Compelling Wealth Management...

65

Oppenheimer funds are distributed by OppenheimerFunds Distributor, Inc., 225 Liberty Street, New York, NY 10281-1008 © 2015 OppenheimerFunds Distributor, Inc. All rights reserved. Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency and involve investment risks, including the possible loss of the principal amount invested. Compelling Wealth Management Conversations Q4 2015

Transcript of Compelling Wealth Management...

Oppenheimer funds are distributed by OppenheimerFunds Distributor, Inc., 225 Liberty Street, New York, NY 10281-1008© 2015 OppenheimerFunds Distributor, Inc. All rights reserved.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency and involve investment risks, including the possible loss of the principal amount invested.

Compelling Wealth

Management Conversations

Q4 2015

2

Agenda

• The Principles of Sound Investing

• Historical Context

• Current Opportunities

The Principles of

Sound Investing

Th

e P

rinc

iple

s

of S

ou

nd

Inve

stin

g

Consistency Courage Balance

4

“Everyone has a plan until they get hit.”– Joe Louis

The Principle ofConsistency

5

20-Year Annualized Returns % (1994–2013)

What Has the Greatest Impact on

Investment Results?

10.2%9.2%

5.8% 5.7% 5.7%

2.9%2.4% 2.5%

REITs U.S. Stocks Gold InternationalEquities

Government-Related Bonds

Homes Inflation AverageInvestor

Source: Bloomberg, 12/31/13. Average asset allocation investor return is based on an analysis by DALBAR, Inc., which utilizes the net of aggregate mutual fund sales,

redemptions and exchanges each month as a measure of investor behavior. Indices shown are as follows: REITs are represented by the FTSE NAREIT Equity REIT Index, Gold

is represented by the U.S. dollar spot price of one troy ounce, Homes are represented by U.S. existing home sales median price, inflation is represented by the Consumer Price

Index. U.S. stocks are represented by the S&P 500 Index, international equities are represented by the MSCI EAFE Index, government-related bonds are represented by the

Barclays U.S. Aggregate Bond Index. Indices are unmanaged and cannot be purchased directly by investors. Index performance is shown for illustrative purposes only and does

not predict or depict the performance of any investment. Index definitions can be found on Page 71. Past performance does not guarantee future results.

Investor BehaviorInvestment Returns

6

Missing Even the 10 Best Days in the Market Reduced

Returns by Almost 50% in the Last 20 YearsS&P 500 Index: performance of $100,000 investment (1994–2014)

The Truth About “Sell in May and Go Away”

Growth of $1,000: S&P 500 Index buy and hold vs. selling

every May, going to T-bills, and buying again in November

No One Has a Crystal Ball, Yet Often People

Act as Though They Do

Source: Morningstar Direct as of 12/31/14. For illustrative purposes only and is not intended as investment advice. The charts are hypothetical examples which are shown for

illustrative purposes only and do not predict or depict the performance of any investment. Index definitions can be found on Page 71. Past performance does not guarantee

future results.

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

$6,000,000

$1,268,814

$5,305,992

Sell in May

and Buy in

November

Buy and

HoldMay

AprilApr

Annualized

Return

8.09%

$474,257

Annualized

Return

4.41%

$236,864

Annualized

Return

-0.12%

$97,651

Annualized

Return

-3.76%

$46,486

Annualized

Return

-5.36%

$33,244

Annualized

Return

1.97%

$149,674

Annualized

Return

-2.03%

$66,416

Fully

Invested

Missed

10

Best

Days

Missed

20

Best

Days

Missed

30

Best

Days

Missed

40

Best

Days

Missed

50

Best

Days

Missed

60

Best

Days

7

Odds of Winning at Various Casino Games Percentage of Years U.S. Stocks Posted Positive

Returns Over Rolling Periods (1926–2014)

Is the Market Really Like a Casino?

Rolling Monthly Returns

Source: Morningstar Direct, 12/31/14. Chart is for illustrative purposes only and is not intended as investment advice. U.S. stocks are represented by the S&P 500 Index.

Source of Casino odds: Wizard of Odds. The charts are hypothetical examples which are shown for illustrative purposes only and do not predict or depict the

performance of any investment. Index definitions can be found on Page 71. Past performance does not guarantee future results.

40.0%

44.7%

48.0%

48.6%

46.6%

23.0%

46.5%

48.8%

40.0%

75.1%

82.9%87.1%

94.4%99.8%

1-Year 3-Year 5-Year 10-Year 15-Year

8

Stocks Go Up Because Earnings Improve

Source: Bloomberg, as of 12/31/14. Company logos are for illustrative purposes only and are not intended as investment advice. The mention of specific companies does

not constitute a recommendation on behalf of any fund or OppenheimerFunds, Inc. Correlation expresses the strength of relationship between distribution of returns of

two sets of data. The correlation coefficient is always between +1 (perfect positive correlation) and –1 (perfect negative correlation). A perfect correlation occurs when the

two series being compared behave in exactly the same manner. Index definitions can be found on Page 71. Past performance does not guarantee future results.

9

“Courage is rightly esteemed the first of human qualities because

it is the quality which guarantees all others.”

– Sir Winston Churchill

The Principle ofCourage

10

$2,520,587

$10,000

$100,000

$1,000,000

0.0%

1.0%

2.0%

3.0%

4.0% Dow Jones Industrial Average: Volatility(3-Month Moving Average), Left Axis

Dow Jones Industrial Average: Growth of$10,000 Right Axis

Every Generation Faces Its Share of Challenges

“In the 20th century, the United States endured two world wars...the Depression, a dozen or so recessions and

financial panics, oil shocks, a flu epidemic, and the resignation of a disgraced president. Yet the Dow rose from

66 to 11,497.” – Warren Buffett, 10/17/08

Dow Jones Industrial Average: Growth of $10,000 and Volatility (1900–2014)

Source: Morningstar Direct and Ibbotson, 12/31/14. The charts are hypothetical examples which are shown for illustrative purposes only and do not predict or depict the

performance of any investment. Index definitions can be found on Page 71. Past performance does not guarantee future results.

(Log S

cale

)

1900 1920 1940 1960 1980 2000 2014

11

-7-10

1517

1

26

15

2

12

27

-7

26

47

-2

34

20

31

27

20

-10-13

-23

26

9

3

14

4

-38

23

13

0

13

30

11

-18

-14

-7

-13

-8 -9

-33

-8 -8

-20

-6 -6-5

-9

-3

-8-11

-19

-12

-17

-26

-32

-14

-8 -7 -8-10

-47

-26

-16-19

-10

-6

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Volatility Does Not Equal Loss Unless You Sell

Source: Bloomberg, 12/31/14. Calendar year returns are price returns, meaning that they do not include the reinvestment of dividends. The index is unmanaged and

cannot be purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any investment.

Index definitions can be found on Page 71. Past performance does not guarantee future results.

S&P 500 Index Calendar Year Price Return(%) S&P 500 Index Largest Intra-Year Price Decline (%)

Annualized

Total Return

+11.1%

Average Intra-

year Decline

–14.4%

“I’ve lived through some terrible things in my life some of which have actually happened.”

—Mark Twain

12

Stocks Outperform Most Asset Classes Over Time

Source: Morningstar Direct, 12/31/14. Small-Cap Stocks are represented by the total return for the SBBI U.S. Small Company Stock Index. Large-Cap Stocks are

represented by the SBBI U.S. Large Company Stock Index. Government bonds are represented by the SBBI U.S. Long-Term Government Bond Index. Gold is

represented by the U.S. dollar spot price of one troy ounce. Real estate is represented by the Shiller Real Home Price Index. Government bills are represented by the

SBBI U.S. (30-day) Treasury Bills. Inflation is represented by the Consumer Price Index. The charts are hypothetical examples which are shown for illustrative purposes

only and do not predict or depict the performance of any investment. Index definitions can be found on Page 71. Past performance does not guarantee future results.

13

-100%

0%

100%

200%

300%

400%

500%

1 2 3 4 5 6 7 8 9 10

Years after crisis

MSCI Mexico Index – December 1994 MSCI Korea Index – November 1997

“When there is blood on the street, I am buying”

– Baron RothschildCumulative Monthly Returns

Source: Bloomberg,12/31/14. The charts are hypothetical examples which are shown for illustrative purposes only and do not predict or depict the performance of any investment.

Index definitions can be found on Page 71. Past performance does not guarantee future results.

MSCI Russia Index – August 1998 MSCI Argentina Index – December 2001

-100%

-50%

0%

50%

100%

150%

200%

1 2 3 4 5 6 7 8 9 10

Years after crisis

0%

500%

1000%

1500%

2000%

1 2 3 4 5 6 7 8 9 10

Years after crisis

-1000%

0%

1000%

2000%

3000%

4000%

5000%

6000%

1 2 3 4 5 6 7 8 9 10

Years after crisis

443%

3891%

175%

1165%

14

$100,000 Investment in Barclays High Yield Bond Index

(1989–2014)

$100,000 Investment in Barclays Municipal Bond Index

(1981–2014)

Forget About the Price, Focus on Income

Source: Bloomberg,12/31/14. The charts are hypothetical examples which are shown for illustrative purposes only and do not predict or depict the performance of any investment.

Index definitions can be found on Page 71. Past performance does not guarantee future results.

“The most powerful force in the universe is compound interest.”— Albert Einstein

$816,740

$0

$200,000

$400,000

$600,000

$800,000

1989 1993 1996 1999 2002 2005 2008 2012

Price Growth Total Growth

$1,191,386

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

1981 1986 1990 1994 1999 2003 2007 2012

Price Growth Total Growth

More than 101% of the return

has come from the income!

98% of the return

has come from the income!

15

“Life is about balance. The good and the bad. The highs and the lows.

The piña and the colada.”— Ellen DeGeneres

The Principle ofBalance

16

Annual Returns % (2003–YTD 2015)

Asset Classes Move In and Out of Favor

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

Emerging

Markets

55.82

REITs

31.58

Emerging

Markets

34.00

REITs

35.06

Emerging

Markets

39.42

U.S.

Aggregate

5.24

Emerging

Markets

78.51

MLPs

35.85

MLPs

13.88

Emerging

Markets

18.22

U.S.

Small Cap

38.82

REITs

30.14

U.S.

Aggregate

0.45

U.S.

Small Cap

47.25

Emerging

Markets

25.55

Commodities

21.36

Emerging

Markets

32.14

Commodities

16.23

High Yield

–26.55

MLPs

76.41

REITs

27.96

REITs

8.29

REITs

18.06

U.S.

Large Cap

33.11

U.S.

Large Cap

13.24

High Yield

0.04

MLPs

44.54

International

Stocks

20.25

International

Stocks

13.54

International

Stocks

26.34

MLPs

12.72

U.S.

Small Cap

–33.79

High Yield

58.17

U.S.

Small Cap

26.85

U.S.

Aggregate

7.84

International

Stocks

17.32

MLPs

27.58

U.S.

Aggregate

5.97

International

Stocks

–0.21

International

Stocks

38.59

U.S.

Small Cap

18.33

REITs

12.16

MLPs

26.07

International

Stocks

11.17

Commodities

–35.65

International

Stocks

31.78

Emerging

Markets

18.88

High Yield

6.97

U.S.

Large Cap

16.42

International

Stocks

22.78

U.S.

Small Cap

4.89

U.S.

Large Cap

–2.57

REITs

37.13

MLPs

16.67

MLPs

6.32

U.S.

Small Cap

18.37

U.S.

Aggregate

6.97

MLPs

–36.91

U.S.

Large Cap

28.43

Commodities

16.83

U.S.

Large Cap

1.50

U.S.

Small Cap

16.35

High Yield

8.23

MLPs

4.80

U.S.

Small Cap

–2.97

U.S.

Large Cap

29.89

U.S.

Large Cap

11.40

U.S.

Large Cap

6.27

U.S.

Large Cap

15.46

U.S.

Large Cap

5.77

U.S.

Large Cap

–37.60

REITs

27.99

U.S.

Large Cap

16.10

U.S.

Small Cap

–4.18

High Yield

15.39

REITs

2.47

High Yield

2.21

REITs

–6.52

High Yield

26.80

High Yield

11.10

U.S.

Small Cap

4.55

High Yield

11.56

High Yield

2.58

REITs

–37.73

U.S.

Small Cap

27.17

High Yield

14.74

International

Stocks

–12.14

MLPs

4.80

U.S.

Aggregate

–2.02

Emerging

Markets

–2.19

Commodities

–12.82

Commodities

23.93

Commodities

9.15

U.S.

Aggregate

2.43

U.S.

Aggregate

4.33

U.S.

Small Cap

–1.57

International

Stocks

–43.38

Commodities

18.91

International

Stocks

7.75

Commodities

–13.32

U.S.

Aggregate

4.21

Emerging

Markets

–2.60

International

Stocks

–4.90

Emerging

Markets

–12.85

U.S.

Aggregate

4.10

U.S.

Aggregate

4.34

High Yield

2.42

Commodities

2.07

REITs

–15.69

Emerging

Markets

–53.33

U.S.

Aggregate

5.93

U.S.

Aggregate

6.54

Emerging

Markets

–18.42

Commodities

–1.06

Commodities

–9.52

Commodities

–17.01

MLPs

–18.17

Source: FactSet, 8/31/15. High Yield is represented by the JPMorgan Domestic High Yield Index. U.S. Aggregate is represented by the Barclays Aggregate Bond Index. REITs are

represented by the FTSE NAREIT Equity REITs Index. MLPs are represented by the Alerian MLP Index. International Stocks are represented by the MSCI EAFE Index. EM is

represented by the MSCI EM Index. Commodities are represented by the Bloomberg Commodity Index. Small-Cap Stocks are represented by the total return for the Russell 2000

Index. Large-Cap Stocks are represented by the Russell 1000 Index. Index definitions can be found on Page 71. Diversification does not guarantee profit or protect against loss.

Past performance does not guarantee future results.

17

Countries Move In and Out of Favor

Sources: Morningstar, Dimon-Marsh-Staunton Global Indices. Study goes through 2010. The DMS Global and Country-Specific Indices measure the long-run performance of

stocks in 20 countries and three global regions around the world. Index definitions can be found on Page 71. Past performance does not guarantee future results.

1818

His

toric

al

Co

nte

xt

Historical ContextDebunking Mythsand Misperceptions

1919

“Our intuition about the future is linear. But the reality of technology is

exponential and that makes a profound difference. If I take 30 steps

linearly, I get to 30. If I take 30 steps exponentially, I get to a billion.”– Ray Kurzweil

Overpopulation,Demographics,and Energy

20

Overpopulation and Food Shortages?… Nope

Sources: United Nations and World Bank, as of 12/31/10.

21

Source: Bureau of Labor Statistics, Census Bureau, 2014.

How Are We Going to Handle All of Those

Baby Boomers?

20–39 59+ 40–59 20–39 59+ 40–59

59.0Million82.2

Million

85.3Million

Age in years Age in years

Perception RealityU.S. Population by Age

Top 10 Most Common Ages in the U.S.

23242021222526272829

#1

#10

22

Isn’t the U.S. Demographically Set to

Become the Next Japan?

Source: U.S. Census Bureau. Note: There are 19 permanent members of the G20.

23

Income and Unemployment Levels Reflect

Educational Attainment

Source: Brookings Institution and Federal Reserve Survey of Consumer Finances, June 2014.

24

Aren’t We in the Twilight of the American

Century?Answer: A. United States

Source: Ned Davis Research, 2013.

25

What About Peak Oil?

Source: BP Statistical Review of World Energy, 2014.

26

U.S. Energy Renaissance

1. Sources: U.S. Energy Information Administration, 2014, Bloomberg, New York Mercantile Exchange, 12/4/14.

2. Source: U.S. Department of Energy, 2013.

3. Sources: Bloomberg, New York Mercantile Exchange, 12/31/14.

27

U.S. Energy Consumption

Sources: U.S. Department of Energy, as of 12/31/11, and Census Bureau and U.S. Bureau of Economic Analysis, as of 12/31/13.

2828

“Where have you gone, Joe DiMaggio? A nation turns its lonely eyes to you.”– Simon & Garfunkel

The ImprovingHuman Condition

29

All Good Economies Evolve

Source: World Bank, 2013. For illustrative purposes only and not intended as investment advice. The placement of specific countries on the scale is based on the

percentage of economic activity coming from the agricultural, manufacturing and service sectors.

30

Global GDP Growth

Source: World Bank, as of 12/31/13.

31

The Big Story: Global Educated Middle Class

Sources: Middle Class Data: Brookings Institute, 2012, Population Data: World Bank: Health Nutrition and Population Statistics. Forecasts may not be achieved.

32

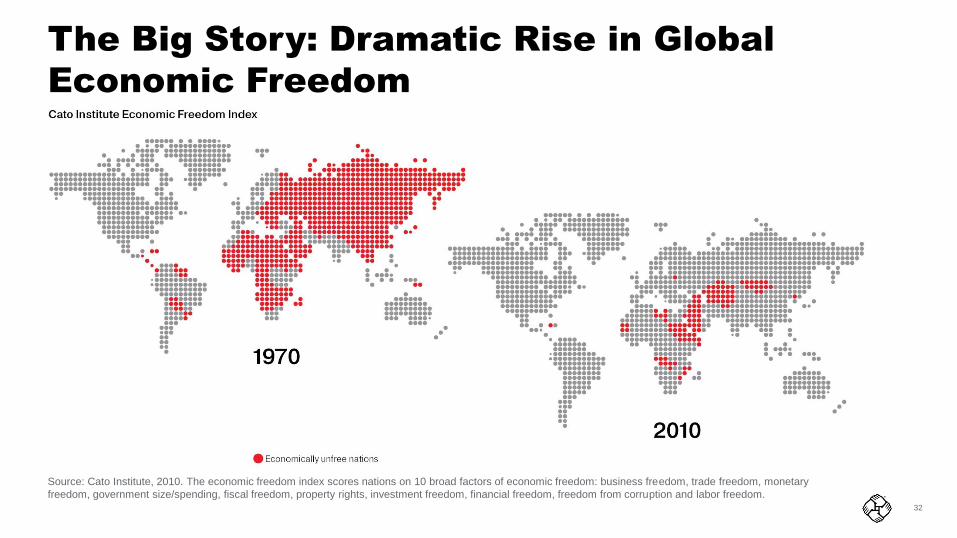

The Big Story: Dramatic Rise in Global

Economic Freedom

Source: Cato Institute, 2010. The economic freedom index scores nations on 10 broad factors of economic freedom: business freedom, trade freedom, monetary

freedom, government size/spending, fiscal freedom, property rights, investment freedom, financial freedom, freedom from corruption and labor freedom.

33

The Big Story: Dramatic Decrease in Global

Violence

Percentage of World Population that Was Killed in Specific World Events

Source: Statistics on Violent Conflict, 2014.

World War II(1939–1945)

3.7%

“The decline of violence may be the most significant and least appreciated

development in the history of our species.”—Steven Pinker, Psychologist, Harvard University

34

The Big Story: These Are the Good Old Days

Sources: Federal Reserve Bank of Boston, Statistical Abstract of the United States, International Labor Organization, United Nations, Bureau of Labor Statistics, as of

12/31/13. “Its Getting Better All The Time: 100 Greatest Trends of the Last 100 Years,” Stephen Moore & Julian L. Simon.

35

Our “Great Recession”....Like the Great

Depression?

Sources: Bureau of Labor Statistics, FDIC, Bureau of Economic Analysis, Bloomberg, and U.S. Federal Reserve, as of 12/31/14. For illustrative purposes only. Index

definitions can be found on Page 71. Past performance does not guarantee future results.

36

The Big Story: The American Dream Is Alive and Well

Source: United for a Fair Economy, 2011 and thomasjstanley.com

* 3% of the on deck individuals are undetermined.

37

U.S. Still a Manufacturing Powerhouse

Source: United Nations Industrial Development Organization, 2013. For illustrative purposes only and not intended as investment advice.

3838

“Americans always do the right thing but only after exhausting all other options.”— Winston Churchill

Hating theGovernmentIs Not anInvestmentStrategy

39

Gallup Poll Presidential Approval Ratings and Dow Jones Industrial Average Growth of $10,000

Approval Ratings and Markets Don’t Always

Move in the Same Direction

0

10

20

30

40

50

60

70

80

90%

Source: Gallup 12/31/14. The Presidential Approval ratings were introduced in the late 1930s to gauge public support for the President of the United States during the

term. For illustrative purposes only and not intended as investment advice. See Page 71 for index definitions. Past performance does not guarantee future results.

$100,000

$1,000,000

Log Scale

1961 1963 1969 1977 1981 1989 1993 2001 20091974 2014

Presidential Approval

RatingGain/

Annum% of Time

>65 2.4% 15.9%

50-65 6.8% 39.1%

36-50 11.8% 37.3%

<35 -13.8% 7.7%

40

Our Campaigns Have Never Been Filled with

Such Vitriol, Right?

For illustrative purposes only and not intended as investment advice.

41

But What About Debt and Deficits?

Source: Congressional Budget Office, 2014.

42

What About Those Trillions of Unfunded

Liabilities? The Reality of Social Security

Source: Congressional Budget Office Social Security Policy Options, July 2010.

4343

Cu

rren

tO

pp

ortu

nitie

s

CurrentOpportunities

44

45

Macro Insights

Deflationary Spiral Great Moderation 2.0 Expansion

Outcome:

• Broadly positive for bonds

• Extended period of low

equity returns

• Interest rates trend lower

Outcome:

• Stocks outperform bonds

• Interest rates low for long

• Growth and income scarce, investors pay up for it

Outcome:

• Stocks outperform bonds

• Cyclical sectors outperform

• Interest rates trend higher

Probability: Low Probability: High Probability: Low

Growth below trend,

disinflationary forces

Growth strong enough to support earnings but

not strong enough to raise inflation concerns

Secular growth forces prevail

ChineseConsumerism

EnergyRenaissance

Reform TechnologyRevolution

CrashingOil

PolicyMistake

FallingYuan

Trade

These views represent the opinions of OppenheimerFunds, Inc. and are not intended as investment advice or to predict or depict performance of any investment. These

views are as of the open of business on August 31, 2015, and are subject to change based on subsequent developments.

46

Global Contraction Extends the Cycle, Rather

than Curtailing It

Source: OFI Global Multi Asset Group Proprietary Leading Indicator and Organization for Economic Cooperation and Development (OECD), 8/31/15.

Past performance does not guarantee future results.

Output above trendOutput below trend

Acce

lera

tin

gD

ece

lera

ting

Recovery

Contraction

Expansion

Slowdown

Euro area

USChina Japan

Germany

France

UK

Brazil

Italy

Russia

India

Australia

Korea

Global

Indonesia

Poland

South Africa

Chile

49

47

And what do we know about bubbles?

Source: Strategas research partners 8/31/2015. Index definitions can be found on page 71. China is represented by the Shanghai SE Index. Oil is represented

by West Texas Intermediate Crude, Biotech is represented by the S&P Biotech index. Past performance does not guarantee future results.

Ind

ex b

ase

d to

10

0All indexes based to 100 at beginning of bubble period

0.0

100.0

200.0

300.0

400.0

500.0

600.0

1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Nikkei

China

Nasdaq

Oil

Biotech

China 2015

Nikkei

Nasdaq

China

Oil

Biotech

China

48

Fed in No Rush1

Composition of Fed (Based on member speeches/papers)

Global Central Banks in No Rush2

Consumer Price Index by Country and Central Bank Targets

“None of the... expansions… died of old age; every one

was murdered by the Federal Reserve” – Rudi Dornbush

1. U.S. Bank Asset Management Group analysis based on FOMC member speeches/papers

2. Source: Bloomberg, 8/31/15. Index definitions can be found on Page 71.

Dove Neutral Hawk

Yellen

Fischer

Tarullo

Dudley

Brainard

Powell

Evans Lacker

Lockhart

Williams

-0.1

0.1 0.2 0.20.3 0.3

1.3 1.5 1.6

-1.0

0.0

1.0

2.0

3.0

4.0

Y/Y

Perc

ent C

hange

Flag depicts Central Bank target

%

49

Most Likely Fed Path is Gradual

S&P 500 Index Around Start of Fed Tightening Cycles (Index based to 100 at beginning of rate hikes) Since 1946

Source: Ned Davis Research, 6/30/15. Index definitions can be found on Page 71. Past performance does not guarantee future results.

80

85

90

95

100

105

110

115Slow Tightening Cycles

Fast Tightening Cycles

Average

1-Year Returns

After 1st Rate Hike

10.78%

Pre-First Rate Hike Post-First Rate Hike

Fast

Tightening

Cycles

-2.67%

0

Time from Event

6 - Months 1 - Year-1 - Year -6 - Months

50

2.22%

3.70%3

6

9

12

15

1955 1958 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

10-Year U.S. Treasury Rate Nominal GDP (Real GDP + Consumer Price Index)

10-Year Treasury Rate and Nominal Gross Domestic Product (GDP) Y/Y Percent Change (10-Year Moving Average)

Interest Rates Likely to Stay Low for a

Long Time

Sources: U.S. Bureau of Economic Analysis and Bloomberg, as of 8/31/15. Nominal GDP is smoothed over 10 years, and as of 6/30/15. Forecasts may not be achieved. GDP (gross

domestic product) is the total value of all final goods and services produced in a country in a given year. Correlation expresses the strength of relationship between distribution of

returns of two sets of data. The correlation coefficient is always between +1 (perfect positive correlation) and –1 (perfect negative correlation). A perfect correlation occurs when the

two series being compared behave in exactly the same manner. Index definitions can be found on Page 71. Past performance does not guarantee future results.

Income Objective

Treasuries

Oversold

Correlation

0.90

Treasuries

Overbought

2014

51

350 bps

0 bps

500 bps

1,000 bps

1,500 bps

2000 2003 2006 2009 2012 2015

Senior Loans Spread Over LIBOR

A Conversation on Senior Loans

Source: Top Chart – Credit Suisse, 8/31/15. Left Chart – JPMorgan, 8/31/15. Right Chart – JPMorgan, 8/31/15. Senior loans are represented by the Credit Suisse

Leveraged Loan Index. High yield bonds are represented by the Barclays High Yield Bond Index. Index definitions can be found on Page 71. Past performance does

not guarantee future results.

Percent of New Loans Used for Refinancing

and Repricing

15 1625

42

52 50

3527

19 1911

45

35

5955

71

47

0

20

40

60

80

1998 2000 2002 2004 2006 2008 2010 2012 2014

Leveraged Loan and High Yield Bond

Maturity Schedule

0

50

100

150

200

250

2015 2016 2017 2018 2019 2020 2021 2022 2023

Senior Loans High Yield

Income Objective

Next 2 Years:

Only 3.8% of the

bond market matures

Only 0.7% of the

loan market matures

Num

ber

of M

atu

ring

Bonds a

nd L

oans

52

50

100

150

200

250%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Municipal / Treasury Yield Ratio Average

BBB-Rated Spreads Attractive

Municipal Bond Spread Ratios

Low Issuance

U.S. Municipal Bond Issuance

229 221 258 274208

261 280

146 145 161 14490

88 131 79 76109

8699

90156 111 126

111

4256 51

8073

6255

51

7561 65

53

359408 388

430390 409

434

287

376333 335

254

0

100

200

300

400

500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTDas of

8/31/15New Money Refunding Combined

A Conversation on Municipal Bonds

Sources of spread charts: FactSet, Bloomberg, Merrill Lynch, 8/31/15. AAA and BBB are represented by Merrill Lynch Municipal Indices which are derived from data points on the Merrill Lynch

Municipal AAA Yield to Worst and Merrill Lynch BBB Yield to Worst, respectively. The yield ratio indicates the relationship between the Merrill Lynch Municipal Master Index and the U.S. 10-Year

Treasury. Source of issuance chart: The Bond Buyer, 8/31/15.

Source of municipal default rate chart: Moody’s Investors Service. Data regarding default rates is from a study titled “U.S. Municipal Bond Defaults and Recoveries, 1970-2014,” dated. July

24,2015 The study is conducted annually and this is the latest data available. The above figures provide cumulative default rates for Moody’s-rated Corporate and Municipal debt rated Baa. For

example, obligations in the Baa Municipal category had a default rate of 0.01% within one year of the initial rating, 0.03% within two years, etc.

Performance is shown for illustrative purposes only and does not predict or depict the performance of any Oppenheimer fund. Index definitions can be found on Page 71.

Low Historical Default RatesDefault Rates, Average Cumulative Issuer-Weighted, Moody’s Rated Baa Only, 1970–2014

0

1

2

3

4

5%

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Baa Municipals Baa Corporates

Income Objective

100

150

200

250%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

BBB/AAA Yield Ratio Average

53

S&P 500 Index Minus 10-Year Treasury Yield

Stocks Trading Cheap to Bonds Globally

-8

-4

0

4

8%

1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

Source of chart data: Bloomberg, 8/31/15. The earnings yield is calculated as earnings divided by price. The earnings yield spread which is the difference between the

S&P 500 earnings yield and the 10-year U.S. Treasury yield and the spread between the earnings yield of the MSCI country specific indices and that country's 10-year

government bond yield. Index definitions can be found on Page 71.

Past performance does not guarantee future results.

Stocks cheap

to bonds

Bonds cheap

to stocks

Earnings Yields vs.

10-Year Government

Bond Yields

584 bps

450 bps

681 bps

529 bps

496 bps

363 bps

366 bps

Spre

ad (

%)

Growth Objective

380bps

54

Business Cycle: United States Valuations: U.S. and Developed Markets

0

5

10

15

20

25

SP500 MSCI EAFE

10 Yr Median P/E Current P/E

U.S. Economy Expanding, Valuations

Still Reasonable

Source: OFI Global Multi Asset Group Proprietary Leading Indicator and Organization for Economic Cooperation and Development (OECD) and Bloomberg, 8/31/15.

The charts are for illustrative purposes only and do not predict or depict the performance of any investment. Index definitions can be found on Page 71. Past

performance does not guarantee future results.

Current

P/E

Ratio

Growth Objective

Recovery Expansion

Contraction Slowdown

2 Years

Ago

55

Current

Business Cycle: Euro Area Valuations: U.S., Europe and Japan

Europe on the edge of a slowdown,

Japan recovering

Source: OFI Global Multi Asset Group Proprietary Leading Indicator and Organization for Economic Cooperation and Development (OECD) and Bloomberg, 8/31/15.

The charts are for illustrative purposes only and do not predict or depict the performance of any investment. Index definitions can be found on Page 71. Past

performance does not guarantee future results.P

/E R

atio

0

5

10

15

20

25

MSCI EuropeIndex

MSCI USA MSCI Japan Index

10-Year Median Current

Growth Objective

Business Cycle: Euro Area

RECOVERY EXPANSION

CONTRACTION SLOWDOWN

Current

2 Years

Ago

Business Cycle: Japan

RECOVERY EXPANSION

CONTRACTION SLOWDOWN

2 Years Ago

56

Valuations: U.S., Developed Markets and Emerging

Markets

0

5

10

15

20

25

S&P 500 Index MSCI EAFE Index MSCI EM Index

10 Yr Median P/E Current P/E

Emerging Markets in Recovery and

Valuations Are Favorable

Source: OFI Global Multi Asset Group Proprietary Leading Indicator and Organization for Economic Cooperation and Development (OECD) and Bloomberg, 8/31/15.

The charts are for illustrative purposes only and do not predict or depict the performance of any investment. Index definitions can be found on Page 71. Past

performance does not guarantee future results.P

/E R

atio

Growth Objective

Current

Business Cycle: China

RECOVERY EXPANSION

CONTRACTION SLOWDOWN

Current2 Years

Ago

RECOVERY EXPANSION

CONTRACTION SLOWDOWN

2 Years Ago

Business Cycle: India

57

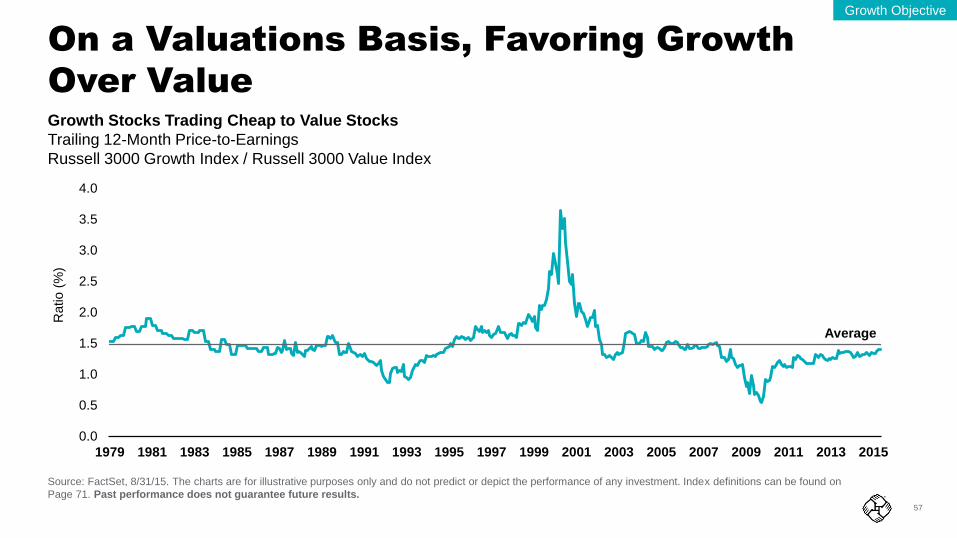

Growth Stocks Trading Cheap to Value Stocks

Trailing 12-Month Price-to-Earnings

Russell 3000 Growth Index / Russell 3000 Value Index

On a Valuations Basis, Favoring Growth

Over Value

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Ratio (

%)

Source: FactSet, 8/31/15. The charts are for illustrative purposes only and do not predict or depict the performance of any investment. Index definitions can be found on

Page 71. Past performance does not guarantee future results.

Growth Objective

Average

58

Growth Assets Historically Outperform in

Rising Rate Environments

Sources: Barclays Live, Credit Suisse, Alerian and Bloomberg, 12/31/14. The average 10-year Treasury rate over the past 20 years is 4%. “Low” is defined as below 4%. TIPS is represented by U.S. Generic Treasury Inflation

Protected Bond Securities. Core Bonds are represented by the Barclays Aggregate Bond Index. Gold is represented by the U.S. dollar spot price of one troy ounce. Commodities are represented by the Dow-Jones UBS

Commodity Index. Senior Loans are represented by the Credit Suisse Leveraged Loan Index. International Equities are represented by the MSCI EAFE Index. Emerging Market Equities are represented by the MSCI Emerging

Market Index. Large-Cap Stocks are represented by the Russell 1000 Index. Master Limited Partnerships are represented by the Alerian MLP Index. Small-Cap Stocks are represented by the Russell 2000 Index. Index

definitions can be found on Page 71. Past performance does not guarantee future results.

59

-0.23-0.08 -0.02

0.06 0.120.25 0.25 0.34

-0.50

0.00

0.50

U.S. DollarIndex

AlerianMLPIndex

CSLeveraged

LoanIndex

BloombergCommodity

Index

HFRIRelativeValue:Multi-

Strategy

FTSENAREITEquityREITIndex

Swiss ReCat Bond

Index

Gold

10 Yr Correlation with Barclays Aggregate Bond Index 10 Yr Correlation with S&P 500 Index

Correlations of Assets to Equities,

Fixed Income, and to Each Other

Sources: FactSet, 8/31/15. HFRI as of 7/31/15. Diversification does not guarantee profit or protect against loss. Correlation expresses the strength of relationship

between distribution of returns of two sets of data. The correlation coefficient is always between +1 (perfect positive correlation) and –1 (perfect negative correlation). A

perfect correlation occurs when the two series being compared behave in exactly the same manner. Index definitions can be found on Page 71. Past performance does

not guarantee future results.

-0.52

0.07 0.230.50 0.52 0.61 0.67 0.75

-1.0

0.0

1.0

U.S. DollarIndex

Gold Swiss ReCat Bond

Index

BloombergCommodity

Index

AlerianMasterLimited

PartnershipIndex

CSLeveragedLoan Index

HFRIRelative

Value: MultiStrategy

FTSENAREIT

Equity REITIndex

HFRI Relative

Value: Multi-

Strategy

Swiss Re Cat

Bond Index

CS Leveraged

Loan Index

Bloomberg

Commodity

Index Gold

FTSE NAREIT

Equity REIT

Index

U.S. Dollar

Index

Alerian MLP

Index

HFRI Relative Value: Multi-Strategy 1.00 0.40 0.83 0.58 0.21 0.49 -0.41 0.58Swiss Re Cat Bond Index 0.40 1.00 0.32 0.17 0.07 0.20 -0.16 0.18CS Leveraged Loan Index 0.83 0.32 1.00 0.43 0.03 0.54 -0.25 0.56Bloomberg Commodity Index 0.58 0.17 0.43 1.00 0.53 0.31 -0.67 0.45Gold - Continuous Contract 0.21 0.07 0.03 0.53 1.00 0.10 -0.42 0.00FTSE NAREIT Equity REIT Index 0.49 0.20 0.54 0.31 0.10 1.00 -0.38 0.33U.S. Dollar Index -0.41 -0.16 -0.25 -0.67 -0.42 -0.38 1.00 -0.28Alerian MLP Index 0.58 0.18 0.56 0.45 0.00 0.33 -0.28 1.00

60

Po

sitio

nin

gY

ou

r Pra

ctic

e

PositioningYour Practice

61

The Two Questions Everyone Wants an

Answer To

62

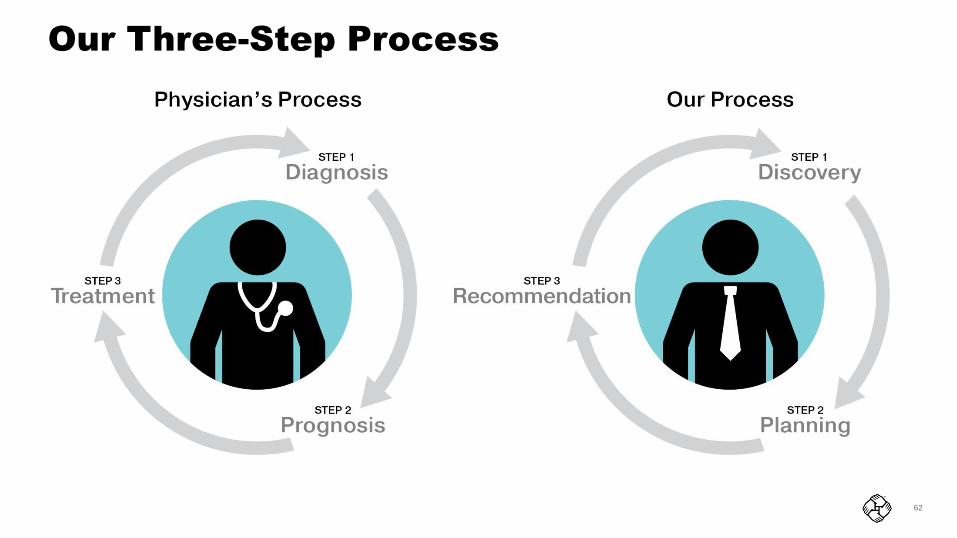

Our Three-Step Process

63

Why We Formed a Team

64

Contingency Planning: The Big Three

65

Index DefinitionsThe 10-Year U.S. Treasury Yield is generally considered to

be a barometer for long-term interest rates.

The Alerian MLP Index is a composite of the 50 most

prominent energy Master Limited Partnerships (MLPs).

The Barclays Aggregate Agencies Index, Agency Mortgage-

Backed Securities (MBS) Index and Commercial Mortgage-

backed Securities (CMBS) Index represent the U.S.

Government Related-Agencies, U.S. MBS and CMBS

components of the Barclays U.S. Aggregate Bond Index,

respectively.

The Barclays Aggregate Bond Index is an index of U.S.

Government and corporate bonds that includes reinvestment

of dividends.

The Barclays Aggregate Corporate Bond Index represents

primarily investment-grade corporate bonds within the

Barclays Aggregate Bond Index.

The Barclays Aggregate U.S. Treasuries Index represents

public obligations of the U.S. Treasury

with a remaining maturity of one year or more.

The Barclays High Yield Bond Index covers the universe of

fixed rate, non-investment- grade debt. The JPMorgan GBI-EM

Global Diversified Index tracks total returns for local-currency-

denominated money market instruments in the emerging

markets.

The Barclays Municipal Bond Index is a rules-based, market-

value-weighted index engineered for the long-term tax-exempt

bond market and includes bonds rated investment-grade by at

least two of the three major rating agencies (Moody’s, S&P

and Fitch).

The Bloomberg Commodity Index is comprised of commodities

traded on U.S. exchanges, with the exception of aluminum,

nickel and zinc, which trade on the London Metal Exchange.

The Citigroup Non-U.S. World Government Bond Index (USD

Unhedged) is comprised of foreign government bonds with

maturities over one year.

The Credit Suisse Leveraged Loan Index is a composite index

of senior loan returns representing an unleveraged investment

in senior loans that is broadly based across the spectrum of

senior bank loans and includes reinvestment of income (to

represent real assets).

Consumer Price Index (CPI) program produces monthly data

on changes in the prices paid by urban consumers for a

representative basket of goods and services.

The DMS Global Index, DMS Japan Index, DMS Spain Index,

DMS Australia Index, DMS Canada Index, DMS United Kingdom

Index, DMS United States Index, DMS France Index, DMS Europe

Index, DMS Italy Index, and DMS Germany Index represent equity

market performance in those countries or regions.

The Dow Jones Industrial Average is a price-weighted average of

30 blue-chip stocks that are generally the leaders in their industry.

The FTSE National Association of Real Estate Investment Trusts

(NAREIT) Equity REITs Index is an index consisting of certain

companies that own and operate income-producing real estate

that have 75% or more of their respective gross invested assets in

the equity or mortgage debt of commercial properties.

The Gold Spot price is quoted as U.S. dollar per troy ounce.

The HFRI RV (Hedge Fund Research, Inc. Relative Value) Multi-

Strategy Index employs an investment thesis predicated on

realization of a spread between related yield instruments in which

one or multiple components of the spread contains a fixed income,

derivative, equity, real estate, MLP or combination of these or

other instruments.

The JPMorgan Domestic High Yield Index tracks the investable

universe of domestic below-investment-grade bonds in the United

States.

The JPMorgan EMBI Global Diversified Bond Index is a uniquely

weighted version of the EMBI Global Index, which limits the

weights of those countries with larger debt stocks by only including

specified portions of these countries’ eligible current face amounts

of debt outstanding.

The MSCI EAFE Hedged to USD Index is 100% hedged to the

USD by selling each foreign currency forward at the one-month

forward weight.

The MSCI EAFE Index is designed to measure developed market

equity performance, excluding the U.S. and Canada.

The MSCI Emerging Markets (EM) Index is designed to measure

global emerging market equity performance.

The MSCI World Index is designed to measure global developed

market equity performance.

The Merrill Lynch AAA Municipal Indices measure the

performance of U.S. tax-exempt bonds rated AAA.

The Merrill Lynch BBB Municipal Bond Index is an index designed to

measure the performance of below-investment-grade municipal bonds.

BBB is the highest grade of rating by Moody’s that is considered below

investment grade.

The MSCI Italy, MSCI Germany, MSCI United Kingdom, MSCI

Canada, MSCI France, MSCI U.S., MSCI Thailand, MSCI Poland,

MSCI Mexico, MSCI Korea, MSCI Russia, MSCI Argentina and MSCI

Europe ex. U.K. represent equity market performance in those

countries or regions.

The Nikkei 225 Index components are among the most actively traded

issues on the TSE first section. The Index represents the performance

of first section stocks and the general market. Components have been

rebalanced from time to time to assure liquidity and representation of

Japan’s industrial structure.

SBBI U.S. Large Company Stock Index is an unmanaged index of

stocks of large U.S. companies.

SBBI U.S. Long-Term Government Bond Index is an unmanaged index

generally representative of the bond market.

SBBI U.S. Small Company Stock Index is an unmanaged index of

stocks of small U.S. companies.

SBBI U.S. (30-day) Treasury Bills is generally representative of the

rate of return on a savings investment.

Swiss Re Cat Bond Index is constructed to track the total return for

U.S. dollar- denominated catastrophe bonds.

The Russell 1000 Index measures the performance of large-

capitalization stocks.

The Russell 1000 Growth Index measures the performance of those

Russell 1000 companies with higher price-to-book ratios and higher

forecasted growth values.

The Russell 1000 Value Index measures the performance of those

Russell 1000 companies with lower price-to-book ratios and lower

forecasted growth values.

The Russell 2000 Index measures the performance of small-

capitalization stocks

The Russell 2000 Growth Index measures the performance of those

Russell 2000 companies with higher price-to-book ratios and higher

forecasted growth values.

The Russell 2000 Value Index measures the performance of

those Russell 2000 companies with lower price-to-book ratios

and lower forecasted growth values.

The Russell Midcap Index measures the performance of mid-

capitalization stocks.

The Russell Midcap Growth Index measures the performance of

those Russell Midcap companies with higher price-to-book ratios

and higher forecasted growth values.

The Russell Midcap Value Index measures the performance of

those Russell Midcap companies with lower price-to-book ratios

and lower forecasted growth values.

The S&P 500 Index is a market capitalization weighted index of

the 500 largest domestic U.S. stocks.

The S&P Biotechnology Select Industry Index is designed to

measure the performance of the Biotechnology GICS® sub-

industry. The Index comprises stocks in the S&P Total Market

Index that are classified in the GICS biotechnology sub-industry.

The Shanghai SSE Index is a domestic Chinese equity market

index where A shares in China are listed.

Shiller Home Price Index tracks changes in home prices

throughout the United States.

Treasury Inflation Protected Securities is generic U.S.

Government inflation-index bonds.

The U.S. existing home sales median price tracks changes in

residential property prices of existing single-family homes,

condos and co-op sales.

The West Texas Intermediate Crude price is the price of a barrel

of oil at the Cushing, Oklahoma-based distribution point for

almost all domestically produced oil in the United States.

Indices are unmanaged and cannot be

purchased directly by investors. Index

performance is shown for illustrative purposes

only and does not predict or depict the

performance of any investment. Past

performance does not guarantee future

results.