitative characteristics include relevance and faithful representation:

► Relevance: relevant financial information is/has:► Capable of making a difference in the decisions made by users.► Capable of making a difference in decisions if it has predictive value, confirming value or both.► Predictive value for users of financial information. ► Confirmatory value about previous evaluations.

► Materiality:► “Materiality is an element of relevance and is entity-specific based on the nature or magnitude or both of the items to which the information relates,

in the context of an individual entity’s financial report.”14

► “Information is material if omitting it or misstating it could influence decisions that users make on the basis of the financial information of a specific reporting entity.”15

14SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 3, “Qualitative Characteristics of Useful Financial Information,” QC11.15Ibid.

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Academic Resource Center

Conceptual framework Page 18

► Qualitative characteristics of useful financial information (continued):► Fundamental qualitative characteristics include relevance and faithful representation

(continued):► Faithful representation: “Financial reports represent economic phenomena in words and numbers. To

be useful, financial information must be relevant but also must faithfully represent the phenomena that it purports to represent.”16 The characteristics of faithful representation include:► Completeness: “all information that is necessary for a user to understand the phenomena being depicted.”17 ► Neutrality: there should not be bias in the selection or presentation of financial information. Financial

information should not be slanted, weighted, emphasized, de-emphasized or otherwise manipulated to increase the probability that financial information will be received favorably or unfavorably.

► Free from error: “no errors or omissions in the description of the phenomenon, and the process used to produce the reported information.”18

16SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 3, “Qualitative Characteristics of Useful Financial Information,” QC12.17Ibid, QC13.18Ibid, QC15.

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Academic Resource Center

Conceptual framework Page 19

► Qualitative characteristics of useful financial information (continued):► Applying the fundamental qualitative characteristics: usually, the most efficient and effective

process for applying the fundamental qualitative characteristics and the cost constraint is as follows: ► “Identify an economic phenomenon that has the potential to be useful to users.”19

► “Identify the type of information about the phenomenon that would be most relevant if it is available and be faithfully represented.”20

► “Determine whether that information is available and can be faithfully represented.”21

► “If so, the process of satisfying the fundamental qualitative characteristics ends at that point. If not, then the process is repeated with the next most relevant type of information.”22

19SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 3, “Qualitative Characteristics of Useful Financial Information,” QC18.20Ibid.21Ibid.22Ibid

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Academic Resource Center

Conceptual framework Page 20

► Qualitative characteristics of useful financial information (continued):► Enhancing qualitative characteristics: qualitative characteristics that enhance the usefulness

of information that is relevant and faithfully represented. These include comparability, verifiability, timeliness and understandability. “Enhancing qualitative characteristics should be maximized to the extent possible.”23 ► Comparability: “Enables users to identify and understand similarities and differences among items.”24

► Consistency is not the same as comparability although related and is described as “the use of the same methods for the same item either from period to period within a reporting entity or in a single period across entities.”25

► Verifiability:► “Assures users that information faithfully represents the economic phenomena it purports to represent.”26

► “Means that different and knowledgeable and independent observers could reach consensus, although not necessarily complete agreement, that a particular depiction is a faithful representation.”27

23SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 3, “Qualitative Characteristics of Useful Financial Information,” QC33.24Ibid, QC21.25Ibid, QC22.26Ibid, QC26.27Ibid.

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Academic Resource Center

Conceptual framework Page 21

► Qualitative characteristics of useful financial information (continued):► Enhancing qualitative characteristics (continued):

► Timeliness: providing information to decision makers in time to be capable of influencing their decisions.► Understandability: “Classifying, characterizing, and presenting information clearly and concisely.”28

► Pervasive constraint on useful financial information: costs, which are a pervasive constraint on financial information, should be assessed as to whether the benefits of reporting particular information are likely to justify the costs incurred to provide and use the information.

28SFAC No. 8, Conceptual Framework for Financial Reporting, Chapter 3, “Qualitative Characteristics of Useful Financial Information,” QC30.

Overview of Chapter 3, “Qualitative Characteristics of Useful Financial Information”

Academic Resource Center

Conceptual framework Page 22

Comparison of SFAC No. 1 replaced by SFAC No. 8, Chapter 1

Similarities► There is continued focus on the importance of cash flows for users of financial statements.► Information should be provided for economic resources, claims on resources and changes in

resources and claims.► There is acknowledgment that there are limitations of general purpose financial statements.► Accrual accounting is emphasized.

Differences► SFAC No. 8 is much shorter and more succinct.► There is a reduced number of identified users in SFAC No. 8, which is focused on “primary

users.”► Terminology differences include more general terms with respect to financial information

required.

Academic Resource Center

Conceptual framework Page 23

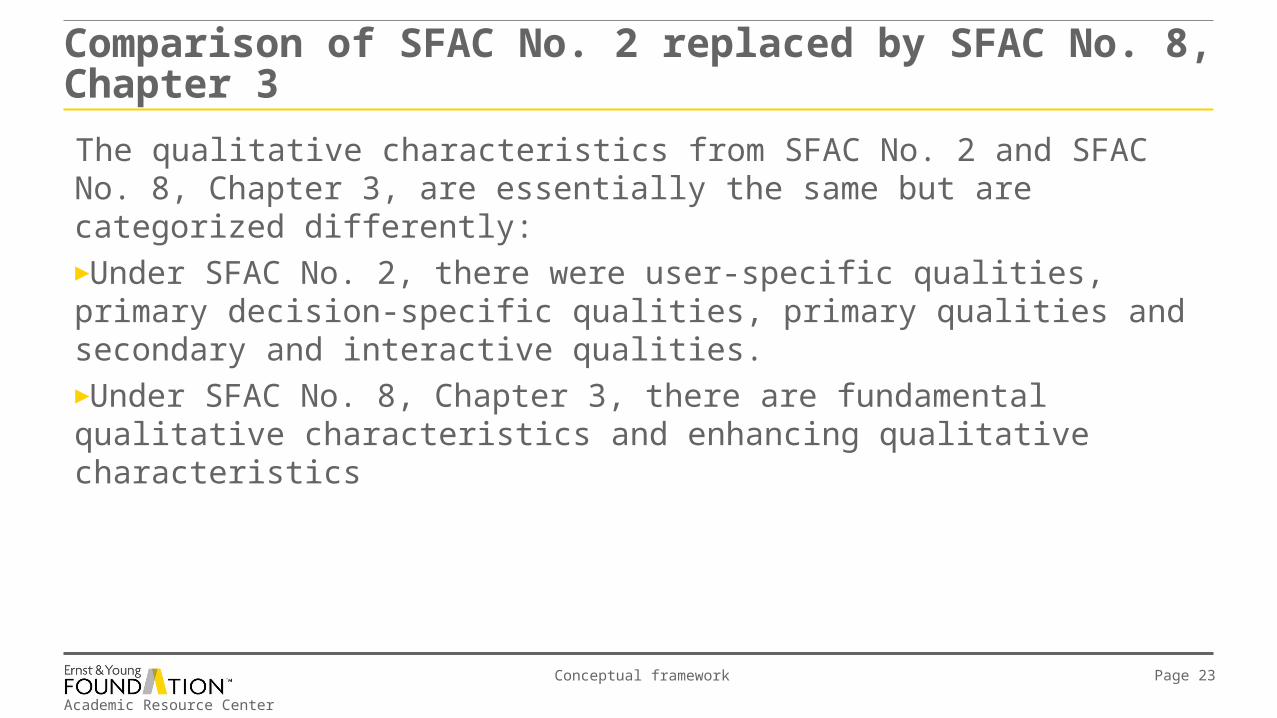

Comparison of SFAC No. 2 replaced by SFAC No. 8, Chapter 3

The qualitative characteristics from SFAC No. 2 and SFAC No. 8, Chapter 3, are essentially the same but are categorized differently: ►Under SFAC No. 2, there were user-specific qualities, primary decision-specific qualities, primary qualities and secondary and interactive qualities. ►Under SFAC No. 8, Chapter 3, there are fundamental qualitative characteristics and enhancing qualitative characteristics

Academic Resource Center

Conceptual framework Page 24

► This section of the conceptual framework module compares the elements of financial statements, the recognition and measurement criteria and prescribed financial statements between the FASB’s SFACs No. 5, 6 and 7 and the IASB’s Conceptual Framework.

► The following slides include tables comparing these items between the FASB and IASB followed by additional slides that include explanatory detail.

► For a more detailed history of the development of the comparative Conceptual Framework, please see the supplementary reference material in the attached Appendix.

OverviewElements of financial statements, recognition and measurement criteria and financial statements

Academic Resource Center

Conceptual framework Page 25

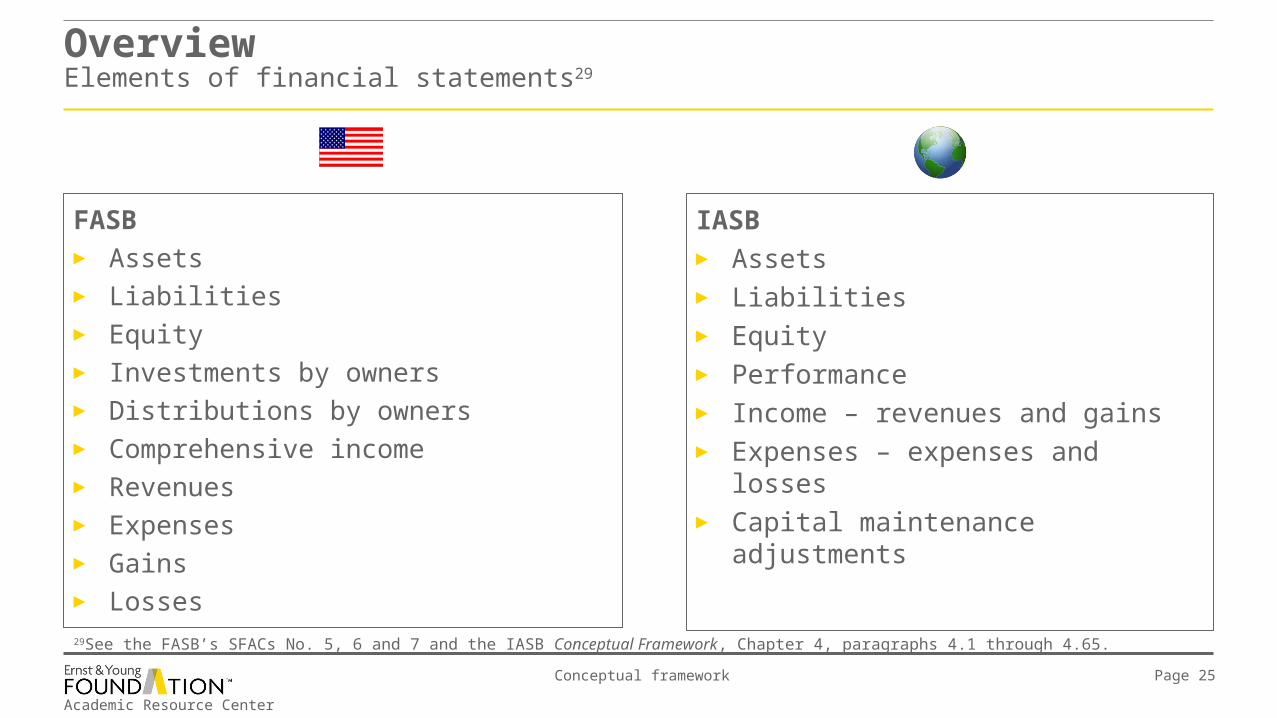

OverviewElements of financial statements29

FASB► Assets► Liabilities► Equity► Investments by owners► Distributions by owners► Comprehensive income► Revenues► Expenses► Gains► Losses

IASB► Assets► Liabilities► Equity► Performance► Income – revenues and gains► Expenses – expenses and losses► Capital maintenance adjustments

29See the FASB’s SFACs No. 5, 6 and 7 and the IASB Conceptual Framework, Chapter 4, paragraphs 4.1 through 4.65.

Academic Resource Center

Conceptual framework Page 26

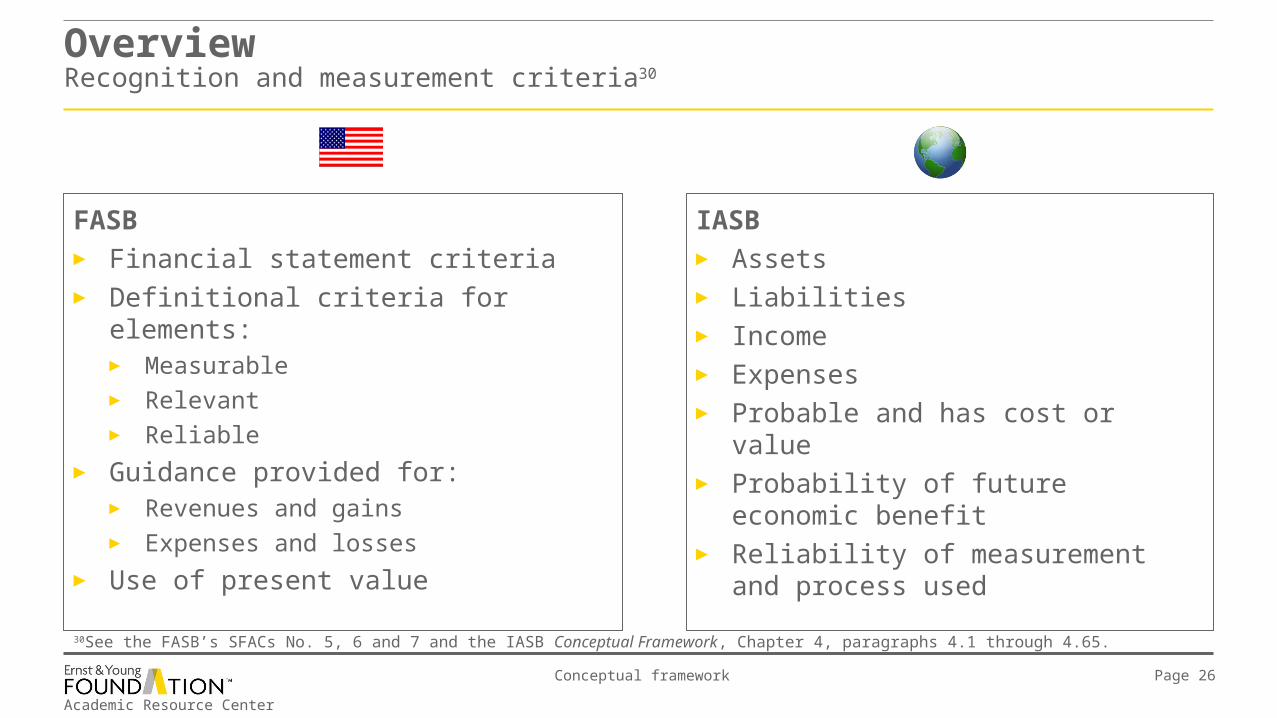

OverviewRecognition and measurement criteria30

FASB► Financial statement criteria► Definitional criteria for elements:

► Measurable► Relevant► Reliable

► Guidance provided for:► Revenues and gains► Expenses and losses

► Use of present value

IASB► Assets► Liabilities► Income► Expenses► Probable and has cost or value► Probability of future economic benefit► Reliability of measurement and process

used

30See the FASB’s SFACs No. 5, 6 and 7 and the IASB Conceptual Framework, Chapter 4, paragraphs 4.1 through 4.65.

Academic Resource Center

Conceptual framework Page 27

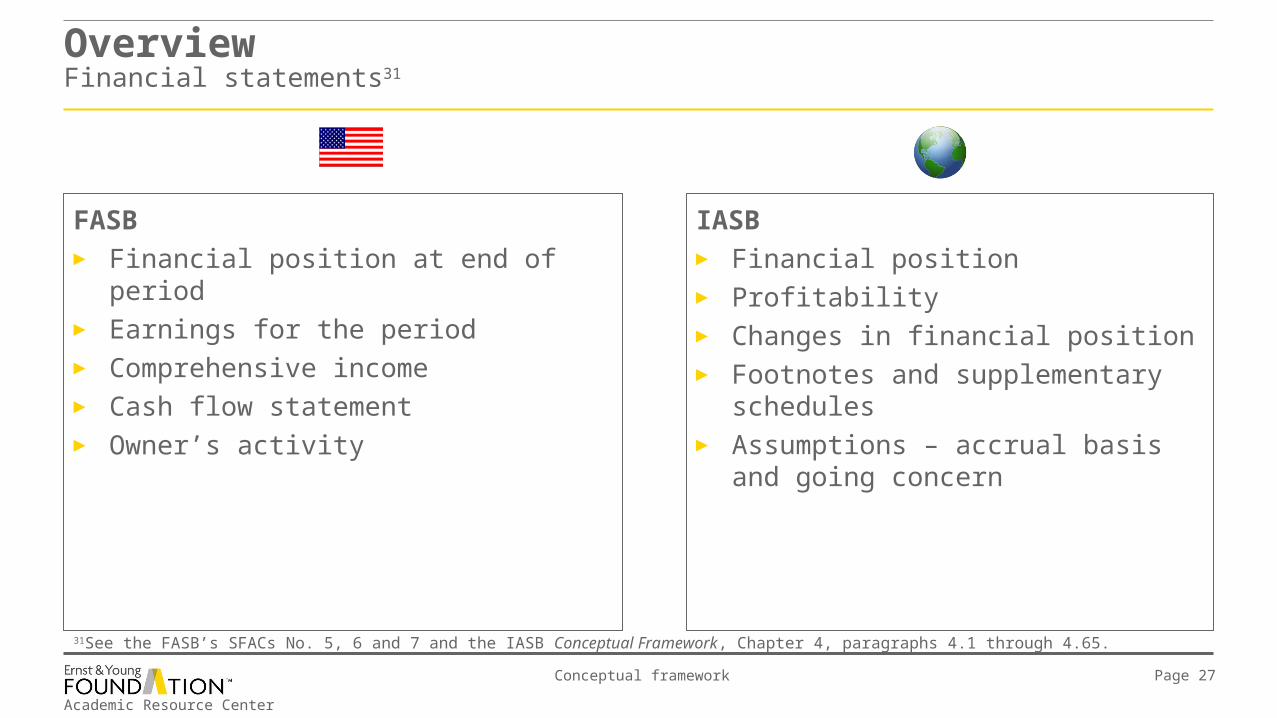

OverviewFinancial statements31

FASB► Financial position at end of period► Earnings for the period► Comprehensive income► Cash flow statement► Owner’s activity

IASB► Financial position► Profitability► Changes in financial position► Footnotes and supplementary

schedules► Assumptions – accrual basis and going

concern

31See the FASB’s SFACs No. 5, 6 and 7 and the IASB Conceptual Framework, Chapter 4, paragraphs 4.1 through 4.65.

Academic Resource Center

Conceptual framework Page 28

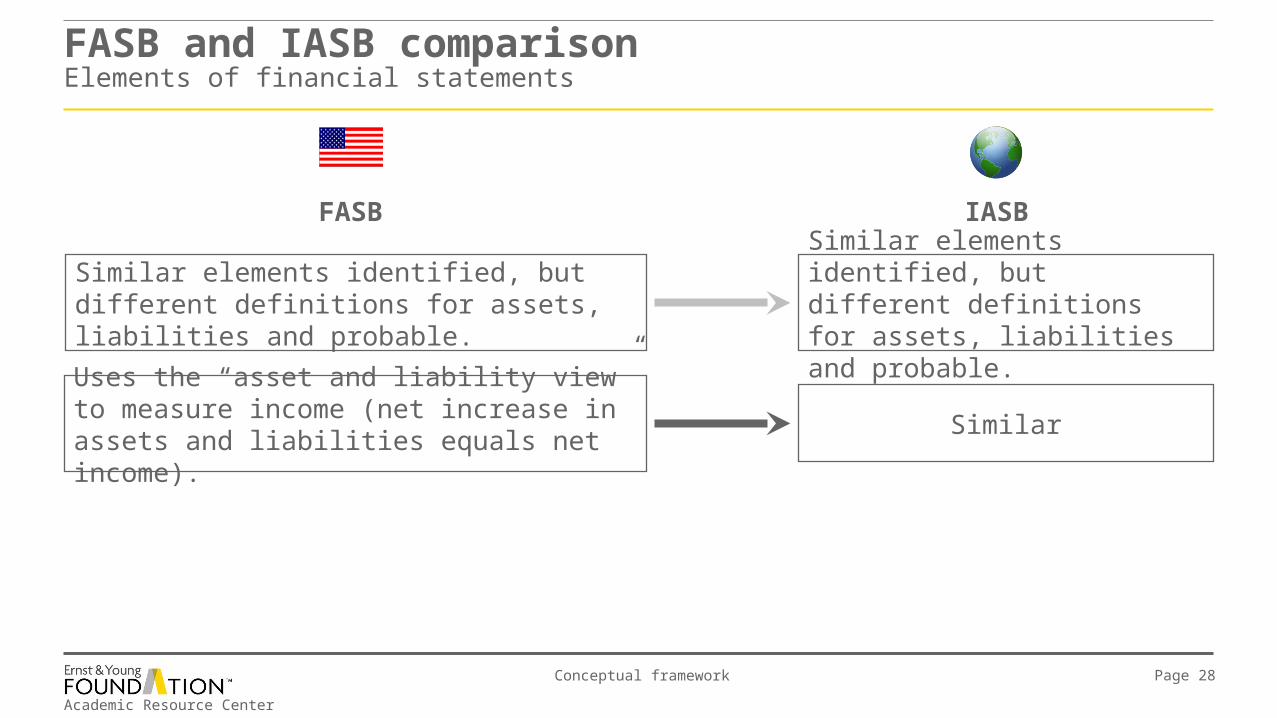

FASB and IASB comparison Elements of financial statements

Similar elements identified, but different definitions for assets, liabilities and probable.

Uses the “asset and liability view” to measure income (net increase in assets and liabilities equals net income).

Similar elements identified, but different definitions for assets, liabilities and probable.

Similar

IASBFASB

Academic Resource Center

Conceptual framework Page 29

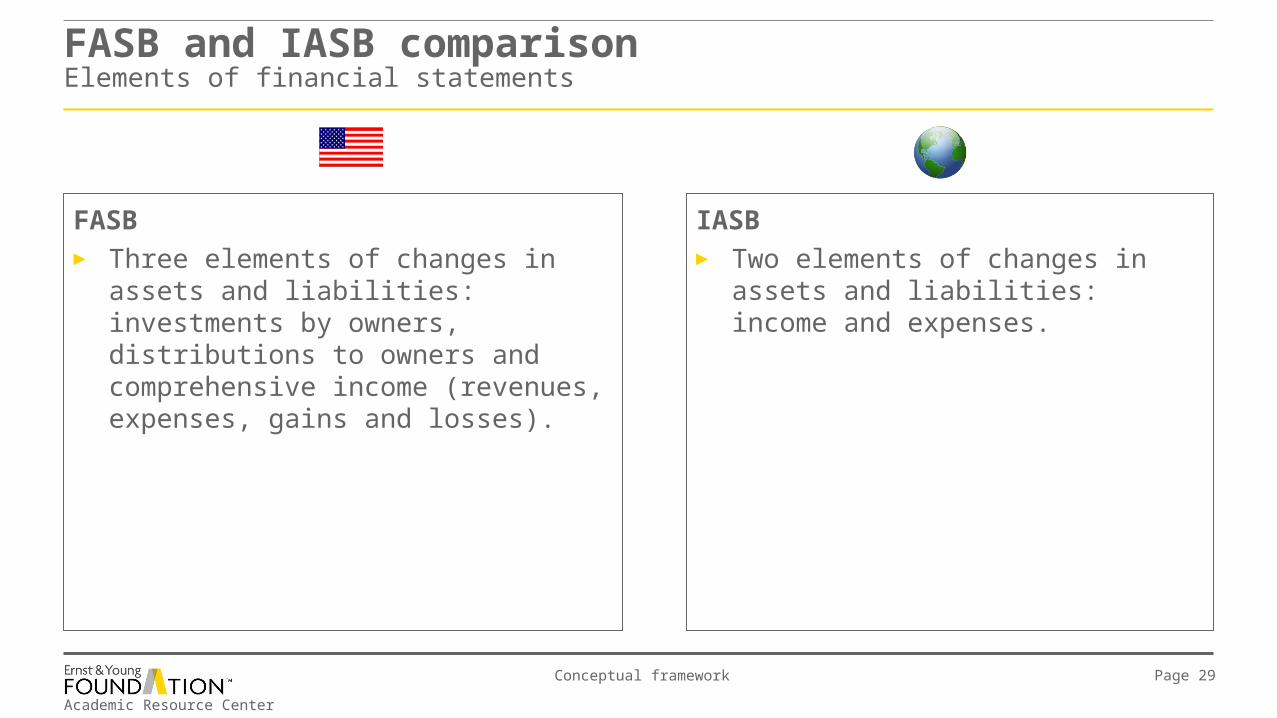

FASB ► Three elements of changes in assets and

liabilities: investments by owners, distributions to owners and comprehensive income (revenues, expenses, gains and losses).

IASB► Two elements of changes in assets and

liabilities: income and expenses.

FASB and IASB comparison Elements of financial statements

Academic Resource Center

Conceptual framework Page 30

Recognition criteria: element and cost or value. Similar

Contains measurement criteria. Similar

IASBFASB

FASB and IASB comparison Recognition and measurement

Academic Resource Center

Conceptual framework Page 31

FASB ► Includes criterion that an item must be

relevant:► Capable of making a difference in user

decisions.

► Specifies use of a cash flow statement and use of present value as a measurement technique.

IASB► Not specified.

► Provides less emphasis on the use of a cash flow statement or use of present value as a measurement technique.

FASB and IASB comparison Recognition and measurement

Academic Resource Center

Conceptual framework Page 32

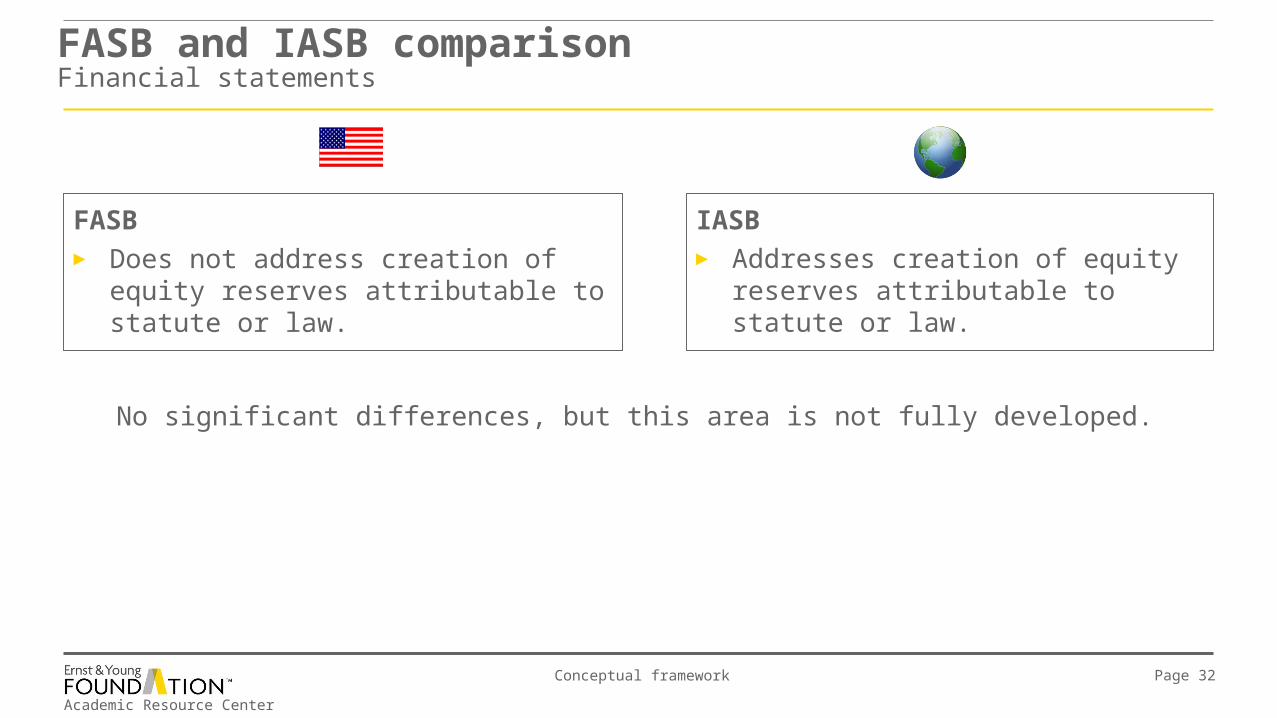

FASB and IASB comparison Financial statements

FASB ► Does not address creation of equity

reserves attributable to statute or law.

IASB► Addresses creation of equity reserves

attributable to statute or law.

No significant differences, but this area is not fully developed.

Academic Resource Center

Conceptual framework Page 33

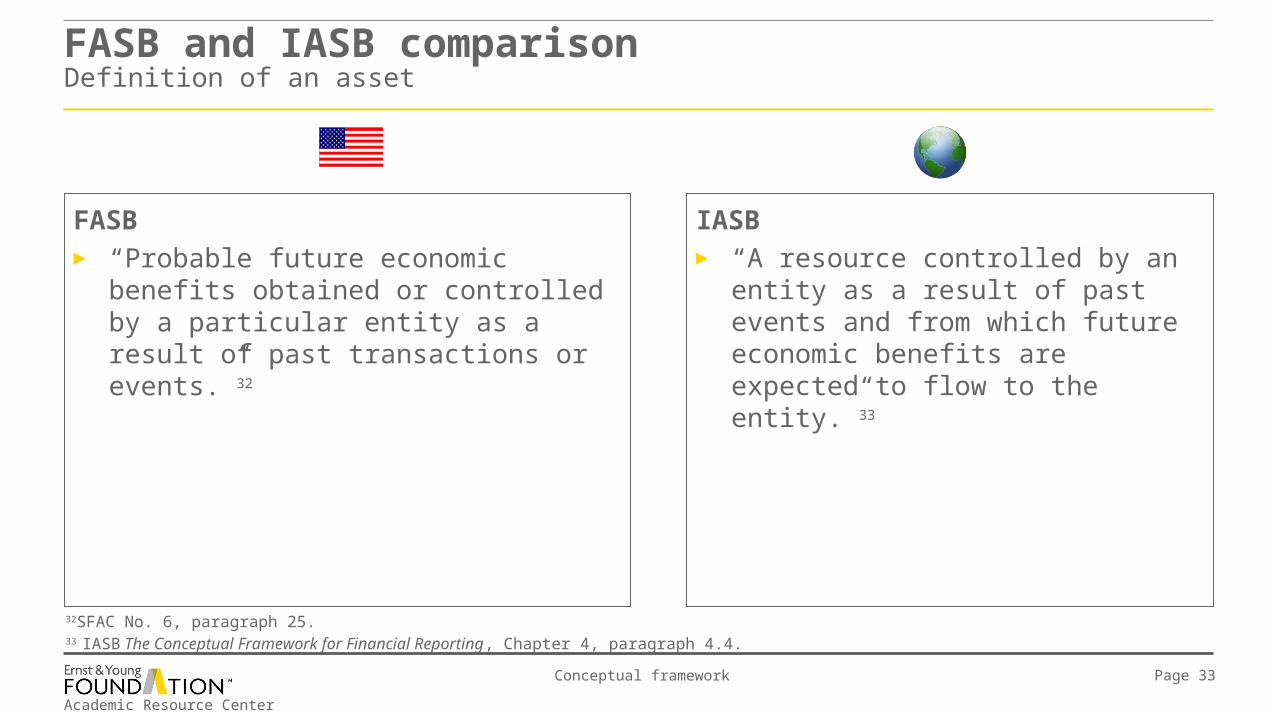

FASB► “Probable future economic benefits

obtained or controlled by a particular entity as a result of past transactions or events.”32

IASB► “A resource controlled by an entity as a

result of past events and from which future economic benefits are expected to flow to the entity.”33

32SFAC No. 6, paragraph 25.33 IASB The Conceptual Framework for Financial Reporting, Chapter 4, paragraph 4.4.

FASB and IASB comparison Definition of an asset

Academic Resource Center

Conceptual framework Page 34

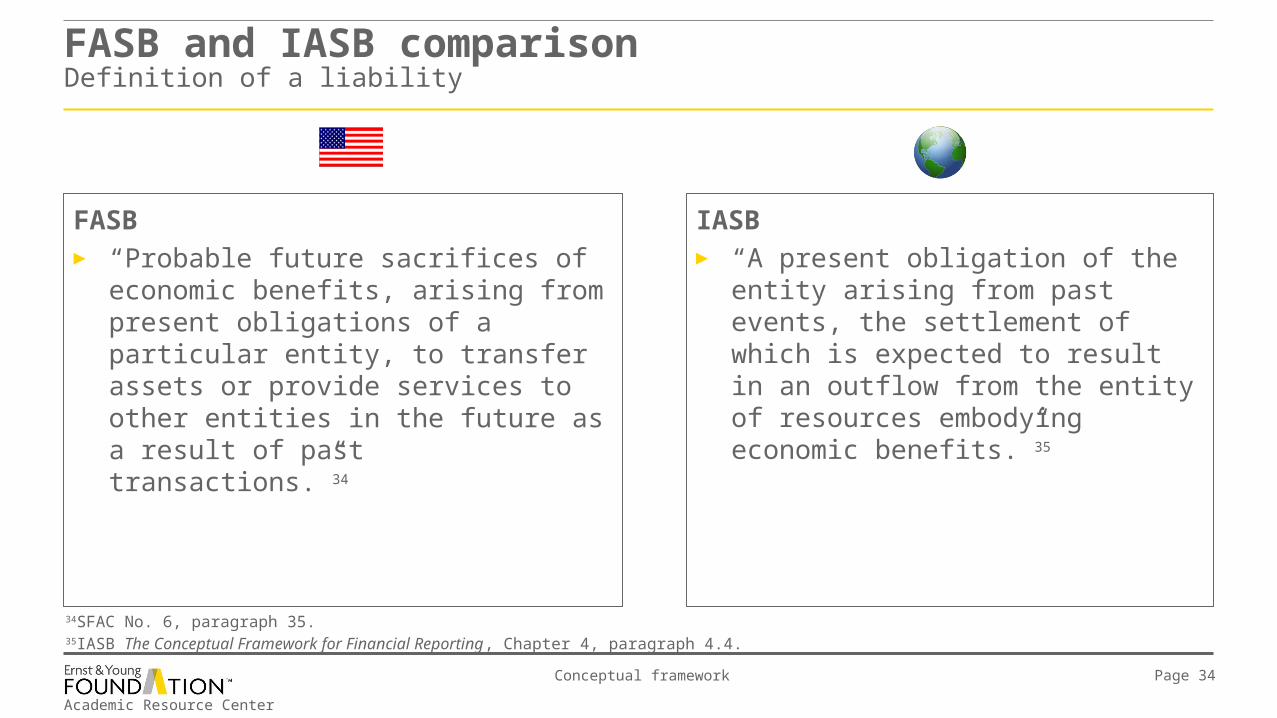

FASB► “Probable future sacrifices of economic

benefits, arising from present obligations of a particular entity, to transfer assets or provide services to other entities in the future as a result of past transactions.”34

IASB► “A present obligation of the entity

arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.”35

34SFAC No. 6, paragraph 35.35IASB The Conceptual Framework for Financial Reporting, Chapter 4, paragraph 4.4.

FASB and IASB comparison Definition of a liability

Academic Resource Center

Conceptual framework Page 35

FASB► “That which can reasonably be expected

or believed on the basis of available evidence or logic, but which is not certain nor proven.”36

IASB► “The degree of uncertainty that future

economic benefits associated with the item will flow to or from the entity.”37

36SFAC No. 6, paragraph 18.37IASB The Conceptual Framework for Financial Reporting, Chapter 4, paragraph 4.4.

FASB and IASB comparison Definition of probable

Academic Resource Center

Conceptual framework Page 36

FASB ► No fundamental difference in concepts,

but definition differences are apparent.► Longer, more detailed and specific.

► Not part of US GAAP hierarchy and, therefore, not authoritative.

IASB► No fundamental difference in concepts,

but definition differences are apparent.► Shorter, less detailed.► Developed from FASB Concept

Statements.► High-level presentation (principles

based) to accommodate various countries’ accounting models and emphasizes substance over form.

► Third level of accounting to be followed in the IFRS hierarchy.

FASB and IASB comparison Overall differences

Academic Resource Center

Conceptual framework Page 37

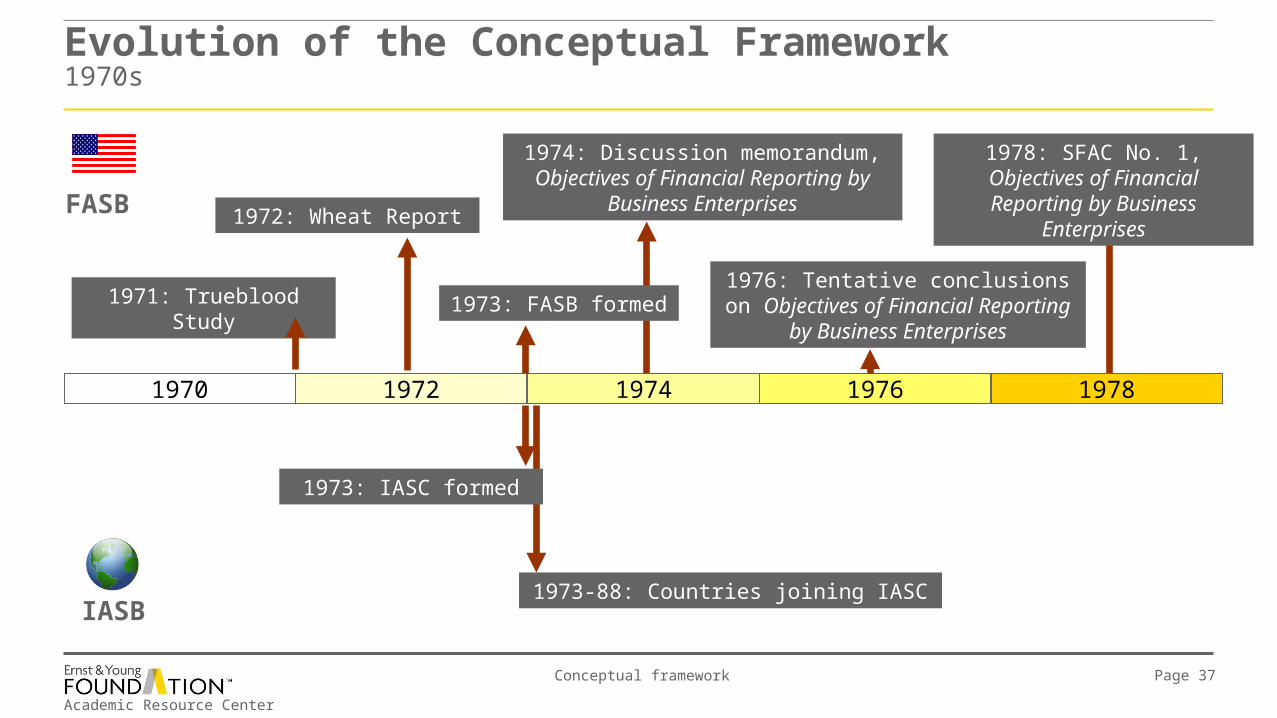

Evolution of the Conceptual Framework1970s

1970 1972 1974 1976 1978

1971: Trueblood Study

FASB

IASB

1972: Wheat Report

1973: FASB formed

1974: Discussion memorandum, Objectives of Financial Reporting by

Business Enterprises

1976: Tentative conclusions on Objectives of Financial Reporting by

Business Enterprises

1978: SFAC No. 1, Objectives of Financial Reporting by

Business Enterprises

1973: IASC formed

1973-88: Countries joining IASC

Academic Resource Center

Conceptual framework Page 38

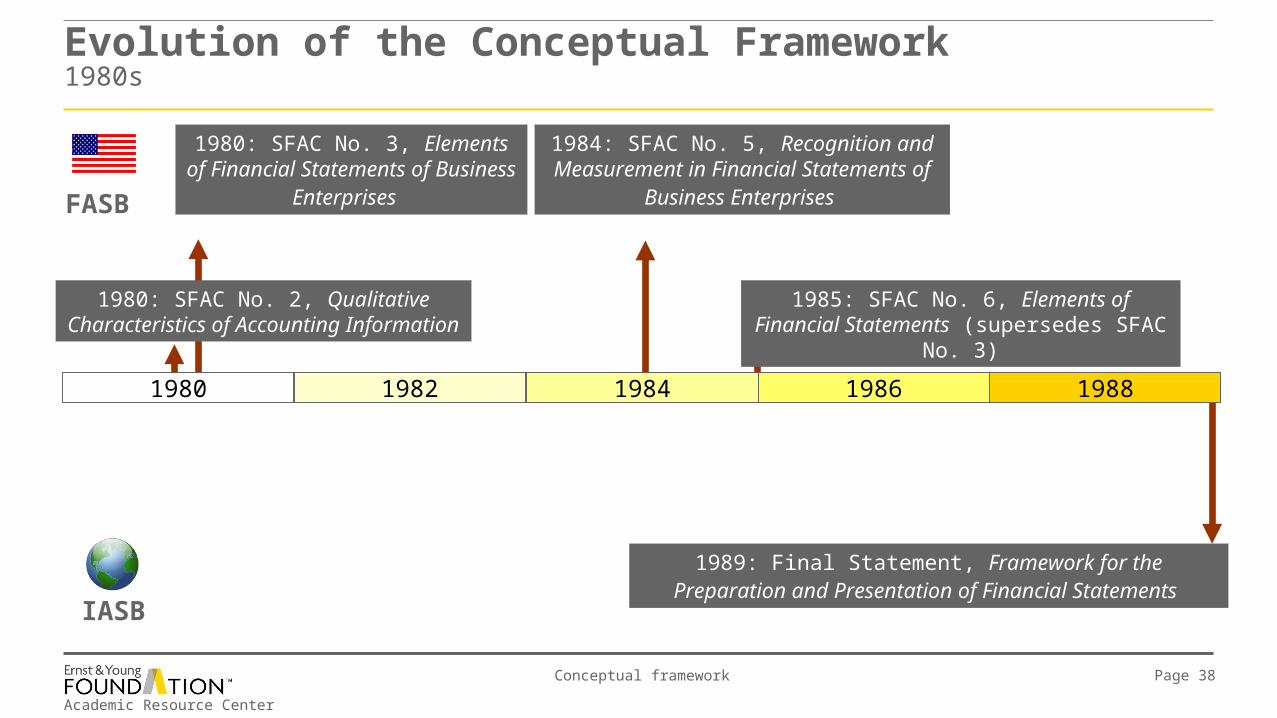

1980: SFAC No. 3, Elements of Financial Statements of Business

Enterprises

Evolution of the Conceptual Framework1980s

1980 1982 1984 1986 1988

1980: SFAC No. 2, Qualitative Characteristics of Accounting Information

1984: SFAC No. 5, Recognition and Measurement in Financial Statements of

Business Enterprises

1985: SFAC No. 6, Elements of Financial Statements (supersedes SFAC No. 3)

1989: Final Statement, Framework for the Preparation and Presentation of Financial Statements

FASB

IASB

Academic Resource Center

Conceptual framework Page 39

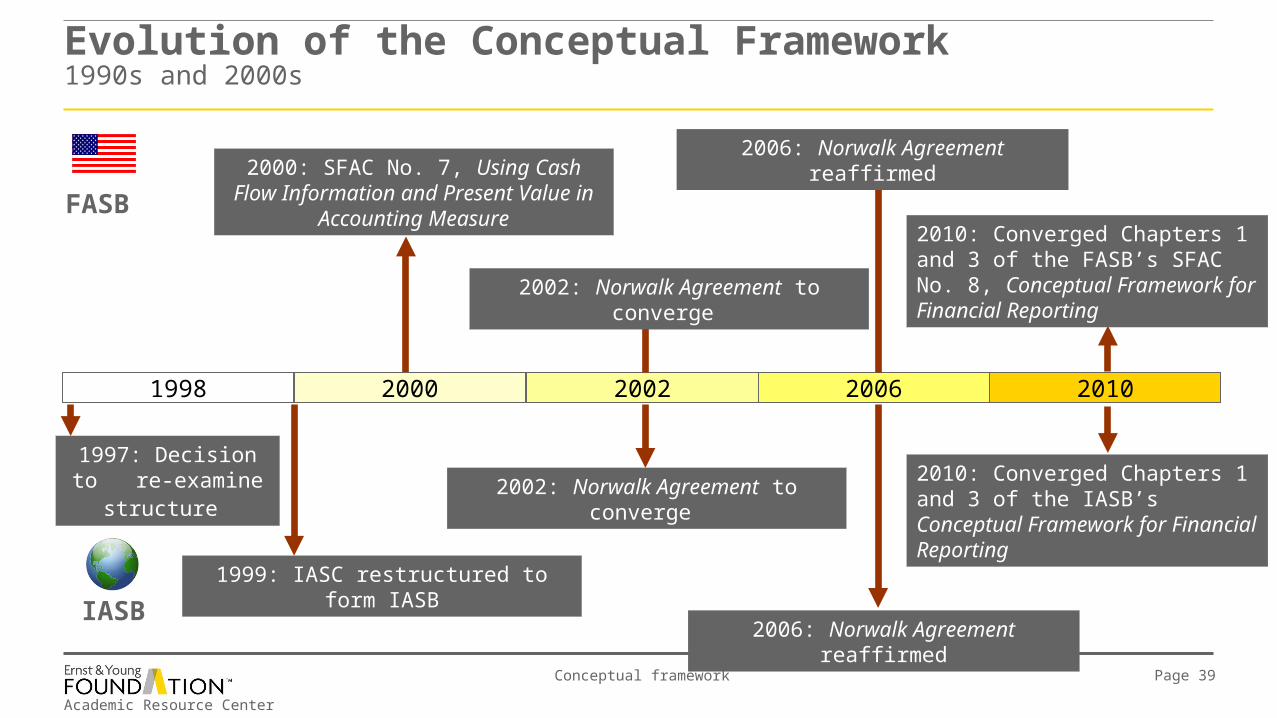

Evolution of the Conceptual Framework 1990s and 2000s

1998 2000 2002 2006 2010

2000: SFAC No. 7, Using Cash Flow Information and Present Value in

Accounting Measure

2002: Norwalk Agreement to converge

2006: Norwalk Agreement reaffirmed

1997: Decision to re-examine structure

1999: IASC restructured to form IASB

2002: Norwalk Agreement to converge

2006: Norwalk Agreement reaffirmed

FASB

IASB

2010: Converged Chapters 1 and 3 of the FASB’s SFAC No. 8, Conceptual Framework for Financial Reporting

2010: Converged Chapters 1 and 3 of the IASB’s Conceptual Framework for Financial Reporting

Academic Resource Center

Conceptual framework Page 40

Convergence Norwalk Agreement

► In October 2002, the FASB and IASB agreed to make their accounting standards compatible, including the Conceptual Framework.

► In February 2006, a road map was released for short-term and long-term projects.

► In November 2009, the Boards reaffirmed their commitment to the 2006 Memorandum of Understanding.

► The Joint Project of the IASB and FASB Conceptual Framework (the Project) is long term and has several objectives:► Sound formulation for developing accounting standards.► Should be principles based. ► Internally consistent.► International convergence.

Academic Resource Center

Conceptual framework Page 41

Convergence The Project has eight phases (Phases A-H), which are as follows, with their status indicated:

Phase A – Objectives and Qualitative Characteristics ► Purpose is to consider:

► The objective of financial reporting.► The qualitative characteristics.► The trade-offs among qualitative characteristics and concepts of materiality and cost-benefit

relationships.

► Decisions to date:► The Boards issued converged chapters on the objectives of general purpose financial reporting and

the qualitative characteristics of useful financial information in September 2010.

Academic Resource Center

Conceptual framework Page 42

ConvergencePhase B – Elements and Recognition

► Purpose is to revise and clarify various issues:► Revise and clarify definition of asset and

liability.► Resolve differences regarding other elements

and their definitions.► Revise recognition criteria, resolve

derecognition and unit of account.

► Asset “… is a present economic resource to which an entity has a right or other access that others do not have,”38 which is:► Present – at date of financial statements.► Economic resource – scarce, provides cash.► A right or other access that others do not have

– legally enforceable or equivalent.

► Liability “… is a present economic obligation for which the entity is the obligor,”39 which is:► Present – at date of financial statements.► Economic obligation – to provide resources.► Entity is the obligor – enforceable against entity.

► The Boards are to reconsider the definition of a liability.

► A Discussion Paper is expected in 2011.

38Current working definition of the Project.39Ibid.

Academic Resource Center

Conceptual framework Page 43

ConvergencePhase C – Measurement

► Purpose is to provide guidance for selecting measurement bases that satisfy the objectives and qualitative characteristics of financial reporting.40

► Tentative decisions reached by the Boards:► Measurement should consider the effect of a particular measurement selection on all of the financial

statements.► An explanation should be included in the measurement chapter of how fundamental qualitative

characteristics (relevance and faithful representation) must be considered in selecting measures.► Because historical cost and fair value do not clearly and accurately describe measurement methods,

the terms should not be used in the measurement chapter.► The measurement chapter should describe possible measures in a manner that facilitates standard

setting, given the qualitative characteristics and cost constraint.

► A Discussion Paper is expected in 2011.

40The Project update – July 2010.

Academic Resource Center

Conceptual framework Page 44

ConvergencePhase D – Reporting Entity Concept

► Purpose is to determine what constitutes a reporting entity for purposes of financial reporting.41

► ED issued in March 2010:► Definition (per paragraph S1): “A reporting entity is a circumscribed area of economic activities whose

financial information has the potential to be useful to existing and potential equity investors, lenders, and other creditors who cannot directly obtain the information they need in making decisions about providing resources to the entity and in assessing whether the management and the governing board of that entity have made efficient and effective use of the resources provided.”

► Consolidation (per paragraph S2): “An entity controls another entity when it has the power to direct the activities of that entity to generate benefits for (or limit losses to) itself. If an entity that controls one or more entities prepares financial reports, it should present consolidated financial statements.”

► Reporting (per paragraph S3): “A portion of an entity could qualify as a reporting entity if the economic activities of that portion can be distinguished objectively from the rest of the entity and financial information about that portion of the entity has the potential to be useful in making decisions about providing resources to that portion of the entity.”

► The comment period ended in July 2010, at which time the staff began to analyze comments received. A final pronouncement is expected in 2011.

41The Project update – July 2010.

Academic Resource Center

Conceptual framework Page 45

ConvergencePhases not yet started

The following phases have yet to be started:► Phase E – Presentation and Disclosure,

including Financial Reporting Boundaries► Phase F – Framework Purpose and Status in

US GAAP Hierarchy ► Phase G – Applicability to Not-for-Profit

Sector► Phase H – Remaining Issues

Academic Resource Center

Conceptual framework Page 46

ConvergenceVision for the Conceptual Framework

► Importance:► Principles based.► Internally consistent.► International convergence.► Information vital to capital provider.

► Timing:► Slow due to the process of preliminary views, Discussion

Papers, EDs and final statements.► Some pressure from SEC and Congress.

Academic Resource Center

Conceptual framework Page 47

Ernst & Young LLP

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 141,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global and of Ernst & Young Americas operating in the US.

© 2011 Ernst & Young Foundation (US) All Rights Reserved.SCORE No. MM4080C.