Competition Act 2010: What It Means · The Competition Act 2010: What it Means for ... Assoc. Prof....

36

(838740P) ISSUE 06 2012 Competition Act 2010: What It Means For The Financial Industry Bank Capital Evolution Financing Technological Innovation

Transcript of Competition Act 2010: What It Means · The Competition Act 2010: What it Means for ... Assoc. Prof....

C

M

Y

CM

MY

CY

CMY

K

fa1317_AIF AD_FinanceMagazine_march_ins_REV.pdf 2/23/12 5:57:20 PM

(838740P)

ISSUE 06 2012

CompetitionAct 2010:

What ItMeansFor TheFinancialIndustry

Bank CapitalEvolution

FinancingTechnologicalInnovation

Asian Link 2

Editorial Committee

3Editor's Note

4The Competition Act 2010: What it Means for the Financial Industry

8 Bank Capital Evolution

15Point of View:The World Needs a Second (and third) Reserve Currency

16The Impact of Demographic Trends on Economic Growth

21Financing Technological Innovation

24A Winning Talent Development Strategy

27E-Learning Guidelines

29The Rise of Asia and the Role of Human Capital: New Platforms for Economic Growth

DISCLAIMER: The Asian Institute of Finance does not represent nor warrant the completeness, accuracy, timelines or adequacy of this material and it should not be relied on as such. The Asian Institute of Finance does not accept nor assumes any responsibility or liability whatsoever for any data, errors or omissions that may be contained in this material or for any consequences or results obtained from the use of this information. This publication does not necessarily reflect the views or the positions of the Asian Institute of Finance.

Tan Sri Dr. Zeti Akhtar AzizChairman of the Board, Governor, Bank Negara Malaysia

Tan Sri Zarinah AnwarVice Chairman of the Board,

Chairman, Securities Commission Malaysia

Tan Sri Azman HashimChairman, AmBank Group

Dato’ Zukri SamatManaging Director, Bank Islam Malaysia Berhad

Dato’ Hj. Syed Moheeb Syed Kamarul ZamanPresident and CEO, Takaful Ikhlas Sdn Bhd

Dato’ Dr. Nik Norzrul Thani Nik Hassan ThaniChairman and Senior Partner, Zaid Ibrahim & Co

Dato’ Yusli Mohamed YusofNon-Executive Chairman, Mudajaya Group Berhad

Assoc. Prof. Low Chee KeongAssoc. Prof. in Corporate Law,

The Chinese University of Hong Kong

Mr. Hashim HarunPresident and CEO, Malaysian Re

Mr. Kung Beng HongDirector, Alliance Financial Group Berhad &

Alliance Bank Malaysia Berhad

Editor - Dr Amat Taap Manshor

Managing Editor - Dr Wan Nursofiza Wan Azmi

Assistant Managing Editor - Dr Zamros Dzulkafli

- Sarala J. Marimuthu

- Yogaretnam Kanagandram

Editorial Executive - Fara Iza Abd Rahim

AIF Board Of Directorscontentscontents

3 Asian Link

Human capital or talent is one of the most important

elements for growth and has been deliberated a lot among policymakers alike.

Nations and industries are dashing to find the right talent to remain ahead of

their competitors. For Malaysia to move forward, the issue is vital and need to be

addressed properly. And, as human capital investment is a long term continuous

proposition, its affiliation with economic growth and development has a longer

term perspective and calls for consistent commitments. As such, other human

capital related issues such as labour productivity, innovations, market size and

other demographic indicators are all important ingredients that drive the nation’s

competitiveness.

We should take heed from the Prime Minister, who recently suggested that

Malaysia would not be able to achieve the target to be a developed nation by

2020 if we cannot produce sufficient human capital with proper qualifications

and positive values. Malaysia, he said must use the benchmark of a developed

nation, with at least half of its citizens having access to tertiary education.

Latest figures show that only 33% of Malaysians have pursued education up

to tertiary level.

In this issue, we also highlight the views of Professor Tan Sri Dato’ Dzulkifli Abdul

Razak the speaker at the recent AIF’s Distinguished Speaker Series. Professor Tan

Sri Dato’ Dzulkifli propagated that the rise of the new Asia is about virtues and

about being responsible human beings. The courage to challenge the status quo

and work towards creating a new platform to build a better future are equally

essential and while economics is important, it should not be at the expense of

the economic ethics and community consciousness.

Malaysia’s population is expanding, albeit at a slower rate. So does our working

age population group, which will continue to provide us with the much needed

human capital for the foreseeable future. As such, strategies and policies must

be directed towards being competitive and sustaining economic growth.

Because, having the quantity without the necessary qualities will only impede

us from realising our growth potential, especially during the period coined as

the “new normal”.

Dr Amat Taap [email protected]

noteeditor'scontents

Asian Link 4

Legislation

COMPETITIONACT 2010

The term “competition” is not new to the financial industry in Malaysia. Integration in the banking sectors took place after the economic crisis in 1997 where some of the weak and ailing financial institutions were dissolved or merged with the stronger ones. The purpose was to ensure the financial industry delivers efficiency gains, and ultimately consumer welfare. Recently, the financial sector was also liberalized with the introduction of new foreign players and products which inevitably would push the domestic players to be more competitive in the provision of their products and services in the market.

While we understand that prudent considerations form the basis of a sound financial system for the country, the foundation of competitiveness must be built without compromising the basic competition principles enshrined in the Malaysian Competition Act 2010 which came into force on 1 January, 2012. Therefore, I will not be wrong if I say, competition and stability are not at odds.

Curtail Anti-Competitive PracticesFinancial services are vital to the functioning of an efficient market and to each and every one of us here today. They directly affect us as consumers. When financial services markets are integrated and competitive, they enable the most efficient allocation of economic resources. This is translated into better economic performance, better prices and better services for consumer and businesses.

Regulations by Bank Negara Malaysia alone are not enough. While these regulations tackle structural failures, competition policy is needed to address the harmful behaviour of individual market

participants. The introduction of such a policy will ensure that market evolve in a healthy manner and do not lead to the evolution of structures that harm users and others in the market. In particular we should also not encourage or rather we should prevent any one entity or group to control essential infrastructure. The aim is not to eliminate market power but to facilitate an environment that promotes competitive behaviour.

The Malaysian Competition Act 2010 provides the legal framework for curtailing anti-competitive practices in the market and applies to any commercial activity within Malaysia and also outside of Malaysia insofar as the activity which is transacted outside Malaysia has an effect on competition in any market in Malaysia. This therefore does not preclude the financial services sector.

The Competition Act 2010 introduces 2 main prohibitions, namely anti-competitive agreements and an abuse of dominant positions. Anti-competitive agreements between enterprises which are either horizontal or vertical in nature but have the object or effect of significantly preventing, restricting or distorting competition in any market for goods or services are prohibited.

Therefore, agreements between enterprises operating at the same level of business, which are horizontal; to fix purchase or selling price, sharing market or sources of supply, limiting or controlling production, market outlets or market access, technical or technological development, or investment, and bid rigging are strictly prohibited. This is because all these agreements are deemed to have the object of significantly preventing, restricting or distorting competition in any market for goods or services.

What It Means ForThe Financial Industry

By Tan Sri Dato’ Seri Siti Norma Yaakob

Asian Link 4

5 Asian Link

Meanwhile, vertical agreements between enterprises operating at different levels in the production or distribution chain would also breach the prohibition if the conduct mentioned earlier has the effect of significantly preventing, restricting or distorting competition in any market. To establish the said effect, in depth economic analysis has to be carried out besides determining the relevant market in which the alleged anti-competitive conduct has taken place. Vertical agreements are complicated in the sense that in most instances, they bring about efficiencies but nonetheless, if in any instance there is a complaint lodged, the Malaysia Competition Commission or MyCC will examine the case to determine if at all, it merits an investigation.

The second type of prohibition is the abuse of a “dominant position” by an enterprise in any market for goods or services. An enterprise is said to be in a dominant position if it possesses such significant power in a market to adjust prices or outputs or trading terms, without any restraint from competitors or potential competitors, regardless of the level or percentage of market share of the enterprise. Although such is the definition of dominant position, MyCC will inevitably consider an enterprise’s market share as one of the criteria to determine its market power.

An abuse of dominant position occurs amongst others, where such enterprise imposes unfair prices or unfair trading conditions on any supplier or customer; controls production, market outlets or market access, technical or technological development, or investment; refuses to supply to a particular enterprise or group of enterprises; engages in discriminatory practices for equivalent transactions; makes a contract conditional upon the acceptance by the other party of extraneous terms; engages in predatory behaviour towards competitors, or buys up, without any reasonable justification, scarce supply of intermediate goods or resources needed by a competitor.

Exemptions or ExclusionsThe Act provides several grounds for exemptions or exclusion from the application of the law. Some activities, though prima facie are commercial in nature do not fall within the definition of “commercial activity” as the activities are not commercial per se. The law also provides for the application of an individual exemption or a block exemption for particular category of agreements in so far as the agreements meet the relief of liability tests set in section 5 of the Act. For the moment, the prohibitions do not apply to agreements entered into pursuant to a legislative requirement, collective agreements governing employment terms, and enterprises engaged in providing services of general economic interest or in the nature of a revenue-producing monopoly where the prohibitions would obstruct the performance of their tasks. However, in this case the Minister of Domestic Trade, Cooperatives and Consumerism is empowered to amend this category of activities.

5 Asian Link

Asian Link 6

Based on these exclusions, the prohibition under sections 4 and 10 of the Act, i.e. anti-competitive agreements and abuse of dominant positions shall not apply to any anti-competitive practices by banks and other financial institutions provided those activities or conduct are carried out in order to comply with legislative requirements, such as the Banking and Financial Institutions Act 1989 (BAFIA) or any other laws in force to which the banks and financial institutions are subjected to. However, if agreements or conduct engaged into by banks and other financial institutions are not spelt out in the said legislations, then those conducts may constitute infringements.

This can be illustrated with an example. If under the BAFIA or any other relevant legislation, it is provided that Bank Negara Malaysia can fix rates for penalty for defaults for credit card payments, this conduct may not be caught under the Competition Act although fixing rates or trading conditions may be anti-competitive. However, if competing banks collude to fix such rates and other trading conditions or a bank which is in a dominant position imposes unfair trading conditions like tying or bundling, for example insurance coverage with no options given to the customer, this may constitute an infringement. In any event, the law does not prohibit the dominant bank from taking any steps which are deemed to be “reasonable commercial justification”.

Promote Market EfficiencyIn almost every country the financial sector is concentrated; this to some extent is deliberately done in order to ensure stability. Excessive competition in the banking sector leads to greater instability and more market failures, other things being equal. Excessive competition could also put more pressure on profits and may create higher incentives for banks to take greater risks resulting in greater instability. On the other hand, a higher concentration of larger firms is also thought to increase contagion risk. This will then need supervision because larger banks offer an array of services, making them more complicated to monitor. Therefore, the goal of having the Competition law to the financial sector is to ensure that the actual evolution of the market does not lead to structures that harm users and legitimate market participants.

The question that arises is: Does this new law have any implication on the financial sector? As mentioned earlier, the law applies to all commercial activities unless the activities are exempted or excluded under the law. As competition can contribute to promote market efficiency, the application of the competition law to this technically complex but economically significant sector is crucial and is a priority. The Malaysian Competition Act is very much modelled against the European competition legislations and jurisprudence. In recent years, the European Competition Commission through its vigorous enforcement actions and the European Court of Justice’s decisions has put to rest the notion that the regulated financial sectors might be protected from the competition law. The European Commission’s financial sector inquiries evidenced that the prices of certain products were rigid and there were low customer mobility, suggesting a low level of competition. The focus was on the retail banking market and the insurance market.

Among the issues identified are those activities revolving around credit cards. Issues like high entry barriers, high degree of concentration among credit cards’ issuers and acquirers, imposition of unfair trading terms and applying different trading conditions to equivalent transactions were some of the activities of card issuers like VISA and Mastercard. All these point towards lack of sufficiently robust competition in this particular sector.

The European case of Morgan Stanley/Visa International and Visa Europe (Case COMP/D1/37860) OJ C 183, 5.8.2009 illustrates a case of anti-competitive agreements involving credit card issuers. The brief facts are these. Morgan Stanley Bank Independent International (MSB) which is a subsidiary of Morgan Stanley, US established its operations in the UK in 1999. Whilst its parent operates the Discover card network in the US, MSB applied for Visa membership in March 2000 as Visa was a more widely accepted card in the UK and Europe. However, Visa International Service Association has “membership rules” among which the applicants who operate a credit card system that is deemed to compete with Visa’s credit card system are rejected.

Tan Sri Dato’ Seri Siti Norma Yaakob

Asian Link 6

7 Asian Link

Based on data and evidence collected, the European Commission (EC) found the followings:

UK merchants prefer banks that provide credit card package •of both Visa and MasterCard and that Visa Card transactions comprise 60% of all credit/debit/charge card transactions in the UK.In addition to its relatively small market share in the •US, Morgan Stanley’s Discover card system has limited international acceptance.The Discover credit card cannot be introduced into the •European Economic Area (EEA) because of prevailing (legal and regulatory) barriers to market entry.The relevant market (in UK) defined the market as the “credit •and deferred debit/charge card acquiring market”.MSB’s entry into the relevant market could be reasonably •expected to have a positive and competitive effect on the prices and quality of credit and debit card and charge card acquiring services.

Pursuant to the EC’s findings, Morgan Stanley and Visa Europe concluded a settlement agreement in September 2006. As a result, Visa Europe granted MSB an unconditional membership of Visa’s credit card scheme and Morgan Stanley withdrew its competition complaint filed with the EC in April 2000. Nonetheless EC found Visa International and Visa Europe to have (jointly and severally) breached Article 101 Treaty on the Functioning of the European Union by excluding, without objective justification, MSB from Visa’s credit card network. Subsequently, Visa was fined €10.2 million.

Long Term Stability and Efficient GrowthMost of the financial sectors’ activities in Malaysia are regulated by Bank Negara Malaysia pursuant to various legislations. Under the Competition Act 2010, although an agreement or conduct is anti-competitive or an abuse of dominance, it is excluded from the application of the law if such agreement or conduct if done in compliance with a legislative requirement. However, activities and conduct which do not fall within the purview of Bank Negara Malaysia but are exercised extraneously by the banks could have anti-competitive effects. One example could be when subjecting the borrower to accept supplementary conditions which may not have any connection to the main subject matter of the contract or better known as bundling or tying. This is normally exercised by an entity in a dominant position. The new competition law is expected to have far-reaching implications on trade and businesses by encouraging efficiency, innovation and entrepreneurship by protecting the competition

The Malaysian Competition Act 2010 provides the legal framework for curtailing anti-competitive practices in the market and applies to any commercial activity within Malaysia and also outside of Malaysia insofar as the activity which is transacted outside Malaysia has an effect on competition in any market in Malaysia.

process. In so far as the financial industry is concerned, its competitiveness should be truly reflected in their products that are made available to the consumers through competitive pricing, improvement in the quality of products and services and the availability of wider choices.

In view of the new competition regime, players in the financial sectors should to stay vigilant and identify and review areas that could have potential anti-competitive business practices. CEOs and Directors should also ensure that their companies adopt and adhere to competition policy and culture in their respective organisations. Many financial institutions by now would have their own competition law compliance programmes for their management and staff with a view to identifying problematic business practices and minimizing the risk of competition law infringement.

Competition Compliance programmes should include formulation and dissemination of a compliance manual, operation of education or awareness programmes, establishment of a monitoring system and provisions of sanctions to be meted out to individuals who violate competition related laws.

Investigation of a competition related matter would incur a large amount of administrative resources to the entity suspected of committing an infringement of the competition law. Beside the huge penalties that could be levied, the offending entities will also need to incur legal costs. Officers responsible for the management of the entity also risk being punished while the consequence of such an action by the competition authority could tarnish the corporate image of the entity. But when compliance programs are put in place and when companies voluntarily abide by competition laws, law enforcement and the repercussion of action for non compliance could be minimised.

Competition enforcement and financial regulation are not meant to stifle growth in the industry. In fact both the regulators, in this case Bank Negara Malaysia and MyCC would work closely to ensure that the financial market develops in ways that are compatible with long term stability and efficient growth.

Tan Sri Dato’ Seri Siti Norma Yaakob is Chairman of Malaysia Competition Commission. She also sits on the Boards of Tenaga Nasional Berhad, KAF Investment Bank Berhad, RAM Holdings Berhad, RAM Rating Services Berhad and RAM Rating (Lanka) Limited. She is also the Pro-Chancellor of the University of Malaya and since April 2011 assumed the Chairmanship of the Malaysia Competition Commission. This is an excerpt from the speech she delivered at the 4th AIF Distinguished Speaker Series held in Kuala Lumpur.

7 Asian Link

Asian Link 8

Capital1 is particularly critical to banks since they generally operate at a high degree of leverage. Only a sliver of capital separates solvency from insolvency. A slight decline in asset value could spell disaster for a bank, obliterating its entire capital and “eating” into debt thus affecting its ability to fully repay its creditors. Conversely, a small increase in asset value is a boon to shareholders. This payoff is naturally to the advantage of shareholders who commit a very small fraction of the total funding relative to depositors but potentially enjoy a huge upside. It’s almost cliché yet true in financial circles to say “Heads, I win, Tails you lose” – referring to shareholders who revel on the upside whilst depositors or tax payers pick up the tab on the downside.

Capital Deliberations Way Back WhenThe idea of capital as a general indicator of a bank’s financial health is not a recent phenomenon. It has been documented as far back as the 1840s where the capital to asset ratio for banks in the United States was in the region of a conservative 50%. Since then, the capital levels had generally been on the decline.

For a long time, regulators worldwide were well aware of the notion of capital as a cushion against insolvency but did not reach a consensus on the details. Each jurisdiction had its own version. Some focussed on capital to asset ratio; others scrutinised capital to deposits ratio and those who attached risk weights to assets could not agree to a uniform set. Despite this,

1 Capital in this context represents the owners’ interest in a business or equity

BankCapitalEvolution

By Yogaretnam Kanagandram

9 Asian Link

Bank

the models are variants of the same theme - that capital is a margin of safety for creditors and the larger it is the more financially secure the entity is from insolvency.

Authorities have also long realised the macro implications emanating from the collapse of a large multinational bank. In this respect, the acronym SIFI was recently coined not in reference to “science fiction” but “systemically important financial institution”. They were conscious of the interdependency of financial institutions. It is of little help to be an exceptionally profitable, stable and solvent bank when surrounded by banks that are going bust. Sooner or later the contagion will adversely impact the financials of the healthy bank. This was brought to the fore in 1974 when Herstatt, a German Bank, collapsed before fulfilling their corresponding foreign exchange obligations resulting in a punishing counterparty settlement failure and a great loss of confidence in the payments system. The story was that several banks in trading foreign exchange had released payments denominated in Deutchemarks and waited for the equivalent in dollars. The German authorities in the meantime forced its closure due to its insolvency. When the US banks opened for business, Herstatt’s correspondent bank was barred from making the payments as they probably would have been construed as illegal preferential repayment.

On another front, Japanese banks grew by leaps and bounds in the 1980s. Only one Japanese bank featured amongst the top 10 largest banks in the world in 1981. But by 1988, nine of the top 10 largest banks were Japanese. In the same period, Japanese banks’ share of the total assets of the top 20 largest banks soared from just over a quarter to in excess of 70%.

What was the octane that boosted their balance sheets? It’s leverage. Japanese banks were very much more leveraged than their western counterparts that they could literally undercut the market in enticing loans. For instance from 1981 to 1988, Dai-Ichi Kangyo’s equity to assets ratio declined from 3.26% to 2.41% whereas Bank of America’s ratio increased from 3.54% to 4.45%2. I personally recall a conversation amongst offshore bankers in Labuan in the early 1990s where a few Malaysian banks submitted bids to extend a loan priced in the neighbourhood of 40 to 50 basis points above the London Interbank Offered Rate when a Japanese bank swooped in with an un-contestable 28 basis points above the same!

Why would anyone tolerate credit exposure to poorly capitalised banks? There were substantiated allegations that

2 The Banker

Asian Link 10

the Japanese government supplied implicit and explicit safety nets, such as guarantees to provide a measure of assurance for parties dealing with the banks.

The Committee

From the ashes of the Herstatt debacle, the G-10 nations at the end of 1974 formed the Basel Committee on Banking Supervision (Committee) – so named because its secretariat was located in the Bank for International Settlements in Basel Switzerland. The Committee is primarily a forum for regular cooperation on banking supervisory matters. Its objective is to enhance understanding of key supervisory issues and improve the quality of banking supervision worldwide. This Committee was instrumental in the formulation and subsequent evolution of the Basel Accords. To clarify, the Committee has no supranational power to force any nation to adopt the capital frameworks it dishes out.

In the wake of the Latin American crisis in the 1980s, there were calls from the US Congress to raise capital levels of US banks. Well aware that this would weaken the competitiveness of the US banks, the Congress urged the Federal Reserve Board and the Treasury Department to “encourage” the powers that be of other major banking countries to work towards maintaining and strengthening the capital bases of internationally active banks.3

Initial presentation to the Committee by Paul Volcker, the then Federal Reserve Chairman in 1984 was met by unenthusiastic response. Later in 1986 the US and UK, reached a bilateral agreement on capital standards after

extensive interactions. They then added momentum towards capital convergence intimating that foreign banks seeking to set up shop in their jurisdictions or acquire their banks may need to observe these standards. Operationally, it was executed by requiring capital adequacy data in conformity with categories and definitions of the bilateral agreement. Although the Japanese bankers resisted, the Japanese Ministry of Finance agreed to the arrangement but not without concessions from the rest of the Committee members.

The chart below depicts the average capital level of the largest US banks in the 1970s. Those with assets in excess of US$5 billion had declined by as much as 21% in that decade whilst the 17 largest multinational banks declined even more significantly by 26%. The increased vulnerability of large banks naturally increased the precariousness of the financial system worldwide.

The 1988 Basel Accord

Basel 1 (as it is commonly known) was concluded in 1988. Besides the intention to achieve worldwide financial stability, it was also meant to level the bankers’ playing field. The latter made it a trade negotiation of sorts. In a nutshell, Basel 1 required banks to set aside a minimum of 8% of its risk-weighted assets as capital i.e. Total Capital/Total Risk-Weighted Assets ≥ 8%.

No tangible rationale can be extracted from the 28-page document as to why 8% was chosen except that it was agreed “in the light of consultations and preliminary testing of the framework”. The essence of

the Accord was in the definitions as to what constituted capital, the risk weights of the various classes of assets and the conversion factors of off-balance sheet items to bring them to on balance sheet equivalents. The general idea is that capital consumption should be concomitant to the perceived riskiness of the assets. Some compromise was achieved in order to make the accord more palatable to the banks. The respective supervisory authorities who chose to subscribe to the

accord were given some leeway to adjust the framework to fit their local banking conditions.

3 International Lending and Supervision Act

Note: All figures are percentage of equity capital to total assets.

Source: Board of Governors of the Federal Reserve System (1983)

11 Asian Link

Basel 1 in 2 Minutes

All assets of a bank are attributed one of five risk weights – 0%, 10%, 20%, 50% and 100%. A low risk asset like cash

or central government obligations is assigned a 0% risk weight. Hence, a RM100 million amount in this category

would attract no capital requirement since 100 million x 0% (risk weight) x 8% = 0. On the other hand, a RM100

million exposure in a typical business loan would require a capital of RM8 million [i.e. 100 million x 100% (risk

weight) x 8%] to underpin the risk. An exposure to a Bank is considered an intermediate level risk, consequently

a RM100 million loan to a bank would require 100 million x 20% (risk weight) x 8% = RM1.6 million capital. It is

noteworthy that all assets including the kitchen sink had to be weighted. Hence, if you have no where to put

them, by default they come under the broad brush of 100% risk weight. A novelty of Basel 1 which is sustained

through subsequent accords is that off-balance sheet items, be it contingent claims such as guarantees or

counterparty exposures in over-the-counter derivatives, are first brought onto the balance sheet by prescribed

credit conversion factors before subjecting the resultant to the foregoing risk weights.

When Basel 1 was first announced, many banks had difficulty meeting the minimum requirement. As a compromise, the banks were given a four-year transition period from 1989 to 1992 where the minimum capital requirement was imposed in equal increments from 7% to 8%. The Committee acknowledged that the framework assessed capital only in relation to credit risk and admitted that other risks such as interest rate risk needed to be taken into account in assessing overall capital adequacy. To largely redress this, in 1996, a framework to derive capital cushion for market risk mainly for the trading book was added to the Basel 1 framework. It was also a paradigm shift by the Committee when it allowed banks the option to use their respective internal models to derive market risk capital charge. However to ensure model integrity, onerous parameters and requirements had to be met before the figures could be accepted.

Basel 1 was originally meant for “internationally active” banks since they fit the bill for systemic risk in the event of a collapse. However, the framework soon had a large following due to its simplicity, practicality and robustness. Even today, notwithstanding the subsequent significant upgrades of Basel 2 and the impending Basel 3, many banks still adhere to Basel 1. Despite its misgivings, it is still better than what existed before. Its consistency in definitions and calculations has made it an international benchmark.

Currently, Basel 1 is either applicable to all banks within a jurisdiction or a dichotomy exists with simpler banks subscribing to Basel 1 whilst the sophisticated ones adopting the more state-of-the-art framework. Ironically at the time of writing, the US which had played a major role in driving the Basel 2 development, has most of its banks on Basel 1 with only a handful of large internationally active

banks on the advanced version of Basel 2. In Malaysia, Development Financial Institutions such as Agrobank and EXIM Bank, are still on Basel 1 discipline. It’s probably sufficient given that they are mainly the uncomplicated deposit-taking and lending outfits. The Malaysian commercial and investment banks however are keeping up with the latest framework.

Concept of “Basel” Capital

Capital is demarcated into Tier 1 – the high-grade form which regulators love to see plenty of and a low-grade Tier 2 which as a compromise, was given limited recognition. Tier 1 capital in gist represents the commitments or investments of the true owners of a business. Typically, they include ordinary share capital, retained earnings, share premium and certain specific reserves. Qualitatively, they would have the following credentials:

paid-up •freely and permanently available to absorb losses in •the course of an on-going business represent no fixed charge on earnings and•rank below the claims of all creditors in the event of •liquidation

What about non-cumulative perpetual preference stock? It’s a type of capital which to all intents and purposes is equity except that dividends and/or capital repayments upon liquidation rank ahead of equity shareholders. After some lobbying by the US, it was justifiably included in the Tier 1 category.

The lower quality Tier 2 is a fascinating capital grade.

The finance textbooks of the pre-accord era would have

labelled them as liability or even expense. We could

picture them in the grey area, sandwiched between

Asian Link 12

pure equity and pure liability. They may add strength to the banks’ balance sheets, but in reality do not possess all the entrepreneurial risk-taking characteristics of Tier 1. Included under Tier 2 are undisclosed reserves – i.e. reserves that have passed through the income statement but by virtue of subsequent perhaps excessively prudent expense/income recognition results in accumulation of secret reserves. Due to the lack of transparency and objectivity, such practices are not encouraged in most jurisdictions.

Asset revaluation reserve is another interesting Tier 2 item with a story to tell. It comprises of two types. - one arising from a formal revaluation process and is reflected on the balance sheet and the other was the subject of intense Japanese lobbying. During the halcyon asset-bubble days of the 1980s, Japanese banks sat on large holdings of quoted securities whose market values far exceeded their purchase prices. These substantial unrealised amounts were not reflected on the financial statements perhaps in the name of prudence. The Japanese wanted these latent profits to be recognised as capital. The Committee compromised but not without a brutal 55% discount.

Other instruments allowed as Tier 2 capital are general provisions on loans – recognition of which was subject to a limit of 1.25% of risk-weighted assets; hybrid instruments such as cumulative preference shares, so long as they can absorb losses without triggering liquidation; and subordinated debts - capped in amount at 50% of Tier 1 and subject to an amortising schedule over its last five years due to the absence of the key quality of being able to absorb losses in the course of an on-going business.

In aggregate because of its doubtful qualities, amount recognised as Tier 2 capital was not permitted to exceed Tier 1. In other words, Tier 1 had to comprise at least 50% of recognised capital. The recent global financial crisis revealed serious shortcomings of Tier 2 capital, particularly in loss absorbency. As such under Basel 3 they will play a smaller role.

Capital DeductionsCertain bank assets, in the eyes of the authorities, have rather dubious value. Hence prudently they recommend that such assets be charged-off before arriving at regulatory

The essence of the Accord was in the definitions as to what constituted capital, the risk weights of the various classes of assets and the conversion factors of off-balance sheet items to bring them to on balance sheet equivalents.

capital. This is an extremely punitive treatment compared to the alternative of weighting the assets and applying 8% minimum capital charge. If you do the math, every dollar charged-off would imply a loss of support of asset value of up to twelve-and-a-half times.

To describe a few, ...Goodwill due to its intangible nature is given the •harshest treatment – direct deduction from the high grade and precious Tier 1. The framework was meant to be applicable on a •consolidated basis to banking groups since consolidated accounts will fully reflect the entire group’s assets. Therefore any investment in unconsolidated subsidiaries be it financial institutions or otherwise, is deducted from total capital. This takes care of double-leveraging on the same capital. Bank Negara Malaysia takes the less punitive approach of deducting firstly from Tier 2 before impacting Tier 1.

Likewise the same treatment is accorded to substantial •

minority interest in financial institutions as well as

any holdings of bank capital instruments. The latter,

however, are exempted from deduction under

certain circumstances such as acquired incidental to

underwriting activities but only for the first 90 days

after issue. During that period it’s subject to the less

punitive trading book market risk capital charge. Market

risk charge instead of capital deduction is also applied

where the bank holds the bank capital instruments for

trading or market making purposes.

In the years following Basel 1, asset-backed securitisation •

grew in popularity, partly for the dubious reasons of

exploiting the framework’s loop hole. After slicing

and dicing the assets to be securitised, the banks are

often left holding highly toxic or risky assets. These are

understandably deducted from capital – Tier 2 followed

by Tier 1.

The foregoing is not an exhaustive list. Subsequent Basel

pronouncements have suggested other deductions

including net deferred tax asset (since its value can only

be reaped in the future only if and when a taxable profit is

registered) and gain on sale in a securitisation. Gains and

losses arising from changes in own credit risk on fair valued

liabilities is derecognised.

13 Asian Link

Necessity as they say is the mother of invention. A new breed of capital instruments turned up on the horizon - designed to please regulators, shareholders, creditors and the investors of the instrument. They are structured to meet the stringent Tier 1 requirements. These are essentially hybrid instruments, in substance containing equity features necessary to shore up capital but made up to look like debt thus disclosed as such with no adverse impact on earnings per share, return on equity and perhaps receiving favourable tax treatment. However, due to their inherent encouragement to redeem usually via step-ups as well as the possible legal uncertainties amidst the complex structures to support as a going concern in the event of stress ….. under Basel 3 they will be phased out albeit over 10 years commencing 2013.

Basel 2 in Essence

The 239-page technical document of Basel 2 was a mind-boggling quantum leap of complexity over the corresponding 28-page Basel 1. Though the minimum capital ratio remained unchanged at 8%, in absolute terms it had increased due to the introduction of a capital charge to underpin operational risk. Mathematically, the basic idea of Basel 2 can be summarised as follows:

Capital / [Credit RWA + Market RWA + Operational RWA] > 8%

RWA – Risk Weighted Asset

Radical changes were made in the derivation of credit risk capital charge. Basel 1 adopted a club-based approach in determining creditworthiness of an obligor. Those who were members of the Organisation for Economic Co-operation and Development (OECD) were regarded as more creditworthy than those who were not. It translated into favourable risk weights for banks and sovereigns from the OECD. A US dollar loan to the central government of an OECD member required no capital, implying no risk whilst the same to a non-OECD member bore the full capital charge. Oddly as a consequence, Turkey and Mexico which had at one time defaulted on their foreign currency bank debt, fetched lower risk weight compared to non-members like Hong Kong and Singapore.4 Basel 2 sharpened capital consumption with the degree of risk by basing capital charge on either externally or internally developed ratings. A more comprehensive framework

4 Turkey and Mexico defaulted in 1978 and 1982 respectively – Federal Reserve Bank of New York “Current Issues on Economics and Finance June 1995 5 Basel III: A global framework for more resilient banks and banking systems

was also developed for securitisations. The improved risk-sensitivity lessened the incentives for banks to commit regulatory capital arbitrage thus perverting the aim of the whole capital adequacy exercise.

Basel 3 the Next Frontier5

The 2007 global financial crisis revealed several weaknesses of the capital adequacy framework. The spotlight was on the quality of capital or rather the lack of it. Shareholders fretted as the Committee was poised to release the initial proposals for the 3rd generation Basel. What’s got to be done has to be done. However, there was great relief and bank stocks rallied when it was announced that Basel 3’s somewhat harsh proposals would be implemented gradually over a six-year timeframe from 2013 to 2019.

Basel 3 differentiates Tier 1 capital which supports losses on a going concern basis into “Common Equity Tier 1” and “Additional Tier 1”. To enhance capital quality, the profile of “Common Equity Tier 1”, the purest grade of equity will be raised and quantum bolstered to 4.5% of risk-weighted assets by January 2015. The Committee has gone to great lengths to stipulate exactly what it could comprise of.

There were the other events from the financial crisis that provoked the pronouncement of additional features by the Committee. Taxpayers, Occupy-Wall-Streeters, academicians and the like were understandably seething when public funds were injected to rescue troubled institutions whilst hybrids, subordinated debts and other non-core capital instruments got away unscathed. Isn’t it logical that after the true owners are pummelled, the Tier 2 type investors should be next in line? In theory, since they enjoyed added returns (over depositors) correlated with the risk then they should suffer the consequences when things get difficult. It was not to be in reality as authorities had to act before the core equity could be completely extinguished as market confidence was fast disappearing. In addition, SIFIs acted with impunity, in full confidence that the government would catch them should they slip - after all they were simply too big to fail! The Committee feels that SIFIs due to their privileged position should have loss-absorbing capacity beyond minimum standards. In all fairness

Those who were members of the Organisation for Economic Co-operation and Development (OECD) were regarded as more creditworthy than those who were not. It translated into favourable risk weights for banks and sovereigns from the OECD.

Asian Link 14

however, the insistence of larger capital would put them at a disadvantage.

The reaction of the authorities to these oddities was to seriously consider contingent convertibles or CoCos and bail-in debtsThe Committee refers to the former as Convertible Capital. These are bonds that automatically convert to equity in times of specified distress events for example when the Tier 1 capital of a bank is bashed to below a certain minimum limit. Under normal market conditions CoCos would probably bear strong resemblance to an ordinary bond except that the bondholders would likely be compensated with added yield relative to the equivalent for bearing the risk of conversion.

Bail-ins are more radical. They are debts which authorities could dictate to either partially write-off or force a conversion to equity. An audacious idea being bounced around is for all non-core equity capital instruments to be subject to bail-in! Interestingly, mentioned in Basel 3 is that “Additional Tier 1” instruments classified as liabilities for accounting purposes must have principal loss absorption through conversion to common equity or write-down at a pre-specified trigger point. The regulator can take comfort that the two foregoing instruments will inject millions in equity when it’s needed most. Other creditors, depositors and taxpayers will be glad for the additional margin of safety. CoCos and bail-ins should be a welcome compromise.

It was much publicised to the vexation of many when weakened banks in the centre of the financial storm somehow still managed to pay dividends and handsome bonuses to CEOs who had led them to the slaughterhouse. Helpless creditors stood by while the coffers were emptied. Besides the remote possibility of greed, the plausible reason given was that stopping such discretionary payments generates negative public perception of possible weakness which could further erode confidence and aggravate the crisis. In response, the Committee decided to add a Capital Conservation Buffer of 2.5% above the regulatory minimum capital of 4.5% of Common Equity Tier 1, bringing the total of this top grade capital to 7% under normal market conditions. A Common Equity Tier 1 capital of between 4.5% and 7% takes away the bank’s right to an assortment of discretionary payments.

Another phenomenon noticed was that banks that apparently had sufficient regulatory capital had somehow built up an excessive leverage. Strangely, there seem to be some disconnect between capital

ratio and leverage. When confidence diminished and rapid deleveraging kicked-in, asset prices took a severe beating and this further intensified the crisis. The response by the Committee was to go back to the basics – forget about risk weighting. It prescribed a simple non-risk based Tier 1 to total assets leverage ratio of 3% (including off-balance sheet items). A parallel run will be conducted from 2013 to 2017, with a view to migrate to enforcement via Pillar 1 by 2018.

The dependence on ratings irrespective of internal or external in determining credit risk capital charge has the tendency of enhancing the amplifications of the business cycle. The downturn particularly if preceded by a by excessively large credit growth can be extremely destabilising for the banks. It starts a vicious cycle affecting the real sector, which then feeds back to the banking sector further destabilising it. To mitigate this procyclicality, the Committee advocates a Countercyclical Buffer of up to 2.5% of risk-weighted assets to be built up when the economy is getting a little overheated and released when it is on the downturn.

Capital adequacy does not automatically translate into liquidity sufficiency. The crisis revealed that lofty asset prices and low funding cost can reverse in the blink of an eye. To address this, the Committee has developed two key ratios that are destined to become a minimum standard. The “Liquidity Coverage Ratio” focuses on the asset side, measuring the ability of the bank to survive in a stress situation for thirty days. It is based on availability of high quality, unencumbered, liquid and central bank-worthy assets. The “Net Stable Funding Ratio” sets the minimum proportion of stable funding such as customer deposits and long term funds that is required to finance less liquid assets.

ConclusionAcademicians and practitioners have conducted some discourse on the matter of capital adequacy and the Basel pronouncements. Many are of the view that Basel 3 will not be the last pronouncement that puts the final nail onto the coffin of bank insolvencies. Cynics such as my colleague Dr Bobker opines that whilst Basel 3 is headed in the right direction, given the distant and long time frame, we may be debating a Basel 4 courtesy of another crisis

even before implementation is complete.

Yogaretnam Kanagandram is General Manager of the Risk Management Centre, AIF

15 Asian Link

World NeedsSecond (and third)

Reserve Currencya

The

By Moorad Choudhry

An inability to apply objective analytical thought is a recurring theme in history, usually condemning the unfortunate subject to failure. The weight of history is

on us once again, with the slowly changing status of the US dollar as the world’s de facto reserve currency. The importance of the dollar in the world economy is based on history. When the Bretton-Woods exchange rate mechanism was devised in 1944, the US economy was the dominant force in the world and the US dollar the pre-eminent currency. It naturally followed that the economic system the Allied powers set up at the end of the war would use the US dollar to back the fixed-rate regime. But 20-odd years later, the US chose to pay for the cost of the Vietnam war on credit, and when the imbalances created by Bretton-Woods made continued backing with US dollars impossible, as the US economy wasn’t generating sufficient foreign exchange (FX) reserves, the system broke down and we moved, ultimately, to the floating-rate arrangement we have today.

The problem was, the rest of the economy didn’t move with it. World trade is still priced in US dollars, everything from crude oil to gold to wheat. While on the surface this doesn’t appear to be an issue, it is a problem when the US constitutes a steadily decreasing share of world economic output and world exports. Is it efficient, economically speaking, that when a Malaysian rubber exporter sells its product to a Korean car manufacturer, both parties have to transact in US dollars? As the value of the dollar depreciates steadily (for example, it has lost over 15% of its value against the euro in the last five years), it makes less and less sense to maintain pricing exclusively in this currency.

The export performance of the OPEC and Asia-Pacific currencies was a causal factor of the 2007-2008 financial crisis. The US dollar reserves of these countries were invested in the West, contributing to excess cheap liquidity which found its outlet in sub-prime and corporate lending. The rest is, again, history. The US dollar’s status as “reserve currency” means that the US economy has something of a free lunch because it will always find buyers of its assets: the rest of the world. The size of the US public sector deficit today is testament to this lack of fiscal discipline (when we are in trillions territory, the exact size becomes, as Stalin might have said, merely a statistic). Investors will always seek risk-free assets, which is why the Federal Reserve can always print Treasury bills.

The current situation is not desirable from a number of viewpoints, whether one is a non-US exporter or a bank regulator trying to mitigate against the next financial crash. Is there a solution? Bear in mind this is a long-term project, one cannot set up a reserve currency quickly. An IMF-style special drawing right (SDR) we can dismiss out of hand, as lacking liquidity. The euro is a genuine contender, but has to sort out its structural problems first – it needs a centralised fiscal management system (some form of political union) as well as an objective review of whether economically weaker eurozone countries are viable long-term members. That leaves the Chinese renminbi. Although not a freely tradeable liquid currency, it is surely only a matter of time before it does become one. The Chinese economy is going to be growing over the next 20 years, and as its exports start to dominate world trade, it makes sense to transact more in its currency.

Fast forward 10 years. If the world had three reserve currencies to pick from, for both its risk-free asset holdings and its global commerce, would this be a good thing? The answer is a definite “Yes.” In the first instance, the kind of global cash flow imbalances we experienced during 2001-2007, an d which contributed to the financial crash, would not build up to the same extent. This would contribute to economic stability. Secondly, exporters would be less exposed to FX rate fluctuations, enabling companies around the world to save money on hedge costs. And third, it would enforce an element of fiscal discipline on future US governments, which would be good for the US economy, and by extension the world, in the long run.

This is not to underestimate the importance of the US dollar. It will still be the main currency for payments and risk-free assets in 10, and even 20 years’ time. But the availability of the euro and renminbi on a similar basis – as freely tradeable, liquid currencies and with an open government bond market in China – will mean that central banks can diversify their currency holdings, and there

would be less correlated risk with the entire world to the US economy. This can only be a good thing.

Moorad Choudhry is Visiting Professor at the Department of Mathematical Sciences, Brunel University and author of The Principles of Banking (John Wiley & Sons, April 2012, ISBN: 978-0-470-82521-1).

15 Asian Link

Asian Link 16

By Dr Zamros Dzulkafli

the newly created jobs from investments in various sectors of the economy by 2020. And based on Bank Negara Malaysia’s Financial Sector Blueprint, Malaysia needs an additional 56,000 manpower in the financial sector alone. Having the human capital to fill in the jobs is one thing but having to prepare them with the required skills and expertise is another daunting task which requires dynamic and strategic long term planning.

Global Demographic Trends People play a dual role in the economy; as the beneficiaries of economic prowess attained and at the same time act as an important input into the process of growth itself. In light of this, some believe that population growth should be limited in order to curb the use of resource while others believe that population provides additional human capital or labour force to be engaged in those activities needed to support economic growth as well as the increasing demand for consumption. Thomas Malthus, a British economist, put forth the observation that human population increases geometrically whilst food supply can only increase arithmetically. Therefore, he argued

the

demographic trends oneconomic growth

impact of

or decades, the issues relating to population change on economic growth have been at the heart of policy debates amongst economist and social thinkers. Of particular importance have been changes on the size and age structure of the population or the

demographic transition. As people’s behaviour and needs vary naturally at different stages of life, changes in a country’s age structure can have significant effects on its economic well being as well as on the economic structure.

A demographic transition also encourages the growth of savings, thus improving a country’s prospects for investment and growth. Generally, the young and the old consume more than what they can generate. But those people in the working-age group tend to have a higher level of economic outputs, and also a higher level of savings. And these private savings provide the needed capital accumulation and liquidity in the domestic economy to finance growth.

As Malaysia strives to become a high income nation, PEMANDU projected that the country requires 3.3 million workers to fill in

17 Asian Link

economic growth

that if left unrestrained, the population growth will eventually overtake the ability to produce food and subsequently lead to starvation.

This gloomy view was derived during the early years of the Industrial Revolution where developments in agricultural efforts had not reached the level that could increase food supply sufficient enough to feed. However, technological progress and innovations have enabled rapid growth in agricultural produce and food production, thereby ensuring swift transportation as well as continuous supply of food anywhere in the world. Meanwhile, the global population continues to swell over the years. The world population is currently estimated to be 7.0 billion people with 60% of them residing in Asia. And this is forecasted to reach 9.3 billion people by the year 2050, with Asia still maintaining its status as the most populous region. Figure 1 clearly shows that Asia has been experiencing periods of unprecedented population growth. Asia’s population has more than doubled over the past 7 decades and is expected to grow to more than 5 billion by 2050.

Despite worries put forward by Malthus, statistical analysis shows that there is insignificant evidence that population growth would impede economic growth. Other additional factors such as supportive government policies, openness to trade, technological advancement and quality of human capital play the equally crucial role in promoting growth hand in hand with the growing population. While Malthus’s proposition did not materialise, Adam Smith in his book titled “Inquiry into the Nature and Causes of the Wealth of Nations” (1776), suggested that growth is rooted in the division of labour which he noted leads to greater productivity. This is primarily because the division of labour allows workers to specialise and thus improve their skills.

Various studies had also shown that demography does have some impact on economic growth, if we are to also take into consideration changes in age structure. As the population continues to grow over time, the structure of the population changes too. What is more important under such scenario is the age structure of the population as that would lead to

1950-1970 1970-1990 1990-2010 2010-2030(f ) 2030-2050(f )

%3.5

2.5

1.5

0.5

-0.5

3

2

1

-1

0

Figure 2: Average annual growth rate of population (percent)

Source: World Economic Forum

Figure 1: Global population

Source: United Nations

million10,000

8,000

6,000

4,000

2,000

0

19501990

19602000

19702010

1980

2020(f )

2030(f )

2040(f )

2050(f )

Oceania

North America

Latin America

Europe

Africa

Asia

Asia

Malaysia

Japan

China

India

Asian Link 18

Indicator 2000 2010

Total Population (million) 23.2 28.3

Population Growth (%) 2.6 2.0

Aged 0-15 (%) 33.3 27.6

Aged 15-64 (%) 62.8 67.3

Aged Above 65 (%) 3.9 5.1

Median Age (years) 23.6 26.2

Fertility Rate 3.0 2.3

Life expectancy at birth (years)

Male

Female

70.0

74.7

71.9

77.0

Table 1: Selected indicators from Census 2010

Source: Department of Statistics, Malaysia

changes in economic demand and activities as well as in the supply of human capital. Hence, appropriate government policies as well as human capital development strategies would be needed to cater to the changing demographic structure.

Changes in population age structure may affect savings level, physical capital accumulation and total factor productivity (TFP) as well. The human capital and savings are affected through changes in income and consumption patterns by different age groups. Those in the working age group tend to work and save more than the youth or the elderly. Children rely on their parents for support while the elderly relies on income derived from their earlier savings, support from their working children as well as pension benefits.

Asia and some parts of the world are currently going through a demographic transition, attributed to decreasing fertility rate and at the same time increasing life expectancy. The developed countries such as those in Europe, North America and Japan had much earlier experienced demographic transitions. Fertility rates are decreasing as people are delaying marriage due to longer time spent on education and work related reasons. Advancement in birth control may also have some impact. Meanwhile, life expectancy gets better due to vast improvements in access to public health and advancement in medical technology, leading to better living conditions. If this trend continues, the average annual population growth in Asia is expected to decrease to 0.3% only by 2030-2050 from the current 1.3% (see Figure 2). Could this be detrimental to Asia’s goal to become the epicentre of global economic growth and sustain that position as well?

If this trend is evident in Malaysia, what would be the impact on growth potential and strategies needed to ensure that Malaysia has the capacity and capability to move forward on a sustainable growth path. Japan for instance, is already in the negative population growth trajectory while China is following suit and is expected to shrink by 0.4% in 2050. This will give a significant impact on China’s effort to sustain its position as the world’s second largest economy and making domestic consumption and investment as its growth drivers.

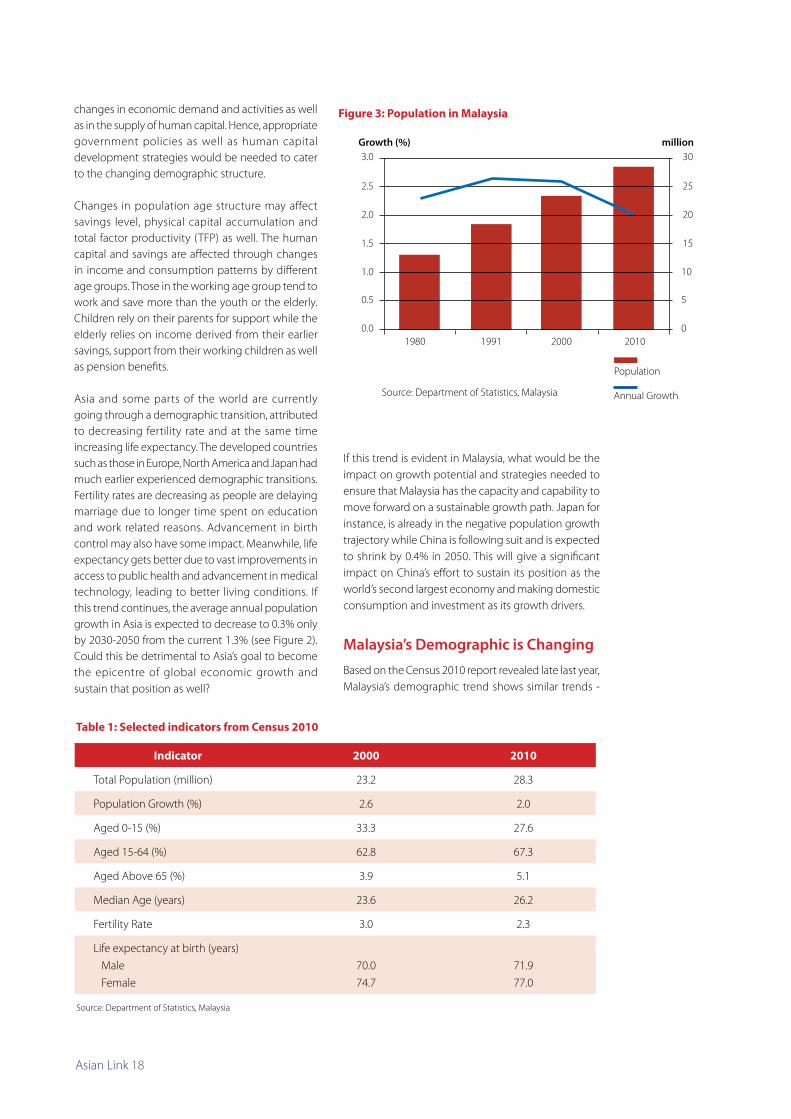

Malaysia’s Demographic is ChangingBased on the Census 2010 report revealed late last year, Malaysia’s demographic trend shows similar trends -

3.0

2.5

1.5

0.5

2.0

1.0

0.0

Growth (%) million30

25

15

5

20

10

1980 20001991 20100

Figure 3: Population in Malaysia

Source: Department of Statistics, Malaysia

Population

Annual Growth

19 Asian Link

Economy

slower fertility rate, higher life expectancy and higher median age. Hence, we are slowly moving towards an older society but still expanding in the working age group.

Although Malaysia’s population had increased nearly threefold over the past four decades, its growth rate had slowed down to 2.0% from 2.6% in 2000. The fertility rate dropped to 2.3% as compared with 3.0% in 2000. The proportion of the population of Malaysia below the age of 15 years decreased to 27.6% as compared with 33.3% in 2000. In contrast, the proportion of working age population (aged 15 to 64 years) increased to 67.3% from 62.8%. The proportion of population aged 65 years and over also increased to 5.1% as compared with 3.9% in 2000. As a result, the median age increased from 23.6 years in 2000 to 26.2 years in 2010, while the dependency ratio dropped from 59.2% to 48.5% (refer to Table 1). The expanding working age group bodes well with Malaysia’s needs for human capital to support investment activities and eventually lead to the economic expansion.

The trend of these indicators is in line with the transition of age structure towards an ageing population in Malaysia. In this case, the definition of an aging population is when the number of people aged over 65 is more than 7% of the population. Hence, Malaysia is not yet an ageing society. The Department of Statistics projected that Malaysia’s population is expected to peak at 57 million by 2090 and the nation could become an ageing society in 2024, if current population trends were to continue. The projection is based on Malaysia’s increasing life expectancy and decreasing fertility rate.

Another important factor is the trend of shrinking working age population as a percentage of total population. As those in the 0-15 years of age and above 65 age brackets do not have regular income and are dependant on those in the working age for support, a shrinking working age population would put higher pressure on the society to support them. A shrinking working age population will also put pressure on the supply of labour and in a way will affect growth potential. We have already seen the trend in Japan whereby the working age population started to shrink as early as in 1990. Now, similar trends can be seen in South Korea

and China as the working age population shrunk from their peaks in year 2000. Malaysia is projected to experience similar trends by 2020, albeit mildly, while India is expected to be enjoying expansion in working age population until 2040.

Comparing Asia to other regions, Asia is expected to remain as the major area providing the highest working age population, followed closely by Latin America. Nevertheless, the potential of the younger population in Africa is expected to bear fruit in providing an increasing stream of working age population well into the foreseeable future and thereby support economic developments for them. Situations in Europe and North America are on the opposite end of the scale as their working age population as a percentage of total population continue to shrink further.

“Comparing Asia to other regions, Asia is expected to remain as the major area providing the highest working age population, followed closely by Latin America. “

19701980

19902000

2010

2020(f )

2030(f )

2040(f )

2050(f )

per cent75

65

55

70

60

50

Figure 4: Working age population (percent of total population)

Source: United Nations

19501990

19702010

19602000

1980

2020(f )

2040(f )

2030(f )

2050(f )

70

60

65

55

50

Figure 5: Working age population by regions (percent of total population)

Source: United Nations

Japan

Korea

China

India

Malaysia

Thailand

Indonesia

Asia

Africa

Europe

Latin America

North America

Oceania

Asian Link 20

Ageing and The EconomyJapan remains as the world’s most rapidly ageing country, with the highest life expectancy at 83.2 years. Fertility rates are low in Japan at 1.3 children per woman and policymakers strive to prepare for the challenge of an increasingly elderly population. In 2010, it is estimated that about 23% of Japan’s population is 65 years old or over. This figure is expected to increase to 30.3% in 2030 and 35.6% by 2050. Their provision of daily care and medical needs is a challenge. Pensions are also a delicate issue and with the young workforce now supporting a pay-as-you-go pension system, expenditure on pensions could push Japan’s budget deficit further up. With the drop in fertility rates, and many people retiring as well as the shrinking working age population, Japan’s economy would be further challenged and would risk persistent slowing growth.

This would come from the adverse impact in reducing consumption leading to Japan’s dire state of aggregate domestic demand. The elderly tend to save more rather than spending. As a result, Japan depends on external demand to generate its growth. In a way, these when combined with other contributing factors such as the strength of its currency, natural disasters and political instability, have contributed to disinflationary pressure and eventually would lead to deflation in Japan’s domestic market.

ConclusionCountries with a high proportion of children are likely to devote a high proportion of available resources to their care and education, hence different products and services are in high demand. On the other hand, countries with a huge share of their population ratio within the working ages, the added productivity of this group can produce a ‘demographic dividend’ of economic growth, provided that supportive government policies are in place. The combined effect of a large working age population and health, family, labour, financial, and human capital policies can generate cycles of wealth creation. And if a large proportion of a country’s population consists of the elderly, the effects can be similar to those of a very young population, as a large share of resources is needed by a relatively less productive division of the population, which can then inhibit maximum potential in economic growth.

We have already seen the impact of such demographic changes in the Europe, North America and Japan. And we should take cue from their experiences to manage and minimise the impact of any demographic transitions so as not to jeopardise our growth potential. Furthermore, Malaysia is scheduled for the sixth census in 2020. If everything is according to the strategies outlined under the Economic Transformation Plan (ETP), Malaysia would be a high income nation by then. And, by then too, some of us may not be in the working age group anymore, but already be in the elderly age group for good!

Dr Zamros Dzulkafli is Research Fellow of the Applied Finance Research and Publication Centre, AIF.

19901970

20102000

1980

2020(f )

2040(f )

2030(f )

2050(f )0

10

20

30

40

Figure 6: Percentage of population above 65

Source: United Nations

Japan

Korea

China

India

Malaysia

Thailand

Indonesia

Malaysia would be a high income

nation by then. And, by then

too, some of us may not be in

the working age group anymore,

but already be in the elderly age

group for good!

21 Asian Link

inancial innovation has been a critical and persistent part of the economic landscape over centuries. At the core of financial innovation is technology. Through technology, financial innovation – the creation and marketing of new types of securities – has revolutionized the way financial institutions conduct their businesses.

As the twin engines of growth, both financial innovations and technological innovations are inextricably linked. The major source of innovation is new technology-based companies but most often these companies find it difficult to raise capital. In response for funding by techno-entrepreneurs, business angels and venture capital have emerged as the alternatives to the traditional financing structure.

By Dr Wan Nursofiza Wan Azmi

FINANCINgTEChNOLOgICAL

Financing Technology

Technological innovation has pushed forward the growth curves of

many organizations and transformed the way businesses operate

today. Innovation in technology has been recognized as a major

driver of economic growth and social progress, yet it is chronically

underfinanced in most developing countries. In many instances,

technology-based small medium-size enterprises (SMEs) find it

difficult to obtain the necessary financial resources to effectively

scale up and grow their businesses. These hi-tech SMEs are

predominantly young, technology focused and with powerful

product or service ideas but posses poor market connectivity and

few tangible assets that can be used as collaterals for loans.

F

INNOVATION

Asian Link 22

Financial agents are reluctant to finance te c h n o l o gi c a l d e ve l o p m e n t s i n c e technological innovation is mostly associated with uncertainty, imperfect monitoring and in some cases imperfect intellectual property rights. Needless to say, the risks inherent in technological innovation – technological viability, uncertainty of potential market size and lack of precedent – make the valuation of high-tech SMEs a daunting task to potential investors. This challenge is more acute for seed-stage and early-stage high-tech SMEs.

Asian Link 22

Successful technological innovations have typically required new financial arrangements. Financial innovation from venture capital financing continues to serve as a critical funding source and many venture capital funds have been established to serve this purpose. Venture capital differs in several ways from traditional financing sources. Typically, venture capital:

f o c u s e s o n y o u n g , h i g h - g r o w t h •companies;invests with equity capital, rather than with •debt financing;takes higher risks in exchange for potential •higher returns;has longer investment horizon than •traditional financing; andactively monitors portfolio companies via •board participation, strategic marketing, governance and capital structure.

Venture capital, as a form of private equity for new and emerging businesses that have great potential for innovation and growth, comes in many different forms. The two most distinguished are business angels and venture capitalists. Business angels or also known as angel investors are high-net worth individuals with great business experience. They are known as “angels” because they often invest in risky, unproven business ventures for which debt financing is not available. Often business angels take a hands-on approach in managing the enterprise they invest in by contributing their skills, expertise, knowledge and networking. As opposed to business angels who invest their own money into the business, venture capitalists raise money from various institutional funds such as foundations, endowment funds and retirement funds; and divest these funds into high growth companies. However, in order to limit their risks most venture capital firms invest in many different start-up companies at any one time.

Another source of financing technological innovation is innovation fund. Many innovation funds have been set up to support innovations with high commercial potentials, including funding the development of new or improvement of existing products, process or services. These funds offer financial assistance to early stage or start-up companies, particularly those confronting challenges in assessing funding from traditional sources of financing due to lack of assets or cash flow.

23 Asian Link

Global Innovation Footprint

The innovation performance of Malaysia as reported in the Global Innovation Index 2011 published by the Institute of European Administration and Development (INSEAD) was ranked at number 31 among 125 economies. This is a drop from the 25th position in 2009 and 28th position in 2010. In the Asian region, Singapore and Hong Kong were ranked among the top 10 innovative economies in the world with Singapore ranking 3rd followed by Hong Kong in the 4th position. According to the Index, innovation areas which Malaysia needs to enhance include the infrastructure pillar (rank 53), the institutions pillar (rank 51) and the human capital and research pillar (rank 42). In the Global Competitiveness Index 2011-2012 released by the World Economic Forum, Malaysia’s position under the innovation pillar improved one notch to record 24th position. These rankings are evident that more initiatives are needed to shift Malaysia to a high income economy and be at par with its neighbouring Asian countries.

An Innovation Economy

As the Malaysian economic activities grow to become more knowledge-intensive, greater attention has been given to the economic role of innovation. Several policy efforts have been accelerated aiming at strengthening the national innovation system. Furthermore, the New Economic Model has also identified innovation as the key mechanism that will propel Malaysia to a high income status. In line with this, the Ministry of Science, Technology and Innovation (MOSTI) has drawn up a National Innovation Model (NIM) that sets the blueprint for the transition of Malaysia into an innovation-led economy that promotes knowledge acquisition.

The innovation model adopted by Malaysia is a balanced approach between technology driven and market driven innovation. In technology driven innovation, technology is the primary driving force in both organic as well as indigenous science and technology development. In this model approach, scientists are provided funding for R&D and for commercializing their ideas. Market driven innovation model, on the other hand, is user-driven based on sustainable demand trends and acquired technology.

The four major recommendations made under the NIM are:

Domestic private enterprises should lead the transition from resource-led •economy (linear growth) to innovation-led economy (exponential growth).Both technology and market driven innovation must seek to seize opportunities •for growth, wealth creation and employment in the short, medium as well as long term.On the supply side, the government shall play a major role in funding scientific •research whereas market innovation shall be driven by the private sector.The government should be an enabler to facilitate the private sector in its pursuit •of technology innovation. This may be in the form of risk mitigation, grants, incentives and support for organic technology development in basic science.

A supportive and robust ecosystem for innovation is critical for Malaysia in its quest to climb the income ladder through innovation-led growth strategy. At the forefront is the ability to leverage on leading edge technologies which is often a role that is fulfilled by venture capitalists in the developed countries. Although the growth of the venture capital industry in Malaysia has been on a positive track, the industry is still in its infancy both in terms of overall size as well as number of players in the market. Yet, this industry has huge potential.

Dr Wan Nursofiza Wan Azmi is Senior Research Fellow of the Applied Finance Research and Publication Centre, AIF.

Technological innovation has pushed forward the growth curves of many organizations and transformed the way businesses operate today. Innovation in technology has been recognized as a major driver of economic growth and social progress, yet it is chronically underfinanced in most developing countries.

23 Asian Link

Asian Link 24

Talent DevelopmentStrategy

Winning