Common Schools Average Annual Enrollment (FTE)

53

Forecast Contact: Paula Moore 360-664-9376 [email protected] Common Schools Enrollment Caseload Forecast Council February 11, 2022 Common Schools Average Annual Enrollment (FTE) The Common School enrollment forecast includes K-12 grade level enrollments, Running Start enrollments, the University of Washington Transition Program, Open Door Dropout Reengagement Program, summer school, and private and home-schooled students receiving ancillary services from public schools. Forecast Comparisons (Academic Year Averages FTEs) The February 2022 forecast is, on average, 1,674 students or 0.2 percent lower than the November 2021 forecast for the 2021-23 Biennium. Academic Year Nov-21 Forecast Feb-22 Forecast Nov to Feb Difference Percent Difference 2021-22 1,060,406 1,059,125 -1,281 -0.1% 2022-23 1,067,806 1,065,739 -2,067 -0.2% 1

Transcript of Common Schools Average Annual Enrollment (FTE)

Forecast Contact:

Paula Moore 360-664-9376

Common Schools Enrollment Caseload Forecast Council

February 11, 2022

Common Schools Average Annual Enrollment (FTE)

The Common School enrollment forecast includes K-12 grade level enrollments, Running

Start enrollments, the University of Washington Transition Program, Open Door Dropout

Reengagement Program, summer school, and private and home-schooled students receiving

ancillary services from public schools.

Forecast Comparisons (Academic Year Averages FTEs)

The February 2022 forecast is, on average, 1,674 students or 0.2 percent lower than the

November 2021 forecast for the 2021-23 Biennium.

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 1,060,406 1,059,125 -1,281 -0.1%

2022-23 1,067,806 1,065,739 -2,067 -0.2%

1

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast (FTEs)

Actuals for Common Schools are tracking on par with the November forecast.

Academic Year Caseload Change (FTEs)

In 2020-21, Common Schools enrollment declined year-over-year by 3.7 percent due to concerns

about COVID-19 and remote/hybrid schooling. Some families opted for home-based instruction,

private school instruction, and delayed their child’s enrollment in kindergarten. Additional

families may have relocated out-of-state. Finally, immigrants moving into Washington state

significantly dropped.

In 2021-22, total enrollment remained flat. Kindergarten and 1st grade public school enrollment

rates improved from those of the prior year, though not to pre-pandemic rates. Further, year-

over-year declines occurred in grades 4-8 as well as grade 10, Running Start and Open Door. The

forecast assumes a shift in the enrollment trajectory and slower growth trends than occurred pre-

pandemic. Note, around 2009, with the great recession, birth rates declined resulting in smaller

age cohorts. The babies of 2009 are now in the 6th and 7th grade. The overall future growth trends

will be lower as these smaller age cohorts progress through the K-12 system.

Risks to the Forecast

The risks to the Common Schools enrollment forecast (K-12, Open Door, and Running Start) are

high. Demand for Common School enrollment, private school, and home-based instruction are

highly influenced by the state’s economic conditions, demand for labor, and net in-state

migration. Additional factors adding uncertainty: (1) remote-work providing opportunities for

families to relocate out-of-state and (2) immigration, both US policy and backlog of VISA

applications.

Nov-21 Percent

Forecast Actual Variance Variance

Nov-21 1,058,795 1,059,164 369 0.0%

Dec-21 1,057,248 1,057,106 -142 0.0%

Jan-22 1,055,075 1,054,075 -1,000 -0.1%

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-14 1,002,769

2014-15 1,015,076 12,306 1.2%

2015-16 1,028,594 13,519 1.3%

2016-17 1,079,421 50,827 4.9%

2017-18 1,089,687 10,266 1.0%

2018-19 1,091,958 2,271 0.2%

2019-20 1,101,758 9,800 0.9%

2020-21 1,060,586 -41,172 -3.7%

Forecast 2021-22 1,059,125 -1,461 -0.1%

2022-23 1,065,739 6,614 0.6%

2

Forecast Contact:

Paula Moore 360-664-9376

Common School Special EducationCaseload Forecast Council

February 11, 2022

Special Education Average Annual Enrollment (HC)

(Age 3-PreK and State Funded Age K-21)

The Common School Special Education forecast consists of two programs: a separately

funded Age 3-Pre-Kindergarten program, and the Age K-21 school-based Special Education

program, indexed to 13.5 percent of each school district’s total full-time equivalent

enrollment. Up until the 2020-21 school year, Special Education also included the Age 0-2

Infant and Toddler program.

Forecast Comparisons (Academic Year Averages)

The February 2022 forecast is, on average, 1,171 students or 0.8 percent higher than the

November 2021 forecast for the 2021-23 Biennium.

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 141,455 142,969 1,514 1.1%

2022-23 145,167 145,995 829 0.6%

3

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast

The reported Special Education enrollment is tracking within 0.3 percent of forecast.

However, Special Education 3-PreK enrollment is tracking 5.6 percent above forecast, while

the tracking of K-21 is on par with the forecast. The tracking data is of reported Special

Education enrollment. These numbers are slightly different from the forecasted caseload

which, for those in the K-21 program, includes only students funded under the Special

Education basic funding target.

Academic Year Caseload Change

The Special Education forecast declined in 2020-21 for two reasons. First, the state-funded

Birth to Age 2 Special Education program shifted from OSPI to the Early Support for Infant

and Toddlers program at DCYF. This reduced the 2020-21 forecast by 10,381. Second,

Special Education enrollment declined due to concerns about COVID-19 and remote/hybrid

schooling. In 2021-22, the Special Education enrollment continued declined slightly from the

prior year, both in 3-PreK and K-age 21. By 2022-23, the 3-PreK participation rate is

forecasted to increase by the 2022-23. However, due to declining birth rates, this younger

group will not rebound to pre-pandemic levels. For 2022-23, the Special Education K-21

caseload, like Common Schools, will shift and follow a slower growth trajectory than pre-

pandemic. However, it is assumed that trajectory will slightly higher than Common Schools.

Risks to the Forecast

The risks to the Special Education enrollment forecast are high. Special Education enrollment is

subject to the same risks as the Common Schools forecast during this period of uncertainty.

Nov-21 Percent

Forecast Actual Variance Variance

Nov-21 146,611 146,661 50 0.0%

Dec-21 147,230 147,776 546 0.4%

Jan-22 148,081 148,866 785 0.5%

*Special education reported program headcount (Age 3-21)

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-14 136,983

2014-15 138,909 1,926 1.4%

2015-16 141,992 3,083 2.2%

2016-17 145,006 3,014 2.1%

2017-18 151,515 6,509 4.5%

2018-19 156,201 4,686 3.1%

2019-20 160,361 4,160 2.7%

2020-21 144,060 -16,301 -10.2%

Forecast 2021-22 142,969 -1,091 -0.8%

2022-23 145,995 3,026 2.1%

4

Forecast Contact:

Paula Moore 360-664-9376

Education

Common School Bilingual Education Caseload Forecast Council

February 11, 2022

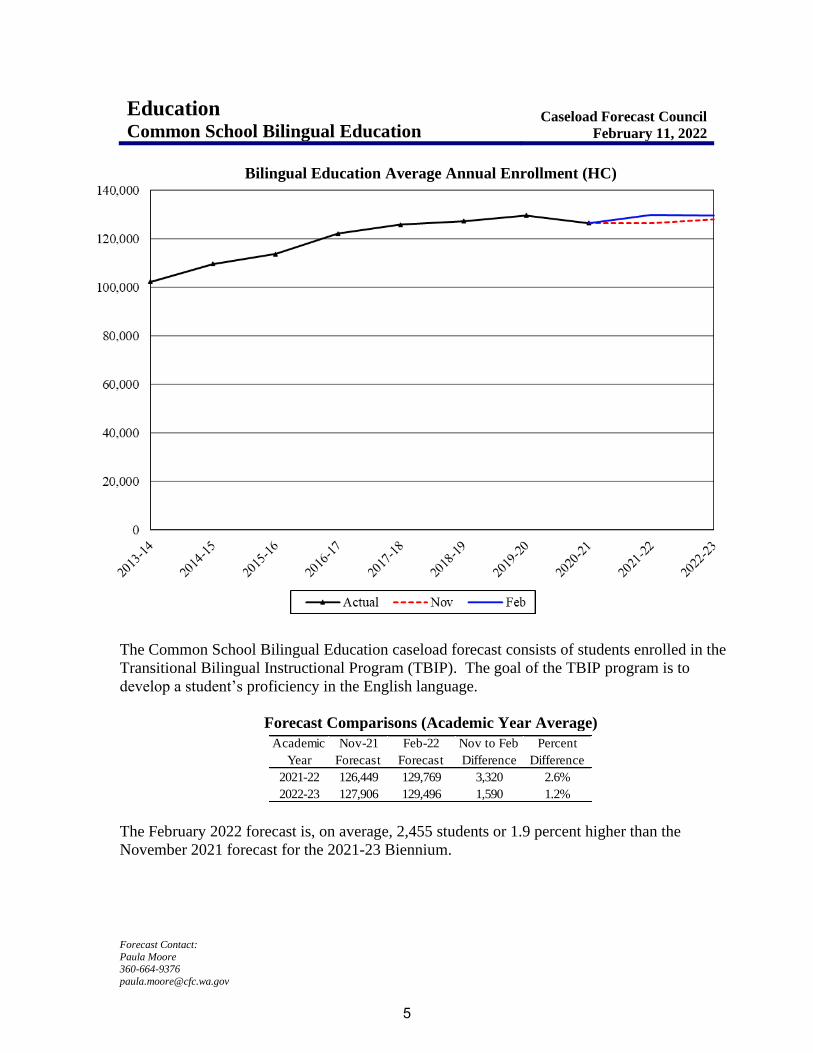

Bilingual Education Average Annual Enrollment (HC)

The Common School Bilingual Education caseload forecast consists of students enrolled in the

Transitional Bilingual Instructional Program (TBIP). The goal of the TBIP program is to

develop a student’s proficiency in the English language.

Forecast Comparisons (Academic Year Average)

The February 2022 forecast is, on average, 2,455 students or 1.9 percent higher than the

November 2021 forecast for the 2021-23 Biennium.

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 126,449 129,769 3,320 2.6%

2022-23 127,906 129,496 1,590 1.2%

5

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast

Actuals for TBIP are tracking 2.5 percent above the November forecast. However, K-6 TBIP

is tracking 3.9 percent above the November forecast, while 7-12 TBIP is on par with

November.

Academic Year Caseload Change

The TBIP forecast is sensitive to testing changes, the state’s job growth, US immigration policies

and VISA processing, and families moving to Washington State from other US states. The 2020-

21 caseload decline is due to concerns about COVID-19 and remote/hybrid schooling. In 2021-

22, more elementary children were identified for the program, as children returned from

remote/hybrid and the state implemented a new screener. For 2022-23, the forecast assumes flat

enrollment compared to pre-pandemic due to lower immigration to the state. It is also assumed

that students will stay in the program longer due to (1) the transition to a new state assessment

and (2) the impact remote/hybrid schooling in the 2020-21 school year.

After Exit Enrollment Courtesy Forecast

The After Exit program provides an additional two years of funding for students who exit the

TBIP program after demonstrating proficiency on the spring assessment. The February 2022

forecast is on par with the November 2021 forecast for the 2021-23 biennium.

Risks to the Forecast

Risks to the Bilingual Education forecast are high given the implementation of a new testing

system, COVID-19, and changes in immigration policy and processing of immigrant VISAs.

Nov-21 Percent

Forecast Actual Variance Variance

Nov-21 125,299 128,080 2,781 2.2%

Dec-21 126,317 129,403 3,086 2.4%

Jan-22 126,593 130,349 3,756 3.0%

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-14 102,281

2014-15 109,516 7,236 7.1%

2015-16 113,676 4,160 3.8%

2016-17 122,074 8,398 7.4%

2017-18 125,775 3,701 3.0%

2018-19 127,154 1,379 1.1%

2019-20 129,601 2,447 1.9%

2020-21 126,427 -3,174 -2.4%

Forecast 2021-22 129,769 3,342 2.6%

2022-23 129,496 -273 -0.2%

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 22,685 22,431 -255 -1.1%

2022-23 23,442 23,634 192 0.8%

6

Forecast Contact:

Paula Moore 360-664-9376

Charter Schools Enrollment Caseload Forecast Council

February 11, 2022

Charter Schools Average Annual Enrollment (FTE)

The charter school forecast includes grade-level enrollments, special education, and bilingual

education. The CFC’s current charter school forecast dates to the 2016 legislative session, when

ESSB 6194 re-established charter schools as an educational system operating separately from the

common school system. The Washington State Charter School Commission (WA CSC) and the

Spokane School District (SSD) are the only approved authorizers of charter schools.

Forecast Comparisons (Academic Year Averages)

The February 2022 forecast is, on average, 189 students or 3.6 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 4,669 4,515 -155 -3.3%

2022-23 5,668 5,445 -222 -3.9%

7

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast

Actuals for the 2021-22 school year are tracking 2.7 percent below the November forecast,

primarily due to 4 programs experiencing mid-year enrollment decline.

Academic Year Caseload Change

Charter schools are still in an implementation and growth period in Washington State. The

enrollment initially grew through 2018-19, then declined in 2019-20 due to the closure of

four charter schools. An additional school announced a closure at the end of 2020-21.

Collectively, in 2020-21 charter schools expanded. Three new schools opened, serving 316

new students. In 2021-22, 5 additional schools opened, adding an estimated 625 students.

Two more schools will open in 2022-23, serving 287 students. These new schools are funded

on their budgeted, not actual, enrollment for the first year of operation. The only exception

would be if schools delay opening or close mid-year.

Charter school enrollment is forecasted to continue to grow in 2021-22 and 2022-23 as the

currently established and new charters expand grade levels served.

Risks to the Forecast

The risks to the charter school forecast are high. New schools vary in their success rates of

enrollment and scale-up. Another risk is overly optimistic enrollment and expansion plans from

authorized charter schools. COVID-19 adds additional risk to the forecast as it may temporarily

change the operations for some schools and impact charters’ recruitment, expansion, and/or

opening plans.

Nov-21 Percent

Forecast Actual Variance Variance

Nov-21 4,672 4,578 -93 -2.0%

Dec-21 4,665 4,544 -121 -2.6%

Jan-22 4,660 4,503 -157 -3.4%

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-14

2014-15

2015-16

2016-17 1,603 1,603

2017-18 2,408 804 50.2%

2018-19 3,286 878 36.5%

2019-20 2,866 -420 -12.8%

2020-21 3,645 779 27.2%

Forecast 2021-22 4,515 870 23.9%

2022-23 5,445 931 20.6%

8

Forecast Contact:

Paula Moore 360-664-9376

College Bound Scholarship Program

Caseload Forecast Council

February 11, 2022

College Bound Scholarship Program

(Academic Year Enrollment)

The College Bound Scholarship Program (CBSP) provides the value of four years of tuition (at

public institution rates) and a book allowance to low-income students who pledge in the 7th, 8th

and, in some situations, 9th grade, graduate high school with a "C" or better average, avoid a

felony conviction, and enroll in an eligible education institution located in Washington state. The

CBSP caseload includes all CBSP eligible students enrolled in eligible institutions, including

those with financial need met through other sources. A student in CBSP needs to enroll within

two years of graduating from high school and has a five-year window to fully use the award.

Forecast Comparisons (Academic Year Averages)

The February 2022 forecast is, on average, 145 cases or 0.8 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 19,348 19,488 140 0.7%

2022-23 19,129 18,698 -430 -2.3%

9

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast

Actuals for Fall Term of the 2021-22 academic year are tracking 0.9 percent above the

November forecast. CBSP data updates occur four times per year. The February forecast

compares enrollment for Fall Term compared to the November forecast. The forecast model

relies on Fall Term to estimate the year’s overall enrollment as a portion of students defer

enrollment until spring and/or summer term.

Academic Year Caseload Change

Disruptions from COVID-19 caused a sharp decline in the CBSP caseload during the 2020-

21 year as fewer students enrolled in higher education. This resulted in a 7.7 percent decline

from the prior year. The 2021-22 year followed with a significantly improved labor market,

also lowering the demand for higher education. The forecast assumes a drop of 3.1 percent in

the CBSP caseload for the 2021-22 year. Enrollment is projected to decline further in the

2022-23 year, rather than stay flat or rebound, as high school seniors are signaling less

interest in post-secondary opportunities. Early FAFSA filings for the 2022-23 year by low-

income families are lower than prior years, particularly among high school seniors. The

combined impact of fewer entries and fewer continuing students is forecasted to cause a 4.1

percent year over year decline in the 2022-23 year for CBSP enrollment.

Risks to the Forecast

Risks to the CBSP forecast are high. Uncertainty due to COVID-19 adds additional risk to

the forecast. Shifts in the labor market could also impact the forecast. The demand for higher

education financial aid is often cyclical with the labor market—enrollment often declines

during when there is a strong demand for labor.

Nov-21 Percent

Forecast Actual Variance Variance

Fall Term 16,166 16,307 141 0.9%

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-14 8,687

2014-15 12,318 3,631 41.8%

2015-16 15,599 3,281 26.6%

2016-17 17,251 1,652 10.6%

2017-18 19,730 2,479 14.4%

2018-19 20,431 701 3.6%

2019-20 21,798 1,367 6.7%

2020-21 20,109 -1,689 -7.7%

Forecast 2021-22 19,488 -621 -3.1%

2022-23 18,698 -790 -4.1%

10

Forecast Contact:

Paula Moore 360-664-9376

Washington College Grant

Caseload Forecast Council

February 11, 2022

Washington College Grant Forecast

Starting in the 2020-21 academic year, the Washington College Grant (WCG) provides all

eligible students with financial aid awards based on public tuition rates. WCG can be used at

public and private participating institutions of higher education in Washington State. A grant will

also be offered to certain registered apprentices. The Washington Student Achievement Council

(WSAC) administers the WCG. This is a new caseload under HB 2158, passed during the 2019

legislative session. Previously, the program was not an entitlement.

Headcount Forecast Comparisons (Academic Year Averages)

The February 2022 forecast is, on average, 3,599 cases or 3.7 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Academic

Year

Nov-21

Forecast

Feb-22

Forecast

Nov to Feb

Difference

Percent

Difference

2021-22 97,796 95,563 -2,233 -2.3%

2022-23 98,078 93,113 -4,965 -5.1%

11

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast

Actuals for Fall Term of the 2021-22 academic year are tracking 2.3 percent below the

November forecast. WCG data updates occur four times per year. The February forecast

compares enrollment for Fall Term compared to the November forecast. The forecast model

relies on Fall Term to estimate the year’s overall enrollment as a portion of students defer

enrollment until spring and/or summer term.

Academic Year Caseload Change (Headcount)

The WCG became an entitlement during the 2020-21 year, when COVID-19 impacted

demand for higher education. The tight labor market has further dampened the demand for

higher education in the 2021-22 year. The February forecasted revised down enrollment

estimates for the 2021-22 year based on lower fall term enrollment in the WCG. Enrollment

is projected to decline further in 2022-23 year, rather than stay flat or rebound, as high school

seniors are signaling less interest in post-secondary opportunities. Early FAFSA filings for

the 2022-23 year by low-income families are lower than prior years, particularly among high

school seniors.

Apprenticeships

The WCG forecast assumes flat enrollment for registered apprenticeships. The February 2022

forecast for WCG apprenticeships is set at 70 for both 2021-22 and 2022-23. This is a

downward revision from the November 2021 forecast, which assumed 375 for 2021-22 and

750 for 2022-23. These headcounts are included in the total WCG forecast.

Risks to the Forecast

Risks to the WCG forecast are high, as it is a new forecast. Uncertainty due to COVID-19

adds risk to the forecast. Shifts in the labor market are likely to have the most impact the

forecast. The demand for higher education financial aid is often cyclical with the labor

market—enrollment often declines during when there is a strong demand for labor.

Nov-21 Percent

Forecast Actual Variance Variance

Fall Term 74,014 72,308 -1,706 -2.3%

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-14

2014-15

2015-16

2016-17

2017-18

2018-19

2019-20

2020-21 100,427 100,427

Forecast 2021-22 95,563 -4,864 -4.8%

2022-23 93,113 -2,451 -2.6%

12

Forecast Contact:

Paula Moore 360-664-9376

Early Support for Infants and Toddlers Caseload Forecast Council

February 11, 2022

Early Support for Infants and Toddlers (ESIT)

(Unofficial Courtesy Forecast)

The Early Support for Infants and Toddlers program (ESIT) coordinates and provides services

for eligible infants and toddlers and is administered by the Department of Children, Youth, and

Families (DCYF). The ESIT caseload is defined as the number of children with active

Individualized Family Service Plans (IFSPs). Children are evaluated and become eligible if

found to have specific developmental delays. As of September 1, 2020, ESIT includes state

funded services previously provided through Special Education Birth to Age 2.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 88 cases or 0.9 percent lower than the November

2021 forecast for the 2021-23 Biennium.

-

2,000

4,000

6,000

8,000

10,000

12,000

Actual Nov Feb

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 9,637 9,591 -46 -0.5%

2023 10,185 10,056 -129 -1.3%

13

Forecast Contact:

Paula Moore 360-664-9376

Tracking the Current Forecast

Actuals are tracking, on average, 8 cases or 0.1 percent below the November forecast.

Academic Year Caseload Change

The COVID-19 pandemic resulted in a sharp decline in the ESIT caseload, starting in March

of 2020. The program experienced reductions in entries and active participants. Referrals

from pediatricians and pediatric service providers also declined. The decline reversed starting

in January 2021, and growth returned as vaccines became available for providers and adult

caregivers. In total, for FY 2021, the ESIT caseload declined by 11.8 percent due to COVID-

19. In FY 2022 and 2023, the ESIT caseload is projected to grow, but at a lower rate than the

pre-pandemic average. This is because the overall age 0 to 2 population is forecasted to

decline due to drops in birth rates and fewer families moving into Washington State.

Risks to the Forecast

Risks to the February 2022 forecast are higher than normal as a result of uncertainty due to

COVID-19 prevalence, access to pediatric vaccines, birth rates, and net in-state migration.

Historically, changing birth rates and policy changes have most impacted this forecast.

Nov-21 Percent

Forecast Actual Variance Variance

Oct-21 9,502 9,483 -19 -0.2%

Nov-21 9,540 9,544 4 0.0%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 6,143

2015 6,609 466 7.6%

2016 7,436 827 12.5%

2017 7,832 396 5.3%

2018 8,500 668 8.5%

2019 9,649 1,149 13.5%

2020 9,991 342 3.5%

2021 8,808 -1,182 -11.8%

Forecast 2022 9,591 782 8.9%

2023 10,056 465 4.8%

14

Forecast Contact:

Erik Sund 360-664-9374

Early Childhood Education and Assistance (ECEAP)

Caseload Forecast Council

February 11, 2022

Early Childhood Education and Assistance

The Early Childhood Education and Assistance Program (ECEAP) provides comprehensive

nutrition, health, education, and family support services to eligible children between the ages

of three and five years old who are not eligible for kindergarten to enhance their opportunity

for success in the common school system. ECEAP enrollment is forecast as total annual

enrollment calculated as a ten-month average to more accurately reflect that the majority of

enrollment occurs during the standard school year. Per statute, children who participate in

Head Start are not eligible for ECEAP and, as a result, are not included in the forecast.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 191 cases or 1.4 percent lower than the November

2021 forecast for the 2021-23 Biennium.

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Actual Nov Feb

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 11,847 11,465 -382 -3.2%

2023 14,890 14,890 0 0.0%

15

Forecast Contact:

Erik Sund 360-664-9374

Tracking the Current Forecast

Actuals are tracking, on average, 145 cases or 1.4 percent below the November forecast.

ECEAP eligibility is primarily based on a child’s age and family income. Children otherwise

ineligible may also participate under rules adopted by the Department of Children, Youth and

Families (DCYF), provided that the number of such children is no more than 25 percent of

enrollment in the program. During the 2020-2021 school year, the program served an average of

about 729 such children per month. These children are not considered part of the state-funded

entitlement caseload and are not counted in this forecast.

ECEAP enrollment during the 2020-2021 school year was heavily impacted by the COVID-19

pandemic, with average monthly caseloads being 23.1 percent lower than during the 2019-2020

school year. While program participation has been higher so far during the 2021-2022 school

year, monthly caseloads are still below 2019-2020 levels. This forecast assumes the caseload will

continue increase gradually over the rest of the 2021-2022 school year as it did in 2020-2021 and

will return to historical levels, adjusted for increases in the number of enrollment slots funded by

the legislature, in the 2022-2023 school year.

Academic Year Caseload Change

Risks to the Forecast

Risks to this forecast are high. ECEAP participation was low throughout the 2020-2021

school year and has been low for first half of the 2021-2022 school year. The pace of

caseload recovery will continue to be influenced the progress achieved in limiting COVID-19

case counts in the community and by the availability of COVID-19 vaccines for younger

children.

Nov-21 Percent

Forecast Actual Variance Variance

Oct-21 10,398 10,174 -224 -2.2%

Nov-21 10,797 10,731 -66 -0.6%

Academic

Year Caseload

Change from

Prior Year

Percent

Change

Actual 2013-2014 8,196

2014-2015 9,356 1,160 14.2%

2015-2016 10,965 1,610 17.2%

2016-2017 11,294 329 3.0%

2017-2018 11,989 695 6.2%

2018-2019 12,660 671 5.6%

2019-2020 12,955 295 2.3%

2020-2021 9,964 -2,991 -23.1%

Forecast 2021-2022 11,465 1,501 15.1%

2022-2023 14,890 3,425 29.9%

16

Forecast Contact:

Liz Dehlbom 360-664-9373

Corrections Juvenile Rehabilitation

Caseload Forecast Council

February 11, 2022

Juvenile Rehabilitation

The Juvenile Rehabilitation (JR) caseload is comprised of three components: Juvenile

Commitments, Juvenile Parole Revocations, and Adult Commitments.

• Juvenile Commitments are individuals sentenced for crimes committed under age 18

and are under Juvenile Court jurisdiction.

• Juvenile Parole Revocations are individuals returned to confinement for up to 30 days

for violating parole after releasing from a Juvenile Commitment.

• Adult Commitments are individuals who committed crimes under age 18 and are

sentenced as adults to the Department of Corrections (DOC). They begin their

sentences in JR facilities.

Forecast Comparisons (Fiscal Year Averages)

17

Forecast Contact:

Liz Dehlbom 360-664-9373

The February 2022 forecast is, on average, 39 cases or 10.5 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Tracking the Current Forecast

Actuals have been tracking, on average, 7 cases or 2.2 percent above the November 2021

forecast. The caseload declined in December after being near even for four months.

Declines were expected as new admissions continue to be depressed for both Juvenile and Adult

commitments compared to the overall average during the COVID-19 period. At the same time,

Juvenile commitment releases continue to be slightly increased as a result of the May policy

change relating the calculation of release dates near the minimum sentence range. The current

policy has produced shorter lengths of stay on average, though the number of new admissions

since implementation is too small to calculate the ongoing impact.

The forecast delays the timeline for admission increases for the next three months and extends

the timeframe for the courts to clear any case backlog by one year through FY 2024. This was

done to account for slower than expected court recovery. The caseload will continue to contract

through FY 2022 before gradually increasing over the biennium as admissions increase. The

caseload is expected to resume growth associated with E2SSB 6160 and E2SHB 1646 for the

next few years, though at diminished levels due to ongoing reductions in the volume of Juvenile

cases in the criminal justice system.

Fiscal Year Caseload Change

Risks to the Forecast

Risk to this forecast is high. There is substantial uncertainty surrounding the impact of

COVID-19 on the timeline for increased capacity in the criminal justice system in the short-

term as well as the long-term impact on future case volume. This may impact the expected

magnitude of E2SSB 6160 and E2SHB 1646.

18

Forecast Contact:

Liz Dehlbom 360-664-9373

Corrections Adult Inmate

Caseload Forecast Council

February 11, 2022

Adult Inmate

The Adult Inmate forecast includes adult criminal sentences under the state’s jurisdiction and

housed in prisons and partial confinement facilities. The forecast includes the effects of

changing demographics, offense types, and policy changes (new legislation or initiatives).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 262 cases or 1.9 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Actuals have been tracking, on average, 61 cases or 0.5 percent below the November 2021

forecast. The caseload has experienced a slower decline in the last four months compared with

earlier in the COVID-19 period.

19

Forecast Contact:

Liz Dehlbom 360-664-9373

Tracking the Current Forecast

The overall decline of the caseload is a function of fewer admissions than releases with the

slowing of this decline in recent months reflective of fewer individuals releasing rather than an

increase in new admissions. The courts continue to have constrained capacity to process pending

cases given public health guidance during the COVID-19 pandemic and has resulted in the delay

in the resolution of cases. As a result of recent high case rates in the community, many counties

have again paused in-person proceedings through February. Additionally, the courts continue to

process cases as a result of the Washington State Supreme Court decision in State v. Blake,

requiring courts to vacate and resentence individuals with possession convictions in their

criminal history.

The forecast delays the timeline for admission increases for the next two months and extends the

timeframe for the courts to clear any case backlog by one year through FY 2025. This was done

to account for slower than expected court recovery. The caseload will continue to contract

slightly through FY 2022. It is expected that the caseload will gradually increase over the

biennium as admissions increase and courts begin to clear any case backlog.

Fiscal Year Caseload Change

Risks to the Forecast

Risk to this forecast is high. There is substantial uncertainty surrounding the impact of

COVID-19 on the timeline for increased capacity in the criminal justice system in the short-

term as well as the long-term impact on future case volume.

20

Forecast Contact:

Liz Dehlbom 360-664-9373

Corrections Contact-Required Community Supervision

Caseload Forecast Council

February 11, 2022

Contact-Required Community Supervision

The Contact-Required Community Supervision caseload includes adults who have been convicted

of a crime(s), are actively supervised by the Department of Corrections (DOC), and have

requirements to maintain contact with the DOC.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 415 cases or 3.3 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Actuals have been tracking, on average, 249 cases or 1.9 percent above the November 2021

forecast. The caseload has experienced a slower decline in the last four months compared with

earlier in the COVID-19 period.

21

Forecast Contact:

Liz Dehlbom 360-664-9373

Tracking the Current Forecast

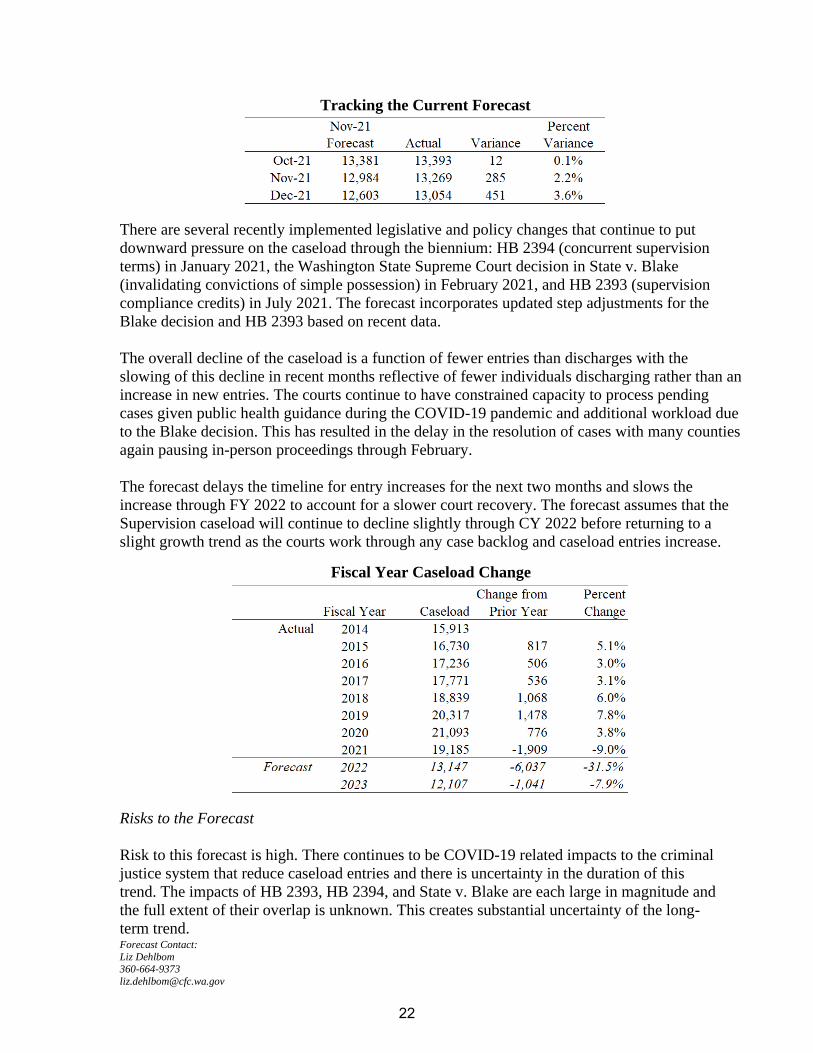

There are several recently implemented legislative and policy changes that continue to put

downward pressure on the caseload through the biennium: HB 2394 (concurrent supervision

terms) in January 2021, the Washington State Supreme Court decision in State v. Blake

(invalidating convictions of simple possession) in February 2021, and HB 2393 (supervision

compliance credits) in July 2021. The forecast incorporates updated step adjustments for the

Blake decision and HB 2393 based on recent data.

The overall decline of the caseload is a function of fewer entries than discharges with the

slowing of this decline in recent months reflective of fewer individuals discharging rather than an

increase in new entries. The courts continue to have constrained capacity to process pending

cases given public health guidance during the COVID-19 pandemic and additional workload due

to the Blake decision. This has resulted in the delay in the resolution of cases with many counties

again pausing in-person proceedings through February.

The forecast delays the timeline for entry increases for the next two months and slows the

increase through FY 2022 to account for a slower court recovery. The forecast assumes that the

Supervision caseload will continue to decline slightly through CY 2022 before returning to a

slight growth trend as the courts work through any case backlog and caseload entries increase.

Fiscal Year Caseload Change

Risks to the Forecast

Risk to this forecast is high. There continues to be COVID-19 related impacts to the criminal

justice system that reduce caseload entries and there is uncertainty in the duration of this

trend. The impacts of HB 2393, HB 2394, and State v. Blake are each large in magnitude and

the full extent of their overlap is unknown. This creates substantial uncertainty of the long-

term trend.

22

Forecast Contact:

Liz Dehlbom 360-664-9373

Corrections Community Custody Violator

Caseload Forecast Council

February 11, 2022

Community Custody Violator

The Community Custody Violator forecast includes adults who were under community custody,

violated their supervision conditions, and were sanctioned with confinement. Most of these

individuals are housed in local county/city jails, with the balance housed in state prisons.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 136 cases or 17.9 percent lower than the November

forecast for the 2021-23 Biennium.

Actuals have been tracking, on average, 110 cases or 23.0 percent below the November 2021

forecast. The caseload’s sharp decline over CY 2021 stalled in October and has remained even

through December.

23

Forecast Contact:

Liz Dehlbom 360-664-9373

Tracking the Current Forecast

The stall in decline is due to the Department of Corrections (DOC) in November 2021 phasing

out some of the temporary practice changes that have been in place due to COVID-19. These

have included suspension of certain treatment programs, reduction of urinalysis testing, and a

reduction of in-person caseload contacts. The caseload likely did not increase as anticipated

because of the historically seasonal nature of the caseload. The February forecast applies a

seasonal factor to the caseload until DOC fully phases out the temporary practices.

The forecast additionally incorporates revised step adjustments based on the implementation

experience in recent months for the DOC policy change reducing violation confinement sanction

length and the reductions in the overall Supervision caseload.

DOC had expected to implement the final phase-in to fully revert to pre-pandemic procedures in

January 2022, but due to the sharp rise in COVID-19 cases in the community this was revised to

March 2022. The forecast assumes that the Violator caseload will grow to a new ongoing level

over three months with the resumption of normal DOC operations.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to this forecast are high. The timeline for full resumption of DOC supervision practices

may change as COVID-19 conditions in the community develop. The magnitude of step

adjustments adds an extra layer of risk to the forecast. It is also unclear how closely the large

decline in the supervision caseload will be mirrored in the Violator caseload over time.

24

Forecast Contact:

Erik Cornellier 360-664-9375

Temporary Assistance for Needy

Families (TANF)

Caseload Forecast Council

February 11, 2022

TANF Assistance Units (Courtesy Forecast)

The Temporary Assistance for Needy Families (TANF) forecast combines two forecasts: one for

WorkFirst or “All Family” cases that include children and their parents and one for “Child Only”

cases in which the parents or guardians do not receive part of the grant and are not subject to

work requirements. WorkFirst cases made up 52% of the caseload during calendar year 2019.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is 1,593 cases or 6.1 percent higher than the November 2021

forecast for the 2021-23 Biennium.

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Actual Nov Feb

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 26,793 27,949 1,156 4.3%

2023 25,212 27,242 2,030 8.0%

25

Forecast Contact:

Erik Cornellier 360-664-9375

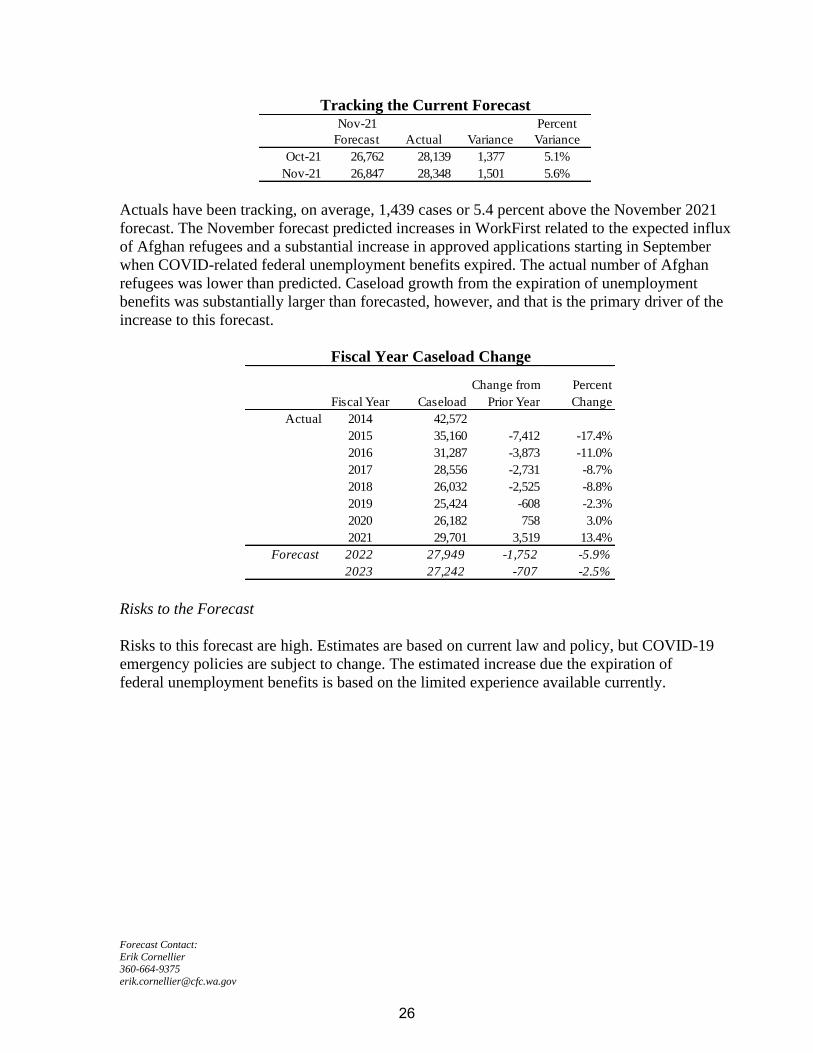

Tracking the Current Forecast

Actuals have been tracking, on average, 1,439 cases or 5.4 percent above the November 2021

forecast. The November forecast predicted increases in WorkFirst related to the expected influx

of Afghan refugees and a substantial increase in approved applications starting in September

when COVID-related federal unemployment benefits expired. The actual number of Afghan

refugees was lower than predicted. Caseload growth from the expiration of unemployment

benefits was substantially larger than forecasted, however, and that is the primary driver of the

increase to this forecast.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to this forecast are high. Estimates are based on current law and policy, but COVID-19

emergency policies are subject to change. The estimated increase due the expiration of

federal unemployment benefits is based on the limited experience available currently.

Nov-21 Percent

Forecast Actual Variance Variance

Oct-21 26,762 28,139 1,377 5.1%

Nov-21 26,847 28,348 1,501 5.6%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 42,572

2015 35,160 -7,412 -17.4%

2016 31,287 -3,873 -11.0%

2017 28,556 -2,731 -8.7%

2018 26,032 -2,525 -8.8%

2019 25,424 -608 -2.3%

2020 26,182 758 3.0%

2021 29,701 3,519 13.4%

Forecast 2022 27,949 -1,752 -5.9%

2023 27,242 -707 -2.5%

26

Forecast Contact:

Erik Cornellier 360-664-9375

Economic Services Administration Aged, Blind and Disabled Assistance Grant

Caseload Forecast Council

February 11, 2022

Aged, Blind and Disabled Assistance Grant Program – Total Caseload

The Aged, Blind and Disabled Assistance program (ABD) provides financial assistance to persons

whose long-term mental and/or physical disabilities likely qualify them for the federal

Supplemental Security Income (SSI) program, regardless of citizenship status. This forecast

includes three components: Presumptive SSI, Aged, and Disabled.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is 250 cases or 1.2 percent higher than the November 2021 forecast

for the 2021-23 Biennium.

-

5,000

10,000

15,000

20,000

25,000

30,000

Actual Nov Feb

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 20,898 21,122 225 1.1%

2023 20,828 21,103 275 1.3%

27

Forecast Contact:

Erik Cornellier 360-664-9375

Tracking the Current Forecast

Actuals have been tracking, on average, 305 cases or 1.5 percent above the November 2021

forecast for the past two months. This coincides with an increase in Temporary Assistance for

Needy Families cases with the expiration of federal unemployment benefits in September of

2021.

Fiscal Year Caseload Change

The ABD growth rate exhibits large volatility. This is mainly due to:

1. HB 2667 that provided for a client to receive both the ABD program and the Essential

Needs and Housing Support program (HEN) assistance concurrently while an

application for federal SSI benefits is pending.

2. HB1831 that increased resources exempted when determining eligibility for public

assistance.

3. COVID-19 and related policy changes.

Risks to the Forecast

The risks to the forecast are moderate. The risks are mainly due to the uncertainties of the

COVID-19 impact and corresponding policy changes.

Nov-21 Percent

Forecast Actual Variance Variance

Oct-21 20,869 21,198 329 1.6%

Nov-21 20,821 21,103 282 1.4%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 24,309

2015 21,914 -2,395 -9.9%

2016 20,512 -1,402 -6.4%

2017 20,075 -437 -2.1%

2018 19,707 -368 -1.8%

2019 20,293 586 3.0%

2020 20,442 149 0.7%

2021 21,528 1,087 5.3%

Forecast 2022 21,122 -406 -1.9%

2023 21,103 -19 -0.1%

28

Forecast Contact:

Erik Sund 360-664-9374

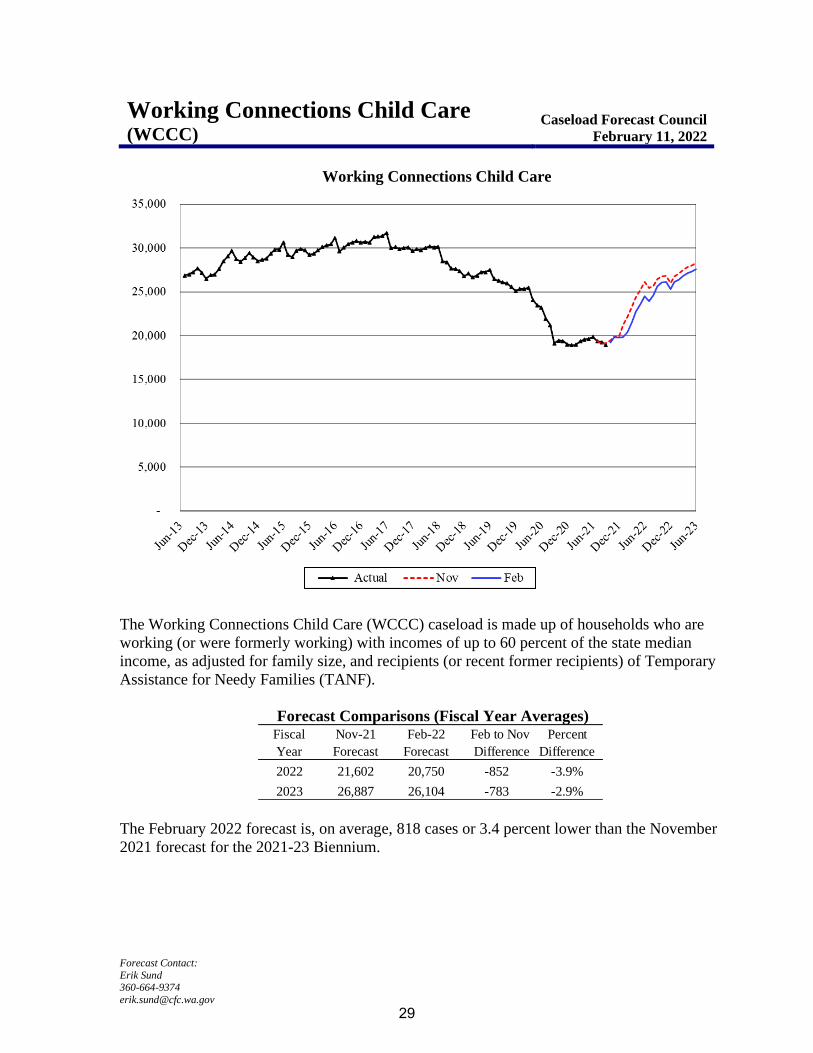

Working Connections Child Care (WCCC)

Caseload Forecast Council

February 11, 2022

Working Connections Child Care

The Working Connections Child Care (WCCC) caseload is made up of households who are

working (or were formerly working) with incomes of up to 60 percent of the state median

income, as adjusted for family size, and recipients (or recent former recipients) of Temporary

Assistance for Needy Families (TANF).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 818 cases or 3.4 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 21,602 20,750 -852 -3.9%

2023 26,887 26,104 -783 -2.9%

29

Forecast Contact:

Erik Sund 360-664-9374

Tracking the Current Forecast

Actuals are tracking, on average, 16 cases or 0.1 percent below the November forecast.

Fiscal Year Caseload Change

This forecast includes three step adjustments to account for the expected caseload impacts of

E2SSB 5237 (Chapter 199, Laws of 2021). Among other changes to state programs for

children, this legislation: (1) changed the maximum family income eligible for WCCC from

200 percent of the federal poverty level to 60 percent of the State median income (SMI) for a

given family size; (2) established new schedules for copayments for families in WCCC with

lower maximum amounts; and (3) expanded the exemption from work requirements

previously provided to single parents enrolled in certain programs at community, technical,

and tribal colleges to include both parents that are not single and additional courses of study.

Each of these step adjustments serves to increase the caseload forecast, with the adjustments

increasing gradually from July 2021.

Additionally, the forecast continues to incorporate a step adjustment estimating the reduction

in the caseload caused by both reduced entries of new households and increased exits from

the program over the past 19 months due to health concerns, difficulty meeting work

requirements, and other effects of the COVID-19 pandemic. Due to the resurgence of COVID

infections late in 2021, this adjustment has been extended and will be phased out between

February and September of 2022.

Risks to the Forecast

Risks to this forecast are high. The pandemic has affected patterns of work and child care

utilization and has also affected the supply of child care services, leading in turn to a

substantial decline in the WCCC caseload. While this forecast anticipates that the caseload

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 19,424 19,378 -46 -0.2%

Aug-21 19,082 19,272 190 1.0%

Sep-21 19,130 18,938 -192 -1.0%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 27,605

2015 29,175 1,570 5.7%

2016 29,828 653 2.2%

2017 30,767 939 3.1%

2018 29,991 -776 -2.5%

2019 27,412 -2,579 -8.6%

2020 25,200 -2,213 -8.1%

2021 19,699 -5,501 -21.8%

Forecast 2022 20,750 1,051 5.3%

2023 26,104 5,353 25.8%

30

Forecast Contact:

Erik Sund 360-664-9374

will begin to recover this year, the pandemic’s impact has been such that any divergence

from the expected trend of recovery due to changes in epidemiological conditions may

produce significant variance. The scale of the step adjustments associated with the program

expansion under E2SSB 5237 introduce further risks to the forecast.

31

Forecast Contact:

Erik Cornellier 360-664-9375

Tiered Reimbursement

Caseload Forecast Council

February 11, 2022

Tiered Reimbursement

Early Achievers is Washington’s quality rating and improvement system for early learning

providers. Early Achievers supports early learning professionals by providing resources such as

professional development opportunities, coaching, and financial incentives. Licensed childcare

centers, licensed family homes, and Early Childhood Education and Assistance Programs

(ECEAP) are required to enroll in Early Achievers to receive state subsidy for childcare services.

The Department of Children, Youth, and Families (DCYF) rates providers based on quality, and

they receive additional reimbursement based on quality. There are six tiers, and providers receive

higher reimbursement in each tier.

Providers enrolling in Early Achievers must rate at Level 3 within 30 months of enrollment,

and ECEAP providers must rate at Level 4 within 12 months if they are license-exempt or 18

months if they are licensed or certified.

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Actual Nov Feb

32

Forecast Contact:

Erik Cornellier 360-664-9375

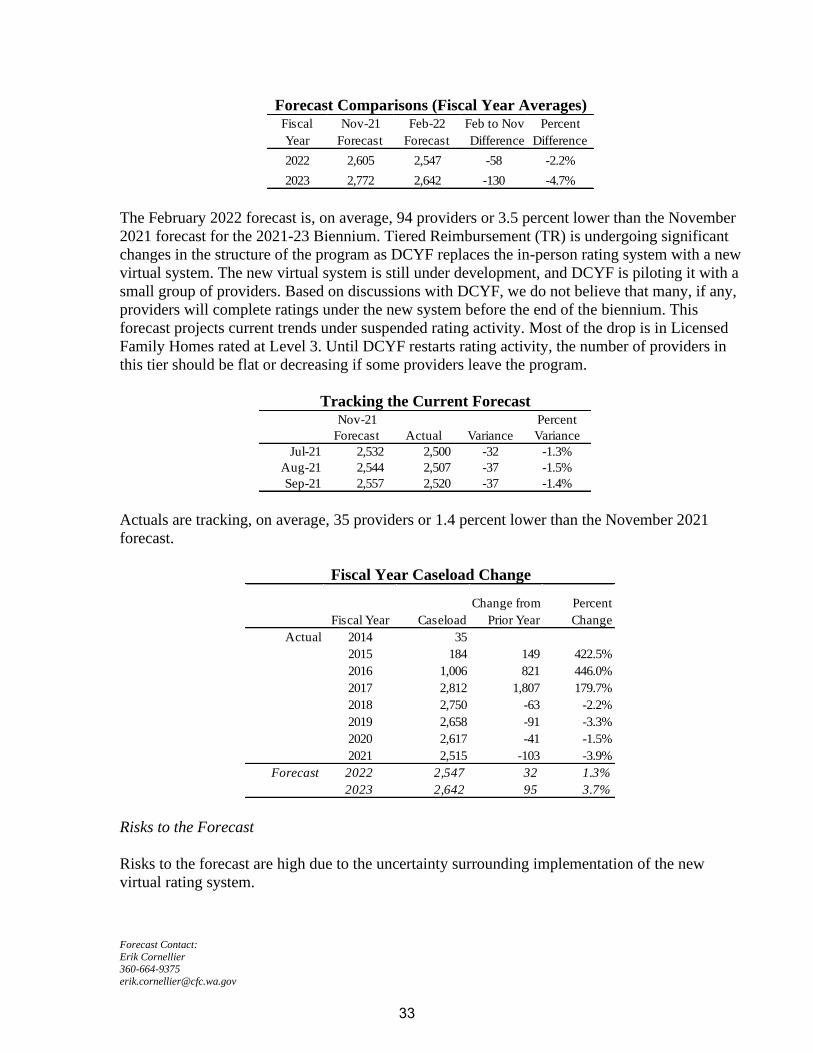

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 94 providers or 3.5 percent lower than the November

2021 forecast for the 2021-23 Biennium. Tiered Reimbursement (TR) is undergoing significant

changes in the structure of the program as DCYF replaces the in-person rating system with a new

virtual system. The new virtual system is still under development, and DCYF is piloting it with a

small group of providers. Based on discussions with DCYF, we do not believe that many, if any,

providers will complete ratings under the new system before the end of the biennium. This

forecast projects current trends under suspended rating activity. Most of the drop is in Licensed

Family Homes rated at Level 3. Until DCYF restarts rating activity, the number of providers in

this tier should be flat or decreasing if some providers leave the program.

Tracking the Current Forecast

Actuals are tracking, on average, 35 providers or 1.4 percent lower than the November 2021

forecast.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to the forecast are high due to the uncertainty surrounding implementation of the new

virtual rating system.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 2,605 2,547 -58 -2.2%

2023 2,772 2,642 -130 -4.7%

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 2,532 2,500 -32 -1.3%

Aug-21 2,544 2,507 -37 -1.5%

Sep-21 2,557 2,520 -37 -1.4%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 35

2015 184 149 422.5%

2016 1,006 821 446.0%

2017 2,812 1,807 179.7%

2018 2,750 -63 -2.2%

2019 2,658 -91 -3.3%

2020 2,617 -41 -1.5%

2021 2,515 -103 -3.9%

Forecast 2022 2,547 32 1.3%

2023 2,642 95 3.7%

33

Forecast Contact:

Erik Sund 360-664-9374

Children’s Services Screened-In Reports

Caseload Forecast Council

February 11, 2022

Screened-In Reports

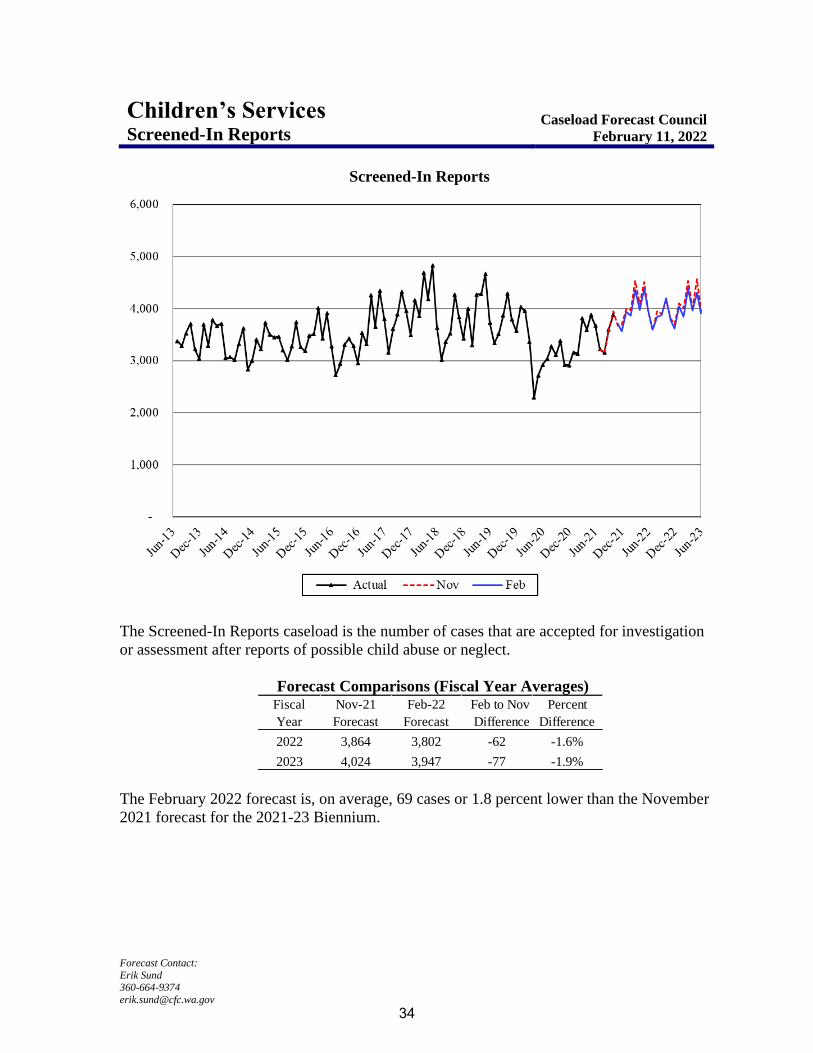

The Screened-In Reports caseload is the number of cases that are accepted for investigation

or assessment after reports of possible child abuse or neglect.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 69 cases or 1.8 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 3,864 3,802 -62 -1.6%

2023 4,024 3,947 -77 -1.9%

34

Forecast Contact:

Erik Sund 360-664-9374

Tracking the Current Forecast

Actuals are tracking, on average, 18 cases or 0.5 percent below the November forecast.

This forecast assumes that the caseload for FY 2020 and FY 2021 were negatively impacted by

the COVID-19 pandemic and that, starting from January 2022, this caseload will gradually go

back to levels closer to those of the years immediately prior to the pandemic.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to this forecast are high. The risks are due to both to uncertainty about the recovery

from the COVID-19 pandemic and to the historical volatility of this caseload.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 3,222 3,222 0 0.0%

Aug-21 3,157 3,156 -1 0.0%

Sep-21 3,604 3,605 1 0.0%

Oct-21 3,957 3,884 -73 -1.8%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 3,446

2015 3,302 -144 -4.2%

2016 3,443 141 4.3%

2017 3,464 21 0.6%

2018 3,984 520 15.0%

2019 3,808 -176 -4.4%

2020 3,472 -336 -8.8%

2021 3,324 -148 -4.3%

Forecast 2022 3,802 478 14.4%

2023 3,947 145 3.8%

35

Forecast Contact:

Erik Sund 360-664-9374

Children’s Services Licensed Foster Care

Caseload Forecast Council

February 11, 2022

Licensed Foster Care

The Licensed Foster Care (LFC) caseload is a forecast of the number of children in licensed

foster care during a calendar month. Financial assistance for licensed foster care includes a

monthly stipend, medical care, and a variety of additional services. This caseload has two

components – Basic Foster Care & Receiving Care (BFCRC) and Behavioral Rehabilitation

Services (BRS).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 155 cases or 2.8 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 5,304 5,189 -115 -2.2%

2023 5,650 5,455 -195 -3.5%

36

Forecast Contact:

Erik Sund 360-664-9374

Tracking the Current Forecast

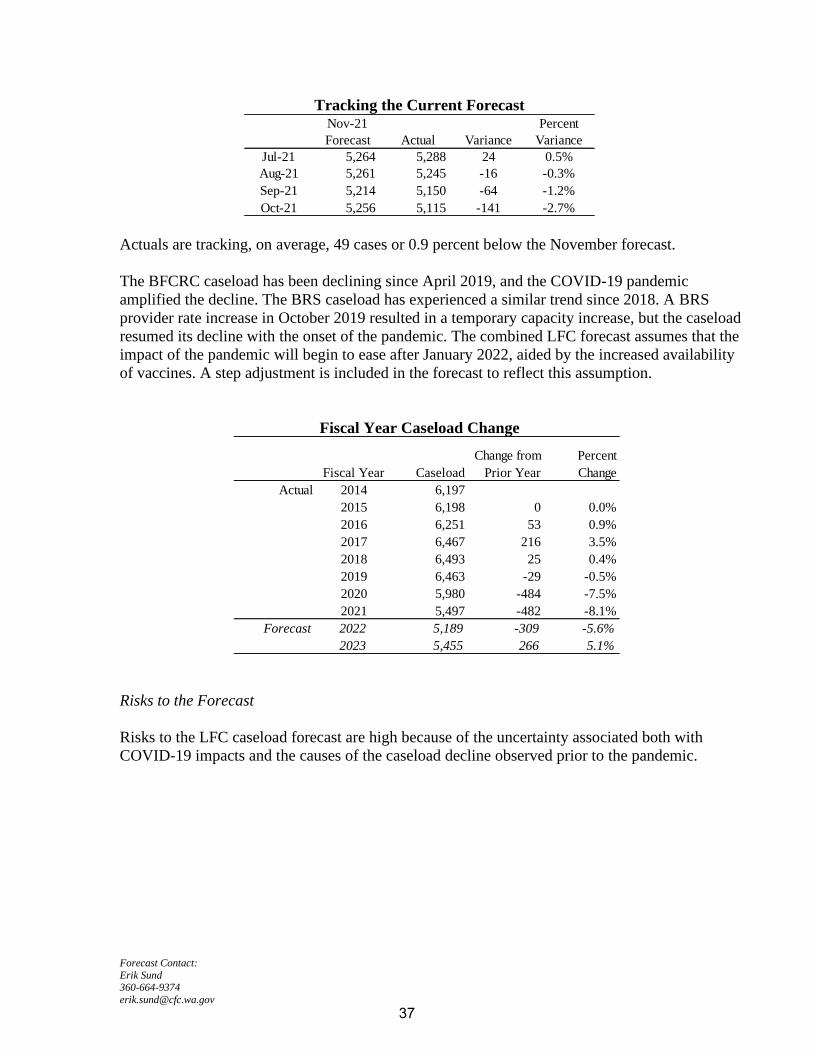

Actuals are tracking, on average, 49 cases or 0.9 percent below the November forecast.

The BFCRC caseload has been declining since April 2019, and the COVID-19 pandemic

amplified the decline. The BRS caseload has experienced a similar trend since 2018. A BRS

provider rate increase in October 2019 resulted in a temporary capacity increase, but the caseload

resumed its decline with the onset of the pandemic. The combined LFC forecast assumes that the

impact of the pandemic will begin to ease after January 2022, aided by the increased availability

of vaccines. A step adjustment is included in the forecast to reflect this assumption.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to the LFC caseload forecast are high because of the uncertainty associated both with

COVID-19 impacts and the causes of the caseload decline observed prior to the pandemic.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 5,264 5,288 24 0.5%

Aug-21 5,261 5,245 -16 -0.3%

Sep-21 5,214 5,150 -64 -1.2%

Oct-21 5,256 5,115 -141 -2.7%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 6,197

2015 6,198 0 0.0%

2016 6,251 53 0.9%

2017 6,467 216 3.5%

2018 6,493 25 0.4%

2019 6,463 -29 -0.5%

2020 5,980 -484 -7.5%

2021 5,497 -482 -8.1%

Forecast 2022 5,189 -309 -5.6%

2023 5,455 266 5.1%

37

Forecast Contact:

Erik Sund 360-664-9374

Children’s Services Extended Foster Care

Caseload Forecast Council

February 11, 2022

Extended Foster Care

The Extended Foster Care (EFC) caseload is the count of youth receiving certain foster care

benefits after turning 18 years old. EFC is intended to promote better outcomes for youth

who have aged out of the traditional foster care system.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 10 cases or 1.2 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 901 891 -10 -1.1%

2023 871 860 -11 -1.3%

38

Forecast Contact:

Erik Sund 360-664-9374

Tracking the Current Forecast

Actuals are tracking, on average, 15 cases or 1.5 percent above the November forecast.

This program has experienced many policy changes which have expanded eligibility for the

program and increased the caseload. The November forecast reflected the impact of the last

months of a temporary policy change, effective April 2020, that allowed youth who turn 21

while enrolled in EFC to continue receiving EFC support through September 2021.

Fiscal Year Caseload Change

Risks to the Forecast

The risks to the EFC forecast are moderate. The future rate of caseload growth is less certain

because program participation was directly impacted by a variety of policy changes in recent

years.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 1,063 1,073 10 0.9%

Aug-21 1,079 1,094 15 1.4%

Sep-21 1,101 1,126 25 2.3%

Oct-21 829 839 10 1.2%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 259

2015 365 106 40.8%

2016 465 100 27.4%

2017 533 68 14.6%

2018 586 53 10.0%

2019 663 77 13.2%

2020 747 84 12.6%

2021 849 102 13.7%

Forecast 2022 904 55 6.5%

2023 860 -44 -4.9%

39

Forecast Contact:

Erik Sund 360-664-9374

Children’s Services Adoption Support

Caseload Forecast Council

February 11, 2022

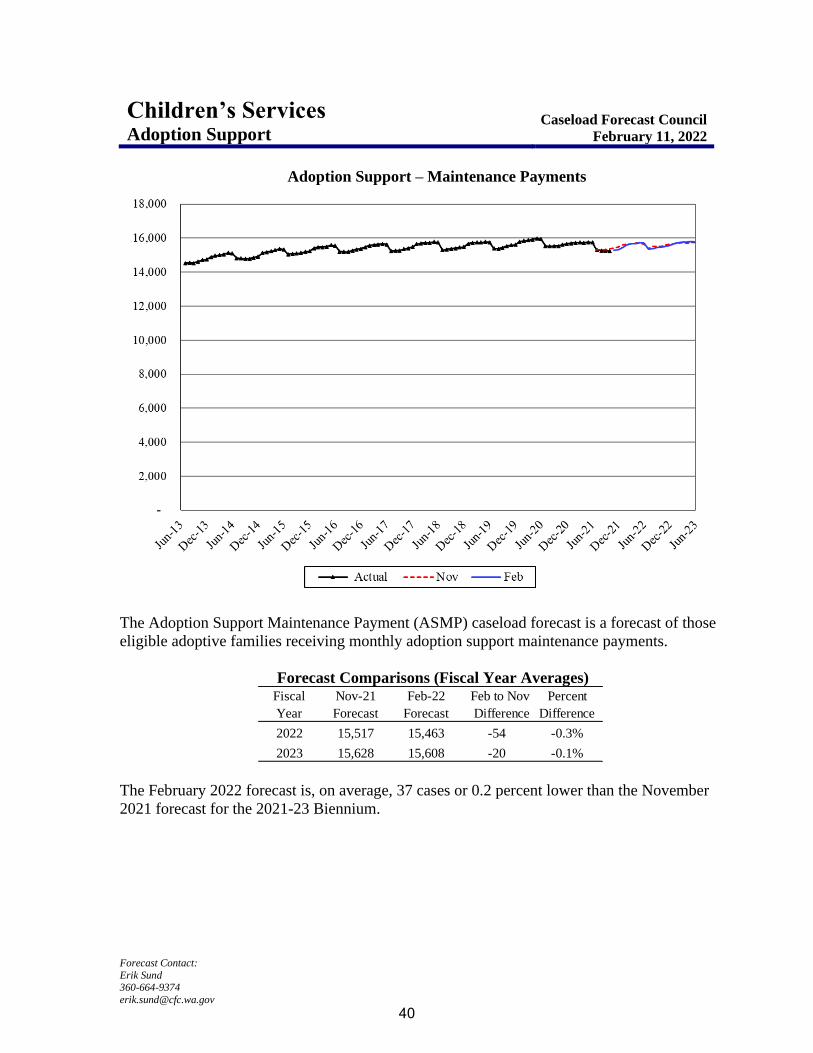

Adoption Support – Maintenance Payments

The Adoption Support Maintenance Payment (ASMP) caseload forecast is a forecast of those

eligible adoptive families receiving monthly adoption support maintenance payments.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 37 cases or 0.2 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 15,517 15,463 -54 -0.3%

2023 15,628 15,608 -20 -0.1%

40

Forecast Contact:

Erik Sund 360-664-9374

Tracking the Current Forecast

Actuals are tracking, on average, 63 cases or 0.4 percent below the November forecast.

This forecast assumes that the caseload for FY 2021 and early FY 2022 have been negatively

impacted by the COVID-19 pandemic and that, starting from January 2022, this caseload will

gradually return to levels more like those seen in the years immediately prior to the pandemic.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to the ASMP forecast are low as it is a relatively stable caseload.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 15,308 15,288 -20 -0.1%

Aug-21 15,308 15,271 -37 -0.2%

Sep-21 15,334 15,268 -66 -0.4%

Oct-21 15,379 15,251 -128 -0.8%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 14,819

2015 15,043 224 1.5%

2016 15,317 274 1.8%

2017 15,432 115 0.8%

2018 15,530 98 0.6%

2019 15,566 36 0.2%

2020 15,693 127 0.8%

2021 15,655 -39 -0.2%

Forecast 2022 15,463 -192 -1.2%

2023 15,608 145 0.9%

41

Forecast Contact:

Shidong Zhang 360-664-9370

Medical Assistance Adult Caretakers and Children

Caseload Forecast Council

February 11, 2022

Medical Assistance for Adult Caretakers and Children

The Medical Assistance for Adult Caretakers and Children category is composed of seven

caseloads for parents/caretakers, pregnant clients, and children by citizenship and income level.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 37,078 cases or 3.7 percent higher than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 1,043,180 1,071,302 28,123 2.7%

2023 945,195 991,229 46,034 4.9%

42

Forecast Contact:

Shidong Zhang 360-664-9370

Tracking the Current Forecast

Actuals are tracking, on average, 434 cases or a negligible percent above the November

forecast.

This February forecast updated two critical assumptions:

1. Extending the assumed Public Health Emergency (PHE) ending date from January 16,

2022 to June 30, 2022. In the PHE period, the Health Care Authority (HCA) cannot

terminate a client’s eligibility except for a few exemptions according to the Families

First Coronavirus Response Act (FFCRA), resulting in a continuous accumulation of

this caseload. On the other hand, it also reduced new enrollments and related potential

client pool. The changes of the PHE ending date assumption are the primary reason

for forecast changes in the pandemic period.

2. Extending the post-PHE eligibility re-determination completion time from 6 months

to 12 months. After the PHE, HCA will start to process the accumulated cases

according to federal requirements. The longer processing time assumption resulted in

a higher caseload forecast.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to this forecast are high because of the uncertainties of the COVID-19 impact and

corresponding economic and policy impacts, especially the uncertainties of the PHE ending

time and the post PHE eligibility re-determination processing time.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 1,045,983 1,047,056 1,073 0.1%

Aug-21 1,053,025 1,053,784 759 0.1%

Sep-21 1,058,108 1,058,561 454 0.0%

Oct-21 1,062,201 1,061,652 -549 -0.1%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 889,916

2015 949,123 59,208 6.7%

2016 986,444 37,321 3.9%

2017 996,893 10,449 1.1%

2018 988,464 -8,430 -0.8%

2019 972,688 -15,776 -1.6%

2020 966,060 -6,628 -0.7%

2021 1,020,234 54,174 5.6%

Forecast 2022 1,071,302 51,068 5.0%

2023 991,229 -80,073 -7.5%

43

Forecast Contact:

Shidong Zhang 360-664-9370

Medical Assistance Low Income Adults

Caseload Forecast Council

February 11, 2022

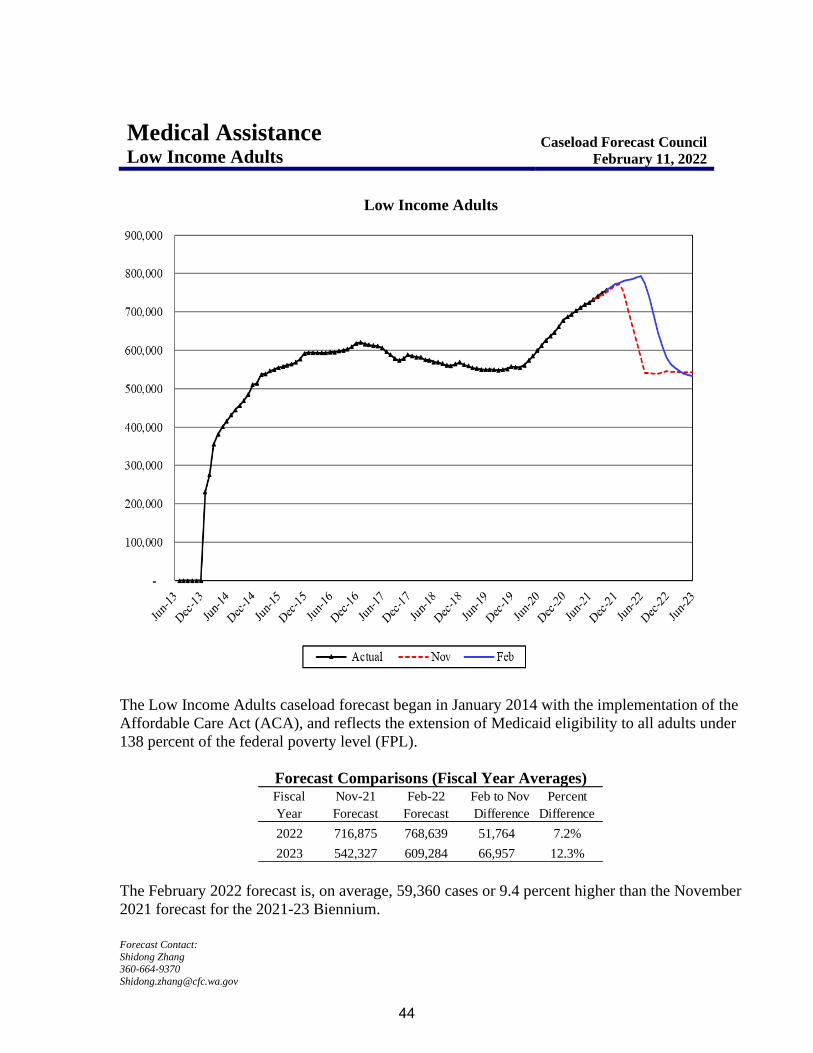

Low Income Adults

The Low Income Adults caseload forecast began in January 2014 with the implementation of the

Affordable Care Act (ACA), and reflects the extension of Medicaid eligibility to all adults under

138 percent of the federal poverty level (FPL).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 59,360 cases or 9.4 percent higher than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 716,875 768,639 51,764 7.2%

2023 542,327 609,284 66,957 12.3%

44

Forecast Contact:

Shidong Zhang 360-664-9370

Tracking the Current Forecast

Actuals are tracking, on average, 3,525 cases or 0.5 percent above the November forecast.

This February forecast updated two critical assumptions:

1. Extending the assumed Public Health Emergency (PHE) ending date from January 16,

2022 to June 30, 2022. In the PHE period, the Health Care Authority (HCA) cannot

terminate a client’s eligibility except for a few exemptions according to the Families

First Coronavirus Response Act (FFCRA), resulting in a continuous accumulation of

this caseload. On the other hand, it also reduced new enrollments and related potential

client pool. The changes of the PHE ending date assumption are the primary reason

for forecast changes in the pandemic period.

2. Extending the post-PHE eligibility re-determination completion time from 6 months

to 12 months. After the PHE, HCA will start to process the accumulated cases

according to federal requirements. The longer processing time assumption resulted in

a higher caseload forecast.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to this forecast are high because of the uncertainties of the COVID-19 impact and

corresponding economic and policy impacts, especially the uncertainties of the PHE ending time

and the post PHE eligibility re-determination processing time.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 732,046 732,740 693 0.1%

Aug-21 738,881 741,489 2,608 0.4%

Sep-21 744,825 749,728 4,904 0.7%

Oct-21 750,564 756,457 5,893 0.8%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 171,842

2015 503,331 331,489 192.9%

2016 582,126 78,795 15.7%

2017 608,845 26,719 4.6%

2018 581,128 -27,717 -4.6%

2019 559,726 -21,402 -3.7%

2020 561,665 1,938 0.3%

2021 675,256 113,592 20.2%

Forecast 2022 768,639 93,383 13.8%

2023 609,284 -159,355 -20.7%

45

Forecast Contact:

Shidong Zhang 360-664-9370

Medical Assistance Aged, Disabled and Other Medical

Caseload Forecast Council

February 11, 2022

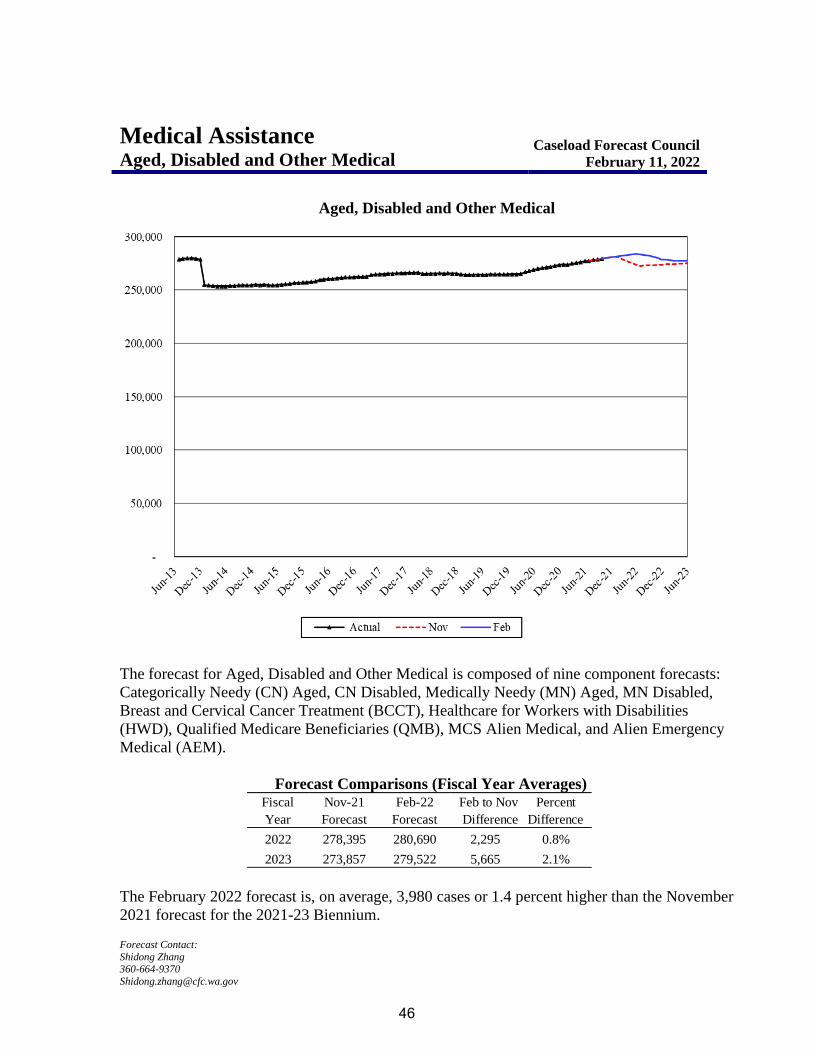

Aged, Disabled and Other Medical

The forecast for Aged, Disabled and Other Medical is composed of nine component forecasts:

Categorically Needy (CN) Aged, CN Disabled, Medically Needy (MN) Aged, MN Disabled,

Breast and Cervical Cancer Treatment (BCCT), Healthcare for Workers with Disabilities

(HWD), Qualified Medicare Beneficiaries (QMB), MCS Alien Medical, and Alien Emergency

Medical (AEM).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 3,980 cases or 1.4 percent higher than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 278,395 280,690 2,295 0.8%

2023 273,857 279,522 5,665 2.1%

46

Forecast Contact:

Shidong Zhang 360-664-9370

Tracking the Current Forecast

Actuals are tracking, on average, 100 cases or a negligible percent below the November

forecast.

This February forecast updated two critical assumptions:

1. Extending the assumed Public Health Emergency (PHE) ending date from January 16,

2022 to June 30, 2022. In the PHE period, the Health Care Authority (HCA) cannot

terminate a client’s eligibility except for a few exemptions according to the Families

First Coronavirus Response Act (FFCRA), resulting in a continuous accumulation of

this caseload. On the other hand, it also reduced new enrollments and related potential

client pool. The changes of the PHE ending date assumption are the primary reason

for forecast changes in the pandemic period.

2. Extending the post-PHE eligibility re-determination completion time from 6 months

to 12 months. After the PHE, HCA will start to process the accumulated cases

according to federal requirements. The longer processing time assumption resulted in

a higher caseload forecast.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to this forecast are high because of the uncertainties of the COVID-19 impact and

corresponding economic and policy impacts, especially the uncertainties of the PHE ending

time and the post PHE eligibility re-determination processing time.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 277,498 277,360 -138 0.0%

Aug-21 278,127 278,086 -41 0.0%

Sep-21 278,765 278,759 -6 0.0%

Oct-21 279,463 279,248 -216 -0.1%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 266,626

2015 254,523 -12,103 -4.5%

2016 257,518 2,995 1.2%

2017 262,535 5,017 1.9%

2018 265,611 3,075 1.2%

2019 264,910 -701 -0.3%

2020 265,572 662 0.3%

2021 273,448 7,876 3.0%

Forecast 2022 280,690 7,242 2.6%

2023 279,522 -1,167 -0.4%

47

Forecast Contact:

Shidong Zhang 360-664-9370

Long Term Care Nursing Homes

Caseload Forecast Council

February 11, 2022

Nursing Homes

The Nursing Homes (NH) forecast consists of Medicaid eligible clients who receive care in

state licensed nursing facilities. Nursing facilities provide care to eligible clients who require

short post-hospital, recuperative care, are no longer capable of independent living and require

nursing services or are patients with chronic disabilities needing long-term rehabilitation

and/or medical services.

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 163 cases or 1.9 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 8,274 8,103 -171 -2.1%

2023 8,811 8,656 -155 -1.8%

48

Forecast Contact:

Shidong Zhang 360-664-9370

Tracking the Current Forecast

Actuals are tracking, on average, 87 cases or 1.1 percent below the November forecast.

The February forecast change reflects the extension of the Public Health Emergency (PHE)

ending date assumption from January 16, 2022 to June 30, 2022. As in previous forecasts, the

assumption of a caseload rebound to the pre-pandemic normal is pegged to PHE because PHE

reflects federal government’s belief of the pandemic situation.

Fiscal Year Caseload Change

This caseload has been hit hard by COVID-19. Many clients left NH facilities in the first two

pandemic waves around April 2020 and January 2021.

Risks to the Forecast

The risks to the nursing homes forecast are high due to the significant downward effect that the

COVID-19 pandemic has had on nursing homes. There are many layers of uncertainty in terms

of when the caseload will begin to rebound, how long a rebound will take, and at what level the

caseload reaches when it eventually resumes to a steady state.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 7,925 7,899 -26 -0.3%

Aug-21 7,961 7,951 -10 -0.1%

Sep-21 8,101 7,875 -226 -2.8%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 10,150

2015 10,032 -119 -1.2%

2016 9,915 -117 -1.2%

2017 9,775 -140 -1.4%

2018 9,706 -69 -0.7%

2019 9,635 -71 -0.7%

2020 9,212 -423 -4.4%

2021 7,968 -1,244 -13.5%

Forecast 2022 8,103 135 1.7%

2023 8,656 553 6.8%

49

Forecast Contact:

Shidong Zhang 360-664-9370

Long Term Care Home and Community Services (HCS)

Caseload Forecast Council

February 11, 2022

Home and Community Services

The Home and Community Services (HCS) promote, plan, develop, and provide long-term

care services for persons with disabilities and the elderly who may need Medicaid to help pay

for them. The services can be provided through individual provider (IP), agency provider

(AP), adult family homes (AFH), adult residential centers (ARC), assisted living (AL), and

Program of All-inclusive Care for the Elderly (PACE).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 810 cases or 1.2 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 64,779 64,032 -746 -1.2%

2023 67,239 66,364 -874 -1.3%

50

Forecast Contact:

Shidong Zhang 360-664-9370

Tracking the Current Forecast

Actuals are tracking, on average, 670 cases or 1.0 percent below the November forecast.

The February forecast change is primarily due to adjusting the AP and ARC caseload forecasts

lower, largely because of a tight job market. In addition, this forecast added a step adjustment to

quantify a planned PACE program expansion starting in February 2022.

Fiscal Year Caseload Change

Caseload growth for the 2021-23 Biennium is projected to be lower than projected in the

November forecast, primarily due to the above-mentioned adjustment.

Risks to the Forecast

Risks to this forecast are moderate mainly due to a tight job market making it challenging to

hire qualified staff.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 63,611 63,191 -420 -0.7%

Aug-21 63,889 63,175 -714 -1.1%

Sep-21 64,077 63,200 -877 -1.4%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 49,714

2015 52,275 2,561 5.2%

2016 54,082 1,807 3.5%

2017 53,618 -464 -0.9%

2018 55,392 1,774 3.3%

2019 57,235 1,843 3.3%

2020 59,713 2,478 4.3%

2021 62,111 2,398 4.0%

Forecast 2022 64,032 1,921 3.1%

2023 66,364 2,332 3.6%

51

Forecast Contact:

Shidong Zhang (360) 664-9370

Developmental Disabilities Personal Care Services

Caseload Forecast Council

February 11, 2022

DDA Personal Care

The DDA Personal Care caseload includes adults and children receiving Medicaid personal

care services. These services can be provided through individual provider (IP), agency

provider (AP), adult family homes (AFH) or adult residential centers (ARC).

Forecast Comparisons (Fiscal Year Averages)

The February 2022 forecast is, on average, 423 cases or 2.5 percent lower than the November

2021 forecast for the 2021-23 Biennium.

Fiscal

Year

Nov-21

Forecast

Feb-22

Forecast

Feb to Nov

Difference

Percent

Difference

2022 16,552 16,184 -367 -2.2%

2023 17,173 16,695 -478 -2.8%

52

Forecast Contact:

Shidong Zhang (360) 664-9370

Tracking the Current Forecast

Actuals are tracking, on average, 340 cases or 2.1 percent below the November forecast.

The agency provider (AP) caseload has stabilized at a lower level after an initial COVID-related

exit spike in April 2020. The individual provider (IP) caseload shows significant exit jumps

related to COVID waves around April 2020 and January 2021, in addition to a relatively smaller

delta variant wave that not assumed in the November forecast. The AFH and ARC forecasts are

consistent with previous forecasts.

Fiscal Year Caseload Change

Risks to the Forecast

Risks to the overall forecast are moderate due to the volatility introduced by the COVID-19

pandemic, primarily impacting the Agency and Individual Provider caseload trends.

Nov-21 Percent

Forecast Actual Variance Variance

Jul-21 16,228 15,944 -284 -1.7%

Aug-21 16,292 15,986 -306 -1.9%

Sep-21 16,353 15,925 -428 -2.6%

Fiscal Year Caseload

Change from

Prior Year

Percent

Change

Actual 2014 12,672

2015 12,831 159 1.3%

2016 13,143 312 2.4%

2017 13,722 580 4.4%

2018 14,586 863 6.3%

2019 15,263 677 4.6%

2020 15,671 408 2.7%

2021 15,901 230 1.5%

Forecast 2022 16,184 283 1.8%

2023 16,695 511 3.2%

53