Computation of total income

21

1 Computation of total income

Transcript of Computation of total income

1 Computation of total income

2 Computation of total income

3 Computation of total income

Acknowledgement

We are very thankful to everyone who supported us, for we have completed our project effectively

and moreover on time. We thank the group members for their contribution towards this project. We

also thank our classmates and friends for all the help they have offered.

We are equally grateful to my teacher Prof. Renu Tiwari; she gave us moral support and guided us in

different matters regarding the topic. She had been very kind and patient while suggesting us the

outlines of this project and correcting our doubts’. We thank her for her overall supports.

Last but not the least, I would like to thank our parents who helped us a lot in gathering different

information, collecting data and guiding us from time to time in making this project despite of their

busy schedules ,they gave us different ideas in making this project unique.

Thanking you.

Group 6 members

(8136-8144)

Class- SYBBI

4 Computation of total income

Index

SR NO PARTICULARS PAGE

NO.

1. Introduction 6

2. Inclusion and exclusion from tax 7

3. Types of total income 9

4. Tax liability 13

5. Steps to compute total income 15

6. Illustrations 17

7. Conclusion 21

9. References 22

5 Computation of total income

INTRODUCTION

MEANING OF TOTAL INCOME

Total income is just what the term implies -- the sum of all income from all sources. If there is no

qualifier (i.e. taxable or non-taxable) then it includes all income, even income that isn't taxable. If you

mean what is "total income" as defined on your tax form, it is just what it sounds like - the sum of

every source of taxable income that you have regards of where it came from, and before any

deduction, exemptions, or adjustments are applied.

Just add up all your wages, salaries, bonuses, pensions, rental income, business income, farm income,

taxable IRA distributions, taxable Soc Security benefits, interest, dividends, state tax refunds,

gambling winning, hobby income, jury duty pay, contests won, and anything else you can think of.

MEANING OF INCOME TAX

An income tax is a government levy (tax) imposed on individuals or entities (taxpayers) that varies

with the income or profits (taxable income) of the taxpayer. Details vary widely by jurisdiction. Many

jurisdictions refer to income tax on business entities as companies’ tax or corporation tax.

Partnerships generally are not taxed; rather, the partners are taxed on their share of partnership items.

Tax may be imposed by both a country and subdivisions thereof. Most jurisdictions exempt locally

organized charitable organizations from tax.

Income tax generally is computed as the product of a tax rate times taxable income. The tax rate may

increase as taxable income increases (referred to as graduated rates). Tax rates may vary by type or

characteristics of the taxpayer. Capital gains may be taxed at different rates than other income. Credits

of various sorts may be allowed that reduce tax. Some jurisdictions impose the higher of an income

tax or a tax on an alternative base or measure of income.

Taxable income of taxpayers resident in the jurisdiction is generally total income less income

producing expenses and other deductions. Generally, only net gain from sale of property, including

goods held for sale, is included in income. Income of a corporation's shareholders usually includes

distributions of profits from the corporation. Deductions typically include all income producing or

business expenses including an allowance for recovery of costs of business assets. Many jurisdictions

allow notional deductions for individuals, and may allow deduction of some personal expenses. Most

jurisdictions either do not tax income earned outside the jurisdiction or allow a credit for taxes paid to

other jurisdictions on such income. Non-residents are taxed only on certain types of income from

sources within the jurisdictions, with few exceptions.

Most jurisdictions require self-assessment of the tax and require payers of some types of income to

withhold tax from those payments. Advance payments of tax by taxpayers may be required.

Taxpayers not timely paying tax owed are generally subject to significant penalties, which may

include jail for individuals or revocation of an entity's legal existence.

6 Computation of total income

Inclusion and exclusion from income tax

INCLUSION:

Income from employment, retirement or survivors’ programs, interest, dividends, life insurance death

benefits, unemployment compensation and operation of a business are countable income. The

following are additional sources of income which have been determined to be countable:

1. Allowances – Reasonable value of allowances to a person in service in addition to base pay such as

Housing Allowance, Reserve Housing Allowance, Food Allowance, Supplemental Subsistence

Allowance, Combat Pay, Hostile Fire Zone Pay, and Imminent Danger Pay.

2. Complaint Settlement – Payments from EEO settlement, personal injury, tort, medical malpractice,

and other claims.

3. Cooperative (Co-op) Dividends – Cash dividends from rural cooperatives and similar entities are

countable income. Co-op dividends in the form of discounts on the purchase of merchandise or

services are not countable income.

4. Department of Labour Employment Programs – Income received by participants in programs

operated by the Department of Labour, such as the Green Thumb and the Older Americans

Community Service Employment program, is countable.

5. Dependency and Indemnity Compensation – This benefit program pays a monthly payment to a

surviving spouse, child, or parents of a deceased military service member or Veteran.

6. Gas Reserves – Income from a lease is countable as income for Department of Veterans Affairs

(VA) purposes. This is true whether it’s from a lease on the land or just the mineral rights or both. It’s

basically rent.

7. Gifts and Inheritance of Property or Cash – Gifts and inheritances are countable in the year

received. The value of the gift or inheritance of property is the fair market value of the property at the

time it is received.

8. Individual Retirement Account (IRA) Distributions – When an individual retirement account (IRA)

or similar instrument starts paying benefits, count the entire amount even though it represents a partial

return of principal.

EXCLUSIONS:

1. Caregiver Payments – Amounts paid to a wife or husband, mother or father, sister or brother,

daughter or son, or loving family member or friend – who cares for a Veteran are not counted as

income

2. Chore Service Payments – Amounts paid by the government entity to an individual to care for a

disabled Veteran in the Veteran’s home are not countable provided eligibility for the payments is

based on the disabled Veteran’s financial need. Payments are not counted if they are paid to a

dependent of the disabled Veteran where counting the payments would reduce the disabled

7 Computation of total income

VA beneficiary’s rate of pension and eligibility for the payments is based on the VA beneficiary’s

financial need.

Example: A spouse of a Veteran beneficiary is paid by the state to take care of the Veteran in their

home under a Chore Service program. Whether the state pays the spouse directly or pays the Veteran,

the payments are not countable.

3. Crime Victims Compensation Act Payments – Amounts paid by governmental entities to

compensate crime victims are not countable provided eligibility for the payments is based on financial

need.

4. Income Tax Refunds – Income Tax Refunds (including the Federal Earned Income Credit) are not

counted.

5. Inherited Property – The sale of inherited property is considered income if inherited and sold in the

same year. If sold in another year, proceeds from the sale are considered an asset.

6. Instalment Sale – The purchase of property using monthly installments in order to pay back sales

price.

a. Payments received until the sales price is recovered are not counted as income, but as assets.

b. After the sales price has been exceeded, any amount received will be counted as income.

7. Proceeds of Casualty Insurance – If a Veteran loses property due to fire, flood, theft, etc., and the

Veteran collects on an insurance policy; the amount received is not countable as long as it does not

exceed the value of the lost property.

8. Pension Payments – Available to Veterans, surviving spouses, and children, if the Veteran has

qualifying service and there is financial need. Veterans must also have a qualifying disability which

need not be Service-connected.

8 Computation of total income

Types of taxable income

a. Income from Salary

b. Income from House Property

c. Income from profits and gains of Business or Profession

d. Income from Capital gains

e. Income from Other sources.

Income from Salary

Salary includes the pay, allowances, bonus or commission payable monthly or otherwise or any

monetary payment, in whatever name called from one or more employers, as the case may be, but

does not include the following, namely: a. dearness allowance or dearness pay unless it enters into the

computation of superannuation or retirement benefits of the employee concerned. employer's

contribution to the provident fund account of the employee’s. allowances which are exempted from

payment of taxed. The value of perquisites specified in sub-section (2) of section 17 of the Income-tax

Act; It also includes the following:

a. Wages;

b. Any annuity or pension;

c. Any gratuity;

d. Any fees, commissions, perquisites or profits in lieu of or in addition to any salary or wages;

e. Any advance of salary;

f. Any payment received by an employee in respect o

f any period of leave not availed of by him;

g. The annual accreditation to the balance at the credit of an employee participating in a recognized

provident fund, to the extent to which it is chargeable to tax under Rule 6 of Part A of the Fourth

Schedule; and

h. The aggregate of all sums that are comprised in the transferred balance as referred to in sub-rule (2)

of rule 11 of part A of the Fourth Schedule of an employee participating in a recognized provident

fund, to the extent to which it is chargeable to tax under sub-rule (4) thereof

Income from House Property

9 Computation of total income

Income from House property is computed by taking what is called Annual Value. The annual value

(in the case of a let out property) is the maximum of the following:

•Actual Rent received

•Municipal Valuation

•Fair Rent (as determined by the I-T department)

If a house is not let out and not self-occupied, annual value is assumed to have accrued to the owner.

Annual value in case of a self-occupied house is to be taken as NIL. (However if there is more than

one self-occupied house then the annual value of the other house/s is taxable.) From this, deduct

Municipal Tax paid and you get the Net Annual Value.

From this Net Annual Value, deduct:

•30% of Net value as repair cost •

•Interest paid or payable on a housing loan against this house

In the case of a self-occupied house interest paid or payable is subject to a maximum limit of

Rs,1,50,000 (if loan is taken on or after 1 April 1999) and Rs.30,000 (if t he loan is taken before 1

April 1999). For all non-self-occupied homes, all interest is deductible, with no upper limits.

The balance is added to taxable income.

Income from profits and gains of Business or Profession

Under section 28 , the following income is chargeable to tax under the head “ Profits and gains of

business or profession”

a. Profits and gains of any business or profession

b. Any compensation or other payments due to or received by any person specified in section 28(ii)

c. Income derived by a trade, professional or similar association from specific services performed

for its members.

d. The value of any benefit or perquisite, whether convertible into money or not, arising from

business or the exercise of a profession.

e. Any profit on transfer of the duty free replenishment certificate.

f. Any profit on the transfer of the Duty Entitlement Pass Book Scheme.

g. Export incentive available to exporters.

h. Any interest, salary, bonus, commission or remuneration received by a partner from firm.

i. Any sum received for not carrying out any activity in relation to any business or not to share

any know how, patent, copyright, trademark etc.

10 Computation of total income

j. Any sum received under a Key man insurance policy including bonus.

k. Any sum received or receivable in cash or kind, on account of any capital asset other than land or

goodwill or financial instrument being demolished, destroyed, discarded or transferred, if the whole of

the expenditure on such capital asset has been allowed as a deduction under section 35AD applicable

from the assessment year 2010-11 onwards

l. Profit and gains of managing agency

m. Income from speculative transaction.

In view of section 2(13) business includes any (a) trade, (b) commerce, (c) manufacturer or (d) any

adventure or concern in the nature of trade, commerce, or manufacture. Though the definition is not

exhaustive, it covers every facet of an occupation carried on by a person with a view to earning with a

view to earning profit. Production of goods from raw material, buying and selling of goods to make

profit and providing services to others are different forms of “business”, profits arising therefrom are,

therefore, chargeable to tax under the head “ Profits and gains of business or profession”. The term

“business” is a word of wide import and in fiscal statutes in must be constructed in a broad rather than

a restricted sense.

Income from capital gains

S 2(14): Capital asset means property of any kind held by an assesse whether or not connected with

his business or profession. It however does not include the following:

1. Any stock-in-trade, consumable stores or raw materials held for the purpose of his business or

profession;

2. Personal effects, i.e., movable property (including wearing apparel and furniture, excluding

jewellery), held for personal use by the assesse or any member of his family dependent on him.

3. Agricultural land in India, not being land situated in the following:-

a. In any area which is comprised within the jurisdiction of a municipality (whether known as a

municipality, municipal corporation, notified area committee, town area committee, town committee,

or by any other name) or a cantonment board and, which has a population of not less than ten

thousand according to the last preceding census of which the relevant figures have been published

before the first day of the previous year; or

b. In any area within such distance, not being more than eight kilometers, from the local limits of any

municipality or cantonment board referred to in item (a), as the Central Government may, having

regard to the extent of, and scope for, urbanization of that area and other relevant considerations,

specify in this behalf by notification in the Official Gazette;

4. 6.5 per cent Gold Bonds, 1977, or 7 per cent Gold Bonds, 1980, or National, Defence Gold Bonds,

1980, issued by the Central Government;

5. Special Bearer Bonds, 1991, issued by the Central Government;

11 Computation of total income

6. Gold Deposit Bonds issued under the Gold Deposit Scheme, 1999 notified by the Central

Government.

Income from other sources

Income of every kind, which is not chargeable to income tax under the heads

• Salary

• Income from house property,

• Profits and gains of business and profession,

• Capital gains can be taxed under the head "income from other sources".

However such income should also not fall under income not forming part of total income under the IT

Act.

The following income shall be chargeable to income tax under the head "Income from other sources",

namely: -

1. Dividend;

2. Any annuity due or commuted value of any annuity paid under section 280D.

3. Any winning from lotteries, crossword puzzles, races including horse races, card games and other

games of any sort or from gambling or betting of any form or nature whatsoever.

4. Any sum, received by the assesse from his employees as contributions to any provident fund or

Superannuation fund or any fund set up under the provisions of the Employees State Insurance Act,

1948 (34 of 1948), or any officer fund for the welfare of such employees, if such income is not

chargeable to income-tax under the head "Profits and gains of business or profession";

5. Income from machinery, plant or furniture belonging to the assesse and let on hire, if the income is

not chargeable to income -- tax under the head "Profits and gains of business or profession".

12 Computation of total income

Tax liability

Tax liability is the amount of money a person owes the government in a year in terms of tax. This

amount is often calculated as a percentage of one’s income and varies according to income. A tax

liability is money that is owed for some type of tax. The term is typically used to refer to income or

business taxes owed to a national, regional, or local tax authority. For example, if a person owes 15

lakhs at the end of a tax year, that is his tax liability. Sometimes, however, a person also has tax

liability because of the sale of property or even because he receives an inheritance. In most

jurisdictions, a person or business calculates tax liability by using tax tables and formulas provided by

a tax authority, and deductions and credits can be used to reduce the amount owed

In most jurisdictions, people who earn above a very low threshold of income owe taxes to at least one

tax authority. For example, many people pay taxes each year to a national government. Often, the

taxes are a percentage of the amount of income a person has in a given year, which means liability

varies from person to person. Likewise, deductions for certain expenses and the care of dependents

may also affect a person’s tax liability.

Businesses can have tax liability as well. Depending, for example, on the way a business is structured,

it may be subject to personal taxes on income, such as in the case of a sole proprietorship, or corporate

taxes if it is a corporation. The various types of taxation a business may be subject to and the amounts

it will have to pay may depend not only on its structure, but also on the jurisdiction in which it is

located and the types of services or goods it sells. As with individuals, however, there are usually

deductions and credits a business can take to reduce the tax it owes.

Sometimes people have tax liability that is related to income from work or the operation of a business.

For example, if a person sells property, such as a home, car, or even an investment, he may be liable

for taxes on the sale. Likewise, a person who receives money in the form of an inheritance may be

liable for taxes as well. In some places, even such things as lottery winnings are subject to taxation.

In some cases, a person or business would normally have tax liability but has so many deductions and

credits that he doesn’t have to pay any taxes in a given tax year. For example, a person may owe 2

lakhs in a particular tax year. If his allowed deductions and credits equal 2 lakhs, however, he will

usually not owe taxes. Sometimes the deductions and credits are more than the taxes due. In some

cases, this may translate into a refund of money, even if the person did not pay taxes in that year.

TYPES OF TAX LIABILITY

Limited tax liability

Tax liability can be either unlimited or limited. Limited tax liability refers to the liability of parties

without permanent residence in India for income tax payments on income arising in India. Permanent

residence is the place where a party, an individual or a legal person, is deemed subject to tax liability

because of his domicile, residence, place of management or other similar conditions, and where he has

closer personal and business relations. The types of earnings specified in Article 3(1) to (9) are subject

to limited tax liability, such as income from employment, all types of pension payments, income from

personal services or businesses, income from intellectual property rights, income from the leasing of

movables (usufruct), and income from real estate and capital assets, e.g. gains from sales, dividends

and interests.

13 Computation of total income

Unlimited tax liability

Unlimited tax liability refers to the liability of those parties who permanently reside in the country for

income tax payment. The types of earnings that are subject to income tax liability under unlimited

head are income from employment, house property etc.

14 Computation of total income

Steps to compute total income

Income earned during the previous year (April 1, 2010 to 31st March 2011) is taxable in the

immediately following assessment year. It is imperative for individuals to have basic knowledge

about computing taxable income. We have tried to provide an elementary write up on this topic:

Steps 1 –

Income of salaried individual is to be computed under the following heads of income:

Income from Salary

Income from House property

Income from Business and Profession

Income from Capital Gains

Income from Other sources

While computing income under the aforesaid heads, applicable exemptions should be claimed as

provided in sections 10 to 13A. The provisions for clubbing of income should also be considered.

Step 2-

After computing the income under the different heads, losses of the year or brought forward losses of

the earlier years are to be set off. The income after such set off is called Gross Total Income (GTI).

Step 3 –

After computing the gross total income the deductions under chapter VIA should be claimed.

Step 4 –

The income arrived at after providing the deductions under chapter VIA is rounded off u/s 288A to

the nearest Rs. 10 and it is called Total Income or Taxable Income.

After computing total income, tax is computed on such total income at the rate applicable for the

relevant assessment year. For this purpose due consideration is to be made for long term capital gain

(LTCG). LTCG on transfer of specified listed shares, on which security transaction tax (STT) is paid,

shall be exempt. Further, the agricultural income is also to be considered for rate purposes.

Step 5 –

After adding the surcharge to the tax liability the relief u/s 89 is claimed.

15 Computation of total income

The tax liability arrived at after claiming the said relief is the final tax liability and in case proper

advance tax is not paid or the return is not filed within due date, the tax liability is to be further

increased by adding interest u/s 234A, 234B, 234C.

The aforesaid tax liability is then reduced by the prepaid taxes like TDS on own income or on income

of other person included in the total income of the assesse, Tax collected at source (TCS) and advance

tax paid.

If tax liability is more than prepaid taxes, the difference should be paid as self assessment tax and in

case where the prepaid taxes exceed the tax liability refund should be claimed.

16 Computation of total income

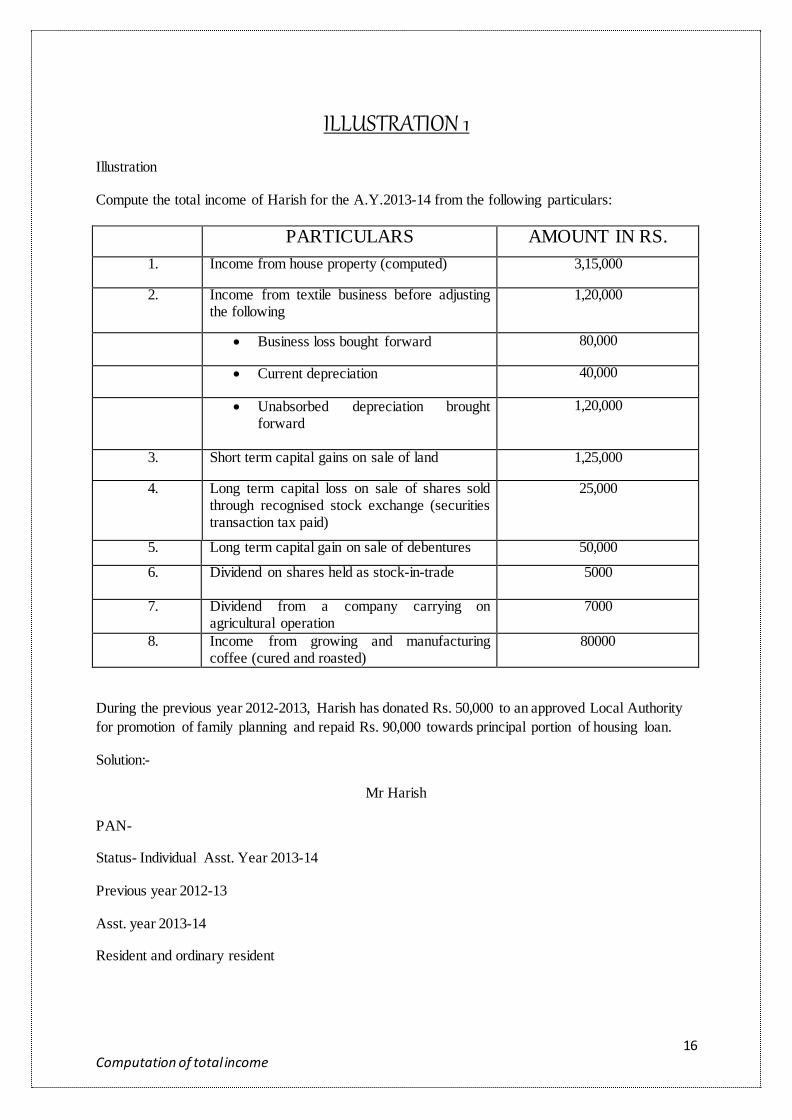

ILLUSTRATION 1

Illustration

Compute the total income of Harish for the A.Y.2013-14 from the following particulars:

PARTICULARS AMOUNT IN RS.

1. Income from house property (computed) 3,15,000

2. Income from textile business before adjusting the following

1,20,000

Business loss bought forward 80,000

Current depreciation 40,000

Unabsorbed depreciation brought forward

1,20,000

3. Short term capital gains on sale of land 1,25,000

4. Long term capital loss on sale of shares sold through recognised stock exchange (securities transaction tax paid)

25,000

5. Long term capital gain on sale of debentures 50,000

6. Dividend on shares held as stock-in-trade 5000

7. Dividend from a company carrying on agricultural operation

7000

8. Income from growing and manufacturing coffee (cured and roasted)

80000

During the previous year 2012-2013, Harish has donated Rs. 50,000 to an approved Local Authority

for promotion of family planning and repaid Rs. 90,000 towards principal portion of housing loan.

Solution:-

Mr Harish

PAN-

Status- Individual Asst. Year 2013-14

Previous year 2012-13

Asst. year 2013-14

Resident and ordinary resident

17 Computation of total income

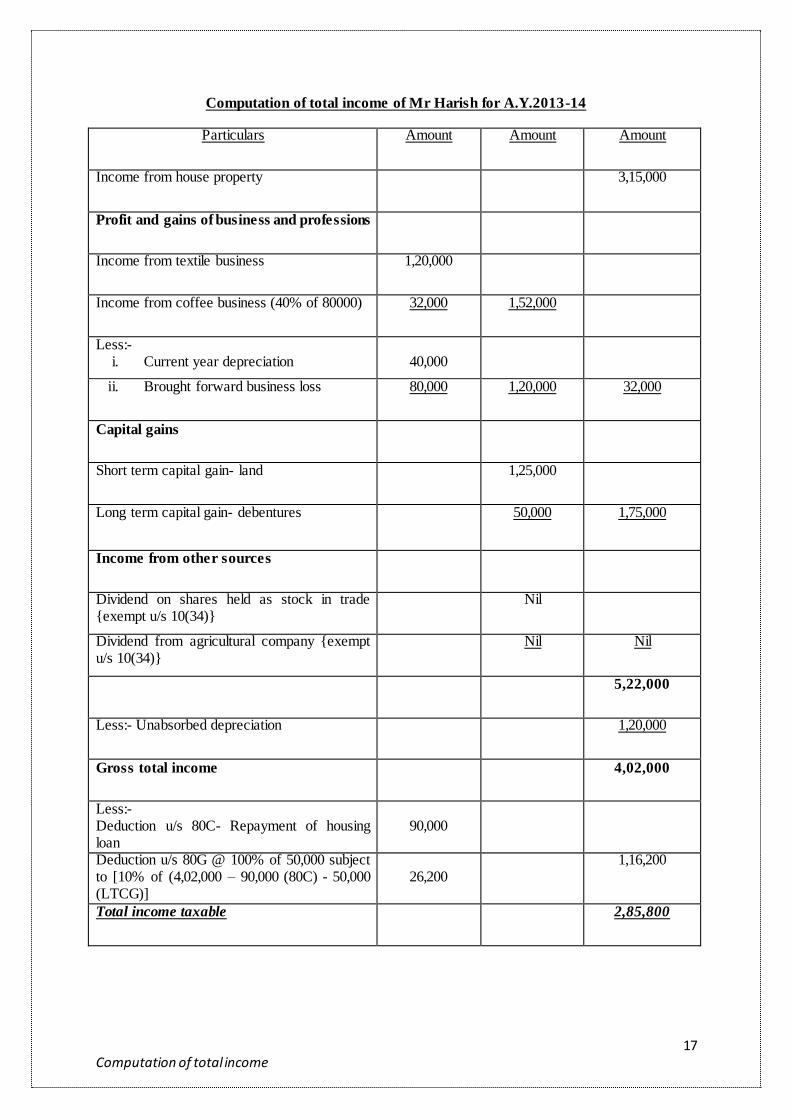

Computation of total income of Mr Harish for A.Y.2013-14

Particulars Amount Amount Amount

Income from house property 3,15,000

Profit and gains of business and professions

Income from textile business 1,20,000

Income from coffee business (40% of 80000) 32,000 1,52,000

Less:- i. Current year depreciation

40,000

ii. Brought forward business loss 80,000 1,20,000 32,000

Capital gains

Short term capital gain- land 1,25,000

Long term capital gain- debentures 50,000 1,75,000

Income from other sources

Dividend on shares held as stock in trade {exempt u/s 10(34)}

Nil

Dividend from agricultural company {exempt u/s 10(34)}

Nil Nil

5,22,000

Less:- Unabsorbed depreciation 1,20,000

Gross total income 4,02,000

Less:- Deduction u/s 80C- Repayment of housing loan

90,000

Deduction u/s 80G @ 100% of 50,000 subject to [10% of (4,02,000 – 90,000 (80C) - 50,000 (LTCG)]

26,200

1,16,200

Total income taxable 2,85,800

18 Computation of total income

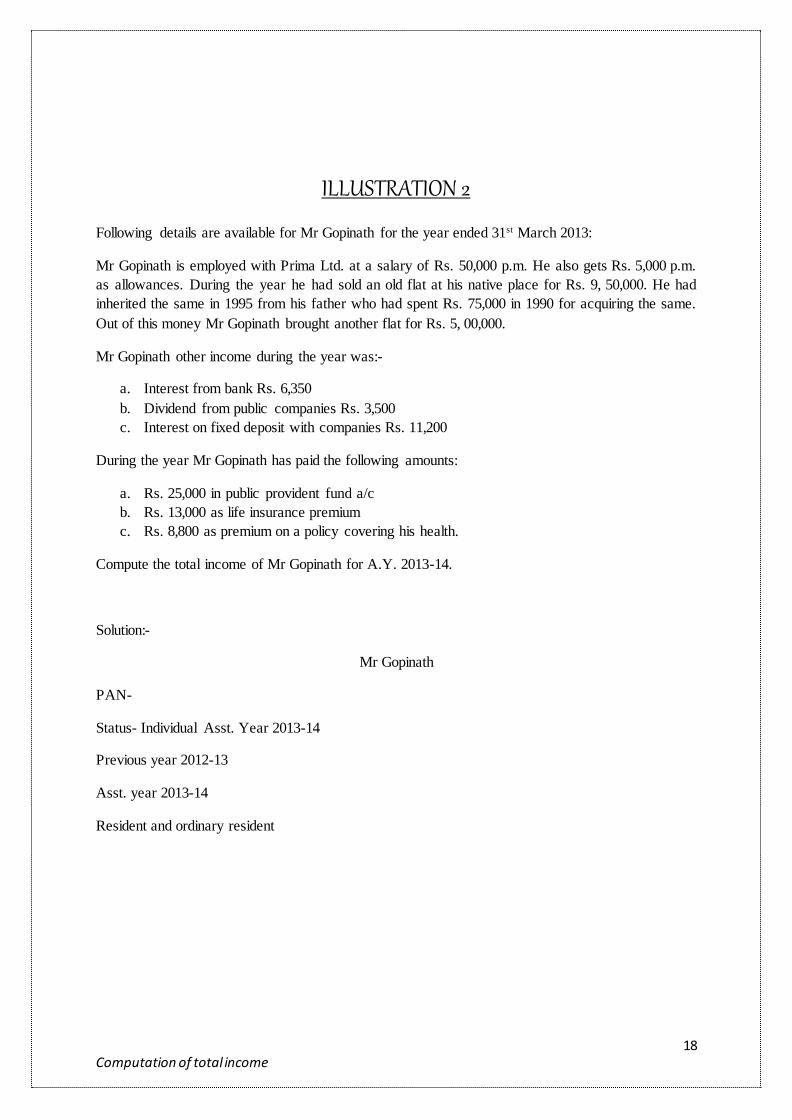

ILLUSTRATION 2

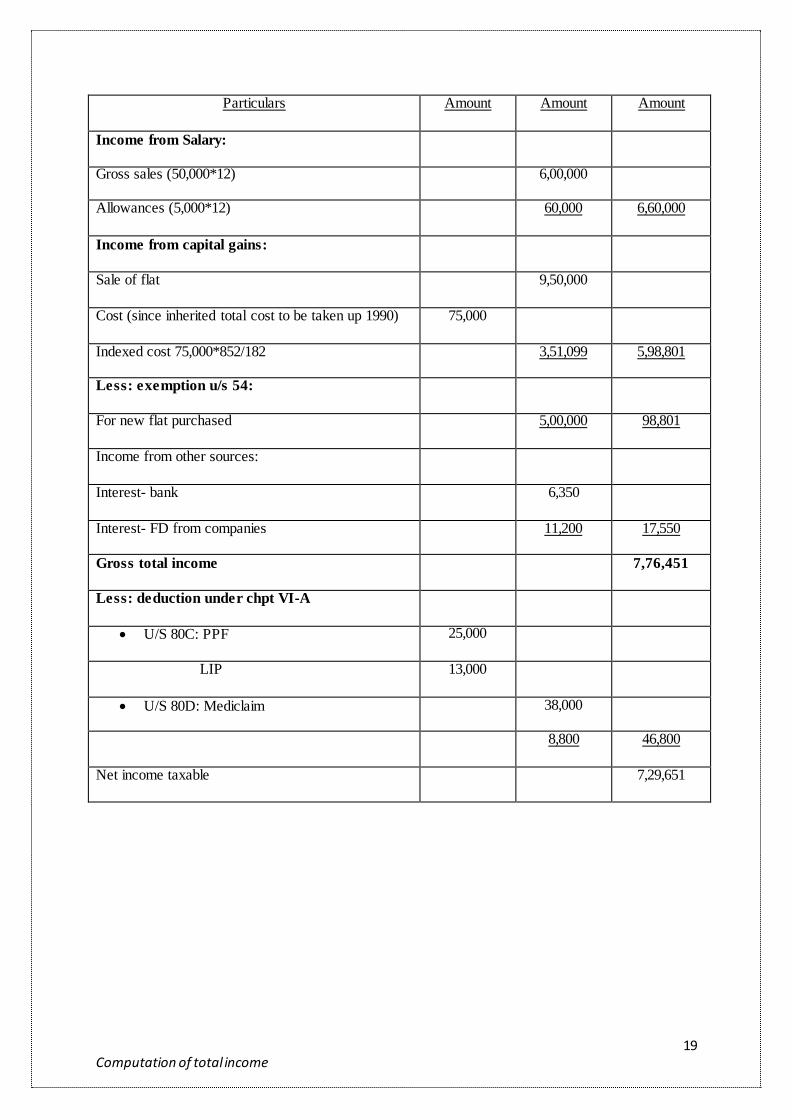

Following details are available for Mr Gopinath for the year ended 31st March 2013:

Mr Gopinath is employed with Prima Ltd. at a salary of Rs. 50,000 p.m. He also gets Rs. 5,000 p.m.

as allowances. During the year he had sold an old flat at his native place for Rs. 9, 50,000. He had

inherited the same in 1995 from his father who had spent Rs. 75,000 in 1990 for acquiring the same.

Out of this money Mr Gopinath brought another flat for Rs. 5, 00,000.

Mr Gopinath other income during the year was:-

a. Interest from bank Rs. 6,350

b. Dividend from public companies Rs. 3,500

c. Interest on fixed deposit with companies Rs. 11,200

During the year Mr Gopinath has paid the following amounts:

a. Rs. 25,000 in public provident fund a/c

b. Rs. 13,000 as life insurance premium

c. Rs. 8,800 as premium on a policy covering his health.

Compute the total income of Mr Gopinath for A.Y. 2013-14.

Solution:-

Mr Gopinath

PAN-

Status- Individual Asst. Year 2013-14

Previous year 2012-13

Asst. year 2013-14

Resident and ordinary resident

19 Computation of total income

Particulars Amount Amount Amount

Income from Salary:

Gross sales (50,000*12) 6,00,000

Allowances (5,000*12) 60,000 6,60,000

Income from capital gains:

Sale of flat 9,50,000

Cost (since inherited total cost to be taken up 1990) 75,000

Indexed cost 75,000*852/182 3,51,099 5,98,801

Less: exemption u/s 54:

For new flat purchased 5,00,000 98,801

Income from other sources:

Interest- bank 6,350

Interest- FD from companies 11,200 17,550

Gross total income 7,76,451

Less: deduction under chpt VI-A

U/S 80C: PPF 25,000

LIP 13,000

U/S 80D: Mediclaim 38,000

8,800 46,800

Net income taxable 7,29,651

20 Computation of total income

CONCLUSION

Taxes, which are the main source of federal, state and local government revenues, pay for buildings,

public education, highways, airplanes, rockets, road signs, and the salaries of millions of government

employees. Large amounts of tax revenues are raised from levies on personal incomes, including

investment income. The federal income tax is structured to tax different levels of income at different

rates, on a gradually increasing scale.

Taxes are an important aspect of nearly every person’s life. Your pay check is adjusted for taxes.

Contributions to charitable organizations are no doubt influenced by the expected tax savings. Taxes

affect the cost of owning a home, and tax considerations probably also influence the votes that are

cast in local, state and national elections. Taxation of investment income is also an important

consideration when deciding upon which investments to purchase, especially if you earn a substantial

income that’s taxed at a high rate.

Only without governments would there be no taxes; therefore, without taxes there would be no

governments. Taxation is one of the several ways by which governments raise money to pay for the

goods and services that they are called on to provide. Governments lack the major sources of revenue

available to other sectors of the economy and must therefore rely on taxes to finance the majority of

their expenditures. Unlike businesses, governments generally produce very few goods and services

that can be sold, especially at a profit. In addition, governments don’t have wage and investment

income as do individuals and families. Without these sources of income, governments have little

choice but to finance their spending needs by assessing businesses as well as individuals.

Governments are continually searching for additional funds to pay for the needs of their citizens,

businesses, and bureaucrats. At the local level, taxes support spending for schools roads, libraries,

athletic facilities, fire and police services, and the salaries of county and municipal employees. States

collect taxes for highway construction and upkeep, public colleges, buildings, and law enforcement.

The federal government levies taxes in order to provide its citizens with an interstate highway system,

a capable military force, health services, an Internal Revenue Service, thousands of parks and

monuments, and scores of other things.

Taxation, however, is not the only means by which governments finance their spending. They also

levy a variety of user and service fees to pay for parks, bridges, transit systems, parking complexes

and sports stadiums, where the users rather than taxpayers are expected to bear the operating costs of

the facilities. These fees, however, are frequently supplemented by special taxes. In addition,

governments at all levels regularly borrow funds to augment their tax revenues. In the 1980s and

1990s, the federal government borrowed billions and billions of dollars annually to pay for

expenditures that exceeded the billions and billions of dollars that it took in from tax revenues.

In summation, although unpopular (and many may argue, unfair), taxes are a necessity. The standard

of living of a modern society demands it; governments must collect the revenues in order to provide

the goods and services that their citizens need, want and demand.

21 Computation of total income

REFERENCES

http://www.icai.org/resource_file/19770ipcc_it_vol1_cp8.pdf

http://www.ctim.org.my/file/news/14/01516_Computation%20of%20Total%20Income%20for%20Ind

ividual%20-%20PR%2001-2005%20%28050205%29.pdf

http://www.caclubindia.com/articles/steps-to-computation-of-total-income-390.asp#.Uj6d4X9Ow-g

http://www.incometaxmanagement.com/Pages/Gross-Total-Income/Computation-of-Total-

Income.html

http://www.syndbankservices.in/UserFiles/sYN%20bANK.pdf

http://www.finweb.com/taxes/why-do-we-have-taxes.html#PxfRqJUoVeBJPOTp.99

THE END

Thank You

***********

![An Overview of Income Computation & Disclosure Standardsvoiceofca.in/siteadmin/document/11_07_17_ICDS.pdf · [income computation and disclosure standards] ... For Individuals having](https://static.fdocuments.us/doc/165x107/5f939edf9edd3508c04613cc/an-overview-of-income-computation-disclosure-income-computation-and-disclosure.jpg)