Collie SuperTown Combined Report - South West report - collie supertow… · Collie SuperTown...

130

Collie SuperTown Combined Report South West Development Commission Final Draft Report April, 2012

-

Upload

nguyenminh -

Category

Documents

-

view

217 -

download

1

Transcript of Collie SuperTown Combined Report - South West report - collie supertow… · Collie SuperTown...

Collie SuperTown

Combined Report

South West Development Commission

Final Draft Report

April, 2012

Collie SuperTown Combined Report

Final Draft Report

i

Document Control

Job ID: 16132

Job Name: SWDC ED Plans for Three SuperTowns in SW WA

Client: South West Development Commission

Client Contact: Richard Oades

Project Manager: Michael Campbell

Email: [email protected]

Telephone: 0409 349 256

Document Name: AECgroup Report - Collie SuperTown Combined Report - Final Draft Report

Last Saved: 10/4/2012 2:36 PM

Version Date Reviewed Approved

Draft Report 20 February 2012 MC SS

Draft Report V2.0 24 February 2012 MC SS

Final Draft Report 2 March 2012 MC SS

Final Combined Report 10 April 2012 MC SS

Collie SuperTown Combined Report

Final Draft Report

ii

Executive Summary

Introduction

SuperTowns (Regional Centres Development Plan) is a Royalties for Regions initiative to encourage regional communities in the southern half of the state to plan and prepare for the future so they can take advantage of opportunities created by Western Australia’s population growth to 2050. Western Australia's population is predicted to more than double over the next 40 years to 4.9 million people.

The SuperTowns' vision is to have balanced communities, with lifestyle options and access to services. They will have affordable, quality housing and a diverse range of job opportunities. The towns will offer more choices for people to live in regional areas and an attractive alternative to living in the metropolitan area.

Nine SuperTowns were selected throughout Western Australia to achieve this vision and accommodate future population growth. Within the South West Development Commission (SWDC) Region the areas Manjimup, Collie and Margaret River were selected as SuperTowns under the Royalties for Regions program.

This document provides the Economic Development Plan for the Shire of Collie.

Collie benefits from a range of economic drivers which will assist in its economic development into the future. Whilst economic diversification is a key focus of the economic development of Collie, improvements in the amenity of Collie will also be required in order to attract the desired population to the area.

Population & Demographics

Collie has a population of 9,470 people and has historically experienced slow growth of 0.5% p.a. - well below State and regional averages. Collie has a relatively young population due to high proportions of families with children. However, Collie has historically had difficulties in retaining its youth post-school due to a limited availability of education and training and employment opportunities outside of the mining and industrial sector activities.

The majority of residents of working age are blue collar workers due to the strength of the local mining and industrial sectors which have high demands for technicians and trades workers and machinery operators and drivers.

Average incomes in Collie are typically above the State and broader regional averages. This is largely due to the higher wages that are paid by the mining sector. Higher average wages usually results in higher median dwelling prices, however, Collie has an affordable housing market with lower median dwelling prices compared to the median for the SWDC Region and regional Western Australia.

Employment & Business Activity

Collie is the mining and industrial hub of the SWDC region and employs around 45% of its workforce either in local coal mining, alumina refining or electricity generated from the local coal production activities.

Collie has a labour force of 4,918 people and 4,598 people were employed in June Quarter 2011. Unemployment rates in Collie have historically been substantially higher than the SWDC region and Western Australia unemployment rates.

Sixty percent (60%) of Collie's businesses are small businesses and almost a quarter of all businesses undertake agriculture, forestry and fishing activities. Collie also has higher proportions of medium-sized businesses (20 to 49) as well as larger businesses (100+ employees) than the SWDC region and State averages. This is due to the presence of major industry players in the mining and manufacturing sector in Collie as well as a good representation of medium-sized construction businesses and supporting supply chain.

Disclaimer:

Whilst all care and diligence have been exercised in the preparation of this report, AEC Group Limited does not warrant the accuracy of the information contained within and accepts no liability for any loss or damage that

may be suffered as a result of reliance on this information, whether or not there has been any error, omission or negligence on the part of AEC Group Limited or their employees. Any forecasts or projections used in the

analysis can be affected by a number of unforeseen variables, and as such no warranty is given that a

particular set of results will in fact be achieved.

Collie SuperTown Combined Report

Final Draft Report

iii

Investment & Major Projects

Collie is currently experiencing significant levels of investment in mining and industry related projects and supporting infrastructure. The Shotts Industrial Estate is one of these projects, and is located adjacent to the Premier Coal mine. The estate is a strategic land project for coal-related industrial uses and will look to accommodate five tenants, complementing the Coolangatta heavy industrial estate. $83 million in funding has been provided by the State government to fund infrastructure upgrades to support Shotts Industrial Park.

Perdaman Chemicals and Fertilisers and Premier Coal will be the major tenants of the estate. Perdaman is planning to develop a $3.8 billion urea manufacturing plant at the site.

Significant investment of $2 billion has also made by BHP Billiton in the expansion of the Worsley Alumina Refinery.

These major projects will have the capacity to drive economic activity, not only during the construction phase but during the operational phases as well.

Economic Growth

Collie's estimated Gross Regional Product (GRP) has grown steadily by an average of 14.2% per annum since 2006-07 to over $2 billion in 2010-11.

Overall, 90% of Collie's industry value add is generated by mining, electricity, manufacturing and construction types of activities - making Collie a mining and industrial focussed region with little diversification. Local industry is also required to service the growing population in Collie, providing services such as education, retail and health care. Key opportunities for the Collie LGA in the future are likely to centre around capturing and localising the existing major industries' supply chains to facilitate economic growth.

Figure ES.1: Industry Structure

Source: AECgroup

Future economic growth in Collie will largely be determined by the ability of the area to diversify its economic base whilst continuing to support the activity of its leading mining and industrial sectors. Job creation will be important for sustaining population growth, as will be the provision of infrastructure and services for the local population.

Foundation Industry

•Coal mining & Electricity Generation

•Metals manufacturing

Population Serving

•Due to increased population growth, an extended regional catchment and income growth

Opportunity

• Capture of supply chains from mining sector including processing, transportation and energy sector activity

Collie SuperTown Combined Report

Final Draft Report

iv

The SuperTown Target

Under the SuperTowns’ growth plan, the aspirational growth target for Collie is a doubling of the population by 2031, resulting in an average annual growth rate of 3.4% per annum to 15,580 residents by 2031. This is equivalent to an additional 371 residents each year, which is roughly 300 more than the historical trend. This growth target is ambitious and will require significant proactive economic development in order to be achieved.

Obtaining this stretch target will require the average annual delivery of 179 new dwellings each year. This rate of dwelling development significantly exceeds the recent trend of an average delivery of 112 dwellings per year, so in order to facilitate population growth, the housing supply will also need to increase.

Figure ES. 1: Collie SuperTown Population Target, 2010-2031

Source: ABS (2011a)

Key Economic Drivers

There are four key economic growth drivers for Collie:

Increased Demand for Coal and Electricity: Population growth and economic growth in Western Australia and the South West region are expected to continue into the future, driving demand for coal and electricity from Collie's industry. As such, this future demand will ensure the future economic growth of Collie.

Coal and Alumina Sector: The Collie economy is benefitting from a range of major projects which are expanding its capacity for coal and alumina production. The expanded economic capacity of these expansions will continue to provide for economic growth in the future.

Climate Change and Carbon Tax Impacts: Climate change is making an impact on the global environment. The enactment of the Carbon Tax in July 2012 will have an impact on the way Australian businesses operate. Managing these impacts will be essential to driving future growth in Collie.

Internet: The internet has changed the way that people work and live as well as the way in which business is conducted. Ensuring that the Collie economy can tap into the internet with high speeds will be critical to the future economy.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

3,000

6,000

9,000

12,000

15,000

18,000

Po

pu

latio

n G

row

th R

ate

(%)

Po

pu

lati

on

Ta

rge

t

Collie Township Collie Township SuperTown Growth Rate Collie Township Historical Trend

Collie SuperTown Combined Report

Final Draft Report

v

Issues & Challenges

A range of issues and challenges are evident in the Collie economy which will need to be addressed if the town is to reach its goal of becoming a SuperTown. These issues include:

Existing shortage of skilled labour

Economic dependence on the coal industry

Lack of translation of the economic activity in the region into local jobs

Lack of broadband connections

Low rates of population growth and an ageing demographic

Lack of professional service delivery and supply chain gaps

These issues will need to be addressed in order for Collie to succeed in reaching its SuperTown population growth target of doubling its population by 2031. Diversifying the economy is of critical importance in Collie. A broader range of job opportunities will give incentive to young adults to stay and work in the region rather than having to leave in order to find suitable employment. Likewise, creating a range of post-school education and training options will stem the flow of young adults leaving Collie to gain further qualifications and also up-skill residents, helping to alleviate the shortage of skilled labour in Collie.

Opportunities

A range of opportunities are available to Collie to grow its economy into the future, these include:

Mining (including coal mining)

Heavy Manufacturing (including alumina manufacturing and other heavy industrial processes)

Utilities (including electricity generation)

Light Industry, Transport and Logistics (including light industry and logistics operations)

Professional Services (including population-related professional services and business-related professional services)

Health and Community (including health services, aged care services and allied health services)

Education (including high-quality secondary schooling and industry-oriented tertiary education)

Retail (including food and other retailing)

Tourism (including outdoor leisure and water activities)

The Economic Development Plan

Clearly defined and targeted action (as identified by the Economic Development Framework and both Strategic and Economic Development Initiatives) will assist in supporting the existing business community, marketing the shire, attracting and facilitating new investments into the shire and will assist in developing the local workforce. The key Strategic Initiatives are transformational projects which are inextricably linked to the Economic Development Initiatives. These projects will provide a solid base for future economic and residential growth.

This economic development plan will provide for a long-term foundation on which to achieve the goals of the SuperTowns’ initiative.

Collie SuperTown Combined Report

Final Draft Report

vi

Figure ES.2: Economic Development Plan Overview

Source: AECgroup

SuperTowns Vision: “To have balanced, well-connected regional communities, with lifestyle options and access to services – SuperTowns

will have affordable, quality housing and a growing and diverse range of job opportunities. They will offer more choices for people living in regional areas and an attractive alternative to living in the metropolitan area”

What Does it Take to

Become a SuperTown?

Improve amenity.

Grow the population.

Secure jobs locally.

Diversify the economy.

Change perceptions.

Economic Development Plan

Strategic Projects

1. Redevelopment of CBD: transforming the CBD including improving amenity of the river, redevelopment of the Wallsend Precinct, revitalisation of CBD and new community swimming pool.

2. Tourism Precincts Improvements: including new Motorplex and Lake Kepwari.

3. Wilson Park Redevelopment: urban renewal project to reinvigorate neighbourhood and raise socio-economic standing.

Economic Development Initiatives

1. Support Existing Business: develop programs to proactively engage with and assist the growth of local companies.

2. Market the Shire: marketing the Shire for new residences and businesses.

3. Attract and Facilitate New Investment: through pro-active business attraction and support.

4. Develop the Local Workforce: develop and attract new skills in the region.

Outcomes

Increased economic prosperity.

Improved economic capacity.

Increased retention of economic benefits in the local

region.

Increased opportunities.

Improved sustainability.

Increased service provision.

Collie SuperTown Combined Report

Final Draft Report

vii

Economic Growth Influences

Collie benefits from significant competitive advantages and opportunities, which could underpin strong economic and population growth over the next 20 years. In particular, the concentration of major mining, metal manufacturing and electricity generation, relative proximity to Bunbury and the associated Port and a diversity of outdoor and water sport attractions in the surrounding area, present opportunities to leverage external growth drivers and build greater local economic diversification.

However, there are some areas of weakness which will need to be addressed in order to support desired economic and population growth in Collie, which include:

An underrepresentation of skilled labour in the region, presenting capacity constraints to local business and industry growth and resulting in the inability to leverage the opportunity to become a major service centre.

Lack of translation of economic activity into local employment, with a combination of strong Drive-In/Drive-Out travel patterns to Collie from Bunbury and the surrounding region.

Low population growth and an ageing population demographic.

Lack of professional service delivery in Collie, due to the relative small size of the town and its local labour force as well as strong competition from Bunbury.

Lack of retail and residential service offering.

Collie is located within Bunbury’s regional catchment for major services like health and education.

Gaps in the supply chain with regards to industrial and professional services.

In addition to local advantages and weaknesses, a number of future economic drivers will also influence local economic conditions (such as population growth as well as the State and national economic outlook). Whilst many of these drivers are outside of the control of the Shire of Collie, proactively planning for the management of these impacts will be essential to achieving desired future economic and population outcomes.

Future Direction of the Collie Economy

The growth of the local economy needs to translate into employment if the residential population is to grow sufficiently large to support Collie’s transformation into a SuperTown. While mining and bauxite/alumina refining generate significant economic value and incomes, the operations have failed to translate to the generation of significant local jobs, reflected in above average unemployment rates in Collie.

Leveraging existing and potential new investments in mining and the bauxite/alumina refinery can create opportunities for growth in the supply chain and support service industries. This will require provision of quality, well located serviced industrial land for both light industry and transport / logistics businesses, which generate high employment yields. Additionally, commercial office floorspace is required in the township to increase Collie’s capture of professional service supply chain elements from these anchor industries.

The growth of the population of Collie, as it transforms into a SuperTown will increase demand for health and education related services. This demand will be further influenced by drivers such as population ageing and income growth. Growth in demand for these services will generate opportunities for increased economic activity, with the health sector currently the largest employing industry in Australia as well as one of the fastest growing. Opportunities exist to support the creation of a health precinct in Collie that builds upon general hospital-based health care provision to include ancillary health, sports health, retirement villages and aged care facilities.

In terms of education, increasing the scope of offering to capture secondary and tertiary education demand that currently escapes the local economy, to areas like Bunbury, will require increased cooperation and linkages with local industry. The critical mass of population in Collie in 20 years will likely remain insufficient for a full scale tertiary education offering, but partnership with mining, utility and heavy metal manufacturing

Collie SuperTown Combined Report

Final Draft Report

viii

industries can assist in the establishment and growth of niche tertiary education facilities and services. This may include industry-specific research capability. These specialty capabilities will assist in not only diversifying the economy but can act as a catalyst for change, attracting additional businesses to the area. The opportunity to offer a residential high school for families located inland from Collie who cannot afford a private boarding school may also prove to be an opportunity for education in Collie, particularly given the fact that there is a decommissioned aged care facility currently located adjacent to the existing high school.

Attracting new residents to Collie will require increases in local amenity. This includes reconnecting with the natural environment (particularly the Collie River) and revitalisation of public realm (such as the Central Business District). It also requires an increase in the scale, quality and diversity of retail offering in Collie. Enhancing the quality of the natural and urban environments along with some urban renewal in areas such as Wilson Park and increasing resident access to quality retail, health and education services will underpin efforts to attract and retain an increased population in Collie to support its transformation in a SuperTown.

This improved amenity will also increase the attractiveness of Collie to visitors. Collie has the opportunity to increase the quality of retail, café and restaurant offering for residents by capturing expenditure from visitors attracted by the region’s outdoor leisure and water sport activities. Attracting more visitors to the area would be assisted by strong transport interconnections with Bunbury and Perth and effective branding and marketing to counter Collie’s existing industrial profile. This leisure-based tourism can also be supplemented by heritage and industrial tourism activities, as well as increased business-related travel associated with the growth of the local professional services sector.

Collie SuperTown Combined Report

Final Draft Report

ix

Table of Contents

DOCUMENT CONTROL ....................................................................................... I

EXECUTIVE SUMMARY .................................................................................... II

TABLE OF CONTENTS ...................................................................................... IX

1. INTRODUCTION ....................................................................................... 1

1.1 BACKGROUND .............................................................................................. 1 1.2 PROJECT OVERVIEW ....................................................................................... 1 1.3 GEOGRAPHY ................................................................................................ 2

2. POPULATION & DEMOGRAPHIC PROFILE .................................................. 3

2.1 POPULATION & DEMOGRAPHICS .......................................................................... 3 2.1.1 HISTORICAL POPULATION ........................................................................ 3 2.1.2 POPULATION PROJECTIONS ...................................................................... 3 2.1.3 AGE STRUCTURE ................................................................................. 6 2.1.4 FAMILY/HOUSEHOLD TYPES ..................................................................... 8 2.1.5 HOUSEHOLD & DWELLING GROWTH ............................................................ 9

2.2 SOCIO-ECONOMIC CHARACTERISTICS .................................................................... 9 2.2.1 EDUCATION/QUALIFICATIONS ................................................................... 9 2.2.2 OCCUPATION .................................................................................... 10 2.2.3 INCOME .......................................................................................... 11 2.2.4 HOUSE PRICES .................................................................................. 11

2.3 KEY FINDINGS ............................................................................................ 13

3. EMPLOYMENT & BUSINESS ACTIVITY ..................................................... 14

3.1 LABOUR FORCE & UNEMPLOYMENT ...................................................................... 14 3.2 EMPLOYMENT & BUSINESS ............................................................................... 15

3.2.1 EMPLOYMENT BY INDUSTRY ..................................................................... 15 3.2.2 BUSINESS BY INDUSTRY ........................................................................ 15 3.2.3 BUSINESSES BY EMPLOYMENT SIZE ............................................................ 16 3.2.4 BUSINESSES BY TURNOVER ..................................................................... 17 3.2.5 SMALL BUSINESS ............................................................................... 17 3.2.6 TOURISM ACTIVITY.............................................................................. 18

3.3 KEY FINDINGS ............................................................................................ 20

4. INVESTMENT & MAJOR PROJECTS .......................................................... 21

4.1 BUILDING APPROVALS & PROPERTY MARKET ........................................................... 21 4.1.1 RESIDENTIAL APPROVALS ....................................................................... 21 4.1.2 NON-RESIDENTIAL APPROVALS ................................................................ 21 4.1.3 LAND RELEASES & DEVELOPMENTS ............................................................ 22

4.2 MAJOR PROJECTS ......................................................................................... 23 4.2.1 SHOTTS INDUSTRIAL ESTATE................................................................... 23 4.2.2 WORSLEY ALUMINA REFINERY EXPANSION .................................................... 23

5. ECONOMIC GROWTH .............................................................................. 24

5.1 CURRENT GROSS REGIONAL PRODUCT .................................................................. 24 5.2 FOUNDATION INDUSTRY - COAL MINING & POWER GENERATION ..................................... 25 5.3 FOUNDATION INDUSTRY - METALS MANUFACTURING ................................................... 26 5.4 KEY FINDINGS ............................................................................................ 27

6. ECONOMIC OUTLOOK ............................................................................. 28

6.1 FUTURE ECONOMIC DRIVERS............................................................................. 28 6.1.1 INTERNAL DRIVERS ............................................................................. 28 6.1.2 EXTERNAL DRIVERS ............................................................................. 28 6.1.3 REGIONAL & LOCAL DRIVERS .................................................................. 30

6.2 POTENTIAL FUTURE ECONOMIC GROWTH PATH ......................................................... 31 6.3 KEY FINDINGS ............................................................................................ 33

7. REGIONAL GAP ANALYSIS...................................................................... 34

Collie SuperTown Combined Report

Final Draft Report

x

7.1 IMPORT & EXPORT ANALYSIS ............................................................................ 34 7.2 SUPPLY CHAIN ANALYSIS ................................................................................. 36 7.3 COMPARATIVE ASSESSMENTS ............................................................................ 42 7.4 JOURNEY TO WORK ....................................................................................... 44 7.5 KEY FINDINGS ............................................................................................ 45

8. OPPORTUNITIES ASSESSMENT ............................................................... 46

8.1 LOCATION QUOTIENTS.................................................................................... 46 8.2 COMPETITIVE ASSESSMENT .............................................................................. 49

8.2.1 COMPETITIVE EDGE ............................................................................. 50 8.2.2 AREAS FOR IMPROVEMENT ...................................................................... 50

8.3 CLUSTER MAPPING ........................................................................................ 52 8.4 KEY FINDINGS ............................................................................................ 55

9. INDUSTRIAL LAND ASSESSMENT............................................................ 56

9.1 EXISTING SUPPLY & DEMAND ............................................................................ 56 9.2 FUTURE DEMAND FOR LAND .............................................................................. 56 9.3 KEY FINDINGS ............................................................................................ 57

10. RETAIL ASSESSMENT ............................................................................. 58

10.1 CATCHMENT ANALYSIS ................................................................................... 58 10.2 POPULATION GROWTH .................................................................................... 58

10.2.1 POPULATION PROJECTIONS ..................................................................... 59 10.3 RETAIL SUPPLY ............................................................................................ 60

10.3.2 RETAIL SUPPLY OUTSIDE THE CATCHMENT .................................................... 62 10.4 RETAIL EXPENDITURE ..................................................................................... 64

10.4.1 AVERAGE HOUSEHOLD RETAIL EXPENDITURE ................................................. 64 10.4.2 FORECAST HOUSEHOLD RETAIL EXPENDITURE POTENTIAL ................................... 64 10.4.3 MARKET SHARE ANALYSIS ...................................................................... 65 10.4.4 ESTIMATED RETAIL EXPENDITURE WITHIN THE CATCHMENT ................................. 66

10.5 RETAIL DEMAND .......................................................................................... 66 10.6 CURRENT DEMAND VS SUPPLY ........................................................................... 67 10.7 FUTURE DEMAND VS SUPPLY............................................................................. 68 10.8 KEY FINDINGS ............................................................................................ 69

11. COMMERCIAL & GOVERNMENT OFFICES ................................................. 70

11.1 METHODOLOGY ............................................................................................ 70 11.2 CURRENT DEMAND ........................................................................................ 71

11.2.1 COMMERCIAL OFFICE SPACE DEMAND ......................................................... 71 11.2.2 GOVERNMENT OFFICE SPACE DEMAND ........................................................ 73

11.3 PROJECTED FUTURE DEMAND ............................................................................ 73 11.3.1 COLLIE LABOUR FORCE GROWTH .............................................................. 73 11.3.2 FUTURE COMMERCIAL FLOORSPACE DEMAND ................................................. 74 11.3.3 FUTURE GOVERNMENT FLOORSPACE DEMAND ................................................. 75

11.4 KEY FINDINGS ............................................................................................ 76

12. FUTURE OPPORTUNITIES & GAPS .......................................................... 77

12.1 ECONOMIC OPPORTUNITIES .............................................................................. 77 12.2 POTENTIAL IMPEDIMENTS................................................................................. 81

13. KEY ECONOMIC DRIVERS & IMPORTANT TRENDS ................................... 82

13.1 INCREASED DEMAND FOR COAL & ELECTRICITY ........................................................ 82 13.2 COAL & ALUMINA SECTOR EXPANSION .................................................................. 82 13.3 CLIMATE CHANGE & CARBON TAX IMPACTS ............................................................ 83 13.4 INTERNET .................................................................................................. 84

14. ECONOMIC ISSUES & CHALLENGES ........................................................ 85

14.1 SKILLED LABOUR SHORTAGE ............................................................................. 85 14.2 ECONOMIC DEPENDENCE ON THE COAL INDUSTRY ..................................................... 86 14.3 TRANSLATION OF ECONOMIC ACTIVITY INTO LOCAL EMPLOYMENT .................................... 87 14.4 BROADBAND INTERNET CONNECTIONS .................................................................. 88 14.5 LOW POPULATION GROWTH & AGEING POPULATION DEMOGRAPHIC .................................. 88 14.6 PROFESSIONAL SERVICE DELIVERY ...................................................................... 90

Collie SuperTown Combined Report

Final Draft Report

xi

14.7 SUPPLY CHAIN OF INDUSTRIAL & PROFESSIONAL SERVICES ........................................... 91

15. ECONOMIC DEVELOPMENT PLAN ............................................................ 93

15.1 OVERVIEW ................................................................................................. 93 15.2 STRATEGIC PROJECTS .................................................................................... 95 15.3 ECONOMIC DEVELOPMENT INITIATIVES .................................................................. 96

15.3.1 SUPPORTING EXISTING BUSINESSES .......................................................... 96 15.3.2 MARKET THE SHIRE ............................................................................. 97 15.3.3 ATTRACT & FACILITATE NEW INVESTMENT .................................................... 97 15.3.4 DEVELOP THE LOCAL WORKFORCE ............................................................. 98

16. IMPLEMENTATION PLAN ........................................................................ 99

REFERENCES ............................................................................................... 107

APPENDIX A: MODELLING APPROACH .......................................................... 110

APPENDIX B: JOURNEY TO WORK DETAILS .................................................. 112

APPENDIX C: DETAILED LOCATION QUOTIENTS ........................................... 114

APPENDIX D: GRP METHODOLOGY ............................................................... 116

Collie SuperTown Combined Report

Final Draft Report

1

1. Introduction

1.1 Background

In recent years, a combination of robust migration-led population growth and increasingly constrained metropolitan housing markets has led to an increase in median house prices across the Perth urban area and a significant deterioration in housing affordability. The lack of population decentralisation in Western Australia limited the capacity for the State as a whole to accommodate new residents without rapid price growth, due to limited genuine alternate residential centres outside of the metropolitan area.

To provide greater levels of residential housing choice for a growing population, capitalise on existing infrastructure and capture a greater share of increased business investment in primary industries, the Government of Western Australia, through the Royalties for Regions program, established the Regional Centres Development Plan. In this Plan, nine regional centres or “SuperTowns” were identified - one of these being Collie.

The SuperTowns’ vision is to have balanced communities, with lifestyle options and access to services, with affordable, quality housing and a diverse range of job opportunities, offering an attractive alternative to living in the metropolitan area.

Collie is one of the twelve LGAs located in the South West Development Region1 in Western Australia. Augusta-Margaret River and Manjimup were also named as SuperTowns within the South West Development Region.

The town of Collie is located 60 kilometres from the regional City of Bunbury and is linked to the Bunbury Port by the Coalfields Highway and by a rail freight network. Mining and power generation are the leading sectors of the Collie economy with Collie's coal resources representing 100% of Western Australia's coal production, the majority of which is used in domestic electricity generation. Collie also produces alumina and is home to the Worsley Alumina Refinery.

1.2 Project Overview

Each SuperTown is required to prepare an Economic Development Growth Plan to assist guide the town during this growth phase.

The Economic Development Growth Plan will build on the existing strategic framework of each Shire and identify specific opportunities for economic development. This will complement, stimulate and strengthen the Growths Plans for the region. A key component of the plans will be an implementation framework comprising strategies and programs to align delivery partners, attract funding and facilitate action and investment to achieve a local vision for growth.

In the development of an Economic Development Growth Plan for the Shire of Collie, the following reports have been developed:

Socio-Economic Profile

Opportunities and Gap Analysis

Economic Development Plan

All of these reports, which were originally delivered separately, have been combined into this single report.

1 The South West Development Region is comprised of the LGAs of Bunbury, Augusta-Margaret River, Boyup Brook, Bridgetown-Greenbushes, Busselton, Capel, Collie, Dardanup, Donnybrook-Balingup, Harvey, Manjimup and

Nannup.

Collie SuperTown Combined Report

Final Draft Report

2

1.3 Geography

Data in this report is presented for the Local Government Area (LGA) of Collie, which primarily comprises the urban areas of the township of Collie and surrounding areas. Statistics in the report are primarily provided for the overall LGA, however, where relevant and available, data is reported for the Collie township (Collie Urban Centre).

In order to compare the area’s profile to other regions, and better understand its key features and strengths, statistics are benchmarked against Perth Statistical Division (SD) and Western Australia. In addition, where relevant, figures are also benchmarked against the South West Development Commission (SWDC) region, which comprises the LGAs Bunbury, Augusta-Margaret River, Boyup Brook, Bridgetown-Greenbushes, Busselton, Capel, Collie, Dardanup, Donnybrook-Balingup, Harvey, Manjimup and Nannup. This approach recognises the strong interrelationship that currently exists, and will continue to, between Collie and the surrounding South West region and the need for the benefits of Collie’s evolution to a SuperTown to flow through to surrounding townships and areas.

Collie SuperTown Combined Report

Final Draft Report

3

2. Population & Demographic Profile

This section provides an overview of historical and current population, demographic and socio-economic trends in the Collie and the impact of achieving aspirational population target for the Collie in the future.

2.1 Population & Demographics

2.1.1 Historical Population

Since 2006 the Collie LGA’s population has grown by 1.0% per annum (an average of approximately 96 additional residents each year), recording a total of 9,470 residents in 2010. This growth resulted in the expansion of the Collie Town population from 7,475 to 7,790 residents over the period, equating to 82.3% of the LGA’s population.

The recent growth in the Collie LGA’s population is below the growth of the broader SWDC region (average annual growth of 3.2% p.a.) which has been driven in large by population growth of coastal regions including Busselton (4.2% p.a.), Capel (5.6% p.a.), Dardanup (4.7% p.a.) and Harvey (3.0% p.a.).

Figure 2.1: Population Growth Comparison, 2006-2010

Source: ABS (2007), ABS (2011)

2.1.2 Population Projections

Population projections for Collie LGA are presented from three different sources – the Commonwealth Government Department of Health and Ageing, the Western Australia Planning Commission and more recently from the Collie Shire Council.

WAPC and DoHA projections estimate an average annual decline in Collie's population of -0.4% p.a. This is well below historical growth and is expected to underestimate future growth in Collie.

Commonwealth Government Department of Health & Ageing

The Commonwealth Government Department of Health and Ageing (DoHA) projections were published in 2007 and are based on 2006 Census and Estimated Resident Population (ERP) figures (Figure 2.2). These projections do not take into account the recent population growth in the Collie Region (0.5% p.a.) but rather estimate a declining

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2006 2007 2008 2009 2010

Co

llie

Po

pu

lati

on

Collie Urban Centre Remainder of Collie LGA

Collie SuperTown Combined Report

Final Draft Report

4

growth trend of 0.4% per annum to 8,760 persons by 2031 (a loss of 34 people each year). These projections are based primarily on a consideration of demographic drivers, reflecting the use of the projections nationally for the purposes of health and aged care funding.

Figure 2.2: Collie LGA Projections, Federal Government Department of Health and Ageing 2010-2031

Source: Federal Government Department of Health and Ageing (2007)

Western Australia Planning Commission

The Western Australia Planning Commission (WAPC) projections were released in 2005 and are also based on older population data, and do not take into account the recent growth trends of the Collie LGA. As a result, these projections are also expected to underestimate future growth. Like the Commonwealth Government Department of Health and Ageing projections, the WAPC projections indicate the same declining growth trends of 0.4% p.a. to 8,748 persons by 2031 (refer to Figure 2.3).

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,0002010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

An

nu

al %

Ch

an

ge

Co

llie

LG

A P

op

ula

tio

n

Collie SLA Collie SLA SWDC Perth SD Western Australia

Collie SuperTown Combined Report

Final Draft Report

5

Figure 2.3: Collie LGA Projections, Western Australia Planning Commission 2010-2031

Source: Western Australia Planning Commission (2005)

Collie SuperTown Growth Target

Under the SuperTown growth plan, the aspirational growth target for the Collie Town is a doubling of the population by 2031.

Figure 2.4 shows Collie Town's anticipated growth trend of 3.4% per annum to 15,580 residents by 2031. This is equivalent to an additional 371 residents each year. This is above the historical and projected growth rates for the South West Development Region, Perth SD and Western Australia.

In order for the SuperTown population projection target to be achieved in Collie Town there is an immediate need for acceleration of population growth trends above the historical 0.5% per annum. Proactive planning schemes, infrastructure and community services will be required to support population growth. Investment attraction, industry growth and diversification of the economic base will also be critical to support job creation and the overarching sustainability of the economy.

Figure 2.4: Collie SuperTown Population Target, 2010-2031

Source: Shire of Collie (2011)

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

1,500

3,000

4,500

6,000

7,500

9,000

10,500

12,000

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

An

nu

al %

Ch

an

ge

Co

llie

LG

A P

op

ula

tio

n

Collie(S) Collie(S) SWDC Perth SD Western Australia

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

3,000

6,000

9,000

12,000

15,000

18,000

Po

pu

latio

n G

row

th R

ate

(%)

Po

pu

lati

on

Ta

rge

t

Collie Township Collie Township

Collie SuperTown Combined Report

Final Draft Report

6

2.1.3 Age Structure

Collie has a younger population (average age of 36.7 years) than the broader SWDC (37.3 years). This is due to the higher proportion of persons aged under 19 years than the SWDC region - an occurrence of Collie having higher proportions of families with children.

Despite having higher proportions of children and a lower average age than the broader region, Collie has very low proportions of people aged between 19 and 34 years, when compared to both the SWDC region and State averages.

This highlights the migration trends of Collie's youth from the region post school. Limited availability of post-school education and training and job opportunities outside of the region's mining and industrial sectors is likely to be a key factor that draws youth from Collie. The closest university to Collie is located in Bunbury - another locality of the SWDC region. A campus of the South West Institute of Technology is located in Collie, however, courses are limited to certificates in education, resources and infrastructure work preparation and business administration. Addressing the insufficient provision of education opportunities in Collie is necessary to ensure future skills demand will be met locally and that local residents can have clear education pathways that lead to jobs locally.

Figure 2.5: Age Distribution, Collie LGA, 2005-2010

Source: ABS (2011)

13.9%

15.5%

12.0%

12.7%

14.1%

13.9%

9.6%

5.4%

3.0%

14.6%

15.1%

10.2%

13.4%

15.7%

14.0%

8.2%

5.6%

3.0%

20.0% 15.0% 10.0% 5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

0 to 9

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 to 79

80 and over

Collie SLA

2005

2010

Collie SuperTown Combined Report

Final Draft Report

7

Figure 2.6: Age Distribution, Collie Urban Centre, 2006

Source: ABS (2007)

Figure 2.7 and Figure 2.8 show the age distribution for the SWDC region and Western Australia. Comparison of 2005 to 2010 average age changes show that Collie has aged in line with the State trends over the past five years.

Figure 2.7: Age Distribution, South West Development Region, 2005-2010

Source: ABS (2011)

14.8%

16.0%

10.6%

11.8%

13.9%

15.0%

9.0%

5.9%

2.9%

13.7%

14.3%

9.6%

14.6%

14.3%

13.9%

8.3%

6.7%

4.5%

20.0% 15.0% 10.0% 5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

0 to 9

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 to 79

80 and over

Collie Urban Centre Age Structure, 2006

Female

Male

13.5%

14.1%

11.9%

13.5%

14.9%

13.5%

9.9%

5.5%

3.3%

13.8%

15.1%

10.9%

14.1%

15.9%

13.2%

8.6%

5.5%

3.0%

20.0% 15.0% 10.0% 5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

0 to 9

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 to 79

80 and over

SWDC Region

2005

2010

Collie SuperTown Combined Report

Final Draft Report

8

Figure 2.8: Age Distribution, Western Australia, 2005-2010

Source: ABS (2011)

2.1.4 Family/Household Types

Collie has high proportions of families with children (45.3%) when compared to the SWDC region (43.3%). This is slightly above the State average (45.1%).

A large proportion of Collie's families are also couple families with no children (38.7%), and is likely to comprise older adults or empty nesters. This reflects the migration of young adults of post-school age who leave the area to seek job opportunities or further studies outside of Collie.

The proportion of couple families without children in Collie is slightly above the State average, however well below the proportion of the broader SWDC region - a result of the attractiveness of the broader region to both empty nesters and young couple families without children.

Figure 2.9: Family/Household Type, Collie Urban Centre, 2006

Source: ABS (2007)

12.9%

13.3%

15.1%

14.3%

14.4%

12.6%

9.0%

5.1%

3.2%

13.0%

14.3%

13.8%

14.7%

15.1%

12.9%

8.1%

5.2%

2.9%

20.0% 15.0% 10.0% 5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

0 to 9

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 to 79

80 and over

Western Australia

2005

2010

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Couple Family w/ no

children

Couple Family w/ children

Single Parent Family

Other family

Collie Urban Centre, 2006

Collie Urban Centre

Collie (S)

SWDC

Perth SD

Western Australia

Collie SuperTown Combined Report

Final Draft Report

9

2.1.5 Household & Dwelling Growth

The total number of dwellings in the Collie LGA has grown from 2,990 dwellings in 2006 to 3,336 in 2011, an increase of 11.6%. The proportion of these dwellings that are classified as detached dwellings has fallen slightly over that time period, down from 92.2% of total dwellings in 2006 to 87.3% of total dwellings in 2011.

The average household size in the Collie Town was estimated to be 2.5 persons per household in 2006. If Collie Town's average household size decreases at the rate of regional WA projections (ABS, 2010) to 2.3 persons per household by 2031, there would a requirement for an additional 3,774 dwellings to be built between 2010 and 2031 to support the SuperTowns population growth target of 15,580 residents.

Figure 2.10: Forecast Household Growth, Collie Township, 2006-2031

Source: ABS (2007), ABS (2010)

2.2 Socio-Economic Characteristics

Collie has a unique set of socio-economic characteristics that differentiate it from other regional centres. Key indicators include education and qualifications, occupation, income and house-price based wealth and affordability.

2.2.1 Education/Qualifications

Collie's working aged population (15 years and over) has a low proportion of persons that have completed year 12 or undertaken tertiary education when compared to the broader SWDC region and Western Australia. However, almost 35% of Collie's working aged population have achieved certificate qualifications - well above Western Australia or the SWDC region averages.

The nature of industry and skills demand in Collie has resulted in this qualification trend towards certificate and trade type qualifications which do not require completion of year 12 or tertiary education.

High numbers of youth leaving the region for post-school tertiary education and job opportunities compounds this trend. Once youth have migrated from the region Collie does not provide sufficient job diversity to re-attract these workers back to the region after higher qualifications have been attained.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

No

. o

f H

ou

se

ho

lds

Collie Township

Collie SuperTown Combined Report

Final Draft Report

10

Figure 2.11: School & Post-School Qualifications, 2006

Source: ABS (2007)

2.2.2 Occupation

As indicated by post-school qualifications trends, blue-collar workers make up the majority of Collie's workers (over 55%). This is well above the proportions for the SWDC region and Western Australia.

Growth of the local mining, electricity industry and associated industrial supply chain will continue to drive demand for blue-collar workers in Collie. However, the lack of industry and occupational diversification outside of blue-collar workers will contribute to the loss of young people that is currently being experienced by the region as well impacting the future ability to attract residents to Collie.

Figure 2.12: Employment by Occupation, 2008-2009

Source: ABS (2011)

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Postgraduate Degree

Graduate Diploma and Graduate Certificate

Bachelor Degree

Advanced Diploma and Diploma

Certificate

% Finished Year 12

Collie SLACollie Urban Centre Collie (S) SWDC Perth SD Western Australia

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Blue Collar White Collar Service Workers

% o

f W

ork

forc

e

Collie SLA SWDC Perth SD WA

Collie SuperTown Combined Report

Final Draft Report

11

Service worker shares are also below regional and State average. This is a point of concern as it would be expected that regional service centres like Collie would have larger service sector labour forces in light of its role servicing large secondary and tertiary trade catchments.

2.2.3 Income

Regional centres commonly have below-average income levels, however, despite having high proportions of blue-collar workers Collie's population generate above-average incomes ($56,277) compared to the SWDC region and State averages. Higher earning occupations compared to the SWDC region and State averages include:

Machinery operators & drivers ($80,078)

Technicians & trades workers ($79,804)

Labourers ($45,167)

Dominance of the mining and industrial sector in the regional economy is the key driver of high wages and wage growth in Collie compared to other areas of the SWDC region and the State.

Figure 2.13: Average Income by Occupation, 2008-2009

Source: ABS (2011)

2.2.4 House Prices

In Australia, household wealth is dominated by the family home. This is particularly the case for older generations, who have not had the benefits of exposure to long-term compulsory superannuation.

During the last few years, and especially between 2005 and 2008, Western Australia generally, and Perth specifically, experienced significant increases in house prices.

As a regional area of the SWDC, Collie has experienced a relatively stable house price market that has not been heavily influenced by the broader property market fluctuations over the past five years.

In fact, Collie's median dwelling prices remain at an affordable level recording a median house price of $250,000 in 2010-11. This was 78% of the median prices for the SWDC and 67% of the median prices for the regional Western Australia house price.

$- $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 $80,000 $90,000

Managers

Professionals

Tecnhicians & Trade Workers

Community & Personal Service Workers

Clerical & Administrative Workers

Sales Workers

Machinery Operators & Drivers

Labourers

Collie SLA SWDC Perth SD Western Australia

Collie SuperTown Combined Report

Final Draft Report

12

Figure 2.14: Median Dwelling Prices

Source: REIWA (2011)

Lower house prices are often associated with regions with lower incomes, however this is not the case for Collie which recorded above average incomes when compared to the SWDC region and Western Australia trends (refer to Section 2.2.3). Lower median house prices and above average incomes levels represent the combination required to support an affordable housing market.

Comparison of incomes to house prices shows that households would require almost 4.0 years worth of income to purchase a house of median price outright. This is affordable compared to regional Western Australia housing standards, which is regarded internationally as highly unaffordable.

Figure 2.15: Ratio of Median House Prices to Median Household Incomes, 2008/2009

Source: ABS 5673.0 Wage and Salary Earners (2011), REIWA (2011) and AECgroup

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

2006-07 2007-08 2008-09 2009-10 2010-11

Me

dia

n D

we

llin

g P

rice

s (

$)

Collie LGA Regional WA SWDC Perth City

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Collie SWDC Regional WA

Me

dia

n M

ult

iple

Collie SuperTown Combined Report

Final Draft Report

13

2.3 Key Findings

Collie LGA (for which an estimated 82% of the population is located in Collie Town) has experienced steady growth of 0.5% p.a. to 9,470 between 2001 and 2010. Compared to the SWDC region and the State, this is low population growth.

The region is characterised by a younger population than the broader SWDC region due to the presence of high proportions of families with children under the age of 19 years. However, Collie loses significant proportions of its post-school aged youth due to a lack of local available vocational and tertiary education and training and job opportunities.

The working aged population (15 years and over) is mainly comprised of blue collar workers (over 55%) that have attained certificate level qualifications. Due to the dominance of the mining sector and associated industrial industries, average incomes are above the level of the State and the SWDC region, highlighting a certain level of prosperity held by the resident workforce.

Higher incomes usually suggest higher house prices, however, Collie enjoys lower median house prices compared to State and the SWDC region averages, which complement higher average incomes, making it an ideal combination for an affordable housing market.

SuperTowns population growth targets for Collie are for the town's population to double by 2031, indicating an immediate need for acceleration of population growth trends above the historical level if targets are to be achieved.

Proactive planning schemes, infrastructure and community services will be required to support population growth. Retention of youth will be important for creating vitality and a balanced community. Investment attraction, industry growth and diversification of the economic base will also be critical to support job creation and the overarching sustainability of the economy, as will be the provision of local education and training opportunities to support industry diversification and jobs growth.

Collie SuperTown Combined Report

Final Draft Report

14

3. Employment & Business Activity

This section profiles the employment and business characteristics of the Shire of Collie including labour force and unemployment trends, employment by industry and occupation and business size, growth and formation.

3.1 Labour Force & Unemployment

Growth of Collie's labour force and employment has generally been slower that of the broader SWDC region and the State over the past four years. In the June Quarter 2011, Collie recorded a labour force of 4,918 people and 4,598 people employed. This was 1.1% more than the previous year for both labour force and employment.

Figure 3.1: Labour Force & Unemployment Rate, 2006-2011

Source: DEEWR (2011)

Unemployment rates have averaged significantly higher than the SWDC region and State rates over the last four years. Economic diversification and job creation will be necessary to support attraction and sustainable growth of the Collie population over the next 20 years.

Table 3.1: Labour Force & Employment, June Q 2011

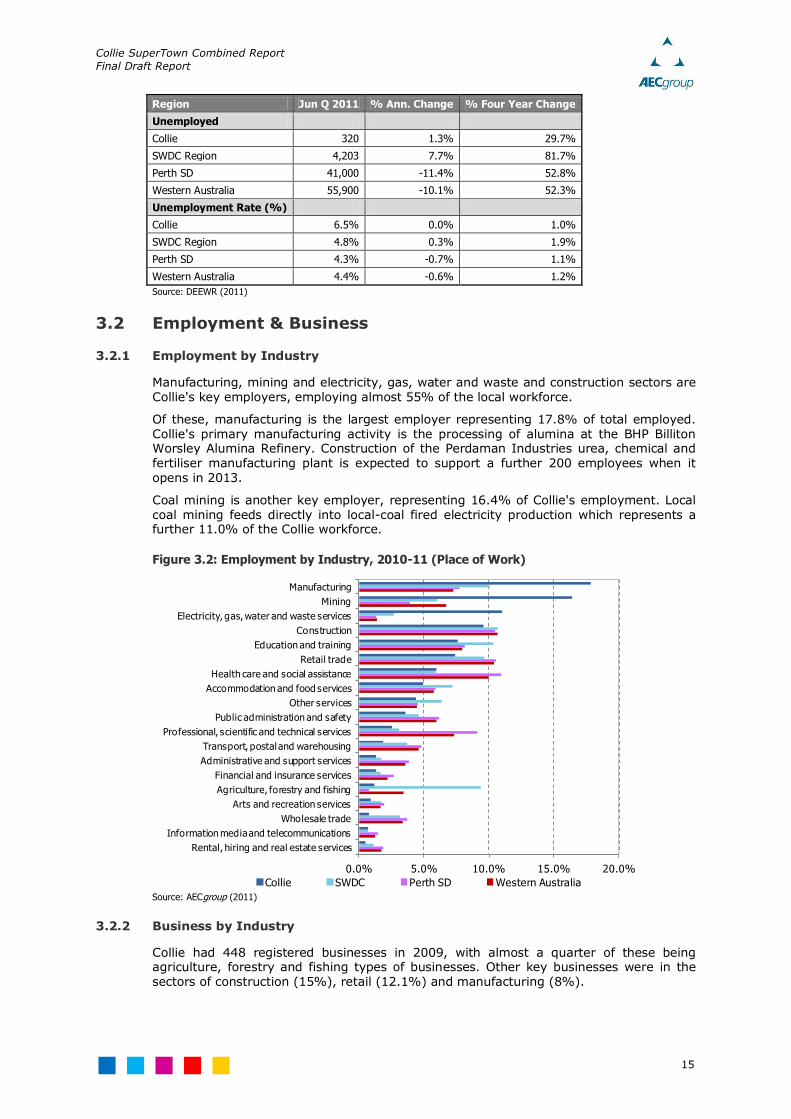

Region Jun Q 2011 % Ann. Change % Four Year Change

Labour Force

Collie 4,918 1.1% 9.5%

SWDC Region 87,249 1.1% 11.3%

Perth SD 960,400 2.5% 12.8%

Western Australia 1,283,100 2.6% 12.1%

Employment

Collie 4,598 1.1% 8.3%

SWDC Region 83,046 0.8% 9.2%

Perth SD 919,400 3.2% 11.5%

Western Australia 1,227,200 3.2% 10.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

750

1,500

2,250

3,000

3,750

4,500

5,250

6,000

Un

em

plo

ym

en

t Ra

teLa

bo

ur

Fo

rce

Collie (S) Collie (S) SWDC Region Perth Western Australia

Collie SuperTown Combined Report

Final Draft Report

15

Region Jun Q 2011 % Ann. Change % Four Year Change

Unemployed

Collie 320 1.3% 29.7%

SWDC Region 4,203 7.7% 81.7%

Perth SD 41,000 -11.4% 52.8%

Western Australia 55,900 -10.1% 52.3%

Unemployment Rate (%)

Collie 6.5% 0.0% 1.0%

SWDC Region 4.8% 0.3% 1.9%

Perth SD 4.3% -0.7% 1.1%

Western Australia 4.4% -0.6% 1.2%

Source: DEEWR (2011)

3.2 Employment & Business

3.2.1 Employment by Industry

Manufacturing, mining and electricity, gas, water and waste and construction sectors are Collie's key employers, employing almost 55% of the local workforce.

Of these, manufacturing is the largest employer representing 17.8% of total employed. Collie's primary manufacturing activity is the processing of alumina at the BHP Billiton Worsley Alumina Refinery. Construction of the Perdaman Industries urea, chemical and fertiliser manufacturing plant is expected to support a further 200 employees when it opens in 2013.

Coal mining is another key employer, representing 16.4% of Collie's employment. Local coal mining feeds directly into local-coal fired electricity production which represents a further 11.0% of the Collie workforce.

Figure 3.2: Employment by Industry, 2010-11 (Place of Work)

Source: AECgroup (2011)

3.2.2 Business by Industry

Collie had 448 registered businesses in 2009, with almost a quarter of these being agriculture, forestry and fishing types of businesses. Other key businesses were in the sectors of construction (15%), retail (12.1%) and manufacturing (8%).

0.0% 5.0% 10.0% 15.0% 20.0%

Rental, hiring and real estate services

Information media and telecommunications

Wholesale trade

Arts and recreation services

Agriculture, forestry and fishing

Financial and insurance services

Administrative and support services

Transport, postal and warehousing

Professional, scientific and technical services

Public administration and safety

Other services

Accommodation and food services

Health care and social assistance

Retail trade

Education and training

Construction

Electricity, gas, water and waste services

Mining

Manufacturing

Collie SWDC Perth SD Western Australia

Collie SuperTown Combined Report

Final Draft Report

16

Figure 3.3: Business Counts by Industry, % of Total Businesses, June 2007 to June 2009

Source: ABS (2011)

3.2.3 Businesses by Employment Size

Sixty percent of Collie's businesses are non-employing (i.e. owner/operator) due to the rural nature of the region with a large proportion of agricultural businesses. However, this is below the representation of small business in the broader SWDC region and Western Australia economies.

Collie does however, have higher proportions of medium-sized businesses (20 to 49) as well as larger businesses (100+ employees). This is due to the presence of major industry players in the mining and manufacturing sector in Collie as well as a good representation of medium-sized construction businesses and supporting supply chain.

Figure 3.4: Business Counts by Industry by Number of Employees, June 2007 to June 2009

Source: ABS (2011)

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Mining

Information Media and Telecommunications

Electricity, Gas, Water and Waste Services

Arts and Recreation Services

Public Administration and Safety

Education and Training

Wholesale Trade

Administrative and Support Services

Health Care and Social Assistance

Other Services

Accommodation and Food Services

Financial and Insurance Services

Transport, Postal and Warehousing

Professional, Scientific and Technical Services

Rental, Hiring and Real Estate Services

Manufacturing

Retail Trade

Construction

Agriculture, Forestry and Fishing

Collie (S) SWDC Perth SD Western Australia

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Non employing

1 to 4

5-19

20-49

50-99

100-199

200+ Collie (S)

SWDC

Perth SD

Western Australia

Collie SuperTown Combined Report

Final Draft Report

17

3.2.4 Businesses by Turnover

Over 20% of businesses in Collie earn less than $25,000 per year with the second largest revenue category being businesses that earn between $200,000 and $500,000 each year (16.1% of businesses).

Not surprisingly, Collie has a higher proportion of businesses that earn over $10 million per annum (2%) compared to the SWDC (0.8%) and Western Australia (1.5%).

Figure 3.5: Business Counts by Industry by Turnover Size Ranges, June 2007 to June 2009

Source: ABS (2011)

3.2.5 Small Business

Small business incomes in Collie are generally significantly lower than the broader SWDC region or the State. In 2008-09, the average income of small unincorporated business in Collie was $10,250, relative to the average income in the SWDC region of $16,499 and State of $25,857.

Figure 3.6: Average Unincorporated Small Business Income, 2008-09

Source: ABS (2011)

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Zero to less than $25k

$25k to less than $50k

$50k to less than $75K

$75k to less than $100k

$100k to less than $150k

$150k to less than $200k

$200k to less than $500k

$500k to less than $1m

$1m to less than $2m

$2m to less than $5m

$5m to less than $10m

$10m to less than $20m

$20m to less than $50m

$50m to less than $200m

$200m or more

Collie (S)

Collie (S)

SWDC

Perth SD

Western Australia

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Collie (S) SWDC Perth SD Western Australia

Inco

me

($

)

Unincorporated Small Business Income

Collie SuperTown Combined Report

Final Draft Report

18

3.2.6 Tourism Activity

Collie received 134,000 visitors in the year ending September 2011, which was an increase of 20% from recent years. The increase can be attributed to an increase in business travellers, likely visiting Collie in relation to major mining projects or expansion of the Worsley refinery. Visitors come to Collie for a diverse range of reasons, with the purpose of visit evenly distributed across holiday, visiting friends and relatives and business.

Figure 3.7: Total Visitors, Collie, 2000-2011

Note: Data is year ending September 2011 Source: TRA (2011)

Figure 3.8: Purpose of Visit, Collie, 2011

Note: Data is year ending September 2011 Source: TRA (2011)

Room occupancy rates have fallen dramatically from 59.4% during the year ending September 2007 to 38.0% in the most recent year ending September 2011. Occupancy rates above 65% are considered to be an indicator that a region would be able to support new entrants into the tourism accommodation market. The underperformance of the

0

20

40

60

80

100

120

140

160

180

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nu

mb

er

of

Vis

ito

rs (

'00

0)

Day Trip Domestic Overnight International

34%

29%

27%

10%

Holiday or leisure

Visiting friends and relatives

Business

Other

Collie SuperTown Combined Report

Final Draft Report

19

occupancy rates in Collie in recent years suggest that, at present, the tourism accommodation market is over supplied with four establishments in the region providing 115 rooms2.

Despite the recent fall in guest arrivals and occupancy rates within the LGA, takings from accommodation have risen 39.0% over the past year and 20.4% from the year ending September 2007 to the year ending September 2011 (ABS, 2011).

Figure 3.9: Guest Arrivals and Room Occupancy Rates, December 2006 – September 2011

Source: ABS (2011)

Collie has numerous tourism attractions within the town and in its surrounding areas. These attractions include Lake Kepwari, Wellington Dam, Kostecki Motorplex, the Munda Biddi Trail and Honeymoon Point.

Lake Kepwari is located 10 kilometres south-east of Collie. It is a water filled former open-cut mine that is approximately 2 km long, 1 km wide and 70 metres deep. The lake has been rehabilitated by Premier Coal.

The Wellington Dam was constructed in 1933 and further enlarged in 1956. The dam is the second largest in the State and acts as home to one of two hydro power stations in Western Australia. The dam offers tourists camping facilities, canoe hire, BBQ’s as well as spectacular views across the dam. It is one of only a few dams that allows camping and recreational activities (South West Life, 2010).

The Kostecki Motorplex is located approximately 14km east of Collie within the Collie State Forest. The 1.7km circuit track hosts a series of motorsport events throughout the year (Collie River Valley, 2007).

The Munda Biddi Trail is a 609km mountain biking trail stretching from Mundaring to Manjimup. The trail is still a work in progress, with the final trail running for close to 1,000km all the way south to Albany. The trail also has eight purpose built shelters along the way with camping areas available (Munda Biddi Trail Foundation, 2011).

Honeymoon Point is situated along the Collie River in Wellington National Park. The point offers camping and picnic facilities, wood BBQ’s, toilets as well as swimming and canoeing areas (Department of Environment and Conservation, 2011).

These attractions highlight the vast array of recreational tourism opportunities on offer in and around the Collie area. Tourism can be a beneficial industry of opportunity as tourism

2 Note ABS statistics only include establishments with over 15 rooms.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

Ro

om

Occu

pa

ncy

Ra

te (%

)

Gu

est

Arr

iva

ls

Guest Arrivals Room Occupancy Rate Sept YE Occupancy Rates

Collie SuperTown Combined Report

Final Draft Report

20

expenditure can flow through the local economy without significant infrastructure requirements (which are needed to support permanent residents). Additionally, tourism expenditure often goes to small businesses in the area, so increases in tourism can aid the small business sector locally. Additionally, given the recreational nature of many of Collie’s attractions, there would be a considerable amount of local usage and visitors from Bunbury and the surrounding region may not be accurately captured in the survey instruments used, given the dispersed nature of where these visitors are located (i.e. many visitors would be camping or located in national forests).

3.3 Key Findings

Collie's key employers are the manufacturing, mining and electricity, gas, water and waste services sectors. Specifically, Collie employs around 45% of its workforce either in local coal mining, alumina refining or electricity generated from the local coal production activities. In short, Collie is easily characterised as a mining and industrial hub in the SWDC region.

Labour force and employment growth is steady but below regional and State averages, and is mainly dictated by the rate of investment and development of its leading sectors. Interestingly, unemployment rates are substantially higher in Collie than the SWDC region and the State. This could be a factor of Collie being relatively undiversified with limited opportunity for people to work in sectors outside of mining, manufacturing and energy generation - leaving limited potential for couple families to have both adults working in local jobs. This is supported by census data which indicated that on average Collie has 1.1 working adults per household compared to 1.8 in the SWDC region and 1.3 working adults per household for the State.

As a rural area, over 60% of Collie's businesses are small businesses and almost a quarter of all businesses undertake agriculture, forestry and fishing activities. Collie also has higher proportions of medium-sized businesses (20 to 49) as well as larger businesses (100+ employees) that the SWDC region and State averages. This is due to the presence of major industry players in the mining and manufacturing sector in Collie as well as a good representation of medium-sized construction businesses and supporting supply chain.

While tourism visitation to Collie is not as significant as other established tourist destinations, Collie does offer a wide range of recreational activities and attractions and tourism can provide some economic diversity. Collie’s tourism sector has seen a boost from recent major investments and the recreational amenities of the area are likely enjoyed by locals as well as visitors from around the surrounding region.

Collie SuperTown Combined Report

Final Draft Report

21

4. Investment & Major Projects

This section profiles activity and investment in the Collie economy. It includes review of residential and commercial building approvals, land releases and development and major proposed investments in the region.

4.1 Building Approvals & Property Market

4.1.1 Residential Approvals

The number and value of residential approvals have grown steadily in Collie over the past 10 years, rising from 24 approvals at a total value of $3.2 million in the 2002 financial year to a 10-year high of 75 residential approvals at a value of $18.7 million by the end of the 2010 financial year. Residential building approvals dropped back to a total of 44 at a value of $11.6 million by the end of the 2011 financial year.

While the historical trend in residential building approvals shows a general increase, considerably more development will be needed in the future in order to meet the SuperTown growth targets. Based on the population of the town doubling, an average of 121 new residential dwellings will be needed every year until 2031.

Figure 4.1: Residential Approvals (No.) and Value ($‘M), Collie LGA

Source: ABS (2011)

4.1.2 Non-Residential Approvals

Non-residential building activity was almost non-existent until the 2005 financial year when $14.8 million worth of building activity occurred. The 2008 financial year saw by far the greatest amount of investment in non-residential building to date, with $62.8 million worth of approvals recorded.

The strong growth in both the number and value of residential and non-residential building approvals reflects the improving economic conditions of the Collie area resulting from its booming mining, manufacturing and electricity, gas, water and waste services industries.

$-

$2.5

$5.0

$7.5

$10.0

$12.5

$15.0

$17.5

$20.0

0

10

20

30

40

50

60

70

80

Va

lue

of A

pp

rov

als

($'M

)

Nu

mb

er

of

Re

sid

en

tia

l A

pp

rov

als

Dwelling Approvals - Houses (No.) Dwelling Approvals - Other Residential (No.) Value of Approvals ($'M)

Collie SuperTown Combined Report

Final Draft Report

22

Figure 4.2: Non-Residential Building Approvals ($ ‘M)

Note: Major projects that must receive approval outside of the normal development application process are not recorded by the ABS. Source: ABS (2011)

4.1.3 Land Releases & Developments

Figure 4.3 shows that lot approvals, particularly residential and commercial, have substantially grown in Collie in recent years. Residential lot approvals have averaged 29 per year since 2006-07, whereas the five years preceding 2006-07 saw an average of only four lots being approved per year. An average of 121 new residential dwellings are required until 2031 in order to meet the SuperTown growth target.

Figure 4.3: Shire of Collie Lot Activity, Final Approvals, 2001-02 to 2010-11

Source: Shire of Collie Council (2011)

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

Va

lue

of

No

n-R

esid

en

tia

l A

pp

rov

als

($

'M)

Collie SLA

0

5

10

15

20

25

30

35

40

Ap

pro

va

ls

Commercial Industrial Residential Rural

Collie SuperTown Combined Report

Final Draft Report

23