Cmemagazine Sp 08

44

MICHAEL BLOOMBERG : INSPIRA TION FOR INNO V A TION p20 CLEARING THEWA Y p26 SPRING 2008 • A MAGAZINE PUBLISHED BY CME GROUP , A CME/ CHICAGO BOARD OF TRADE COMP ANY

-

Upload

rsaittreya -

Category

Documents

-

view

214 -

download

0

Transcript of Cmemagazine Sp 08

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 1/44

MICHAEL BLOOMBERG : INSPIRATION FOR INNOVATION p20 CLEARING THE WA

SPRING 2008 • A MAGAZINE PUBLISHED BY CME GROUP, A CME/CHICAGO BOARD OF TRADE COMPANY

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 2/44

BAXTER focuses on "Best Execution" in Currency markets. Our mission is to open access to

the most competitive and liquid FX markets, in the most efficient way. A choice of our proprietary

multi-bank ECN and a selection of the best 3rd party FX venues. Advanced trading functions for profestraders, delivered over the Web, electronically via the FIX Protocol or a choice of the best ISV's.

BAXTER’s product range includes

BAXTER Financial Services Ltd.

www.baxter-fx.com

Tel 24hr: +353 (1) 670 04

Best Execution inCurrency Markets

Spot-FX & Currency DerivativesCutting-edge technology

24hr trading in 70+ currency pairs

Currency Futures

DMA (Direct Market Access) to 3rd party Platforms and Exchanges

EFP's Spot-FX

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 3/44

“If you’re going to succeed,

you need a vision – onethat’s affordable, practical

and fills a customer need.

Then go for it.”

MICHAEL BLOOMBERG

MAYOR, NEW YORK CITY

ON THE COVER

Bloomberg L.P. founder and New

York City Mayor Michael Bloomberg

in Chicago, where he received the

2008 CME Group Fred Arditti Award.

To read CME Group Magazine online, visit us at

www.cmegroup.com/magazine

CME Group Magazine

CME Group20 South Wacker DriveChicago, IL 60606-7499312.930.1000 tel312.466.4410 [email protected]

Editorial DirectorsAnita Liskey, William Parke

Managing EditorPamela Plehn

Editorial Advisory BoardMeg Austin (Legal), Neal Brady (Business Development),Tim Doar(Clearing), Randy Frink (Corporate Marketing), Mary Haffenberg (ProductPublic Relations),John Harangody (Commodity Products), Alex Harris(Corporate Marketing), Jeremy Hughes (EMEA Corporate Communications),Dave Lerman (Equity Products), Chris Mead (Product Marketing), Gail Moss(Marketing Communications), Robin Ross (Interest Rate Products), DerekSammann (Foreign Exchange Products),Allan Schoenberg (TechnologyPublic Relations)

CME Group Magazine is published by CME Group in conjunction withNewsdesk Media Inc. and VSA Partners, Inc. All rights reserved.

Newsdesk Media Inc.700 12th Street, NW,Suite 700

Washington, D.C. 20005202.904.2423 tel202.904.2424 faxwww.newsdeskmedia.com

Maysoon Kaibni, Vice President Business DevelopmentMaryellen Thielen, Consulting Editor

VSA Partners, Inc.1347 S. State StreetChicago, IL 60605312.427.6413 tel312.427.6534 faxwww.vsapartners.com

Art DirectorsDavid Cooper, Newsdesk Media Inc.Brock Conrad, VSA Partners, Inc.

Do you have a question for CME Group Magazine?E-mail us at [email protected] with your questions and comments,or to be added to or removed from the mailing list. Further informationabout CME Group and its products is available on our Web site atwww.cmegroup.com. Information made available on our Web site doesnot constitute part of this document.

The Globe logo,CME®, CME Group™, Clearing360™, E-mini®, Globex®, IdeasThat Change the World®, International Monetary Market™, IMM® and SPAN®

are trademarks of Chicago Mercantile Exchange Inc. The Chicago Board ofTrade®, CBOT® and e-cbot® are trademarks of The Board of Trade of the Cityof Chicago,Inc.All other trademarks are the property of their respectiveowners and are licensed for use by CME Group. CMA DatavisionSM and CMAQuotevisionSM are service marks of Credit Market Analysis (CMA). Dow JonesIndustrial AverageSM is a trademark of Dow Jones & Company,Inc. and usedunder license.FXMarketSpace Ltd. (a U.K.Company) is the owner of thetrademark “FXMarketSpace.” LIFFEConnect® is a trademark of LIFFEAdministration and Management and is used with permission. NASDAQ®

is a trademark of The Nasdaq Stock Market, used under license. Pivot InstantMarkets™ is a registered trademark of Pivot, Inc.“S&P 500®” is a trademarkof Standard & Poor’s,a division of The McGraw-Hill Companies, Inc.Swapstream® and sPro™ are trademarks of Swapstream Operating ServicesLtd., a subsidiary of CME Group.BLOOMBERG PROFESSIONAL® is atrademark of Bloomberg Financial L.P., a Delaware limited partnership,or its subsidiaries.

All matters pertaining to rules and specifications herein are made subjectto and are superseded by official CME Group rules.Current CME Grouprules should be consulted in all cases concerning contract specifications.

© 2008 CME Group Inc.All rights reserved.CME Group Magazine is printed on recycled paper.

A Newsdesk Media Group Company

MEDIA INC.

Spring

Issue Ten

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 4/44

Successful traders and investors

understand that superior technology

and low trading costs hold the keyto greater returns.

6WRFNVp2SWLRQVp)XWXUHVp)RUH[p%RQGVp)XQGV

Markets

Worldwide

70from One Account

LQRYHU

Options

*

$0.15 - $0.70

per contract

SOXVH[FKDQJHIHHV

Futures &Commodities

$0.25 - $1.20per contract

SOXVH[FKDQJHIHHV

Stocks &ETFs*

$0.005 or less

per share

DOOLQ

ForexAs low as 1/2 PIP

wide spreadsplus 0.1 - 0.2 of

trade value

Bonds

(all-in)$1.00 per $1,000

face value (d$10,000)

$0.25 per $1,000

face value (>$10,000)

InterestUSD Fed Funds

-0.25 to -0.50% Paid

USD Fed Funds

+0.50% to 1.5%

Charged

Interactive BrokersThe Professional’s Gateway to the World’s Markets

Interactive Brokers LLC is a member of NYSE, FINRA, SIPC — * $1.00 minimum on all orders, no extra ticket charge. No technology surcharges. Commissions above arproducts, international products available at comparable rates. Supporting documentation for any claims and statistical information will be provided upon request

05

www.interactivebrokers.com

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 5/44SPRING 2008

FEATURES CONTENTS

8 Global Insight 6 From the Top A letter from the CME G

executive chairman and C

41 Cutting EdgeGaining Exposureto the CreditDerivatives MarketThe strategic acquisition

of CMA, a leading provid

of market data, opens ne

opportunities for CME G

12 Guest ColumnThe Financial CrisisDoes the Road to GlSerfdom Lie Ahead?Bernard Connolly predic

the collapse of the global

boom in our spring 2007

He explains why he was r

– and the implications

38 Current Pulse

U.S. Secretary of Agricul visits CME Group • NYS

Euronext to purchase me

complex • A new source

information • Survey pro

insights on FX trends •

Nonfarm payroll futures

launch • CME Group

earns top honors

42 Industry ConnectionInsight for Tomorro

As change accelerates,CME Group plans to hos

a new forum for financia

industry leaders to discu

trends in global finance,

politics and business

16 Partner Ties

20 Cover Story

26 Market Efficiencies

34 Product FocusCME Swaps on Swapstream –

Efficient and Effective

Soon there will be a better way

to trade interest rate swaps

Clearing the Way

A new look at the futures industry’s

longstanding model: centralized

clearing, where futures exchangesaround the world operate their

own clearing houses

30 At Your ServiceTwo Legacies Under One Roof

Blueprints. Timelines. Meetings.

Now the Chicago-based futures

pits are operating in a single location

for the first time in 100-plus years

Michael Bloomberg:

Inspiration for Innovation

As someone who brought

groundbreaking change to financial

markets, Michael Bloomberg offers

his perspective on innovation

U.S. Grain Contracts Tap

Benefits of CME Globex

Grain contracts traded at the

Minneapolis Grain Exchange,

Kansas City Board of Trade

and Chicago Board of Trade have

come together on CME Globex

The Hunger for New Solutions

The daily headlines discuss rising

food prices and resulting unrest.

Noted economist David Hale looks at

why this is happening and the forcesreshaping global agricultural markets

Spring

Issue Ten

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 6/446 CME GROUP MAGAZINE

Craig Donohue (left) and Terry Duffy

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 7/44SPRING 2008

FROM THE TOP

TERRENCE A. DUFFY

Executive ChairmanCRAIG S. DONOHUE

Chief Executive Officer

CME Group has never been known to avoid tough subjects. In this edition of CME Group Magazine

we take a closer look at a number of the challenging issues our global economy is currently facing.

Those of you who have been reading our magazine for a while may recall our spring 2007 cove

story,“Collapse of the Global Boom?”by Banque AIG’s Global Strategist Bernard Connolly. Written at a

time when most markets were still buoyant,Connolly presciently outlined the economic problems thatwere on the horizon. Now that the credit bubble has burst, we have invited Connolly back to provide his

thoughts on the current state of the financial system and global economy.

In the wake of the subprime meltdown and credit crunch, concerns about counterparty risk

have grown.This has turned the spotlight on the role of clearing houses like CME Clearing and revived

the periodic debate about whether the derivatives industry is best served by an exchange-owned or a

utility clearing model. In our view, the derivatives market has been well-served, both in terms of risk

management and product innovation, by the exchange-owned model. “Clearing the Way” takes a

closer look at the critical factors involved in this debate.

World commodity markets are facing unprecedented volatility and all of us are experiencing

the shock of rising food prices. As is often the case, the issue is far more complex than simply rising

demand and falling supply. In “The Hunger for New Solutions,” international economist and CME Group

Center for Innovation advisory council member, David Hale, examines various forces at play in one o

the most important global food markets – grains and oilseeds.

As participants in a global economy, it is important to understand the trends that directly and

indirectly affect our markets – and our lives. With that goal in mind, we are hosting our first-ever GlobaFinancial Leadership Conference in September. It will provide an opportunity for leaders in ou

industry, as well as the broader business and political communities, to discuss vital issues in today’s

increasingly challenging environment.We look forward to sharing highlights of the conference with you

later this year.

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 8/448

GLOBAL INSIGHT

CME GROUP MAGAZINE

THE HUNGERFOR NEW

SOLUTIONSUNDERSTANDING WORLD

FOOD MARKETS

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 9/44

The impact of rising food prices is of global concern. The UnitedNations considers “food insecurity” to be a major emerging risk of

the 21st century. According to the World Economic Forum’s Global

Risks 2008: A Global Risk Network Report, food prices in 2007

increased 17 percent in China, 4.7 percent in the United Kingdom

and 4.4 percent in the United States. The core of the solution is to

grow more food.

Supply and demand issues have affected the markets as long

as markets have existed. What is noteworthy now is that tradi-

tional supply issues are the most severe they have been in some

time, while, simultaneously, demand is increasing. The result is

a one-two punch for prices.

SUPPLYAND DEMAND IN THE GRAIN MARKETS

The worldwide grain trade represents a classic example of how

supply and demand shape markets. Fundamental supply issues,

including weather – witness the recent catastrophic flooding in

Iowa and other Midwestern states – and export policies are push-

ing up prices. At the same time, increased demand is coming from

emerging markets, with more corn diverted to the creation of bio-

fuels and fewer soybeans planted as farmers turn to corn as the

grain of choice. Also helping push up prices is the declining dollar,

which makes dollar-denominated products look like attractivebuys, and fuel prices, which are running up the cost of fertilizer

and distribution.

The result? Global grain stocks are declining, placing greater

pressure on prices. According to the International Food Policy

Research Institute’s 2007 report, The World Food Situation: New

Driving Forces and Required Actions, wheat and corn production

decreased 12 to 16 percent in the United States and UnitedKingdom between 2004 and 2006. Cereal stocks in China, w

constitute approximately 40 percent of total stocks, declined

nificantly from 2000 to 2004 and had yet to recover in 2007

For most observers of the grain and oilseed markets, clim

among the biggest factors causing declining global stocks of

For example, due to drought, the Australian wheat crop prod

only 12.7 million tons in 2007-2008 and 9.7 million tons in 2

2007, compared with 25 million tons in 2005-2006, accordin

the Australian Government’s Department of Agriculture, Fis

and Forestry.

Some crop experts also cite “carbon fertilization,” the ithat plants grow faster and larger as they absorb the atmosp

increased levels of carbon dioxide. This can result in highe

duction for crops such as rice and soybeans, but not necess

for corn, sugarcane and other crops because of temperatur

other factors.

On the other side of the supply-and-demand equation, f

demand is rising as incomes increase in emerging economie

including the fast-developing BRIC nations – Brazil, Russia,

and China – especially in cities where people now can afford

richer in calories and protein. In India, meat consumption h

grown 40 percent over the last five years. Demand is rising fpork in Russia, beef in Indonesia and dairy products in Mexi

Higher meat consumption creates greater demand for grain

feed cows, pigs and chickens.

Further competition now exists between food and fu

U.S. legislation is fostering demand for ethanol, a renew

gas that burns cleaner than petroleum gas and is domest

SPRING 2008

Increased demand and insufficient supply are causing food pricesto rise and reshaping how we think about agricultural markets.

By David Hale

International Economist and President of Hale Advisers, LLC

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 10/44

it’s your trading system,

build it your way...“I can have my coffee exactly the way I want it, so why should my trading system be different.”

We’ll never try to push a one-size-fits-all trading system onto you. We’ll work with you to deliver tailored solutions, built from modularcomponents, that maximize the investment you’ve already made and align with your business strategies.

From high speed trading platforms with global market access, to our pre- and post-trade risk management systems, Patsystems’solutions are designed to enhance derivatives trading performance and trade processing. We call it FlexAbility.

For more information call our sales team at +1 312 922 7600.

www.patsystems.co

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 11/44SPRING 2008

RIGHT: Actress Drew Barrymoreand World Food Program

Executive Director JosetteSheeran tour the CME Groupagricultural trading floor at thehistoric CBOT building.

FAR RIGHT: WFP’s JosetteSheeran tours the Central GrainMarket in Addis Ababa, Ethiopia– where transportationobstacles can contributeto food shortages.

produced from corn. Biofuels are expected to consume up to

30 percent of the U.S. corn crop by 2010, according to the

World Economic Forum’s Global Risks 2008: A Global Risk

Network Report.

Ironically, U.S. ethanol production still contributes only mar-

ginally to meeting domestic demand for transportation fuel, says

Dr. Peter Goldsmith, extension specialist, agribusiness manage-ment, in the Department of Agriculture and Consumer Economics

at the University of Illinois at Urbana-Champaign.

“U.S. ethanol has no role in fuel pricing, while the reverse

holds that ethanol prices are tightly correlated to petroleum prices.

The corn-based ethanol market is still relatively small, so it only

minimally reduces our dependence on foreign oil,” Goldsmith says.

Government trade policies also have had an impact on food

prices. The trend is toward increasing export tariffs and decreasing

import tariffs on grain and oilseeds. For example, India has

increased its grain export tariffs while lowering import tariffs on

edible oils. China has announced a further increase in edible oilimports with projections currently up an additional 14 percent.

The result of keeping domestic production off the global market

while lowering barriers for the acquisition of grain and other com-

modities from the global market has been increased demand for

U.S. grain and oilseed products.

Also worth noting is the recent attention focused on index

funds. According to Commodity Futures Trading Commission

(CFTC) data, there is no evidence that these funds are the cause

of the bull market in grains. Data published by the CFTC indicate

the percentage of open interest held by index funds has remained

relatively constant since 2006, when this data was first published.This means that, while index fund positions are growing, positions

by commercial and non-commercial participants have been grow-

ing at about the same rate. It should also be noted that wheat

futures, which hit a record $13 in March, closed below $7 in the

beginning of June. Speculators, including index funds, remained

in grain markets throughout the price drop.

All market participants play important roles. The speculator’s

role is to provide liquidity. Speculators often take on the other side

of the trade when a buyer or seller is needed. They are taking

the risk someone else wants to lay off. It is also important to

that speculators participate on both sides of the market – ho

both long and short positions.

RESPONDING TO THE MARKET

These issues are reflected in CME Group’s grain and oilseed m

kets, which provide a venue for price discovery and a means

manage price risk. As a result of market volatility, increased a

to the markets and expanded trading hours, volume in corn a

soybeans is up 23 and 29 percent, respectively, and wheat vo

is up nine percent.

CME Group has responded to rising volatility and pri

in these markets by increasing price limits for its grain an

oilseed contracts. This move was made to allow market papants to continue to utilize the contracts for price discove

and risk mitigation at levels more aligned with today’s ma

CME Group also has submitted a petition to the CFTC for

approval to clear over-the-counter (OTC) calendar swaps

for corn, wheat and soybeans and basis swaps for corn. Th

OTC swaps would enhance risk management practices, im

transparency in the OTC grains swap market, and reduce

counterparty credit risk.

P h o t o c r e d i t : W F P / A n t o n i o J a e n

Beyond Feeding the Poor On March 3, actress Drew Barrymore visited the CME Group trading floo

141 W. Jackson,with Josette Sheeran, executive director of the United N

World Food Program (WFP). The two were in Chicago for the Oprah Winf

Show – where Barrymore announced a $1 million personal donation to t

WFP for feeding Kenyan schoolchildren.But they also made a point to v

CME Group for insight into the global food markets.

“I think the traders have a feel for where things are going,”Sheeran

“It’s important for the World Food Program to get a better sense of whet

we are going to see a sustained high level of food prices, to help us help

who are simply being priced out of the food market.”

Although WFP’s primary mission is to feed those in need, the organ

also focuses on improving nutrition and quality of life, building assets an

moting the self-reliance of poor people and communities. For more infor

tion on this organization,please visit www.wfp.org.

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 12/4412 CME GROUP MAGAZINE

THE

FINANCIALCRISIS:Does the Road

to Global

Serfdom

Lie Ahead

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 13/44

In this magazine a year ago, I wrote that a compla-

cent consensus held by the central banking, politi-

cal, media and financial market worlds was totally

wrong. I wrote that credit conditions that formed

the “fundamentals” of the U.S. economy were likely

to deteriorate dramatically, with profound effects

both on the U.S. financial system and the worldwide

real economy.

The U.S. and world economy had been massive-

ly distorted by then-Federal Reserve Chairman Alan

Greenspan’s mistaken reaction to the technological

innovation and entrepreneurial dynamism trans-

forming the U.S. economy in the mid-1990s.

Greenspan rightly praised this free-market capital-ism but totally misread the appropriate monetary

policy response. A year ago, I warned that Greenspan

unwittingly might have delivered free-market capi-

talism into the hands of its enemies. Sadly, that pre-

diction was horribly accurate.

Has the financial crisis opened the door toworld government?

Now, we should have grave fears about the future

organization of the global financial system and the

global economy. It is clear that the U.S. authorities

are prepared to do whatever it takes to fend off the

risk of depression. Unfortunately, “whatever it

takes” will be very unwelcome to all of us who rec-ognize the moral and practical superiority of a free-

market capitalist system. Those who do not admit

that superiority are undoubtedly gleeful about the

present mess. They see it as an opportunity to

increase government control.

The global Financial Stability Forum, though a

worthy body in itself, is seeking to issue instructions

to the U.S. Securities and Exchange Commission

SPRING 2008

In the spring 2007 issue of CME Group Magazine, Bernard Connolly predicted the collapse of the global market boom. He was right. Here’s w– along with his views on the implications of today’s global financial cris

The U.S. economy is stillstructurally excellent, butsimply cannot operate except

with real long interest ratessignificantly below “normal.”

By Bernard Connolly

Global Strategist, Banque AIG

and, ultimately, to Congress. British Prime Minister

Gordon Brown is talking about a vision of “a global

covenant. . . to build the truly global society.” Brown

and some European Union allies may even view the

financial crisis as an opportunity to try to impose

elements of the bureaucratic E.U. model on the

United States.

In April, Greenspan wrote in the Financial

Times that, “[F]ree competitive markets are the

unrivalled way to organize economies. We have

tried regulation ranging from heavy to central plan-

ning. None meaningfully worked.” He is absolutely

right in that. But he ended, “Do we wish to retest

the evidence?” There are many who wish to do pre-cisely that, with a worrying risk that they will get

their way. Why?

Has Greenspan killed free-market capitalism in theUnited States?

I wrote a year ago that, “The tumor is inoperable,

but fatal if nothing is done. Chemotherapy can halt

the progression of the disease; but at the cost of

severe damage to the overall health of the organism

– the global free-market capitalist financial system.”

The tumor is a level of real long rates of interest far

below reasonable guesses of the economy’s p

growth rate. Greenspan wrote in April that “

matic fall in real long-term interest rates”

2001 and 2006 created housing bubbles an

credit boom-bust in many countries. He

right. But he will no doubt claim that the

long real rates fell was some alleged “globa

glut” and that Fed [Federal Reserve] po

nothing to do with it.

The reality is very different. In Marc

the Treasury inflation-protected securities

curve was virtually flat at about 4.4 percent

2007, the 10-year TIPS yield reached 2.83

In both episodes, the peaks in long rates wemal” somewhat above the expected trend

growth. But both were immediately follow

burst bubble – NASDAQ in spring 2000, c

summer 2007. In both episodes, long rate

quently plunged – not because of a “global

glut” but because markets became pessimist

the U.S. economy’s growth prospects.

The U.S. economy is still structurally e

but simply cannot operate except with r

interest rates significantly below “norma

conclusion is deeply disturbing – indeed, t

implies that free-market capitalism no lon

work properly in the United States. The r

rate of interest is the single most importantor of a capitalist economy. If it once goes s

“wrong,” getting it “right” again will be ex

painful and dangerous. The 1930s show

bringing a retreat from free markets even

United States.

The Fed implicitly shares the judgment

risks involved in trying to put real long rate

are just too horrible. But avoiding them requ

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 14/4414

GUEST COLUMN

long rates to stay aberrantly low indefinitely , bring-

ing misallocated capital, lower productivity growth,

and depressed confidence about the future. Assetprices would have to go back to substantially over-

valued levels to sustain U.S. domestic demand in

line even with reduced potential growth rates.

Without a new credit bubble, that will require real

interest rates to move ever lower on a secular basis.

The alternative is to allow U.S. real rates to nor-

malize, but to offset the U.S. growth impact by

encouraging further massive dollar depreciation.

That is probably neither financially nor politically

feasible, either for the United States or the rest of

the world.

In short, the United States is, at best, likely to

become an economy with inefficiently allocated

capital, distorted risk-reward incentives, a low rateof productivity growth, inflated asset prices and

ever-increasing financial vulnerability, all as part of

a Ponzi game. Income-distribution questions will

become more and more politically pointed. Even

worse, this unsatisfactory outcome can be achieved

only if the financial system is bailed out, possibly by

taxpayers. In such circumstances, it is almost

inevitable that financial regulation will become

more intrusive, onerous and harmful to economic

efficiency and economic freedom.

Euro-barbarians at the gate – but don’tblame markets

If there had not been a credit bubble, even lower realrates would have been needed. Those lower rates

would have produced a credit bubble. Ponzi games

and bubbles are symptoms of an underlying problem

– distorted intertemporal price signals – for which

central banks, not the private financial markets, are

squarely to blame. It is pointless to worry about

“price discovery” in financial or property markets

unless the central banks are prepared to eliminate

the underlying distortion. To do that, central banks

would have to try to engineer a very sharp rise in

real long rates – particularly in U.S. real long rates.

That would be the most irresponsible action of all at

this time.

Policy needs to find a middle way. At one extremeare the fundamentalists who abhor any government

intervention, however dangerous the liquidation that

could result. At the other extreme are those who want

a more statist financial and economic system. The U.S.

authorities should certainly take no notice of advice

from Europe. Any unavoidable government interven-

tion should be done by people who hate doing it, not

by people who do it gleefully.

CME GROUP MAGAZINE

What we most admire in Greenspan is his devo-

tion to free-market capitalism. He would be well-quali-

fied to advise on the least harmful form of intervention.However, he now seems to have reverted to the funda-

mentalist camp. That is ironic, given his disastrous, anti-

“Austrian” reluctance in the mid-1990s to prevent asset-

price booms, which are clear indications of distorted

intertemporal price signals. Did Greenspan’s failure to

act come from his close association with the prepos-

The United States is, at best, likely to become an economy with inefficiently allocated capital, distorted risk-rewardincentives, a low rate of productivity growth, inflatedasset prices and ever-increasing financial vulnerability.

terous novelist and philosopher Ayn Rand, w

the great Austrian-British economist Fried

Hayek in contempt for being insufficiently inist and too open to an altruistic ethic that sup

opened the door to collectivism?

Hayek identified and warned against

to serfdom in the world. One has to hope

journey will not turn out to have been rout

Rand via Greenspan.

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 15/44

“Solutions should t the risk.”

ANDREW COYNE

Managing Director,

Head of FX Prime Finance

and eCommerce, Citi

In the face of global exchange rate fluctuations, traders demand risk management

solutions that fit. That’s why Andrew Coyne relies on CME Group, the largest regulated

foreign exchange (FX) marketplace in the world. CME Group offers unparalleled liquidity,

with tight bid-offer spreads, in all major currencies—including the euro, British pound,

Swiss franc and Japanese yen. By trading on the CME Globex electronic platform, leading

corporate and investment banks like Citi utilize cutting-edge technology to provide

customers with credit-efficient, cost-effective ways to manage FX exposure.

By improving the way markets work, CME Group is a vital force in the global economy,

offering futures and options products on interest rates, equity indexes, foreign exchange,

commodities and alternative investments. Learn how CME Group can change your world

by visiting www.cmegroup.com/info.

The Globe logo, CME®, Chicago Mercantile Exchange®, CME

CME Group™ are trademarks of Chicago Mercantile Exchange

Chicago Board of Trade® are trademarks of the Board of Trade

Chicago. Copyright © 2008 CME Group. All rights reserved.

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 16/4416

Grain contracts traded at the MinneapolisGrain Exchange, Kansas City Board of Tradeand Chicago Board of Trade have come together

on CME Globex – creating new opportunitiesand efficiencies for market participants.

When the Chicago Board of Trade (CBOT) merged with the Chicago

Mercantile Exchange (CME) in 2007, one of the most obvious benefits was

the efficiencies to be gained by consolidating trading operations. While legacy CME floor-traded contracts moved to the trading floor at the CBOT building,

legacy CBOT electronic contracts moved in the other direction, migrating

from the e-cbot platform to the CME Globex electronic trading platform.

With them moved wheat contracts from the Kansas City Board of Trade

(KCBT) and Minneapolis Grain Exchange (MGEX). As a result of thorough

preparation for the shift to CME Globex, officials at all three exchanges agree

that the migration was seamless and hardly noticeable to customers when it

occurred in January 2008.

“Having all three exchanges on the same platform provides the eff

cies of one-stop shopping for U.S. grain risk management needs,” says J

Borchardt, KCBT president and chief executive officer. “For those tradi

companies or intermediaries that deal in grain, it requires access to few

forms to conduct business, thereby reducing costs. It also gives the thre

exchanges the ability to offer trading strategies between products more

ciently, intra-platform rather than inter-platform.” Although all three exchanges trade wheat on CME Globex, each exc

trades a different class of wheat with different uses.

“CME Group trades a soft red winter wheat (milled mainly for flou

in crackers, biscuits and cookies), KCBT a hard red winter wheat (a hig

protein wheat milled into flour used for breads), and MGEX a hard red

wheat (a higher protein class milled into flour used in breads, bagels an

baked goods),” explains Richard Jelinek, associate director, commoditie

Group. CME Group’s wheat class has the lowest physical production –

CME GROUP MAGAZINE

U.S. GRAIN CONTRACTS

TAP BENEFITS

OF CME GLOBEX

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 17/44

highest volume of all wheat markets in the world – due to its liquidity and

transparency. Having all three exchanges’ products on the same platform

allows for easier electronic spreading.

When it comes to trading platforms, putting multiple markets together on

one platform is an excellent idea, especially when that platform is CME

Globex, which has won renown around the world for its speed, reliability and

scalability since it was launched in 1992.“Electronic availability is the key for all of today’s markets, not just wheat,

and consolidating products on a single platform creates efficiencies,” adds

Susan Sutherland, associate director, commodities, at CME Group.

For CME Group, the shift to one platform means the exchange can con-

centrate on further developing and enhancing CME Globex. Jelinek points out

that this ongoing process has improved the average round-trip response time

across all product complexes from 31 milliseconds to 13.7 milliseconds in the

first quarter of 2008.

Electronic trading in grain and soybean futures has grown dramatic

since side-by-side trading began on Aug. 1, 2006, and now accounts for m

than 80 percent of total volume in some of the major CME Group future

contracts. The focus has now turned to options. The platform’s sophistica

technology, rich functionality and strong distribution provide perfect gro

conditions for those contracts. Side-by-side trading for grain and oilseed

during regular daytime trading hours began on April 14. As side-by-side f

trading has produced a marked increase in total volume, attracted new m

SPRING 2008

“Electronic availability is the key for all of todamarkets, not just wheat, and consolidatingproducts on a single platform creates efficienc

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 18/44

0 2 4 6 8

2008

Futures

2007

Futures

311,727 489,802

363,663 267,504

Q1

Q1

1 3 5 7

Ope

Elec

18

PARTNER TIES

participants and hiked the electronic share of trading, CME Group anticipates

similar results from side-by-side trading of grain and oilseed options.

“We are excited to have our products listed on the CME Globex platform,”

says James Facente, director, market operations, clearing and information tech-nology at MGEX, describing CME Group as innovative market leaders and

CME Globex as the “premier” trading platform in the world. “We now have

exposure to new participants and new markets when you look at the platform’s

connectivity to overseas areas. We have always had overseas customers, but the

ease of access to one platform that is as reliable and easy to use as CME Globex

gives us a much greater audience.”

With the growing role of Brazil, Russia, India and China, as well as other

developing nations in global markets, those connections will become increas-

ingly important. CME Globex already has a world network distribution of

1,100 direct connections in more than 80 countries.

“Having all three U.S. grain exchanges on one platform offering electronic

trading day and night allows worldwide access to all of these global benchmark

products in the most efficient and cost-effective manner,” Borchardt says. “At

KCBT, we have certainly noticed an increase in global commercial participa-tion in our contracts as a result.”

First-quarter 2008 trading volume already shows the effect of having all

the grain futures contracts available on CME Globex for most of the quarter.

Average daily volume of grain and oilseed futures jumped 27 percent for the

first quarter of 2008 from the same period a year earlier. As the chart illus-

trates, electronic futures trading growth was even more impressive. CME

Globex accounted for 61 percent of wheat futures volume for the first quarter

of 2008 versus 42 percent for the year-earlier period.

MGEX and KCBT also felt the positive effects of the migration to CME

Globex. At MGEX, wheat futures volume rose 24.5 percent for the first quarter

of 2008 compared with the same period a year ago, and the percentage traded

electronically doubled to 41.3 percent in 2008 from 20.8 percent in 2007.

Total wheat futures volume at KCBT climbed 16.7 percent in the first quarter

of 2008 compared with the prior year.For the futures commission merchants and brokerage firms, having all

contracts on CME Globex also means more efficient operations on the other

end of the connectivity pipe, because the firms need to maintain only one con-

nection to a trading platform instead of accommodating multiple configura-

tions of different platforms.

And for customers, having everything they trade on CME Globex provides

a number of benefits: shorter execution trading times, reduced trade costs and

more choices in trading products and venues.

“The broad distribution that CME Globex offers makes it easier for our

global customers, both hedgers and traders alike, to participate in CME

Group’s grain and oilseed complex,” Jelinek says.

At the same time, those who have been trading agricultural products have

improved access to the other product complexes available on the same CME

Globex platformWhen it comes to futures and options trading and CME Globex, there is

power in one.

CME GROUP MAGAZINE

Growth of Grain and Oilseed Futures

Contracts in thousands

“Having all three U.S. grain exchanges onone platform offering electronic trading dayand night allows worldwide access to allof these global benchmark products in themost efficient and cost-effective manner.”

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 19/44

I$ Your Dough Ri $ing?For over 150 years, the Kansas City Board of Trade has been the world’s market for the trading of hard red winter wheat, the predominant bread wheat variety. KCBT

wheat futures and options offer choice of access — electronic or open outcry, so you can reach us whenever and from wherever. Integrity, liquidity, transparency and attention to customer service are our cornerstones of market trust and thereason for our continued growth as the global benchmark for “bread wheat”.

For more information,call 1-800-821-5228 or visit www.kcbt.com

The World’s “Bread Wheat” Market

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 20/4420 CME GROUP MAGAZINE

NSPIRATIOFOR

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 21/44SPRING 2008

INNOVATIO

In 1981, Michael Bloomberg started a company with three

co-workers and a revolutionary idea: proprietary terminals

offering real-time market data and analytical technology

to businesses and traders. More than 25 years later,

Bloomberg L.P. has become one of the largest financial

information and news organizations in the world – andits wide-ranging impact on the financial markets led the

CME Group Center for Innovation to name Bloomberg

its 2008 winner of the Fred Arditti Innovation Award.

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 22/44

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 23/44

ONE DOOR CLOSES, ANOTHER OPENS

Bloomberg L.P. came into being after the suddenend of Bloomberg’s career as a partner at SalomonBrothers. He was shown the door after 15 years atthe firm, as one of 63 top-level Salomon execu-tives to lose their jobs when Salomon merged withPhibro Corporation, a publicly held commoditiestrading firm.

The good news was he was given a $10 mil-lion severance package. Bloomberg finished his

last day at Salomon on Sept. 30, 1981, the way hebegan his first, working a 12-hour day. The nextday, he went to work at his own company.

Today, Bloomberg L.P. has more than 10,000employees at 130 state-of-the-art offices all over the world. But back then, as Bloomberg tells it, it was“four guys, one room and a coffee pot” in a smalloffice in Manhattan with a view of an alley.Bloomberg was the first employee, but he startedthe firm with three other colleagues from Salomon.

“The real fun was back at the beginning,” hesays. “I’ll never forget how hard we worked forthree years to get our first order.”

That order would be the best transaction

Bloomberg ever made. Merrill Lynch ordered20 terminals at a cost of $1,000 per terminal.“I remember writing 20 x $1,000 on the back

of an envelope thinking, ‘That would cover ouroverhead,’” Bloomberg says. “Today, that wouldn’tcover our food bill.”

The deal with Merrill Lynch was actually more complicated, more speculative and, well,luckier than that, as detailed in his book

Bloomberg by Bloomberg . In the sales meeting withMerrill, Bloomberg explained that his firm’s tech-nology would provide data unique in the capitalmarkets – a system that would provide yield curveanalysis, updated throughout the day as the mar-kets moved, including futures versus cash. Thetechnology would then note every transaction andmark positions to market instantly. Bloombergsaid that he could deliver the system within sixmonths – faster than Merrill would be able to do

if the company developed it internally.In June 1983, Bloomberg delivered the sys-tem to Merrill on time. They ran one function onthe computer and it crashed, but no one seemedto mind. The pieces were in place and Bloomberg was on his way.

As it turned out, this was virtually the only break Bloomberg needed because Merrill Lynchsigned him to an exclusive deal that prevented himfrom selling his terminals to competitors for five years. Merrill Lynch later took a 30 percent stakein the firm for $30 million and helped disseminateBloomberg terminals to its customers around theglobe. Both companies expanded rapidly, equipped

with technology that gave them an edge.Today, the terminals have evolved into theBLOOMBERG PROFESSIONAL service, which isused by approximately 250,000 subscribers fromthe world’s central banks, investment institutions,commercial banks, government offices and agen-cies, law firms, corporations and news organiza-tions in more than 150 countries. BloombergNews encompasses television and radio programs

in seven languages, financial book publisaward-winning magazine and print newsby more than 400 publications in 70 coun

WHAT’S SO SPECIAL?

Bloomberg L.P. is known by the general puits media services rather than for its antechnology. But it was the technology Bloomberg apart from every other dataand newswire service. Bloomberg had t

customer in Merrill. And it had the right at the right time when the bond markesomed in the 1980s.

SPRING 2008

As the winner of CME Group Center for Innovation’s Fred Arditti Innovation Aw

in April, Michael Bloomberg was recognized for his entrepreneurial skills and abi

to bring truly groundbreaking change to the financial markets.

What is admirable about Michael Bloomberg is not just that he built his company,

Bloomberg L.P., into one of the top data and news companies in the world, but thatdid it with his own money, from scratch, and almost entirely internally and organic

Bloomberg, now worth an estimated $11.5 billion according to Forbes Magazine,

reveals the secret to building a successful company or organization.

“Innovation is having the instinct that it might work,” Bloomberg says. “We wan

people who try things that don’t work, but don’t quit. Don’t walk away from trying

the next thing.”

New York Mayor Michael Bloomberg received theCME Group Fred Arditti Innovation Award for hisrole in revolutionizing the analysis of financial data.

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 24/4424

COVER STORY

What made Bloomberg terminals so valu-able is that they could provide bond pricinginformation in a way no one else could.Bloomberg terminals provided the relative valueof debt instruments based on their yield and

price histories, giving Merrill Lynch an accuratepicture of the bond market instantly. Such infor-mation was valuable for anyone trading theinterest rate market.

Bloomberg advanced his company further inMay 1987, when he convinced The Wall Street

Journal and Associated Press that his company should become the sole disseminator of daily U.S.government bond prices, a role that had beenhandled by the Federal Reserve Bank of New York for more than a century. The Fed was liter-ally hand-delivering critical bond data to newspa-pers and wire services via a courier. Bloombergsimply automated that delivery process, a move

that put the company on the map.By 1990, Bloomberg decided it was time tomove into the news business. He began buildingnews desks to cover the financial marketsaround the world. The company held its ownagainst newswire behemoths Dow Jones andReuters by proving to customers that its newscoverage was as good as or better than the com-petition. The company broke into the televisionand radio sectors in 1991 and is now considereda major force in financial news.

Bloomberg News implemented new and bet-ter ways to generate and send financial news tocustomers. For example, Bloomberg computers

are programmed to periodically update marketinformation, rather than have reporters do so. Automated market information about the Dow Jones Industrial Average, S&P 500 Index or otherindexes is created and sent to customers in a matterof milliseconds – and reads like a story. The screen will display something like, “The Dow JonesIndustrial Average was 1.09 percent lower at 3:01p.m. Eastern time, down 62.14 at 12202.” The story includes the biggest gainers and losers in the index.

Interestingly, for an entrepreneur who paysincredible attention to detail in all aspects of hisbusiness – down to the salt-water fish tanks andfree snacks for employees at each office –

Bloomberg finds very little value in detailinga long-term business plan.“If you’re going to succeed, you need a vision,

one that’s affordable, practical and fills a customerneed,” he writes in his book. “Then go for it. Don’t worry too much about the details. Don’t second-guess your creativity. Avoid overanalyzing the new project’s potential. Most importantly, don’t strate-gize about the long-term too much.”

CME GROUP MAGAZINE

From left: Leo Melamed, CME Group chairmanemeritus; Michael Bloomberg, mayor of New York;and Robert Merton, 1997 Nobel Laureate in economics

The CME Group Center for Innovation (C

founded in 2003 to create and sponsor thou

voking original programming that identifies,

es and fosters examples of significant innova

creative thinking across multiple industries.

The CME Group Fred Arditti Innovation

sponsored by the center, honors an individual

whose innovative ideas, products or services

ated significant change to markets, comm

trade. The annual award honors innovation

had a positive impact on the economic well-

individuals, industries or nations. The award

after the exchange’s former chief ec

Fred Arditti, who was instrumental in develoInternational Monetary Market index upo

CME Group’s Eurodollar futures contract, the

most actively traded futures contract, was fou

Michael Bloomberg, founder of Bloomb

and current mayor of New York City, was the

of the 2008 award in April. He was recognize

tremendous innovations in financial market

fostered through the founding of his compan

one of the largest financial information a

organizations in the world.

Prior recipients of the award include:

Sharpe, Nobel Prize-winner in economics;

Fama, Distinguished Service Professor of

at the University of Chicago Graduate SBusiness; and Leo Melamed, CME Grou

man emeritus.

CFI’s advisory council is responsible for

each year’s recipient. John P. Gould,

G. Rothmeier Distinguished Service Prof

Economics, University of Chicago Graduate S

Business, serves as the council’s chairman

noted committee members include Gary S

and Robert Merton, Nobel Prize-winning eco

David D. Hale, international economist;

H. Moskow, former president, Federal Reser

of Chicago; and Robert J. Shiller, Stanley

Professor of Economics, Yale University a

economist, Macro Securities Research, LLC.

GOVERNMENT ENTREPRENEURSHIP

Bloomberg entered public service when he waselected mayor of New York City in 2001. He wasre-elected in 2005 and plans to step down in 2009 when his term ends. As mayor of New York City,Bloomberg has brought much of the same innova-tive spirit to government.

The budget overseen by the mayor’s office isthe largest municipal budget in the United States– roughly $63 billion a year. The city employsmore than 370,000 full-time and full-time equiv-alent employees and spends about $20 billion toeducate almost 1.1 million children. Bloombergsays innovation is needed in the public sphereand jokes that running a government budget is

the exact opposite of running a corporate one.“Business is a dog-eat-dog world,” Bloombergsays. “Government is actually just the reverse.”

In business, executives typically move moreresources into the profitable lines of the company and cut away resources from failing product lines.In government, however, profitable areas oftenare used to bolster unprofitable and underper-forming areas.

Yet even there, Bloomberg has tried to bringefficiency and innovation to government by tryingto measure the effectiveness of programs and hold various sectors accountable.

“You have to be able to collect and trust the

data,” Bloomberg says. “If you can’t measure it, you can’t manage it.”Bloomberg says he doesn’t know what his

next step will be after he steps down as mayorafter his second term. He’s often been rumored tobe a strong candidate for a federal post, althoughhe ruled out a run for president. But if he followshis personal credo that transformation is good,Bloomberg will likely be leading change.

CME GROUP CENTER

FOR INNOVATION ADDS

BLOOMBERG TO WINNERS’ L

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 25/44

www.newedgegroup.com

“Newedge” refers to Newedge Group and all of its branches and subsidiaries. Only Newedge USA, LLC and Newedge Financial Inc. are members of FINRA and SIPC (although SIPC only pertains to securtransactions and positions). Newedge Group (UK Branch) and Newedge Group (Frankfurt Branch) and Newedge Group (Dubai) do not deal with, or for, Retail Clients (as dened by MiFID and Dubai FinanAuthority). Only Newedge Canada Inc. is a member of the CIPF. Not all services are available from all Newedge organizations or personnel. Consult your local oce for details.

Global Asset Execution

Global Asset Clearing

Prime Brokerage

Fimat and Calyon Financial have united to create Newedg

Cutting-edge talent and technologies. Access to 70+ exchanges

across multiple asset classes. Serving institutional clients worldw

To support your strategies and help realize your vision.

Global, impartial, innovative, Newedge is the heartbeat

of today’s nancial market.

new forcein the world of brokerag

An innovative

new forcein the world of brokerag

An innovative

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 26/4426 CME GROUP MAGAZINE

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 27/44SPRING 2008

THE WAYFutures exchanges around the world have operated their own clearing houses for decades,but this longstanding business model is facing a new debate in the United States and Europ

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 28/4428

MARKET EFFICIENCIES

When it comes to clearing, futures and equity

exchanges have taken separate paths.One clear-

ing model isn’t superior to another because each

is designed for the unique business needs of the

markets it serves.

For more than 100 years, the futures industry

has benefited from a central counterparty clear-

ing (CCP) model in which exchanges own their

own clearing houses. This “vertical” model has

allowed exchanges to invest confidently in devel-

oping innovative new products and services that

have helped markets grow.It also has encouraged

the development of risk management tools, such

as the Standard Portfolio Analysis of Risk (SPAN)

system, which has become the industry standard

for portfolio risk assessment and is now used by

more than 50 exchanges worldwide.

In contrast,the securities and options world,

where exchanges list stocks and options issued

by third-party corporations, uses a “horizontal”

or utility model, with one participant-owned

clearing house for all the exchanges’ products.For stocks, it is the Depository Trust & Clearing

Corporation and for options, the Options

Clearing Corporation. This model works because

stocks are issued by a third party, whereas

futures are proprietary products, created by the

exchanges on which they trade.

As consolidation and globalization

reshape the industry, a tug of war has devel-

oped between established futures exchanges

and the large investment banks and hedge

funds that are some of their biggest users. For

example, several of the big banks plan to start

electronic exchanges to compete with CME

Group in the United States and Liffe in Europe.

One of the newest startups,Electronic LiquidityExchange (ELX), is backed by investment

banks, such as JPMorgan and Merrill Lynch,

and financial services firms, such as Citadel

Investment Group and Peak6. And in Europe,

brokers including Goldman Sachs and UBS are

in talks to start a rival exchange to Liffe, called

Project Rainbow.

These firms contend that the ownership of

clearing services that futures exchanges like

CME Group have makes it harder for new

exchanges to enter the market and build liquidi-

ty. Other market participants have added their

opinions to the conversation, suggesting that it

may be time to mandate a horizontal model

rather than continuing to let the market deter-

mine which model best meets its needs. The

Futures Industry Association (FIA),whose board

is weighted toward many of the large investment

banks, also favors instituting a horizontal clear-

ing model.

Proponents of vertical clearing counter

that this clearing model has been the industry

standard for decades, with astonishing success.

The CCP model has protected exchange-traded

markets against many of the issues aroundtransparency, liquidity, and valuations that peri-

odically crop up in over-the-counter (OTC)

markets. CME Clearing has operated without a

single default in the 100-plus years it has existed.

Basically, they say, “If it ain’t broke,don’t fix it.”

In a speech to the Managed Funds

Association earlier this year, CME Group Chief

Executive Officer Craig Donohue pointed out

that, “Despite [CME Group’s] significant growth,

we have improved market efficiencies, reducing

capital, margining and financing costs,as well as

exchange trading fees, by hundred of millions of

dollars over the last decade.”

Donohue also contended that central coun-

terparty clearing systems guarantee threeessential benefits to the customer: transparency

of valuation, because CCPs show daily mark-to-

market prices to all participants; independence;

CME GROUP MAGAZINE

To bridge the gap between over-the-co

(OTC) markets and central counte

clearing, CME Clearing offers a ser

services called CME Clearing360,

extends the benefits of exchange-t

clearing to the OTC market in some

vanilla” products, and also provides

clearing services.

Through CME Clearing360, firms

as hedge funds, proprietary trading

and global and regional banks have acc

the same performance guarantee tha

traditionally been available only

exchange-traded products.CME Clearin

provides these customers with greater

tal and operational efficiencies, inc

risk offsets against related futures

options positions.It also delivers world

risk management of the credit, opera

and legal risks related to OTC trading,a

as regulated market protections.

CME Clearing360 includes transa

executed on FXMarketSpace, cleared

est rate swaps, block trades exe

through Pivot, ethanol calendar swap

substitutions. CME Group also serve

market participants in the credit deriv

markets through its subsidiary CMA.

Some of these initiatives are CME

“firsts”: FXMarketSpace, a joint ve

company of CME Group and Reuters,

first centrally-cleared, global FX platfo

the cash FX market. Later this year

Clearing360 will offer clearing services

new product, CME Swaps on Swaps

which will be the first interest rate swap

uct to offer all OTC market participan

full benefit of central counterparty clea

Trader A

Defaults

on Trade

Central CounterpartyContains Default

Trader B

Buying fromTrader A

Trader B Customers

Protected

Trader A Customers

Protected

BUYS

SELLS

Trader ADefaultson Trade

Trader BBuying from

Trader A

Trader B Customerunprotected

Trader A Customersunprotected

HOW CLEARING MODELS MANAGE RISK

With a central counterparty model, the clearing house is the buyer

to every seller and the seller to every buyer. So, if Trader A defaults,

the default is contained between Trader A and the clearing house,

protecting everyone in the green circles below.

CENTRALCOUNTERPARTY MODEL

The over-the-counter market’s bilateral model works differen

If Trader A defaults, neither Trader A, Trader B, nor the others

they transact business with are protected from that default,

leaving everyone in the orange circles at risk.

BILATERAL MODEL

Customers protected from losse

Customers at risk for losses

CME Clearing360

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 29/44

and neutrality, because they are not dominated

by a few large interested parties.

Over the years, exchange-owned clearing

houses have demonstrated their ability to

enhance transparency and reduce systemic

credit risk. By contrast, the intermediaries that

own a utility clearing house have the potential to

limit clearing services to selected products and

markets in the pursuit of proprietary trading

profits or prime brokerage revenue streams. In

turn, this may limit transparency and exacerbate

risk in the swap and credit markets.

Opponents of the vertical model contend

that, by making it harder for new exchanges to

compete, the current model discourages inno-

vation and perpetuates higher prices. But the

current vertical model is the one that truly

encourages innovation, say its proponents.

Exchanges that depend upon clearing as a prof-

it center have an incentive to improve their

products and innovate in the clearing arena.

“The clearing house structure in the indus-try has been very innovative over the last 25

years,” says Tom Kloet, former senior executive

vice president and chief operating officer of

NewEdge Financial, a clearing member of CME

Group. “Regulators should ask the question,

‘Would a single, horizontal model bring develop-

ments like SPAN?’”

He acknowledges that it would be difficult

for newcomer exchanges to duplicate CME

Group’s operational excellence and product inno-

vation. “A‘me too’ effort won’t create a competi-

tive model,” he says.“But there is room to create

something better.”

The issue of global competition

Competition in futures is now global, and the

global trend is toward increased vertical clearing,

Donohue pointed out. Some 70 percent of all

futures and options contracts traded globally are

cleared through exchange-owned or controlled

clearing facilities. However, looking at derivatives

volumes worldwide, only about 17 percent of

derivatives trading is transacted on an exchange,

a percentage dwarfed by the 83 percent of trad-

ing done in the OTC derivatives market.

In Europe, Liffe is renegotiating its contract

with LCH.Clearnet in order to manage its own

clearing house and compete on a more level play-

ing field with CME Group and Eurex. In a letter to

the Financial Times, Liffe’s Chief Executive Hugh

Freedberg said, “The vast majority of derivatives

exchanges in the world also operate their own

clearing services… If Liffe is not able freely to

choose its clearing solution, it would not be able

to compete on a level playing field and would be

at a competitive disadvantage.”

At least two futures regulators share the

view that the current structure does not need

SPRING 2008

to be replaced. Walter Lukken, acting chair-

man of the Commodity Futures Trading

Commission (CFTC), said the CFTC is “confi-

dent that the U.S. futures exchanges and

clearing houses are functioning well, espe-

cially during these turbulent economic

times.” CFTC Commissioner Bart Chilton also

released a statement questioning the

Department of Justice’s (DOJ) judgment and

Q: What about the charge that CME Grou

become so powerful that it now inhibit

exchanges from starting up?

A: Other exchanges are starting all the tim

no dearth of clearing services provid

choose from. The IntercontinentalExc

(ICE) is a very good example of a successf

entrant. ICE used an available clearing p

for a while and then decided to support i

product innovations with its own market m

They’ve already done it in the United Stat

are now seeking an exchange-owned c

model in Europe. Another new exchange

hasn’t announced a clearer yet, but they

number of choices. There is no compelli

dence that clearing makes or breaks succ

entering a market.What is important in a

ing people to use a less liquid market is th

need to offer them some added benefit.

who have added electronic access to a h

cally non-electronic market have been su

ful in competing against established liquid

Q: Which clearing model is more conswith the Commodity Futures Moderni

Act of 2000?

A: The CFTC is pretty clear in the way it

ates – it is open to competition in the mar

regulates. The U.S. futures industry is pr

the easiest market to enter with either

exchange vehicle or a new clearing vehic

clearing structure can be efficient and p

appropriate risk management.But each cl

structure is optimized for a slightly differe

of participants.

Q: What are the potential dangers of a reg

imposing a clearing model on the industr

A: A regulator-mandated structure could

tially create a system that is less responschanges in market conditions. Depending

ownership, a utility model’s only goal may

keep transaction costs down. Transaction

consist of the fees and the spread. So

exchange charges “lower”fees, but lacks l

ty so spreads are wide, the end users’

transaction costs will actually go up.

We believe in a market-driven so

which allows more than one type of cl

model, as opposed to a solution man

by regulators.

Q: Which solution really benefits the end user

of the markets: the “vertical”exchange-owned

central counterparty clearing model (i.e., CME

Clearing) or the “horizontal” utility model?

A: A vertical model gives end users access to a

pool of liquidity where they can trade at the

best price. But it also provides them with

access to innovation in products.

In the horizontal model, the clearing mem-

bers own the clearing house. That model is

aligned to benefit just that group, rather than

all end users. In contrast, CME Group – and

CME Clearing – is publicly owned by a wide

variety of different investors. Vertical models

focus on several areas: supporting innovation,

bringing new products to market quickly,deliv-

ering cost efficiencies through low clearing

fees and/or rebates for intermediaries, and

enhancing operational efficiencies that allow

clearing members to connect with the lowestcost. In contrast, horizontal models focus

solely on the last two.

Some people define competition very nar-

rowly as the ability of different trading vehicles

offering the same products to compete solely

on the fees they charge. We define competition

much more broadly: there is competition

among different service models and among

clearing houses for the right to provide services

to various markets. This type of competition

benefits the end users of the market, rather

than only benefiting the clearing members.

timing of its February 2008 letter to t

Treasury, calling for a change in c

structure. “The business model that t

staff is now condemning received, on

short months ago, the legal blessing

following its extensive, comprehensi

exhaustive review of the CME/CBOT m

The CFTC considers itself “market-n

regarding clearing structure.

KIM TAYLOR, PRESIDENT, CME CLEARING

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 30/4430 CME GROUP MAGAZINE

TWOLEGACIES

UNDERONEROOF

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 31/44SPRING 2008

MAY 19 MARKED A NEW MILESTONE AT THE HISTORIC TRADING FLOOR

IN THE CHICAGO BOARD OF TRADE BUILDING AT LASALLE STREET AND

JACKSON BOULEVARD IN CHICAGO. FOR THE FIRST TIME IN MORE THAN

100 YEARS, ALL CHICAGO-BASED FUTURES PITS ARE UNDER A SINGLE ROOF.

The integration of the Chicago Mercantile

Exchange (CME) and Chicago Board of Trade

(CBOT) trading floors to a single location at 141

W. Jackson Blvd. was the natural outcome of

the exchanges’historic merger in mid-2007,

which promised greater efficiencies to the

exchanges and market participants alike. It also

marks the first time that traders can see (and

hear) trading on the entire yield curve, as well

as on all the major equity index contracts.

“Bringing together all the open outcry

markets under one roof has created new cross-

product trading opportunities and enabled the

trading firms to be more flexible and efficient inassigning personnel and resources,” says Bryan

Durkin, managing director and chief operating

officer of CME Group.“We also believe our

exchange can better address the needs of

market participants by focusing resources on

a single location.”

PLANNING THE MOVE

Bringing all the floor traders under one roof

required a level of planning worthy of a military

operation. Detailed discussions began as soon

as the CME-CBOT merger was completed in

July 2007. CME Group developed a list of the

areas that would be consolidated and

designated a team of lead managers from bothCBOT and CME to manage the policy,

procedure and physical changes in each area.

A subcommittee of board members – Chris

Stewart, Howard Siegel, Bill Salatich, Gary

Katler,Marty Gepsman and Bob Corvino –

acted as a conduit for communication between

the floor population, management and the

board. This strong emphasis on ongoing dialog

enabled management and the board to b

more sensitive to end users’ needs and

concerns about change.

Developing a methodical plan and

disciplined timelines for each area requ

more time up front, but saved time as t

transition gathered steam. The teams

developed a process to identify and sol

potential roadblocks, resulting in many

issues being solved almost as soon as t

were identified.

The scope of the project was vast, a

upon the technology integration simulta

under way.The trading floor needed toaccommodate 45 different class A firms

2,500 additional traders, clerks, brokers

others moving over from the CME locati

a mile away at 20 S.Wacker Drive. Physi

changes ranged from subtle to substant

Almost all the CBOTfinancial trading pit

to be moved to a greater or lesser degre

make room for the CME-traded products

Booths were built or reassigned. A comp

new wallboard system was mounted.

Thousands of new phone and data lines

installed so that CME phone numbers co

transferred to the CBOT location betwee

trading day and the next. No detail was t

small to note – for example, traders tryintheir new pit for the first time pulled out

tape measure to verify that one step was

inches shallower than in the old pit.

As part of the project, CME Group t

also helped evaluate technologies being

on the CME and CBOTtrading floors. Th

was to identify the most user-friendly, ro

and scalable platforms for use on the

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 32/4432

AT YOUR SERVICE

consolidated trading floor. Once decisions

were made on which technologies to adopt,

the trading floor operations staff trained floor

personnel on technology that was new to

them. For example, CME traders learned the

CBOT electronic order routing system and

CBOT traders were trained on CMEhandhelds. From January through early

March, about 100 employees also were

trained on a new price reporting system.

ALL IN A WEEKEND’S WORK

The actual move took place over three

weekends. The CME equity complex relocated

over the first weekend in April and began full

operation at the CBOT’s historic art deco

building on Monday,April 7. The foreign

exchange (FX) and interest rate complexes

moved over the last weekend in April and

began operation in their new home on

Monday, April 28.Finally, the commodity

complex made its transition over the third

weekend in May, starting to trade at 141 W.

Jackson on Monday, May 19.

“We held a series of mock trading sessions

that were designed to identify potential issues

prior to live trading on Day one,” says Julie

Holzrichter, managing director of operations

for CME Group.“Our expectations and

planning were validated through the process

CME GROUP MAGAZINE

as we received positive feedback from our

customers. That’s a testimony to the hard work

of hundreds of people – especially the

operations staff, project managers, technology

team members and construction crews.”

In conjunction with the trading floor

consolidation, the CME Globex Learning Centerwill move this summer from 20 S. Wacker to 141

W. Jackson. The newly renamed Trading

Knowledge Center will be located on the

mezzanine level of the Van Buren Street

entrance. The 1,500-square-foot center will

enable market participants to learn the basics

of electronic trading in a simulated

environment using CME Group workstations,

trading and charting software from various

independent software vendors (ISVs), and real-

time news and data feeds. The center also will

provide access to industry periodicals, books,

journals and various seminars.

‘NEW’ FLOOR HIGHLIGHTS

More than 3.3 million contracts per day traded

via open outcry in the first quarter of 2008,

making the consolidated CME Group trading

floor a very busy place.“There’s a different

‘vibe’ when everyone is on the same floor,”

Holzrichter notes.

S&P futures and options are now

positioned in the northwest section of the

integrated trading floor,adjacent to the

futures and options. FX futures and optio

to the northeast, with Eurodollar contrac

the southeast. The agricultural complex

accommodated in the southwest quadra

an adjacent room. Nearly 1,500 booths r

trading floor. Media cameras will continucapture the activity and roar of the floor

platform overlooking the S&P pits and o

opposite side of the floor overlooking the

Eurodollar futures pit.

“Coming together on one trading flo

hugely historical moment for our institut

says Durkin.“But it also shows how dyna

and resilient our markets are. We integra

CME Group trading floor in a way that wa

largely transparent to end users, thanks

of forethought, confidence, and ability to

manage dozens of operational and techn

issues. I’m very pleased and proud of ev

who made it happen, from our members

market reporters.”

“We’ve been so busy with the hubb

the integration that I think it will take the

year for us to truly realize its significanc

maybe, when we see cross-trading evolv

that Dow traders routinely spread again

S&P contracts and Eurodollar traders a

Treasury contracts. There is a lot of

opportunity here.”

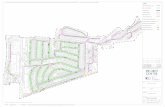

EQUITIES TREASURIES

FX

INTEREST RATESCME AGRICULTURE

FINANCIAL ROOM

FOR THE FIRST TIME IN

CENTURY, ALL CHICAGOFUTURES TRADE UNDER

SAME ROOF. NOW TRADCAN SEE, HEAR AND REA

TO TRADING ACROSS TH

ENTIRE YIELD CURVE ANALL THE MAJOR EQUITY

CONTRACTS, FOR EXAM

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 33/44

Not your grandfather’s

exchange anymore...

www.mgex.com

Side-by-side

Futures and Options

on CME Globex®

Financially Se

Agricultura

Index Produ

Remote Clearing

and Innovative

Market Solutions

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 34/4434 CME GROUP MAGAZINE

CMESWAPS ONSWAPSTREAM

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 35/44SPRING 2008

EFFICIENTANDEFFECTIVE

7/29/2019 Cmemagazine Sp 08

http://slidepdf.com/reader/full/cmemagazine-sp-08 36/44