CNBC Fed Survey, September 17, 2013

of 36

Transcript of CNBC Fed Survey, September 17, 2013

-

7/29/2019 CNBC Fed Survey, September 17, 2013

1/36

CNBC Fed Survey September 17, 2013Page 1 of 36

FED SURVEYSeptember 17, 2013

These survey results represent the opinions of 47of the nations top money managers, investment

strategists, and professional economists.

They responded to CNBCs invitation to participate in our online survey. Their responses were collecte

on September 12-13, 2013. Participants were not required to answer every question.

Results are also shown for identical questions in earlier surveys.

This is not intended to be a scientific poll and its results should not be extrapolated beyond those whodid accept our invitation.

1.For all of 2013 and for all of 2014 (and only in 2014), what isthe total amount of additional asset purchases the Federal

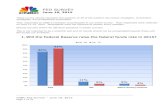

Reserve will have made?

$858.8$917.0 $936.6

$883.6$921.9 $941.9

$948.5

$370.6 $367.1 $373.5 $374.8 $381.9

$0

$200

$400

$600

$800

$1,000

$1,200

1/29/2013 3/19/2013 4/30/2013 6/18/2013 7/30/2013 9/6/2013 9/17/2013

Billions

2013 2014

-

7/29/2019 CNBC Fed Survey, September 17, 2013

2/36

CNBC Fed Survey September 17, 2013Page 2 of 36

FED SURVEYSeptember 17, 2013

3.In what month do you expect the Fed to begin tapering itspurchases?

0%

10%

20%

30%

40%

50%

60%

June 18 July 30 Sept 6 Sept 17

Averages

Jan 29: Dec 2013

March 19: Jan 2014

April 30: Feb 2014

June 18: Dec 2013

July 30: November 2013

Sep 6: November 2013

Sept 17: November 2013

48% selected September 2013 and76% said tapering would begin in

September or October 2013

-

7/29/2019 CNBC Fed Survey, September 17, 2013

3/36

CNBC Fed Survey September 17, 2013Page 3 of 36

FED SURVEYSeptember 17, 2013

4.By how much do you believe the Fed will reduce its assetpurchases in that first month?

$22.1

$19.2

$12.6

$14.5

$0

$5

$10

$15

$20

$25

July 5 July 30 Sept 6 Sept 17

Billions

On average, respondents

believe the Fed willmaintain its new level ofasset purchases for 3.63months.

-

7/29/2019 CNBC Fed Survey, September 17, 2013

4/36

CNBC Fed Survey September 17, 2013Page 4 of 36

FED SURVEYSeptember 17, 2013

6.What mix of Treasuries vs. mortgage-backed securities do yoexpect in the Federal Reserve's taper?

Treasuries72%

MBS28%

-

7/29/2019 CNBC Fed Survey, September 17, 2013

5/36

CNBC Fed Survey September 17, 2013Page 5 of 36

FED SURVEYSeptember 17, 2013

7.When do you expect the Federal Reserve will completely stoppurchasing assets?

0%

5%

10%

15%

20%

25%

30%

June 18 July 30 Sept 6 Sept 17

Averages

Jan 29: Nov 2013

Mar 19: May 2014

Apr 30: July 2014Jun 18: July 2014

July 30: August 2014

Sept 6: August 2014

Sept 17: August 2014

-

7/29/2019 CNBC Fed Survey, September 17, 2013

6/36

CNBC Fed Survey September 17, 2013Page 6 of 36

FED SURVEYSeptember 17, 2013

8.Based on your expectations for tapering, what percentage ofthe ultimate impact on each market is already discounted inthe overall prices of that market?

66%

58%

68%

81%

73%

82%81%

70%

81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Treasuries Equities Mortgages

July 30 Sept 6 Sept 17

-

7/29/2019 CNBC Fed Survey, September 17, 2013

7/36

CNBC Fed Survey September 17, 2013Page 7 of 36

FED SURVEYSeptember 17, 2013

9.Do you believe the U.S. SHOULD/WILL launch a military attacon Syria?

16%

65%

19%

9%

67%

23%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Yes No Don't know/unsure

Should Will

-

7/29/2019 CNBC Fed Survey, September 17, 2013

8/36

CNBC Fed Survey September 17, 2013Page 8 of 36

FED SURVEYSeptember 17, 2013

10.What would be the short-term impact on equities if the U.S.does launch a military attack on Syria?

0%

5%

10%

15%

20%

25%

30%

35%

40%

-20% -16% -12% -8% -4% 0% +4% +8% +12% +16% +20%

Average:

-4.8%

-

7/29/2019 CNBC Fed Survey, September 17, 2013

9/36

CNBC Fed Survey September 17, 2013Page 9 of 36

FED SURVEYSeptember 17, 2013

11.Who will President Obama nominate as the next Fedchairman? Sept 12-13 represents responses before Summers withdrew fromconsideration. Sept 16 responses are from a separate survey after Summers withdrew

0%

0%

2%

0%

2%

20%

72%

4%

0%

2%

2%

0%

0%

58%

30%

7%

0%

2%

6%

0%

2%

88%

2%

0% 20% 40% 60% 80% 100%

Ben BERNANKE

Martin FELDSTEIN

Roger FERGUSON

Glenn HUBBARD

Don KOHN

Alan KRUEGER

Christine ROMER

Larry SUMMERS

John TAYLOR

Paul VOLCKER

Janet YELLEN

Don'tknow/unsure

July 30 Sept 12-13 (before) Sept 16 (after)

-

7/29/2019 CNBC Fed Survey, September 17, 2013

10/36

CNBC Fed Survey September 17, 2013Page 10 of 36

FED SURVEYSeptember 17, 2013

Who should President Obama nominate as the next Fed

chairman?

10%

2%

6%

8%

2%

2%

6%

10%

2%

44%

4%

2%

2%

5%

2%

2%

0%

0%

12%

16%

56%

0%

0% 10% 20% 30% 40% 50% 60%

Ben BERNANKE

Martin FELDSTEIN

Roger FERGUSON

Glenn HUBBARD

Don KOHN

Alan KRUEGER

Christine ROMER

Larry SUMMERS

John TAYLOR

Paul VOLCKER

Janet YELLEN

Don'tknow/unsure

July 30 Sept 17

-

7/29/2019 CNBC Fed Survey, September 17, 2013

11/36

CNBC Fed Survey September 17, 2013Page 11 of 36

FED SURVEYSeptember 17, 2013

7.Compared to Ben Bernanke, the next Fed chairman will be:

2%

26%

52%

14%

2%4%

2%

17%

43%

30%

0%

7%

0%

10%

20%

30%

40%

50%

60%

Much more

dovish

Somewhat

more dovish

No different Somewhat

more

hawkish

Much more

hawkish

Don't

know/unsure

July 30 Sept 17

-

7/29/2019 CNBC Fed Survey, September 17, 2013

12/36

CNBC Fed Survey September 17, 2013Page 12 of 36

FED SURVEYSeptember 17, 2013

8.Please rate the following four candidates for the Fedchairmans job on the listed qualities. (On a scale of 1 to 5,where a higher number means a higher rating.)

Numbers in parentheses to the right of the qualities represent how essential they are to the job of Fe

chairman on a scale of 1 (least) to 5 (most), as ranked in the July 30 survey.

4.63

4.37

3.71

4.16

3.34

3.61

4.42

4.16

3.61

3.89

4.21

3.56

3.17

3.74

3.45

3.55

3.45

3.59

3.03

3.67

3.08

3.61

2.63

3.53

3.63

3.55

3.71

3.46

2.76

3.16

4.61

3.71

3.58

3.68

3.05

3.39

3.95

4.63

3.24

3.51

2.00 2.50 3.00 3.50 4.00 4.50 5.0

Monetary policy expertise (4.52)

Ability to manage a financial crisis (4.30)

Good communication skills (4.22)

Respect from financial markets (4.18)

Concern about inflation (4.08)

Financial market expertise (4.04)

Respect from international financial leaders (3.41)

Concern about unemployment (3.39)

Good political skills (3.27)

Banking regulatory expertise (2.94)

Bernanke Kohn Summers Yellen

-

7/29/2019 CNBC Fed Survey, September 17, 2013

13/36

CNBC Fed Survey September 17, 2013Page 13 of 36

FED SURVEYSeptember 17, 2013

Sum of candidate ratings weighted by essentialness of each quality.

0

20

40

60

80

100

120

140

160

180

Summers Yellen Bernanke Kohn

Banking regulatory expertise (2.94)

Good political skills (3.27)

Concern about unemployment (3.39)

Respect from international financial

leaders (3.41)

Financial market expertise (4.04)

Concern about inflation (4.08)

Respect from financial markets (4.18)

Good communication skills (4.22)

Ability to manage a financial crisis

(4.30)

Monetary policy expertise (4.52)

-

7/29/2019 CNBC Fed Survey, September 17, 2013

14/36

CNBC Fed Survey September 17, 2013Page 14 of 36

FED SURVEYSeptember 17, 2013

9.What grade would you give Fed Chairman Ben Bernanke?

Numerical average based on A=4, B=3, C=2, D=1, F=0

26%

42%

22%

5%

5%

22%

48%

19%

5%

3%

4%

23%

48%

13%

9%

0%

7%

30%

48%

18%

2%

2%

0%

0% 10% 20% 30% 40% 50% 60%

A

B

C

D

F

Don't know/unsure

Dec 22, 2010 July 21, 2011 Jan 23, 2012 Sept 17, 2013

Average forSept 17 survey:

B (3.00)

-

7/29/2019 CNBC Fed Survey, September 17, 2013

15/36

CNBC Fed Survey September 17, 2013Page 15 of 36

FED SURVEYSeptember 17, 2013

Comments on this question:

Marshall Acuff, Cary Street Partners: (C) Over communicated.

Robert Brusca, Fact and Opinion Economics: (B) Great for in-crisis managementlesser grade for afterward.

John Donaldson, Haverford Trust Co.: (A) His knowledge of the Depressionultimately prevented another one.

Stuart Hoffman, PNC: (A) The right chairman at the right time for the rightmonetary policy strategy.

Hugh Johnson, Hugh Johnson Advisors: (A) Largely because of his understandinof financial and economic history, particularly his understanding of the 1930s,Bernanke has been fortunately an excellent chairman. The next chair needs to beequally familiar with financial market history to be effective.

John Kattar, Ardent Asset Advisors: (B) Good handling of financial crisis, but ZIRand QE went on too long.

Barry Knapp, Barclays PLC: Crisis policies and creativity should create a very

favorable legacy. The non-crisis QE period will be criticized by left-leaning intelligentsand neo-classical economists alike.

Subodh Kumar, Subodh Kumar & Associates: (C) Over entire term one mustconsider missing the buildup to the crisis and the controversial 2011/12 expansion ofQE as well as the laudable initiation of QE response in first phase.

Guy LeBas, Janney Montgomery Scott: (A) Although the long term implications oaggressive monetary expansion aren't clear, Bernanke has done an excellent job inpreventing financial Armageddon.

Donald Luskin, Trend Macrolytics: (B) Good man in a storm. In the aftermath, noso much.

Ward McCarthy, Jefferies: (B)He, like Treasury, the White House, Congress andother regulators, was among those who failed to anticipate the crisis. His performansince the crisis has been extraordinary.

-

7/29/2019 CNBC Fed Survey, September 17, 2013

16/36

CNBC Fed Survey September 17, 2013Page 16 of 36

FED SURVEYSeptember 17, 2013

Larry McMillan, McMillan Analysis: (D) This will be his grade in retrospect when tfull effect of his policies becomes known.

Lynn Reaser, Point Loma Nazarene University: (B) Chairman Bernanke handledthe financial crisis with great expertise. His grade on the Fed's exit strategy is still"incomplete."

John Roberts, Hilliard Lyons: (B) Would probably offer a B+.

John Ryding, RDQ Economics: (C) He gets an A for the handling of the crisis but aD otherwise.

Hank Smith, Haverford Investments: (A) For all of the Bernanke critics: what wathe alternative??

Stephen Stanley, Pierpont Securities: (B) High marks for navigating the crisis.Dismal performance since then.

Diane Swonk, Mesirow Financial: (A) It was serendipity that an expert on financiacrises got the job; he deserves credit for saving the credit markets from themselves.

.

-

7/29/2019 CNBC Fed Survey, September 17, 2013

17/36

CNBC Fed Survey September 17, 2013Page 17 of 36

FED SURVEYSeptember 17, 2013

10.Since September 2012, market functioning in the governmenbond market has:

2%

8%

4%

19%

11%12%

17%

20%

60%

65%

47%46%

42%

15%

15%

29%

25%27%

2% 2% 2%2%

0%

10%

20%

30%

40%

50%

60%

70%

March 19 April 30 June 18 July 30 Sept 17

Worsened somewhat

Improved somewhat

Improved a lot

Sta ed the same

Worsened a lot

-

7/29/2019 CNBC Fed Survey, September 17, 2013

18/36

CNBC Fed Survey September 17, 2013Page 18 of 36

FED SURVEYSeptember 17, 2013

Since September 2012, market liquidity in the government

bond market has:

4%5%

6%4%

29%

17%

21%

30%

20%

48%

52%

41%

28%

40%

15%

17%19%

20%

29%

4%

2%

5%

8%

4%

0%

10%

20%

30%

40%

50%

60%

March 19 April 30 June 18 July 30 Sept 17

Stayed the same

Improved somewhat

Worsened a lotIm roved a lot

Worsened somewhat

-

7/29/2019 CNBC Fed Survey, September 17, 2013

19/36

CNBC Fed Survey September 17, 2013Page 19 of 36

FED SURVEYSeptember 17, 2013

11.Since September 2012, market functioning in the mortgage-backed security market market has:

4%

2%

5%4% 5%

31%

22%

21%

31%

23%

29%

39%

21%

31%

41%

20% 20%

32%

20%18%

2%

4%5%

6%

5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

March 19 April 30 June 18 July 30 Sept 17

Stayed the same

Worsened a lot

Improved a lot

Worsened somewhat

Improved somewhat

-

7/29/2019 CNBC Fed Survey, September 17, 2013

20/36

CNBC Fed Survey September 17, 2013Page 20 of 36

FED SURVEYSeptember 17, 2013

Since September 2012, market liquidity in the mortgage-

backed security market market has:

4%

2%

7%

6%7%

21%

28%

25%

30%

18%

40%

28%

18%

28%

34%

19%

22%

30%

20%

25%

7%

5%

8%7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

March 19 April 30 June 18 July 30 Sept 17

Worsened somewhat

Improved a lot

Worsened a lot

Improvedsomewhat

Stayed the same

-

7/29/2019 CNBC Fed Survey, September 17, 2013

21/36

CNBC Fed Survey September 17, 2013Page 21 of 36

FED SURVEYSeptember 17, 2013

12.Compared with the debate at the beginning of the year, thenext round of discussions to raise the debt ceiling will be:

19%

44%

35%

2%

24%

49%

27%

0%0%

10%

20%

30%

40%

50%

60%

More contentious About the same Less contentious Don't know/unsure

July 30 Sept 17

-

7/29/2019 CNBC Fed Survey, September 17, 2013

22/36

CNBC Fed Survey September 17, 2013Page 22 of 36

FED SURVEYSeptember 17, 2013

What is the probability that the United States fails to raise the

debt ceiling in the coming months and defaults on at least someof its payments?

0%

10%

20%

30%

40%

50%

60%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Percentage

ofrespondents

Default probability

July 30 Sept 17

AveragesJuly 30: 6.6%Sept 17: 8.4%

-

7/29/2019 CNBC Fed Survey, September 17, 2013

23/36

CNBC Fed Survey September 17, 2013Page 23 of 36

FED SURVEYSeptember 17, 2013

13.When it comes to the budget deficit, the United States:

80%

67%

52%

40% 40%

50%

16%

25%

39%

44%

52%

41%

4% 4%9%

12%

8% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

January 29 March 19 April 30 June 18 July 30 Sept 17

Should urgently enact a plan that puts it on a path toward a sustainablebudget deficit

Has at least a couple of years before it must enact such a plan

Does not need to enact a plan that puts it on a path toward a sustainablbudget deficit

Don't know/unsure

-

7/29/2019 CNBC Fed Survey, September 17, 2013

24/36

CNBC Fed Survey September 17, 2013Page 24 of 36

FED SURVEYSeptember 17, 2013

14.Where do you expect the S&P 500 stock index will be on ?

1547

1589

1612

1655

1691

1654

1685

1723

1751

1709

1752

1,400

1,450

1,500

1,550

1,600

1,650

1,700

1,750

1,800

Jan 29

2013

March 19 April 30 June 18 July 30 Sept 6 Sept 30

Survey Dates

December 31, 2013 June 30, 2014

-

7/29/2019 CNBC Fed Survey, September 17, 2013

25/36

CNBC Fed Survey September 17, 2013Page 25 of 36

FED SURVEYSeptember 17, 2013

15.What do you expect the yield on the 10-year Treasury notewill be on ?

2.31% 2.35%

2.10%

2.41%

2.73%

3.00% 3.02%

2.80%

3.10%

3.33%3.39%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan 29

2013

March 19 April 30 June 18 July 30 Sept 6 Sept 30

Survey Dates

December 31, 2013 June 30, 2014

-

7/29/2019 CNBC Fed Survey, September 17, 2013

26/36

CNBC Fed Survey September 17, 2013Page 26 of 36

FED SURVEYSeptember 17, 2013

16.What is your forecast for the year-over-year percentagechange in real U.S. GDP for ?

+2.6%

+2.7%

+2.6%

+2.3%

+2.2%

+1.9%

+2.1%+2.1%+2.1%+2.1%

+1.9%

+2.0%

+2.6%+2.6%+2.6%

+2.6%+2.5%

+2.6%

1.0%

1.5%

2.0%

2.5%

3.0%

Survey Dates

2013 2014

-

7/29/2019 CNBC Fed Survey, September 17, 2013

27/36

CNBC Fed Survey September 17, 2013Page 27 of 36

FED SURVEYSeptember 17, 2013

17.When do you think the FOMC will first increase the fed fundsrate?

Increase fed funds rate

(Average response)

Survey Date

Dec

11,

2012

Jan

29,

2013

Mar

19,

2013

Apr

30,

2013

Jun

18,

2013

Jul

30,

2013

Sept

6,

2013

Sept

17,

2013

2013 Q2

Q3

Q4

2014 Q1

Q2

Q3

Q4

2015 Q12015

Q12015

Q12015

Q1

Q22015

Q22015

Q22015

Q2

Q32015

Q32015

Q3

Q4

2016 Q1

Q2

Q3

Q4

2017 or later

-

7/29/2019 CNBC Fed Survey, September 17, 2013

28/36

CNBC Fed Survey September 17, 2013Page 28 of 36

FED SURVEYSeptember 17, 2013

Currently, Fed policy is not to raise interest rates until the

unemployment rate is at least 6.5%. Will the Fed change thatguidance?

30%

60%

10%

44%

51%

4%

0%

10%

20%

30%

40%

50%

60%

70%

Yes No Don't know/unsure

July 30 Sept 17

-

7/29/2019 CNBC Fed Survey, September 17, 2013

29/36

CNBC Fed Survey September 17, 2013Page 29 of 36

FED SURVEYSeptember 17, 2013

If the Fed does change its guidance, what will be the new

threshold?

2%

32%

11%

52%

2%3%

49%

5%

43%

0%0%

10%

20%

30%

40%

50%

60%

Thresholds

July 30 Sept 17

Averages for thoseanswering with a

numberJuly 30: 6.23%Sept 17: 6.07%

-

7/29/2019 CNBC Fed Survey, September 17, 2013

30/36

CNBC Fed Survey September 17, 2013Page 30 of 36

FED SURVEYSeptember 17, 2013

24.Where do you expect the fed funds target rate will be on ?

0.33%

0.27%

0.21%0.17%

0.19%0.19%0.16%0.15%

0.13%0.13%

0.20%0.18%

0.16%0.14%

0.28%

0.21%

0.97%

0.92%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Jul 31 Sep 12Dec 11Jan 292013

Mar19

Apr 30Jun 18 Jul 30 Sept 6 Sept17

Survey Dates

Dec 31, 2013 June 30, 2014 Dec 31, 2014 Dec 31, 2015

-

7/29/2019 CNBC Fed Survey, September 17, 2013

31/36

CNBC Fed Survey September 17, 2013Page 31 of 36

FED SURVEYSeptember 17, 2013

25.In the next 12 months, what percent probability do you placeon the U.S. entering recession? (0%=No chance of recession,100%=Certainty of recession)

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

15.2%

16.2%

16.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Survey Dates

-

7/29/2019 CNBC Fed Survey, September 17, 2013

32/36

CNBC Fed Survey September 17, 2013Page 32 of 36

FED SURVEYSeptember 17, 2013

26.What is the single biggest threat facing the U.S. economicrecovery?

Other responses: Toss up: tax and regulations vs. deflation Low capex Low wage growth and household

deleveraging

20%

31%

20%

2%

0%

2%

2%

2%

9%

11%

0%

15%

28%

20%

2%

3%

3%

0%

2%

13%

13%

0%

8%

30%

22%

4%

0%

2%

2%

0%

4%

10%

14%

4%

4%

0% 5% 10% 15% 20% 25% 30% 3

European recession/financial crisis

Tax/regulatory policies

Slow job growth

High gasoline prices

Overall inflation

Deflation

Debt ceiling

Too little budget deficit reduction

Too much budget deficit reduction

Rise in interest rates

Other

Don't know/unsure

April 30 Jun 18 Jul 30 Sept 17

-

7/29/2019 CNBC Fed Survey, September 17, 2013

33/36

CNBC Fed Survey July 30, 2013Page 33 of 36

FED SURVEYSeptember 17, 2013

27.What is your primary area of interest?

Comments:

Marshall Acuff, Cary Street Partners: Unless political leadership

improves, valuations of U.S. equities are not likely to sustain anysignificant increase from current levels.

Robert Brusca, Fact and Opinion Economics: Fiscal policy = 0.Monetary policy is disoriented. The economy is growing butsputtering. The president thinks he makes things better by givingspeeches. U.S. foreign policy is now a tangled mess. There is nothingsolid investors can be sure of (apart from death and even MOREtaxes). You can taste the entropy and feel the concern for the

future. It's a good thing we have discovered so much oil/energy athome now if we could only agree to develop it. Or maybe just havethe president give a speech about it...

Tony Crescenzi, PIMCO: There has been a gigantic switcheroo inpositioning in the bond market, with non-commercial traders in

Economics

50%

Equities18%

Fixed Income

16%

Currencies0%

Other16%

-

7/29/2019 CNBC Fed Survey, September 17, 2013

34/36

CNBC Fed Survey July 30, 2013Page 34 of 36

FED SURVEYSeptember 17, 2013

eurodollar futures shifting by 1 million contracts from long to shortsince May to price in Fed rate hikes as early as next year. With rate

hikes priced in, interest rate volatility should simmer downsomewhat, save for further technical reverberations.

John Donaldson, Haverford Trust Co.: If the bond market canabsorb the Verizon deal and have good Treasury auctions this week,it can certainly handle a little tapering.

Mike Dueker, Russell Investments: Fed decisions about thetiming and pace of tapering will not have a great effect on the overall

size of the balance sheet that the Fed carries into the second half of2014 and 2015. Unfortunately the Fed has put itself in a box whereevery decision is supposed to be viewed as important. Theimportant thing, which does not depend much on the shape oftapering, is that the Fed will carry a very accommodative balancesheet until the first rate hike, probably in 2015Q3.

Stuart Hoffman, PNC: The "taper worm" will not cause theeconomy much indigestion. It will increase market function/signal in

the Treasury and MBS markets.

John Kattar, Ardent Asset Advisors: The Fed has done a verygood job of preparing the markets for taper, and the markets(especially stocks) have discounted this well. It is likely that stocksin particular would react positively to a taper of $10 billion or less.

Subodh Kumar, Subodh Kumar & Associates: Markets appear tobe shifting to fundamentals as central bank dominance on long fixed

income fades. Central banks and the Federal Reserve in particularneed to explicitly acknowledge collateral damage from QE on crucialcapital market health issues like impact on savers and on hot moneyflows to emerging economies as well as being less compliant onpolitical procrastination on deficit reduction. Market volatility issuesremain elevated. Quality favored as investment theme.

-

7/29/2019 CNBC Fed Survey, September 17, 2013

35/36

CNBC Fed Survey July 30, 2013Page 35 of 36

FED SURVEYSeptember 17, 2013

William Larkin, Cabot Money Management: The risks in the bondmarket are elevated because many bond investors arent aware of

the true potential dangers of the current monetary policyexperiment.

Guy LeBas, Janney Montgomery Scott: The taper is hands downthe single most clearly telegraphed move in the history of monetarypolicy. We first started talking about it in the Jan. FOMC minutes,and there's been a slow progression ever since. We also know thatthe Fed wants to be buying $0 in bonds by mid-2014. Whether thereductions start in September of November doesn't matter. There's

a starting point ($85 billion), and ending point ($0 billion), and atimeframe that's already been set.

Ward McCarthy, Jefferies: It would be more logical for the FOMCto implement tapering later this year and coordinate the taperingwith a change in rate guidance. The market has already done quitea bit of tightening for the Fed at a time when disinflation is stillongoing.

Rob Morgan, Fulcrum Securities: Fed Chair Bernanke said thattapering will begin sometime this year if economic data holds up.Weekly initial jobless claims are near six-year lows and existinghome sales are near three-year highs. What's not to like?

Joel Naroff, Naroff Economic Advisors: Starting the tapering isnot being based on economic growth, which is still not strong enoughfor the Fed to declare victory. Instead, concerns about marketdamage and inflation are driving the decision making, which makes

determining the starting point and speed of the tapering difficult.

James Paulsen, Wells Capital Management: Annual wageinflation is now 2.2%. In the next few months, if wage inflation risesmuch higher as the unemployment rate nears 7%, the discussionwithin and surrounding the Fed may change from a primary focus on

-

7/29/2019 CNBC Fed Survey, September 17, 2013

36/36

FED SURVEYSeptember 17, 2013

the job market to an increasing focus about inflation risk.Remember, the 1970s proved inflation can rise from high

unemployment rates and this fear would be heightened should wageinflation rise above 2.5 percent while the U.S. dollar was weak andcommodity prices were rising.

Lynn Reaser, Point Loma Nazarene University: Monetary policyis at a point of only bad choices. Tapering now could choke offeconomic growth through the housing, stock market, and emergingmarket economic channels. Failure to begin to scale back assetpurchases will only delay the inevitable and give a brief period of

respite without setting the economy on a fundamentally strongertrack.

John Roberts, Hilliard Lyons: Our major worry is whether risingrates, should they continue over the near term, derail the currentmeager level of growth. The answer is up in the air with theuncertainty of interest rate increases in the near term from thecurrent higher plateau. However, should we see meaningfulincreases from here, we believe the likelihood of growth slowing is

very high.

Allen Sinai, Decision Economics: Finally, the U.S. economy isshowing more signs of a normal business cycle expansion.

Hank Smith, Haverford Investments: When is the Fed going tobecome more vocal about the need for better pro-growth fiscalpolicy? Better fiscal policy is the key for the Fed moving to a moreneutral monetary policy.

Diane Swonk, Mesirow Financial: Markets need to get used to theidea that QE3 is not QE infinity.