Compensation - FCA Handbook · COMP Contents Compensation COMP INTRO B Introduction 1B INTRO 1B...

140

Compensation

-

Upload

truongkhue -

Category

Documents

-

view

225 -

download

3

Transcript of Compensation - FCA Handbook · COMP Contents Compensation COMP INTRO B Introduction 1B INTRO 1B...

Compensation

COMP Contents

Compensation

COMP INTROA INTRO 1

INTRO 1 Foreword

COMP 1 Introduction and Overview

1.1 Application, Introduction, and Purpose1.2 The FSCS1.3 Claimants1.4 EEA Firms [deleted]1.5 Application to Lloyd's1.6 Cooperation with the FSCS

COMP 2 The FSCS

2.1 Application and Purpose2.2 Duties of the FSCS

COMP 3 The qualifying conditions for compensation

3.1 Application and Purpose3.2 The qualifying conditions for paying compensation

COMP 4 Eligible claimants

4.1 Application and Purpose4.2 Who is eligible to benefit from the protection provided by the FSCS?4.3 Exceptions: Circumstances where a person coming within COMP 4.2.2R

may receive compensation4.4 Exceptions: Relevant general insurance contracts: mesothelioma claims

COMP 5 Protected claims

5.1 Application and Purpose5.2 What is a protected claim?5.5 Protected investment business5.6 Protected home finance mediation5.7 Protected non-investment insurance mediation5.8 Protected debt management business

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP–i

COMP Contents

COMP 6 Relevant persons and successors in default

6.1 Application and Purpose6.2 Who is a relevant person?6.3 When is a relevant person in default?6.3A When is a successor in default?

COMP 7 Assignment or subrogation of rights

7.1 Application7.2 How does the assignment of rights work?7.3 Automatic subrogation7.4 Duty on FSCS to pursue recoveries7.6 Treatment of recoveries

COMP 8 Rejection of application and withdrawal of offer

8.1 Application and Purpose8.2 Rejection of application for compensation8.3 Withdrawal of offer of compensation

COMP 9 Time limits on payment and postponing payment

9.1 Application and Purpose9.2 When must compensation be paid?

COMP 10 Limits on the amount of compensation payable

10.1 Application and Purpose10.2 Limits on compensation payable

COMP 11 Payment of compensation

11.1 Application and Purpose11.2 Payment

COMP 12 Calculating compensation

12.1 Application and Purpose12.2 Quantification: general12.3 Quantification date12.4 The compensation calculation12.5 [deleted]12.6 Quantification: trustees, operators of pension schemes, persons winding

up pension schemes, personal representatives, agents, and joint claims

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP–ii

COMP Contents

COMP 12A Special cases

12A.1 Trustees and pension schemes12A.2 Personal representatives, agents and joint claims12A.3 Collective investment schemes12A.4 Foreign law12A.5 Claims arising under COMP 3.2.4R

COMP 13 Funding

13 Ann 1 [deleted: the provisions in relation to the funding of the FinancialServices Compensation Scheme are set out in FEES 6 (Financial ServicesCompensation Scheme Funding)]

COMP 14 Participation by EEA Firms

14.1 Application and Purpose14.2 Obtaining top-up cover14.3 Co-operation between the FSCS and Home State compensation schemes14.4 Ending top-up cover14.5 EEA UCITS management companies

Transitional provisions and Schedules

TP 1 Transitional ProvisionsSch 1 Record-keeping requirementsSch 2 Notification requirementsSch 3 Fees and other required paymentsSch 4 Powers ExercisedSch 5 Rights of action for damagesSch 6 Rules that can be waived

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP–iii

Compensation

Chapter INTRO

INTRO 1

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP INTRO A/1

COMP INTRO A : INTRO 1 Section INTRO 1 : Foreword

INTRO

INTRO

INTRO

INTRO

INTRO

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP INTRO A/2

INTRO 1 Foreword

(This Foreword to the Compensation sourcebook does not form part ofCOMP.)

The Act requires the FCA and the PRA to make rules establishing a schemefor compensating consumers in cases where: (i) relevant persons are unable,or likely to be unable, to satisfy claims against them; or (ii) persons who haveassumed responsibility for liabilities arising from acts or omissions ofauthorised firms (“successors”) are unable, or likely to be unable, to satisfyclaims against the successors that are based on those acts or omissions. Thebody established to operate and administer the compensation scheme is theFinancial Services Compensation Scheme Limited (FSCS). The PRA’scompensation rules deal with claims for deposits and under contracts ofinsurance and the FCA’s compensation rules deal with other types of claim.

By making rules that allow the FSCS to pay compensation to retail consumersand small businesses, and focusing protection on those who need it most,the compensation scheme rules form an important part of the toolkit theFCA will use to meet its statutory objectives. This module of the FCAHandbook contains the rules and guidance that allow the FSCS to pay claimsfor compensation when an authorised person or, where applicable, asuccessor, is unable or likely to be unable to meet claims against it. The rulesspecify who is eligible to receive compensation and in what circumstances,how much compensation can be paid to a claimant; and how the scheme willbe funded. The compensation rules are of interest to consumers. The rulesapply to the FSCS, authorised firms and successors.

The Sourcebook is divided into the following Chapters covering all aspects ofthe scheme:

Chapter 1: Introduction and Overview

This chapter provides an introduction to the FSCS rules and a table ofquestion and answers that may be of interest to consumers.

Chapter 2: The FSCS

This chapter gives the FSCS the duty to administer the compensation scheme.It also sets out the general conditions the FSCS must follow whenadministering the scheme, such as having regard to the efficient andeconomic use of resources, the requirement to publish an Annual Report,and the duty to ensure consumers are informed about how they can make aclaim. The rules in this chapter also require the FSCS to have in placeprocedures for dealing with complaints.

COMP INTRO A : INTRO 1 Section INTRO 1 : Foreword

INTROINTRO

INTRO

INTRO

INTRO

INTRO

INTRO

INTRO

INTRO

INTRO

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP INTRO A/3

Chapter 3 The qualifying conditions for paying compensation

This chapter sets out the main qualifying conditions that must be satisfiedbefore the FSCS can pay compensation to claimants. These are that aclaimant is eligible to claim; the activity that gave rise to the loss is protectedby the scheme; the firm against which the claim is being made is protectedby the scheme; and that the claimant has assigned his rights to the scheme.Chapters 4 to 7 expand on the general conditions described in Chapter 3.

Chapter 4 Eligible claimants

This chapter specifies who is eligible to receive compensation provided bythe FSCS.

Chapter 5 What is a protected claim?

This chapter specifies the activities that are protected by the FSCS.

Chapter 6 Relevant persons and successors in default

This chapter specifies the circumstances when a firm is in default, that is,when a firm is to be taken as being unable or likely to be unable to meetclaims against it. The FSCS can only pay compensation if the circumstancesspecified in Chapter 6 are met.

Chapter 7 Assignment of rights

This chapter enables the FSCS to make an offer of compensation conditionalon the claimant assigning to it their rights to claim against the failed firm. Ifthe FSCS recovers from the firm a greater sum than it has paid to theclaimant, it must pay the balance to the claimant.

Chapter 8 Rejection of application and withdrawal of offer

This chapter allows the FSCS to reject an application for compensation orwithdraw an offer of compensation in specified circumstances.

Chapter 9 Time limits on payment and postponing payment

This chapter requires the FSCS to pay a claim for compensation within aspecified time unless specified conditions apply.

Chapter 10 Limits on the amount of compensation payable

This chapter specifies the maximum amount of compensation the FSCS canpay to a claimant.

Chapter 11 Payment of compensation

This chapter specifies to whom the FSCS may pay compensation. In certaincircumstances compensation may be paid to a person other than theclaimant.

COMP INTRO A : INTRO 1 Section INTRO 1 : Foreword

INTROINTRO

INTRO

INTRO

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP INTRO A/4

Chapter 12 Calculating compensation

This chapter specifies how the FSCS will calculate the amount ofcompensation it can pay to a claimant.

Chapter 13 Funding

Chapter 13 relating to the funding of the FSCS has now been deleted. Thefunding provisions for the FSCS are now contained in FEES 6 instead andallow the FSCS to make levies on authorised firms to fund the operation ofthe scheme or to pay compensation. FEES 6 specifies how FSCS can makelevies, how costs are to be allocated, the maximum the FSCS can levy in anyparticular period of time, and how sums recovered from failed firms are tobe treated.

Chapter 14 Participation by EEA firms

This chapter sets out the way the FSCS deals with incoming EEA firms whomay choose to top-up into the FSCS to supplement the compensationavailable from their home state scheme.

Compensation

Chapter 1

Introduction and Overview

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 1/1

COMP 1 : Introduction and Section 1.1 : Application, Introduction, andOverview Purpose

1

G1.1.1

G1.1.2

G1.1.3

G1.1.4

G1.1.5

G1.1.6

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 1/2

1.1 Application, Introduction, andPurpose

Application......................................................................................................This chapter is relevant to:

(1) the FSCS;

(2) eligible claimants;

(3) firms; and

(4) successors.

This sourcebook is principally relevant to the FSCS. It sets out thecircumstances in which compensation may be paid, to whom compensationmay be paid, and on whom the FSCS can impose levies to meet the costs ofpaying compensation (see in particular COMP 3, 4, and ■ FEES 6). It alsodescribes how the FSCS is to calculate compensation in particular cases (see■ COMP 12).

Claimants and their advisers will be particularly interested in the sections ofthis sourcebook which deal with eligibility for claiming compensation, theway that the FSCS calculates compensation, and how they can make a claim.For convenience, the relevant parts of this sourcebook are highlighted in alist of questions and answers in ■ COMP 1.3.3 G.

Firms will be particularly interested in ■ FEES 6, which deals with levies, and■ COMP 1.6.1R, which requires firms to deal with the FSCS in an open,cooperative and timely way.

Introduction......................................................................................................The FSA established the Financial Services Compensation Scheme Limited, acompany limited by guarantee (FSCS). The FSCS exercises the functions thatare conferred on the scheme manager by Part XV of the Act, dealing withcompensation.

The FCA and PRA are also required, under section 213 of the Act (Thecompensation scheme), to make rules establishing a compensation scheme.The FCA’s rules are set out in the remaining chapters of this sourcebook, andare directed to the FSCS, claimants and potential claimants, and firms. ThePRA’s rules dealing with claims for deposits and under contracts of insuranceare set out in the PRA Rulebook.

COMP 1 : Introduction and Section 1.1 : Application, Introduction, andOverview Purpose

1G1.1.7

G1.1.8

G1.1.9

G1.1.9A

G1.1.9B

G1.1.10

G1.1.10A

G1.1.10B

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 1/3

Purpose......................................................................................................The FSCS will only pay claims if a firm or a successor is unable or likely to beunable to meet claims against it because of its financial circumstances. If afirm (or, where applicable, a successor) is still trading and has sufficientfinancial resources to satisfy a claim, the firm (or, where applicable, thesuccessor) will be expected to meet the claim itself. This can, for example, bean amount the firm agrees with the claimant, or the amount of anOmbudsman award from the Financial Ombudsman Service.

■ COMP 1 consists of guidance which is aimed at giving an overview of howthis sourcebook works. The provisions of ■ COMP 2 to ■ COMP 14 cover who iseligible, the amount of compensation and how it might be paid.

[deleted]

This sourcebook is one of the means by which the FCA will meet its statutoryobjectives of securing an appropriate degree of protection for consumersand protecting and enhancing the integrity of the UK financial system.

[deleted]

[deleted]

By making rules that allow the FSCS to provide compensation at a levelappropriate for the protection of retail consumers and small businesses, theFCA enables consumers to participate in the financial markets with theconfidence that they will be protected, at least in part, should the relevantperson with whom they are dealing, or a successor, be unable to satisfyclaims against it.

[deleted]

COMP 1 : Introduction and Section 1.2 : The FSCSOverview

1

G1.2.1

G1.2.2

G1.2.2A

G1.2.2B

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 1/4

1.2 The FSCS

While this sourcebook deals with the main powers and duties of the FSCS, itdoes not provide the complete picture. Other aspects of the operation of theFSCS are dealt with through the powers of the Financial ServicesCompensation Scheme Limited under company law (such as the power toborrow, to take on premises, etc.).

(1) [deleted]

(2) [deleted]

(1) In addition, the Act itself confers certain powers upon the FSCS, suchas a power under section 219 of the Act (Scheme Manager's powersto require information) to require persons to provide information.These powers are not, therefore, covered by this sourcebook.

(2) Of specific relevance to the way in which the FSCS fulfils itsresponsibilities is the relationship between the FSCS and the FCA. Thisis covered in a Memorandum of Understanding which can be foundon the FCA website http://www.fca.org.uk .

[deleted]

COMP 1 : Introduction and Section 1.3 : ClaimantsOverview

1

G1.3.1

G1.3.2

G1.3.3

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 1/5

1.3 Claimants

The FSCS provides information to claimants and potential claimants aboutthe way the FSCS works and the procedures that need to be followed whenmaking a claim. The FSCS can be contacted at Financial ServicesCompensation Scheme, 10th Floor, Beaufort House, 15 St Botolph Street,London EC3A 7QU, or by telephone or fax (Tel: 0800 678 1100 or Fax: 0207741 4100).

Information about the operation of the FSCS and how to claim is alsoavailable from the FSCS website (www.fscs.org.uk).

Areas of particular interest to claimants (see COMP 1.1.3G).

This Table belongs to ■ COMP 1.1.3 G.

What do I need to do in order to receive com-Q1 pensation?

A1 In order to receive compensation:

(-1) If your claim is for a deposit or under acontract of insurance, see the PRA’s De-positor Protection or Policyholder Pro-tection rules;

(1) you must be an eligible claimant; COMP 4.2

(2) you must have a protected claim; COMP 5.2

(3) you must be claiming against a relevant COMP 6.2.1 Rperson or a successor;

(4) where the claim is against a relevant COMP 6.3; COMPperson, the relevant person must be de- 6.3Afault; or where the claim is against asuccessor, the successor must be indefault.

In addition, if the FSCS requires you to do so, COMP 7.2you must assign your legal rights in the claimto the FSCS.

And you must bring your claim to the FSCS COMP 8.2.3 R -within a set time (normally within six years of COMP 8.2.5 Rthe date on which your claim against the relev-ant person occurred).

It is possible, in certain circumstances, for some- COMP 3.2.2 Rone else to make a claim on your behalf.

Q2 How much compensation will I be offered?

This depends on whether your protected claim

COMP 1 : Introduction and Section 1.3 : ClaimantsOverview

1

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 1/6

A2 is:

(1) [deleted]

(2) [deleted]

(3) a claim in connection with protected in- COMP 5.5vestment business; or

(4) a claim in connection with protected COMP 5.6home finance mediation; or

(5) a claim in connection with protected COMP 5.7non-investment insurance mediation.

Different limits apply to different types of COMP 10.2.3 Rclaim.

How will the FSCS calculate the compensationQ3 that is offered to me?

Again, this will depend on whether your pro-A3 tected claim is:

(1) [deleted]

(2) [deleted]

(3) a claim in connection with protected in- COMP 12.2.1 R,vestment business; or COMP 12.3.5 R

and COMP 12.4.2R

(4) a claim in connection with protected COMP 12.4.17 Rhome finance mediation; or

(5) a claim in connection with protected COMP 12.4.20 Rnon-investment insurance mediation.

Certain types of protected investment business COMP 12.4.5 Rclaim require the FSCS to use a particularmethod of calculation.

Q4 [deleted]

COMP 1 : Introduction and Section 1.4 : EEA Firms [deleted]Overview

1

1.4

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 1/7

1.4 EEA Firms [deleted]

COMP 1 : Introduction and Section 1.5 : Application to Lloyd'sOverview

1

G1.5.7

R1.5.8

R1.5.9

G1.5.10

G1.5.11

R1.5.12

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 1/8

1.5 Application to Lloyd's

Compensation arrangements for individual members......................................................................................................The compensation scheme will not compensate members or former membersif firms are unable to satisfy claims made in connection with regulatedactivities relating to their participation in Lloyd's syndicates. Separate rulesand guidance are therefore needed.

The Society must maintain byelaws establishing appropriate and effectivearrangements to compensate individual members and former members whowere individual members if underwriting agents are unable, or likely to beunable, to satisfy claims by those members relating to regulated activitiescarried on in connection with their participation in Lloyd's syndicates.

For the purposes of ■ COMP 1.5.8 R "individual member" includes a memberwhich is a limited liability partnership or a body corporate whose membersconsist only of, or of the nominees for, a single natural person or a group ofconnected persons.

The arrangements referred to in ■ COMP 1.5.8 R:

(1) will not compensate losses arising only as a result of underwriting orinvestment risk to which individual members or former members whowere individual members are or were exposed by their participationin Lloyd's syndicates;

(2) may be restricted to compensation for losses arising out of fraud,dishonesty or failure to account; and

(3) should cover all regulated activities carried on by underwriting agentsrelating to Lloyd's syndicate capacity and syndicate membership.

The arrangements referred to in ■ COMP 1.5.8 R should have a governancestructure that is operationally independent from the Society, but which isnevertheless accountable to the Society for the proper administration of thecompensation arrangements.

A contravention of ■ COMP 1.5.8 R does not give rise to a right of action by aprivate person under section 138D of the Act (Actions for damages) and thatrule is specified under Section 138D(3) of the Act as a provision giving rise tono such right of action.

COMP 1 : Introduction and Section 1.6 : Cooperation with the FSCSOverview

1

R1.6.1

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 1/9

1.6 Cooperation with the FSCS

A firm must deal with the FSCS in an open, cooperative and timely way.

COMP 1 : Introduction and Section 1.6 : Cooperation with the FSCSOverview

1

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 1/10

Compensation

Chapter 2

The FSCS

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 2/1

COMP 2 : The FSCS Section 2.1 : Application and Purpose

2

R2.1.1

G2.1.2

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 2/2

2.1 Application and Purpose

Application......................................................................................................This chapter applies to the FSCS.

Purpose......................................................................................................In order to carry out its functions and put into effect the provisions set out inCOMP 3 - COMP 14 (which deal with determining whether compensation ispayable, calculating the amount of compensation that should be paid, andmaking levies on firms), the FSCS needs to have a variety of powers. Thepurpose of this chapter is to set out these powers, and the restrictions uponthem.

COMP 2 : The FSCS Section 2.2 : Duties of the FSCS

2

R2.2.1

G2.2.2

R2.2.3

R2.2.4

G2.2.5

R2.2.6

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 2/3

2.2 Duties of the FSCS

Administering the compensation scheme......................................................................................................The FSCS must administer the compensation scheme in accordance with therules in this sourcebook and any other rules prescribed by law to ensure thatthe compensation scheme is administered in a manner that is procedurallyfair and in accordance with the European Convention on Human Rights.

The FSCS may:

(1) pay compensation to eligible claimants when a relevant person (or,where applicable, a successor) is unable or likely to be unable to meetclaims against it in accordance with this sourcebook; and

(2) make levies on participant firms, in accordance with ■ FEES 6 (FinancialServices Compensation Scheme Funding), to enable it to paycompensation or meet the costs of discharging its functions under thissourcebook.

Information for claimants......................................................................................................The FSCS must publish information for claimants and potential claimants onthe operation of the compensation scheme.

Assistance to claimants......................................................................................................The FSCS may agree to pay the reasonable costs of an eligible claimantbringing or continuing insolvency proceedings against a relevant person or,where applicable, a successor (whether those proceedings began before orafter a determination of default), if the FSCS is satisfied that thoseproceedings would help it to discharge its functions under the requirementsof this sourcebook.

Annual Report......................................................................................................The FSCS must make and publish an annual report on the discharge of itsfunctions (section 218 of the Act (Annual report)).

Finance and resources......................................................................................................The FSCS must have regard to the need to use its resources in the mostefficient and economic way in carrying out its functions under therequirements of this sourcebook.

COMP 2 : The FSCS Section 2.2 : Duties of the FSCS

2

R2.2.7

R2.2.8

G2.2.9

R2.2.10

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 2/4

Publication of defaults......................................................................................................The FSCS must take appropriate steps to ensure that potential claimants areinformed of how they can make a claim for compensation as soon as possibleafter a determination has been made that a relevant person (or, whereapplicable, a successor) is in default, whether by the FSCS or the FCA.

Complaints......................................................................................................The FSCS must put in place and publish procedures which satisfy theminimum requirements of procedural fairness and comply with the EuropeanConvention on Humans Rights for the handling of any complaints ofmaladministration relating to any aspect of the operation of thecompensation scheme.

Informing the FSCS......................................................................................................The FCA will inform the FSCS if it detects problems in a firm that is likely togive rise to the intervention of the FSCS.

[deleted]

Compensation

Chapter 3

The qualifying conditions forcompensation

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 3/1

COMP 3 : The qualifying Section 3.1 : Application and Purposeconditions for compensation

3

R3.1.1

G3.1.2

G3.1.3

G3.1.4

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 3/2

3.1 Application and Purpose

Application......................................................................................................This chapter applies to the FSCS.

It is also relevant to claimants.

Purpose......................................................................................................The purpose of this chapter is to set out in general terms the conditions thatmust be satisfied before the FSCS can make an offer of compensation.

The qualifying conditions for paying compensation are set out in greaterdetail in ■ COMP 4 - ■ COMP 7.

COMP 3 : The qualifying Section 3.2 : The qualifying conditions forconditions for compensation paying compensation

3

R3.2.1

R3.2.1A

R3.2.2

G3.2.3

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 3/3

3.2 The qualifying conditions for payingcompensation

The FSCS may pay compensation to an eligible claimant, subject to COMP 11(Payment of compensation), if it is satisfied that:

(1) an eligible claimant has made an application for compensation (orthe FSCS is treating the person as having done so);

(2) the claim is in respect of a protected claim against a relevant person(or, where applicable, a successor) who is in default; and

(3) where the FSCS so requires, the claimant has assigned the whole orany part of his rights against any one or more of the relevant person,any third party or, where applicable, a successor, to the FSCS, on suchterms as the FSCS thinks fit.

(4) [deleted]

Treating a person as having claimed......................................................................................................The FSCS may treat persons who are or may be entitled to claimcompensation as if they had done so.

Claims on behalf of another person......................................................................................................The FSCS may also pay compensation (and any recovery or other amountpayable by the FSCS to the claimant) to a person who makes a claim onbehalf of another person if the FSCS is satisfied that the person on whosebehalf the claim is made:

(1) is or would have been an eligible claimant; and

(2) would have been paid compensation by the FSCS had he been able tomake the claim himself, or to pursue his application for compensationfurther.

Examples of the circumstances covered by ■ COMP 3.2.2 R are:

(1) when personal representatives make a claim on behalf of thedeceased;

(2) when trustees make a claim on behalf of beneficiaries (for furtherprovisions relating to claims by trustees, see ■ COMP 12A.1.1R to■ 12A.1.7R);

COMP 3 : The qualifying Section 3.2 : The qualifying conditions forconditions for compensation paying compensation

3

R3.2.4

G3.2.5

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 3/4

(3) when the donee of an enduring power of attorney or a lasting powerof attorney makes a claim on behalf of the donor of the power;

(4) when the Court of Protection makes a claim on behalf of a personincapable by reason of mental disorder of managing andadministering his property and affairs;

(5) when an eligible claimant makes a claim for compensation but diesbefore his claim is determined.

The FSCS may also pay compensation to a firm, who makes a claim inconnection with protected non-investment insurance mediation on behalf ofits customers, if the FSCS is satisfied that:

(1) each customer has borne a shortfall in client money held by the firmcaused by a secondary pooling event arising out of the failure of abroker or settlement agent which is a relevant person in default;

(2) the customers in respect of which compensation is to be paid satisfythe conditions set out in ■ COMP 3.2.2 R (1);

(3) the customers do not have a claim against the relevant persondirectly, nor a claim against the firm, in respect of the same loss;

(4) the customers would have been paid compensation by FSCS if thecustomers had a claim for their share of the shortfall, and if the firmwere the relevant person; and

(5) the firm has agreed, on such terms as the FSCS thinks fit, to pay, orcredit the accounts of, without deduction, each relevant customer in(1), that part of the compensation equal to the customer's financialloss, subject to the limits in ■ COMP 10.2.

Special cases......................................................................................................See ■ COMP 12A (Special cases) for how the FSCS may pay compensation incertain cases.

Compensation

Chapter 4

Eligible claimants

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 4/1

COMP 4 : Eligible claimants Section 4.1 : Application and Purpose

4

R4.1.1

G4.1.2

G4.1.3

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 4/2

4.1 Application and Purpose

Application......................................................................................................This chapter applies to the FSCS.

It is also relevant to those who may wish to bring a claim for compensation.

Purpose......................................................................................................The purpose of this chapter is to set out the types of person who are able toclaim compensation or benefit from the protection the FSCS is able toprovide. A claimant needs to be an eligible claimant to satisfy COMP3.2.1R(1).

COMP 4 : Eligible claimants Section 4.2 : Who is eligible to benefit fromthe protection provided by the FSCS?

4

R4.2.1

R4.2.2

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 4/3

4.2 Who is eligible to benefit from theprotection provided by the FSCS?

An eligible claimant is any person who at any material time:

(1) did not come within ■ COMP 4.2.2 R; or

(2) did come within ■ COMP 4.2.2 R, but satisfied the relevant exception in■ COMP 4.3 or ■ COMP 4.4.

Persons not eligible to claim unless COMP 4.3 applies (seeCOMP 4.2.1R)......................................................................................................

This table belongs to COMP 4.2.1R

(1) Firms (other than a sole trader firm; a credit union; a trusteeof a stakeholder pension scheme (which is not an occupa-tional pension scheme) or personal pension scheme; a firm car-rying on the regulated activity of operating, or winding up, astakeholder pension scheme (which is not an occupational pen-sion scheme) or personal pension scheme; or a small business;in each case,whose claim arises out of a regulated activity forwhich they do not have a permission)

(2) Overseas financial services institutions

(3) Collective investment schemes, and anyone who is the oper-ator or depositary of such a scheme.

(4) Pension and retirement funds, and anyone who is a trusteeof such a fund. However, this exclusion does not apply to:

(a) a trustee of a personal pension scheme or a stake-holder pension scheme (which is not an occupationalpension scheme); or

(b) a trustee of an occupational pension scheme insofar asmembers’ benefits are money-purchase benefits; or

(c) insofar as members’ benefits are not money-purchasebenefits, a trustee of an occupational pension schemeof an employer which is not a large company, largepartnership or large mutual association.

(5) Supranational institutions, governments, and central adminis-trative authorities

(6) Provincial, regional, local and municipal authorities

(7) Directors of the relevant person in default or, in respect of aclaim against a successor in default, directors of any successoror directors of the relevant person. However, this exclusiondoes not apply if:

COMP 4 : Eligible claimants Section 4.2 : Who is eligible to benefit fromthe protection provided by the FSCS?

4

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 4/4

(a) (i) the relevant person in default is a mutual associ-ation which is not a large mutual associationand the directors do not receive a salary orother remuneration for services performed bythem for the relevant person in default; or

(ii) in respect of a claim against a successor in de-fault, the relevant person or a successor, towhichever the directorship relates, is a mutualassociation which is not a large mutual associ-ation and the directors do not receive a salaryor other remuneration for services performedby them for the relevant person or a successor,as applicable; or

(b) (i) the relevant person in default is a credit union;or

(ii) in respect of a claim against a successor in de-fault, the relevant person or a successor, towhichever the directorship relates, is a creditunion.

(8) [deleted]

(9) Bodies corporate in the same group as the relevant person indefault or, in respect of a claim against a successor in default,bodies corporate in the same group as a successor or the relev-ant person, as applicable, unless that body corporate is:

(a) a trustee of a stakeholder pension scheme (which isnot an occupational pension scheme) or a personal pen-sion scheme (but in each case if the trustee is a firm itwill only be an eligible claimant if its claim arises outof a regulated activity for which it does not have a per-mission); or

(aa) a trustee of:

(i) an occupational pension scheme in relation tomembers’ benefits which are money-purchasebenefits; or

(ii) (unless (i) applies) an occupational pensionscheme of an employer which is not a large com-pany, large partnership or large mutual associ-ation; or

(b) carrying on the regulated activity of operating or wind-ing up a stakeholder pension scheme (which is not anoccupational pension scheme) or personal pensionscheme.

(10) [deleted]

(11) [deleted]

COMP 4 : Eligible claimants Section 4.2 : Who is eligible to benefit fromthe protection provided by the FSCS?

4

R4.2.3

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 4/5

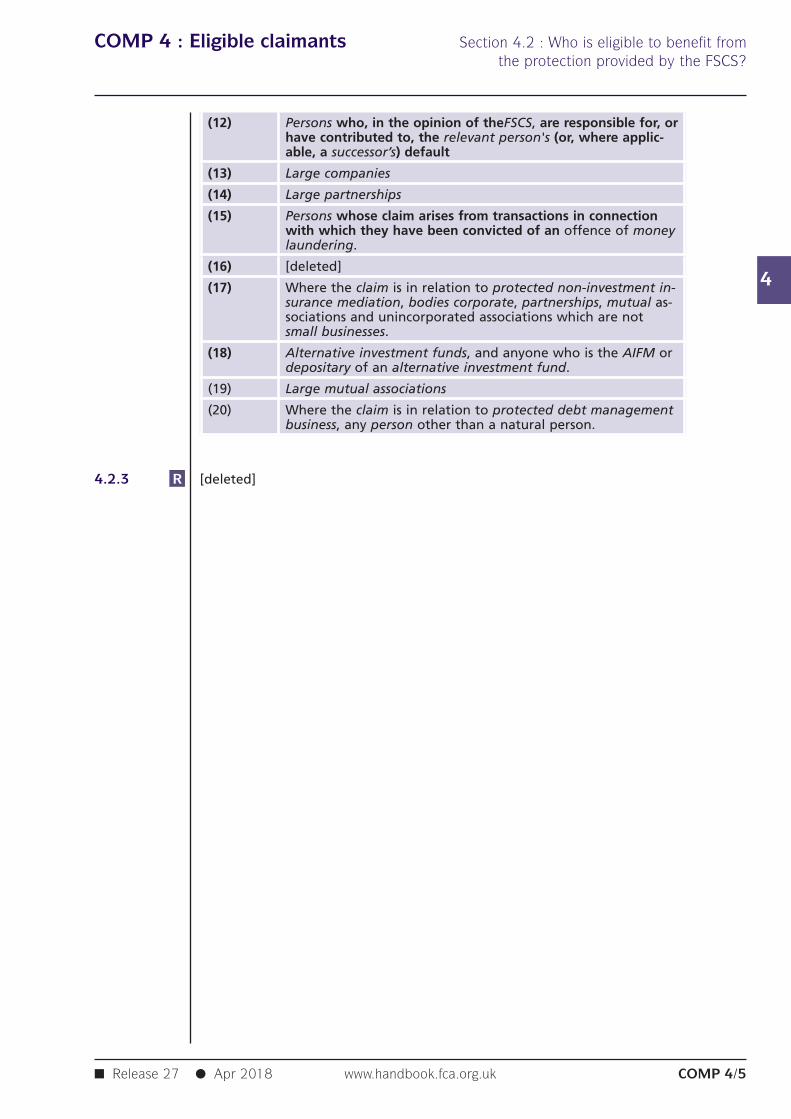

(12) Persons who, in the opinion of theFSCS, are responsible for, orhave contributed to, the relevant person's (or, where applic-able, a successor’s) default

(13) Large companies

(14) Large partnerships

(15) Persons whose claim arises from transactions in connectionwith which they have been convicted of an offence of moneylaundering.

(16) [deleted]

(17) Where the claim is in relation to protected non-investment in-surance mediation, bodies corporate, partnerships, mutual as-sociations and unincorporated associations which are notsmall businesses.

(18) Alternative investment funds, and anyone who is the AIFM ordepositary of an alternative investment fund.

(19) Large mutual associations

(20) Where the claim is in relation to protected debt managementbusiness, any person other than a natural person.

[deleted]

COMP 4 : Eligible claimants Section 4.3 : Exceptions: Circumstanceswhere a person coming within COMP 4.2.2R

may receive compensation

4

R4.3.1

R4.3.2

R4.3.3

R4.3.4

R4.3.5

R4.3.6

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 4/6

4.3 Exceptions: Circumstances where aperson coming within COMP 4.2.2Rmay receive compensation

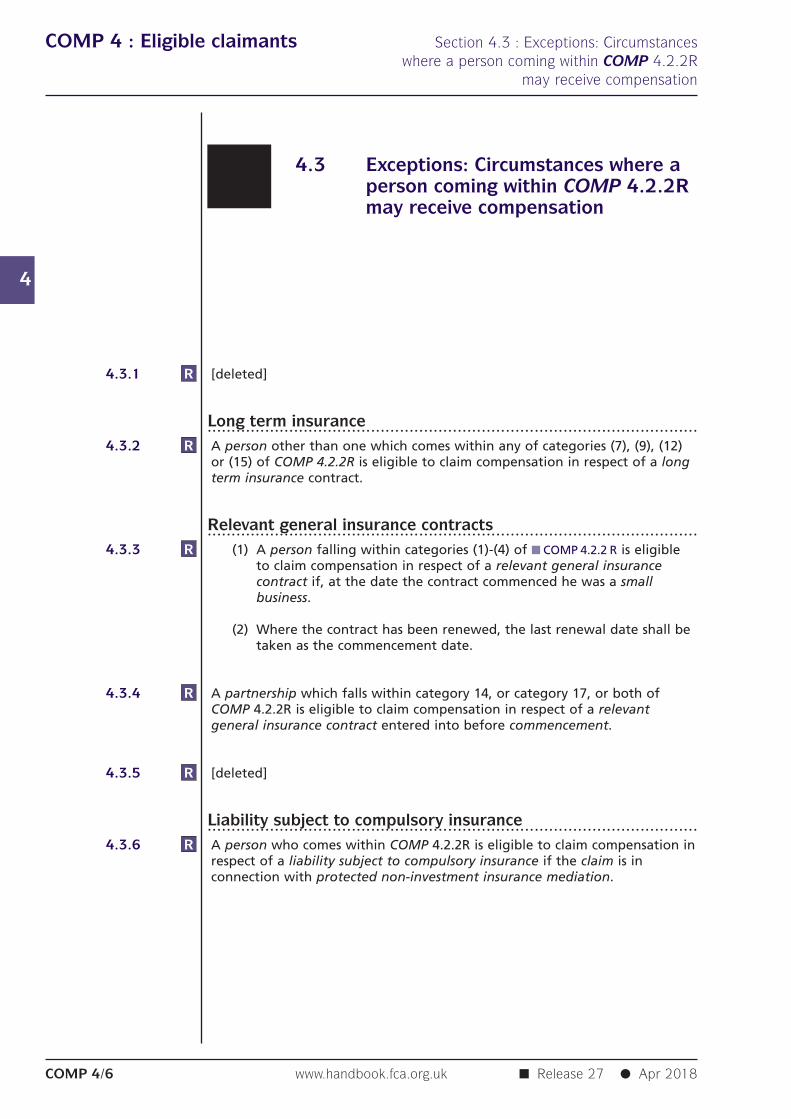

[deleted]

Long term insurance......................................................................................................A person other than one which comes within any of categories (7), (9), (12)or (15) of COMP 4.2.2R is eligible to claim compensation in respect of a longterm insurance contract.

Relevant general insurance contracts......................................................................................................(1) A person falling within categories (1)-(4) of ■ COMP 4.2.2 R is eligible

to claim compensation in respect of a relevant general insurancecontract if, at the date the contract commenced he was a smallbusiness.

(2) Where the contract has been renewed, the last renewal date shall betaken as the commencement date.

A partnership which falls within category 14, or category 17, or both ofCOMP 4.2.2R is eligible to claim compensation in respect of a relevantgeneral insurance contract entered into before commencement.

[deleted]

Liability subject to compulsory insurance......................................................................................................A person who comes within COMP 4.2.2R is eligible to claim compensation inrespect of a liability subject to compulsory insurance if the claim is inconnection with protected non-investment insurance mediation.

COMP 4 : Eligible claimants Section 4.3 : Exceptions: Circumstanceswhere a person coming within COMP 4.2.2R

may receive compensation

4

G4.3.7

R4.3.8

R4.3.9

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 4/7

Protected home finance mediation......................................................................................................There are no exceptions to COMP 4.2.2R for claims made in connection withprotected home finance mediation.

Eligibility to claim in specified circumstances......................................................................................................The FSCS may treat a person who comes within category (7) or (12) of■ COMP 4.2.2 R as eligible to claim compensation where:

(1) this is desirable to achieve the efficient performance of any of itsfunctions, including without limitation; to achieve the efficientpayment of compensation; and

(2) treating these persons as eligible to claim compensation would, in theopinion of the FSCS, be beneficial to the generality of eligibleclaimants who will be affected by the action in (1).

Protected investment business......................................................................................................A person is eligible to claim compensation for claims made in connectionwith protected investment business if, at the date at which the relevantperson (or, where applicable, a successor) is deemed to be in default, he:

(1) came within category (14) of ■ COMP 4.2.2 R and he does not exceedthe limits for a body corporate which qualifies as a small companyunder section 247 of the Companies Act 1985 or section 382 of theCompanies Act 2006 as applicable; or

(2) came within category (19) of ■ COMP 4.2.2 R.

COMP 4 : Eligible claimants Section 4.4 : Exceptions: Relevant generalinsurance contracts: mesothelioma claims

4

R4.4.1

R4.4.2

R4.4.3

R4.4.4

R4.4.5

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 4/8

4.4 Exceptions: Relevant generalinsurance contracts: mesotheliomaclaims

Application......................................................................................................[deleted]

Claims for contribution by responsible persons......................................................................................................[deleted]

[deleted]

[deleted]

Limits to amounts payable for contribution claims......................................................................................................[deleted]

Compensation

Chapter 5

Protected claims

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 5/1

COMP 5 : Protected claims Section 5.1 : Application and Purpose

5R5.1.1

G5.1.2

G5.1.3

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 5/2

5.1 Application and Purpose

Application......................................................................................................This chapter applies to the FSCS.

It is also relevant to claimants.

Purpose......................................................................................................The purpose of this chapter is to set out the various categories of claim forwhich compensation may be payable.

COMP 5 : Protected claims Section 5.2 : What is a protected claim?

5R5.2.1

G5.2.2

R5.2.3

G5.2.4

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 5/3

5.2 What is a protected claim?

A protected claim is:

(1) [deleted]

(2) [deleted]

(3) a claim in connection with protected investment business (see■ COMP 5.5); or

(4) a claim in connection with protected home finance mediation (see■ COMP 5.6); or

(5) a claim in connection with protected non-investment insurancemediation (see ■ COMP 5.7); or

(6) a claim in connection with protected debt management business (see■ COMP 5.8).

() [deleted]

Claims in respect of Law Society members......................................................................................................Notwithstanding ■ COMP 5.2.1 R and paragraph (1)(d) of the definition ofparticipant firm, where the relevant person is in default:

(1) is an authorised professional firm that is subject to the rules of theLaw Society (England and Wales) or the Law Society of Scotland; and

(2) with respect to its regulated activities, does not participate in therelevant society's compensation scheme:

a claim with respect to that person is only a protected claim if, when thebasis for the claim arose, that person did not participate in the relevantsociety's compensation scheme with respect to its regulated activities.

Claims in respect of successors......................................................................................................Where a claim for compensation is in respect of a claim against a successor,the following rules apply to the relevant person for whose liabilities thesuccessor has assumed responsibility (or to such relevant person’s activities, asthe case may be):

(1) ■ COMP 5.5.1R;

COMP 5 : Protected claims Section 5.2 : What is a protected claim?

5

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 5/4

(2) ■ COMP 5.5.2R;

(3) ■ COMP 5.5.3R;

(4) ■ COMP 5.6.1R;

(5) ■ COMP 5.6.2R; and

(6) ■ COMP 5.7.2R.

COMP 5 : Protected claims Section 5.5 : Protected investment business

5R5.5.1

R5.5.2

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 5/5

5.5 Protected investment business

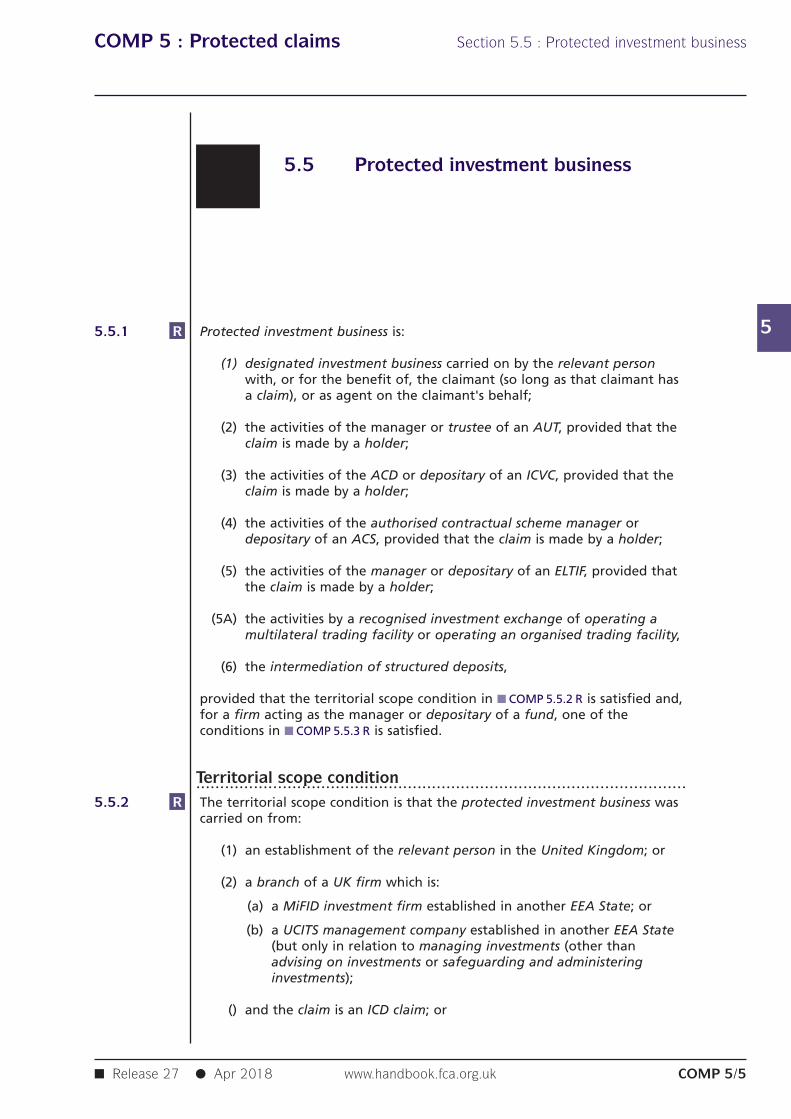

Protected investment business is:

(1) designated investment business carried on by the relevant personwith, or for the benefit of, the claimant (so long as that claimant hasa claim), or as agent on the claimant's behalf;

(2) the activities of the manager or trustee of an AUT, provided that theclaim is made by a holder;

(3) the activities of the ACD or depositary of an ICVC, provided that theclaim is made by a holder;

(4) the activities of the authorised contractual scheme manager ordepositary of an ACS, provided that the claim is made by a holder;

(5) the activities of the manager or depositary of an ELTIF, provided thatthe claim is made by a holder;

(5A) the activities by a recognised investment exchange of operating amultilateral trading facility or operating an organised trading facility,

(6) the intermediation of structured deposits,

provided that the territorial scope condition in ■ COMP 5.5.2 R is satisfied and,for a firm acting as the manager or depositary of a fund, one of theconditions in ■ COMP 5.5.3 R is satisfied.

Territorial scope condition......................................................................................................The territorial scope condition is that the protected investment business wascarried on from:

(1) an establishment of the relevant person in the United Kingdom; or

(2) a branch of a UK firm which is:

(a) a MiFID investment firm established in another EEA State; or

(b) a UCITS management company established in another EEA State(but only in relation to managing investments (other thanadvising on investments or safeguarding and administeringinvestments);

() and the claim is an ICD claim; or

COMP 5 : Protected claims Section 5.5 : Protected investment business

5

R5.5.3

R5.5.4

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 5/6

(3) both (1) and (2); or

(4) (a) a UK branch of an EEA UCITS management company; or

(b) an establishment of such an EEA UCITS management company inits Home State from which cross border services are being carriedon;

and in either case the management company is providing collectiveportfolio management services for a UCITS scheme but only if theclaim relates to that activity; or

(5) an establishment of an incoming EEA AIFM in another EEA State ifthe claim relates to providing AIFM management functions on a crossborder services basis for an authorised AIF.

Managers and depositaries of funds......................................................................................................The conditions referred to in ■ COMP 5.5.1 R for a manager or depositary of afund are:

(1) for the activities of managing an AIF, managing a UCITS orestablishing, operating or winding up a collective investment scheme,the claim is in respect of an investment in:

(a) an authorised fund; or

(b) any other fund which has its registered office or head office inthe UK or is otherwise domiciled in the UK unless it is an AIF thatis a body corporate and not a collective investment scheme;

(2) where a firm is acting as depositary of a fund, the claim is in respectof their activities for:

(a) an authorised fund; or

(b) a charity AIF unless it is a body corporate that is not a collectiveinvestment scheme.

Advising without a personal recommendation......................................................................................................The FSCS must treat a claim relating to advice in relation to a designatedinvestment that falls outside article 53(1) of the Regulated Activities Orderby virtue of article 53(1A) of that Order as being ‘in connection withprotected investment business’ for the purposes of ■ COMP 5.2.1R(3) wherethe relevant person giving the advice, at the time the act or omission givingrise to the claim took place:

(1) had, or required, permission to carry on; or

(2) (in the case of an appointed representative) was exempt from thegeneral prohibition in respect of,

an activity that was designated investment business.

COMP 5 : Protected claims Section 5.6 : Protected home financemediation

5R5.6.1

R5.6.2

R5.6.3

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 5/7

5.6 Protected home finance mediation

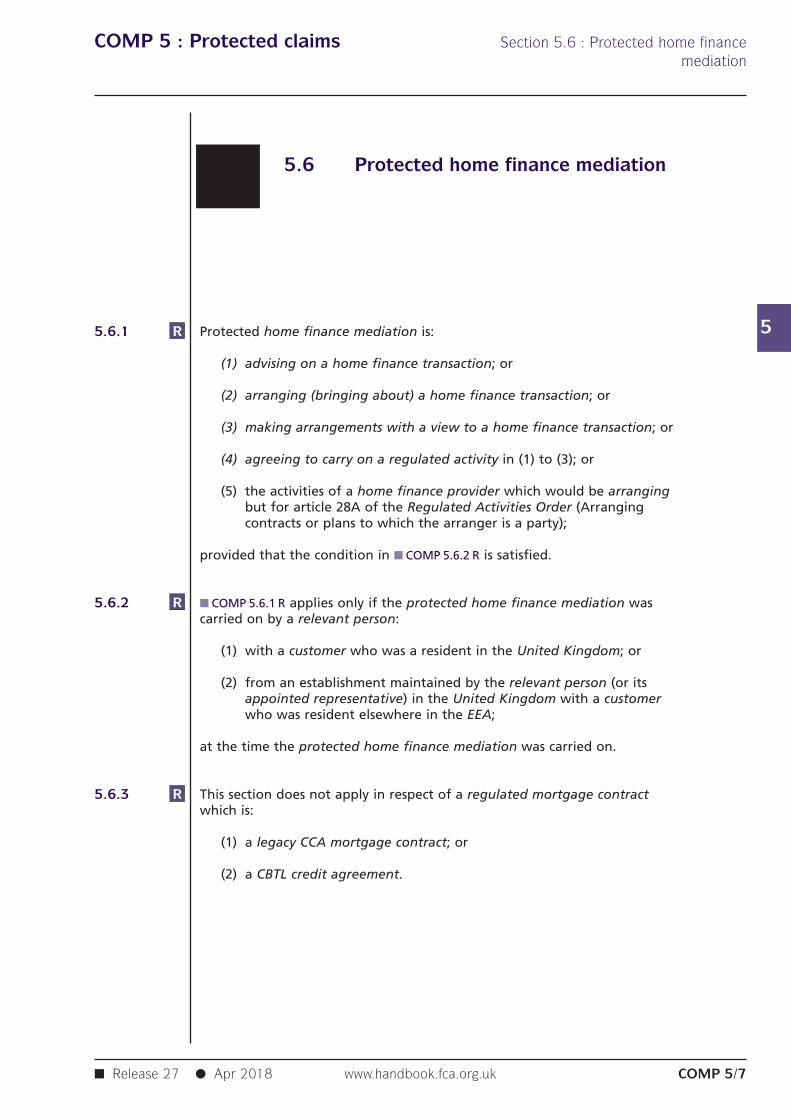

Protected home finance mediation is:

(1) advising on a home finance transaction; or

(2) arranging (bringing about) a home finance transaction; or

(3) making arrangements with a view to a home finance transaction; or

(4) agreeing to carry on a regulated activity in (1) to (3); or

(5) the activities of a home finance provider which would be arrangingbut for article 28A of the Regulated Activities Order (Arrangingcontracts or plans to which the arranger is a party);

provided that the condition in ■ COMP 5.6.2 R is satisfied.

■ COMP 5.6.1 R applies only if the protected home finance mediation wascarried on by a relevant person:

(1) with a customer who was a resident in the United Kingdom; or

(2) from an establishment maintained by the relevant person (or itsappointed representative) in the United Kingdom with a customerwho was resident elsewhere in the EEA;

at the time the protected home finance mediation was carried on.

This section does not apply in respect of a regulated mortgage contractwhich is:

(1) a legacy CCA mortgage contract; or

(2) a CBTL credit agreement.

COMP 5 : Protected claims Section 5.7 : Protected non-investmentinsurance mediation

5R5.7.1

R5.7.2

G5.7.3

G5.7.4

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 5/8

5.7 Protected non-investment insurancemediation

Protected non-investment insurance mediation is an insurance mediationactivity where the investment concerned is a relevant general insurancecontract or a pure protection contract but which is not a long-term careinsurance contract or a reinsurance contract, provided that the conditions in■ COMP 5.7.2 R are satisfied.

■ COMP 5.7.1 R only applies if the conditions in (1) and (2) are satisfied:

(1) the protected non-investment insurance mediation was carried onfrom:

(a) an establishment of the relevant person in the United Kingdom;or

(b) a branch of a UK firm established in another EEA State in theexercise of an EEA right derived from the IMD; and

(2) the claimant making the claim (or where ■ COMP 3.2.4 R applies, thecustomer on behalf of whom a firm makes a claim) dealt initially,with a view to entering into a relevant general insurance contract ora pure protection contract but not a long-term care insurancecontract or a reinsurance contract, with an intermediary that was:

(a) established in the United Kingdom; or

(b) a branch of a UK firm established in another EEA State in theexercise of an EEA right derived from the IMD.

The FSCS will not cover a claim against an intermediary or a successor of anintermediary that meets the criteria of either ■ COMP 5.7.2 R (2)(a) or■ COMP 5.7.2 R (2)(b) where the claimant was introduced to that intermediaryby an intermediary that does not meet the criteria of either■ COMP 5.7.2 R (2)(a) or ■ COMP 5.7.2 R (2)(b).

The FSCS will not cover a claim in respect of an intermediary that is not arelevant person, for example a retailer selling extended warranties that areconnected contracts. However, ■ COMP 5.7.2 R has the effect that a claim inrespect of a relevant person further up the chain carrying on protected non-investment insurance mediation in accordance with ■ COMP 5.7.2 R (1)(a) maybe covered by the FSCS if the claimant dealt initially with a UK intermediarythat is not a relevant person.

COMP 5 : Protected claims Section 5.7 : Protected non-investmentinsurance mediation

5

R5.7.5

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 5/9

Advising without a personal recommendation......................................................................................................The FSCS must treat a claim relating to advice on a relevant generalinsurance contract or a pure protection contract (which is not a long-terminsurance contract or a reinsurance contract) that falls outside article 53(1) ofthe Regulated Activities Order by virtue of article 53(1A) of that Order asbeing ‘in connection with protected non-investment insurance business’ forthe purposes of ■ COMP 5.2.1R(5) where the relevant person giving the advice,at the time the act or omission giving rise to the claim took place:

(1) had, or required, permission to carry on; or

(2) (in the case of an appointed representative) was exempt from thegeneral prohibition in respect of,

an activity that was non-investment insurance business.

COMP 5 : Protected claims Section 5.8 : Protected debt managementbusiness

5R5.8.1

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 5/10

5.8 Protected debt managementbusiness

Protected debt management business is debt management activity carriedout by a CASS debt management firm from an establishment maintained byit in the United Kingdom, but only in so far as the claim relates to a shortfallin client money.

Compensation

Chapter 6

Relevant persons andsuccessors in default

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 6/1

COMP 6 : Relevant persons and Section 6.1 : Application and Purposesuccessors in default

6R6.1.1

G6.1.2

G6.1.3

G6.1.4

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 6/2

6.1 Application and Purpose

Application......................................................................................................This chapter applies to the FSCS.

It is also relevant to claimants.

Purpose......................................................................................................The purpose of this chapter is to specify the types of person against whom aclaimant must have a claim in order to be eligible for compensation, andwhen those persons are 'in default'. Generally, this occurs when they areinsolvent or unable to meet their liabilities to claimants.

To be eligible for compensation a claimant's claim must be against a relevantperson (or, where applicable, a successor) in default: see ■ COMP 3.2.1 R (2).

COMP 6 : Relevant persons and Section 6.2 : Who is a relevant person?successors in default

6

R6.2.1

G6.2.2

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 6/3

6.2 Who is a relevant person?

A relevant person is a person who was, at the time the act or omission givingrise to the claim against it took place:

(1) a participant firm; or

(2) an appointed representative of a participant firm.

[deleted]

COMP 6 : Relevant persons and Section 6.3 : When is a relevant person insuccessors in default default?

6R6.3.1

G6.3.1A

R6.3.2

R6.3.3

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 6/4

6.3 When is a relevant person indefault?

A relevant person is in default if:

(1) (except in relation to an ICD claim) the FSCS has determined it to bein default under ■ COMP 6.3.2 R, ■ COMP 6.3.3 R or ■ COMP 6.3.4 R; or

(2) (in relation to an ICD claim):

(a) the FCA has determined it to be in default under ■ COMP 6.3.2 R;or

(b) a judicial authority has made a ruling that had the effect ofsuspending the ability of eligible claimants to bring claims againstthe participant firm, if that is earlier than (a); and

if a relevant person is in default in relation to an ICD claim it shall bedeemed to be in default in relation to any other type of protectedclaim.

[Note: article 2(2) of the Investor Compensation Directive]

The FSCS (or, where ■ COMP 6.3.1 R(2)(a) applies, the FCA) may determine arelevant person to be in default when it is, in the opinion of the FSCS (or theFCA):

(1) unable to satisfy protected claims against it; or

(2) likely to be unable to satisfy protected claims against it.

The FSCS may determine a relevant person to be in default if it is satisfiedthat a protected claim exists (other than an ICD claim), and the relevantperson is the subject of one or more of the following proceedings in theUnited Kingdom (or of equivalent or similar proceedings in anotherjurisdiction):

(1) the passing of a resolution for a creditors' voluntary winding up;

(2) a determination by the relevant person'sHome State regulator thatthe relevant person appears unable to meet claims against it and hasno early prospect of being able to do so;

COMP 6 : Relevant persons and Section 6.3 : When is a relevant person insuccessors in default default?

6

R6.3.4

R6.3.5

R6.3.6

R6.3.7

R6.3.8

R6.3.9

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 6/5

(3) the appointment of a liquidator or administrator, or provisionalliquidator or interim manager;

(4) the making of an order by a court of competent jurisdiction for thewinding up of a company, the dissolution of a partnership, theadministration of a company or partnership, or the bankruptcy of anindividual;

(5) the approval of a company voluntary arrangement, a partnershipvoluntary arrangement, or of an individual voluntary arrangement.

The FSCS may determine a relevant person to be in default if it is satisfiedthat a protected claim exists (other than an ICD claim), and:

(1) the FSCS is satisfied that the relevant person cannot be contacted atits last place of business and that reasonable steps have been takento establish a forwarding or current address, but without success; and

(2) there appears to the FSCS to be no evidence that the relevant personwill be able to meet claims made against it.

[deleted]

[deleted]

[deleted]

Claims arising under COMP 3.2.4 R......................................................................................................For the purposes of ■ COMP 6.3 a claim made by a firm under ■ COMP 3.2.4 R isto be treated as if it were a protected claim against the relevant person.

Scheme manager's power to require information......................................................................................................For the purposes of sections 219(1A)(b) and (d) of the Act (Scheme manager'spower to require information) whether a relevant person is unable or likelyto be unable to satisfy claims shall be determined by reference to whether itis in default.

COMP 6 : Relevant persons and Section 6.3A : When is a successor insuccessors in default default?

6

R6.3A.1

R6.3A.2

R6.3A.3

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 6/6

6.3A When is a successor in default?

A successor is in default if:

the FSCS has determined it to be in default under■ COMP 6.3A.2R, ■ COMP 6.3A.3R, or ■ COMP 6.3A.4R, unless theclaim is within (b); or

(in relation to an ICD claim against a successor that is a MiFIDinvestment firm):

the FCA has determined it to be in default under■ COMP 6.3A.2R; or

a judicial authority has made a ruling that had the effect ofsuspending the ability of eligible claimants to bring claimsagainst the successor, if that is earlier than (i).

If a successor is in default in relation to an ICD claim within (1)(b) it isto be deemed to be in default in relation to any other type ofprotected claim.

The FSCS (or, where ■ COMP 6.3A.1R(1)(b)(i) applies, the FCA) may determine asuccessor to be in default when it is, in the opinion of the FSCS (or the FCA):

(1) unable to satisfy protected claims against it; or

(2) likely to be unable to satisfy protected claims against it.

The FSCS may determine a successor to be in default if it is satisfied that aprotected claim exists (other than an ICD claim against a successor that is aMiFID investment firm), and the successor is the subject of one or more ofthe following proceedings in the United Kingdom (or of equivalent or similarproceedings in another jurisdiction):

(1) the passing of a resolution for a creditors' voluntary winding up; or

(2) a determination by the successor’s Home State regulator that thesuccessor appears unable to meet claims against it and has no earlyprospect of being able to do so; or

(3) the appointment of a liquidator or administrator, or provisionalliquidator or interim manager; or

(4) the making of an order by a court of competent jurisdiction for thewinding up of a company, the dissolution of a partnership, the

COMP 6 : Relevant persons and Section 6.3A : When is a successor insuccessors in default default?

6

R6.3A.4

R6.3A.5

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 6/7

administration of a company or partnership, or the bankruptcy of anindividual; or

(5) the approval of a company voluntary arrangement, a partnershipvoluntary arrangement, or an individual voluntary arrangement.

The FSCS may determine that a successor to be in default if it is satisfied thata protected claim exists (other than an ICD claim against a successor that isan MiFID investment firm), and:

(1) the FSCS is satisfied that the successor cannot be contacted at its lastplace of business and that reasonable steps have been taken toestablish a forwarding or current address, but without success; and

(2) there appears to the FSCS to be no evidence that the successor will beable to meet claims made against it.

For the purposes of sections 219(1A)(b) and (d) of the Act (Scheme manager'spower to require information) whether a successor is unable or likely to beunable to satisfy claims is to be determined by reference to whether it is indefault.

COMP 6 : Relevant persons and Section 6.3A : When is a successor insuccessors in default default?

6

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 6/8

Compensation

Chapter 7

Assignment or subrogation ofrights

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 7/1

COMP 7 : Assignment or Section 7.1 : Applicationsubrogation of rights

7

R7.1.1

G7.1.2

G7.1.3

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 7/2

7.1 Application

Application and Purpose......................................................................................................This chapter applies to the FSCS.

It is also relevant to claimants.

Purpose......................................................................................................The FSCS may (and in some cases must) make an offer of compensationconditional on the assignment of rights to it by a claimant. The FSCS mayalso be subrogated automatically to the claimant's rights.The purpose of thischapter is to make provision for and set out the consequences of anassignment or subrogation of the claimant's rights.

COMP 7 : Assignment or Section 7.2 : How does the assignment ofsubrogation of rights rights work?

7

R7.2.1

R7.2.2

R7.2.3

R7.2.3A

R7.2.3AA

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 7/3

7.2 How does the assignment of rightswork?

The FSCS may make any payment of compensation to a claimant in respectof any protected claim conditional on the claimant assigning the whole orany part of his rights against any one or more of the the relevant person,any third party, or, where applicable, a successor, to the FSCS on such termsas the FSCS thinks fit.

If a claimant assigns the whole or any part of his rights against any person tothe FSCS as a condition of payment, the effect of this is that any sum payablein relation to the rights so assigned will be payable to the FSCS and not theclaimant.

(1) Before taking assignment of rights from the claimant under■ COMP 7.2.1 R, the FSCS must inform the claimant that if, after takingassignment of rights, the FSCS decides not to pursue recoveries usingthose rights it will, if the claimant so requests in writing, reassign theassigned rights to the claimant. The FSCS must comply with such arequest in such circumstances (see ■ COMP 7.4.2 R).

(2) [deleted] [Editor's Note: The text of this sub-paragraph has beenmoved to new ■ COMP 7.4.1 R.]

(3) [deleted]

[deleted]

Electronic assignment......................................................................................................Where the FSCS has paid compensation in respect of a claim, this has theeffect that:

(1) an assignment completed and signed electronically in a formprescribed by the FSCS will be deemed to satisfy the formalities for avalid legal assignment;

(2) production of a hard copy of the electronically signed assignmentform is conclusive evidence (or, in Scotland, sufficient evidence) thatthe formalities of a legal assignment have been complied with andthat a legal assignment has occurred; and

COMP 7 : Assignment or Section 7.2 : How does the assignment ofsubrogation of rights rights work?

7

R7.2.3B

G7.2.3C

G7.2.3D

R7.2.3E

R7.2.4

R7.2.4A

R7.2.5

G7.2.6

R7.2.7

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 7/4

(3) an assignment completed electronically in the prescribed form is to betreated as having been made by writing under the hand of theassignor for the purposes of section 136 of the Law of Property Act1925 and any other formal requirement.

[deleted]

[deleted]

[deleted]

[deleted] [Editor's Note: The amended text of this provision has been movedto new ■ COMP 7.6.1 R.]

[deleted] [Editor's Note: The amended text of this provision has been movedto new ■ COMP 7.6.2 R.]

[deleted] [Editor's Note: The text of this provision has been moved to new■ COMP 7.6.3 R.]

[deleted] [Editor's Note: The amended text of this provision has been movedto new ■ COMP 7.6.4 R.]

[deleted] [Editor's Note: The text of this provision has been moved to new■ COMP 7.6.5 G.]

Claims arising under COMP 3.2.4R......................................................................................................(1) For the purposes of compensation paid under ■ COMP 3.2.4 R, FSCS

may require any firm (including, but not limited to, the claimant firm)to assign to FSCS any rights the firm may have to claim against therelevant person in relation to the amount of the shortfall in clientmoney arising out of the failure of the relevant person.

(2) A firm required by FSCS to assign its rights in (1), must assign thoserights as requested, unless it has a reasonable excuse for not doingso.

COMP 7 : Assignment or Section 7.3 : Automatic subrogationsubrogation of rights

7

R7.3.1

R7.3.2

R7.3.3

R7.3.4

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 7/5

7.3 Automatic subrogation

[deleted]

The FSCS's powers in this section may be used:

(1) separately or in any combination as an alternative and in substitutionfor the powers and processes elsewhere in this sourcebook; and/or

(2) [deleted]

(3) in relation to all or any part of a protected claim or class of protectedclaim made with respect to the relevant person (or, where applicable,a successor).

(4) [deleted]

The FSCS may determine that the exercise of any power in this section issubject to such incidental, consequential or supplemental conditions as theFSCS considers appropriate.

Determinations by the FSCS......................................................................................................(1) Any power conferred on the FSCS to make determinations under this

section is exercisable in writing.

(2) An instrument by which the FSCS makes the determination mustspecify the provision under which it is made, the date and time fromwhich it takes effect and the relevant person (or, where applicable, asuccessor) and protected claims, parts of protected claims and/orclasses of protected claims in respect of which it applies.

(3) The FSCS must take appropriate steps to publish the determination assoon as possible after it is made. Such publication must beaccompanied by a statement explaining the effect of ■ COMP 7.4.2 R.

(4) Failure to comply with any requirement in this rule does not affectthe validity of the determination.

(5) A determination by the FSCS under this section may be amended,remade or revoked at any time and subject to the same conditions.

COMP 7 : Assignment or Section 7.3 : Automatic subrogationsubrogation of rights

7

R7.3.5

R7.3.6

R7.3.7

R7.3.8

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 7/6

Verification of determinations......................................................................................................(1) The production of a copy of a determination purporting to be made

by the FSCS under this section:

(a) on which is endorsed a certificate, signed by a member of theFSCS's staff authorised by it for that purpose; and

(b) which contains the required statements;

is evidence (or in Scotland sufficient evidence) of the facts stated inthe certificate.

(2) The required statements are:

(a) that the determination was made by the FSCS; and

(b) that the copy is a true copy of the determination.

(3) A certificate purporting to be signed as mentioned in (1) is to betaken to have been properly signed unless the contrary is shown.

(4) A person who wishes in any legal proceedings to rely on adetermination may require the FSCS to endorse a copy of thedetermination with a certificate of the kind mentioned in (1).

Effect of this section on other provisions in this sourcebook etc......................................................................................................Other provisions in this sourcebook and ■ FEES 6 are modified to the extentnecessary to give full effect to the powers provided for in this section.

Other than as expressly provided for, nothing in this section is to be taken aslimiting or modifying the rights or obligations of or powers conferred on theFSCS elsewhere in this sourcebook or in ■ FEES 6.

Rights and obligations against the relevant persons,successors and third parties......................................................................................................The FSCS may determine that:

(1) the payment of compensation by the FSCS;

COMP 7 : Assignment or Section 7.3 : Automatic subrogationsubrogation of rights

7

R7.3.9

R7.3.10

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 7/7

(2) [deleted]

shall have all or any of the following effects:

(3) the FSCS shall immediately and automatically be subrogated, subjectto such conditions as the FSCS determines are appropriate, to all orany part (as determined by the FSCS) of the rights and claims in theUnited Kingdom and elsewhere of the claimant against the relevantperson (or, where applicable, a successor) and/or any third party(whether such rights are legal, equitable or of any other naturewhatsoever and in whatever capacity the relevant person (or, whereapplicable, a successor) or third party is acting) in respect of or arisingout of the claim in respect of which the payment of or on account ofcompensation was made;

(4) the FSCS may claim and take legal or any other proceedings or stepsin the United Kingdom or elsewhere to enforce such rights in its ownname or in the name of, and on behalf of, the claimant, or in bothnames against the relevant person (or, where applicable, a successor)and/or any third party;

(5) the subrogated rights and claims conferred on the FSCS shall be rightsof recovery and claims against the relevant person (or, whereapplicable, a successor) and/or any third party which are equivalent(including as to amount and priority and whether or not the relevantperson (or, where applicable, a successor) is insolvent) to and do notexceed the rights and claims that the claimant would have had; and/or

(6) such rights and/or obligations (as determined by the FSCS) as betweenthe relevant person (or, where applicable, a successor) and theclaimant arising out of the protected claim in respect of which thepayment was made shall be transferred to, and subsist between,another authorised person (or, where a successor is not an authorisedperson, an authorised person) with an appropriate permission and theclaimant provided that the authorised person has consented (but thetransferred rights and/or obligations shall be treated as existingbetween the relevant person (or where applicable, a successor) andthe FSCS to the extent of any subrogation, transfer or assignment forthe purposes of (3) to (5) and ■ COMP 7.3.9 R).

The FSCS may alternatively or additionally make the actions in■ COMP 7.3.8R (1) conditional on the claimant assigning or transferring thewhole or any part of all such rights as he may have against the relevantperson (or, where applicable, a successor) and/or any third party on suchterms as the FSCS determines are appropriate.

(1) The FSCS may determine that:

(a) if the claimant does not assign or transfer his rights under■ COMP 7.3.9 R;

(b) if it is impractical to obtain such an assignment or transfer; and/or

(c) if it is otherwise necessary or desirable in conjunction with theexercise of the FSCS's powers under ■ COMP 7.3.8 R or■ COMP 7.3.9 R;

COMP 7 : Assignment or Section 7.3 : Automatic subrogationsubrogation of rights

7

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 7/8

that claimant shall be treated as having irrevocably andunconditionally appointed the chairman of the FSCS for the timebeing to be his attorney and agent and on his behalf and in hisname or otherwise to do such things and execute such deeds anddocuments as may be required under such laws of the UnitedKingdom, another EEA State or any other state or law-country tocreate or give effect to such assignment or transfer or otherwise givefull effect to those powers.

(2) The execution of any deed or document under (1) shall be as effectiveas if made in writing by the claimant or by his agent lawfullyauthorised in writing or by will.

COMP 7 : Assignment or Section 7.4 : Duty on FSCS to pursuesubrogation of rights recoveries

7

R7.4.1

R7.4.2

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 7/9

7.4 Duty on FSCS to pursue recoveries

If the FSCS takes assignment or transfer of rights from the claimant or isotherwise subrogated to the rights of the claimant, it must pursue all andonly such recoveries as it considers are likely to be both reasonably possibleand cost effective to pursue.

If the FSCS decides not to pursue such recoveries and a claimant wishes topursue those recoveries himself and so requests in writing, the FSCS mustcomply with that request and assign the rights back to the claimant.

COMP 7 : Assignment or Section 7.6 : Treatment of recoveriessubrogation of rights

7

R7.6.1

R7.6.2

R7.6.3

R7.6.4

G7.6.5

■ Release 27 ● Apr 2018www.handbook.fca.org.ukCOMP 7/10

7.6 Treatment of recoveries

If the FSCS makes recoveries in relation to a claim, it may deduct from anyrecoveries paid over to the claimant under ■ COMP 7.6.2 R part or all of itsreasonable costs of recovery and distribution (if any).

Unless compensation was paid under ■ COMP 9.2.3 R, if a claimant assigns ortransfers his rights to the FSCS or a claimant's rights and claims are otherwisesubrogated to the FSCS and the FSCS subsequently makes recoveries throughthose rights or claims, those recoveries must be paid to the claimant:

(1) to the extent that the amount recovered exceeds the amount ofcompensation (excluding interest paid under ■ COMP 11.2.7 R) receivedby the claimant in relation to the protected claim; or

(2) in circumstances where the amount recovered does not exceed theamount of compensation paid, to the extent that failure to pay anysums recovered to the claimant would leave a claimant who hadpromptly accepted an offer of compensation or whose rights andclaims had been subrogated to the FSCS at a disadvantage relative toa claimant who had delayed accepting an offer of compensation orwhose claims had not been subrogated (see ■ COMP 7.6.4 R).

For the purpose of ■ COMP 7.6.2 R compensation received by eligible claimantsin relation to contracts of insurance written at Lloyd’s may include paymentsmade from the Central Fund.

The FSCS must endeavour to ensure that a claimant will not sufferdisadvantage arising solely from his prompt acceptance of the FSCS's offer ofcompensation or from the subrogation of his rights and claims to the FSCScompared with what might have been the position had he delayed hisacceptance or had his claims not been subrogated.

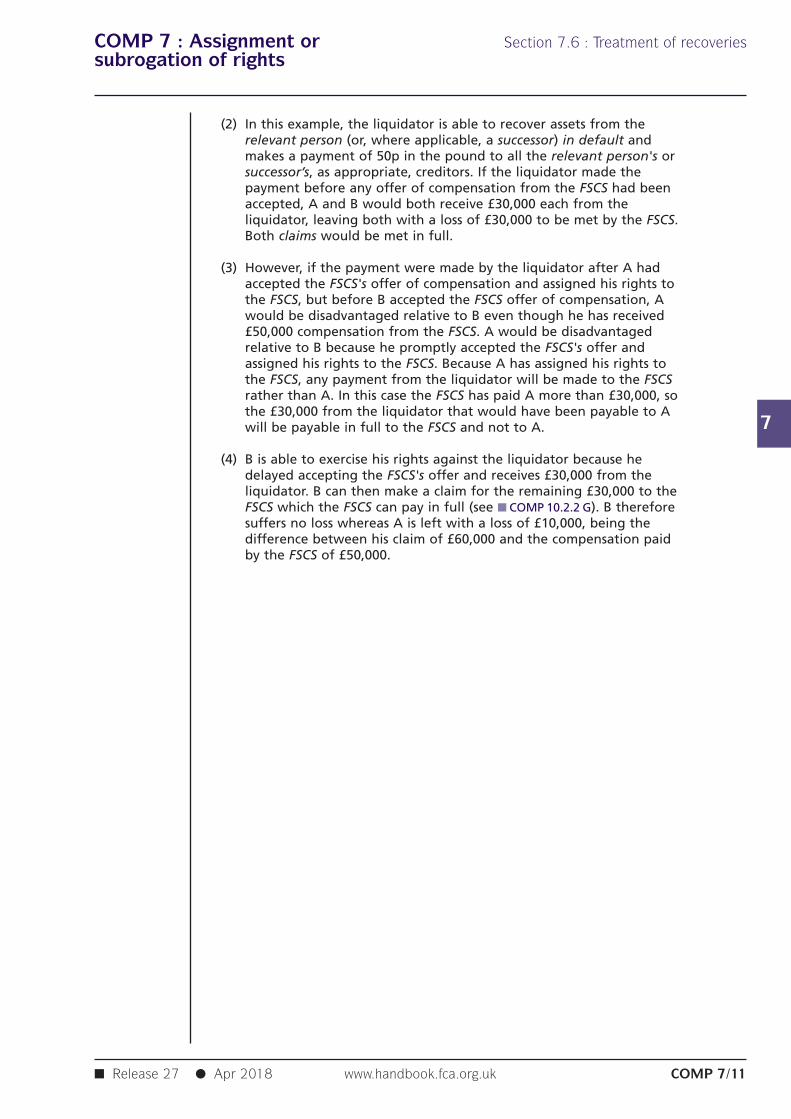

As an example of the circumstances which ■ COMP 7.6.4 R is designed toaddress, take two claimants, A and B.

(1) Both A and B have a protected investment business claim of £60,000against a relevant person (or, where applicable, a successor) indefault. The FSCS offers both claimants £50,000 compensation (themaximum amount payable for such claims under ■ COMP 10.2.3 R). Aaccepts immediately, and assigns his rights against the relevant person(or, where applicable, a successor) to the FSCS, but B delays acceptingthe FSCS's offer of compensation.

COMP 7 : Assignment or Section 7.6 : Treatment of recoveriessubrogation of rights

7

■ Release 27 ● Apr 2018 www.handbook.fca.org.uk COMP 7/11

(2) In this example, the liquidator is able to recover assets from therelevant person (or, where applicable, a successor) in default andmakes a payment of 50p in the pound to all the relevant person's orsuccessor’s, as appropriate, creditors. If the liquidator made thepayment before any offer of compensation from the FSCS had beenaccepted, A and B would both receive £30,000 each from theliquidator, leaving both with a loss of £30,000 to be met by the FSCS.Both claims would be met in full.

(3) However, if the payment were made by the liquidator after A hadaccepted the FSCS's offer of compensation and assigned his rights tothe FSCS, but before B accepted the FSCS offer of compensation, Awould be disadvantaged relative to B even though he has received£50,000 compensation from the FSCS. A would be disadvantagedrelative to B because he promptly accepted the FSCS's offer andassigned his rights to the FSCS. Because A has assigned his rights tothe FSCS, any payment from the liquidator will be made to the FSCSrather than A. In this case the FSCS has paid A more than £30,000, sothe £30,000 from the liquidator that would have been payable to Awill be payable in full to the FSCS and not to A.