COMPANY PRESENTATION 1H 2011 –JUNE 2011 · PT Trakindo Utama PT Chandra SaktiUtama Leasing 3. ABM...

32

COMPANY PRESENTATION 1H 2011 – JUNE 2011

Transcript of COMPANY PRESENTATION 1H 2011 –JUNE 2011 · PT Trakindo Utama PT Chandra SaktiUtama Leasing 3. ABM...

COMPANY PRESENTATION 1H 2011 – JUNE 2011

PT ABM Investama Tbk a member of Tiara Marga Trakino Group

ABM Consolidated Financial Highlight 1H 2011

SBU: PT. Cipta Kridatama (CK) – Contract Mining Services

SBU: PT. Sumberdaya Sewatama (SS) – Power Solutions

SBU: PT Reswara Minergi Hartama (Reswara) – Coal Production

SBU: PT.Sanggara Sarana Baja (SSB) – Engineering Services

SBU: PT. Cipta Krida Bahari (CKB)- Integrated Logistic

p. 3

p.15

p.18

p.21

p.24

p.30

p.31

Table of Contents

2

Overview of Tiara Marga Trakindo Group

— Established in 1970, Trakindo was

founded by AHK Hamami

— Trakindo became the sole authorized

dealer for Caterpillar in 1971 and now

has more than 70 branches

— Over a 40 year period, Trakindo has

developed into one of the largest

national groups in Indonesia

Shareholder Value Addition

— Access to financial resources to support

growth plans

— Timely market intelligence and access

— TMT refers customers and is itself and

important customer to ABM

ABM Investama A Member of Tiara Marga Trakindo Group

Tiara Marga Trakindo Group Structure

PT Tiara Marga Trakindo Group (TMT)

PT. Chitra

Paratama

PT Tri Swardana

Utama

Others

PT Chakra Jawara

PT Mahadana

Dasha Utama

PT ABM

Investama

Tbk

PT Trakindo

Utama

PT Chandra

Sakti Utama

Leasing

3

ABM Investama Tbk

ABM is an integrated energy company with three key business units in coal production, contract

mining services, and power solutions, supported by two crucial components of engineering

services and integrated logistics.

Our integrated business allow us to create synergy and offer end-to-end energy solutions that

enable us to provide a more efficient cost structure, increasing profitability and assuring business

sustainability.

Vision

“To be the leading investment

company with strategic

investments in energy

resources, services, and

infrastructures.”

Mission

1. To continually create meaningful and challenging

job opportunities for as many Indonesians as

possible

2. To ensure sustainable and profitable growth that

maximize shareholders value

3. To provide value adding solutions that will

optimize customer satisfaction

4. To actively engage with communities as a good

corporate citizen.

Vision and Mission

4

Rachmat Mulyana Hamami

President Commissioner

• Worked in various positions within the

Tiara Marga Trakindo group for more

than 19 years

• Appointed in 2005 as Secretary General

of the China Committee of the

Indonesian Chamber of Commerce and

Industry

• Worked in various positions within the

Tiara Marga Trakindo group for more

than 10 years

• Holds the position of President Director

in PT Mahadana Dasha Utama

Mivida Hamami

Commissioner

• Commissioner of PT Weda Bay Nickel

• Independent Commissioner of PT Hero

Supermarket Tbk.

• Former President Commissioner of

Bank BNI

• Former Vice Chairman /

Superintendent of the Corruption

Eradication Commission

Erry Riyana Hardjapamekas

Independent Commissioner

Board of Commissioners

5

• Former Managing Director at

Standard Chartered Bank,

Jakarta

• Previously Partner of

Corporate Finance / Advisory

Department at Fund Asia,

Jakarta

• Former Managing Director of

Abacus Capital, Jakarta

Achmad Ananda

Djajanegara

President Director

Syahnan Poerba

Corporate Support Service

Director

• Former Country Manager at

PT D&B (Dun & Bradstreet),

Indonesia

• Former Director of

operations at PT AXA

Mandiri Financial Services

• Former Chief Financial Officer

of Sime Darby (Minamas

Plantation), and San Miguel,

Indonesia

• Former Senior Financial

Controller at PT John Crane,

Indonesia

• Former General Manager of

Corporate Finance and

Administration at Keris Group

Willy A. Adipradhana

Finance Director

• Former President Director of

PT Mitra Energi Batam and

PT Dalle Energy Batam

• Former Senior Vice President

of Corporate Growth and

Planning at PT Medco Power

Indonesia

Yovie Priadi

Corporate Strategy Director

Board of Directors

6

Contract Mining: PT Cipta Kridatama (“CK”)

• Top 5 mining contractor in Indonesia by overburden volume providing full end-to-end “pit to port”

services including project survey, mine design, overburden removal, coal extraction, hauling, and mine

rehabilitation

Subsidiaries (SBU)

Power Solutions: PT Sumberdaya Sewatama (“SS”)

• A power solutions related service provider in Indonesia servicing mainly the utility and mining sectors.

Currently has more than 880MW of electricity generation capacity

• Has a 20% stake in Meppogen (80MW simple cycle power plant)

Coal Production: PT Reswara Minergi Hartama (“Reswara”)

• Coal production business with three direct subsidiaries: PT Tunas Inti Abadi (coal producer), PT Media

Djaya Bersama (coal producer) and PT Pelabuhan Buana Reja (manage and service the port subject to

the completion of the port construction and license approval)

Engineering Services: PT Sanggar Sarana Baja (“SSB”)

• Operates engineering services such as fabrication, remanufacturing, transport equipment and site

services

Integrated Logistics: PT Cipta Krida Bahari (“CKB”)

• Provides integrated logistics services, including freight forwarding, project logistics, industrial, offshore

and coal logistics shipping, and warehouse and shore base management services

7

Coal production;

Sub-Holding for

BEL and Mifa

PT Cipta

Kridatama (“CK”)

Contract Mining

99.99%

PT Sumberdaya

Sewatama (“SS”)

Power solutions

99.98%

PT Cipta Krida Bahari (“CKB”)

Integrated logistics

99.99%

PT Sanggar Sarana

Baja (“SSB”)

Engineering services

99.96%

Sub-Holding for

thermal energy IPP

PT Pradipa

Aryasatya (“PAS”)

99.9%

Sub-Holding for

renewable energy

IPP

PT Nagata Bisma

Shakti (“NBS”)

99.9%20.0%

Coal logistics

PT Baruna Dirga

Dharma (“BDD”)

99.9%

Shipping

PT Alfa Trans

Raya (“ATR”)

99.99%

Valle Verde Pte. Ltd. PublicPT Tiara Marga Trakindo (“TMT”)

23.12% 55% 21.88%

99.98%

IPP

PT Metaepsi Pejebe Power

Generation (“Meppogen”)

General trading

PT Prima Wiguna

Parama (“PWP”)

PT Reswara Minergi Hartama

(“Reswara”)

Coal production

PT Bara Energi Lestari

(“BEL”)

Coal production

PT Mifa Bersaudara

(“Mifa”)

Coal production

99.99%

70.0%99.99%99.99%

99.99% 99.99%

Coal

production

PT Tunas Inti

Abadi (“TIA”)

Port operator &

management

PT Pelabuhan Buana

Reja (“PBR”)

PT Media Djaya

Bersama (“MDB”)

ABM Group and Shareholding Structure

8

9

1 Strategically positioned to capitalize on Asian and Indonesian energy markets

2

Exposure across the energy value chain with diverse product offering3

4 Well-established and broad customer base

5 Comprehensive footprint and market coverage across Indonesia

6 Strong sponsorship and support from reputable shareholder

7 Experienced and highly qualified management team with a proven track record

Leading energy market player in Indonesia

Positioning and Highlight

10

— Coal imports in China, India, South East Asia and Indonesia are expected to grow strongly from 2011E to 2014E

114 117 122 124

0

50

100

150

2011E 2012E 2013E 2014E

Million

tons

Thermal Coal Imports

(China)

Source Wood Mackenzie

MALAYSIA

CHINA

INDONESIA

PHILIPPINES

SINGAPORE

INDIA63

75

98107

0

50

100

150

2011E 2012E 2013E 2014E

Million

tons

Thermal Coal Imports

(India)

6473

8288

0

40

80

120

2011E 2012E 2013E 2014E

Million

tons

Thermal Coal Consumption

(Indonesia)

Source Wood Mackenzie

4452

5660

0

30

60

90

2011E 2012E 2013E 2014E

Million

tons

Thermal Coal Imports (SE

Asia)

Source Wood Mackenzie

Source Wood Mackenzie

MDB

TIA

Strategically Positioned to Capitalize on Asian and Indonesian Energy Markets

919

420 365 358 221 159 117

2,836

17%8%

7% 7% 4% 3% 2%

0

1,000

2,000

3,000

Coal ProductionLow Rank Coal Reserves, Market Share by Reserves

MM tons, %

Source Wood Mackenzie, JORC

53%

468

295

357

0

200

400

600

Aggreko Others

42%

26%

32%

Source PLN e-procurement website, Aggreko website Investor Relation March 2011

Temporary PowerProduction capacity (2011), Market Share by Capacity

MW, %

661

470

319

128 100 93 85 72

426

28%

20%

14%

5% 4% 4% 4% 3%

18%

0

200

400

600

800

Overburden Removal (2010), Market Share by Overburden Removal

Million BCM, %

Contract Mining

Source Wood Mackenzie

Leading Energy Market Player in Indonesia

11

Exposure Across the Energy Value Chain (1)

Engineering

Services

Integrated

Logistics

Power

Solutions

Contract

Mining

Services

Coal

Production

• 7,703 hectares

concession area under 4

IUPs

• Estimated coal reserves

and resources of 221 and

561 million tons,

respectively

• Fleet of 428 heavy

equipment serving 7

customers as of June 30,

2011

• Estimated outstanding

contracted overburden

removal and coal of 465

million bcm and 34.4

million tons, respectively,

as of June 30, 2011

• Approximately 745

gensets (884MW

capacity)

• Manages more than 70

diesel power generation

projects in Indonesia

• 20% stake in Meppogen,

IPP with simple cycle

power plant

• Operates fleet of vessels,

trucks, loaders and dry

containers

• Provides coal logistics,

freight forwarding and

project logistics

• 35 branches and offices

located throughout

Indonesia

• 10 engineering services

workshops providing

fabrication,

remanufacturing,

transport equipment and

site services

• Customers mainly in

mining, oil and gas,

petrochemical and power

sectors

12

Contract Mining

Project Sites

Integrated Logistics

Offices

Engineering Services

Main Operating Sites

BATAM

PADANG

PEKANBARU

DURI

MEDAN

JAMBI

PALEMBANG

PONTIANAK

PANGKALANBUN

BANJARMASIN

SATUI

BATULICIN

MAKASSAR

SOROAKO

TARAKAN

AMBON

SORONG

BATU HIJAU

MATARAM

DENPASAR

LAMONGAN

SURABAYA

JAKARTA

MANADO

TANJUNG ADARO

SANGATTA

BATUKAJANG

TIMIKA

BANDA ACEH

BALIKPAPAN

SAMARINDA

TERNATE

TANGERANG

GRASBERG

KUALA KENCANA

BONTANG

AIR MUNING MUKO-MUKO

MANGKAL API

SUNGAI

DANAU

SUNGKAI

KOTA BANGUN

JONGGON

KUTAI

KERTANEGARA

SANGA-SANGA

— Able to operate throughout the country; competitive advantage over competitors

— Difficult to replicate coverage strength and poses barriers to entry for new entrants

BENGALON

Comprehensive Footprint and Market Coverage in Indonesia

13

SAMPLE SLIDES

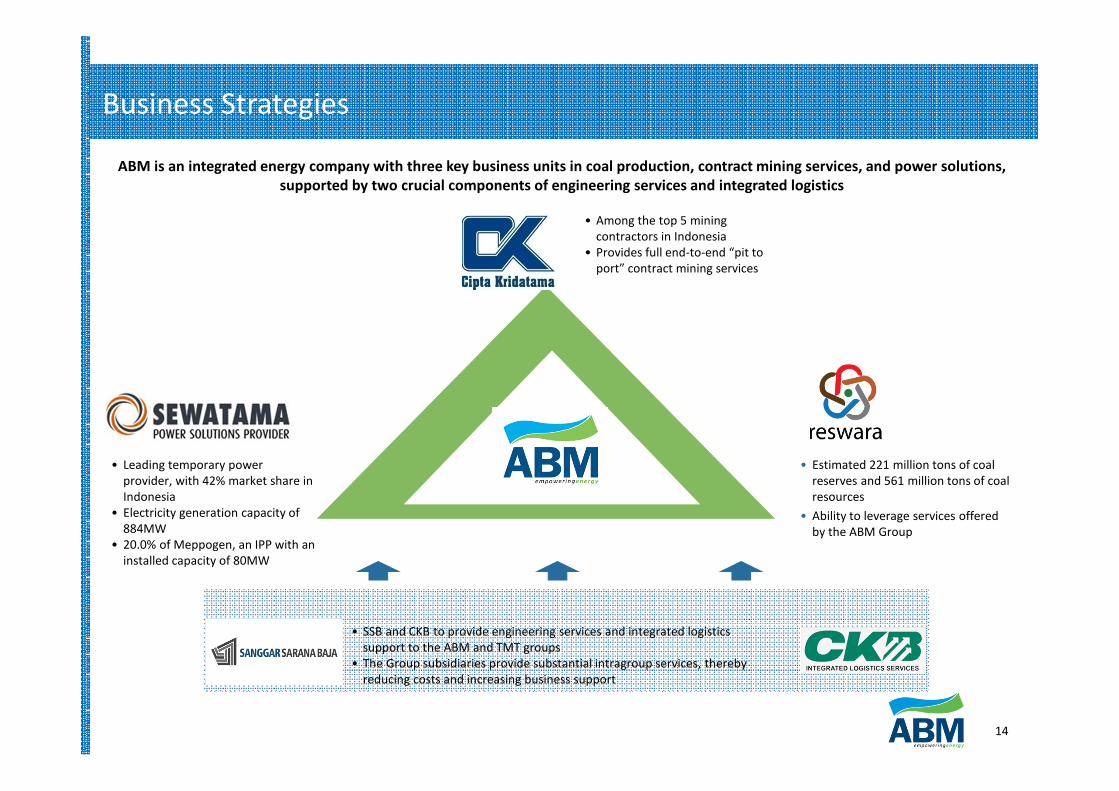

• Leading temporary power

provider, with 42% market share in

Indonesia

• Electricity generation capacity of

884MW

• 20.0% of Meppogen, an IPP with an

installed capacity of 80MW

• Among the top 5 mining

contractors in Indonesia

• Provides full end-to-end “pit to

port” contract mining services

• Estimated 221 million tons of coal

reserves and 561 million tons of coal

resources

• Ability to leverage services offered

by the ABM Group

• SSB and CKB to provide engineering services and integrated logistics

support to the ABM and TMT groups

• The Group subsidiaries provide substantial intragroup services, thereby

reducing costs and increasing business support

Business Strategies

14

ABM is an integrated energy company with three key business units in coal production, contract mining services, and power solutions,

supported by two crucial components of engineering services and integrated logistics

1.372

493 478 377 376

0

500

1.000

1.500

CK SSB SS CKB Reswara

(4) (11)

127 53 208(0%) (0%)

3%2%

7%

(4%)

0%

4%

8%

(150)

0

150

300

2008 2009 2010 1H 2010 1H 2011

Net Income Margin

Net Income(1)

IDR BN

3.2353.926

4.486

2.1972.778

0

2.000

4.000

6.000

2008 2009 2010 1H 2010 1H 2011

Revenue(1)

IDR BN

Income / (Loss) from Operations(1)

IDR BN

(470)

491 316 140341

(15%)

13% 7% 6%

12%

(15%)

0%

15%

(800)

0

800

2008 2009 2010 1H 2010 1H 2011

Income / (Loss) from Operations Margin

Year Ended Dec 31 6 Months Ended Jun 30

Year Ended Dec 31 6 Months Ended Jun 30

Year Ended Dec 31 6 Months Ended Jun 30

Breakdown of Revenue and Income / (Loss) from Operations(3)

IDR BN

Revenue

6 Months Ended Jun 30, 2011

Income from Operations

6 Months Ended Jun 30, 2011

(4)

(5)

44% 16% 15% 12% 12%

135 133

41 40 25

0

50

100

150

CK SS CKB SSB Reswara

36% 36% 11% 11% 7%

ABM Consolidated – Financial Highlight 1H 2011

Notes

1. ABM Group consolidated figures

2. CAGR = (2010 figure / 2008 figure) ^ (1 / number of years) -1

3. Based on standalone financials. Includes intragroup transactions

4. Net Income Margin = Net Income / Revenue

5. Income / (Loss) from Operations Margin = Income / (Loss) from Operations / Revenue 15

16

1.372

493 478 377 376

0

500

1.000

1.500

CK SSB SS CKB Reswara

2.222

844 803 539

97

0

1.000

2.000

3.000

CK SSB SS CKB Reswara

Revenue by Division

Year Ended Dec 31, 2010(1) 6 Months Ended Jun 30, 2011(1)

Income from Operations by Division

Year Ended Dec 31, 2010(1)(2) 6 Months Ended Jun 30, 2011(1)

Notes:

1. Figures are based on pre-elimination of intercompany transactions

2. Includes loss of IDR48BN from coal production

49% 19% 18% 12% 2% 44% 16% 15% 12% 12%

154

130

65

41

(41)(50)

0

50

100

150

200

CK SS SSB CKB Reswara

44% 37% 19% 12% -12%

135 133

41 40 25

0

50

100

150

200

CK SS CKB SSB Reswara

36% 36% 11% 11% 7%

IDR BN

IDR BN

IDR BN

IDR BN

Breakdown by Subsidiaries

17

510 463 713 508 1.006

1.9121.216

1.2111.141

2.825

0

2.000

4.000

2008 2009 2010 1H 2010 1H 2011

Short Term Long Term

Total Debt(1)

IDR BN

12,0x

3,1x2,8x 2,7x

4,3x

0,0x

5,0x

10,0x

15,0x

2008 2009 2010 1H 2010 1H 2011

Total Debt / EBITDAx

153% 171%

140%

287%

0%

100%

200%

300%

2008 2009 2010 1H 2010 1H 2011

Total Debt / Total Equity%

1.8x

4,3x

6,8x 6,5x

7,8x

0,0x

2,0x

4,0x

6,0x

8,0x

2008 2009 2010 1H 2010 1H 2011

EBITDA / Interest Expensex

Notes:

1. Total debt = Short term bank loans + long term bank loans + current maturities of long term debts and finance lease obligations + other long term loans (related and third parties) +

finance leases (related and third parties)

2. Used two times 1H2010 EBITDA as proxy for LTM 1H2010 EBITDA in calculation; Used LTM EBITDA in 1H2011 calculation

3. Used two times 1H2010 EBITDA and Interest expense for LTM calculation; Used LTM EBITDA and LTM interest expense in 1H2011 calculation

NM

(2)

(3)

Year Ended Dec 31 6 Months Ended Jun 30 Year Ended Dec 31 6 Months Ended Jun 30

Year Ended Dec 31 6 Months Ended Jun 30 Year Ended Dec 31 6 Months Ended Jun 30

(2)

(3)

Consolidated Balance Sheet

Contract Mining Operations Brief as of June 2011

• Top 5 contract mining service in Indonesia by overburden

removal(1)

• Full end-to-end “pit to port” contract mining services from

exploration(2), mine planning, overburden removal, coal

extraction and loading, transportation and processing,

rehabilitation and reclamation

• Experienced management having worked in major

companies

• As of 30 Jun 2011, CK employs over 2,800 employees

• Provides services to seven Indonesian coal producers for

nine different projects. The contract mining agreements

have terms ranging from three years to life of the mine

• Fleet of 428 heavy vehicles and mining equipment,

including bulldozers, excavators, cranes and drilling

machines

• Equipment manufactured by Caterpillar, Liebherr,

Hitachi, and Terex

PT. Cipta Kridatama (CK)- Contract Mining Services

18

Overburden Removal and Coal Production Volumes

Year Ended Dec 31

73,8

104,2100,0

49,6 53,05,4

7,1

8,3

3,5

4,6

0

4

8

12

0

40

80

120

Overburden Removal (LHS) Coal Production (RHS)

Source Company Information

Million BCM Million Tons

6 Months Ended Jun 30

2008 2009 2010 1H2010 1H2011

Overburden and Key Customers

19

Type of equipment Capacity Number of units Average age (in years)

Excavator 250 - 350 tons 13 3 – 5

20 - 100 tons 83 3.4 - 6.5

Truck 40 - 100 tons 220 3.8 - 5.6

Dozer 64 4.5

Grader 14 - 16 feet 30 2.8

Wheel loader 6 5.3

Compactor 11 7.2

Drill machine 1 6

Total 428

20

Operating Agreements

12

3

4

6

7

Kalimantan

Sumatra

Concession Holder

Mining Project Sites Expected Contract Duration

Estimated Outstanding Contracted Volume of Coal /

Overburden (Million Tons / Million BCM) as of

June 30, 2011(3)

Samarinda, East Kalimantan

From Jun 14, 2004 – Aug 31, 2015 125.0

Kotabangun, Kutai Kertanegara, East Kalimantan

From Dec 2007 – Completion of all work< 42 months from the commencement of overburden removal

12.5

Desa Batuah (Air Panas), Kecamatan Loa Janan, Kabupaten Kutai Kartanegara, East Kalimantan

From Mar 18, 2005 – Target of 54.2 million BCM of overburden and/or 7.7 MT coal ROM is reached

2.8 / 12.3

Jonggong, Busang and Loa Kulu, East Kalimantan

From Nov 29, 2007 – Oct 18, 2015 1.1 / 14.4

Satui and Kusan Hulu, Tanah Bumbu,East Kalimantan

From Jun 25, 2009 – Later of Life of mine, or Jun 30, 2020

27.0 / 155.3

Batulicin,South Kalimantan

From Jul 1, 2006 – Life of mineSungkai site: From start of operations or by Aug 2008 – Earlier of Jul 2011 or when the pit coal reserve is considered to be un-economical to mine

3.5 / 16.2

Tanjung Dalam Village,Bengkulu Province

From Mar 18, 2011 – 72 months from start of operations, or completion of obligations, whichever is earlier

- / 129.6

Total 34.4 / 465.3

1

2

3

4

5

6

7

5

CK’s Current Customers

SS Operations- PLTD Bitung Menado Services Offer

Temporary Power

Pillar and

Operations and

Maintenance

(“O&M”)

Independent

Power Generation

• Provides power solutions mainly to utility sector customers

• 884MW of electricity generation capacity as of June 30, 2011

• Main customer is PT PLN (Persero) (“PLN”),

• Utility customers contributed 80.6% of Temporary Power

division’s revenue for 6 months ended June 30, 2011

• Pillar business provides dewatering management services,

rental of centrifugal pumps, load bank, temperature control

units, and intends to provide optimization and consultation

services

• O&M provides end-to-end power plant operations,

maintenance services and specific repair and maintenance

services

• Thermal Energy

– 20% stake in Meppogen, a 80MW simple cycle power plant

in South Sumatra.

– Mepoggen to convert to a 110MW combined cycle

power plant

– Entered into a PPA in 2005 with PLN Kitlur Sumbagsel to

sell 80MW of power for 20 years

– Subsidiary PAS to acquire 2 independent power producers

• Renewable Energy

– SS and NBS to invest / acquire to develop independent

power production through renewable energy

PT Sumber Daya Sewatama (SS) – Power Solutions

21

Key Customers

Year Ended Dec 31, 2010

Total Revenue: IDR803BN(1)

6 Months Ended Jun 30, 2011

Total Revenue: IDR478BN(1)

Temporary

Power

94.7%

Other Services(2)

5.3%

65,5%78,2% 81,8%

0%

25%

50%

75%

100%

2008 2009 2010

Revenue Contribution from PLN to SS

PT PLN (Persero)

Temporary

Power

95.7%

Other Services(2)

4.3%

Revenue By Division and key Customers

22

ModelNumber of Units as

of Jun 30, 2011Capacity

(kW)

Average Useful Life

(Yrs) (2)

Average Age as of Jun 30, 2011

(Yrs)

Diesel

Generator

Sets

745 875,492 10 6

Gas

Generator

Sets

5 8,662 15 2

Total 750 884,154

Generators

Electricity Generation Capacity and Average

Utilization RatekW %

637.214

757.804 791.680 759.680

884.154

72%70%

74%72%

73%

60%

65%

70%

75%

80%

0

250.000

500.000

750.000

1.000.000

2008 2009 2010 1H 2010 1H 2011

Electricity Generation Capacity Average Utilization Rate

Average Lease Rate per kWh

196 199

235 233249

0

100

200

300

2008 2009 2010 1H2010 1H2011

IDR / kWh

Electricity Generations Capacity, Lease Rate, Generators, Competition

23

TIA Operations Reswara

— Coal mining conducted through Reswara’s 2 subsidiaries

— PT Tunas Inti Abadi (“TIA”, 99.99% ownership)

— PT Media Djaya Bersama (“MDB”, 70% ownership)

— Port to be owned and managed through PT Pelabuhan Buana

Reja (“PBR”) (99.99% shareholding), upon construction

completion and license approval

— Current port management utilize third party services

— Reswara to utilize services of PBR when it achieves full

commercial capability, subject to construction completion

and license approval

— TIA mine utilizes open cut mining methodology, producing

low rank coal with low ash and low sulphur content

— Coal mined from TIA’s mines are marketed as “TIA Compliant

Coal”; coal bought from third parties are sold as “TIA Traded

Coal”

PT. Reswara Minergi Hartama (Reswara) – Coal Production

24

TIA MDB Total

Coal Reserves (MT)

Proved Reserves 13 7 20

Probable Reserves 39 162 201

Total Reserves 52 169 221

Coal Resources

Measured 32 18 50

Indicated 39 289 328

Inferred 35 148 183

Total 106 455 561

Concession (ha) 3,074 4,629 7,703

Balikpapan

South Kalimantan

Central Kalimantan

Palangkaraya

Banjarmasin

Indonesia

Kalimantan

Tunas Inti Abadi Project Area

Balikpapan

South Kalimantan

Central Kalimantan

Palangkaraya

Banjarmasin

Indonesia

Kalimantan

Tunas Inti Abadi Project Area

TIA

23.5%

MDB

76.5%

TIA

18.9%

MDB

81.1%

Coal Resources

Total Resources: 561 Million Tons Total Reserves: 221 Million Tons

Coal Reserves

Source PT Runge Indonesia Statement of Open Cut Coal Resources and Reserves for TIA, BEL and Mifa concessions, as of 30 June 2011

MDB Site

TIA Site

Coal Resources and Reserves

TIA Operations

Coal Productions

Coal Productions

26

Year Ended Dec 31

113

999

537

873

70

1.179

590

940

0

500

1000

1500

2009 2010 1H2010 1H2011

Production Volume Sales Volume

‘000 tons

6 Months Ended Jun 30

PT Tunas Inti Abadi

— TIA was acquired in Dec 2007, commenced commercial production

in Aug 2009 and coal sales in Oct 2009

— Coal mining is contracted to ABM subsidiary, CK

— 25 km from pit to port at Bunati

— 26 kmfrom port to anchorage point at Muara Satui

— 8,000 ton barge loading capacity at jetty

— 120,000 tons temporary pile facility at the mining pit

— Logistic advantages: Close to the Ocean

Road Concession Area Sea

Indonesia

ROM SP

PLTU

PLTU

X

Meulaboh Port

INDIAN OCEAN

PT. Mifa

Bersaudara

PT Bara Energi Lestari

Mifa and BEL

PT Media Djaya Bersama

— 70% ownership in MDB

— To begin coal production in 2012 by using existing

infrastructure and begin construction of own infrastructure

in 2012

— Intends to sell coal to Indian power plants for blending

— Logistic advantages: Close to the Ocean – 12 km pit to port

— Plan to build land conveyer belt for logistic

Site Layout of TIA Concession Area Site Layout of MDB Concession Areas

Sumatra

Indonesia

Kalimantan

TIA

Concession Area

Pt Tunas Inti Abadi

Rom Stockpile

Office and Camp Facilities

Intermediate

Stockpile

Area Port Pt. PBR

Road Concession Area River

Site Layout – Concession Area

27

Entity

Concession

Holding

Company

Type of

Concession Location

Current

Concession

Area (ha)

Expiry

Date of

Current

Phase

TIA TIA IUP(1) South

Kalimantan2,355

Mar 16,

2021

TIA TIA IUP(1) South

Kalimantan719

Mar 5,

2021

BEL BEL IUP(1) Aceh 1,495Sep 26,

2017

Mifa Mifa IUP(1) Aceh 3,134Apr 13,

2025

TIA MDB

Calorific Value (Adb) 5,370 kcal/kg 5,310 kcal/kg

Caloric Value (GAR) 3,960 kcal/kg 3,440 kcal/kg

Total Moisture (AR) 37.4% 43.8%

Ash Content (Adb) 5.7% 4.6%

Sulfur (Adb) 0.15% 0.16%

Source PT Runge Indonesia Statement of Open Cut Coal Resources and Reserves

for TIA, BEL and Mifa concessions, as of 30 June 2011

Concession Breakdown Coal Characteristics

Concession Breakdown and Coal Char

28

Expected PBR Port Capacity

Loading Conveyor5 mtpa

900 meters long

Barge300 feet barge (8,000 tons)

2 loading facilities

Crusher Up to 750 tons / hour

Stockpile 120,000 tons

28,437,1 34,9

46,6

0

25

50

2009 2010 1H 2010 1H 2011

Year Ended Dec 31

29,0 31,0 30,0 32,0

0

25

50

2009 2010 1H 2010 1H 2011

Year Ended Dec 31

TIA - Average Selling Price(1)

US$ / ton

TIA - Total Cash Cost (1)(3)

US$ / ton

6 Months Ended Jun 30

6 Months Ended Jun 30

Historical Coal Production and Projected Capacity (1)

Million Tons

Average Strip Ratio

Year Ended Dec 31

14,6

4,7 3,76,8

0

5

10

15

2009 2010 1H 2010 1H 2011

6 Months Ended Jun 30

Year Ended Dec 31

0,1

1,0

0,0

0,5

1,0

1,5

2009 2010

(2)

Average Selling Price, Production Cash Cost and Strip Ratio

29

SSB Operations SSB Business

Transport

Equipment

Division

Designing, manufacturing and distributing

products for transportation and material

handling business

Site Services

Division

On-site repair, process plant maintenance and

construction services

Fabrication

Division

Design and manufacture of process equipment,

general fabrication, site construction and

installation solutions

Re-Manufacturing

Division

Salvaging, remanufacturing and manufacturing

of heavy equipment core components

PT. Sanggar Sarana Baja (SSB) – Engineering Services

30

Business Overview

— Integrated logistics provider offering freight forwarding,

project logistics, industrial / offshore and coal logistics

shipping, warehouse and shorebase management services

— Freight forwarding services: Integrated logistics services

via owner and third party operated freight services

— Project logistics: Transportation of over weight and over

size cargo (heavy equipment, machines and engines)

— Energy related logistics: Industrial, offshore and coal

logistics shipping and warehouse and shorebase

management services

— PT Baruna Dirga Dharma (BDD) is our coal logistic.

— Provides through CKB and a third-party sub-contractor,

barging services to TIA as a part of its coal logistics chain

— Over 330 employees and operates integrated sea, air and

road networks from 35 branches and offices in Indonesia

— ISO 9001: 2008 and OHSAS 18001: 2007

PT. Cipta Krida Bahari (CKB) – Integrated Logistic

31

32

Contact

Investor Relations

Errinto Pardede

Tel:6221-2997-6767 Ext.1874

Fax : 6221-2997-6768

Email : [email protected]

Email : [email protected]

Website : www.abm-investama.com

Gedung TMT 1, 18th Fl, Suite 1802

Jl Cilandak KKO No.1

Jakarta 12560 - Indonesia

![[PPT] The Business Case for ABM Pt 1: Planning & Budgeting](https://static.fdocuments.us/doc/165x107/58731fca1a28ab673e8b7311/ppt-the-business-case-for-abm-pt-1-planning-budgeting.jpg)