COMMUNITY AGING AND RETIREMENT SERVICES, INC. Hudson, … rpts/2011... · 2019-11-03 · Community...

30

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Hudson, Florida Statements of Financial Position at December 31, 2011 and 2010 and Statements of Activities, Cash Flows and Functional Expenses for the Years Then Ended and Supplementary Information for 2011 (Together with Independent Auditors' Report)

Transcript of COMMUNITY AGING AND RETIREMENT SERVICES, INC. Hudson, … rpts/2011... · 2019-11-03 · Community...

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Hudson, Florida Statements of Financial Position at December 31, 2011 and 2010 and Statements of Activities, Cash Flows and Functional Expenses for the Years Then Ended and Supplementary Information for 2011 (Together with Independent Auditors' Report)

Unqualified Opinion on the Financial Statements and Supplementary Schedules Independent Auditors' Report Community Aging and Retirement Services, Inc. Hudson, Florida:

We have audited the accompanying statements of financial position of Community Aging and Retirement Services, Inc. (the "Company") at December 31, 2011 and 2010 the related statements of activities, cash flows and functional expenses for the years then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Company at December 31, 2011 and 2010, and the changes in its net assets and its cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated May 7, 2012 on our

consideration of the Company's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be read in conjunction with this report in considering the results of our audit.

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying schedule of expenditures of federal awards and state financial assistance for 2011 is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and Chapter 10.650, Rules of the Auditor General, and is not a required part of the basic financial statements. In addition, the accompanying schedule of functional expenses as required by Department of Elder Affairs (DOEA) for 2011 is presented for purposes of additional analysis and is not a required part of the basic financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole. HACKER, JOHNSON & SMITH PA Tampa, Florida May 7, 2012

2

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Statements of Financial Position

December 31, 2011 2010

Assets Current assets:

Cash $ 47,563 80,517 Beneficial interest in assets held by Community Foundation 84,624 72,579 Accounts receivable 401,897 403,490 Unconditional promises to give 1,794,434 1,909,295 Prepaid assets and deposits 24,305 19,543

Total current assets 2,352,823 2,485,424

Property, net 2,212,515 2,492,031

Total assets $ 4,565,338 4,977,455

Liabilities and Net Assets Current liabilities:

Current portion of notes payable 121,552 108,247 Accounts payable 335,869 239,507 Accrued expenses and other liabilities 135,866 129,422

Total current liabilities 593,287 477,176

Notes payable, noncurrent portion 921,935 1,044,125

Total liabilities 1,515,222 1,521,301 Net assets (deficit):

Unrestricted: Property 323,186 324,356 Other (89,132) 8,665

Total unrestricted 234,054 333,021

Temporarily restricted:

Grants and contracts 1,647,455 1,716,836 Donations 4,045 4,957 Property 1,164,562 1,401,340

Total temporarily restricted 2,816,062 3,123,133

Total net assets 3,050,116 3,456,154

Total liabilities and net assets $ 4,565,338 4,977,455 See accompanying Notes to Financial Statements.

3

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Statement of Activities Year Ended December 31, 2011

Temporarily Unrestricted Restricted Total

Revenues and Support: Grants and contracts $ 2,103,252 1,628,672 3,731,924 Medicare 1,186,147 - 1,186,147 Fund raising and donations 223,474 - 223,474 Centers activities 310,150 - 310,150 Local cash match 60,000 - 60,000 Assessed fees 321,654 - 321,654 Interest and other 226,096 - 226,096 Reclassification of net assets from unrestricted to temporarily restricted (84,624) 84,624 -

Net assets released from restrictions due to satisfaction of program and donor restrictions 2,020,367 (2,020,367) -

Total revenues and support 6,366,516 (307,071) 6,059,445

Expenses: Program Services:

Adult day care 443,904 - 443,904 Care managed services 3,263,398 - 3,263,398 Medicare skilled care 996,782 - 996,782 Senior centers 958,540 - 958,540 Senior health clinic 167,963 - 167,963

Supporting Services:

General administration costs 626,532 - 626,532 Development/fund raising 8,364 - 8,364

Total expenses 6,465,483 - 6,465,483

Decrease in net assets (98,967) (307,071) (406,038) Net assets at beginning of year 333,021 3,123,133 3,456,154 Net assets at end of year $ 234,054 2,816,062 3,050,116 See accompanying Notes to Financial Statements.

4

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Statement of Activities Year Ended December 31, 2010

Temporarily Permanently Unrestricted Restricted Restricted Total

Revenues and Support: Grants and contracts $ 2,020,220 1,761,639 - 3,781,859 Medicare 1,224,207 - - 1,224,207 Fund raising and donations 158,895 - - 158,895 Centers activities 288,352 - - 288,352 Local cash match 40,512 - - 40,512 Assessed fees 278,921 - - 278,921 Interest and other 232,576 - - 232,576 Release of permanent restriction 328,811 - (328,811) -

Net assets released from restrictions due to satisfaction of program and donor restrictions 1,752,419 (1,752,419) - -

Total revenues and support 6,324,913 9,220 (328,811) 6,005,322

Expenses: Program Services:

Adult day care 435,947 - - 435,947 Care managed services 3,112,543 - - 3,112,543 Medicare skilled care 881,606 - - 881,606 Senior centers 739,628 - - 739,628 Senior health clinic 160,713 - - 160,713

Supporting Services:

General administration costs 653,948 - - 653,948 Development/fund raising 29,853 - - 29,853

Total expenses 6,014,238 - - 6,014,238

Increase (decrease) in net assets 310,675 9,220 (328,811) (8,916) Net assets at beginning of year 22,346 3,113,913 328,811 3,465,070 Net assets at end of year $ 333,021 3,123,133 - 3,456,154 See accompanying Notes to Financial Statements.

5

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Statements of Cash Flows

Year Ended December 31, 2011 2010

Cash flows from operating activities: Decrease in net assets $(406,038) (8,916) Adjustments to reconcile decrease in net assets

to net cash provided by (used in) operating activities: Depreciation 127,383 155,483 Loss on disposal of property 202,309 - Decrease (increase) in unconditional promises to give 114,861 (107,456) Decrease (increase) in accounts receivable 1,593 (207,715) Increase in beneficial interest in assets held by others (12,045) (57,357) Increase in prepaid assets and deposits (4,762) (2,786) Increase in accounts payable 96,362 39,382 Increase in accrued expenses and other liabilities 6,444 15,439 Net cash provided by (used in) operating activities 126,107 (173,926) Cash flows from investing activity-

Net (purchase) sale of property (50,176) 94,021 Cash flows from financing activities:

Principal payments on notes payable (108,885) (51,475) Net change in line of credit - 103,118 Net cash (used in) provided by financing activities (108,885) 51,643 Net decrease in cash (32,954) (28,262) Cash at beginning of year 80,517 108,779 Cash at end of year $ 47,563 80,517 Supplemental cash flow information:

Cash paid during the year for interest $ 69,621 90,587

Noncash investing and financing transactions: Principal payment on note payable in connection with the sale of property $ - 387,513 Proceeds from note payable used to pay off line of credit $ - 393,118

See accompanying Notes to Financial Statements.

6

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Statement of Functional Expenses Year Ended December 31, 2011

Program Services Supporting Services Adult Care Medicare Senior General Development/ Day Managed Skilled Senior Health Administration Fund Total Care Services Care Centers Clinic Total Costs Raising Total Expenses

Personnel $ 295,710 1,907,685 637,248 160,633 111,799 3,113,075 411,656 - 411,656 3,524,731 Travel 9,161 72,673 44,619 8,330 7,074 141,857 5,651 - 5,651 147,508 Occupancy 44,250 95,131 28,054 67,335 3,244 238,014 10,994 - 10,994 249,008 Communications and postage 8,103 36,905 27,075 17,618 5,806 95,507 32,598 870 33,468 128,975 Printing and supplies 2,213 17,365 7,063 9,729 2,121 38,491 50,287 2,385 52,672 91,163 Maintenance and repair 5,545 13,985 10,908 18,292 2,072 50,802 18,000 - 18,000 68,802 Contract services 31,598 962,765 172,296 8,781 6,058 1,181,498 22,081 1,542 23,623 1,205,121 Special events 113 699 - 13,019 - 13,831 - 2,627 2,627 16,458 Advertising 1,253 6,539 18,107 4,704 361 30,964 11,113 780 11,893 42,857 Insurance 4,031 7,441 3,138 14,661 780 30,051 28,209 - 28,209 58,260 Program supplies 38,871 123,166 41,599 72,591 2,441 278,668 - 102 102 278,770 Utilities - 3,434 - 46,114 11,667 61,215 - - - 61,215 Professional fees - - 2,600 - - 2,600 22,016 - 22,016 24,616 Other costs 3,056 12,411 4,075 403,883 3,206 426,631 13,927 58 13,985 440,616 Depreciation - 3,199 - 112,850 11,334 127,383 - - - 127,383 Total expenses $ 443,904 3,263,398 996,782 958,540 167,963 5,830,587 626,532 8,364 634,896 6,465,483 See accompanying Notes to Financial Statements.

7

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Statement of Functional Expenses Year Ended December 31, 2010

Program Services Supporting Services Adult Care Medicare Senior General Development/ Day Managed Skilled Senior Health Administration Fund Total Care Services Care Centers Clinic Total Costs Raising Total Expenses

Personnel $ 287,152 1,921,216 496,779 158,565 119,733 2,983,445 403,082 - 403,082 3,386,527 Travel 7,333 66,771 38,134 891 6,119 119,248 6,867 - 6,867 126,115 Occupancy 30,330 100,299 16,078 44,012 2,462 193,181 26,107 - 26,107 219,288 Communications and postage 5,149 45,452 19,403 17,260 5,550 92,814 22,115 815 22,930 115,744 Printing and supplies 2,152 20,010 9,760 10,257 1,834 44,013 67,306 2,069 69,375 113,388 Maintenance and repair 4,910 9,681 44 26,127 1,059 41,821 18,439 - 18,439 60,260 Contract services 52,978 820,610 200,685 27,415 6,000 1,107,688 18,755 64 18,819 1,126,507 Special events - - - 450 - 450 - 25,982 25,982 26,432 Advertising 104 6,295 5,003 2,234 1,020 14,656 10,778 800 11,578 26,234 Insurance 3,600 7,019 5,281 16,417 780 33,097 45,741 - 45,741 78,838 Program supplies 40,269 70,474 85,146 79,532 1,082 276,503 - 123 123 276,626 Utilities - 278 144 75,659 3,134 79,215 64 - 64 79,279 Professional fees - - 2,600 - - 2,600 26,191 - 26,191 28,791 Other costs 1,970 5,392 2,549 175,830 482 186,223 8,503 - 8,503 194,726 Depreciation - 39,046 - 104,979 11,458 155,483 - - - 155,483 Total expenses $ 435,947 3,112,543 881,606 739,628 160,713 5,330,437 653,948 29,853 683,801 6,014,238 See accompanying Notes to Financial Statements.

8

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements At December 31, 2011 and 2010 and for the Years Then Ended (1) Summary of Significant Accounting Policies

Operations. Community Aging and Retirement Services, Inc. ("CARES" or "Company") is a tax exempt, Florida not-for-profit corporation organized for the purpose of development, delivery and coordination of high quality programs and services which are responsive to the needs of adults and older persons residing in West Central Florida. CARES conducts its operations through three program offices, five senior centers, two adult day care centers and one senior health clinic. Management has evaluated events occurring subsequent to the balance sheet date through May 7, 2012, which is the date the financial statements were available to be issued, determining no events require additional disclosure in these financial statements.

Estimates. The preparation of financial statements in conformity with accounting principles

generally accepted in the United States of America ("GAAP") requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Financial Statement Presentation. GAAP requires the Company to report information regarding

its financial position and activities according to three classes of net assets: unrestricted net assets, temporarily restricted net assets, and permanently restricted net assets.

Grants, Contracts and Contributions. GAAP requires contributions received, including

unconditional promises to give, to be recognized as revenue in the period received at their fair values. All of the Company's grants and contracts are conditional promises to give which are accounted for as unconditional promises to give because the possibility of the conditions not being satisfied is remote. GAAP also requires not-for-profit organizations to distinguish between contributions received that increase permanently restricted net assets, temporarily restricted net assets and unrestricted net assets. It also requires recognition of the expiration of donor imposed restrictions in the period in which the restrictions expire. Therefore, the Company reports grants, contracts, gifts of cash and other assets as restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions.

(continued)

9

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements, Continued (1) Summary of Significant Accounting Policies, Continued

Unconditional Promises to Give. Contributions, which include grants and contracts, are recognized when the donor makes a promise to give to the Company that is, in substance, unconditional. Contributions that are restricted by the donor are reported as increases in unrestricted net assets if the restrictions expire in the fiscal year in which the contributions are recognized. All other donor-restricted contributions are reported as increases in temporarily or permanently restricted net assets depending on the nature of the restrictions. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets. Substantially all of the unconditional promises to give as of December 31, 2011 will be received in 2012 and management believes all such amounts are collectable (see Note 3).

Property. Property is stated at cost when purchased or the estimated fair market value at the

time of receipt, if donated. Depreciation of assets is computed using the straight-line method over the estimated useful lives of the assets, ranging from five to ten years for equipment and thirty years for buildings. Leasehold improvements are amortized over the shorter of the estimated useful life of the asset or the lease term.

The Company reports gifts of and grants and contracts used to purchase land, building, and equipment as unrestricted support unless explicit donor stipulations specify how the assets must be used. Gifts of and grants and contracts used to purchase long lived assets with explicit restrictions that specify how the assets are to be used and gifts, grants and contracts of cash or other assets that must be used to acquire long-lived assets are reported as restricted support. Absent explicit donor stipulations about how long those long-lived assets must be maintained, the Company reports expirations of donor restrictions when the donated or acquired long-lived assets are placed in service.

Property acquired with governmental grant and contract funds is considered to be owned by the Company while used in the programs; however, the Federal, state or a city government has a reversionary interest in the property. The retirement of this property as well as the ownership of any proceeds therefrom is also subject to government regulations. All property, except certain land, acquired with governmental grant and contract funds is recorded as temporarily restricted net assets. Certain land was recorded as a permanently restricted net asset until its sale in 2010 (see Note 4).

Functional Expenses. Expenses are charged directly to program or supporting services based

on specific identification. Indirect expenses have been allocated based on direct expenditures incurred in specific programs.

Income Taxes. The Company is incorporated as a not-for-profit organization, exempt from

federal income taxes under Section 501(c)(3) of the Internal Revenue Code. In addition, it has been determined by the Internal Revenue Service that the Company is not a private foundation under Section 509(a) of the Code.

Advertising. The Company expenses all media advertising as incurred.

(continued)

10

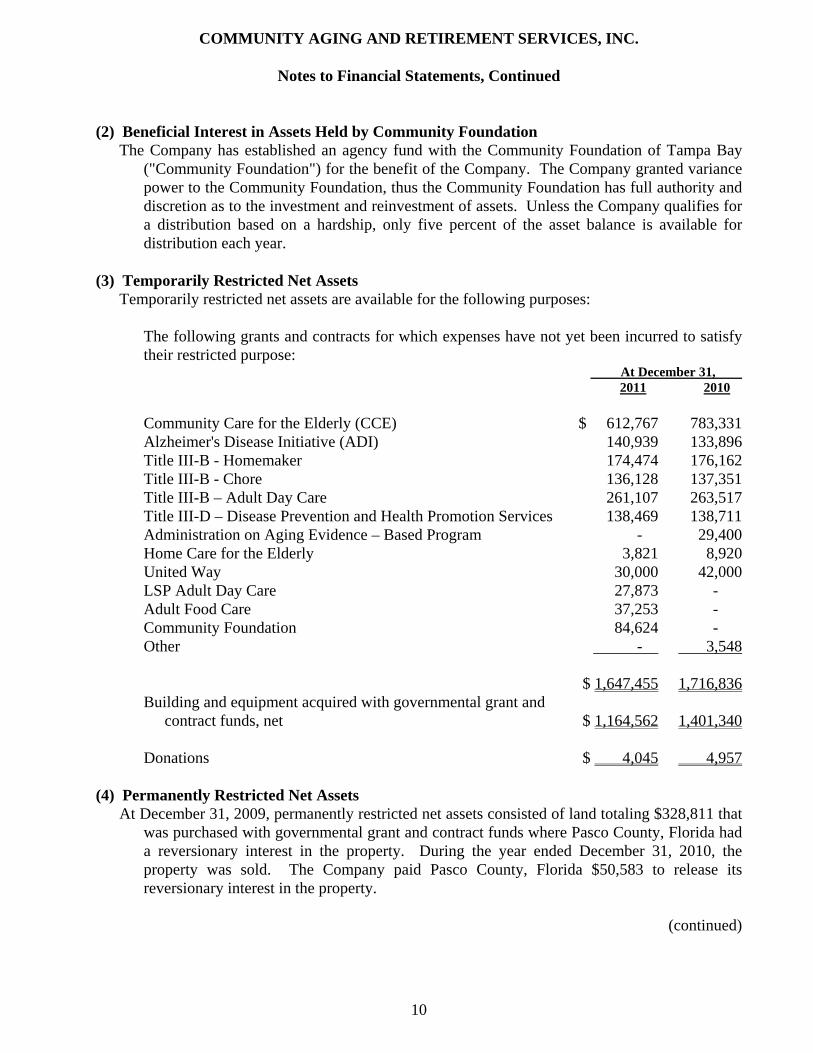

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements, Continued (2) Beneficial Interest in Assets Held by Community Foundation

The Company has established an agency fund with the Community Foundation of Tampa Bay ("Community Foundation") for the benefit of the Company. The Company granted variance power to the Community Foundation, thus the Community Foundation has full authority and discretion as to the investment and reinvestment of assets. Unless the Company qualifies for a distribution based on a hardship, only five percent of the asset balance is available for distribution each year.

(3) Temporarily Restricted Net Assets

Temporarily restricted net assets are available for the following purposes:

The following grants and contracts for which expenses have not yet been incurred to satisfy their restricted purpose:

At December 31, 2011 2010

Community Care for the Elderly (CCE) $ 612,767 783,331 Alzheimer's Disease Initiative (ADI) 140,939 133,896 Title III-B - Homemaker 174,474 176,162 Title III-B - Chore 136,128 137,351 Title III-B – Adult Day Care 261,107 263,517 Title III-D – Disease Prevention and Health Promotion Services 138,469 138,711 Administration on Aging Evidence – Based Program - 29,400 Home Care for the Elderly 3,821 8,920 United Way 30,000 42,000 LSP Adult Day Care 27,873 - Adult Food Care 37,253 - Community Foundation 84,624 -

Other - 3,548

$ 1,647,455 1,716,836 Building and equipment acquired with governmental grant and

contract funds, net $ 1,164,562 1,401,340

Donations $ 4,045 4,957

(4) Permanently Restricted Net Assets At December 31, 2009, permanently restricted net assets consisted of land totaling $328,811 that

was purchased with governmental grant and contract funds where Pasco County, Florida had a reversionary interest in the property. During the year ended December 31, 2010, the property was sold. The Company paid Pasco County, Florida $50,583 to release its reversionary interest in the property.

(continued)

11

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements, Continued (5) Release of Temporarily Restricted Net Assets

The net assets released from grant and contract restrictions by incurring expenses satisfying the restricted purpose were as follows:

Year Ended December 31, 2011 2010

CCE $ (827,246) (837,384) Title III-B (593,419) (594,991) Title III-D (138,469) (138,711) ADI (129,637) (140,600) United Way (42,000) (12,000) Home Care for the Elderly (13,653) (9,267) Other (38,253) (15,173) Decrease (1,782,677) (1,748,126)

The decrease in the temporarily restricted net assets of property is due to the following:

Purchases of property 14,027 - Disposal, retirement and sale of property (202,309) (321,619) Decrease in note payable 22,842 414,318 Depreciation (71,338) (94,337) Decrease (236,778) (1,638) Release of donor-imposed restrictions (912) (2,655) Net assets released from restrictions $(2,020,367) (1,752,419) (continued)

12

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements, Continued (6) Property, Net

Property and related accumulated depreciation and amortization consisted of the following:

At December 31, 2011 2010

Land $ 250,000 250,000 Buildings 2,338,135 2,447,907 Leasehold improvements 103,849 496,743 Furniture and equipment 256,794 249,000 Vehicles 100,047 90,575

Total, at cost 3,048,825 3,534,225

Less accumulated depreciation and amortization (836,310) (1,042,194)

$ 2,212,515 2,492,031

(continued)

13

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements, Continued (7) Notes Payable Notes payable are as follows:

At December 31, 2011 2010

Mortgage note payable due to a bank. The note bears interest at 6.00% with monthly principal and interest payments of $3,909 and a balloon payment due on June 5, 2014. The mortgage note is collateralized by a first mortgage note on the Crescent Service Center, which has a net book value of $1,001,663 at December 31, 2011. $ 408,235 431,077

Mortgage note payable due to a bank. The note bears interest at 6.23%

with monthly principal and interest payments of $3,280 and a balloon payment due on March 20, 2013. The mortgage note is collateralized by a first mortgage on the Rao Musunuru MD Senior Enrichment Center, which has a net book value of $1,019,590 at December 31, 2011. This note along with the promissory note below were refinanced in January 2012 and consolidated. 316,532 335,259

Promissory note due to a bank. The note bears interest at 6.35% with

monthly principal and interest payments of $8,024. All principal and interest is due September 2, 2015. The note is collateralized by all deposit accounts, personal property and equipment of the Company. 318,720 386,036

Total 1,043,487 1,152,372 Less current portion of notes payable 121,552 108,247 Notes payable, noncurrent portion $ 921,935 1,044,125

(continued)

14

COMMUNITY AGING AND RETIREMENT SERVICES, INC. Notes to Financial Statements, Continued (7) Notes Payable, Continued

The annual principal payments due on these notes payable (as refinanced in January 2012) are as follows:

Year Ending December 31, Amount

2012 $ 121,552 2013 404,003 2014 449,615 2015 68,317 $ 1,043,487

The mortgage note with a balance of $316,532 at December 31, 2011 and the promissory note with a balance of $318,720 at December 31, 2011 were consolidated and refinanced in January 2012. The terms of the new note call for monthly principal and interest payments of $4,387 with an interest rate of 4.75% and a balloon payment due on January 10, 2017. The principal balance of the new note was $675,000. The Company received approximately $67,000 in cash at closing. The cash received at closing included a $50,000 draw on the new line of credit discussed in Note 8.

(8) Line of Credit

At December 31, 2009, the Company had a $400,000 line of credit with a financial institution. The line of credit bore interest at prime -1/4% and was due on demand. The line of credit was collateralized by substantially all of the Company's assets. At December 31, 2009, the Company had $290,000 outstanding under this line of credit which was paid off during the year ended December 31, 2010.

On January 10, 2012 the Company entered into a new $50,000 line of credit with a financial

institution which bears interest at the Wall Street Journal Prime rate plus two percent (5.25% at January 10, 2012).

(9) In-Kind Contributed Services

During the years ended December 31, 2011 and 2010, the Company received the following value of in-kind contributed services that do not meet the requirements for recognition in the financial statements under GAAP but do qualify for local matching under federal and state grants.

Year Ended December 31,

Grant 2011 2010

Title III-D Senior Health Promotion and Medication Management $ 258,913 279,239 CCE 48,430 31,039 Title III-B Adult Day Care 26,260 22,668

$ 333,603 332,946

15

Schedule I COMMUNITY AGING AND RETIREMENT SERVICES, INC. Schedule of Expenditures of Federal Awards and

State Financial Assistance For the Year Ended December 31, 2011

CFDA

Federal/State Agency/Pass-Through CSFA Contract Grant Entity Federal Program/State Project Number Number Expenditures Federal Awards Passed through Area Agency on Aging of Pasco-Pinellas, Inc.:

Medicaid Waiver 93.778 - $ 647,745 Title III-B 93.044 EA111-CARES 497,689

Title III-D 93.043 ED011-CARES 138,469 AoA Evidenced Based Grant 93.048 EB010-CARES 33,792 Adult Food Care Program 10.558 Y1111 24,479 Adult Food Care Program 10.558 Y2111 5,095

Total expenditures of Federal awards $ 1,347,269 State Projects Department of Elder Affairs Passed through the State of Florida Department of Elder Affairs and the Area Agency on Aging of Pasco-Pinellas, Inc.: Medicaid Waiver - - $ 325,722 Home Care for the Elderly 65.001 EH010-CARES 13,653 Home Care for the Elderly 65.001 EH011-CARES 18,547 Community Care for the Elderly 65.010 EC011-CARES 929,137 Community Care for the Elderly 65.010 EC010-CARES 827,246 Alzheimer's Disease Initiative 65.004 EZ010-CARES 129,637 Alzheimer's Disease Initiative 65.004 EZ011-CARES 121,022 Title III-B Homemaker (LSP) 65.001 EL010-CARES-2011 23,506 Title III-B Chore (LSP) 65.001 EL010-CARES-2011 26,735 Title III-B Adult Day Care (LSP) 65.001 EL010-CARES-2011 45,489 Adult Day Care (LSP) 65.009 EL011-CARES 5,563 Total State Financial Assistance $ 2,466,257

16

Schedule I COMMUNITY AGING AND RETIREMENT SERVICES, INC. Schedule of Expenditures of Federal Awards and

State Financial Assistance, Continued For the Year Ended December 31, 2011 Note A - Basis of Presentation The accompanying schedule of expenditures of federal awards and state financial assistance includes the federal and state grant activity of Community Aging and Retirement Services, Inc. and is presented on the same basis as stated in Note 1, Summary of Significant Accounting Policies, in the accompanying combined financial statements. The information in this schedule is presented in accordance with the requirements of OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and Rule 10.656 of the Auditor General.

Summary Schedule of Prior Audit Findings May 7, 2012

There were no prior audit findings or questioned costs relative to Federal awards or State projects identified in the audit of Community Aging and Retirement Services, Inc. for the year ended December 31, 2010.

Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards The Board of Directors Community Aging and Retirement Services, Inc. Hudson, Florida:

We have audited the financial statements of Community Aging and Retirement Services, Inc. (the "Company"), as of and for the year ended December 31, 2011, and have issued our report thereon dated May 7, 2012. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Internal Control Over Financial Reporting

Management of the Company is responsible for establishing and maintaining effective internal control over financial reporting. In planning and performing our audit, we considered the Company's internal control over financial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the Company's internal control over financial reporting.

A deficiency in internal control exists when the design or operation of a control does not allow

management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis.

Our consideration of internal control over financial reporting was for the limited purpose

described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over financial reporting that might be deficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over financial reporting that we consider to be material weaknesses, as defined above.

The Board of Directors Community Aging and Retirement Services, Inc. Page Two Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Company's financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

This report is intended for the information of the Board of Directors, management and federal awarding agencies and pass-through entities and is not intended to be and should not be used by anyone other than these specified parties.

HACKER, JOHNSON & SMITH PA Tampa, Florida May 7, 2012

Independent Auditors' Report on Compliance with Requirements That Could Have a Direct and Material Effect on Each Major Federal

Program and State Project and on Internal Control Over Compliance in Accordance with OMB Circular A-133

The Board of Directors Community Aging and Retirement Services, Inc. Hudson, Florida: Compliance

We have audited the compliance of Community Aging and Retirement Services, Inc. (the "Company") with the types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133 Compliance Supplement and the requirements described in the Executive Office of the Governor's State Projects Compliance Supplement, that could have a direct and material effect on each of the Company's major federal programs and state projects for the year ended December 31, 2011. The Company's major federal programs and state projects are identified in the summary of auditors' results section of the accompanying schedule of findings and questioned costs. Compliance with the requirements of laws, regulations, contracts and grants applicable to each of its major federal programs and state projects is the responsibility of the Company's management. Our responsibility is to express an opinion on the Company's compliance based on our audit.

We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and Chapter 10.650, Rules of the Auditor General. Those standards, OMB Circular A-133 and Chapter 10.650, Rules of the Auditor General, require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program or state project occurred. An audit includes examining, on a test basis, evidence about the Company's compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Our audit does not provide a legal determination on the Company's compliance with those requirements.

In our opinion, the Company complied, in all material respects, with the requirements referred to above that could have a direct and material effect on each of its major federal programs and state projects for the year ended December 31, 2011.

The Board of Directors Community Aging and Retirement Services, Inc. Page Two Internal Control Over Compliance

Management of the Company is responsible for establishing and maintaining effective internal control over compliance with requirements of laws, regulations, contracts and grants applicable to federal programs and state projects. In planning and performing our audit, we considered the Company's internal control over compliance with requirements that could have a direct and material effect on a major federal program or state project in order to determine our auditing procedures for the purpose of expressing our opinion on compliance and to test and report on internal control over compliance in accordance with OMB Circular A-133 and Chapter 10.650, Rules of the Auditor General, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of the Company's internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control

over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program or state project on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program or state project will not be prevented, or detected and corrected, on a timely basis.

Our consideration of internal control over compliance was for the limited purpose described in

the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be deficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses, as defined above.

This report is intended for the information of the Board of Directors, management, and federal and state awarding agencies and pass-through entities and is not intended to be and should not be used by anyone other than these specified parties.

HACKER, JOHNSON & SMITH PA Tampa, Florida May 7, 2012

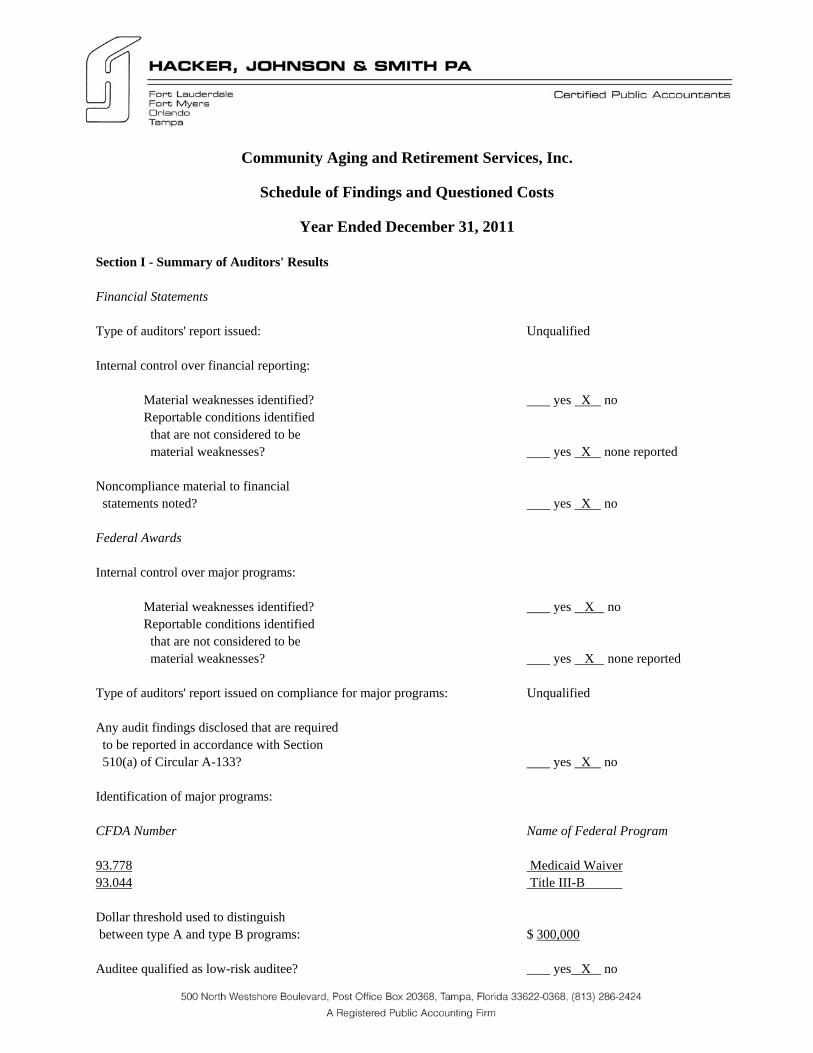

Community Aging and Retirement Services, Inc. Schedule of Findings and Questioned Costs Year Ended December 31, 2011 Section I - Summary of Auditors' Results Financial Statements Type of auditors' report issued: Unqualified Internal control over financial reporting: Material weaknesses identified? yes X no Reportable conditions identified

that are not considered to be material weaknesses? yes X none reported

Noncompliance material to financial statements noted? yes X no Federal Awards Internal control over major programs: Material weaknesses identified? yes X no Reportable conditions identified

that are not considered to be material weaknesses? yes X none reported

Type of auditors' report issued on compliance for major programs: Unqualified Any audit findings disclosed that are required to be reported in accordance with Section 510(a) of Circular A-133? yes X no Identification of major programs: CFDA Number Name of Federal Program 93.778 Medicaid Waiver93.044 Title III-B Dollar threshold used to distinguish between type A and type B programs: $ 300,000 Auditee qualified as low-risk auditee? yes X no

Page Two State Awards Internal control over major state projects: Material weaknesses identified? yes X no Reportable conditions identified

that are not considered to be material weaknesses? yes X none reported

Type of auditors' report issued on compliance for major state projects: Unqualified Any audit findings disclosed that are required to be reported under Rule 10.656? yes X no Identification of major projects: CSFA Number Name of State Program 65010 Community Care for the Elderly - Medicaid Waiver Dollar threshold used to distinguish between type A and type B programs: $ 300,000 Items to be reported in a management letter yes X no Section II – Financial Statement Findings No reportable conditions, material weaknesses, or instances of noncompliance relating to the combined financial statements were identified that are required to be reported in accordance with paragraphs 5.18 through 5.20 of Government Auditing Standards or auditing standards generally accepted in the United States of America. Section III – Federal and State Award Findings and Questioned Costs

No audit findings were identified that are required to be reportable by section 510(a) of Circular A-133 or under Rule 10.656 of the Auditor General. If you have any questions please call Kevin Beerman at (813) 282-7229. Very truly yours, HACKER, JOHNSON & SMITH PA Kevin J. Beerman KJB/yea