comScore: 2017 Cross-Platform Future in Focus

15

For info about the proprietary technology used in comScore products, refer to http://comscore.com/About_comScore/Patents Will have new cover

-

Upload

comscore -

Category

Data & Analytics

-

view

525 -

download

1

Transcript of comScore: 2017 Cross-Platform Future in Focus

For info about the proprietary technology used in comScore products, refer to http://comscore.com/About_comScore/Patents

Will have new cover

© comScore, Inc. Proprietary. 2

About this report

This is a condensed version of the 73-page 2017 U.S. Cross-Platform Future in Focus. To download the full complimentary

version of the report, please visit:

comscore.com/USFutureinFocus2017

Important Definitions:

Total Digital: The combination of desktop and mobile.

Mobile: The combination of smartphone and tablet. When data is referring specifically to smartphones or tablets, it will be labeled accordingly.

Unique visitor: A person who visits an app or digital media property at least once over the course of a month.

Digital Video Recorder (DVR): An electronic device used to record live television and watch later. Viewing via a DVR is often referred to as time-shifted recorded viewing.

Video-on-Demand (VOD): Refers to video content that is made available via the traditional cable, telco or satellite service operators for on-demand viewing, as opposed to the regularly

scheduled live TV viewing or time-shifted DVR viewing.

Over-the-Top (OTT): Refers to video content that is transmitted via the internet to one’s television set, instead of via the traditional cable, telco or satellite service operators.

For more information about subscribing to comScore services, please contact us at comscore.com/learnmore.

© comScore, Inc. Proprietary. 3

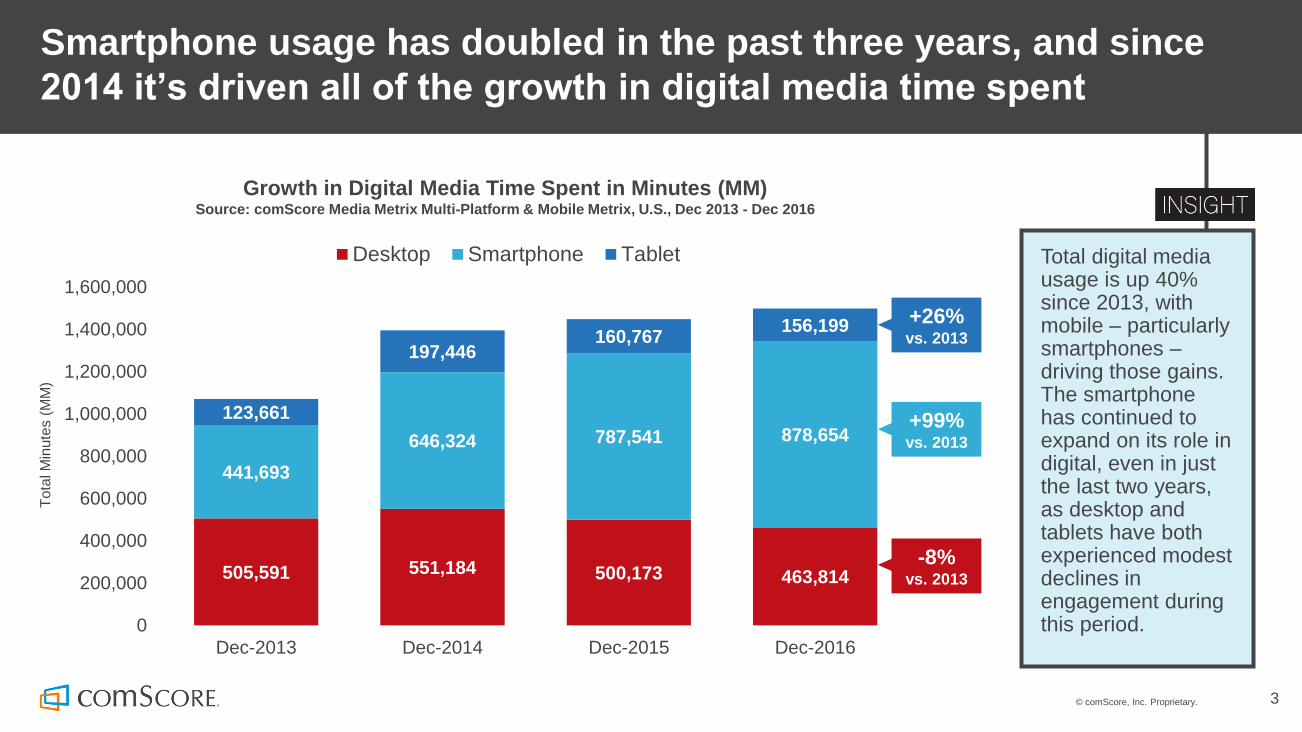

Smartphone usage has doubled in the past three years, and since

2014 it’s driven all of the growth in digital media time spent

Total digital media usage is up 40% since 2013, with mobile – particularly smartphones –driving those gains. The smartphone has continued to expand on its role in digital, even in just the last two years, as desktop and tablets have both experienced modest declines in engagement during this period.

Growth in Digital Media Time Spent in Minutes (MM)Source: comScore Media Metrix Multi-Platform & Mobile Metrix, U.S., Dec 2013 - Dec 2016

505,591 551,184 500,173 463,814

441,693

646,324 787,541 878,654

123,661

197,446160,767

156,199

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Dec-2013 Dec-2014 Dec-2015 Dec-2016

To

tal M

inute

s (

MM

)

Desktop Smartphone Tablet

+26% vs. 2013

+99%vs. 2013

-8%vs. 2013

© comScore, Inc. Proprietary. 4

Mobile now represents almost 7 in 10 digital media minutes, and

smartphone apps alone account for half of all digital time spent

With desktop engagement faltering in recent years, it has lost share to mobile –which now accounts for 69% of digital media time spent. Mobile apps now drive 60% of digital time spent, and smartphone apps alone currently account for a majority of digital media consumption.

Share of Digital Media Time Spent by PlatformSource: comScore Media Metrix Multi-Platform & Mobile Metrix, U.S., Total Audience, Dec 2013 – Dec 2016

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

Dec-2013 Jun-2014 Dec-2014 Jun-2015 Dec-2015 Jun-2016 Dec-2016

Share of Digital Time Spent on MOBILE APP

Share of Digital Time Spent on MOBILE

31%

60%

Share of Digital Time Spent on DESKTOP

+16pts

+16pts

-16pts

44%

53%

47%

Share of Digital Time Spent on SMARTPHONE APP+16pts

35%

51%

69%

© comScore, Inc. Proprietary. 5

Google Sites, Facebook and Yahoo Sites remain the top digital

media properties and the only ones with 200+ MM visitors

The average Top 10 digital media property has 39% of its audience visiting only on mobile and 34% visiting on both mobile and desktop. For five of the Top 10, a majority of their digital media audiences are mobile-only visitors, highlighting the importance of mobile as a primary touchpoint for many large digital media companies.

Top Digital Properties: Unique Visitors (MM) by PlatformSource: comScore Media Metrix Multi-Platform, U.S., Dec 2016

0 50 100 150 200 250 300

Google Sites

Yahoo Sites

Microsoft Sites

Amazon Sites

Comcast NBCUniversal

CBS Interactive

AOL, Inc.

Apple Inc.

Time Inc. Network (U.S)

Desktop Only Multi-Platform Mobile Only

209 MM

206 MM

190 MM

189 MM

164 MM

163 MM

157 MM

153 MM

129 MM

247 MM

© comScore, Inc. Proprietary. 6

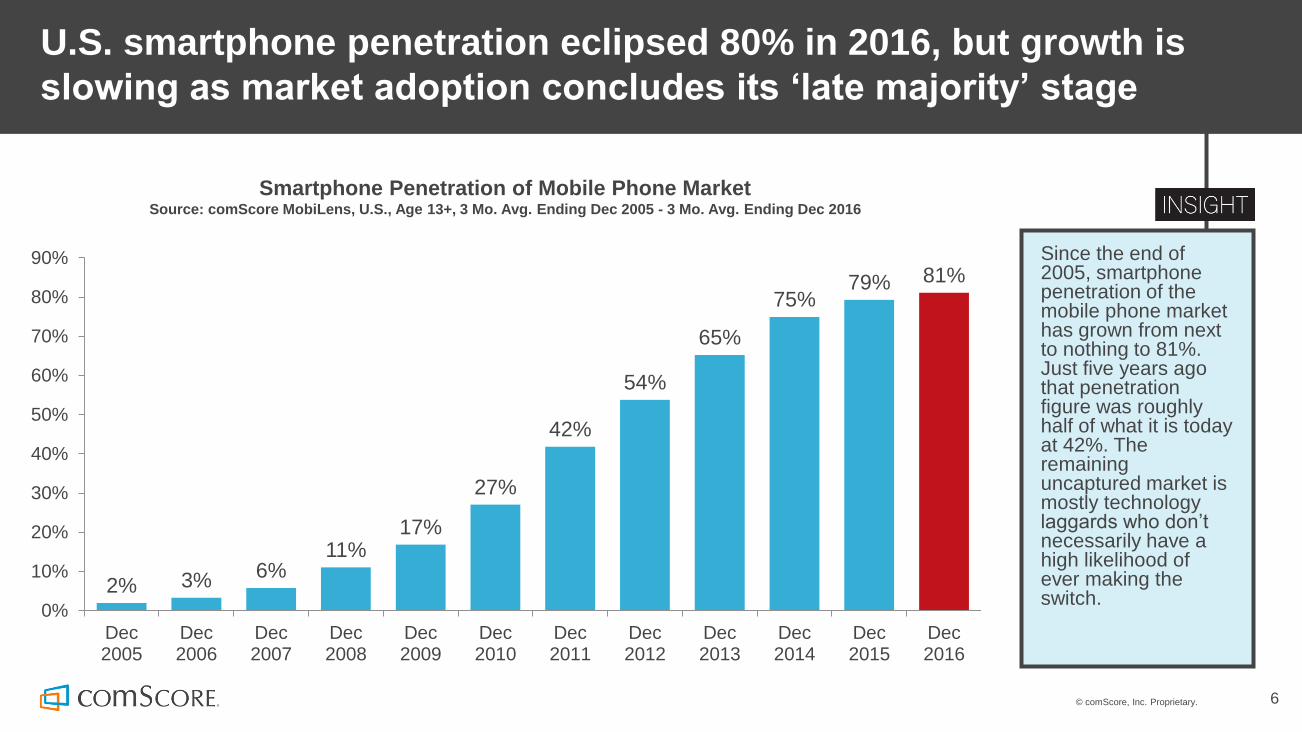

U.S. smartphone penetration eclipsed 80% in 2016, but growth is

slowing as market adoption concludes its ‘late majority’ stage

Since the end of 2005, smartphone penetration of the mobile phone market has grown from next to nothing to 81%. Just five years ago that penetration figure was roughly half of what it is today at 42%. The remaining uncaptured market is mostly technology laggards who don’t necessarily have a high likelihood of ever making the switch.

Smartphone Penetration of Mobile Phone MarketSource: comScore MobiLens, U.S., Age 13+, 3 Mo. Avg. Ending Dec 2005 - 3 Mo. Avg. Ending Dec 2016

2% 3% 6%11%

17%

27%

42%

54%

65%

75%79% 81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Dec2005

Dec2006

Dec2007

Dec2008

Dec2009

Dec2010

Dec2011

Dec2012

Dec2013

Dec2014

Dec2015

Dec2016

© comScore, Inc. Proprietary. 7

Share of Total Digital Time Spent by Content CategorySource: comScore Media Metrix Multi-Platform, U.S., Total Audience, December 2016

Social media and video viewing are the two most popular online

activities, together accounting for more than a third of all internet time

Social Media20%

Multimedia14%

Entertainment - Music11%

Games8%

Portals5%

Retail5%

Directories/Resources4%

News/Information3%

e-mail3%

Search/Navigation3%

Instant Messengers2%

Photos2%

Lifestyles2%

Sports2%

All Other16% Social Media leads

all categories in engagement, accounting for 1 out of 5 minutes spent online. The next largest categories being Multimedia, Music and Games highlight that digital is being increasingly used for entertainment – now more so than ever with the rise of mobile and consumers’ need to make use of their “in-between” time.

© comScore, Inc. Proprietary. 8

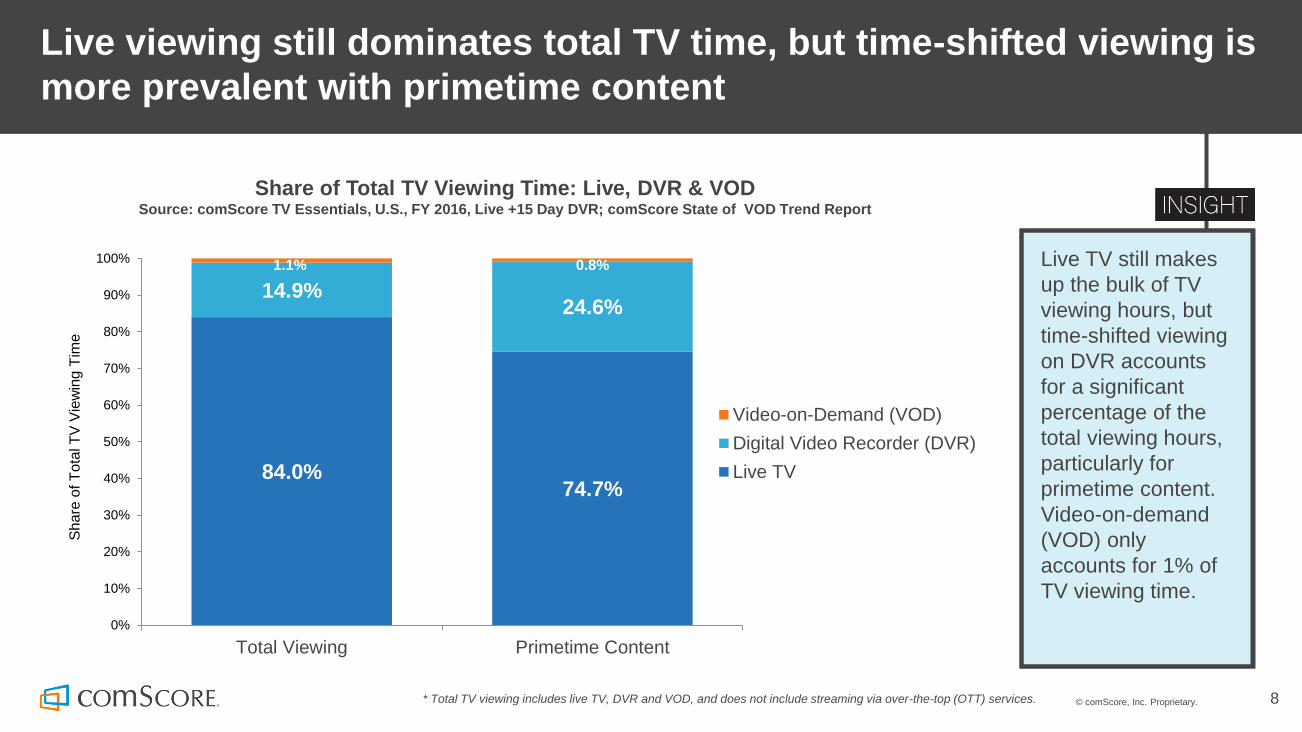

Live viewing still dominates total TV time, but time-shifted viewing is

more prevalent with primetime content

Live TV still makes

up the bulk of TV

viewing hours, but

time-shifted viewing

on DVR accounts

for a significant

percentage of the

total viewing hours,

particularly for

primetime content.

Video-on-demand

(VOD) only

accounts for 1% of

TV viewing time.

Share of Total TV Viewing Time: Live, DVR & VODSource: comScore TV Essentials, U.S., FY 2016, Live +15 Day DVR; comScore State of VOD Trend Report

84.0%74.7%

14.9%24.6%

1.1% 0.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total Viewing Primetime Content

Sh

are

of T

ota

l T

V V

iew

ing

Tim

e

Video-on-Demand (VOD)

Digital Video Recorder (DVR)

Live TV

* Total TV viewing includes live TV, DVR and VOD, and does not include streaming via over-the-top (OTT) services.

© comScore, Inc. Proprietary. 9

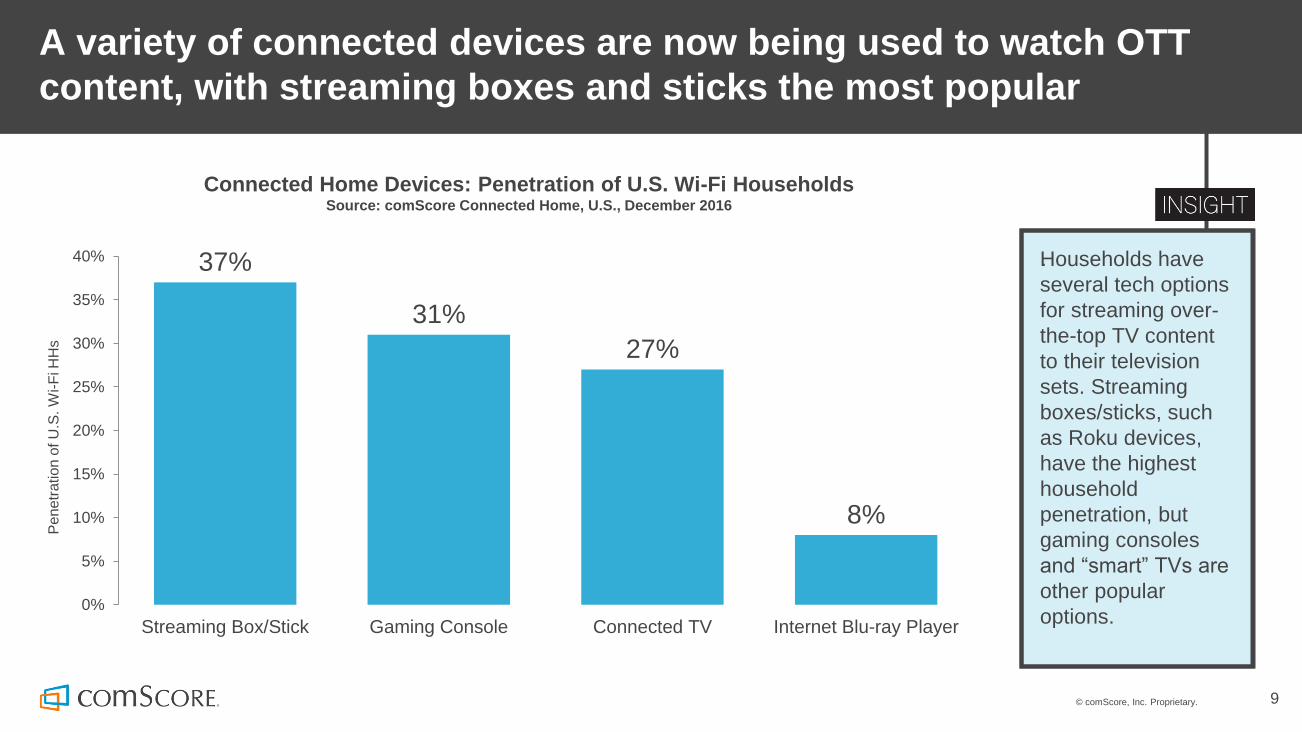

A variety of connected devices are now being used to watch OTT

content, with streaming boxes and sticks the most popular

37%

31%

27%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Streaming Box/Stick Gaming Console Connected TV Internet Blu-ray Player

Pe

ne

tra

tion

of U

.S. W

i-F

i HH

s

Connected Home Devices: Penetration of U.S. Wi-Fi HouseholdsSource: comScore Connected Home, U.S., December 2016

Households have

several tech options

for streaming over-

the-top TV content

to their television

sets. Streaming

boxes/sticks, such

as Roku devices,

have the highest

household

penetration, but

gaming consoles

and “smart” TVs are

other popular

options.

.

© comScore, Inc. Proprietary. 10

Nearly half of digital ad impressions can’t have an impact because

they’re not viewable or not delivered to a human

Nearly half of all desktop ad impressions are unable to deliver an advertising impact. While most of these non-viewable ads are simply delivered to parts of the web page that are out of view, a meaningful percentage is being delivered to bots and other forms of invalid traffic that is by definition not viewable to a human.

Percentage of Viewable Desktop Ad Impressions in U.S.Source: comScore vCE Benchmarks, U.S., Q4 2016

54%40%

6%

Viewable

Non-viewable

Invalid Traffic (IVT)

© comScore, Inc. Proprietary. 11

Both desktop and mobile ads deliver branding effectiveness, but

mobile performs better – particularly at the bottom of the funnel

Mobile ads caused point lifts up to 3x greater than ads on desktop across four key brand metrics and performed especially strong in middle and bottom-funnel metrics, such as favorability, intent to buy and likelihood to recommend. Less ad clutter and proximity to point of purchase may be driving better effectiveness for mobile ads.

Percentage Point Lift in Brand Metrics for Desktop and Mobile AdsSource: comScore BSL and BSL Mobile Benchmarks, U.S., 2014 - 2016

Aided awareness

Favorability

Likelihood to recommend

Purchase Intent

1.3 2.6

1.3 2.9

1.5 2.8

1.3 4.0

Desktop Mobile

3.1xdesktop

1.9xdesktop

2.2xdesktop

2.0xdesktop

© comScore, Inc. Proprietary. 12

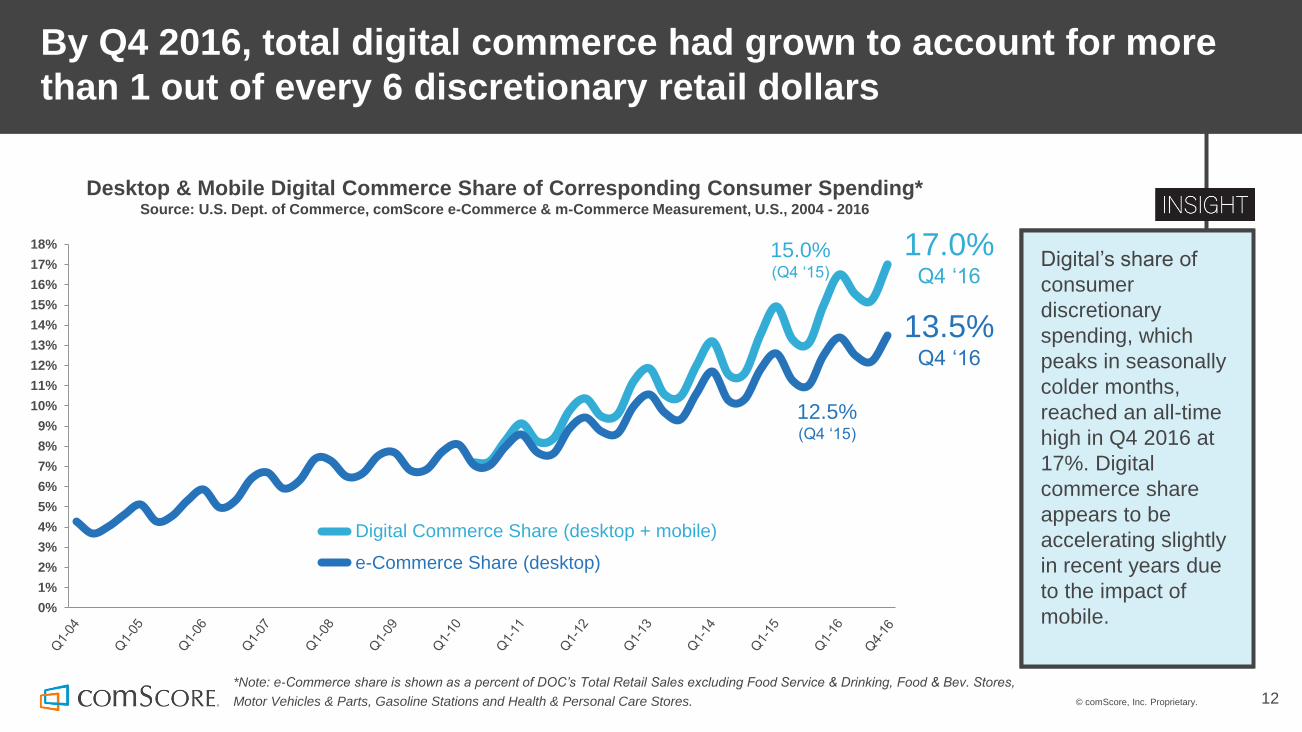

By Q4 2016, total digital commerce had grown to account for more

than 1 out of every 6 discretionary retail dollars

Desktop & Mobile Digital Commerce Share of Corresponding Consumer Spending*Source: U.S. Dept. of Commerce, comScore e-Commerce & m-Commerce Measurement, U.S., 2004 - 2016

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

17%

18%

Digital Commerce Share (desktop + mobile)

e-Commerce Share (desktop)

*Note: e-Commerce share is shown as a percent of DOC’s Total Retail Sales excluding Food Service & Drinking, Food & Bev. Stores,

Motor Vehicles & Parts, Gasoline Stations and Health & Personal Care Stores.

15.0%(Q4 ‘15)

13.5%Q4 ‘16

17.0%Q4 ‘16

12.5%(Q4 ‘15)

Digital’s share of

consumer

discretionary

spending, which

peaks in seasonally

colder months,

reached an all-time

high in Q4 2016 at

17%. Digital

commerce share

appears to be

accelerating slightly

in recent years due

to the impact of

mobile.

© comScore, Inc. Proprietary. 13

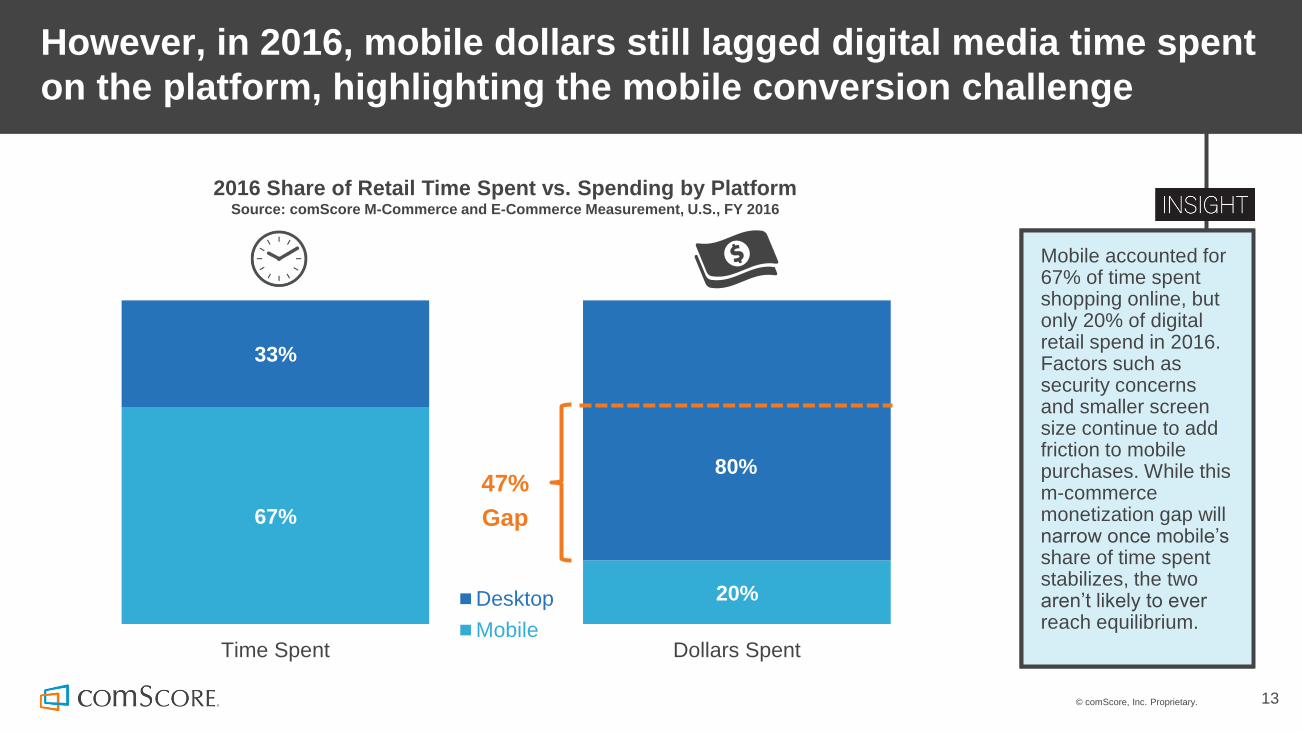

However, in 2016, mobile dollars still lagged digital media time spent

on the platform, highlighting the mobile conversion challenge

Mobile accounted for 67% of time spent shopping online, but only 20% of digital retail spend in 2016. Factors such as security concerns and smaller screen size continue to add friction to mobile purchases. While this m-commerce monetization gap will narrow once mobile’s share of time spent stabilizes, the two aren’t likely to ever reach equilibrium.

2016 Share of Retail Time Spent vs. Spending by PlatformSource: comScore M-Commerce and E-Commerce Measurement, U.S., FY 2016

67%

20%

33%

80%

Time Spent Dollars Spent

Desktop

Mobile

47%

Gap

© comScore, Inc. Proprietary. 14

As was the case in 2015, the Top 10 in 2016 featured mostly action movies and animated family-friendly films, with Disney distributing four of the top five films in 2016. Impressively, Star Wars: The Force Awakens cracked this past year’s Top 10 despite being released in mid-December 2015.

Finding Dory led the 2016 domestic box office as one of six Disney

films to rank in the Top 10

Top 10 Grossing Box Office Movies in 2016 ($ Millions)Source: comScore Box Office Essentials, North America, Jan. 1 – Dec. 31, 2016

$486.3

$408.2

$408.1

$368.4

$364.0

$363.1

$341.3

$330.4

$325.1

$284.7

Finding Dory

Rogue One: A Star Wars Story*

Captain America: Civil War

Secret Life Of Pets, The

Jungle Book, The

Deadpool

Zootopia

Batman V Superman: Dawn Of Justice

Suicide Squad

Star Wars: The Force Awakens

* Rogue One was released on December 16, 2016, and therefore was only in theaters the last two weeks of the year.

Warner Bros.

20th Century Fox

Universal

Disney

© comScore, Inc. Proprietary. 15© 2017 comScore, Inc.For info about the proprietary technology used in comScore products, refer to http://www.comscore.com/About-comScore/Patents

To download the full

73-page version

of this report,

please visit:

For more information about the report, please contact:

ANDREW LIPSMAN,

VP Marketing & Insights

ADAM LELLA,

Senior Marketing Insights Analyst

comscore.com/USFutureinFocus2017