Company Accounts Chapter 14 © Luby & O’Donoghue (2005)

17

Company Company Accounts Accounts Chapter 14 Chapter 14 © Luby & O’Donoghue (2005) © Luby & O’Donoghue (2005)

-

Upload

nigel-jencks -

Category

Documents

-

view

214 -

download

0

Transcript of Company Accounts Chapter 14 © Luby & O’Donoghue (2005)

CompanyCompany Accounts Accounts

Chapter 14Chapter 14

© Luby & O’Donoghue (2005)© Luby & O’Donoghue (2005)

Share capitalShare capital

Share capital represents what has been invested in the company by the owners or shareholders.

A person invests or buys ownership of a company by purchasing shares in that business.

CapitalCapital

Authorised share capital: This is the maximum amount of shares (as stated in the memorandum and articles of association of the company) a company is entitled to issue.

Issued share capital: This is the amount of authorised share capital actually issued and allotted to shareholders.

Called-up capital: This is the amount of capital payment which has actually been demanded by the company. This applies only where shares are issued and are payable by instalments rather than in full on application.

Paid-up capital: This is the amount of the called-up capital that has been actually paid over to the company by the shareholders.

Uncalled capital: This is the amount of capital that shareholders agree to pay if they are called on to do so.

Share premiumShare premium

When shares are issued they have a nominal value. This is the value or denomination the company chooses for its shares. This is a meaningless value. The true value of the shares is the market value.

If a company issues 1,000 shares with a nominal value of €1 and they receive €3 per share, then the shares have been issued at a premium of €2 per share.

Share capital amounts to €1,000 (nominal value)and a Share premium amounts €2,000 (representing the premium got for the shares).

DividendsDividends

A shareholder reward for investing in the company comes in the form of a dividend.

A dividend is a share of the profits made by the company.

The directors of the company decide the amount of profits to be retained in the business for expansion and the balance is given as dividends to the shareholders.

Share capitalShare capital

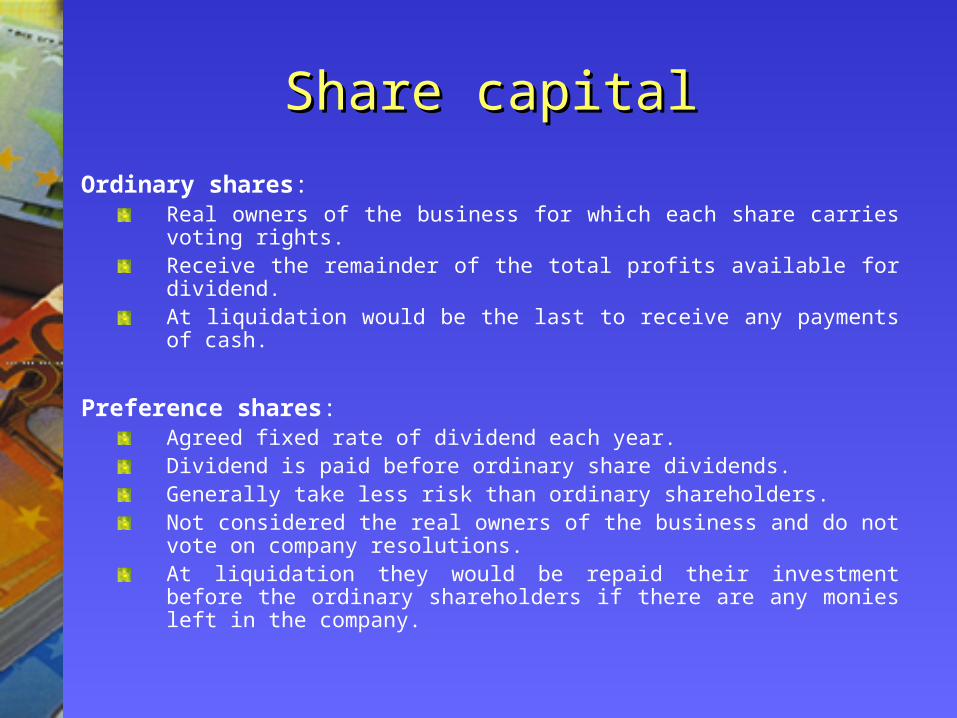

Ordinary shares: Real owners of the business for which each share carries voting rights.Receive the remainder of the total profits available for dividend.At liquidation would be the last to receive any payments of cash.

Preference shares: Agreed fixed rate of dividend each year. Dividend is paid before ordinary share dividends. Generally take less risk than ordinary shareholders.Not considered the real owners of the business and do not vote on company resolutions.At liquidation they would be repaid their investment before the ordinary shareholders if there are any monies left in the company.

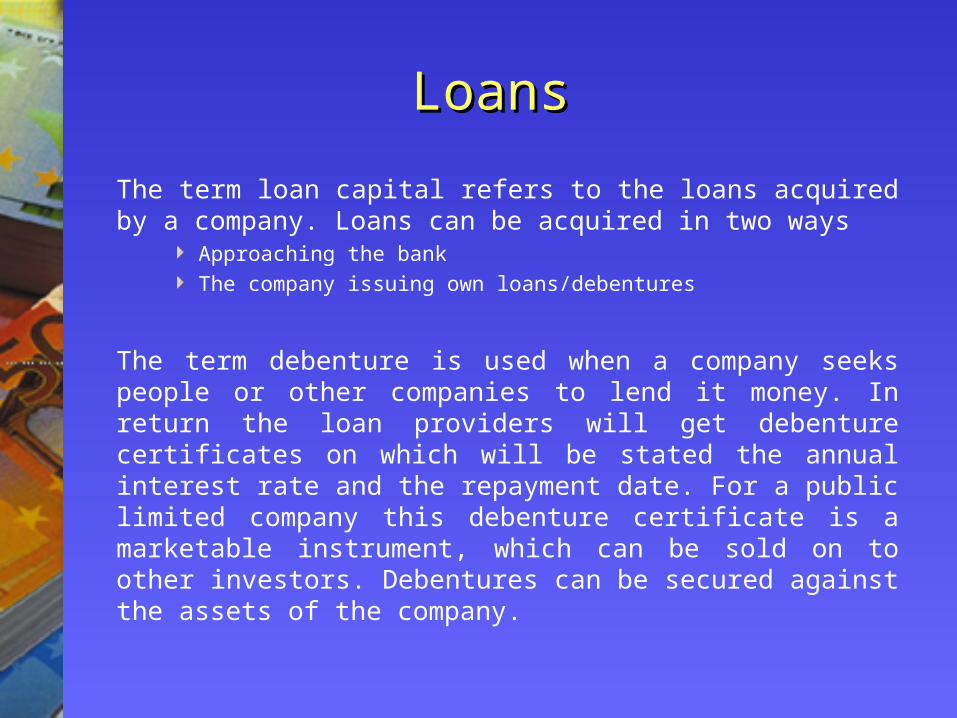

LoansLoans

The term loan capital refers to the loans acquired by a company. Loans can be acquired in two ways

Approaching the bankThe company issuing own loans/debentures

The term debenture is used when a company seeks people or other companies to lend it money. In return the loan providers will get debenture certificates on which will be stated the annual interest rate and the repayment date. For a public limited company this debenture certificate is a marketable instrument, which can be sold on to other investors. Debentures can be secured against the assets of the company.

Final accountsFinal accounts

Example – appropriation accountExample – appropriation account

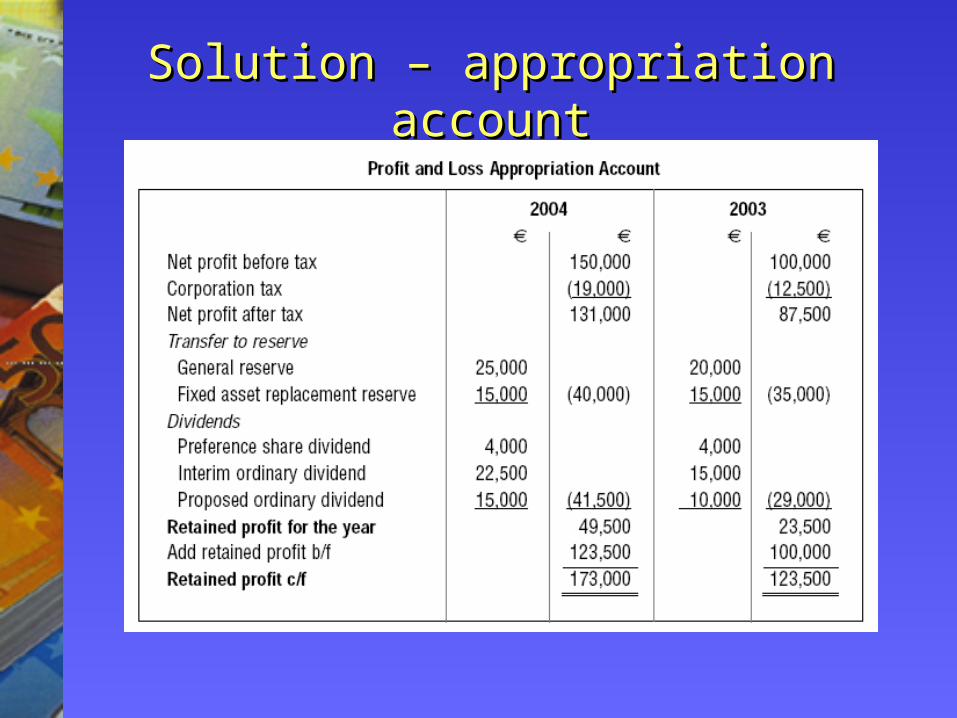

The following details are from the accounts of a hotel company which is financed through a mixture of 200,000 ordinary shares of €1 each and 100,000 8 per cent preference shares of €0.50 each. You are required to prepare an appropriation account for two years.

2004 €

2003 €

Net profit before tax Transfer to general reserveTransfer to fixed asset replacement reserveCorporation tax Ordinary dividend Interim ProposedRetained profit brought forward from last year

150,000 25,000 15,000 19,000 22,500 15,000

100,000 20,000 15,000 12,500 15,000 10,000100,000

Solution – appropriation accountSolution – appropriation account

Comprehensive exampleComprehensive exampleThe trial balance on the right has been extracted at the close of business on 30 June 2005 for Cool Sportswear Ltd a chain of retail sports outlets.

Required

a) Prepare Cool Sportswear Ltd’s Trading Account, Profit & Loss Account and Appropriation Account for the year ended 30 June 2005.

b) Prepare Cool Sportswear Ltd’s Balance Sheet as at 30 June 2005.

Small Companies

Medium Companies

Balance sheet totals not exceeding €1.9m €7.62

Turnover not exceeding €3.81m €15.24

Number of employees not exceeding 50 250

Published accountsPublished accounts

The Company’s (Amendment Act) 1986 is the principle act governing the publication of accounts in Ireland and it derives from the EU Fourth Directive.

All companies in Ireland (both public and private) are required to publish their accounts in accordance with the company’s acts and accounting standards.

Every company has a legal duty to deliver to the Registrar of Companies a copy of its financial statements.

Small and medium sized private companies do not have to publish as much information as large companies.

Terminology in published Terminology in published financial statementsfinancial statements

The published accounts use terminology prescribed by law. The regulatory framework has undergone significant change in recent times. Currently new terminology is being implemented.

There are different timeframes involved in the implementation of the new requirements depending on whether the accounts are those of a public or private company.

Terminology in published Terminology in published financial statementsfinancial statements

Internal use Publication by Plc prior to 1/1/2005by Ltd prior to 1/1/2007

Publication by Plc post 1/1/2005by Ltd post 1/1/2007

Profit & Loss Account Profit & Loss Account Income Statement

Sales Turnover Revenue

Stock (opening & closing) Stock (opening & closing) Inventory (opening & closing)

Net profit Operating profit Profit from operations

Fixed assets Fixed assets Non-current assets

Debtors Debtors Receivables

Current liabilities Creditors: amounts falling due within one year

Current liabilities

Long-term liabilities Creditors: amounts falling due after more than one year

Non-current liabilities

Working capital Net current assets Not shown

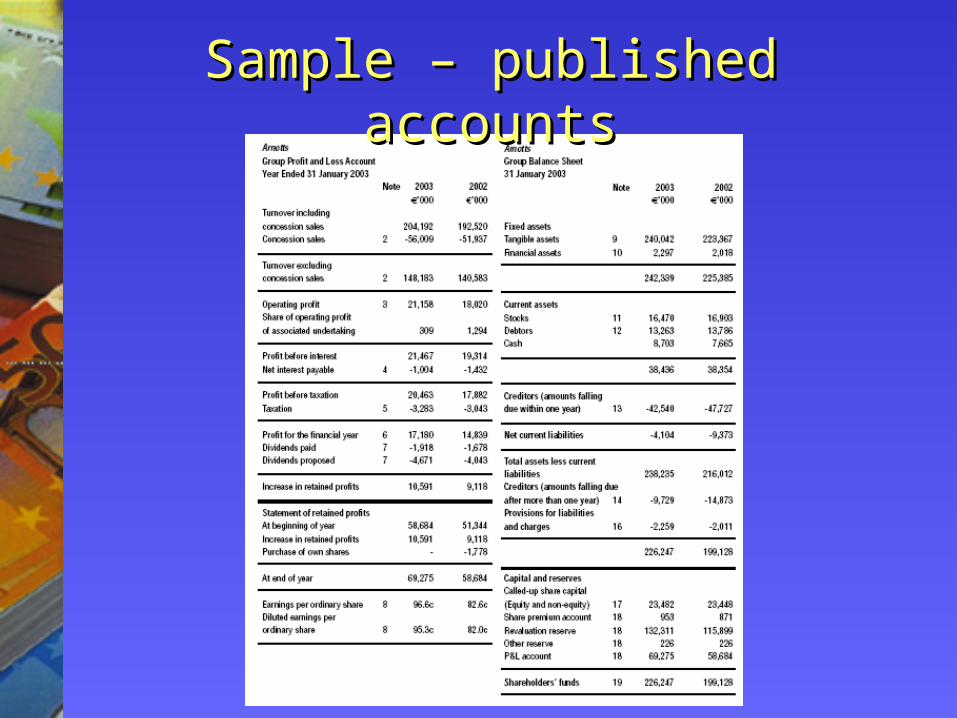

Sample – published accountsSample – published accounts

Financial Reporting Standard 3Financial Reporting Standard 3

Financial Reporting Standard 3 was issued to “aid users in understanding the performance achieved by a reporting entity in a period, and to assist them in forming a basis for their assessment of future results and cash flows”.

Part of the requirements of FRS 3 is to:Show the results of continued and discontinued operations.Provide a statement of total recognised gains and losses.Provide a statement of reconciliation of movement in shareholders funds.