Company Report 2016 Outlook 2017 ENABLER - Schufa · Company Report 2016 _ Outlook 2017. 3 ......

42

ENABLER _ Company Report 2016 _ Outlook 2017

Transcript of Company Report 2016 Outlook 2017 ENABLER - Schufa · Company Report 2016 _ Outlook 2017. 3 ......

ENABLER _Company Report 2016 _ Outlook 2017E

NA

BL

ER

_

Co

mp

an

y R

ep

ort

20

16

_ O

utl

oo

k 2

017

3

WE CREATE TRUSTSCHUFA – “Schutzgemeinschaft für allgemeine Kreditsicherung” (General Credit Protection Agency) – is the leading credit bureau in Germany. For 90 years, we have been a reliable service partner, providing credit rating information to companies and private individuals. Handling around 380,000 enquiries every day, we support industry and consumers and help to ensure that business transactions can be completed safely, quickly and effi ciently. We protect companies against payment defaults, and consumers against possible excessive debt caused by consumer loans. In this manner, we help to build up relationships of trust – without which a market economy cannot operate.

3

DR MICHAEL FREYTAG HOLGER SEVERITT PETER VILLA

Dear Reader,

Digital change has long since caught up with the world of finance. Online banking and e-commerce have become common parts of our everyday consumer lives,

and we are more than happy to make use of these convenient options. But it is not only speed and complexity which have increased; so also has the level of anonymity in

business relationships and transactions. This makes the aspect of trust even more impor-tant, because trust forms the basis for all business relationships and lays the necessary

foundation for reliable interaction.

Ever since it was founded in 1927, SCHUFA has been a dependable partner for companies and consumers. For more than 90 years, it has played a decisive role in establishing a

basis of trust between business partners. In this manner, we contribute towards fast and straightforward business transactions. This is reflected in the high repayment level of

97.8 % for consumer loans.

The dynamics of digitisation have changed the role of consumers and their expectations of companies. For us, this change is primarily a huge opportunity: in future, we aim to

increase the level of quality and convenience in our work for businesses and consumers. In practice, this means expanding our digital products and services constantly not

least through innovative ideas which we combine with our classic portfolio of services.

At the same time, we are aware of our obligations to society. We are committed to sup-porting various social welfare projects. Our educational initiative “WirtschaftsWerkstatt” gives young people confidence and competence in handling their finances. The success of our company rests on the commitment of our employees, and on their input and ideas.

Our world may change – but trust has been and will always be the core value. And SCHUFA is particularly committed to contribute to this. Trust is future.

We wish you informative and inspiring reading!

e n a b l e r _Foreword by the Executive Board

4

SCHUFA is a contemporary information service provider for consumers and companies in

the digital world. But what are the actual points of contact? An overview.

DIGITAL PRESENCE

P.6

Young FinTechs and classic financial service providers can learn a lot from each other. Two experts

explain the benefits of collaboration.

START-UP MEETS TRADITION

P.14

How does digitisation change the world of finance? This was the subject of discussion between SCHUFA

chairman of the board Dr Michael Freytag and André M. Bajorat, CEO of the FinTech company figo.

VISIONARY CHANGE

P.8

Ever since the company was founded in 1927, SCHUFA has been a cornerstone of the German credit

system. Our timeline shows what has happened over the last 90 years, and the developments which have

contributed to the advancement of the company.

MILESTONES FROM 90 YEARS

OF SCHUFAP.20

e n a b l e r _Contents

5

More at WWW.SCHUFA-WEGBEREITER.DE

97.8 %

Blogger: Maike Matzen

Frankfurt, Germany blogging since 2011www.ekiem.de

#beauty #lifestyle #travel #fashion

Message

To date, the WirtschaftsWerkstatt educational initiative has reached more than five million young people – a huge success

which was celebrated with a Youth Summit.

A BIRTHDAY SUMMIT

P.28

Digitisation has changed the role of consumers and their expectations

of companies. Consumers are no longer merely consumers; they are also

increasingly becoming producers.

CONSUMERS 4.0P.22

SCHUFA facts and figures – a concise overview

of the last business year.

THE FACTSP.38

Thinking outside the box and acting astutely – we turn the spotlight on four SCHUFA employees who are

each a source of inspiration in their respective field of work. Whether technological development, occupational

health management or corporate strategy.

TRENDSETTERSP.32

How can SCHUFA shape digital change in the economy and create trust at the same

time? Our associate Dr Michael-Burkhard Piorkowsky, chairman of the Consumer Advisory

Board, tenders an answer.

ASSOCIATEP.40

e n a b l e r _Contents

6

SCHUFA COMPANY REPORT

If you build a house or enter into a long-term business relationship with somebody, you need to be able

to assess the risk realistically. Using SCHUFA company reports, consumers can see who they are dealing

with before they commit themselves. The informa-tion included in a company report gives you

an objective description of your potential business partner, providing you with a

valuable basis on which to make your decision.

BUYING ON ACCOUNT AND PAYING BY INSTALMENTS

Whether it is a television or household furniture, many purchases today are made online. Via digital interfaces, SCHUFA provides suppliers with credit information on shoppers so that

the supplier can then provide the goods in advance and negotiate payment

terms with the customers online.

DIGITAL PRESENCE

SCHUFA is a contemporary information service provider for consumers and companies

in the digital world. But what are the actual points of contact? An overview.

6

e n a b l e r _

Digital Presence

7

OVERVIEW OF SCHUFA DATA

To provide transparency, SCHUFA offers consumers the opportu-nity to view the personal information stored by SCHUFA concern-

ing themselves on the Internet platform meineSCHUFA.de. All meineSCHUFA packages also include an update service. This notifies the consumer via email or text message every time a

credit report is made or changes are made to their credit score or identity, which in turn gives the consumer more

control and better protection against identity theft. If consumers wish to ask questions or add in-

formation to their SCHUFA details, they can do so online.

SCHUFA CREDIT REPORTS

By requesting a SCHUFA credit report, consumers receive conclusive evidence of their creditworthiness. This helps

to create a foundation of trust between themselves and their proposed business partner (e. g. land-lord). Credit reports also contain information

for personal use. They provide a compre-hensive overview of your personal

data stored by SCHUFA.

ONLINE LOAN

When buying a car or just about any other product, consumers today can negotiate

a loan quickly and easily online. One key element for minimising risk is a

SCHUFA credit report on the prospec-tive borrower, which lenders can

request in real time.

SCHUFA-FRAUDPOOL

With its FraudPool, SCHUFA has created a database which supports credit institutes and finance service providers by enabling them to share information on attempted

frauds in a manner which complies with data protection law, thus enabling them to protect themselves against

fraud and the consequences of fraud. Private individuals who have fallen victim to identity

fraud can also register free of charge with SCHUFA to minimise the risk of

repeat offences.

7

e n a b l e r _

Digital Presence

88

How does digitisation change the world of finance? What are the challenges and opportunities?

And how important are trust and responsibility, now and in the future? These questions were discussed

by SCHUFA chairman of the board Dr Michael Freytag and André M. Bajorat, CEO of the FinTech company figo.

photography_ Matthias Haslauer

VISIONARY CHANGE

e n a b l e r _

Visionary Change

99

e n a b l e r _

Visionary Change

10

Dr Freytag, digitisation affects and changes virtually all areas of our lives. How noticeable is this change in the world of finance?

dr michael freytag_ Radical change has long since become a reality in new, widely varying forms of digital communication, in online banking, in e-commerce and in the Internet of Things. There has been an enormous increase in the speed, complexity and anonymity of business relationships and transactions. Frequently, there is a greater physical distance between custom-ers and companies, and there is often no direct personal contact. In such situations, the trust factor is more important than ever.

What exactly do you mean?

dr michael freytag_ Trading and loaning – whether analogue or digital – are inconceivable without trust. For 90 years, SCHUFA has been creating a basis for such trust by providing credit-relevant information on private individuals and compa-nies. We have data on more than 67.2 million natural persons and 5.3 million companies. The demand is high, and it is increasing: every day, we receive 380,000 enquiries for credit reports. SCHUFA supports safe, efficient business deals. And it does so successfully: 97.8 % of all consumer loans are repaid as planned!

andré m. bajorat_ Trust is most definitely an extremely valuable asset in the digital world. When it comes to authorising and authenticating payments, you need to generate trust every single time, and you need to do so at a speed and in quanti -ties which would have defied imagination just a few years ago. Actually, I think the world of finance has always been a driving force for digitisation. Today we see a new quality in this develop-ment, because players outside of the established world of finance are providing fresh ideas and additional momentum.

Does the relationship between established players and new players incline to the competitive or the cooperative?

andré m. bajorat_ Naturally, there is competition, but I think that dialogue between FinTech companies and traditional financiers has increased considerably over the last two years. Both sides have accepted that they can learn a lot from each other to improve processes and products for the benefit of customers. There are lots of overlapping areas; you just have to find them, check them out and verify them. That’s how to make consistent, successful products.

dr michael freytag_ We are constantly developing new products and services. Our Innovation Lab works specifically to develop effective search algorithms, particularly for fraud prevention processes. FinTechs have brought new ideas and new momentum into the world of finance. They inspire us to re-think things and develop new business models. Conversely, even the most recent players in the financial sector benefit from cooperating with SCHUFA, which can fall back on expertise that has matured over the decades.

of classic service providers and banks in Germany buy

successful FinTechs, 47 % enter into partnerships with them.

Source: Statista-Expertenbefragung, 2016

10 %

e n a b l e r _

Visionary Change

11

» Data protection and data quality, in particular the sensitive handling of personal details, takes absolute priority at SCHUFA.« dr michael freytag, SCHUFA chairman of the board

andré m. bajorat

is CEO of figo GmbH, a company based in Hamburg, which programmes so-called APIs (application programming interfaces) to read financial data. This enables third parties to integrate banking services in their products. Bajorat has been working as an entrepreneur, consultant, speaker, business angel and mentor in the German start-up and FinTech world since 1996. His blog paymentand-banking.com looks at banking, payment and mobile themes. Since March 2016, he has been representing the interests of FinTechs as a member of the Bitcom Executive Board.

dr michael freytag is chairman of the board for SCHUFA Holding AG and vice president of the Association of Consumer Credit Infor-mation Suppliers (ACCIS). He worked for ten years as a corporate and invest-ment banker for Deutsche Bank, was a senator of the Free Hanseatic City of Hamburg and a member of the Bundesrat for the Federal Republic of Germany.

e n a b l e r _

Visionary Change

12

» The world of finance has always been a driving force for digitisation. Today we see a new quality in this development.«

andré m. bajorat, CEO figo GmbH

e n a b l e r _

Visionary Change

13

One of the great challenges in the field of digitisation is data protection. What approach do you take here?

dr michael freytag_ Data protection and data quality, in particular the sensitive handling of personal details, takes absolute priority at SCHUFA. Our business activities are regulat-ed by the German Federal Data Protection Act – one of the most stringent data protection acts in the world. We also control the quality of our data extremely meticulously, and continually secure and improve it. In an age of digitisation, it is more impor - tant than ever to handle data responsibly, fairly and in a manner which is transparent for consumers. We store our data on servers in Germany. In order to check creditworthiness, we never use data from social networks, because we have consciously decided to respect consumers’ privacy. And anyway, we already have the data which is actually relevant for credit reports. This plays an important role in winning the trust of partners and custom-ers, and continuing to earn such trust on an ongoing basis.

andré m. bajorat_ I can only agree. figo also continually optimises its internal organisation and its internal security and compliance standards so that we can be a reliable service provider to our business partners and offer maximum protec-tion for the data of their users in the digital world. Digital identity is becoming increasingly relevant, so the question of how and by whom my personal details are being used is also growing in importance. Ultimately, it is all about transparency. Personal data management and personal data rights will become increasingly important in day-to-day life.

dr michael freytag_ I totally agree. In particular, identity protection and fraud prevention are becoming increasingly significant, and will play a decisive role in business success. With our data expertise, we are able to offer comprehensive services in this area. Every 30 seconds, an identity is stolen digitally in Germany, and frequently used to place manipulated orders online. With our SCHUFA-FraudPool, we have created a database which supports credit institutes and finance service providers by enabling them to share information on attempted frauds in a manner which complies with data protection law, thus enabling them to protect themselves against fraud and the consequences of fraud. We also offer private customers an update service to notify them of any recent credit enquiries made to SCHUFA so that they can see whether their name has perhaps been used by fraudsters. Companies and consumers both benefit from this service. SCHUFA has been creating trust – since 1927. And: trust is future.

André M. Bajorat and Dr Michael Freytag met each other in the Barlach Halle K in Hamburg. This exhibition hall is located in the heart of the city, between the Art Society and the Museum Mile.

FinTechs with active business operations FinTechs which were not active before

2016 or which have already ceased business operations

Source: FinTech Markt in Deutschland (FinTech Market in Germany),

Professor Dr Gregor Dorfleitner, Junior Professor Dr Lars Hornuf, 2016,

study commissioned by the Federal Ministry of Finance

87

346

433FINTECHS IN

GERMANY

e n a b l e r _

Visionary Change

14

#N26N26 promotes itself with its claim to set new stan- dards for user experiences in the field of mobile banking. An account can be opened with zero paperwork, and takes fewer than eight minutes to complete. The compa-ny is a fully-fledged bank with real-time overdrafts, international bank transfers in 19 currencies, investment products and real-time loans of up to €25,000. N26 is working on replicating all the aspects of a traditional brick-and-mortar bank, but in digitalised form. #Location: Berlin, 2013

#CEO: Valentin Stalf

#Customers: 300,000 in 17 countries

#Transaction volume: 3 billion euros since the launch in 2015

#Employees: 200

(Date: 15 March 2017)

WWW.N26.COM

14

e n a b l e r _

Start-up Meets Tradition

15

Competitor or partner? Young FinTechs and classic financial service providers

can learn a lot from each other. Two experts explain the benefits of collaboration.

photography_ REUTERS/Axel Schmidt, FinTech Group AG, N26 GmbH, Robert Gross

START-UP MEETS

TRADITION

15

e n a b l e r _

Start-up Meets Tradition

16

Stephan Simmang worked in an invest-ment bank for two decades before becoming CTO for the FinTech Group.

Digitisation has taken the world of finance by storm. FinTech companies reconsider processes from completely new pers - pectives. They take promising ideas to create genuine innova-tions – and in doing so, they challenge the status quo of con- ventional business models. Established players, on the other hand, have the necessary resources, a large customer base, and trust – trust they have worked extremely hard to earn over the years. For this reason, both the established players and the newcomers to the industry have recognised the potential of collaborating. In November 2016, the statistic web portal Statista asked 110 experts from FinTechs, banks and other finance service providers how classic finance service providers predominantly react to German FinTechs: nearly half of all the companies interviewed would like to enter into a partnership.

Digitisation is the driving force for the industry “We are in a phase where digitisation is establishing itself, and not everyone is up-to-date. In some cases, antiquated methods are still being used,” reports Stephan Simmang, CTO of the FinTech Group. Since it was founded in 1999, the company has become one of the leading providers of innova-tive technology in the financial sector. Simmang is a strong proponent for collaboration between established companies and young entrepreneurs: “Start-ups bring the necessary spirit and show the industry that there are cleverer approaches to many processes – naturally, always within a certain frame-work.”

#FinTech Group A G The FinTech Group sees itself as a modern smart bank, and offers innovative technology for the financial sector. In the B2C area, it targets more than 200,000 private customers; in the field of B2B, it is partner to numerous banks which work internationally. Via a banking platform, it provides services from the areas of online banking, payments and brokerage.

#Location: Frankfurt, 1999

#CEO: Frank Niehage

#Customers: 212,040

#Assets under management: 10.9 billion euros

#Employees: 448

(Date: April 2017)

WWW.FINTECHGROUP.COM

e n a b l e r _

Start-up Meets Tradition

17

Valentin Stalf, founder and CEO of N26, would be the last to disagree. N26, a mobile bank, was established four years ago, and has grown from a FinTech start-up into a licensed, full-service bank. Stalf explains the success by claiming that well-known banks in the industry have frequently failed to prioritise digitisation. With its completely digital DNA, the N26 bank has been able to set completely new standards: “We selected a sector in which customers were prepared to use new services in a different form – and we re-invented banking products.” With regard to collaboration, much has happened over the last two years, but Stalf still sees a great deal of potential. “Only a few FinTechs in Germany collaborate with traditional players on a large scale and work together to increase coverage.”

Work cultures are highly differentFor both sides, the challenge is to deal with the different resources and work cultures of the potential partner – work cultures which could hardly be more different. “Traditional banks have a large customer base, which is attractive to new, young companies. But they often do not implement good ideas as fast as the start-ups need them to. New companies often do not have the resources to work on something for years without knowing whether or not they’ll end up with a successful product,” says Stalf. Simmang sees the same challenges, so recommends a cautious and thus more sustain-able approach: “New entrepreneurs often have to get used to working together with large and somewhat rigid organi-sations. When a start-up meets an established player, it can be an eye-opening experience for both sides.”

According to Simmang, this is why some established companies prefer to implement successive internal solutions: “Over the last eighteen months, many large companies have formed agile units to implement this agility internally throughout the company. It has become a focus because people have seen that it actually helps. But transitions like these can be very painful for larger companies.”

From a start-up in a living room in Vienna to a licensed full-service bank: the founders of N26, Valentin Stalf (CEO, left) and Maximilian Tayenthal (CFO).

New standards for bank services thanks to digital DNA: the reception hall of N26 in Berlin.

e n a b l e r _

Start-up Meets Tradition

18

The focus must always be on the customerThe fact that collaboration can be extremely meaningful – provided it generates benefits for both sides – is a given for both Stalf and Simmang. And in some areas, there is no alternative to a partnership – particularly from the point of view of the start-up. This is the case, for example, where processes which require large, well-established databases are involved, as in credit scoring or risk management.

N26 also generates added value in some areas by entering into partnerships, and not solely via innovations it has devel-oped itself. “You have to focus totally on the customer. We aim to always make the best products available. Regardless of whether the solution is one we have developed ourselves, or whether it comes from a traditional company or an innova-tive FinTech, if it increases the value, we want to offer it to our customers – naturally via our own platform,” Stalk explains. The FinTech Group always has an eye on all the market players. In Simmang’s experience, it is often the very young start-ups that have “fantastic ideas” and need a partner to help make them reality. So it is a case of tapping into these.

Trust forms the basisRegardless of whether it is about the relationship between the customer and the service provider, or a partnership between different service providers, there always has to be a founda-tion of trust. “Trust is very important for our customers. We are a bank. It is all about money, and where money is involved, you need trust,” says N26 founder Stalf, summarising the situation. “For a digital product, you can establish trust quickly and easily via app store ratings or via social media. But at the end of the day, the key to winning customers’ trust always lies in the quality of the product.”

The FinTech Group also places trust at the beginning of any business relationship. “How stable is your system, to what extent can I rely on it?” This is the first question potential customers ask us. We use our systems ourselves, so it is easy to prove that they are stable,” responds Simmang. The importance of a strong IT infrastructure became very evident in 2016. The FinTech Group is particularly involved in securities settlement, and operates one of the biggest online brokerages in Germany together with flatex. Due to the surprising results of the Brexit vote and the elections in the USA, the number of orders rose sharply within a very short space of time. “The IT systems functioned perfectly, and were completing more than 80,000 trades per day – three times more than average,” Simmang says. It was a record in the company’s ten-year history. “Had the IT malfunctioned, customers in the fast-paced money market would have lost control over their investments.” Stephan Simmang’s conclusion: “Trust forms the basis for all business – and more so in the world of finance than ever before. If ever you lose credibility, you’ll really struggle on the market.”

“Start-ups show the industry that there are cleverer ways of doing many things.” Normal working day at the FinTech Group in Frankfurt.

» Re-thinking and perfecting established processes on an ongoing basis is our daily business. SCHUFA thinks along the same lines as a start-up – a start-up with 90 years of experience.«peter villa, member of the executive board of SCHUFA

e n a b l e r _

Start-up Meets Tradition

19

FINTECHS

Globally in motion: facts and figures for the highly dynamic FinTech industry

87 % OF ALL THE BANKS INTERVIEWED

IN GERMANY CURRENTLY COLLABORATE WITH

FINTECH COMPANIES, AND SEEK TO

ENTER INTO A JOINT HOLDING OR FURTHER

COLLABORATION IN THE FUTURE.Source: FinTech Markt in Deutschland (FinTech Market in Germany), Professor Dr Gregor Dorfleitner, Junior

Professor Dr Lars Hornuf, 2016, study commissioned by the Federal Ministry of Finance

THE CLASSIC FINANCIAL SERVICE PROVIDERS

AND BANKS IN GERMANY DEVELOP THEIR OWN

PRODUCTS TO COMPETE AGAINST FINTECHS.

Source: Statista-Expertenbefragung 2016

27VOLUME OF INVESTMENT IN FINTECH

START-UPS IN GERMANY BETWEEN 2012 AND

2015, IN MILLION EUROS.

Source: Statista 2017, Barkow Consulting

64

2013

153

2014

276

20152012

36

3.4 billion

978,821 MILLION EUROSCHINA

923,890 MILLION EUROS

USA

103,618 MILLION EUROS

GERMANY

171,868 MILLION EUROS

UK

130,724 MILLION EUROSJAPAN

Yes

No

POTENTIAL USERS THE GLOBAL FINTECH

MARKET WILL HAVE IN 2020.

Source: Statista 2017, Digital Market Outlook

VOLUME OF TRANSACTIONS IN THE FIVE TOP COUNTRIES

FOR THE FINTECH MARKET IN 2017.

Source: Statista 2017, Digital Market Outlook

e n a b l e r _

Start-up Meets Tradition

20

1996 INTRODUCTION OF SCORING SERVICES

At the start of the 1990s, experts at SCHUFA began developing scores –

reliable forecasts to determine payment probability. In 1996, the first scores were offered for bank

loans. This provides banks with an objective, statistics-based

forecasting procedure.

1952 THE FEDERAL SCHUFA E.V. (REGISTERED SOCIETY) IS FOUNDED

In order to provide a database which was as comprehensible as possible, the various SCHUFA associations joined to form a federal society. The head-quarters were originally located in Hanover, but moved to Wiesbaden in 1957.

1972 THE DAWN OF DIGITISATION

On 17 July 1972, the first computer-supported SCHUFA credit report was conducted.

Contract partners were now able to send their enquiries to the

SCHUFA computer directly via ticker, where they were then processed automatically. The

technology was revolutionary for its time.

1983 THE END OF INDEX CARDS

The last index card was electronically processed –

and SCHUFA equipped for new market develop-

ments, such as the dawn of the mobile phone era, or the increasingly wide-

spread use of credit cards.

SCHUFA IS FOUNDED

The Berliner Elektrizitätswerke (Berlin Electricity Works – BEWAG) founded SCHUFA to optimise pay-ment by instalments when selling electrical devices. Managing Direc- tor: Dr Kurt Meyer. The abbrevitation SCHUFA stands for Schutzgemein-schaft für Absatzfinanzierung und Kreditsicherung (General Credit Protection Agency).

THE 1930s EXPANSION

The SCHUFA idea quickly spread from Berlin throughout Germany: in 1930, a SCHUFA bureau was founded in Dortmund, the first association outside of Berlin. Soon after, associations were established in other cities.

CO

MPA

NY

HIS

TO

RY

PR

OD

UC

T H

IGH

LIG

HT

S

1960 1970 1980 199019301920 1940

1990THE EAST GERMAN

SCHUFA IS FOUNDED

Right at the start of the economic, monetary and

social union, SCHUFA was able to provide a functional credit report service for citizens of the former GDR so that they

could complete business trans-actions quickly and easily.

2005 ONLINE ACCESS TO

PERSONAL DATA

With its new consumer web portal, meineSCHUFA.de,

private individuals can now view their personal details

online. This enables them to see 24/7 which companies

have made credit reports or added relevant information.

19501927

THE 1930s GROWTH

The SCHUFA bureau in Berlin worked with 14 telephone lines, 4 tickers and 2.6 million index cards.

MILESTONES FROM 90 YEARS OF SCHUFA Join us on a journey through time and take a look at the interesting milestones in our company history. MORE AT WWW.SCHUFA.DE/90JAHRE

1926THE IDEA

An employee of the Berliner Elek-trizitätswerke (Berlin Electricity Works – BEWAG), Dr Walter Meyer, and his brother, Dr Kurt Meyer, had the idea of centrally collecting information on the payment be-haviour of all consumers who took out loans to purchase products.

e n a b l e r _

Milestones

20

21

90 YEARS OF SCHUFA

2017 2010FUTURE

2010START OF THE

OMBUDSMAN PROCESS

The SCHUFA is the only credit bureau in Germany to

offer a neutral arbitration process for consumers –

swift, free of charge, and with minimum bureaucracy.

2008THE CONSUMER ADVISORY

BOARD IS FOUNDED

With its Consumer Advisory Board, SCHUFA created

a forum in which consumer issues could be brought into

SCHUFA from outside, and discussed in a general and independent manner. The

board consists of experienced professionals from political,

academic, industrial and social backgrounds.

2000 THE SCHUFA HOLDING AG IS FOUNDED

Numerous independent SCHUFA associations joined forces to create a flexible, market-based company.

2014 WORK/LIFE BALANCE

As an employer, SCHUFA seeks to ensure its employees can enjoy a

healthy work life balance. In 2014, the company was awarded the “berufundfamilie” (career and

family) certificate for its family- conscious work policies. The company is aiming to further

improve its HR strategy in this respect in the future.

2014 COMPREHENSIVE FRAUD PREVENTION SOLUTIONS

With the introduction of the SCHUFA-FraudPool, SCHUFA created a new approach which enables banks to share informa-tion on suspected fraud, but within the boundar- ies of data protection law. This helps to protect banks, consumers and the economy from suffering damage.

NEW COMPREHENSIVE PROTECTION FOR PRIVATE INDIVIDUALS

MeineSCHUFA Packages are available for private in-dividuals which include SCHUFA services tailored to their personal needs. Besides 24/7 transparency via online access to their SCHUFA data, these pack-ages also include an update service which pro-vides protection against identity fraud – Customers receive a text message or email whenever enqui-ries or changes are made to their personal details.

2016 NEW SERVICE TO PROTECT VICTIMS OF IDENTITY FRAUD

SCHUFA offers victims of identity fraud a free consumer service which enables them to better protect themselves against further fraud.

DIGITISATION OF CREDIT ENQUIRIES

By further expanding its B2B business, SCHUFA concentrates on growth in the field of full-service credit bureau. Its wide range of credit report ser-vices on 5.3 million com-panies marks another milestone in implementing the B2B strategy. For the first time, SCHUFA now offers customers in the mail order industry real- time credit reports for effective risk management and speedy buying pro-cesses.

RAPID GROWTH OF PRIVATE CUSTOMER PRODUCTS

Within five years, the num-ber of private customers using SCHUFA doubled to total 2 million. 10 million people visited the meine-SCHUFA.de web portal; more than 95 % of the population have heard of SCHUFA.

FAST AND COMPETENT SUPPORT FOR CONSUMERS

The SCHUFA private cus-tomer service centre pro-cesses around 1.2 million phone calls from consum-ers. 97 % of their ques-tions can be answered im-mediately. According to surveys, the level of cus-tomer satisfaction with SCHUFA is consistently high.

2013 THE “WIRTSCHAFTSWERKSTATT” EDUCATIONAL INITIATIVE IS FOUNDED

This initiative is geared towards teenagers and young adults, and provides information on economic and financial topics. The main focus in the workshops is on han-dling personal finances and data in a responsible manner.

2010 EXPANSION OF B2B BUSINESS

The new SCHUFA concise checks provide companies with summarised information on the creditworthiness of customers, interested persons or business partners. This means they can get a general idea of creditworthiness, business risk and default risk.

2011 POS PRESENCE

SCHUFA comes to the con-sumer: from this point on, credit reports can be con-ducted from customer desks in banks, and they will soon also be available online.

2012 IMPROVED PROTECTION AGAINST IDENTITY FRAUD

With SCHUFA IdentSafe, SCHUFA checks to see wheth-er the personal de-tails of private indi-viduals have been published unlawfully on the Internet. If SCHUFA suspects identity fraud, it in-forms the customer immediately and provides support.

2016 AWARD-WINNING

COMPLIANCE MANAGEMENT

SCHUFA handles the subject of compliance

is a responsible and systematic manner.

In 2016, the company’s compliance management

was successfully tested and awarded TÜV

certification.

2000

e n a b l e r _

Milestones

21

22

Consumers

4.0 Digitisation has changed the role of

the consumer to the core. In an interview, trend researcher and communication

expert Andreas Steinle talks about modern consumers, who are increasingly creating

their own worlds.

e n a b l e r _

Consumers 4.0

23

Blogger: Marcel Gorgolewski and Tobias Meyerblogging since 2013 www.homeiswhereyour-bagis.com

#travel #SoutheastAsia

17,398

10,222

39,747

153,300

4

Message

Instagram followers

Facebook followers

Twitter followers

Visits per month

Posts per month

Digital travel tips

We started our blog in 2013 as a hobby, but today it is the best job in the world. Thanks to digitisation, travellers are in a better position to find information via blogs and review sites. They receive current and authentic field reports on travel destinations, activities and accommodation. The diversity of this information and the speed at which it is accessed would be inconceivable without the Internet. Nowadays, bloggers like us play a very special role. We not only write articles in their blogs, we also write e-books. Alongside affiliate marketing and paid collaborations with hotels and destinations, these are our main sources of income.

23

e n a b l e r _

Consumers 4.0

24

Beauty blogI started my blog as a sort of diary. The first time a cosmetics company contacted me for a paid contribu-tion, I was surprised. But now it is my daily bread and butter. Many companies have realised that authen- tic reviews are more effective than classic advertising. Not only am I paid to write articles, but I am also sup- plied with products for articles. The reactions of my readers vary widely. On the subject of beauty, there are often heated discussions – because taste is a very subjective thing.

Blogger: Maike Matzen

blogging since 2011www.ekiem.de

#beauty #lifestyle #travel #fashion

4,057

2,276

1,068

33,480

8

Message

Instagram followers

Facebook followers

Twitter followers

Visits per month

Posts per month

e n a b l e r _

Consumers 4.0

25

Has the role of the consumer changed,

Mr Steinle?

Those who visit the Frankfurt office of the Zukunftsinstitut Workshop GmbH (Future Institute Workshop) are met with inspiring diversity. The world of the co-founder and communi-cation expert Andreas Steinle is colourful and surprising: a bicycle is parked in the conference room; imaginative hand- crafted flowers are bunched in a vase; on privacy screens, there are cards displaying the latest product ideas from various industries. For those who have sudden inspiration, there are paper and pens on the table so you can jot it down. And in the middle, there is a bottle of shower gel. Mint & bergamot. More on that topic later…

The customer is king – is this still true in the 21st century?

More than ever. The customer is increasingly taking centre stage, because we know more about him or her, and products can be tailored accordingly. Not least thanks to the digital assistants that are slowly taking over in the home. Just think about the Echo loudspeakers from Amazon. The integrated Alexa Voice Service is an intelligent system that not only wakes you up in the morning and gives you a weather forecast, but also successively learns about the user’s preferences, and adjusts accordingly.

Has this led to a change in consumer expectations?

Definitely. Digitisation has made an enormous change to the role of the consumer. Customers have gotten used to having their needs met quickly. In other words, products and services have to be instantly available. This explains the success of streaming services such as Netflix or Amazon Prime. People no longer want to wait until a film is being shown in the cinema, or the DVD comes to the shops. The next stage will be personalised films, which are tailored to the consumer’s individual preferences. Because streaming gives providers real- time insights into consumer behaviour. True, it has not hap- pened yet, but it is a theoretical possibility that the consumer’s brain activity and physical reactions could be analysed – is he or she particularly interested in action scenes or love scenes? The stream would then select an appropriate version from a pool of pre-produced film versions.

In this vision of the future, the consumer is highly transparent. In an age of increasing digitisation, what challenges do you think there will be with regard to data protection and consumer protection?

These are important questions, because all opportunities include risk. Companies know an incredible amount, and, naturally, knowledge can be exploited for manipulative purpos-es. Consumers need to know that they leave traces on the Internet; that they are not merely consumers, but also data suppliers. However, we are not helpless in the face of digi- tisation. Often we only discuss the problems involved in change, and forget the advantages it has brought: individual lifestyles, the opportunity to work independently and so much more. People need a deeper understanding of digitisation, data protection and programming – these should be compulsory subjects in schools. This is where the government needs to get involved. The future is whatever we make it.

Talking of “doing”. One of the results of digitisation is that numerous private individuals are suddenly starting to act as “suppliers”. They use eBay to sell unwanted belongings, or sell home-made articles on DaWanda. Or they have products personalised. Are the boundaries between the consumer and the producer role becoming blurred?

Yes, and I think this is a positive trend. A current example for this is miadidas. Here, consumers can design their own trainers, by choosing their preferred colour and material, for example. Or look at this, our creative mint & bergamot shower gel (Steinle smiles and lifts up the Alverde bottle, which has a personalised Zukunftsinstitut Workshop GmbH label, including a photo of the team). Great, isn’t it, that you can make something like this? I am a so-called prosumer – consumer and producer at the same time. Alvin Toffler coined this term back in 1980 in his book “The Third Wave”, foreseeing this development.

e n a b l e r _

Consumers 4.0

26

But isn’t there a huge difference between personalised products and old furniture that you put on eBay?

Why? When we offer old furniture for sale on eBay, take photos of it, write the description and sell it successfully – we are filled with pride. In many areas, consumers today can create their own worlds. Digitisation has hugely increased their opportunities and scope for action. That makes people happy. Autonomy is happiness, we know that from psychology.

That sounds very positive. But are all consumers able to handle this double role?

The roles are not completely blurred. Obviously, you cannot pretend to be a private consumer if you buy seven apart-ments in Berlin just to register them with Airbnb, or if you set up an online pharmacy. These things require special exper-tise, and you have to be aware of the legal requirements too. But nowadays, web portals like eBay or DaWanda are really well-made and easy for “normal” consumers to use.

Up to now, we have only talked about the challenges which consumers face. But how much power does the consumer actually wield over product requirements or government policy, with regard to brand awareness and brand evaluation? Digitisation opens the door to completely new ways of getting involved, doesn’t it?

Consumers have increasing power when it comes to commu-nication. Our society has become more vulnerable for emo-tional responses, particularly through social media. This can be highly dangerous for companies. They desperately need a communication strategy, they need to be more open and transparent. This in turn requires trust, a new relationship between companies and the public. If both sides are actually talking to each other, it is easier to forgive mistakes.

Is there a trend toward ethics? Are companies being judged more often by their behaviour?

Well, sales of sustainable products are on the increase. But this is not something which affects the entire population, as you can see if you look at the clothing industry. On the one hand, people are increasingly becoming interested in fair trade products, but on the other hand, the discounter market is growing – a market in which the goods are certainly not manufactured under fair conditions. Here it is about participa-tion. People define themselves by the clothes they wear, and nowadays, people who once were unable to participate are

now able to join in. Simply because there has never been such a thing as a global production chain for ultra-cheap offers. But moralising in the market has many causes. One important point is transparency. If a textile factory in India collapses, we see it in the media virtually in real time. That encourages moral support, of course. Ethics are part of the evolutionary process. People are successful because they cooperate. Digitisation also means: we’ll meet again. There is no such thing as anonymity on the web. Everything can be traced. So ethical behaviour, transparency and fairness are the best principles for companies to adopt if they want to establish themselves strongly.

Talking of evolution: how is the role of the consumer as a “prosumer” likely to evolve?

I think consumers will incline even more strongly to becom-ing co-creators, to creating their own worlds. New and inter-esting structures are currently emerging in the area of produc-tion and knowledge production. Think of all the breweries, for example, which offer beer brewing courses. Brands and prod-ucts will increasingly come adrift. The brand will become more important, it will have more symbolic value. But the product will be something which the customer has made. Companies are well advised to support their customers in this area.

ANDREAS STEINLE is a communication expert, and offers consultancy services to businesses to help them find practical ways of implementing trends in business innovations. This is the core mission of the Zukunftsinstitut Workshop GmbH (Future Institute Workshop) which he co-founded in 2014, an affiliate company of the Zukunftsinstitut (Future Institute). He is also a speaker, and has authored numerous books and studies.

e n a b l e r _

Consumers 4.0

27

Shop owner: Theresia Fischer

www.dawanda.com/shop/ theresia-fischermember since 2013

50

71

5

Accessories Hats Bags Kids & Co.

5 out of 5 points on the reviews

Shop

Products in shop

Reviews

Subscribers

Creative small businessesAlongside my job as a social worker, I enjoy sewing, crocheting and knitting. For a number of years, I have also been selling the things I make. This would never have been possible without the Internet. My business is far too small to warrant renting a shop floor. DaWanda also offers lots of information on legal questions. That’s great, because all the bureaucracy can be a real strain. I am delighted when people I know buy my things, but when a new customer orders something just because they like the things I make, that’s a real compli-ment.

e n a b l e r _

Consumers 4.0

2828

e n a b l e r _

A Birthday Summit

29

The location: the historic Kalkscheune Centre in Berlin Mitte. The place is buzzing with activity. Dana, from Bellevue Comprehen-sive School in Saarbrucken, is standing next to Isabell from the Luisenburg Grammar School in Wunsiedel. Together with the other participants of the beatbox workshop, the two 16-year-old girls chant their rap: “Darlehen, Dispo, Dauerauftrag” (loans, overdrafts, standing orders). Two rooms further on, Jade Li – a promising young film producer and winner of the WirtschaftsWerkstatt video clip competition – explains how to get the meaning of finance jargon across in a video. Down on the ground floor, it is handicrafts time. One table is full of old packaging materials, from which purses are being made; another table is full of visionary models for affordable accom-modation.

Around 150 pupils from across Germany took part in the Youth Summit, which was hosted by the WirtschaftsWerkstatt to celebrate its third anniversary. SCHUFA founded the initiative in 2013 with the aim of helping young people become more confident and competent with regard to financial affairs, and as a prevention programme to teach them to handle money and contracts responsibly. To date, the WirtschaftsWerkstatt has reached more than five million young adults, predomi-nantly in their favourite places: on the Internet and on social media channels such as Instagram, Facebook and YouTube.

In 2013, SCHUFA launched an educational initiative called “WirtschaftsWerkstatt”. The aim: to increase young people’s confidence and competence in handling their finances. To date, the project has targeted more than five million teenagers – a huge success which was cele-brated at the Youth Summit.photography_ Franziska Krug

A BIRTHDAY SUMMIT

e n a b l e r _

A Birthday Summit

30

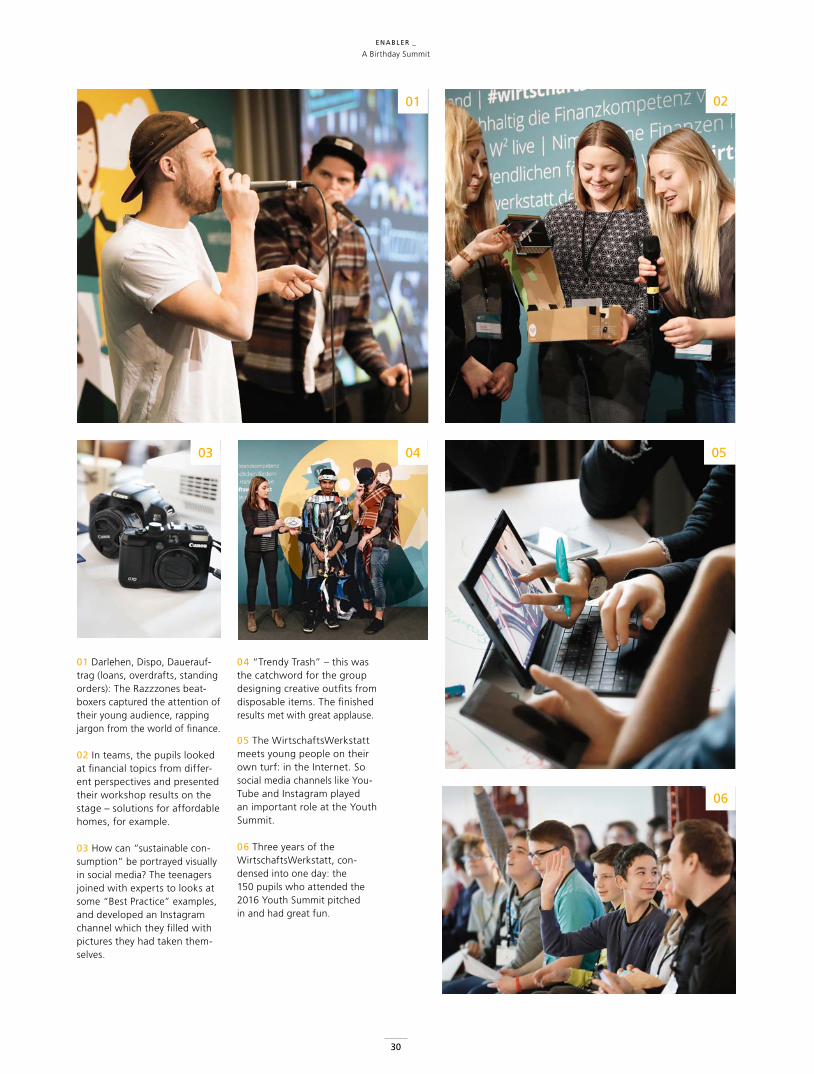

01 Darlehen, Dispo, Dauerauf-trag (loans, overdrafts, standing orders): The Razzzones beat-boxers captured the attention of their young audience, rapping jargon from the world of finance.

02 In teams, the pupils looked at financial topics from differ-ent perspectives and presented their workshop results on the stage – solutions for affordable homes, for example.

03 How can “sustainable con-sumption” be portrayed visually in social media? The teenagers joined with experts to looks at some “Best Practice” examples, and developed an Instagram channel which they filled with pictures they had taken them-selves.

04 “Trendy Trash” – this was the catchword for the group designing creative outfits from disposable items. The finished results met with great applause.

05 The WirtschaftsWerkstatt meets young people on their own turf: in the Internet. So social media channels like You-Tube and Instagram played an important role at the Youth Summit.

06 Three years of the WirtschaftsWerkstatt, con-densed into one day: the 150 pupils who attended the 2016 Youth Summit pitched in and had great fun.

01

0403

02

05

06

e n a b l e r _

A Birthday Summit

31

When learning is funThe centrepiece of the educational initiative www.wirtschafts-werkstatt.de is a study platform which focuses on themes which are highly relevant in the daily lives of young people. Besides providing helpful tutorials and practical facts about money, the initiative also organises numerous campaigns and competitions. Two of the school classes which were amongst the winners of the “Finance Heroes” competition were awarded €500 each in prize money at the Youth Summit. “Our year 11 class won the Finance Check,” says Markus Wagner, a teacher at the Luisenburg Grammar School in Wunsiedel. “The pupils were delighted, and want to use the money to buy new furniture for their break room.”

A business and law teacher, Wagner regularly uses ideas from the website in his lessons. He also makes use of the “SCHUFA macht Schule” material. “SCHUFA macht Schule” is a further component of the educational initiative, and supports teachers with classroom materials for financial topics. “I can use the educational materials, or parts of them, directly in my classroom teaching. It is really valuable, and saves so much time,” Wagner reiterates.

Highly relevantHenning Müller, who has been working at Oberberg Vocational College for nine years, also uses the materials. “The pupils enjoy the material, because it is so relevant to their worlds. We have looked at financing a car, or the ancillary costs you pay when you rent an apartment.” Although his pupils had a basic interest in financial affairs, they understood very little about the world of finance when they embarked on the three year course at the college, says Müller, who teaches business economics, accounting and controlling.

The best was saved to last at the Youth Summit: a presentation of all the creative ideas generated in the workshops. Raul is the first to dance onto the stage, to loud applause. The 17-year-old is wearing the “Trendy Trash” outfit which his group designed using disposable items. To the music of the beatbox group, the audience even shouts for an encore. “The whole setting was perfect, and showed great respect for the pupils,” smiles Markus Wagner. “They have learned so much today. And above all, they were challenged to use skills they would not normally use in school.” The data comes from a survey of 500 young people aged between

16 and 25, which the research institute Forsa conducted together with the WirtschaftsWerkstatt. The survey focussed on the way young people handle money and their understanding of financial matters. For more information on the study and financial topics, please see the WirtschaftsWerkstatt guidebook which was published for the first time in January 2017. This publication offers guidance for financial matters, and also includes a self-test and a budget book.

WWW.WIRTSCHAFTSWERKSTATT.DE

20%

88%

57%

22%

of young people have already experienced diffi-culties in repaying loans.

of young people would like to learn more about financial matters in school.

72%of young people would like more opportunities to learn about financial matters in a practical and relevant manner.

of young people look on the Internet for information on financial matters.

of young people feel confident to very confident when they sign up to pay for something by instalments.

More about the WirtschaftsWerkstatt

e n a b l e r _

A Birthday Summit

3232

e n a b l e r _

Trendsetters

33

Optimising processes, strengthening corporate culture, developing innovations: meet

four SCHUFA employees whose ideas are driving forces for the company – and who equip

SCHUFA to face the future.photography_ Stefan Freund

TRENDSETTERS

33

e n a b l e r _

Trendsetters

34 34

The analystWhenever a new trend emerges on a market relevant to SCHUFA, it is time for Dr Katarzyna Kolesky to get to work. As a market analyst, she identifies themes which will be important in the future, and ranks them for SCHUFA. Not long ago, it was FinTechs which brought momentum to the world of finance. It quickly became apparent that this trend was gaining momentum, causing major upheaval to the status quo and changing the whole com- petition situation in the finance industry. So at the start of 2016, Kolesky – who is Polish by birth – assembled a team of experts and formed the “FinTech Quality Team” to gain a complete overview of these new and innovative financial service providers. SCHUFA uses the insights gained by the FinTech experts to examine innovations, solutions and providers more closely, and derive recommendations for action accordingly. Because the FinTechs not only introduce new players to the finance market; they also offer SCHUFA numerous opportunities for ensuring its future success in positioning itself on the market.

» When a new trend emerges on the market, I have this inner compulsion to get to the bottom of it!« dr katarzyna kolesky, Leading Market Intelligence Expert

» SCHUFA thrives from the commitment and innovation of its employees. Their visionary ideas make our company strong to face the future.«holger severitt, member of the SCHUFA executive board

34

e n a b l e r _

Trendsetters

35

» The developments made by the Innovation Lab enable us to enter new areas of business, and supply our customers with the best products and services, based on high-quality analysis procedures.« dr gjergji kasneci, Chief Technology Officer and Head of Innovation and Strategic Analysis

35

The innovatorDr Gjergji Kasneci gained his doctorate in computer science, and worked for various globally leading research institutes. Since joining SCHUFA in 2014, he has been responsible for innovation and strategic analysis. In this role, Dr Kasneci soon realised just how many benefits advanced data analytics would bring to SCHUFA. Hence in 2015, the Innovation Lab was founded. This lab collaborates with internal and external partners to make technological develop-ments and the business models which are based on these more efficient for SCHUFA. The Innovation Lab develops its own procedures and methods for improving processes and for developing new pro- ducts and services for customers. A recent issue with which Dr Kasneci and his team have grappled is fraud in connection with online identity theft. In addition, the experts in the Innovation Lab actively collaborate with research institutes in universities and other renowned institutes to publish academic work and research results, which in turn enable validated insights to be used in public debate.

3535

e n a b l e r _

Trendsetters

36

The solution finderAbstracting problems and successfully finding solutions – this is not only Dr Gottron’s job at SCHUFA, it is also his passion. Formerly, Dr Gottron – who gained his doctorate in computer science – worked as an expert for search systems and data science, in university research. However, the solutions they developed rarely progressed beyond theory. In his work for SCHUFA, Dr Gottron can now apply his insights in practice. Because well-functioning search systems are a central tool for SCHUFA – when credit reports are requested, they must be allocated flawlessly. However, a single typing mistake, a new address or a name change make it very difficult to find the correct data set for the enquiry when the processes are automated. And because SCHUFA sets such high quality standards for its systems, Dr Gottron develops the respective solution himself – liaising intensively with experts from the various departments, of course. In recent times, he has begun applying the same approach to areas other than search systems. Together with the experts from his data manager team, he has been working on innovative services for SCHUFA customers.

» There is nothing more satisfying than collaborating with our specialist departments and customers to develop innova-tive services which provide the exact solution needed in day-to-day business.« dr thomas gottron, Head of Innovative Business Division

INNOVATION

IDEATECH-

NOLOGY

36

SOLUTION

e n a b l e r _

Trendsetters

37

The attentive observerFor Silvia Mieth, close observation is her daily work. How diverse are the tasks performed by her colleagues? How much responsibility do they have? How do managers interact with their employees? Many factors play a role when it comes to promoting and sustaining the physical health and social well-being of all employees in the workplace. Silvia Mieth’s job is to devise measures and activities which will maintain and optimise these factors. In doing so, she not only looks closely at the employees themselves, but also at other factors which affect the workplace. The post for occupational health management was created by SCHUFA in 2015, and Mieth – a 30-year-old business economist – has filled the position with life thanks to her dedication and expertise. She questions the existing structures and gives targeted recommendations to make employees more aware of health issues – offering everything from seminars for managers to leisure activities to road safety courses for employees with company cars.

» Companies are social systems containing numerous factors which can positively affect the health – and hence the productivity – of the employees.« silvia mieth, Coordination Officer for Occupational Health Management

PRODUCTIVITYMOTIVATION

SUCCESS

COMPENSATION

Health

AWARENESS WORK-LIFE BALANCE

COMMUNITY

EXERCISE

SATISFACTION

DIET

FUN

RESPONSIBILITYINTERACTION

COLLABORATION

37

e n a b l e r _

Trendsetters

38

of all consumer loans were repaid in due form.

97.8%

use SCHUFA products every year. In addition, 9,000 companies

rely on the credit bureau.

MILLION PRIVATE

CUSTOMERS

of the 1.2 million phone calls from consumers handled by the SCHUFA

private customer service centre in 2016 were resolved immediately.

97%

SCHUFA uses computer technology to respond to

enquiries for the first time.

1972

All index cards are electronically registered

and stored.

1983

SCHUFA handles around 140 million enquiries and entries.

2016

1,107

30

of the enquiries were admissible according to the

rules of procedure. In …

484

cases, the ombudsman decided in favour of the consumer. Considering the fact

that SCHUFA responds to 380,000 enqui-ries per day, the number of consumer concerns which are actually justified is

relatively low.

»GOOD«Personal SCHUFA credit reports, as supplied in

accordance with section 34 of the German Federal Data Protection Act (BDSG), were certified “GOOD” (grade:

2.3) in a finance quality test conducted in February 2016 by Stiftung Warentest, coming first in their category. The

test looked at how easy it was to understand the personal credit reports of five different bureaus (Source: Stiftung

Warentest – Finance test, issue 02/2016).

2 consumers applied in writing in 2016 to begin arbitration with a SCHUFA ombudsman. Of these, …

e n a b l e r _

The Facts

39

SCHUFA IN DIALOGUE

OMBUDSMAN

SCHUFA is the only credit bureau in Germany to offer a consumer-friendly ombudsman procedure. The ombuds-man is Dr Hans-Jürgen Papier, former president of the Federal Constitution-al Court. Consumers are thus able to turn for support to a leading person-ality with exceptional legal expertise.

SCHUFA IN FIGURES 2016*

* Figures rounded off

Volume of data

Information stored on natural persons and companies 813 million

Natural persons 67.2 million

Companies 5.3 million

Customers

Number of corporate customers 9,000

Number of private customers 2 million

Products and services

Reports and subsequent information for corporate customers 140.2 million

Information for consumers 2.1 million

Business figures

Sales 163.75 million

Annual net profit 28.2 million

Employees 800

CONSUMER ADVISORY BOARD

As a neutral board, the Consumer Advisory Board plays a special role in reflecting objectively on the work of SCHUFA. Members of the board include academics, journalists, politicians, debt advisors and representatives from business. The main focus of the board’s work is on financial and con-sumer competency. It also looks at consumer and supplier behaviour in the field of loans. The board liaises with the SCHUFA ombudsman, who likewise acts independently.

CUSTOMER ADVISORY BOARDS

Customer advisory boards make an essential contribution to the com-munication structure. Association com mittees have been established for banks and retailers, as well as five regional customer advisory boards. In particular, these boards discuss current topics on corporate strategy and business development. The cross- sectoral boards also supply valuable insights into the world of business.

e n a b l e r _

The Facts

ASSOCIATE

40

For years, we have been experiencing increasing digitisation in virtually all areas of our lives. Data protection and data security are thus a challenge for everyone and everything – right down to protection against identity theft. SCHUFA has played a pioneering role when it comes to handling electronic data in a responsible manner: all data is stored on servers in Germany. SCHUFA not only supplies companies with information, but also private individuals. For example, consumers can request credit reports on property developers or skilled workmen, or even for personal data protection purposes.

With regard to the challenges which SCHUFA and consumers will face, one must consider the fact that the role of the consumer is becoming increasingly mixed with entrepreneurial activities. For example, consumers are selling unwanted house-hold items via Internet auctions, or renting out a bedroom or their car for short-term use, or letting out a property they are not currently living in, or selling the electricity generated by the solar panels on their roof to the local energy provider. Many of these consumer-entrepreneurs buy and sell via Internet and smartphone. For some time, there has been a call for consumers to play a role in politics, for example in environmen-tal protection. People talk about “consumer citizens”. The role of the consumer in the future has to be viewed, support-ed and protected in a multi-dimensional way. One of the basic prerequisites here is for people to be able to control their

personal details. SCHUFA could play a key role here. The SCHUFA Consumer Advisory Board offers support. This is an independent board which looks at issues in a benevolent yet penetrating manner, and includes experts from media, politics, associations, businesses, budget consultancy and the academic world. We meet regularly and form work groups to discuss socially significant consumer issues, and make recommendations, e. g. in the field of data protection, scoring and private bankruptcy. We often take a controversial view-point. Concerns are discussed within the group, while insights are made public.

»We create trust« – SCHUFA is committed to this claim. What role does Germany’s leading credit

bureau play in shaping digital change in the consumer industry such that trust can thrive? Our associate

Dr Michael-Burkhard Piorkowsky, chairman of the Consumer Advisory Board, tenders a personal opinion.

professor dr michael-burkhard piorkowsky

is Professor Emeritus for Household and Consumption Economics at the University of Bonn, Germany. He became a member of the SCHUFA Consumer Advisory Board in 2008 and was appointed chairman in 2015. In his role as chairman he receives suggestions and topics proposed by the members, moderates the meetings and provides insight into the aspect of poverty prevention to the SCHUFA Consumer Advisory Board.

e n a b l e r _

Associate

41

PUBL ISHER

SCHUFA Holding AG Kormoranweg 5 65201 Wiesbaden

Responsible: Dr Astrid Kasper, Head of Public Affairs & CSR

Editing: Regina Porsch, Consultant Public Affairs & Content Management

www.SCHUFA.de

CONCEP T, DES IGN AND REAL IZ AT ION

3st kommunikation GmbH, Mainz

TEX T

Alexandra Schröder, Cornelia Theisen, Ulrich Pontes, 3st kommunikation GmbHPeter Gaide, ag textCatrin Krawinkel, Pressedienst Krawinkel

PHOTOGR APHY

3st kommunikation: TitleSCHUFA Holding AG: U2Shutterstock: p. 4, 6, 7Matthias Haslauer: p. 4, 8, 9, 11, 12, 13REUTERS/Axel Schmidt: p. 4, 14,15 Private: p. 5, 23, 24, 26, 27Stefan Freund: p. 5, 32, 33, 34, 35, 36, 37Franziska Krug: p. 5, 28, 30

Robert Gross: p. 16N26 GmbH: p. 17FinTech Group AG: p. 18Gettyimages: p. 23, 24, 27, U3 PR INT

Werbedruck Petzold GmbH, 64579 Gernsheim

Date: June 2017

40

PUBLISHER

SCHUFA Holding AG Kormoranweg 5 65201 WiesbadenGermany

Responsible: Dr. Astrid Kasper, Head of Public Affairs & CSR

Editing: Regina Porsch, Consultant Public Affairs & Content Management

www.SCHUFA.de

CONCEP T, DES IGN AND REAL IZ AT ION

3st kommunikation GmbH, Mainz

TEX T

Ulrich Pontes, 3st kommunikation GmbHCornelia Theisen, 3st kommunikation GmbHPeter Gaide, ag text

I LLUSTR AT ION

Anna Alexander, 3st kommunikation GmbH

PHOTOGR APHY

Stefan Freund: p. 4, 32-37Uwe Fischer: p. 16Matthias Haslauer: p. 4, 8, 9, 11-13, 26, 29Georg Roske: p. 18Roman Walczyna: p. 19Urban Zintel: p. 4, 15Gettyimages: Cover, p. 20, 21Shutterstock: p. 4, 30, 31Private: p. 17, 25

PR INT ING

Werbedruck Petzold GmbH, 64579 Gernsheim

Date of publication: June 2016

FSC C006527

SCF_Mag_EN_Innenseiten_160727.indd 40 27.07.16 11:09

1

ENABLER _Company Report 2016 _ Outlook 2017E

NA

BL

ER

_

Co

mp

an

y R

ep

ort

20

16

_ O

utl

oo

k 2

017

EN

AB

LE

R_

C

om

pa

ny

Re

po

rt 2

01

6 _

Ou

tlo

ok

20

17

![Microsoft ® Office Outlook ® 2003 Training Organize meetings with Outlook [Your company name] presents:](https://static.fdocuments.us/doc/165x107/56649d7f5503460f94a62ad1/microsoft-office-outlook-2003-training-organize-meetings-with-outlook.jpg)