Classification of Torbanite and Cannel Coal. I. Insights ...

Upload

mjunction-services-ltdCategory

view

287download

13description

Coal Insights, September 2012 3

EDITORIAL

Copyright: All rights reserved. No part of Steel Insights can be reproduced or copied in any form or by any means without the prior permission of mjunction services limited. Please inform us if any copyright has been inadvertently infringed.

Disclaimer: This document is for information purpose only. Certain information herein has been acquired from various external sources believed to be reliable. While we have taken reasonable care to compile this report, we in no way assume any responsibility for any error or discrepancy in regards to information contained herein. Readers are requested to make appropriate judgment without any prejudice or compulsion.

Registered Officemjunction services limited, Tata Centre, 43 J L Nehru Rd, Kolkata 700 071

Website: www.mjunction.inCorporate Head Quarters: Godrej Waterside, 3rd Floor, Tower 1, Plot V, Block DP, Sector V, Salt Lake, Kolkata 700091, Tel: +91 33 6610 6100, Fax: +91 33 6610 6187 Bhilai: Room 321, 3rd Floor, Ispat Bhavan, Bhilai Steel Plant, Bhilai 490001, Tel: +91 788 6451066, Tele/Fax: +91 788 2221071 Bokaro: Room 19, Old Admin Bldg., Bokaro Steel Plant, Bokaro 827001, Tel/Fax: +91 654 2226132 Burnpur: SAIL - IISCO Steel Plant, Materials Building, Order Department, Ground Floor, Burnpur 713325, Telfax: +91 341 2240107 Chennai: Basement, Begum Ispahani Complex, New No 91, Old No 44, Armenian Street, Chennai 600 001, Tel: +91 44 64624733-35, Fax: +91 44 25216536 Durgapur: Room 618, Ispat Bhavan, Durgapur Steel Plant, Durgapur 713203, Tel: +91 343 6510185, Tele/Fax: +91 343 2586946 Jamshedpur: Kashi Kunj, Ground Floor, Road No. 02, Contractors Area, Bistupur, Jamshedpur 831001, Tel: +91 657 6519985/86/90/91, Fax: +91 657 2230040 Mumbai: Jolly Bhavan II, 403, 4th Floor, 7 New Marine Lines, Mumbai 400020, Tel: +91 22 66510663, Tele/Fax: +91 22 66510662 New Delhi: C127, 2nd Floor, A One Plaza, Naraina Industrial Area, Phase I, New Delhi 110028, Tel: +91 11 65661774/65413288, Tele/Fax: +91 11 25897000 Noamundi: C/o TATA Steel Limited, Mines Purchase Cell, PO: Noamundi, Singbhum (West), Jharkhand 833 217, Tel: +91 9204791638/9234368606 Rourkela: Administrative Bldg., Room 624, 6th Flr, Rourkela Steel Plant, Rourkela 769011, Tel: +91 661 6514142/6511412

Chief EditorRakesh Dubey, Tel: +91 91633 48159, Email: [email protected]

Executive EditorArindam Bandyopadhyay, Tel: +91 91633 48016Email: [email protected]

Editorial BoardAlok Srivastava, General Manager, MMTC LtdAmitabh Panda, Group Director (Shipping & Logistics Operations), Tata Steel GroupAnirudha Gupta, Director, P&H JoyMining Equipment India LtdAshok Jain, Managing Director, Saumya Mining LtdDeepak Bhattacharyya, Head – coaljunction, mjunction services ltdGanesan Natarajan, WT Director, President & CEO, Ennore Coke LtdLawrence Metzroth, Vice President – Analysis & Strategy, Arch Coal IncM K Palanivel, President – All India Bulk, Samsara GroupP S Bhattacharyya, former Chairman, Coal India LtdS N Choubey, Head – Commercial, ABG Cement LtdSandeep Kumar, Managing Director, S & T Mining Co Pvt LtdShyamji Agrawal, AVP-Central Procurement Cell, Ultratech Cement LtdSuresh Thawani, Managing Director, Tata Sponge Iron LtdAdvertisingSoumitra Bose, Tel: +91 92310 00232, Email: [email protected] Jalan, Tel: +91 91633 48243, Email: [email protected] Das, Tel: +91 91633 48045, Email: [email protected] Free No.: 1800 4192 000 1. Press 8 for publicationEmail: [email protected] Ray, Sobhan JasFor suggestions, feedback and queries, please write to [email protected]

mjunction believes that all junctionites, customers, suppliers, partners, etc should practice the highest ethical standards in their daily operations.

Report a concern to [email protected]

Dear Readers,

“No man undertakes a trade he has not learned,” said Socrates, “yet everyone thinks himself sufficiently qualified for the hardest of all trades – that of government.”

Wise saying, isn’t it? How aptly it describes the modern democracy, the world’s largest democracy, to be more specific. At present there is not one government, but numerous governments ruling this country. But even one government was too many, if you consider the warring ministries and departments. Coal versus Environment, Power versus Coal, Finance versus RBI, Rail versus Finance, States versus Centre, States versus States, and now Centre plus States versus Comptroller & Auditor General (CAG).

The whole thing seems pretty long-drawn. The government is busy proving itself innocent (and de-allocating blocks, at the same time). CAG is busy trying to prove that the government is at fault. The Central Bureau of Investigation (CBI) is busy implicating black-listed allocattees – the root of all chaos. And then there is a new entrant into the ring, the Central Vigilance Commission (CVC), busy demanding that all captive allocations since 1993 be brought under the CBI scanner. Let the country know the truth…full and final.

So be it. Let the truth be out, of course. And till such time as it’s not, let production be lost, de-allocattees move court, and growth be stalled.

Now what if the truth eludes, just as it has eluded in numerous other cases of grafts and scams? Will the truth-seekers be brought to book for the lost production? Because the truth is that the country is losing on production and growth, every passing day.

Enough on the governance part. Now let’s take a look into the fallout of lost production; i.e. ever growing imports. India’s coal imports are projected to touch nearly 50 percent of the country’s consumption by 2025-30. At this rate of development, that scenario may surface even earlier. What will that imply? Well, the thermal power sector will become critically dependent on foreign resources. Now consider the economy’s current dependence on international crude market. Consider the impact of any spike in international crude prices and the vulnerability of economy to periodic shocks.

Why make the economy vulnerable on another front? Why make the country susceptible to external shocks in yet another energy vertical? Consider the huge forex outgo and the impact of crude import bill on India’s balance of payments? Why go for the last option when you actually have some others?

Happy reading,

(Rakesh Dubey)

4 Coal Insights, September 2012

COnTEnTs

18 CIL board approves import plan 20 Thermal coal import prices remain flat 22 Imported spot coking coal prices ease 28 Delayed delivery defeating purpose of

coal e-auction: ICMA 30 SPU loan restructuring to reach `1.5

trillion: CRISIL 32 India’s August power generation falls

m-o-m: CEA 38 MoC axes allocation of 10 captive coal

blocks 40 Coal crisis spares paper industry 46 MBE CMT India bags order for

Pakistan’s first coal washery 48 JSPL gears up to slash DRI production

cost 50 Anupam wins `130 crore order from

SAIL 51 MoC blamed for messing up coal block

allocations 52 US coal production to drop 6.1% 53 Will China’s decision on export tax

further soften coke? 54‑ Traffic handling by major ports down

3.5% in April-August 56 Railway commodity freight revenue

down in August 58 Updated data on captive coal blocks

44 | In FoCuSBiocoal: the new fuel on the blockThis cheap, renewable fuel developed from agro-wastes deserves a closer look

42 | TECHnoLoGYCIMFR offers technology support for environment managementThe institute develops fly ash soil amendment technology for environmental preservation

36 | FEATuRETime to wind up standalone DRI plants?Only forward or backward integration can save the day for ailing sponge iron industry

26 | FEATuRECIL scraps JV route for mine revivalThe coal behemoth opts for mine developers and operators (MDOs) route to revive UG mines

6 | CoVER SToRYGrowing coal imports may leave India vulnerableExcessive reliance may make India susceptible to external shocks as seen in crude oil

COvER sTORy

6 Coal Insights, August 2012

When India joined WTO way back in the 1990s, the major plank of the protagonists of free trade was the Ricardian theory of comparative advantage. This classical theory, in simple parlance, proposes that the world would be a better place to live

in if individual economies are allowed to hinge on their areas of core competence. For example, if China can produce better peanuts at lower cost, let it produce excess of it so that the rest of the world can be fed better peanuts at cheaper rates. This way the land (and labour and capital etc.) occupied in growing peanuts elsewhere could be released to grow other things, better and cheaper, the theory says. This way the global economy will operate at the peak of its competitiveness and efficiency.

While this may work well in case of peanuts, the theory falls flat when it comes to coal, especially steam coal, where India is an extreme example of indulgence and lassitude. In at least this case, the comparative advantage of one country, say Indonesia, is actually making another (India) less competitive in every other field.

Growing coal imports may leave India vulnerable

Growing coal imports may leave India vulnerable Arindam Bandyopadhyay & Tamajit Pain

8 Coal Insights, September 2012

185, 250, 400…?

It may look like a series of Geometric Progression, but is actually the estimates of coal tonnage that India will be importing five years from now. The presence of multiple numbers indicates the multitude of estimates that keep flowing in ever so often.

Only recently, the Plan Panel projected that imports will rise to a “whopping” 185 million tons (mt) by 2017, the terminal year of the current (Twelfth) Five Year Plan. At about the same time last year, the then coal secretary Alok Perti had put this estimate at 250 mt. Two years ago (at about the same time of the year, again) a top functionary of Coal India projected an import volume of 250 mt by 2020. Then again, a globally renowned research consultant estimated (in March 2012) that the country’s thermal coal imports will go up to 400 mt by 2030.

While these numbers look pretty impressive, considering that global coal import volume is around 900 mt, some Indian importers go a few steps ahead. The country’s coal imports, according to a trader who sought anonymity, has already crossed 200 mt a year. “If you want to know the ground reality, talk to big importers, check out their figures…! Import was 250 mt in (calendar year) 2011. This year (2012) it is going to be 300 mt,” he claimed.

But don’t talk these numbers, a top coal ministry (MoC) official once said. If India started projecting coal import requirements, it would give an indication of the country’s

huge appetite to its suppliers in sourcing countries (Australia, Indonesia, South Africa and the US) who may take advantage of the situation.

“There will be a race to see who can emerge as the potential supplier. We are already paying huge prices and it is expected to get worse with these projections,” he warned.

Coal imports flat in Q1

Contrary to industry expectations and “ground realities”, coal imports into India remained somewhat flat during the first quarter (April-June) of 2012-13 (Q1) and first half of 2012 (H1 2012). According to data available with Coal Insights, coal imports through 12 major ports of the country in Q1 stood at around 19 mt, showing flat growth over the same period last year. Trading sources, however, claimed that the import

volume was larger than the figure estimated.Of the total import in Q1, over 10 mt was

non-coking coal and 7 mt coking coal. The remaining part comprised pet coal, anthracite coal and pulverized coal injection (PCI) coal.

Till August 2012, coal imports through these major ports were estimated at around 27 mt, which included 14.5 mt of non-coking coal and 10.5 mt coking coal. This was significantly lower than around 45 mt imported during April-August 2011. Earlier, overall coal imports in 2012-13 were expected to jump to around 150 mt from around 110 mt in 2011-12. However, as of now, coal imports in the current fiscal seem to fall short of than the volume expected.

“The official figures may be on the down side, as our estimates show import volume is rising all through. Even the figures estimated for last year (FY12) was below our estimates. The domestic supply constraints are leading to huge imports by the consuming sectors. Lately, the drop in international prices has made imports all the more attractive,” a coal trader said.

However, another estimate by Barclays shows India’s coal imports during H1 2012 (January-June) grew only moderately at 3 percent year-on-year. Imports during the half year stood at around 48.5 mt and lagged expectations, the report said.

Stockpile, currency restrict import

Although there remains doubt over the authenticity of various estimates, the coal industry at large agrees that a host of factors have restricted imports during the early months of the current fiscal year.

High domestic productionFirstly, the higher growth in domestic production during the first quarter was a

COvER sTORy

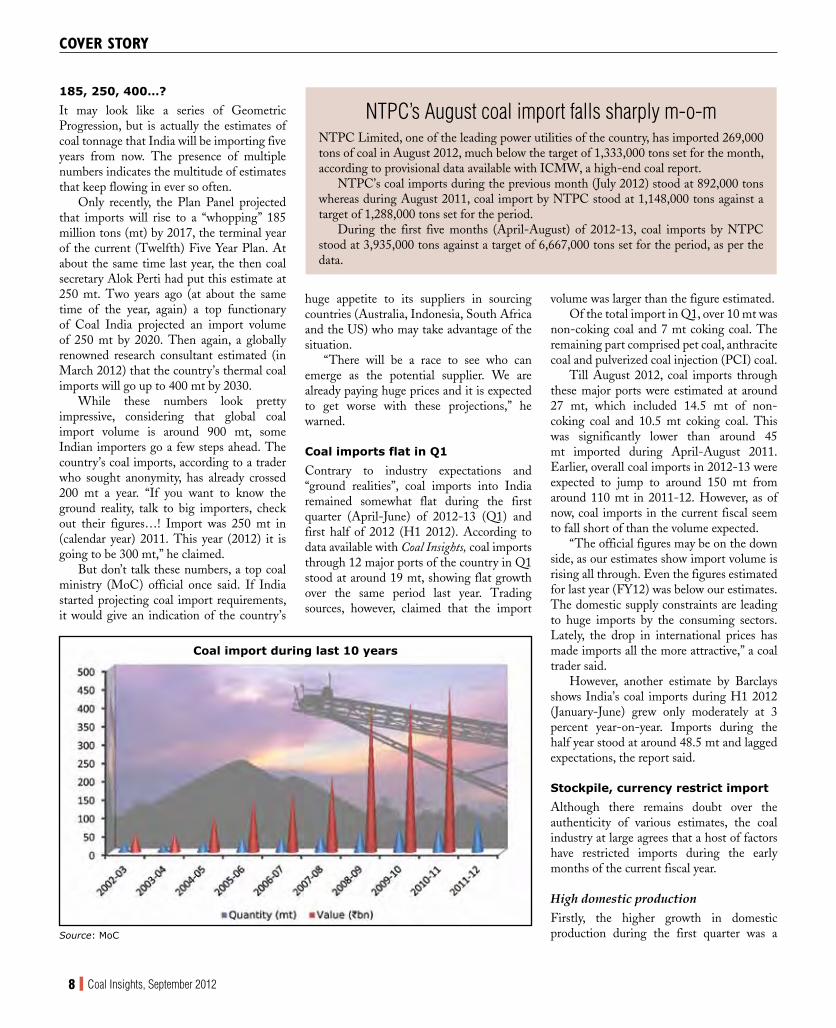

Coal import during last 10 years

Source: MoC

NTPC’s August coal import falls sharply m-o-mNTPC Limited, one of the leading power utilities of the country, has imported 269,000 tons of coal in August 2012, much below the target of 1,333,000 tons set for the month, according to provisional data available with ICMW, a high-end coal report.

NTPC’s coal imports during the previous month (July 2012) stood at 892,000 tons whereas during August 2011, coal import by NTPC stood at 1,148,000 tons against a target of 1,288,000 tons set for the period.

During the first five months (April-August) of 2012-13, coal imports by NTPC stood at 3,935,000 tons against a target of 6,667,000 tons set for the period, as per the data.

GIVE CYCLE TIMES THE CHOP. cHOP. CHOP.

The new G-Series L180G and L220G wheel loader with 20% more lifting power and 10% better breakout force, are the latest workhorses of Volvo’s wheel loader range. New engines and drivelines offer improved productivity, lower emissions, greater smoothness, serviceability and operator comfort. The improvements ensure full buckets, faster cycle times - all day, every day.

Volvo’s G Series wheel loaders: more lift, more shift.

Corporate Office:

Volvo India Pvt. Ltd. Volvo Construction Equipment #65/1, Parin Building, Bagmane Tech Park, C V Raman Nagar, Bangalore 560 093 Tel: +91 80 6691 2000 Fax: +91 80 6691 2287

volvo construction equipment

Authorized Dealers:

Infra Equip Pvt. Ltd., Dhanbad

Pollutech Engineering, Bhubaneshwar

Suchita Earthmoving Solutions, Guwahati

Suchita Millenium Projects Pvt. Ltd., Kolkata

For details contact:

Toll Free No. 1800 108 6586 E-mail: [email protected] www.volvoce.com

10 Coal Insights, September 2012

positive development that the domestic industry was looking forward to for quite some time now. In the first quarter of 2012-13, Coal India Ltd (CIL) achieved a growth of about 6.5 percent in offtake, a record high in recent past. Also, production growth hovered around 6 percent in the April-June 2012 period. This came as a major relief to the consumers after stagnant growth in the past two-three years.

Although this growth in production and offtake declined in the months of monsoon, the consumers were hopeful that CIL would make up for the lost production in the third quarter.

According to CIL chairman S. Narsing Rao, the company is expected to register an overall growth of 6-7 percent during 2012-13.

The company plans to produce 464 mt of coal in 2012-13 and despatch about 470 mt as per Annual Action Plan (AAP) compared with actual production of 435.84 mt and despatch of 433.08 mt in 2011-12. This implies an incremental production of about 30 mt in 2012-13, which Rao is confident of achieving. This growth in production and offtake would actually help restrict the growth in imports during the current year, industry sources believe.

Stockpile at portsAlong with a renewed growth in production, the high stockpile Indian ports posed a major hurdle for imports during the first quarter.

The stock of imported coal for supply to power utilities at various ports of the country

rose by 39.36 percent to 0.524 mt as on August 31, 2012 as compared to 0.376 mt as on July 31, 2012, according to data released by Central Electricity Authority (CEA). This however was lower than the stock of 1.5 mt reported on August 31 last year.

The stock had been rising consistently from March 2012 from a level of 0.390 mt to 0.679 mt as on April 30, 2012 while on May 31, 2012 it stood at 0.705 mt but after witnessing a rise for four consecutive months, it had experienced a fall in July. However, the stock level again moved up in the month of August, according to data available with Coal Insights.

Overall, the total stockpiles of both unsold and contracted coal for (all user

segments) are reported to be around 5-6 mt at various ports, sources said.

Logistics lagsThe high stockpile at ports is primarily caused by lack of handling capacity and inadequate inland transport facility. This problem becomes acute during the monsoon. According to port sources, handling of coal in the monsoon months takes place only in all-weather ports/terminals. As a result, the stockpile increases.

In some cases, environmental factors also restrict handling of the commodity. This was the case with Chennai port, where the High Court had stopped handling of coal on the ground of pollution. During the first five months (April-August) of the current financial year (2012-13), total imports of coking coal via Chennai port stood at 771 tons as compared to 107,717 tons imported during the corresponding period of previous year (2011-12). However, recently the court has reportedly agreed to relax the order.

Besides port congestion, shortage of railway rakes was also a factor inhibiting growth of offtake from CIL mines in July-August.

“It’s not only rains, but also the wagon availability which brought down the offtake rate lately. It is not as per expectation,” said Rao. In July, the wagon availability was around 177 wagons per day against expectations of around 190 wagons per day. There was a shortfall of 13 rakes a day which had a huge impact.

COvER sTORy

*coal imported for power utilities

Source: CEA

Stockpile at ports* in 2012 (in mt)

Bulging coal stock at ports restricts import

12 Coal Insights, September 2012

COvER sTORy

Slack demand Another factor that inhibited growth in import was lukewarm demand from the domestic industries, which are going through a lean patch. Industrial growth stood at a three-year low of minus 0.1 percent in the first quarter (April-June 2012), against 6.9 percent in the corresponding period of last year. Manufacturing sector witnessed a 3.5 percent de-growth in June 2012. Within manufacturing, capital goods production dropped by more than 20 percent in close succession – October 2011 (25.48 percent), March 2012 (21.3 percent) and June 2012 (27.9 percent).

Almost all the coal consuming sectors except power – steel, cement, paper, sponge iron – are facing a demand glut for different reasons. While the steel sector is witnessing slack demand, the cement makers received a severe blow from the Competition Commission of India (CCI) allegedly on earning excessive profit through cartelisation. The sponge iron makers are suffering heavy pressure on margins due to softening demand for steel and increase in raw material prices. All these factors are leading to reduced demand for fuel from these sectors.

Rupee’s depreciationLastly, the recent depreciation of Indian rupee (INR) against the US dollar has to some extent restricted import of the commodity. In fact, the currency’s depreciation nullified the impact of a fall in international coal prices. The rupee’s weakness resulted from an adverse

trade balance and high inflationary pressure. Together these factors pushed the currency down to `56 per US dollar in recent weeks.

A sharp rise in dollar often leads to increased risk of default by domestic importers. The current scenario reminded a short spell of rupee’s depreciation in 2011 which stoked fears of default by some large importers.

Although there has been a little gain in the rupee lately, economic forecasters predict sustained pressure on the local currency in the coming months. This, if comes true, may restrict coal imports going forward.

Prices offset currency pressure

While stockpile and depreciation in the rupee are believed to have restricted India’s import

of coal during the early months of 2012-13, the steep decline in international coal prices has had a contrary effect. This was true for both thermal and coking coal import by the country.

Prices of thermal coal imports from Indonesia dipped 23 percent in the January-September period as ample supplies and continued weak demand from India and other buyers weighed, market sources told Coal Insights.

Indonesian coal of 5,900 kCal GAR was quoted at $72.8 per ton on September 20, 2012 as compared to $95 per ton on January 3, 2012. Similarly, Indonesian coal of 5,000 kCal GAR is quoted at $56.8 per ton on September 20, 2012 as compared to $74 per ton on January 3, 2012.

Simultaneously, imported coal prices from South Africa declined by about 19 percent in the January-September period because of the weak demand. South African coal of 6,000 kCal NAR is quoted at $86.2 per ton on September 20, 2012, down from $106 per ton on January 3, 2012.

Imported (thermal) coal prices from Australia dipped by around 20 percent in the January-September period owing to the weak demand conditions prevailing in the market. Australian coal of 6,300 GAR is quoted at $89.5 per ton on September 20, 2012 compared to $112 per ton on January 3, 2012.

In the coking coal segment, prices of premium hard coking coal from Australia dipped 36 percent to $140.5 per ton on September 20, 2012 from $219 per ton

53.0

53.5

54.0

54.5

55.0

55.5

56.0

56.5

57.0INR movement against USD

50.00

60.00

70.00

80.00

90.00

100.00

110.00

120.00

130.00

PRIC

E ($

/TO

N)

South African Coal (6,000 kcal/kg NAR) Australian Coal (6,300 kcal/kg GAR)Indonesian Coal (5,900 kcal/kg GAR) Indonesian Coal (5,000 kcal/kg GAR)

International steam coal price trends in 2012 (FOB)

14 Coal Insights, September 2012

COvER sTORy

on January 3, 2012, mainly because of ample supplies from the miners and low demand from steel mills in India and other countries.

The semi soft variety also dropped 37 percent to $94.5 per ton on September 20, 2012 compared to $150 per ton on January 3, 2012. As a result of this, prices of imported met coke from Australia also fell 10 percent to $324 per ton CFR India from $363 per ton on January 3, 2012.

Sources said there is too much supply for the fourth quarter. The supply overhang is expected to continue unless there is a significant pick-up in global economic growth.

Analysts still expect the increase in global thermal coal export capacity in 2012-13 to slightly outpace demand growth, causing the market to remain in a state of slack.

There were reports of buying interest in lower-grade coal with a heating value of 5,500 kCal/kg.

News of further production and job cuts by Australian coal producers also added bearish sentiment to the thermal coal market. Reports said the world’s biggest miner, BHP Billiton, announced that it would stop production at its Gregory coking coal mine in Queensland.

Xstrata, the world’s largest producer of seaborne thermal coal, said in a statement that a significant portion of the Australian thermal and coking coal industry is losing money at current prices.

Although coking coal, which is used for steelmaking, and thermal coal, used for power

generation, are largely separate markets, low-grade coking coal and high-grade thermal coal are sometimes substituted for each other and supply and demand impacts can flow from one market to the other.

Power sector most vulnerable

The import boom was started by the sudden increase in coal requirement of the power utilities. While coking coal import remained more or less steady over the years, there was an abrupt increase in thermal coal import since 2002-03. Over the years, what started

as a stop-gap arrangement has become the mainstay of the sector’s expansion strategy.

Amid the ongoing debate over Fuel Supply Agreements (FSA) and price-pooling for imported coal, the power utilities becoming critically dependent on imported coal.

According to an estimate by the Ministry of Coal and Planning Commission, the demand for coal in the country for power utilities during 2012-13 would be 512 mt. Against this projected demand, supply from indigenous sources for power utilities has been estimated at 409 mt, leaving a shortfall of 103 mt.

It is estimated that CIL will supply 347 mt coal to power utilities while SCCL will supply another 37 mt. A total of 25 mt of coal is likely to come from other sources, including captive coal blocks, during the year.

The demand-supply gap during 2012-13 has been envisaged to be met through imports of about 68 mt of coal, equivalent to 103 mt of indigenous coal, according to the estimate.

As per the new FSA norms, the power sector may need to procure a substantial chunk of its coal requirements from overseas sources. Even for a non-coastal plant, this share may go up to 35 percent. Overall, the sector’s exposure to imported coal may rise to 30 percent of total consumption from current 13 percent over the next five years.

115.00

135.00

155.00

175.00

195.00

215.00

235.00

FOB

($/T

ON

)

HCC Peak Down Region Premium Low Vol HCC 64 Mid Vol

International coking coal price trends in 2012

Growing dependence on imported coal makes power sector vulnerable

16 Coal Insights, September 2012

Forex outgo raises concern

Apart from the power sector’s growing dependence on imports, the large forex outgo also poses a serious concern.

At the current rate, coal imports by India costs more than $10 billion, which is a sizeable part of the country’s total import bill. At current exchange rate, India’s coal import bill moved up 10 times in the last eight years. In Rupee terms, coal import bill increased from `50.1 billion (bn) in 2003-04 to a massive `415 bn in 2010-11. During April-October 2011, the value of coal imports shot up further to `457.3 bn. Overall, the country has spent over `250,000 crore on coal imports in the last 10 years.

The huge outgo on imports calls for attention in view of the rising current account deficit (CAD) of the country. CAD hit a record 4.2 percent of GDP in 2011-12 and rose further to 4.5 percent in January-March 2012. Only recently, Reserve Bank of India (RBI) has expressed grave concern over the rising CAD. Former RBI governor Y.V. Reddy has said that the government viewed a CAD of 2.5 percent of GDP as a safe average.

Captive chaos may boost import

The surge in coal imports, trading sources

said, has just begun, and may assume immense proportions in the coming years. While factors like logistics lags, currency depreciation and increasing stockpiles would restrict inflows to some extent, the current fiasco over captive block allocation by the government may s i n g l e - h a n d e d l y open the floodgate for increased flow of the dry fuel into the country.

There, however, may not be any drastic impact in the short term. “I don’t think there will be any significant impact of this controversy on

current production by CIL or others. So there will not be any near-term impact, good or bad, on import too,” said an industry veteran.

In the short term, the coal trading circle believes, the international prices will remain soft and Indian imports will witness a healthy growth in 2012-13 over last year. “The prices are likely to remain subdued this year. This is so because demand scenario is not so good. The US economy is not in a good shape and industries dependent on the US market are not doing well. The Euro Zone too is facing a slowdown. Australia is facing weakness in

industrial growth; so is Japan. Only South America, China and India have some demand,” the expert informed.

As a result, prices will continue to remain soft for some time. “It is to be seen how long they can hold on to these prices. Prices may take a beating,” he added.

According to Barclays, India’s imports could pick up in the second half of 2012 (July-December) and reach around 62 mt. This would take the annual import volume to over 110 mt in the calendar year, the report said.

In the medium term, however, the current controversy over block allocation may actually worsen the domestic supply scenario. If not anything else, the alleged coal scam report released by the Comptroller & Auditor General (CAG) and the subsequent enquiries initiated by the Central Bureau of Investigation (CBI) has put the captive production plans in a quandary.

The MoC can do little at the moment to pep up captive block owners to increase production. The only tool in hand is de-allocation of blocks. Already, a number of blocks have been de-allocated and some others are in the pipeline. Apparently, nobody is not sure about the fate of these de-allocated blocks. Even if these blocks are handed over to CIL – that again would be a lengthy process – the development and production from the same would be postponed for an indefinite period. All these would lead to increased requirement for imports, not only by the power sector but other consumers as well.

At this point, it is to be noted that the ministry’s medium-term goal placed highest importance to the captive production segment. While CIL and SCCL are likely to continue with a moderate rate of growth in production, the captive blocks were banked on for a significant spurt in volume. In the absence of this spurt, India’s dependence on coal imports will only accentuate further, bringing the growth engines of the economy critically dependent on foreign supplies.

Moreover, such a scenario would only replicate the country’s vulnerability to crude price movements in the international market. This would open yet another front of assault. The twin impacts of crude price hike on domestic inflation rates and also on the current account deficit and trade imbalance could be witnessed in case of coal as well. “Not the best of options,” said a coal industry veteran, “given that you have an option to avoid that.”

COvER sTORy

India’s coal import value (in `bn)

Year Coking coal

Non-coking coal

Total import

2003-04 36.7 13.4 50.1

2004-05 72.4 30.2 102.6

2005-06 95.4 53.7 149.1

2006-07 101.8 65.1 166.9

2007-08 121.0 86.4 207.4

2008-09 226.1 187.3 413.4

2009-10 201.3 190.5 391.8

2010-11 208.6 206.9 415.5

2011-12* 241.7 215.6 457.3

*up to October Source: MoC

Indian power utilities’ August import up 2.24% m-o-m

The import of steam coal by Indian power utilities, including imported coal based plants, in August 2012 stood at 4.1 million tons (mt), up marginally by 2.24 percent from 4.01 mt in July, as per provisional data of Central Electricity Authority (CEA) available with Coal Insights.

The import in August was lower than the target of 5.83 mt set by CEA for the month, but 0.91 mt higher than 3.19 mt imported in August 2011, the data revealed.

During August 2012, imported coal based plants had brought in 2.17 mt of coal whereas during the previous month, the figure stood at 1.87 mt.

The import during the first five months of 2012-13 stood at 21.99 mt, 24.61% lower than the target of 29.17 mt set for the period. However, imports during the first five months of current financial year were up 22.58 percent compared with 17.94 mt imported during the corresponding period of 2011-12, according to the data.

CEA has set a target of 70 mt for coal import by power utilities, including 24 mt by imported coal based plants, for 2012-13.

18 Coal Insights, September 2012

COvER sTORy

Coal Insights Bureau

Months after the government asked Coal India Ltd (CIL) to consider imports, the board of directors

of the coal monolith has finally given a go ahead. In a recent development, the board has approved import of coal for power producers that are ready to accept it on a cost-plus basis. This arrangement, however, will be in vogue until there is a consensus on the price-pooling mechanism under which customers will be charged a uniform average price for domestic and foreign fuel.

This stamp of approval brings to end an impasse over the proposal to import coal to meet the miner’s obligatory fuel supply requirements. As of today, CIL is committed to meet 80 percent of the power producers’ coal requirements, 15 percent of which can be met through imports. As per media reports, CIL may consider going for an import volume of around 15 to 18 million tons (mt) of coal per year.

It is, however, still not clear how the company plans to go about the task. CIL chairman S. Narsing Rao had earlier said

that the company would not go for adding another layer in the supply chain, nor will it take any hit to its bottomline. The scenario has become complicated after many consumers raised objections over the price-pooling mechanism.

Meanwhile, CIL’s plan to import coal has faced opposition from expected quarters. The workers’ unions which see the proposed move as a step towards privatisation have raised their objections to the plan.

“We will oppose the plan to import coal by CIL as we oppose any move to privatise the coal sector,” union sources said.

Even the board of CIL is still undecided about the diktat from the government. As per the new fuel supply agreement (FSA) proposed by the ministry, CIL needs to sign agreements for 80 percent of fuel supply requirements of power plants, 15 percent of which may be met by imports. However, with the board failing to take any conclusive stance on the issue, the matter is hanging fire.

Incidentally, the proposal of CIL importing coal was not received well by the market and experts. Shares of the company dipped on concerns that any decision to

CIL board approves import plan, traders unperturbed

import coal by CIL would add to its cost burden.

“The company does not have any exposure to coal import. Also, it will not like to just add another layer in the supply chain and the consumers would not like to source imports by paying a higher price,” said an industry source.

Importers not perturbed

Meanwhile, the pure play traders are not perturbed by CIL’s proposed move to import coal and pool prices to make imports less pricey.

Commenting on the issue, a leading south-based importer said, “First, you have to see how much will they import. I don’t think CIL will import much. Secondly, their operating cost will be high. They will give the coal primarily to government power companies. Private power companies will not take it from them.”

Also, the government organisations are not very flexible in operations and will perhaps not be able to change their operations to take advantage of price movements, he said. Thus, the proposal may not look very lucrative to them after a while.

“Government agencies like MMTC and State Trading Corporation (STC) have high operating costs. There is hardly any accountability on loss. They have a high cost structure as compared to the private players. Also, their transport cost is at par. And they keep 10-12 percent margin. The only advantage they enjoy is that they play on volumes. For instance, these companies can take a few panamax vessels (100,000 tons capacity) at a time. Thus, the law of average helps them manage the operations. But then, their distribution is not good,” the trader said.

In comparison, private players who have integrated systems to import, can have proper supervision and have well-managed stocking facility. “Such players will continue to do well, no matter who comes into the trade. The market is huge and it will continue to grow.”

He however proposed that “a good model could be to involve small traders who can source and trade.” The ministry could consider outsourcing the activity to these players. The large PSUs, in turn, could bring those sources under one umbrella and do the distribution part, he added.

20 Coal Insights, September 2012

In the international market, Australian thermal coal of heating value of 6,300 kcal GAR is being offered at around $89.55 per ton in September against $90 per ton in August. Offers of South African thermal coal of heating value of 6,000 kcal NAR fell marginally to $86.55 per ton in September from $87.65 per ton in August. Offers of Indonesian coal of 5,900 kcal GAR is hovering around $72.8 per ton in September, while coal of heating value 5,000 kcal/kg GAR is quoted at $56.8 per ton.

Traders said deals are struck only if the

commodity is required urgently. No one is buying to stock coal and small power projects are also buying low grade coal with high ash.

Outlook

Analysts feel India’s coal imports are expected to rise in the financial year through March 2013 as more end-users turn overseas. Excess supply has hammered international thermal coal prices in recent months, with top exporter Indonesia cutting its output forecast to around 360 million tons (mt) from 390 mt to 400 mt for 2012.

According to analysts, based on the current global supply and demand picture, end users expect thermal coal prices to remain well below $100 per ton for the next 10-12 months.

COAL mARkET funDAmEnTALs

Coal Insights Bureau

Imported thermal coal prices remained flat in September even as inquiries from India increased as the monsoon season is

almost over. However, the rise in inquiries is not translating into business due to a wide gap between bids and offers.

Inquiries for low calorific value 3,600 kcal/kg to 4,200 kcal/kg GAR coal have risen, but there is a $2-4 per ton difference between bids and offers. Participants added that Indian buying demand is almost negligible as the country grapples with a sluggish industrial economy and high stockpiles at ports.

The stockpiles of both unsold and contracted coal are reported to be around 5 million-6 million tons at various ports, sources said. Some sources said a couple of large power utilities are renegotiating their contracts or finding loopholes to wriggle out of old coal contracts.

Meanwhile, the softening of Richards Bay FOB prices has reignited the interest of Indian buyers and inquiries have started coming in for South African coal.

Ultratech Cement, for example, is in the market for 170,000 tons of South African coal, according to reports. Sources said that

several cement producers are more interested in cheaper US coal than South African coal.

Analysts also expect imports to take place with appreciation of rupee to `53.54 per dollar from levels of ̀ 55 per dollar in August.

Thermal coal import prices remain flat in Sept

Steam coal CFR India ($/ton)

Date West (6,300 kcal/kg GAR)

West (5,900 kcal/kg GAR)

West (5,000 kcal/kg GAR)

East (6,300 kcal/kg GAR)

East (5,900 kcal/kg GAR)

East (5,000 kcal/kg GAR)

5-Jul 107.05 83.40 66.65 108.65 82.90 66.15 11-Jul 101.15 82.00 64.75 102.55 81.40 64.25 18-Jul 102.65 81.40 64.35 104.10 80.70 64.00 24-Jul 101.60 80.90 64.35 103.05 80.00 63.70 25-Jul 101.70 80.75 64.30 103.15 79.80 63.60 26-Jul 102.00 80.55 64.20 103.50 79.60 63.50 31-Jul 104.55 79.50 63.40 106.05 78.55 62.70 2-Aug 104.25 79.05 62.90 105.75 78.10 62.20 3-Aug 103.75 79.05 62.90 105.25 78.10 62.20 17-Aug 104.10 79.70 63.75 105.60 78.70 63.05 20-Aug 103.90 79.70 63.75 105.40 78.70 63.05 23-Aug 103.90 80.15 64.25 105.40 79.15 63.55 28-Aug 101.30 80.40 64.65 102.80 79.40 63.95 4-Sep 102.70 80.75 65.30 104.30 79.75 64.60 10-Sep 100.15 80.75 64.95 101.65 79.85 64.25 11-Sep 99.45 80.85 65.10 100.95 79.95 64.45 12-Sep 99.15 80.85 65.10 100.65 79.95 64.45 13-Sep 96.80 80.55 64.70 98.10 79.65 64.05 14-Sep 98.35 80.35 64.50 99.65 79.65 64.05 20-Sep 99.60 80.55 64.40 100.80 79.95 64.05

50.00

60.00

70.00

80.00

90.00

100.00

110.00

120.00

130.00

7-Ju

n

13-Ju

n

19-Ju

n

25-Ju

n

1-Ju

l

7-Ju

l

13-Ju

l

19-Ju

l

25-Ju

l

31-Ju

l

6-Au

g

12-A

ug

18-A

ug

24-A

ug

30-A

ug

5-Se

p

11-S

ep

17-S

ep

PRIC

E ($

/TO

N)

East (6,300 kcal/kg GAR) East (5,900 kcal/kg GAR) East (5,000 kcal/kg GAR)

Steam coal price trends CFR India

22 Coal Insights, September 2012

COAL mARkET funDAmEnTALs

Coal Insights Bureau

Imported spot coking coal prices eased 12 percent in September, compared to August, on back of plentiful supply and

lean buying interest. Premium low-volatile hard coking coal dipped further, while the price for second-tier PCI was supported by Chinese buying.

Premium low-vol HCCs traded at around $141 per ton FOB Australia, down from levels of $160 per ton in August end. Low vol PCI prices recovered to $103 per ton from a low $101 per ton with some buying

Imported spot coking coal prices ease 12% in Sept

interest. However, the semi soft variety was quoted at $94 per ton, down from $101 per ton in August.

Major miners of Australia were reported to have given relatively lower offers to China, India and Europe, implying increased pressure on producers to get their coal moved. Some indicative bids found from

Coking coal expected to remain weak till Dec: Coke makerCoal Insights Bureau

The spot prices of premium coking coal may continue to weaken further till December despite BHP

having recently decided to close down operations at two of its mines, an official of a leading coke maker told Coal Insights.

“The current weak trend in spot coking coal prices, which is being quoted at around $145 per ton, has forced miners to cut the contract price for the October-December quarter to around $170 per ton from a high of $221-$225 per ton for the July-September quarter. This weak trend is likely to continue till December and thereafter it will depend on the global economic situation,” the official said.

BHP Billiton had in May decided to shut its Norwich Park mine and on September 9 announced to cease production at Gregory mine, both in Australia, citing steep fall in coking coal prices that made its operations unprofitable.

“In any case, the quality of coal from these two mines was not that good and thus there were hardly any buyers. The

material from these two mines was being sold by BHP at much lower rates. Norwich Park coal was of ultra-low volatile category whereas Gregory mines coal was of high volatile category,” the official said.

Miners generally opt for planned shutdowns whenever the prices of coking coal come down in an attempt to reduce supplies to keep price firm. However, this year till now, this strategy does not seem to have worked.

According to industry experts, there is abundant availability of coking coal in the market at present while demand from steel makers is not that encouraging due to weak market conditions in most part of the world, including China and India.

“It is expected that steel demand will pick up in the fourth quarter of 2012 and that will pave the way for an increase in steel price and consequently an increase in coking coal prices may be from the beginning of 2013 ,” he said.

Asked why he feels that coking coal prices would start firming up from January 2013, the official explained that at present miners in the US and Canada are continuing

operations despite not making profits due to sharp fall in prices consequent to decline in natural gas prices and this is maintaining a healthy coal supply situation in the global market.

In fact, they are storing the middlings and rejects and exporting the prime material to maintain cash flow, he said. They are storing the material in the hope that prices would revive soon and they would be able to dispose those materials at better prices later on.

The same thing is happening in Mozambique from where coking coal is now being exported. They too are storing the middling and rejects as there is no outlet for such material.

But there is a limit to which they can continue storing the material, because it amounts to blocking the capital and a stage will surely come when they have to shut operations. Once that happens, probably by December-end, there will be sharp reduction in coking coal supplies world over and then prices would start firming up, the official said.

130.00140.00150.00160.00170.00180.00190.00200.00210.00220.00230.00240.00

FOB

($/T

ON

)

HCC Peak Down Region Premium Low Vol HCC 64 Mid Vol

Coking coal price assessment (FOB)

24 Coal Insights, September 2012

China and Europe were at around $140 per ton FOB; however, no immediate purchase was observed.

Elsewhere, Australian coal miner Anglo American and South Korean steelmaker Posco settled their PCI coal contract price at $125 per ton FOB for the fourth quarter, 22.8 percent lower than $162 per ton FOB in the third quarter.

The two companies also followed the

Q4 premium low-volatile hard coking coal price settled earlier by Japan’s Nippon Steel, and BHP Billiton-Mitsubishi Alliance, and signed German Creek premium HCC at $170 per ton FOB. This is down $55 per ton, or 24 percent, from $225 per ton in Q3.

The settlement of BHP Mitsubishi Alliance labour unrest has proven to be detrimental to the interests of Australian miners. This has resulted in rebound in

supply, thereby hurting price sentiment. Sources said the major purchasers from India and China have been reticent owing to monsoon and cheaper availability from domestic and Mongolian sources.

However, the reticence in the market is not expected to last long. Indian majors cannot postpone buying for more than a month with inventory levels depleting fast. Moreover, with the end of monsoons in September, construction activity is expected to pick up resulting in more demand for steel.

According to Indian coke maker Gujarat NRE Coke Ltd, India’s coking coal import requirement might rise to over 50 million tons per annum (mtpa) from the present 35 mtpa by 2015-16 in line with steel industry production of 120 mtpa by that time.

Met coke

Lack of buying appetite continued to characterise the metallurgical coke market. Coke with 12.5 percent ash was quoted at $324 per ton, down from $343 per ton cfr east India a month earlier.

In India, met coke prices hovered around `19,500 per ton in the eastern region, sources said.

According to Gujarat NRE Coke, only organisations owning large met coke production capacities with strong linkages for raw material sourcing can withstand the competition in the global met coke market with huge opportunities to expand their business.

The demand supply gap across the globe for met coke is significantly attracting more players to enter this segment to reap the benefits. However, shortage in availability of crucial raw material i.e coking coal has restricted the entry of new suppliers, making the market skewed in favour of the suppliers, the company said.

The future of the met coke industry relies heavily on the future of the steel industry, with majority of steel still being produced through blast furnace route. Therefore, any slump in steel industry would adversely affect the met coke industry.

The met coke industry has also been impacted by availability of crucial raw material i.e coking coal with its global supply generally determining the prices of both coking coal and met coke, the company said.

Coking coal FOB Australia ($/ton)

Date HCC Peak Down Region

Premium Low Vol

HCC 64 Mid Vol Low Vol PCI Low Vol 12

Ash PCI Semi Soft

5-Jul 219.00 219.50 175.50 145.00 127.50 109.50

11-Jul 215.50 216.00 171.00 143.00 128.00 105.50

18-Jul 210.00 210.50 170.50 139.50 126.50 104.50

24-Jul 190.50 191.00 165.00 138.00 116.00 102.50

25-Jul 187.50 188.00 163.50 136.50 113.00 102.50

26-Jul 181.50 182.00 158.00 132.50 109.00 95.50

31-Jul 181.00 181.50 157.50 128.50 104.50 95.50

2-Aug 180.00 180.50 157.50 128.00 104.50 96.00

3-Aug 180.00 180.50 157.00 128.00 104.50 96.00

17-Aug 166.50 167.00 146.50 116.00 99.00 108.00

20-Aug NA NA NA NA NA NA

23-Aug 162.00 162.55 139.00 114.50 96.50 104.00

28-Aug 159.50 160.00 139.00 114.00 98.50 101.50

4-Sep 157.50 158.00 133.50 111.00 92.50 98.50

10-Sep 147.50 147.50 131.00 106.50 94.00 98.00

11-Sep 147.00 147.00 131.00 105.00 94.00 98.00

12-Sep 145.50 145.50 130.50 105.00 94.00 98.00

13-Sep 144.00 144.00 128.50 104.00 93.50 98.00

14-Sep 140.50 140.50 124.50 103.50 93.00 97.50

20-Sep 140.50 140.50 124.50 103.00 94.00 94.50

80.00

90.00

100.00

110.00

120.00

130.00

140.00

150.00

160.00

170.00

1-M

ay

7-M

ay

13-M

ay

19-M

ay

25-M

ay

31-M

ay

6-Ju

n

12-Ju

n

18-Ju

n

24-Ju

n

30-Ju

n

6-Ju

l

12-Ju

l

18-Ju

l

24-Ju

l

30-Ju

l

5-Au

g

11-A

ug

17-A

ug

FOB

($/T

ON

)

Low Vol PCI Low Vol 12 Ash PCI Semi Soft

Coking coal price assessment (FOB)

COAL mARkET funDAmEnTALs

26 Coal Insights, September 2012

Coal Insights Bureau

Coal India Ltd (CIL) has scrapped its earlier plan to revive 18 underground (UG) abandoned mines through

selection of joint venture partners due to lack of satisfactory response and the company has now decided to revive these mines by appointing the Mine Developer & Operator (MDO) route, an official of the ministry of coal has said.

Initially 18 UG abandoned mines, each having more than 10 million tons (mt) of reserves were identified for revival by inviting expression of interest (EoI) for selection of JV partners.

“As the response was not satisfactory, CIL had decided to revive these mines by appointing the MDO,” the official said.

Of the 18 mines, Bharat Coking Coal Ltd (BCCL) had the maximum number of eight mines, while Eastern Coalfields Ltd

(ECL) and Central Coalfields Ltd (CCL) had six and four mines respectively.

The move was in line with new CIL chairman S. Narsing Rao’s expressed intention to focus on MDO route for increasing production. Days after assuming office in April, Rao had said that CIL would appoint MDOs to develop and mine new blocks as well as old blocks in difficult terrains.

The issue of reopening abandoned mines has been hanging fire for some time now. Industry sources welcomed the move to opt for MDO route, but expressed doubt about the viability of operations in some of them.

Earlier, CIL in 2008 had planned to open 18 abandoned mines with total reserves of around 1.6 billion tons. The company had completed the bidding process in 2009. Although the bidding process was apparently successful and production was expected to start in 2010, the projects failed to take off as

CIL scraps JV route for mine revival, opts for MDO

bidders did not find them economically viable. The companies shortlisted in the first round of bidding included ArcelorMittal India, Rio Tinto, Titan Mining, JSW Steel, JSW Energy, Monnet Ispat, Essar Mineral Reserves and Sunflag Iron & Steel. The primary reason of the mines not being remunerative was the poor quality of coal available in them, according to industry sources.

SCCL to revive mines

Meanwhile, Singareni Collieries Company Ltd (SCCL) has proposed to revive at least three closed opencast (OC) mines during the 12th Plan period, the coal ministry official said. The mines to be revived are MNG opencast at Manuguru, RKP opencast at Mandamarri and RG opencast III phase 2 at Godavari Khani, he said.

SCCL has currently a total of 174 functional and non-functional coal mines.

The assessed geological coal reserves in the command area of SCCL stand at about 9,877 mt, of which 2,064 mt stand consumed on account of the production from the mines since inception of the company.

About 2,344 mt of reserves are available in the operating mines and about 5,469 mt of reserves are untapped.

However, of these untapped reserves, the reserves that can be projectised are assessed to be 2,959 mt and the balance 2,510 mt are difficult to mine and cannot be projectised due to geological disturbances and adverse geo-mining conditions.

At the current level of production of about 52 mt, the currently assessed extractable reserves in the command area of SCCL are expected to last for over 60 years.

During the 12th Plan (2012-17), an Exploration Programme for Drilling of 650,000 metres in virgin blocks of SCCL command areas is envisaged. It is also planned to carry out 16,500 metres of drilling under Regional Exploration Programme of Geological Survey of India (GSI) and 80,000 meters drilling under the Ministry of Coal’s Plan Scheme of Promotional Exploration during the 12th Plan period in the command area of SCCL.

Further, SCCL envisages increasing the current level of production of about 52 mt achieved in 2011-12, the terminal year of the 11th Plan to 57 mt in 2016-17, the terminal year of the 12th Plan and to 63 mt in 2021-22, the terminal year of the 13th Plan.

fEATuRE

28 Coal Insights, September 2012

fEATuRE

growth in coal production by CIL last year after a period of stagnated growth.

“After near-stagnation in the country’s coal production for two consecutive years 2009-10 and 2010-11 at 533 million tons (mt), the year 2011-12 saw a 12-mt rise at 545 mt. Of this, exactly 80 percent (i.e. 436 mt) came from the main producer, Coal India Ltd, as against its achieving 431 mt in the previous two years,” Arora said.

He said that: “In a situation of restricted activity with imposition of CEPI (comprehensive environmental pollution index) and ‘go-no-go’ hurdle that continued till March 2012, CIL’s building-up a 5-mt increase is a reasonable achievement”.

Arora, however, expressed concern at the lack of growth in production from underground mines.

“From 75 mt of country’s underground raising witnessed two decades ago, the situation in UG production has not improved at all and has rather deteriorated. Hardly 60 mt yearly is now produced from UG mines,” he said.

On the positive side, Arora noted that S. Narsing Rao, currently the chairman of CIL, had put in serious efforts to bring in modernisation in underground technology at Singareni Colliery Company Ltd (SCCL). This effort had helped significantly improve SCCL’s performance in underground mining.

“We are hopeful that under Rao’s stewardship, CIL will soon be able to turn the tables,” he added.

Commenting on the ongoing discussions about fuel supply agreement (FSA), he said, “For the power plants, besides the 80 percent trigger level (a precise percentage of annual contract quantity that coal company will supply and consumer will lift), it has now been decided that Coal India will bear penalties on a slab basis – from 1.5 to as high as 40 percent depending on the extent of supplies.”

While such penalties are being considered for supplies to the power sector, Arora said similar provisions could be thought of for other coal consuming industries. “It is our request to CIL that the interest of a large number of consumers in non-power group where supplies are never made on quality or quantity terms nor even on time and whose contribution is nonetheless significant in the country’s economy, should not be ignored,” he added.

Delayed delivery defeating the purpose of coal e-auction: ICMA

Coal Insights Bureau

Delayed delivery of coal purchased through e-auction is defeating the very purpose of this route and

leading to loss of interest among a section of buyers, the Indian Coal Merchants Association (ICMA) has alleged.

“E-auction has been of mutual interest for the companies and the consumers who earlier had less opportunity to buy fuel directly from the coal companies, but it has been found that after paying the full price in advance, the supplies from Coal India Ltd (CIL) remained stalled for months with large sums remaining blocked with the coal companies,” ICMA president V.K. Arora said.

In fact, a large number of rakes taken in e-auction remain in arrears and consumers are denied timely supplies, he alleged.

Arora, who was addressing the 81st Annual General Meeting of ICMA in Kolkata, further said, “In a way, the very spirit of e-auction is lost due to considerable delay in deliveries. We request CIL and Ministry of Coal to seriously look into the matter,”

About the likely cause of this problem, he said, “We find a trading of charge going between Railways and the collieries. While

Railways put the onus on collieries’ poor loading performance, collieries hold the Railways responsible for their short supply of rakes and heavy left-behinds.”

Besides, ICMA was also concerned about the high prices of coal sold through e-auction route. An “ever-widening” gap between the notified price and the e-auction price by `1,500 and more per ton is a huge problem and at times prevents customers from bidding, Arora said.

Earlier, some of the ICMA members had expressed their dissatisfaction about the alleged mismatch in coal quality announced and delivered (grade slippage) through e-auction. CIL, on its part, however has claimed that such instances were few and far between. In case of specific complaints, CIL sources said, prompt action is taken to redress the problem.

According to data provided by CIL, total revenue from e-auction of coal increased from `1,480.78 crore in 2007-08 to `13,826.88 crore in 2011-12. The total volume of coal sold through e-auction by CIL also increased from 28.79 mt in 2007-08 to 49.70 mt in 2011-12.

Non-power sectors

Meanwhile, ICMA has welcomed the

(Inset) V K Arora, President, ICMA

30 Coal Insights, September 2012

fEATuRE

Power sector feels the heat

SPU loan restructuring to reach `1.5 trillion: CRISIL

Coal Insights Bureau

Restructuring of bank loans taken by state power utilities (SPUs) may reach a staggering `1.5 trillion for

the period 2011-12 to 2012-13, according to a report released by CRISIL.

“In recent months, availability of unsecured short-term loans from Indian banks has diminished. This is exacerbating refinancing and liquidity pressure, especially for the SPUs.

This will lead to a significant increase in restructuring of SPU loans to nearly `1.5 trillion. So far, SPU loans of `0.6 trillion have been restructured,” says Pawan Agrawal, senior director, CRISIL Ratings.

The total volume of loans restructured by Indian banks may increase sharply to `3.25 trillion between 2011-12 and 2012-13,

against the earlier estimate of `2.0 trillion, the report says.

The majority of restructuring will be in loans to SPUs, construction and infrastructure sectors. The rise is a result of significantly higher funding challenges being faced by companies with large debt.

A significant part of the restructured loans may also slip into non-performing assets (NPAs). However, this will depend on the terms of restructuring and fundamental viability of the projects and the companies, the report says.

Loans of `1.6 trillion have already been restructured in 2011-12 and in the first quarter of 2012-13. The majority of restructuring will be in loans to the state power utilities (SPUs), and the construction and infrastructure sectors. The rise is a result of significantly higher funding challenges being faced by companies with large debt.

It is most likely SPU-loan restructuring will happen through a centralised scheme coordinated by the government of India (GoI).

“Furthermore, inability to raise adequate equity in a timely manner is straining the balance sheets and financial flexibility of developers in infrastructure and construction sectors, resulting in an increased likelihood of restructuring”, adds Agrawal. Other vulnerable sectors include iron and steel, textiles, and engineering.

The proportion of restructured loans in this period will be high at around 5.7 percent of banks’ advances as on March 31, 2013. Adds Agrawal, “Around `0.50 trillion of these restructured loans may slip into NPAs, though this will depend on the terms of restructuring and fundamental viability of the projects and the companies. These slippages can aggravate the already stressed asset quality of banks by further increasing NPAs by 50 to 75 basis points beyond March 2013.”

The loans to SPUs are unlikely to slip into NPAs, given the support expected from state and central governments.

Despite continued weak growth and profitability in the corporate sector, the large restructuring will help limit the increase in the banks’ NPAs in the near term. According to CRISIL’s estimates, the lower GDP growth of 5.5 percent expected in 2012-13 may result in increase in banks’ gross NPAs to 3.5 percent by end-March 2013 from around 3.0 percent at the end of June 2012. The increase will be driven largely by delinquencies in the micro, small and medium enterprises, and agriculture and allied sectors.

CRISIL Ratings director, Suman Chowdhury, says, “The banks have sought to arrest the deterioration in asset quality through measures such as strong senior management focus on recovery, setting up dedicated teams for collections, and tightening of underwriting norms. While the banks’ adequate capitalisation, expected support from GoI for public sector banks, and stable resource profiles will continue to support their credit risk profiles, any significant and sustained deterioration in asset quality and earnings may lead to weakening in the banks’ credit quality.”

32 Coal Insights, September 2012

fEATuRE

Capacity addition

A total of 550 MW of power generation capacity was added in India during the month of August 2012, taking the total installed generation of the country to 207,006.04 MW, a provisional data prepared by CEA revealed.

The capacity addition in July was 950 MW. With this total power generation capacity added during the first five months of 2012-13 (April-August) stood at 6,766 MW, as per CEA’s revised data.

The capacity addition of 550 MW in August was in thermal power sector where private sector companies – BPSCL (250 MW) at Bina TPP Unit 1 in Madhya Pradesh and Vidharba Ind. Power Ltd (300 MW) at Butibori TPP Unit 1 in Maharashtra.

In July 2012 also, the entire capacity of 950 MW was added in the thermal sector of which 150 MW came in Andhra Pradesh at Simhapuri Phase-I while the remaining 800 MW was added in Gujarat at Mundra Ultra Mega thermal power project of Tata Power.

Critical coal stock

Inadequate coal supplies by domestic coal companies and lower imports by power utilities have led to critical coal stock position at a number of Indian power plants.

According to data available with Coal Insights, a total of 31 plants of the total 89 in the country were faced with critical coal stock position of less than seven days as on August 30.

Sanjukta Ganguly

India’s power generation in August 2012 fell to 74,338.11 million units (MU) from 76,035.74 MU generated in July,

according to provisional statistics of the Central Electricity Authority (CEA).

The generation in August was significantly lower than the target of 77,794.00 MU, the data showed.

Power generation in August 2011 or the corresponding month of previous financial year was 73,101.19 MU against the target of 72,760.64 MU, which implies that year-on-year generation was up slightly.

The country’s power generation during the first five months (April-August) of 2012-13 stood at 382,305.76 MU, up 1.58 percent compared with the target of 376,363.00 MU for the period and up 4.95 percent compared with 364,281.02 MU generated during the corresponding period of 2011-12.

Of the total generation in August 2012, 56,687.72 MU (53,353.32 MU in August 2011) was from thermal sector, 2,579.08 MU (2,719.71 MU) from nuclear sector, 14,036.04 MU (16,004.07 MU) from Hydro sector and Bhutan imports was 1,035.27 MU (1,024.09 MU).

The actual generation was lower than the target of 58,573 MU for thermal sector and 15,818 MU for hydro sector but higher than 2,527 MU target for nuclear and 876 MU for Bhutan import.

In July 2012, 60,533.85 MU was generated by thermal sector, 2,709.35 MU by nuclear sector and 11,868.66 MU by hydro sector. Imports from Bhutan stood lower at 923.88 MU.

India’s August power generation falls m-o-m: CEA

Source: Central Electricity Authority

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Thermal Hydro Nuclear

Target

Achievement

Achievement vs target in capacity addition (in MW)

Source: Central Electricity Authority

76%

4%

19%1%

Thermal

Nuclear

Hydro

Bhutan Import

Categorywise energy generation in August 2012 (in %)

34 Coal Insights, September 2012

fEATuRE

The data further shows that out of the 31 plants facing ‘critical coal stock’ position, 19 were facing ‘super critical’ coal stock position of less than four days.

On August 15, out of the 31 plants (out of 89 plants) facing critical coal stock position of less than seven days, 20 were facing ‘super critical’ coal stock position of less than four days. Plants in Uttar Pradesh, Bihar, Andhra

Pradesh and West Bengal were the worst sufferers.

Plant load factor

The Plant Load Factor (PLF), a measure of the output of a power plant compared to the maximum output it could produce, for the country for the month of August 2012 stood at 61.47 percent against the planned 65.33 percent. The PLF was 66.84 percent, 72.05 percent and 73.89 percent for July 2012, June 2012 and May 2012, respectively.

The PLF of power plants of central sector run companies such as NTPC and DVC in August 2012 stood at 69.65 percent whereas the figure achieved in July 2012 was at 78.26 percent. In August 2012, the plants in the private sector recorded a PLF of 56.82 percent against the planned 60.03 percent.

The worst performers were Muzaffarpur TPS and Koderma TPS both of which recorded nil PLF against a target of 16.5 percent and 39.78 percent, respectively. Farakka STPS which recorded a PLF of 46.33 percent against a target of 72.45 percent continued to be a poor performer.

Power supply position

In the month of August 2012, the country’s peak power demand was estimated at 82,690 MU, but actual availability was only 75,077 MU, reflecting a shortfall of 7,613 MU or 9.2 percent.

Earlier, in the month of July 2012, the country’s peak power demand was estimated

at 85,504 MU, but actual availability was only 77,731 MU, representing a shortfall of 7,773 MU or 9.1 percent.

An interesting observation is that despite overall peak shortage of power in the country in August 2012, Chandigarh, Lakshadweep and Sikkim did not have any peak power shortage, according to CEA data. Andhra Pradesh faced the highest shortfall among all states during peak period with a total shortfall of 1,723 MU.

Uttar Pradesh recorded the second highest shortfall during the month under review. The state recorded total shortfall of 1,392 MU in August 2012, against 1,377 MU in July 2012. Tamil Nadu was a poor performer recording a shortfall of 1,078 MU against 710 MU in July 2012. Maharashtra recorded a shortfall of 361 MU against 439 MU during July 2012 whereas Bihar faced a shortfall of 161 MU which also stood at the same figure in July.

DPSC welcomes FDI in power exchanges

DPSC Ltd, a power utility and a promoter entity in the National Power Exchange Limited, has

welcomed the government’s decision permitting foreign investment in power exchanges in the country.

“The government’s decision to permit foreign investment up to 49% in power exchanges is a welcome move for the sector. The decision opens the opportunity for many foreign players to be part of India’s growth story. India has a huge opportunity in the infrastructure sector that includes power,” Anup Bhargava, managing director of DPSC, said in a statement. He said the foreign partnerships would bring in efficiency and technological enhancement for the exchanges.

Further, “the partnership would also be helpful in getting financial support from foreign partner. For foreign investors too, the move opens opportunities to become a partner in India’s emerging growth story in the power sector,” he added.Capacity addition (in MW)

Months 2012-13 2011-12

April 1,760 735

May 1,070# 550

June 2,376 2,224

July 950 1,660

August 550 1,200

September 786.5

October 345

November 2,807

December 1,158

January 895

February 972

March 5,482*

Total (Apr-Aug) 6,706 6,369

Total (Apr-March) 6,766# 18,814.5*

*As reported by CEA, capacity addition in March was 5,482 MW, but the total figure for 2011-12 was increased to 20,501.70 MW instead of 18,814.50 MW following revision in March 2012 figures. # CEA had earlier reported that capacity addition in May (2012-13) was 1,070 MW, but it appears that the figures have been revised to 1,130 MW.

Source: Central Electricity Authority

0

10

20

30

40

50

60

70

80

Central State Sector Pvt. Utl.Sector

All India

Program

Achivement

All India PLF factor in August 2012 (in % )

36 Coal Insights, September 2012

fEATuRE

Coal Insights Bureau

The pure-play sponge iron makers are facing extinction. According to an estimate, about 20 percent of the

sponge iron units in the country have shut down operations in the last one year, almost all of them being standalone plants. A good number of them have already been sold. For the remaining units, industry sources say, they may not be able to open shop ever again.

Over the last few years, the number of major operating sponge iron or direct reduced iron (DRI) plants has nearly halved from 150 in 2005 to around 80 in 2012. Periodic closures are nothing new to this industry. In the past too, there were mass closures of smaller units during severe power outages or crackdown by pollution control boards or slackness in steel demand.

But this time round, the sources feel, their basic viability is in peril. Even larger units which run on standalone basis are facing survival woes, and may not survive unless they go for forward or backward integration.

“In the current scenario, standalone sponge iron units are no more viable. The market dynamics will not let these plants

survive the current downturn. In fact, almost all such units have been sold,” said an industry expert.

A short haul

Although the first DRI plant in India was set up in 1979, the sector saw some real action only in the recent past. The emergence of this industry was primarily driven by the shortage of coking coal in the country and relative abundance of non-coking coal and iron ore. Also the scarce supply of scrap for steelmaking played a catalyst.

It was not until the late 1990s that production really picked up. According to a Joint Plant Committee (JPC) survey, the number of operational units in 2000-01 was 23 with total production capacity of 6.97 million tons (mt). This number witnessed a prolific growth in the following years. As of 2005, the total number of working DRI plants was 150 and the capacity around 17 mt. Besides, 58 more coal based units were reported as under-commissioning greenfield projects with total capacity of 6 mt. Moreover, another 7 mt of capacity was in the process of being added through brownfield expansion.

A salient feature of this expansion drive

Time to wind up standalone DRI plants?

was that almost all the new plants were set up as coal-fired units. Of the 150 operating plants in 2005, only three large plants were put up as gas-based units by Essar Steel, Vikram Ispat and Ispat Industries. This was against the global trend and was mainly driven by easy availability of cheap coal.

The factors that led to the growth of the DRI plants were steady growth in domestic steel demand, a robust increase in domestic steel production led by the secondary steelmaking sector, low investment requirement for DRI, availability of mineral resources and lower availability of scrap, among others.

However, within a short period, the scenario changed altogether. Growth in coal production came to a halt as Coal India Ltd (CIL) faced serious hurdles in obtaining statutory clearances from the environment ministry. Iron ore mining was banned by the Supreme Court in Karnataka due to rampant illegal mining. The increasing demand-supply gap led to a rise in raw material prices. Additionally, the scarcity in power supply and strict pollution norms led to the temporary shutdown of a large number of units.

Finally, the sagging demand for steel in the domestic market put price pressure on sponge iron, making small plants unviable altogether. Interestingly, the same factors that helped the sponge iron industry to thrive over the last decade proved their undoing.

Poor economics

Commenting on the viability of the standalone units, industry sources said the market condition for sponge iron is currently in a bad shape. “The DRI plants mainly cater to induction furnaces which in turn produce ingots. From ingot, TMT and structural are made, which are long products used in the construction sector. Since the construction industry is down, demand for TMT and structurals is also subdued.”

Elaborating on the question of viability, the sources said the current cost structure facing the standalone units makes it clear that these projects are facing worst margin pressure.

A rough calculation shows that to produce 1 ton of sponge iron, 1.6 tons of iron ore is required. Currently, the price of iron ore is hovering around `8,000 per ton. Accordingly, the cost of ore (including

Coal Insights, September 2012 37

fEATuRE

freight) comes to around `15,000 per ton. The cost of coal accounts for another `5,000 per ton of DRI. Adding working capital and other miscellaneous cost components, the

total cost of production is arrived at around `21,000-22,000 per ton.

In addition, the sponge iron industry is faced with ongoing problems of high power prices in Maharashtra and power cuts in Andhra Pradesh and Tamil Nadu. Sources said demand has been weak on power issues and most sponge iron plants have reduced production. This further adds to the production costs.

Against this, the current price of sponge iron (ex-works) is around `22,000 per ton, which leaves hardly any margin for the plants to recover the fixed costs or loans taken for the plant. Unless the raw material prices dip, which is quite unlikely, or the sponge iron prices rise, the viability of these plants would remain doubtful, a market expert informed.

“Only if ore price reduces or sponge iron price increases, they can become viable. But now steel demand is low and therefore sponge iron price is low. In September-October, steel demand increases. Sponge iron price may go up to `25,000-26,000 per ton. But when demand increases, ore price will also increase. So on the whole, standalone units will not be viable,” he added.

United they stand

The problem, the sources said, is not so much for units that are either forwardly or backwardly integrated.

Since sponge iron finds its end use in TMT or structural, plants that have forward integration can survive the current onslaught. This is so because the steel mills, though facing low demand, are still earning margins.

Similarly, companies that are backwardly integrated (having own captive mines) also have some breathing space.

“These companies will survive because of the captive mines. Their mining cost is minimal, if compared with the market price of the minerals. For instance, the mining cost for ore is around `1,000 per ton, compared to the market price of `8,000 per ton. This cost advantage will help them survive tough patches.”

Some of the larger firms are now striving to adopt advanced technologies to reduce costs further and also to deal with pollution problems. In the face of severe coal scarcity in the country, some steelmakers are also trying to substitute coal by underground coal gasification (UCG) for their DRI units.

DRI exports up inApril-July period

Even though the domestic market is facing severe survival woes, sponge iron exports from India

rose sharply during the April-July 2012 period, latest provisional steel ministry data showed.

DRI exports during April-July 2012 stood at 22,590 tons, compared to 880 tons in the same period last year, the data showed. Bar and rod exports from India rose 87 percent year-on-year, while structural exports rose 78 percent year-on-year during the April-July period. GP/GC sheet/coil exports rose 22 percent year-on-year, while ferro alloy exports were up 23 percent year-on-year.

38 Coal Insights, September 2012

Sanjukta Ganguly

At a time when coal scarcity has hit expansion plans in almost all consuming sectors, the Indian

paper industry has remained by and large untouched by the supply shortage.