Commercial and Industrial Transaction Turnover Buoyant · latest June vacancy survey results...

4

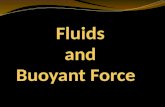

New Zealand Research Report | August 2019 | Colliers International Research 0 1 2 3 4 5 6 7 8 9 No. of Transactions (Thousands) < $2 mil $2 mil to $4.9 mil $5 mil to $9.9 mil $10 mil + 1 August 2019 Colliers’ annual national sales database for all commercial and industrial sales 1 shows 2018 was another stand-out year, with the total value up 2.4% on 2017. A review of 2019 deals so far and an analysis of transaction activity over the past three decades provides interesting insight on the year ahead. In New Zealand, the total number of commercial and industrial transactions in 2018 reached just over 4,860 properties, representing $9.9 billion in total value 1 . This is a couple of hundred short of 2017’s total turnover, but up 2.4% in total value. Given the lag in data reporting, total sales for 2018 could still shift up slightly. Office was the stand-out sector for 2018. There were almost 600 sales representing $3 billion of transactions, the strongest annual result for office on record since our monitoring began in the late 1980s. Industrial remains the stalwart of transaction activity. Around half of all transactions in 2018 were in the industrial sector, representing just under 40% of the total value. This is a similar occurrence year in, year out. Despite the somewhat mixed market commentary surrounding retail property, sales turnover in 2018 was around 2%, representing almost $2 billion. This signals opportunities are still to be found. Across New Zealand, the most transactions were recorded in Auckland, with around one third of transactions and a total value turnover of $5.5 billion. The next two biggest cities, Wellington and Christchurch, provided approximately one quarter of sales volume. Christchurch sales activity was just shy of $1 billion in 2018 representing two thirds of the South Island’s total transaction value. Sales activity in Wellington climbed from 9.4% of all transactions nationally in 2017 to 11.2% in 2018. Total value of sales activity reached $930 million in 2018. 1 Commercial and industrial properties as well as vacant land that transacts for $10,000 or more sold by any agency or privately. Commercial and Industrial Transaction Turnover Buoyant Commercial & Industrial Sales by Sector Source: CoreLogic, Colliers International Commercial and Industrial Sales by Location Source: CoreLogic, Colliers International Commercial and Industrial Sales by Price Source: CoreLogic, Colliers International 0 2 4 6 8 10 $0 $2 $4 $6 $8 $10 $12 No. of Transactions (Thousands) Total Value ($Billions) Auckland Region Wellington Region Christchurch Region Rest of NZ Total Transactions 0 2 4 6 8 10 $0 $2 $4 $6 $8 $10 $12 No. of Transactions (Thousands) Total value (Billions) Commercial Mixed & Vacant Retail Office Industrial Total Transactions

Transcript of Commercial and Industrial Transaction Turnover Buoyant · latest June vacancy survey results...

New Zealand Research Report | August 2019 | Colliers International Research

0

1

2

3

4

5

6

7

8

9

No. of T

ransactio

ns (

Th

ousands)

< $2 mil $2 mil to $4.9 mil $5 mil to $9.9 mil $10 mil +

1

August 2019

Colliers’ annual national sales database for all

commercial and industrial sales1 shows 2018 was

another stand-out year, with the total value up 2.4%

on 2017. A review of 2019 deals so far and an

analysis of transaction activity over the past three

decades provides interesting insight on the year

ahead.

In New Zealand, the total number of commercial and

industrial transactions in 2018 reached just over

4,860 properties, representing $9.9 billion in total

value1. This is a couple of hundred short of 2017’s

total turnover, but up 2.4% in total value. Given the

lag in data reporting, total sales for 2018 could still

shift up slightly.

Office was the stand-out sector for 2018. There were

almost 600 sales representing $3 billion of

transactions, the strongest annual result for office on

record since our monitoring began in the late 1980s.

Industrial remains the stalwart of transaction activity.

Around half of all transactions in 2018 were in the

industrial sector, representing just under 40% of the

total value. This is a similar occurrence year in, year

out.

Despite the somewhat mixed market commentary

surrounding retail property, sales turnover in 2018

was around 2%, representing almost $2 billion. This

signals opportunities are still to be found.

Across New Zealand, the most transactions were

recorded in Auckland, with around one third of

transactions and a total value turnover of $5.5 billion.

The next two biggest cities, Wellington and

Christchurch, provided approximately one quarter of

sales volume.

Christchurch sales activity was just shy of $1 billion

in 2018 representing two thirds of the South Island’s

total transaction value.

Sales activity in Wellington climbed from 9.4% of all

transactions nationally in 2017 to 11.2% in 2018.

Total value of sales activity reached $930 million in

2018.

1 Commercial and industrial properties as well as vacant land that

transacts for $10,000 or more sold by any agency or privately.

Commercial and Industrial Transaction Turnover Buoyant Commercial & Industrial Sales by Sector

Source: CoreLogic, Colliers International

Commercial and Industrial Sales by Location

Source: CoreLogic, Colliers International

Commercial and Industrial Sales by Price

Source: CoreLogic, Colliers International

0

2

4

6

8

10

$0

$2

$4

$6

$8

$10

$12

No. of T

ransactio

ns (

Th

ousands)

To

tal V

alu

e (

$B

illio

ns)

Auckland Region Wellington Region

Christchurch Region Rest of NZ

Total Transactions

0

2

4

6

8

10

$0

$2

$4

$6

$8

$10

$12

No. of T

ransactio

ns (

Th

ousands)

To

tal valu

e (

Bill

ions)

Commercial Mixed & Vacant RetailOffice IndustrialTotal Transactions

New Zealand Research Report | August 2019 | Colliers International ResearchNew Zealand Research Report | August 2019 | Colliers International Research

15%

17%

19%

21%

23%

25%

27%

29%

31%

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Pro

port

ion(%

)

Q1 Q2 Q3 Q4

New Zealand Key Economic Indicators – August 2019

Mar-19

(yr rate)

Mar-19

(qtr rate)

Dec-18

(qtr rate)

Q-o-Q

Change

Mar-18

(yr rate)

Y-o-Y

Change 2020F* 2021F* 2022F*

GDP Growth 2.5% 0.6% 0.6% -0.1% 3.1% -0.6% 2.3% 2.6% 2.6%

Current Account (% of GDP) -3.6% NA NA NA -3.0% -0.6% -3.8% -4.8% -4.8%

Mar-19

(yr rate)

Mar-19

(qtr rate)

Dec-18

(qtr rate)

Q-o-Q

Change

Mar-18

(yr rate)

Y-o-Y

Change 2020F* 2021F* 2022F*

CPI Inflation 1.5% 0.1% 0.1% 0.0% 1.1% 0.4% 1.6% 1.8% 1.8%

Net Migration Gain (000's) 56 16 15 1 51 5 46 33 33

Retail Sales (ex-auto) 4.7% 0.5% 2.3% -1.9% 4.5% 0.2% 4.1% 4.8% 4.8%

Unemployment Rate 4.2% 4.2% 4.3% -0.1% 4.6% -0.4% 4.3% 4.3% 4.3%

May-19

(yr rate)

Apr-19

(yr rate)

M-o-M

Change

May-18

(yr rate)

Y-o-Y

Change

10 Year

Average2020F* 2021F* 2022F*

Tourist Numbers Growth -1.7% 1.3% -0.2% 5.1% -6.8% 4.4% 4.5% 4.0% 4.7%

Official Cash Rate 1.5% 1.75% -25 bps 1.8% -25 bps 2.37% 1.25% 1.25% 1.25%

90 Day Bank Bill Rate 1.7% 1.8% -9 bps 2.0% -30 bps 2.6% 1.5% 1.4% 1.4%

10 Year Government Bond 1.8% 2.0% -17 bps 2.8% -99 bps 3.6% 2.6% 3.0% 3.0%

Floating Mortgage Rate 5.7% 5.9% -12 bps 5.9% -12 bps 6.0% 5.4% 5.4% 5.4%

3 Year Fixed Housing Rate 4.7% 4.8% -11 bps 5.3% -54 bps 6.1% NA NA NA

Consumer Confidence 119 123 -3% 121 -1% 120 NA NA NA

NZD vs US 0.67 0.67 0% 0.70 -3% 0.75 0.65 0.65 0.65

NZD vs UK 0.51 0.52 0% 0.52 0% 0.50 0.49 0.47 0.47

NZD vs Australia 0.94 0.95 0% 0.92 2% 0.87 0.89 0.86 0.86

NZD vs Japan 75 75 0% 76 -2% 74 74 73 73

NZD vs Euro 0.60 0.60 0% 0.59 2% 0.60 0.60 0.62 0.62

Source: NZIER, Colliers International Research

*March year forecast

2

So, what about 2019? Sales transactions for 2019 are

filtering through, and it looks like we will be off to a

modest start. This slower pace of activity is not due to

any disruption on investor behaviour arising from

proposed CGT as some original concerns suggested.

We have analysed transactions since 1998, which

indicate that there were only three times in the past three

decades when first quarter sales activity was

proportionally higher than other quarters, recorded in

2000, 2007 and 2008. It also came close in 1990 and

1997. These were of course all years of economic or

financial disruption.

There are no signs of that so far. The chart adjacent

highlights that over the past five years, first quarter

activity has stabilised at just over 20% of annual turnover.

With a similar number of property deals recorded in the

first quarter of 2019 as in the past few years, this gives us

guidance that 2019 is on track for a solid year of activity.

However, there is one new pattern emerging that has the

potential to offset the momentum. Since 2016, the second

quarter of the year has become the most active while

third quarter activity has slowed. This is a relatively rare

occurrence, recorded only twice before 2016 - in 1996

and 2007. If we do have a strong second quarter and a

lacklustre third quarter, it could suggest sales activity at

its lowest point since 2013. This could be exacerbated by

everyone focussed on the Rugby World Cup 2019, which

runs from Sep 20th to Nov 2nd. Only seven weeks to go!

Commercial Interest Rate Guide

Date3 Year Term

(Indicative Borrowing Rate)

Mar-19 4.47%

Apr-19 4.15%

May-19 4.06%

Jun-19 4.51%

Jul-19 4.41%

Aug-19 4.30%

Source: ANZ, Colliers International Research

Note: the lending rate quoted in the table is not necessarily

what you will be offered, and should be regarded as indicating

medium term trends.

Commercial & Industrial Sales Volumes by Quarter

Source: CoreLogic, Colliers International

New Zealand Research Report | August 2019 | Colliers International Research

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Wellington Auckland

OfficeAuckland CBD office space remains in solid demand as our

latest June vacancy survey results recorded a drop to 5.0%

vacancy rate compared to last year’s 6.2%. Prime vacancy

fell to a low of 2.8% representing less than 18,000 sqm of

available space. Secondary vacancy has dropped to 6.6%

compared to the previous year’s 8.1% vacancy rate.

A supply-side response is underway. Approximately 162,850

sqm of space is under construction. While this will add to the

total available space, pre-commitment rates are increasing.

Pockets of opportunity are available and coworking space

assists short-term requirements, but not all tenant

requirements match supply availability.

In Wellington, the overall vacancy rate reached a record low

5.9% with prime vacancy less than 1%. Secondary vacancy is

at 7.3%, well down from the 9.5% vacancy rate a year ago.

While leasing activity is up, less available space is also

attributable to office premises undergoing refurbishments

and/or earthquake strengthening.

IndustrialTwo major industrial sales in Auckland and Hamilton highlight

the ongoing attractiveness of the sector for local and offshore

investors.

Asia Pacific logistics specialist LOGOS has partnered with

Australia’s largest superannuation and pension fund,

AustralianSuper to extend the 10ha of land originally

purchased last year. The intention is to develop 24 hectares

of land in Wiri, Auckland, transforming the site into a $500

million logistics estate. Land values have been rising in

Auckland over the last few years, with values closer to around

$600 per sqm or more in the area.

A confidential purchaser has also secured an 8.51 hectare

site at 122 Ingham Road, Hamilton. The site has a 36,000

sqm industrial facility with a 20-year lease to the New

Zealand subsidiary of global packaging and paper company,

Visy Industries. While sale details are confidential, high-

profile industrial developments have sold for a yield of

between 4% and 5%.

Retail

Retail spending in the June quarter continued to rise

modestly. Electronic card transactions data from Statistics NZ

shows spending in core retail industries rose 0.7% from the

March 2019 quarter.

When compared across the previous four June quarters,

consumables and hospitality have increased solidly. Strong

sales growth in both the takeaway and restaurant/café

sectors were also recorded. According to the Restaurant

Association of New Zealand, seven new hospitality outlets

are opening across New Zealand daily.

3

Source: StatsNZ, Colliers International Research

Auckland and Wellington CBD Office Vacancy Rate

Source: Colliers International Research

Source: Colliers International Research

0

1

2

3

4

5

6

7

$ (

bill

ions)

Jun-16 Jun-17 Jun-18 Jun-19

Electronic Card Transactions by Value

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Jul-

19

Ne

t P

osi

tive

In

vest

or

Co

nfi

de

nce

New Zealand Overall OfficeIndustrial Retail

Commercial Property Investor Confidence Survey

New Zealand Research Report | August 2019 | Colliers International ResearchNew Zealand Research Report | August 2019 | Colliers International Research

Source: Colliers International Research

*Combination of industrial office & warehouse at a ratio of 20:80.

4

Annual Market Indicator Review – Q2 2019

Recent Commercial Property Sales

Alan McMahon

National Director

Strategic Advisory

David White

Director

Strategic Advisory

For more information contact:

Chris Dibble

Director

Research & Communications

Adrian Goh

Research Analyst

Anna Sizova

Research Analyst

Emily Duncan

Research Analyst

Disclaimer: Whilst all care has been taken to provide reasonably accurate information, Colliers International cannot guarantee the validity of all data and

information utilised in preparing this research. Accordingly Colliers International New Zealand Ltd, do not make any representation of warranty, expressed

or implied, as to the accuracy or completeness of the content contained herein and no legal liability is to be assumed or implied with respect thereto.

© All content is Copyright Colliers International New Zealand Ltd, Licensed REAA 2008 and may not be reproduced without expressed permission.

Chris Farhi

Director

Strategic Advisory

Caity Pask

Senior Analyst

Strategic Advisory

Vernon Sequeira

Analyst

Strategic Advisory

Colliers International

Level 27, SAP

Tower

151 Queen Street

Auckland

+64 9 358 1888

120 Wairau Valley Road, Wairau Valley

Auckland | $4,325,000 | 4.1%

Property Sector

Prime Rents

(% Change)

Prime Capital Values

(% Change)Vacancy Rate

12-Months to Jun-19 12-Months to Jun-19 2018 2019

Office Net Face Based on Net Face Overall (June)

Auckland CBD 1.5% 6.0% 6.2% 5.0%

Office Gross Face Based on Net Face Overall (June)

Wellington CBD 6.5% 4.3% 7.7% 5.9%

Office Net Face Based on Net Face Overall (March)

Auckland Metropolitan 2.6% 9.8% 6.0% 6.3%

Industrial* Net Face Based on Net Face Overall (February)

Auckland 3.8% 14.1% 2.2% 1.5%

Industrial* Gross Face Based on Net Face Overall (November)

Wellington 7.3% 10.9% 2.1% (2017) 1.5% (2018)

Industrial* Net Face Based on Net Face Overall (September)

Christchurch -0.8% 2.3% 1.9% (2016) N/A

Retail Net Face Based on Net Face Overall (June)

Auckland CBD 0.0% 0.0% 3.8% 5.7%

Retail Gross Face Based on Net Face Overall (June)

Wellington CBD 2.3% 3.5% 6.8% 4.2%

Corner of Wordsworth / Hawdon & Kingsley

Street, Sydenham

Christchurch | $2,615,000

758 Dominion Road, Mt Eden

Auckland | $1,227,000 | 5.8%