CMP 700 FY19E PE 18 - Powerchats.moneycontrol.com/plus/upload_pdf_file/ManpasandBeverages_P… ·...

17

Manpasand Beverages BUY - 1 - Monday, 25 th July, 2016 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. STOCK POINTER Target Price ` 1099 CMP ` 700 FY19E PE 18.4X Index Details Despite the recent surge in the stock price of Manpasand (a fruit drink manufacturing company), we still believe that there is considerable potential for upside movement. We initiate coverage on Manpasand as a BUY with a price objective of Rs 1,099, representing a potential upside of 57% from the CMP of Rs 700 over the next 24 months. Manpasand under its flagship brand Mango Sip has grown by leaps and bounds and today commands a 3% market share which, is slated to double by 2020. It has also recently forayed into the premium fruit drink (with pulp content of 16–17%) segment, with its brand Fruits Up, which has also shown promises of becoming a power brand. It is also foraying into a virgin product category of packaged coconut water through its brand Coco Sip. And going by its track record of successful delivery, we are quite upbeat on the prospects of this venture. We expect the brands to deliver a strong revenue growth of 40.3% CAGR to Rs 1,539 crore by FY19 with earnings growing at a CAGR of 55.5% to Rs 190.2 crore over the same period. Currently the stock is valued at 12X FY19 Cash EPS of Rs 57.7 Considering the peer-set median cash PE of 23.8 and the fledgling nature of the company we have given a discount of 20% to this median multiple to arrive at a value of Rs 1,099 per share. Our optimism stems from the following The Indian fruit juice market has grown at a CAGR of 26.3% in value terms to Rs 132 bn in FY15 and we expect this growth trajectory to continue to Rs 417 bn by 2020. Manpasand is expected to improve its market share from 3% in 2015 to 6% in 2019 in the juice drink segment which comprises over 72% of the fruit juice market. Over the period FY12-16, Manpasand has grown at a blistering 60% CAGR to Rs 557 cr mainly on the back of its flagship product Mango Sip (Mango juice). Going forth we expect the brisk pace of growth to be sustained, albeit at a slightly lower CAGR of 40.3% to Rs 1,539 cr by FY19. Sensex 27,808 Nifty 8,541 Industry Beverages Scrip Details MktCap (` cr) 3,499 BVPS (`) 120.1 O/s Shares (Cr) 5.0 AvVol 45,374 52 Week H/L 725.5/348 Div Yield (%) 0.1 FVPS (`) 10.0 Shareholding Pattern Shareholders % Promoters 50.4 Public 49.6 Total 100.0 Manpasand vs. Sensex 100 200 300 400 500 600 700 800 15000 17000 19000 21000 23000 25000 27000 29000 31000 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 SENSEX MANPASAND Key Financials (` in Cr) Y/E Mar Net Sales EBITDA PAT EPS (`) EPS Growth (%) RONW (%) ROCE (%) P/E (x) EV/EBITDA (x) 2016 556.7 110.4 50.6 10.1 68.8 13.7 12.8 69.3 30.9 2017E 811.0 154.9 68.1 13.6 34.6 12.2 10.8 51.5 22.1 2018E 1,141.8 224.9 116.2 23.2 70.8 18.5 16.4 30.1 15.2 2019E 1,538.5 306.2 190.2 38.0 63.6 25.3 22.5 18.4 11.2

Transcript of CMP 700 FY19E PE 18 - Powerchats.moneycontrol.com/plus/upload_pdf_file/ManpasandBeverages_P… ·...

Manpasand Beverages BUY

- 1 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

ST

OC

K P

OIN

TE

R

Target Price ` 1099 CMP ` 700 FY19E PE 18.4X

Index Details Despite the recent surge in the stock price of Manpasand (a fruit drink

manufacturing company), we still believe that there is considerable

potential for upside movement. We initiate coverage on Manpasand as

a BUY with a price objective of Rs 1,099, representing a potential

upside of 57% from the CMP of Rs 700 over the next 24 months.

Manpasand under its flagship brand Mango Sip has grown by leaps and

bounds and today commands a 3% market share which, is slated to

double by 2020. It has also recently forayed into the premium fruit drink

(with pulp content of 16–17%) segment, with its brand Fruits Up, which

has also shown promises of becoming a power brand. It is also

foraying into a virgin product category of packaged coconut water

through its brand Coco Sip. And going by its track record of successful

delivery, we are quite upbeat on the prospects of this venture.

We expect the brands to deliver a strong revenue growth of 40.3%

CAGR to Rs 1,539 crore by FY19 with earnings growing at a CAGR of

55.5% to Rs 190.2 crore over the same period. Currently the stock is

valued at 12X FY19 Cash EPS of Rs 57.7 Considering the peer-set

median cash PE of 23.8 and the fledgling nature of the company we

have given a discount of 20% to this median multiple to arrive at a

value of Rs 1,099 per share.

Our optimism stems from the following

The Indian fruit juice market has grown at a CAGR of 26.3% in

value terms to Rs 132 bn in FY15 and we expect this growth

trajectory to continue to Rs 417 bn by 2020. Manpasand is

expected to improve its market share from 3% in 2015 to 6% in

2019 in the juice drink segment which comprises over 72% of

the fruit juice market.

Over the period FY12-16, Manpasand has grown at a blistering

60% CAGR to Rs 557 cr mainly on the back of its flagship

product Mango Sip (Mango juice). Going forth we expect the

brisk pace of growth to be sustained, albeit at a slightly lower

CAGR of 40.3% to Rs 1,539 cr by FY19.

Sensex 27,808

Nifty 8,541

Industry Beverages

Scrip Details

MktCap (` cr) 3,499

BVPS (`) 120.1

O/s Shares (Cr) 5.0

AvVol 45,374

52 Week H/L 725.5/348

Div Yield (%) 0.1

FVPS (`) 10.0

Shareholding Pattern

Shareholders %

Promoters 50.4

Public 49.6

Total 100.0

Manpasand vs. Sensex

100

200

300

400

500

600

700

800

15000

17000

19000

21000

23000

25000

27000

29000

31000

Ju

l-15

Au

g-1

5

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Ju

n-1

6

Ju

l-16

SENSEX MANPASAND

Key Financials (` in Cr)

Y/E Mar Net

Sales EBITDA PAT

EPS

(`)

EPS

Growth (%)

RONW

(%)

ROCE

(%)

P/E

(x)

EV/EBITDA

(x)

2016 556.7 110.4 50.6 10.1 68.8 13.7 12.8 69.3 30.9 2017E 811.0 154.9 68.1 13.6 34.6 12.2 10.8 51.5 22.1 2018E 1,141.8 224.9 116.2 23.2 70.8 18.5 16.4 30.1 15.2 2019E 1,538.5 306.2 190.2 38.0 63.6 25.3 22.5 18.4 11.2

- 2 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Strategically expanding its capacities by 80% over FY16-18 (capex

of Rs3.2b) into north and south India will not only address the

supply side issues but also help to reduce the logistics cost and

improve the working capital cycle going forward.

Manpasand has expanded its product basket by introducing Fruits

Up in FY15 which in no time achieved great success for

Manpasand clocking a turnover of Rs ~110 cr (FY16) in just 2 years

post launch, that too without an aggressive marketing campaign.

Fruits up being a premium category drink was launched in the

urban centres and will gradually move to rural markets (reverse

strategy of that endeared with Mango Sip).

Manpasand sensing revenue potential in the coconut water

segment launched Coco Sip a packaged coconut water drink

primarily targeted at north and northeast markets. Coco Sip will be

the first of its kind natural coconut water without any preservatives

in it. The product will be available across SKU sizes at affordable

prices starting Rs 10 and will be manufactured through an

outsourcing model.

- 3 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Company Background

Manpasand is a fruit drink manufacturing company with a primary focus on

mango, which is the leading flavour for juice drinks in India. A Mango based

fruit drink, ‘Mango Sip’, is the company’s flagship brand, which is strategically

focused towards customers primarily based in semi urban and rural markets.

With a view to expand the product portfolio, Manpasand has launched two

new brands, ‘Fruits Up’ and ‘Manpasand ORS’. Under the ‘Fruits Up’ brand, It

offers fruit drinks and carbonated fruit drinks in different flavours, and under

the ‘Manpasand ORS’ brand, it offer fruit drinks with energy replenishing

qualities with a primary focus on North East India.

Key brands of Manpasand

Source: Manpasand, Ventura Research

- 4 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Key Investment Highlights

Over the period FY12-16, Manpasand has grown at a blistering 60% CAGR to

557 cr mainly on the back of its flagship product Mango Sip (Mango juice).

Going forth we expect the brisk pace of growth to be sustained, albeit at a

slightly lower CAGR of 40.3% to Rs 1,539 cr by FY19 driven by-

a) Improving market share in the booming fruit juice market (Rs 132bn).

b) Expansion in the product portfolio to desrisk dependence on a single

product

c) Flagship product Mango Sip experiencing significant pan India brand recall

d) Strategic expansion to increase capacity by ~80% from 1.25 lac cases per

day to 2.25 lac cases per day over FY16-19 without impacting the debt free

status

Improving market share in the booming fruit juice market (Rs

132bn).

The Indian fruit juice market has grown at a CAGR of 26.3% in value terms to

Rs 132 bn in FY15 and we expect this growth trajectory to continue to Rs 417

bn by 2020.

Juice drink-dominant segment of the fruit juice market…

The fruit juice market is primarily dominated by juice drinks which constitute

~72% (RS 95.4 bn) of the overall fruit juice market. This market which has

enjoyed similar growth as the overall fruit juice market is expected to outpace

the industry’s growth (CAGR of 28% to 327.4bn in 2020). Manpasand which

operates in this segment is best placed to benefit from this growth.

Manpasand is present

in this segment

- 5 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Manpasand forayed into the juice drink market in 1997 with the launch of

Mango Sip. Today Mango Sip is a well renowned brand growing at a

whopping CAGR of 51% to Rs 449 cr over the period FY12-16.While its

market share in FY 15 stood at 3.2%, we estimate this to nearly double to 6%

by 2020 on the back of

higher brand recall,

availability of the product across maximum SKUs of tetra and PET packs

Fruit juice market in India

Segment Measure 2010 2011 2012 2013 2014 2015 2020

CAGR

(2010-15)

CAGR

(2015-20)

100% Juice Volume 30.4 39.6 51.0 63.1 77.0 93.3 224.7 25.1% 19.2%

Value 3.1 4.1 5.5 7.2 9.4 12.0 38.1 31.3% 26.1%

Nectar Volume 96.9 122.2 153.0 189.9 208.5 229.6 389.8 18.8% 11.2%

Value 8.0 10.4 13.6 17.8 20.8 24.2 51.9 24.8% 16.5%

Juice drink Volume 550.4 678.4 830.5 1,010.0 1,220.2 1,478.8 4,151.1 21.9% 22.9%

Value 29.9 37.2 47.0 59.3 75.0 95.4 327.3 26.1% 28.0%

Total Value 41.0 51.7 66.1 84.2 105.1 131.5 417.3 21.6% 26.0%

Source:Euromonitor 2015, Ventura Research (volume in mn litres, value in RS bn)

Juice drink accounts for 82% volume

5.2%

12.7%

82.1%

100% Juice Nectar Juice drink

Source: Euromonitor 2015, Ventura Research

Juice drink accounts for 72% value

9.1%

18.4%

72.5%

100% Juice Nectar Juice drink

Source: Euromonitor 2015, Ventura Research

- 6 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

differentiated strategy of being a tier II and tier III player and having a

strong rural presence (55% of sales) viz a viz its larger competitors

Maaza and Slice which are more urban centric

direct empanellement with IRCTC (20% of the total revenues) which

provides a wider consumer space and multifolds its brand awareness as

its products are displayed across railway stations

On the back of the above we expect revenues from Mango Sip to clock a brisk

CAGR of 36% to Rs 1,127 cr over FY16-19.

Mango Sip available across maximum SKUs of tetra and PET packs

Source: Manpasand, Ventura Research

Mango-Sip’s share in the juice market to double in 4 years

22.3

15.3

13.6

12.1

8.9

3.2

24.6

Maaza Slice Réal Frooti Tropicana Mango-Sip Others

We expect this to double by 2020

Source: Manpasand, Ventura Research

- 7 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Expansion in product portfolio to derisk dependence on single

product

Emboldened by the success of Mango-Sip, Manpasand embarked on a

journey of adding new product categories. It launched its new brand Fruits Up,

a premium fruit drink with pulp content of 16–17% in multiple flavors (both in

the Carbonated and non-Carbonated variety) in FY15.

Mango Sip to grow at a brisk rate

85.7

234.5 285.0 306.9

448.7

628.2

866.9

1,127.0

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Revenue from Mango Sip

` in cr

Source: Manpasand, Ventura Research

Multi flavor offering in Fruits Up

Source: Manpasand, Ventura Research

- 8 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Fruits Up has been a huge success for Manpasand clocking a turnover of Rs

~110 cr (FY16) in just 2 years post launch, that too without an aggressive

marketing campaign. Fruits up being a premium category drink was launched

in the urban centres and will gradually move to rural markets (reverse strategy

of that endeared with Mango Sip).

Fruits up to grow at the expense of flavored based drinks…

Concerns associated with colas and other flavored non fruit beverages has

seen a steady shift in consumer preferences to natural fruit based drinks,

including carbonated fruit drinks. Manpasand sensing a tremendous

opportunity launced its brand Fruits Up across a plethora of fruit based flavors

viz mango, apple, guava, litchi, orange and mixed fruit. It has also launched

fizzy variants in the carbonated fruit drinks market in multiple flavors of grape,

orange and lemon.

Going forward we expect Fruits Up to maintain its robust growth and clock

revenues of 327 cr (CAGR of 45% over FY16-19)

Coco Sip – Shot in the arm in an untouched market

Coconut water is a popular beverage amongst all age categories in India.

Coconut being pre-dominantly a coastal grown fruit, sees its yield diminish

towards north India Sensing an opportunity Manpasand has ventured into

packaged coconut water under its new brand Coco Sip. Coco Sip will be the

first of its kind natural coconut water without any preservatives in it. The

Fruits Up to grow multi fold

40.0

108.0

172.8

241.9

326.6

-

50.0

100.0

150.0

200.0

250.0

300.0

350.0

FY15 FY16 FY17E FY18E FY19E

Revenue from Fruits Up

` in cr

Source: Manpasand, Ventura Research

- 9 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

product will be available across SKU sizes at affordable prices starting at Rs

10 and will be manufactured through an outsourcing model.

Since the product is at a nascent rollout stage we have assumed revenues to

grow to Rs 60 cr by FY19. This is a high risk category as earlier ventures by

other players have not fructified. However we are enthused by the fact that

outsourcing of Coco Sip’s manufacturing reduces the risk considerably for the

company.

Tender coconut water in Coco-Sip

Source: Manpasand, Ventura Research

Coco Sip to show huge growth

5.0

18.0

60.0

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY17E FY18E FY19E

Revenue from Coco Sip

` in cr

Source: Manpasand, Ventura Research

- 10 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Introduction of new product varieties which have very high growth rates should enable the company to maintain an overall growth rate upwards of 40% despite the fact that its flagship product Mango Sip (~81% of its revenue) will be growing in the mid 30’s.

Strategic expansion to increase capacity by ~80% without

impacting the debt free status

To keep pace with the multifold jump in revenues Manpasand has

aggressively been expanding its overall capacity 4.5X over the last few years.

This capacity ramp up is expected to nearly double from the current 1.25 lac

cases per day to 2.25 lac cases per day by FY19. The company has an

existing facility in Vadodara and Varanasi and commenced another facility in

Vadodara in April 2015. The company has preponed its capex in Ambala from

Sep 2016 to June 2016 to meet the overwhelming demand.

Reducing dependence on Mango Sip

40%

50%

60%

70%

80%

90%

100%

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Mango Sip Fruits Up Coco Sip Manpasand ORS

Source: Manpasand, Ventura Research

- 11 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Aggressive depreciation charge to cool down going forth

Manpasand has been charging depreciation on a triple shift basis as per the

accounting policy adopted by the company. As per the stated policy the

depreciation charge will be higher in the first few years as the WDV is high for

fixed assets. Going forth the depreciation charge will cool down and result in a

higher PAT.

Strategic expansion going forth

40%

45%

50%

55%

60%

65%

0

50000

100000

150000

200000

250000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Capacity ( LHS) Utilsation (RHS)

cases per day

Source: Manpasand, Ventura Research

Higher cash generation going forth

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

-

20.0

40.0

60.0

80.0

100.0

120.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Depreciation EPS Cash EPS

` in cr ` per share

Aggressive depreciation charge( due to 3 shift working) has the cash

EPS growing faster than otherwise

Source: Manpasand, Ventura Research

- 12 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Performance

Manpasand reported stellar growth in its topline as well as bottomline numbers

during Q4 FY16. Net Sales jumped 91% YoY to Rs 230.4 cr from Rs 120.7 cr

in Q4 FY15 on the back of stupendous volume growth in Mango Sip and Fruits

Up. EBITDA jumped 54% YoY from Rs 27.8 crore in Q4 FY15 to Rs 42.8 crore

in Q4 FY16. EBITDA margins fell by 450 bps from 23% in Q4 FY15 to 18.5%

in Q4 FY16 on the back of higher trade discounts. PAT jumped 47.4% YoY to

Rs 25.5 cr from Rs 17.3 cr in Q4 FY15 on the back of stupendous sales

growth.

For FY16, Manpasand’s net sales stood at Rs 556.7 crore registering a growth

of 54.7% YoY. However EBITDA surged 72.0% YoY to Rs 110.4 crore. PAT

rose 68.3% YoY to Rs 50.5 cr in FY16 from 30 cr in FY15.

Consolidated Quarterly Financial Performance (Rs crores)

Description Q4FY16 Q4FY15 FY16 FY15

Net Sales 230.4 120.7 556.7 359.8

Growth (%) 90.9 54.7

Total expenditure 187.6 92.9 446.3 295.6

EBITDA 42.8 27.8 110.4 64.2

Margin (%) 18.6% 23.0% 19.8% 17.8%

Depreciation 16.0 5.6 57.1 20.5

EBIT (Ex. OI) 26.8 22.2 53.3 43.7

Non-Operating Income 2.1 0.0 9.1 0.4

EBIT 28.9 22.2 62.4 44.1

Margin (%) 12.5 18.4 11.2 12.3

Finance Cost 0.3 2.9 5.7 10.7

Exceptional Items 0.0 0.0 0.0 0.0

PBT 28.6 19.3 56.7 33.4

Margin (%) 12.4 16.0 10.2 9.3

Prov. for Tax 3.1 2.0 6.2 3.4

Profit after Tax 25.5 17.3 50.5 30.0

Margin (%) 11.1 14.3 9.1 8.3

Source: Manpasand, Ventura Research

- 13 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Outlook

Revenue growth trajectory is expected to continue going forward as

Manpasand is increasing its capacity to meet the rising demand for its

products. We expect the brisk pace of growth to be sustained, albeit at a

slightly lower CAGR of 40.3% to Rs 1,539 cr by FY19 mainly driven by strong

brand recall pan India, new product launches and rising penetration of juice

market in India. Consolidated net earnings are expected to grow at a lusty

CAGR of 56% from 51 crore in FY16 to 190 cr in FY19. The EBITDA and

margin are expected to reach to 20% and 14% respectively.

Robust revenue growth on the cards

5%

7%

9%

11%

13%

15%

17%

19%

21%

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

FY12 FY13 FY14 FY15 FY16 FY17EFY18EFY19E

Net Sales EBITDA Margin PAT Margin

` in cr

Source: Manpasand, Ventura Research

Stable return ratios going forth

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

RoE RoCE

Source: Manpasand, Ventura Research

Health working capital cycle going forth

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Credit Days Inventory days Debtor Days

No of days

Source: Manpasand, Ventura Research

- 14 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Valuation

Manpasand is a pure play beverage company with no listed peers to compare

with. Manpasand deserves rich valuations due to

its ability to consistently maintain a high growth trajectory

ramp up its brand Fruits Up into the 100 crore club within 2 years of its

launch

All the products categories are sunrise sectors and hence high growth

trends can be sustained over the medium to long term

Robust margins gains are also visible (from 16.3% in FY12 to 19.8% in

FY16) and there is a possibility for further improvement (we have not

factored in our model and remains an upside risk to our estimates)

Heatlh consciousness has brought a marked shift in consumer

preference from traditional aerated colas to fruit based beverages and

this trend is only expected to accelerate providing a higher addressable

market which speaks volume of visibility of growth for the fruit drink

industry and Manpasand.

While the PE model would be the best to capture the high growth story of

Manpasand, we have chosen to value the company using Cash EPS rather

than the traditional EPS method. The rationale behind this is the fact that the

company is charging accelerated depreciation (since plant works on 3 shift

basis) which actually suppresses the true earnings.

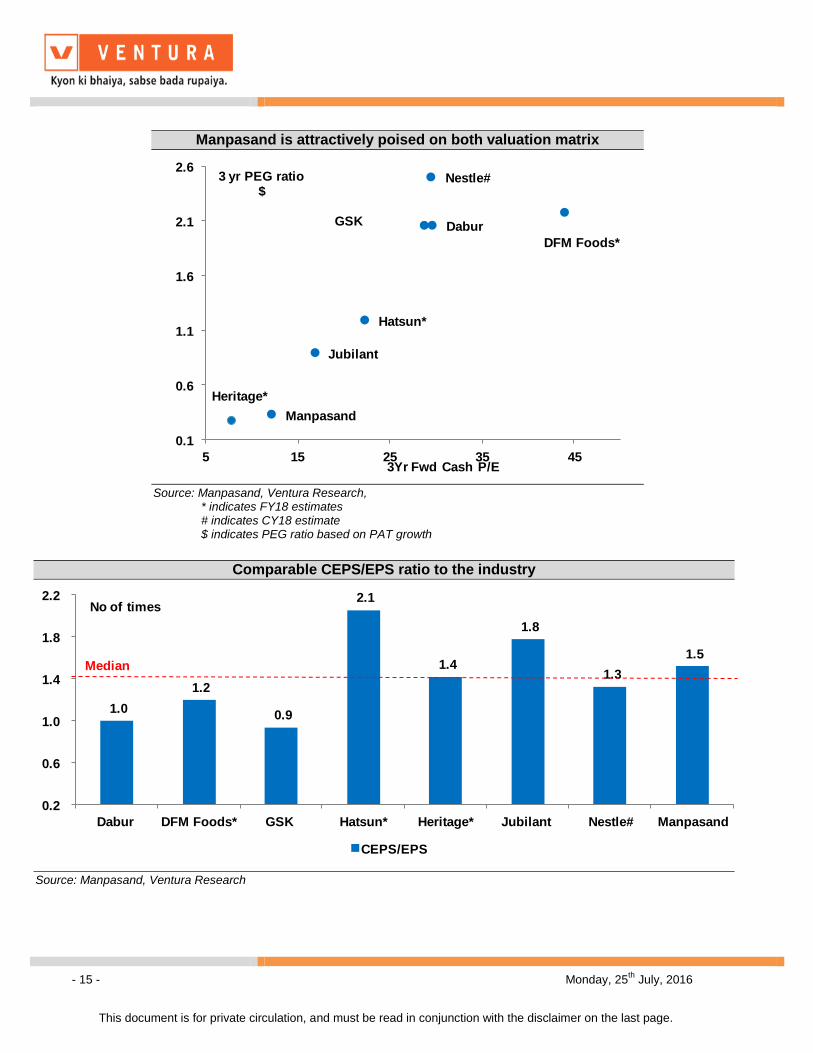

Currently the stock is valued at 12X FY19 Cash EPS of Rs 57.7 Considering

the peer-set median cash PE of 23.8 & the fledgling nature of the company we

have given a discount of 20% to this median multiple to arrive at a value of Rs

1,099 per share. This represents a potential upside of 57% from the CMP of

Rs 700 over the next 24 months.

- 15 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Manpasand is attractively poised on both valuation matrix

Dabur

DFM Foods*

GSK

Hatsun*

Heritage*

Jubilant

Nestle#

Manpasand

0.1

0.6

1.1

1.6

2.1

2.6

5 15 25 35 45

3 yr PEG ratio $

3Yr Fwd Cash P/E

Source: Manpasand, Ventura Research, * indicates FY18 estimates # indicates CY18 estimate $ indicates PEG ratio based on PAT growth

Comparable CEPS/EPS ratio to the industry

1.0

1.2

0.9

2.1

1.4

1.8

1.3

1.5

0.2

0.6

1.0

1.4

1.8

2.2

Dabur DFM Foods* GSK Hatsun* Heritage* Jubilant Nestle# Manpasand

CEPS/EPS

No of times

Median

Source: Manpasand, Ventura Research

- 16 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financials and Projections

Y/E March, Fig in ` Cr FY16 FY17E FY18E FY19E Y/E March, Fig in ` Cr FY16 FY17E FY18E FY19E

Profit & Loss Statement Per Share Data (Rs)

Net Sales 556.7 811.0 1141.8 1538.5 Adj. EPS 10.1 13.6 23.2 38.0

% Chg. 45.7 40.8 34.7 Cash EPS 21.5 29.8 42.9 57.7

Total Expenditure 446.3 656.1 916.9 1232.4 DPS 1.0 2.0 2.5 3.0

% Chg. 47.0 39.7 34.4 Book Value 120.1 131.2 151.4 185.8

EBDITA 110.4 154.9 224.9 306.2 Capital, Liquidity, Returns Ratio

EBDITA Margin % 19.8 19.1 19.7 19.9 Debt / Equity (x) 0.0 0.0 0.0 0.0

Other Income 9.1 3.2 4.6 6.2 Current Ratio (x) 4.0 3.5 2.9 3.4

PBDIT 119.5 158.1 229.5 312.3 ROE (%) 12.8 10.8 16.4 22.5

Depreciation 57.1 81.2 98.6 98.4 ROCE (%) 13.7 12.2 18.5 25.3

Interest 5.7 0.5 0.3 0.2 Dividend Yield (%) 0.1 0.3 0.4 0.4

Exceptional items 0.0 0.0 0.0 0.0 Valuation Ratio (x)

PBT 56.7 76.5 130.6 213.7 P/E 69.3 51.5 30.1 18.4

Tax Provisions 6.2 8.4 14.4 23.5 P/BV 5.8 5.3 4.6 3.8

Reported PAT 50.6 68.1 116.2 190.2 EV/Sales 6.1 4.2 3.0 2.2

Minority Interest 0.0 0.0 0.0 0.0 EV/EBIDTA 30.9 22.1 15.2 11.2

PAT 50.6 68.1 116.2 190.2 Efficiency Ratio (x)

PAT Margin (%) 9.1 8.4 10.2 12.4 Inventory (days) 46.2 51.1 54.8 58.4

Other opr Exp / Sales (%) 0.0 0.0 0.0 0.0 Debtors (days) 85.7 48.8 58.4 59.4

Tax Rate (%) 10.9 11.0 11.0 11.0 Creditors (days) 39.7 32.8 25.2 25.0

Balance Sheet Cash Flow Statement

Share Capital 50.1 50.1 50.1 50.1 Profit Before Tax 56.7 76.5 130.6 213.7

Reserves & Surplus 551.5 607.5 708.6 880.6 Depreciation 57.1 81.2 98.6 98.4

Minority Interest 0.0 0.0 0.0 0.0 Working Capital Changes -34.6 -43.0 -66.1 -91.4

Long Term Borrowings 0.0 0.0 0.0 0.0 Others -9.6 -11.2 -18.6 -29.5

Deferred Tax Liability 0.0 0.0 0.0 0.0 Operating Cash Flow 69.7 103.5 144.5 191.2

Other Non Current Liabilities 0.0 0.0 0.0 0.0 Capital Expenditure -243.1 -78.0 -170.0 -80.0

Total Liabilities 601.6 657.5 758.6 930.6 Other Investment Activities 9.1 3.2 4.6 6.2

Gross Block 357.3 507.3 657.3 757.3 Cash Flow from Investing -234.0 -74.8 -165.4 -73.8

Less: Acc. Depreciation -107.0 -188.2 -286.8 -385.2 Changes in Share Capital 366.8 0.0 0.0 0.0

Net Block 250.3 319.1 370.5 372.1 Changes in Borrowings -101.7 0.0 0.0 0.0

Capital Work in Progress 152.0 80.0 100.0 80.0 Dividend and Interest -11.8 -12.6 -15.4 -18.4

Non Current Investments 0.0 0.0 0.0 0.0 Cash Flow from Financing 253.4 -12.6 -15.4 -18.4

Net Current Assets 179.3 241.4 273.1 466.4 Net Change in Cash 89.0 16.1 -36.4 99.0

Long term Loans & Advances 19.8 17.0 15.0 12.0 Opening Cash Balance 3.5 92.5 108.6 72.2

Total Assets 601.4 657.5 758.6 930.6 Closing Cash Balance 92.5 108.6 72.2 171.2

- 17 - Monday, 25th

July, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Disclosures and Disclaimer Ventura Securities Limited (VSL) is a SEBI registered intermediary offering broking, depository and portfolio management services to clients. VSL is member of BSE, NSE and MCX-SX. VSL is a depository participant of NSDL. VSL states that no disciplinary action whatsoever has been taken by SEBI against it in last five years except administrative warning issued in connection with technical and venial lapses observed while inspection of books of accounts and records. Ventura Commodities Limited, Ventura Guaranty Limited, Ventura Insurance Brokers Limited and Ventura Allied Services Private Limited are associates of VSL. Research Analyst (RA) involved in the preparation of this research report and VSL disclose that neither RA nor VSL nor its associates (i) have any financial interest in the company which is the subject matter of this research report (ii) holds ownership of one percent or more in the securities of subject company (iii) have any material conflict of interest at the time of publication of this research report (iv) have received any compensation from the subject company in the past twelve months (v) have managed or co-managed public offering of securities for the subject company in past twelve months (vi) have received any compensation for investment banking merchant banking or brokerage services from the subject company in the past twelve months (vii) have received any compensation for product or services from the subject company in the past twelve months (viii) have received any compensation or other benefits from the subject company or third party in connection with the research report. RA involved in the preparation of this research report discloses that he / she has not served as an officer, director or employee of the subject company. RA involved in the preparation of this research report and VSL discloses that they have not been engaged in the market making activity for the subject company. Our sales people, dealers, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein. We may have earlier issued or may issue in future reports on the companies covered herein with recommendations/ information inconsistent or different those made in this report. In reviewing this document, you should be aware that any or all of the foregoing, among other things, may give rise to or potential conflicts of interest. We may rely on information barriers, such as "Chinese Walls" to control the flow of information contained in one or more areas within us, or other areas, units, groups or affiliates of VSL. This report is for information purposes only and this document/material should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this document nor anything contained herein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. This document does not solicit any action based on the material contained herein. It is for the general information of the clients / prospective clients of VSL. VSL will not treat recipients as clients by virtue of their receiving this report. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of clients / prospective clients. Similarly, this document does not have regard to the specific investment objectives, financial situation/circumstances and the particular needs of any specific person who may receive this document. The securities discussed in this report may not be suitable for all investors. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives. Persons who may receive this document should consider and independently evaluate whether it is suitable for his/ her/their particular circumstances and, if necessary, seek professional/financial advice. And such person shall be responsible for conducting his/her/their own investigation and analysis of the information contained or referred to in this document and of evaluating the merits and risks involved in the securities forming the subject matter of this document. The projections and forecasts described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections and forecasts were based will not materialize or will vary significantly from actual results, and such variances will likely increase over time. All projections and forecasts described in this report have been prepared solely by the authors of this report independently of the Company. These projections and forecasts were not prepared with a view toward compliance with published guidelines or generally accepted accounting principles. No independent accountants have expressed an opinion or any other form of assurance on these projections or forecasts. You should not regard the inclusion of the projections and forecasts described herein as a representation or warranty by VSL, its associates, the authors of this report or any other person that these projections or forecasts or their underlying assumptions will be achieved. For these reasons, you should only consider the projections and forecasts described in this report after carefully evaluating all of the information in this report, including the assumptions underlying such projections and forecasts. The price and value of the investments referred to in this document/material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance. Future returns are not guaranteed and a loss of original capital may occur. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. We do not provide tax advice to our clients, and all investors are strongly advised to consult regarding any potential investment. VSL, the RA involved in the preparation of this research report and its associates accept no liabilities for any loss or damage of any kind arising out of the use of this report. This report/document has been prepared by VSL, based upon information available to the public and sources, believed to be reliable. No representation or warranty, express or implied is made that it is accurate or complete. VSL has reviewed the report and, in so far as it includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. The opinions expressed in this document/material are subject to change without notice and have no obligation to tell you when opinions or information in this report change. This report or recommendations or information contained herein do/does not constitute or purport to constitute investment advice in publicly accessible media and should not be reproduced, transmitted or published by the recipient. The report is for the use and consumption of the recipient only. This publication may not be distributed to the public used by the public media without the express written consent of VSL. This report or any portion hereof may not be printed, sold or distributed without the written consent of VSL. This document does not constitute an offer or invitation to subscribe for or purchase or deal in any securities and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document is strictly confidential and is being furnished to you solely for your information, may not be distributed to the press or other media and may not be reproduced or redistributed to any other person. The opinions and projections expressed herein are entirely those of the author and are given as part of the normal research activity of VSL and are given as of this date and are subject to change without notice. Any opinion estimate or projection herein constitutes a view as of the date of this report and there can be no assurance that future results or events will be consistent with any such opinions, estimate or projection. This document has not been prepared by or in conjunction with or on behalf of or at the instigation of, or by arrangement with the company or any of its directors or any other person. Information in this document must not be relied upon as having been authorized or approved by the company or its directors or any other person. Any opinions and projections contained herein are entirely those of the authors. None of the company or its directors or any other person accepts any liability whatsoever for any loss arising from any use of this document or its contents or otherwise arising in connection therewith. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Securities Market. Ventura Securities Limited

Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079