Click to edit Master title stylebreport.myiris.com/PRALILLA/UTIBANK_20150102.pdf · ·...

104

India Financials Gradual recovery to unfold – Prefer stock specific approach Nitin Kumar [email protected] +91-22-66322236 Pritesh Bumb [email protected] +91-22-66322232 Click to edit Master title style Lilladher Prabhudas January 2015 Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision. Please refer to important disclosures and disclaimers at the end of the report.

Transcript of Click to edit Master title stylebreport.myiris.com/PRALILLA/UTIBANK_20150102.pdf · ·...

India Financials

Gradual recovery to unfold – Prefer stock specific approach

Nitin Kumar [email protected]

+91-22-66322236

Pritesh Bumb

[email protected] +91-22-66322232

Click to edit Master title style LilladherPrabhudas January 2015

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report.

LilladherPrabhudas Contents

1/2/2015 2

Page No.

Companies

Axis Bank 47

HDFC Bank 50

ICICI Bank 53

IndusInd Bank 56

Kotak Mahindra Bank 59

YES Bank 62

Bank of Baroda 65

Bank of India 68

Punjab National Bank 71

State Bank of India 74

Union Bank of India 77

Federal Bank 80

Jammu & Kashmir Bank 83

South Indian Bank 86

HDFC 89

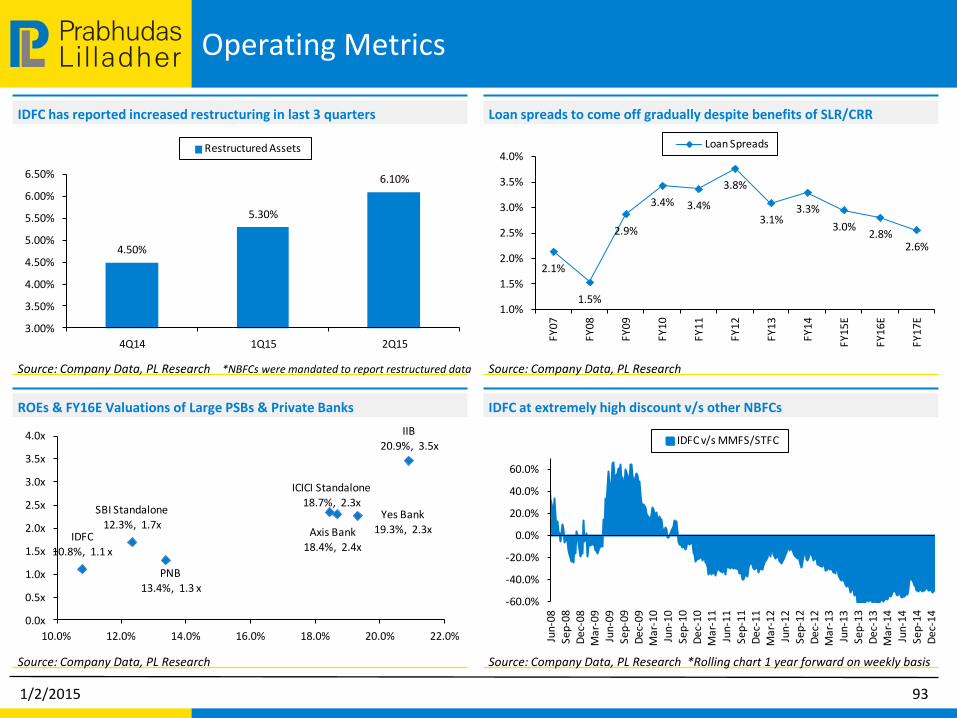

IDFC 92

LIC Housing Finance 95

M&M Financial Services 98

Shriram Transport Finance Company 101

Page No.

Gradual recovery to unfold – Prefer stock specific approach 3

Investment Summary 4

Top-Down Strategy 5

Our key stock ideas 6

Key changes in our earnings estimates 7

PL v/s Consensus estimates 8-9

Macros – Some improvement at the margin 11-13

Rating agency actions – Upgrades trend is firming up 14

Sectoral Deployment of Credit has been overall weak 15-16

GDP multiplier has come-off – revival in industrial growth a must 17-18

Treasury gains – Could now move in bank’s favour 19-20

Net Interest Margins - Fixed rate books to be better placed 21-22

Fees – Slowdown everywhere, we expect a gradual recovery 23

Regulations:- RBI maintains its accommodative stance 24

Capital - Basel III concerns only on some PSU banks ! 25-26

Pension Standardization – Near-term & Long-term impact 27-28

Asset Quality Cycle – Conservative on improvement v/s Last Cycle 29-33

Credit cycle Analysis - Corporate leverage & Interest coverage 34-37

Restructuring Monitor 38-42

Sensitivity Analysis - Loan Growth & Credit Cost effect to target price 43-44

Appendix

Fund & Non-fund based bank exposures 45

(Prices as on January 01, 2015)

LilladherPrabhudas Gradual recovery to unfold – prefer stock specific approach

• Bank nifty has outperformed the market by ~10% over past six months. While we remain constructive on the sector, we believe that further stock movement would depend more on on-ground recovery rather than pure optimism.

• We expect economic recovery to be fairly gradual unlike the previous up-cycle (2005-2008) when the domestic recovery coincided with a period of strong global growth. We expect GDP growth to average ~6.25% over next two years unlike 8.9% average growth between 2005-2008.

• We thus estimate credit cost to improve by ~25bp each over next two years for SOE banks and estimate earnings CAGR of ~24% for the sector aided by improved performance of PSU banks, against a low base. We note that despite this strong earnings traction the RoAs of most PSU banks (except SBI & PNB) would remain around 0.7% and would be significantly lower than previous up-cycles.

• With significant decline in G-sec and corporate bond yields the prospects of treasury gains has improved. However the total quantum of such treasury gains will be small in comparison to the gains made in previous rate easing cycles (please refer slide 20 for details).

• We believe that revival in industrial growth is the key for any sustained improvement in credit growth. Our analysis shows that credit growth to nominal GDP multiplier is most levered to industrial growth. We estimate credit growth to improve to 15% in FY16E as which corresponds to credit growth to nominal GDP multiplier of 1.5x (1.3x average over past four years).

• Our sensitivity analysis indicates that any sharper than expected turnaround in economy would result in ~15% rise in our PTs. We note that this is not a blue sky scenario but a possible outcome if the macro scenario were to improve at a rate, slightly better than expected.

• Stock ideas: We prefer ICICIBC/HDFCB among large private banks; SHTF/LICHF/HDFC amongst NBFCs, SBI/BOB amongst PSUs and Federal bank among small caps. MMFS/PNB are key avoids.

1/2/2015 3

LilladherPrabhudas Investment Summary

• Macros improving at the margin but we expect only a gradual recovery in GDP growth: PPOP growth has been slowing for all banks including private names and we do not expect trend to reverse sharply over next 1-2 qtrs.

• Rate Cycle: We expect a calibrated easing in rate cycle from 4Q FY15 onwards however extent of bond gains will be much lower than the previous cycles. BOI, CBK, PNB are better placed amongst large banks to benefit from decline in bond yields.

• Credit cycle – Industrial growth is the key; modest uptick expected for FY16: We expect modest uptick in credit growth in FY16E as the credit growth to nominal GDP multiple is most levered to industrial growth, which is likely to improve only gradually. Also, some acts of de-leveraging and credit substitution will likely affect overall growth.

• Our revised PTs are based on Sep-16 book and some higher multiple factoring in potential improvement in economic growth/investment cycle. We prefer ICICIBC/HDFCB among large private banks; SHTF/LICHF/HDFC amongst NBFCs, SBI/BOB amongst SOE banks and Federal bank among midcap banks. MMFS/PNB are key avoids.

1/2/2015 4

India Financials – Sector Valuations - ICICI/HDFCB top private picks; SBI/BOB top PSU banks and Federal in Midcap banks

Source: Bloomberg, Company Data, PL Research estimates

LilladherPrabhudas Top-Down Strategy

• Credit growth to improve gradually; industrial growth revival is the key: Credit growth trends continue to remain sluggish despite robust agriculture (20% YoY) and retail loan growth. Muted trends in capex activity, reduced cost of hedged overseas borrowings and moderation in working capital requirements (steep fall in commodity prices) has affected the industrial credit growth. We estimate ~15% credit growth for FY16E factoring in some improvement in industrial/Infra off take.

• PPOP growth to revive; margins are close to peaking out for large private banks: With gradual revival in loan/fee growth we expect PPOP growth to improve for the sector. NII growth will likely follow loan growth as margins have likely peaked out (NIMs for HDFC Bank and Axis Bank are at multiyear peak) while IIB and YES may report margin expansion going forward. PSU banks PPOP growth to also recover aided by bond gains but we do not expect core PPOP/assets to recover meaningfully.

• Credit cycle - No easy fix this time; relapse risk from restructured portfolio remains a worry: We are finally seeing some acts of de-leveraging which is necessary to continue but we expect upgrade/recovery to take longer in this cycle than last one (domestic issues in this cycle v/s commodity related risks in the last one). Nearly ~50% of total restructuring via CDR route has happened in past two years which poses threat to asset quality going forward as these assets comes out of moratorium. On two-year lag basis the CDR failure rate has already increased to 44% on the basis of number of cases and 25% on amount-wise basis.

• Regulator continues with its supportive stance – positive for PSUs: RBI has been more accommodative off-late in banking regulations with recent relaxations in re-financing of Infra loans, pushing out dynamic provisioning, shift in BASEL III transition and payment reschedulement of existing infrastructure loans. Most of these relaxations have brought a large relief for PSU banks.

1/2/2015 5

LilladherPrabhudas Our key stock ideas

• Axis Bank (BUY): (+) Analysis indicates that risk in power/large corporate book is lower than perceived (+) CASA especially CA mobilization is best in class and to some extent under-appreciated (+) Valuations reasonable at 2.2x Sep-16 book. (-) PPOP growth has moderated significantly.

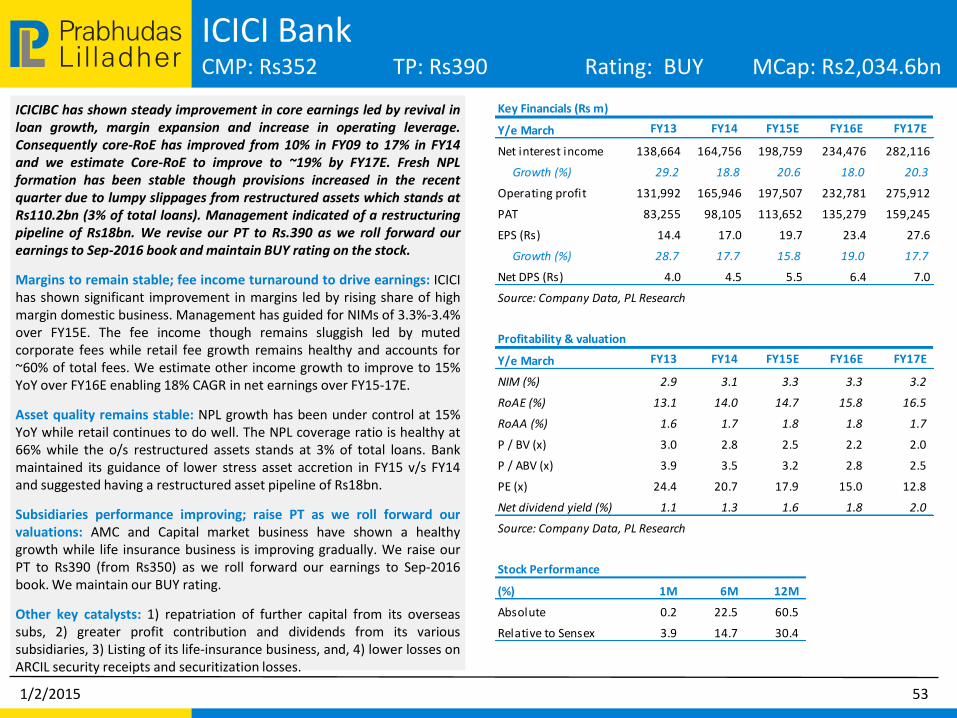

• ICICI Bank (BUY): (+) Like Axis, risk in power/large corporate book low especially in asset class with high loss given default (+) Retail SME portfolio stable despite significant stress. (+) Subsidiaries are gaining scale and their contribution to overall profitability is improving. (+) Relaxation in FDI limit in insurance is a positive trigger. (-) On a relative basis, asset quality risks appear high due to lumpy exposure (-) PPOP moderation to continue in spite of better fee growth expected as there is limited room for further margin expansion.

• HDFCB (BUY): (+) Best placed to overcome current slowdown – Both opex and credit cost flexibility high. (+) Fixed rate book to aid margins in 2H15 while benign earning base will help bank generate ~25% earnings CAGR over FY15-17E (+) Asset quality holding up (-) Slowing PAT growth and retail cycle may not remain as benign.

• Federal bank (BUY): (+) Stability in large corporate portfolio as well after steady performance on SME/Retail (+) Slower branch expansion to aid in cost optimization (+) Loan growth to improve after an year of consolidation while management’s focus on broad-basing fee income yields results (-) Growth still below par and hence leveraging up will take longer.

• PSU banks - Macro turning conducive – Prefer SBI & BOB on cleaner Balance sheet and BOI on valuations: (-) PPOP growth much worse than private banks (lower NIMs/ loan growth / pension costs worries). (+) Prospects of healthy treasury gains and gradual turnaround in asset quality. (-) Large corporate book riskier v/s private peers. (-) Under-provisioned B/S + limited P&L support in this credit cycle (low recoveries/upgrades) (-) Capital constraints. (+) Liability franchise + valuations (+) SBI better placed on pensions, project book and lower restructuring – Will outperform as slippages levels improve.

• Shriram/LICHF still preferred; Sell MMFS: (+) SHTF: Profitability has bottomed out – Initial signs of a pick up in loan growth while credit cost likely to inch lower in 2H15 (+) Margins likely to expand as funding cost has declined (+) Regulatory overhang on NPL recognition is now done away with – Recent up-move limits risk-reward though (2) LICHF: Will be beneficiary of lower rates in 2H15 + Reasonable valuations (3) MMFS: Growth and asset quality disappointment likely to continue – Valuations expensive while AUM growth is likely to remain muted in the near term.

1/2/2015 6

LilladherPrabhudas Key changes in our earnings estimates

1/2/2015 7

Change in earnings estimates

We estimate earnings CAGR of ~24% for private banks vs ~25% growth for PSU Banks. This will be led by gradual revival in loan growth and moderation in provisioning expenses (pls. see slide 32 for details) as we estimate margins to remain stable. NBFCs on other hand are estimated to deliver earnings CAGR of ~24% over FY15-17E.

FY15E FY16E FY15E FY16E FY15E FY16E FY15E FY16E FY15E FY16E FY15E FY16E

Private banks

Axis Bank 136,138 157,739 147,017 174,529 8% 11% 70,688 85,002 73,109 88,262 3% 4%

Federal Bank 23,712 27,178 23,712 27,178 0% 0% 9,564 11,495 9,564 11,495 0% 0%

HDFC Bank 223,407 265,252 221,146 275,981 -1% 4% 102,565 126,063 104,569 133,840 2% 6%

ICICI Bank 189,537 217,494 198,759 234,476 5% 8% 112,031 130,131 113,652 135,279 1% 4%

Indus Ind Bank 34,560 42,755 35,190 44,771 2% 5% 17,957 22,463 17,883 23,265 0% 4%

Yes Bank 33,471 41,714 35,527 45,289 6% 9% 19,275 24,089 19,683 24,089 2% 0%

KMB 53,276 62,980 53,276 62,980 0% 0% 26,663 31,982 26,663 31,982 0% 0%

ING Vysya 19,951 23,319 19,951 23,319 0% 0% 7,165 9,729 7,165 9,729 0% 0%

Federal Bank 23,712 27,178 23,712 27,178 0% 0% 9,564 11,495 9,564 11,495 0% 0%

SIB 16,335 18,935 16,335 18,935 0% 0% 5,549 6,603 5,549 6,603 0% 0%

SOE banks

Bank of Baroda 145,063 167,075 134,161 153,627 -8% -8% 52,209 64,908 51,883 60,628 -1% -7%

Bank of India 130,615 155,237 118,435 142,696 -9% -8% 28,922 40,299 30,909 41,466 7% 3%

Punjab Nat. Bank 172,196 200,240 174,993 205,226 2% 2% 40,723 56,044 41,314 54,009 1% -4%

State Bk of India 552,459 621,239 554,092 640,985 0% 3% 135,546 172,278 136,042 167,462 0% -3%

Union Bank 90,519 103,258 88,485 104,001 -2% 1% 19,375 26,384 23,280 28,831 20% 9%

NBFCs

HDFC 82,373 95,118 81,697 92,139 -1% -3% 63,920 74,046 59,314 66,899 -7% -10%

IDFC 26,434 27,949 26,434 27,949 0% 0% 17,259 19,884 17,259 19,884 0% 0%

LICHF 23,150 28,368 23,666 29,072 2% 2% 14,895 18,526 14,629 18,770 -2% 1%

MMFS 31,019 37,123 31,019 37,123 0% 0% 8,995 11,061 8,995 11,061 0% 0%

STFC 35,765 44,001 35,765 44,001 0% 0% 13,103 16,541 13,103 15,293 0% -8%

YoY Chng.PAT earlier PAT revised(Rs m)

NII earlier NII revised YoY Chng.

Source: Company Data, Bloomberg, PL Research estimates

LilladherPrabhudas PL v/s Consensus estimates

Source: Company data, Bloomberg, PL Research estimates

PL versus consensus EPS estimates

• Our earnings estimates for private banks are marginally higher than consensus, except for Kotak Bank where in we are 5% lower.

• We are significantly higher than consensus (>10%) in our earnings estimate for BOI and Union bank where in our implied FY15-FY17E earnings CAGR stand at 33% and 27% respectively.

• We note that despite this the FY17E RoA for BOI and UNBK would still remain modest at 0.68% and 0.67% respectively.

• Amongst NBFCs we are higher than consensus on LICHF where in we expect spreads to improve from low-base while lower provisioning requirement (aided by reversals) would keep a check on credit cost.

• We are also slightly lower than consensus on MMFS and SHTF where in we expect CV cycle to recover only gradually and the credit cost could swing sharply based on the decision management takes on compliance with the revised NBFC guidelines, recently published by the RBI.

1/2/2015 8

Consensus EPS PL EPS

Private banks

Axis Bank 36.7 37.7 2.9%

Federa l Bank 13.8 13.4 -2.9%

HDFC Bank 52.9 51.7 -2.3%

ICICI Bank 23.0 23.4 1.8%

Indus Ind Bank 43.0 44.5 3.5%

ING Vysya Bank 51.1 51.6 1.1%

J&K Bank 25.5 25.9 1.7%

Kotak Bank 29.3 27.8 -5.1%

South Indian Bank 4.6 4.9 5.4%

Yes Bank 58.1 58.5 0.6%

SOE banks

Bank of Baroda 148.6 138.7 -6.6%

Bank of India 61.3 67.6 10.2%

Punjab National Bank 155.3 149.1 -4.0%

SBI 23.5 22.3 -5.0%

Union Bank 39.8 48.7 22.5%

NBFCs

HDFC 46.4 44.4 -4.2%

IDFC 12.3 12.3 -0.2%

LICHF 35.2 37.1 5.3%

M&M Financia l Services 20.6 19.6 -4.9%

Shriram Transport Finance 76.3 73.5 -3.6%

% differenceFY16E

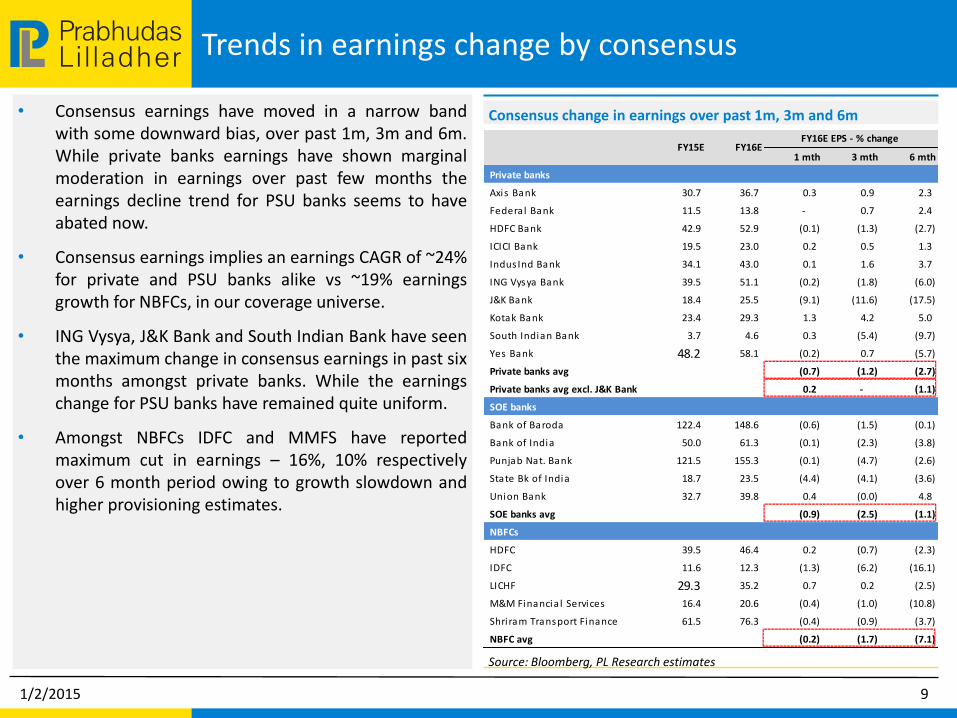

LilladherPrabhudas Trends in earnings change by consensus

Source: Bloomberg, PL Research estimates

Consensus change in earnings over past 1m, 3m and 6m

• Consensus earnings have moved in a narrow band with some downward bias, over past 1m, 3m and 6m. While private banks earnings have shown marginal moderation in earnings over past few months the earnings decline trend for PSU banks seems to have abated now.

• Consensus earnings implies an earnings CAGR of ~24% for private and PSU banks alike vs ~19% earnings growth for NBFCs, in our coverage universe.

• ING Vysya, J&K Bank and South Indian Bank have seen the maximum change in consensus earnings in past six months amongst private banks. While the earnings change for PSU banks have remained quite uniform.

• Amongst NBFCs IDFC and MMFS have reported maximum cut in earnings – 16%, 10% respectively over 6 month period owing to growth slowdown and higher provisioning estimates.

1/2/2015 9

1 mth 3 mth 6 mth

Private banks

Axis Bank 30.7 36.7 0.3 0.9 2.3

Federa l Bank 11.5 13.8 - 0.7 2.4

HDFC Bank 42.9 52.9 (0.1) (1.3) (2.7)

ICICI Bank 19.5 23.0 0.2 0.5 1.3

Indus Ind Bank 34.1 43.0 0.1 1.6 3.7

ING Vysya Bank 39.5 51.1 (0.2) (1.8) (6.0)

J&K Bank 18.4 25.5 (9.1) (11.6) (17.5)

Kotak Bank 23.4 29.3 1.3 4.2 5.0

South Indian Bank 3.7 4.6 0.3 (5.4) (9.7)

Yes Bank 48.2 58.1 (0.2) 0.7 (5.7)

Private banks avg (0.7) (1.2) (2.7)

Private banks avg excl. J&K Bank 0.2 - (1.1)

SOE banks

Bank of Baroda 122.4 148.6 (0.6) (1.5) (0.1)

Bank of India 50.0 61.3 (0.1) (2.3) (3.8)

Punjab Nat. Bank 121.5 155.3 (0.1) (4.7) (2.6)

State Bk of India 18.7 23.5 (4.4) (4.1) (3.6)

Union Bank 32.7 39.8 0.4 (0.0) 4.8

SOE banks avg (0.9) (2.5) (1.1)

NBFCs

HDFC 39.5 46.4 0.2 (0.7) (2.3)

IDFC 11.6 12.3 (1.3) (6.2) (16.1)

LICHF 29.3 35.2 0.7 0.2 (2.5)

M&M Financia l Services 16.4 20.6 (0.4) (1.0) (10.8)

Shri ram Transport Finance 61.5 76.3 (0.4) (0.9) (3.7)

NBFC avg (0.2) (1.7) (7.1)

FY15E FY16EFY16E EPS - % change

LilladherPrabhudas Stock performance of PL coverage universe

1/2/2015 10

Source: Bloomberg, PL Research

1M 3M 6M 12M 1M 3M 6M 12M

NIFTY 8,284 2.4% 4.1% 14.6% 36.0%

Private Banks

ICICI Bank 352 0.2% 23.3% 22.5% 60.5% -2.2% 19.1% 7.9% 24.5%

HDFC Bank 952 0.2% 9.7% 15.6% 43.1% -2.2% 5.5% 1.1% 7.1%

Axis Bank 503 2.8% 32.4% 31.0% 94.6% 0.4% 28.3% 16.4% 58.7%

Kotak Bank 1,259 4.7% 24.4% 42.3% 74.2% 2.3% 20.3% 27.7% 38.2%

Yes Bank 773 8.1% 38.6% 38.9% 106.3% 5.7% 34.4% 24.3% 70.3%

IIB 812 5.1% 34.9% 41.1% 91.8% 2.7% 30.8% 26.5% 55.8%

ING Vysya 870 5.1% 46.2% 30.6% 43.0% 2.7% 42.1% 16.0% 7.0%

J&K Bank 150 7.5% 7.8% -5.2% 4.7% 5.1% 3.6% -19.8% -31.3%

Federal 150 1.6% 21.3% 14.3% 73.9% -0.8% 17.2% -0.3% 37.9%

South Indian 29 6.6% 13.7% -8.7% 40.1% 4.2% 9.6% -23.2% 4.1%

SOE Banks

SBI 314 -1.8% 29.6% 17.2% 77.9% -4.1% 25.4% 2.6% 41.9%

PNB 220 1.7% 24.9% 10.2% 73.0% -0.7% 20.8% -4.4% 37.0%

BOB 1,083 0.0% 20.5% 23.3% 64.8% -2.4% 16.4% 8.7% 28.8%

BOI 304 6.5% 30.8% 0.0% 25.2% 4.1% 26.7% -14.6% -10.8%

Union 241 10.9% 26.5% 2.8% 83.9% 8.5% 22.3% -11.8% 48.0%

NBFCs

HDFC 1,124 -1.2% 7.0% 14.2% 41.7% -3.6% 2.9% -0.4% 5.7%

LICHF 438 3.8% 36.8% 35.5% 97.9% 1.4% 32.7% 21.0% 62.0%

STFC 1,102 -1.3% 21.1% 21.9% 64.0% -3.7% 16.9% 7.3% 28.0%

MMFS 330 8.0% 19.8% 15.5% 3.0% 5.6% 15.6% 1.0% -33.0%

IDFC 158 0.1% 15.8% 16.8% 43.8% -2.3% 11.7% 2.2% 7.8%

CoverageStock Performance (%) Relative Performance (%)CMP

(Rs)

LilladherPrabhudas Macros – Some improvement at the margin

Source: RBI, Company Data, PL Research

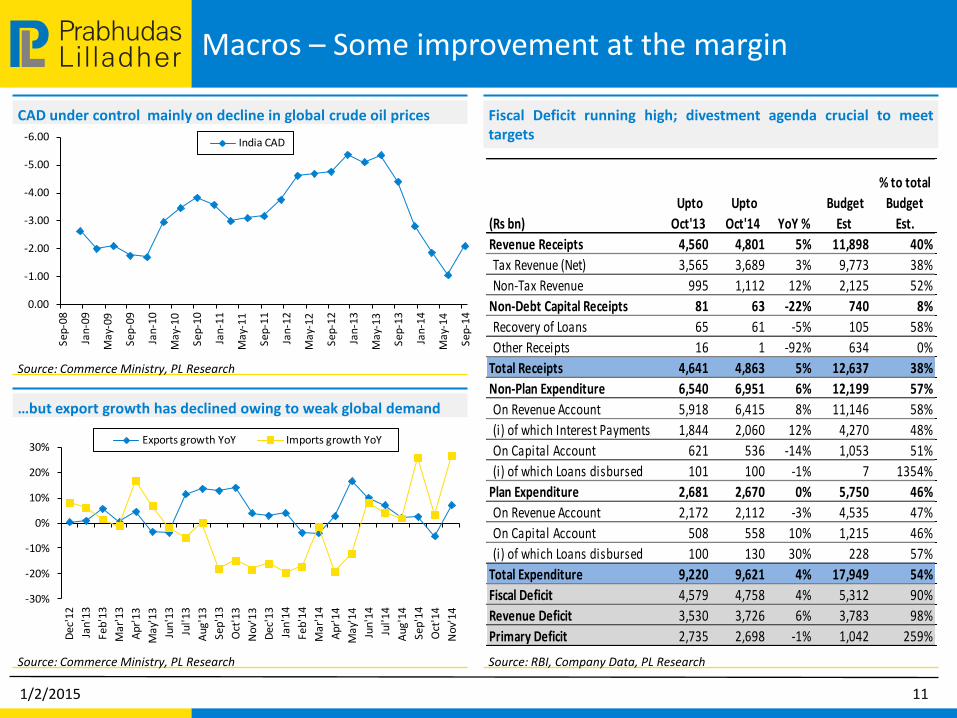

Fiscal Deficit running high; divestment agenda crucial to meet targets

Source: Commerce Ministry, PL Research

…but export growth has declined owing to weak global demand

Source: Commerce Ministry, PL Research

CAD under control mainly on decline in global crude oil prices

1/2/2015 11

(Rs bn)

Upto

Oct'13

Upto

Oct'14 YoY %

Budget

Est

% to total

Budget

Est.

Revenue Receipts 4,560 4,801 5% 11,898 40%

Tax Revenue (Net) 3,565 3,689 3% 9,773 38%

Non-Tax Revenue 995 1,112 12% 2,125 52%

Non-Debt Capital Receipts 81 63 -22% 740 8%

Recovery of Loans 65 61 -5% 105 58%

Other Receipts 16 1 -92% 634 0%

Total Receipts 4,641 4,863 5% 12,637 38%

Non-Plan Expenditure 6,540 6,951 6% 12,199 57%

On Revenue Account 5,918 6,415 8% 11,146 58%

(i) of which Interest Payments 1,844 2,060 12% 4,270 48%

On Capital Account 621 536 -14% 1,053 51%

(i) of which Loans disbursed 101 100 -1% 7 1354%

Plan Expenditure 2,681 2,670 0% 5,750 46%

On Revenue Account 2,172 2,112 -3% 4,535 47%

On Capital Account 508 558 10% 1,215 46%

(i) of which Loans disbursed 100 130 30% 228 57%

Total Expenditure 9,220 9,621 4% 17,949 54%

Fiscal Deficit 4,579 4,758 4% 5,312 90%

Revenue Deficit 3,530 3,726 6% 3,783 98%

Primary Deficit 2,735 2,698 -1% 1,042 259%

-30%

-20%

-10%

0%

10%

20%

30%

Dec

'12

Jan'

13

Feb'

13

Mar

'13

Apr

'13

May

'13

Jun'

13

Jul'

13

Aug

'13

Sep'

13

Oct

'13

Nov

'13

Dec

'13

Jan'

14

Feb'

14

Mar

'14

Apr

'14

May

'14

Jun'

14

Jul'

14

Aug

'14

Sep'

14

Oct

'14

Nov

'14

Exports growth YoY Imports growth YoY

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Se

p-1

1

Jan

-12

Ma

y-1

2

Se

p-1

2

Jan

-13

Ma

y-1

3

Se

p-1

3

Jan

-14

May

-14

Sep

-14

India CAD

LilladherPrabhudas Macros – hopes pinned on FY16 now

Source: Finance ministry, Bloomberg, PL Research

Source: CSO, PL Research

Fiscal deficit has already reached ~90% of the budgeted levels

IIP has been weak after showing initial signs of pick up

Source: Bloomberg, PL Research

GDP growth bounces; RBI keeps growth estimate unchanged

Source: Finance Ministry, RBI, PL Research

Tax collection trails estimates on sluggish economic recovery

1/2/2015 12

0%

5%

10%

15%

20%

25%

Tax Direct tax Indirect tax Receipts

Budgeted Actual

8.28.7

9.6

7.67

6.55.8

4.5 4.6 4.4 4.4 4.75.2

4.6 4.65.7 5.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Sep

-10

Dec

-10

Ma

r-1

1

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

De

c-1

3

Mar

-14

Jun-

14

Sep

-14

(%)

India GDP

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Mar

-13

Apr

-13

May

-13

Jun

-13

Jul-

13

Aug

-13

Se

p-1

3

Oct

-13

No

v-1

3

De

c-1

3

Jan

-14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun

-14

Jul-

14

Aug

-14

Sep

-14

Oct

-14

Overall IIP Mfg. IIP

FY15 4 yr Avg. FY14 FY13 FY12 FY11

Apr 21.4 15.3 18.4 13.7 14.5 14.5

May 45.3 29.2 35.6 28.9 25.3 27

Jun 56.1 33.2 51.7 38.9 31.5 10.8

Jul 61.2 47.4 67 54 44.3 24.3

Aug 74.9 60.5 79.6 68.9 53 40.5

Sep 82.6 60.0 81.1 68.8 54.4 35.7

Oct 89.6 67.1 90.1 75.1 59.5 43.5

Nov 75.7 100.3 84.3 68.4 49.9

Dec 76.8 101.6 86 73.8 45.8

Jan 85.8 104.9 94.7 84.2 59.5

Feb 98.2 117.9 105.7 95.6 73.6

Mar 100 100 100 100 100

LilladherPrabhudas Macros – Expect some monetary easing in 2H15

Source: RBI, PL Research

Source: Bloomberg, PL Research

CPI has moved down on base effect; on track with RBI projections

Corporate yields has dropped sharply on better liquidity conditions

Source: RBI, Bloomberg, PL Research

Liquidity conditions eased; excess liquidity being drained by OMOs

Source: RBI, PL Research

Limited hikes in MSP to help keep food inflation under control

1/2/2015 13

0

5

10

15

20

25

30

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MSP (WPI weighted, % YoY)

(2,000)

(1,500)

(1,000)

(500)

-

500

Nov

-12

Dec

-12

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3M

ay-1

3Ju

n-1

3Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4M

ay-

14

Jun-

14

Jul-

14A

ug-1

4Se

p-1

4O

ct-1

4N

ov-

14

Dec

-14

(Rs

bn)

LAF MSF ECR/Sp Repo Term Repo

10.810.910.4

9.4 9.39.9 9.6 9.5

9.810.2

11.2

9.9

8.8

8.0 8.3 8.68.3

7.58.0 7.7

6.5

5.5

4.3

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

Jan

-13

Fe

b-1

3

Mar

-13

Ap

r-1

3

May

-13

Jun-

13

Jul-

13

Aug

-13

Se

p-1

3

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Fe

b-1

4

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

Se

p-1

4

Oct

-14

Nov

-14

Base effect playing its

way in CPI inflation

7.5

8.0

8.5

9.0

9.5

10.0

10.5

Jun

-11

Aug

-11

Oct

-11

Dec

-11

Fe

b-1

2

Apr

-12

Jun

-12

Aug

-12

Oct

-12

Dec

-12

Feb

-13

Apr

-13

Jun

-13

Aug

-13

Oct

-13

Dec

-13

Fe

b-1

4

Ap

r-1

4

Jun

-14

Aug

-14

Oct

-14

Dec

-14

FIMMDA 3 YR AAA FIMMDA 5 YR AAA

LilladherPrabhudas Rating agency actions – Upgrades trend is firming up

• Rating-action-ratio (ratio of rating upgrades plus affirmations to downgrades) has surpassed one for the first time in past four years.

• More importantly the rating downgrade rate has declined significantly during 2HFY14.

• Average corporate rating which has been drifting lower over past several years has stabilized, though still remains below investment grade as large number of smaller companies are getting rated at the bottom of the pyramid.

Source: CRISIL, PL Research

Source: CRISIL, PL Research

Rating transition stabilizes after successive deterioration over past yrs

…upgrade rate exceeded downgrades for the first time in past 3 years

Source: CRISIL, PL Research

Rating Action Ratio has crossed one as…

1/2/2015 14

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

AAA AA A BBB BB B C D

Mar-10 Mar-12 Mar-14 Sep-14

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

0%

2%

4%

6%

8%

10%

12%

14%

FY95

FY96

FY

97

FY98

FY99

FY

00

FY01

FY02

FY03

FY04

FY

05

FY06

FY07

FY

08

FY09

FY10

FY11

FY12

FY

13

FY14

1H15

IIP GDP RAR (RHS)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1H 0

9

2H

09

1H 1

0

2H 1

0

1H 1

1

2H

11

1H

12

2H 1

2

1H 1

3

2H 1

3

1H

14

2H 1

4

1H 1

5

Downgrade rate Upgrade rate

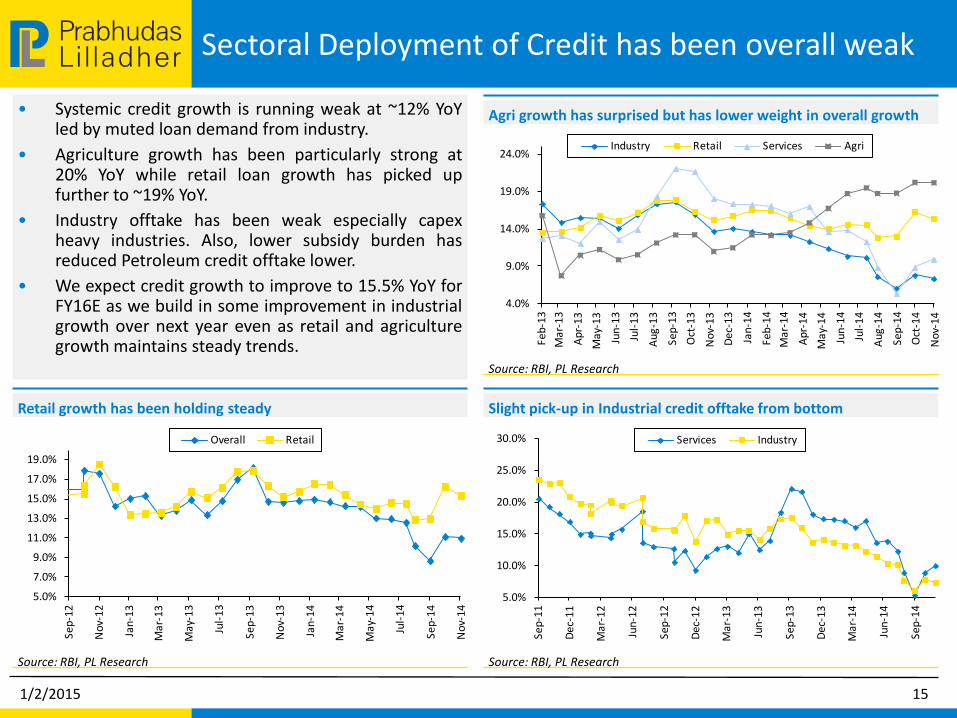

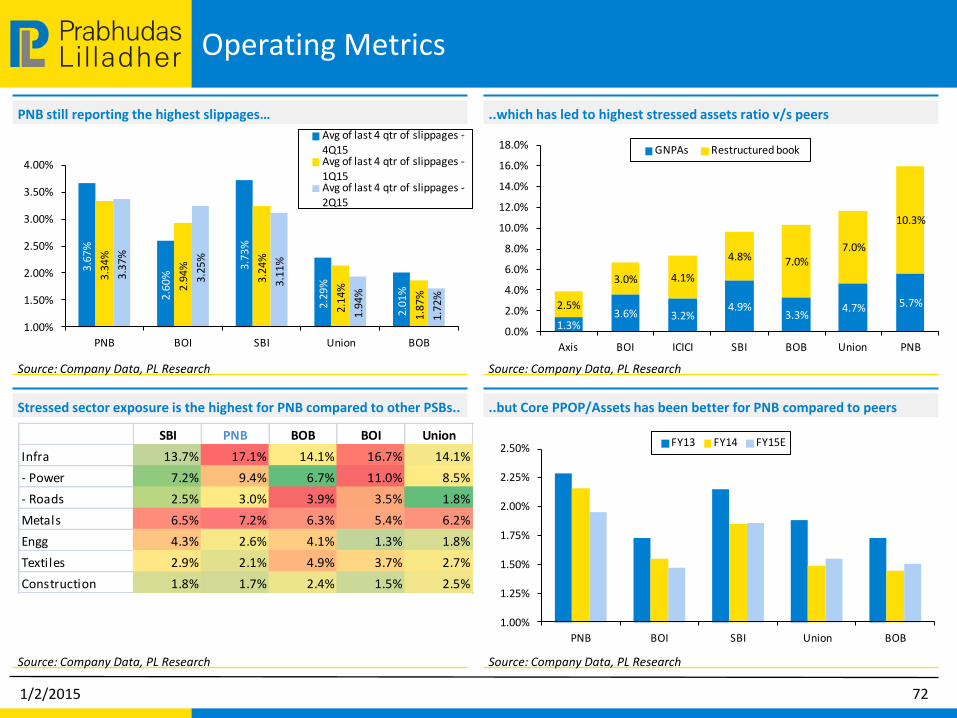

LilladherPrabhudas Sectoral Deployment of Credit has been overall weak

• Systemic credit growth is running weak at ~12% YoY led by muted loan demand from industry.

• Agriculture growth has been particularly strong at 20% YoY while retail loan growth has picked up further to ~19% YoY.

• Industry offtake has been weak especially capex heavy industries. Also, lower subsidy burden has reduced Petroleum credit offtake lower.

• We expect credit growth to improve to 15.5% YoY for FY16E as we build in some improvement in industrial growth over next year even as retail and agriculture growth maintains steady trends.

Source: RBI, PL Research

Source: RBI, PL Research

Agri growth has surprised but has lower weight in overall growth

Slight pick-up in Industrial credit offtake from bottom

Source: RBI, PL Research

Retail growth has been holding steady

1/2/2015 15

4.0%

9.0%

14.0%

19.0%

24.0%

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun

-14

Jul-

14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Industry Retail Services Agri

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

Sep

-12

Nov

-12

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

Nov

-13

Jan

-14

Ma

r-1

4

May

-14

Jul-

14

Se

p-1

4

Nov

-14

Overall Retail

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Ma

r-1

4

Jun-

14

Sep

-14

Services Industry

LilladherPrabhudas Sectoral Credit offtake – Industry offtake has been

extremely weak especially Capex heavy

Source: : RBI, PL Research

Source: RBI, PL Research

Industry growth has declined led by cement and metals segments

Vehicle loans pick up has slowed down after improving in Oct’14

Source: RBI , PL Research

Banks restraint in lending to power is witnessed in credit offtake

Source: : RBI, PL Research

Both Industry and non-infra industry growth has been subdued

1/2/2015 16

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan

-13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun

-14

Jul-

14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Industry Industry (Ex-Infra)

5%

10%

15%

20%

25%

30%

Feb

-13

Ma

r-1

3

Apr

-13

May

-13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Fe

b-1

4

Mar

-14

Apr

-14

May

-14

Jun

-14

Jul-

14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Cement Metals Textiles Capex heavy

10.0%

15.0%

20.0%

25.0%

30.0%

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun

-14

Jul-

14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Vehicle Loans Housing

5%

10%

15%

20%

25%

30%

35%

Feb

-13

Ma

r-1

3

Apr

-13

May

-13

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Fe

b-1

4

Mar

-14

Apr

-14

May

-14

Jun

-14

Jul-

14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Infra ex telecom Roads Power

LilladherPrabhudas Sector Outlook– Credit growth pick-up to remain

modest

Source: RBI, PL Research

15.5% credit growth in FY16: Factoring in some revival in economy

Source: Bloomberg, RBI, PL Research

Credit growth to GDP multiplier to increase as industrial growth picks-up

Source: Bloomberg, RBI, PL Research

Credit growth including CPs is a tad higher at ~11% – Gap with deposit growth though has narrowed

1/2/2015 17

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

Se

p-1

2O

ct-1

2N

ov-

12

Dec

-12

Jan

-13

Fe

b-1

3M

ar-1

3A

pr-1

3M

ay-…

Jun

-13

Jul-

13A

ug-1

3Se

p-1

3O

ct-1

3N

ov-1

3D

ec-

13

Jan

-14

Feb

-14

Ma

r-1

4

Apr

-14

Ma

y-…

Jun

-14

Jul-

14A

ug

-14

Sep

-14

Oct

-14

No

v-1

4D

ec-1

4

Adj Credit for CPs Credit growth

LilladherPrabhudas GDP multiplier has come-off – revival in industrial

growth a must for sustained recovery in credit growth

Source: Bloomberg, RBI, PL Research Estimates

GDP multiplier across GDP/credit growth segments • GDP multiplier is most levered to industrial growth followed by agriculture growth and services growth respectively.

• The gradual decline in credit growth to nominal GDP multiplier can be attributed to the falling share of agriculture segment in the total GDP mix and modest trend in industrial growth besides other extraneous factors (credit substitution, overseas borrowings, etc).

• We estimate credit growth to recover to 15.5% in FY16E as economic recovery takes hold while retail and agriculture segment continue to report steady trends.

• This corresponds to a credit growth to nominal GDP multiplier of 1.5x vs average of 1.3x over past four years.

1/2/2015 18

Agri GDP growth (%) Agri credit growth (%) Multiplier

2009 0% 24% 263.91

2010 1% 23% 28.24

2011 8% 16% 2.04

2012 4% 13% 3.64

2013 2% 8% 4.03

2014 5% 13% 2.81

3.1

Industry GDP growth (%) Industry credit growth (%) Multiplier

2009 4% 21% 4.71

2010 9% 24% 2.66

2011 9% 23% 2.51

2012 3% 20% 5.82

2013 2% 15% 7.17

2014 2% 13% 8.20

5.9

Services GDP growth (%)Retail + Services credit growth (%) Multiplier

2009 10% 15% 1.49

2010 11% 9% 0.82

2011 10% 21% 2.17

2012 8% 14% 1.67

2013 7% 13% 1.87

2014 7% 16% 2.26

2.0

Average of last four years

Average of last four years

Average of last four years

LilladherPrabhudas Treasury gains – Could now move in bank’s favour

• With significant decline in G-sec and corporate bond yields the prospects of treasury gains has improved for the banking sector.

• The RBI has also reduced the SLR limit to 22% owing to poor credit demand yet the bank’s SLR portfolio remains high at ~28% of total NDTL. This will enable banks to make higher treasury gains going forward as they move securities from HTM to AFS, particularly as RBI begins to ease rate cycle from Feb-2015, in our view.

• However the total quantum of such gains will be small in comparison to the gains made in previous rate easing cycles when investment book used to be ~45% of total assets.

Source: Company Data, PL Research

Source: Bloomberg, RBI, PL Research

Corporate Investment Book (As % of FY14 B/s)

Bank’s SLR portfolio remains well above the limit mandated by RBI

Source: Bloomberg, PL Research

G-Sec & Corp bond yields have softened by >55 bps each from last Quarter

1/2/2015 19

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Yes Axis Kotak ICICI Indusind HDFCB

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Jan

-91

Apr

-92

Jul-

93

Oct

-94

Jan

-96

Apr

-97

Jul-

98

Oct

-99

Jan

-01

Apr

-02

Jul-

03

Oct

-04

Jan

-06

Apr

-07

Jul-

08

Oct

-09

Jan

-11

Apr

-12

Jul-

13

Oct

-14

SLR limit Banks' SLR portfolio

Current 1month 3month 6month

Corporate Bond (%)

1Year 8.60 -0.04 -0.48 -0.38

3Year 8.62 -0.04 -0.61 -0.61

5Year 8.61 -0.07 -0.69 -0.69

10Year 8.55 -0.17 -0.76 -0.77

Govt. Securities

1Year 8.21 -0.11 -0.38 -0.32

5Year 7.99 -0.18 -0.53 -0.68

10Year 7.92 -0.25 -0.55 -0.86

Variation

LilladherPrabhudas Treasury gains – Could now move in bank’s favour

• We estimate that 50bp decline in bond-yields would enable banks to incur treasury gains varying between 5% to 21% of their FY15E PBT.

• Canara Bank, Oriental Bank of Commerce, Allahabad Bank, Corporation Bank are better placed to benefit from the decline in bond yields owing to higher AFS composition and the higher duration of their portfolio.

• Amongst private banks, Yes Bank is likely to benefit the most owing to much higher proportion of bonds/debentures in its investment portfolio.

1/2/2015 20

Source: Company Data, PL Research

Potential treasury gains arising from 50bp decline in bond yields

Source: Company Data, PL Research

But treasury gain potential is only ~10-15% of what PSUs had in the last cycle

Bank, (Rs m) SLR % AFS %M Duration

- AFS

Change in

portfolio yield

(%) - bp

Potential

bond gains

FY15E

PBT

As % of

FY15E PBT

Canara 84.7% 29.9% 3.8 50 8,372 40,438 20.7%

BOB 82.8% 23.9% 3.1 50 4,652 70,553 6.6%

BOI 86.3% 24.3% 3.8 50 5,409 39,083 13.8%

UNBK 76.1% 24.1% 3.5 50 3,839 26,910 14.3%

SBI 90.3% 22.3% 2.2 50 9,900 202,308 4.9%

PNB 82.0% 31.2% 3.5 50 7,786 57,145 13.6%

OBC 76.2% 23.7% 4.7 50 3,235 18,191 17.8%

Allahabad 79.0% 29.2% 3.4 50 2,888 16,735 17.3%

Corporation 77.6% 17.4% 3.9 50 2,171 12,076 18.0%

UCO Bank 80.6% 30.0% 3.0 50 2,960 21,365 13.9%

2002-05 Currently

Investments as % of assets 45% 28%

AFS (% of investments) 30-40% 25%

AFS duration 4-5 yrs 3-4 yrs

G-sec fall potential 3-4% 1-1.5%

Treasury gain potential (% of assets) 2.48% 0.30%

LilladherPrabhudas Net Interest Margins - Fixed rate books to be better

placed, but overall margins will remain stable • Corporate bond yields have eased significantly in past 3-4

months in anticipation of RBI easing expected from Q4FY15 onwards.

• Lower inflation, decline in funding cost and steady liquidity will enable banks to pass-on the benefits of lower rates to the borrowers unlike previous instances of policy easing effected by the RBI. We expect RBI to cut repo rate by 100bp over next one year, beginning Q4FY15.

• We expect NIMs to remain stable over FY16 (positive on YES, IIB) as banks focus on lowering their deposit cost before cutting base rates.

• Fixed rate asset books will benefit – Among banks HDFCB/KMB/IIB has high share of fixed rate book. SHTF/MMFS better placed among NBFCs,

Source: Bloomberg, PL Research

Source: Company Data, PL Research

CPI inflation moderating but above trend levels

Margins trends will remain mixed for Banks as loan mix changes

Source: Company Data, PL Research

Retail book - % of loans – Fixed rates books to benefit

1/2/2015 21

10.810.910.4

9.4 9.39.9 9.6 9.5

9.810.2

11.2

9.9

8.8

8.0 8.3 8.68.3

7.58.0 7.7

6.5

5.5

4.3

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

Jan

-13

Fe

b-1

3

Mar

-13

Ap

r-1

3

May

-13

Jun-

13

Jul-

13

Aug

-13

Se

p-1

3

Oct

-13

Nov

-13

Dec

-13

Jan

-14

Fe

b-1

4

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

Se

p-1

4

Oct

-14

Nov

-14

15% 16%

22%

8% 6%4% 5%

30%33%

4% 4%

21%

0%

10%

20%

30%

40%

50%

Axi

s

ICIC

I

HD

FCB

SB

I

PNB

BO

I

Uni

on

Ko

tak

IIB ING

SIB

Fede

ral

Retail Loans Share (ex-mortagage) NIM FY15E FY16E NIM FY15E FY16E

ICICI 3.27% 3.25% SBI 2.92% 2.90%

HDFCB 4.39% 4.47% PNB 3.06% 3.09%

Axis 3.62% 3.54% BOB 1.95% 1.94%

Kotak 4.65% 4.63% BOI 2.02% 2.06%

Yes 3.14% 3.35% Union 2.43% 2.54%

IIB 3.80% 3.86% HDFC 3.27% 3.18%

Federal 3.06% 3.01% LIC HF 2.10% 2.23%

ING 3.18% 3.18% STFC 6.75% 7.47%

J&K 3.49% 3.49% MMFSL 9.23% 9.52%

SIB 2.82% 2.80% IDFC 3.78% 3.68%

LilladherPrabhudas Margin trends – Large private banks expand margins

Source: Company Data, PL Research

Margin trend for banks

Source: Bloomberg, PL Research

While base rate has remained stable for most banks except AXSB

Source: Bloomberg, PL Research

Most banks have cut deposit rates, mostly at the shorter end…

1/2/2015 22

Cut in peak deposit rate 0-3M 3-9M 9-15M 15-36M >36M

HDFC Bank -0.50% -0.50% -0.25% 0.00% 0.00%

Axis Bank 0.00% 0.00% -0.10% 0.25% 0.25%

ICICI bank 0.00% 0.00% -0.25% -0.25% 0.00%

IndusInd bank 0.50% 1.00% -0.25% -0.25% 0.25%

Yes Bank 0.00% 0.00% 0.00% 0.00% 0.00%

SBI -0.50% 0.00% -0.25% -0.25% -0.25%

Bank of Baroda 0.00% -1.30% -0.35% -0.20% 0.00%

Bank of India -0.25% -0.25% -0.35% -0.15% -0.15%

Punjab National Bank 0.00% 0.00% 0.00% 0.00% -0.25%

Canara Bank -0.50% 0.25% 0.00% 0.00% -0.05%

Union Bank 0.25% 0.00% -0.05% -0.05% -0.45%

Banks 6 month change in base rate

HDFC Bank No change

Axis Bank -0.10%

ICICI bank No change

IndusInd bank No change

Yes Bank No change

SBI No change

Bank of Baroda No change

Bank of India No change

Punjab National Bank No change

Canara Bank No change

Union Bank No change

Margin trend (%) 2Q13 4Q13 2Q14 4Q14 2Q15 YoY chng. (bps)

Private Banks

AXSB IN 3.5% 3.7% 3.8% 3.9% 4.0% 0.5%

HDFCB IN 4.2% 4.5% 4.3% 4.4% 4.5% 0.3%

ICICIBC IN 3.0% 3.3% 3.3% 3.4% 3.4% 0.4%

IIB IN 3.3% 3.7% 3.7% 3.8% 3.6% 0.4%

YES IN 2.9% 3.0% 2.9% 3.0% 3.2% 0.3%

KMB IN 4.7% 4.7% 4.9% 4.9% 5.0% 0.3%

FB IN 3.6% 3.1% 3.3% 3.3% 3.4% -0.2%

JKBK IN 3.5% 3.7% 3.5% 3.7% 3.5% 0.1%

SIB IN 3.1% 3.2% 3.1% 3.0% 2.8% -0.3%

VYSB IN 3.5% 3.7% 3.5% 3.7% 3.5% 0.1%

SOE Banks

BOB IN 2.7% 2.5% 2.3% 2.3% 2.4% -0.3%

BOI IN 2.4% 2.5% 2.4% 2.3% 2.4% -0.1%

CBK IN 2.4% 2.4% 2.2% 2.3% 2.2% -0.1%

PNB IN 3.5% 3.5% 3.5% 3.2% 3.2% -0.3%

SBIN IN 3.3% 3.3% 3.2% 3.2% 3.1% -0.2%

UNBK IN 3.0% 2.9% 2.5% 2.6% 2.5% -0.5%

LilladherPrabhudas Fees – Slowdown everywhere, we expect a gradual

recovery

• Fee income remains tepid: Private banks have reported substantial moderation in fee income as corporate loan growth remains tepid. PSU banks on other hand have been lower impacted due to their lower dependence on off-balance sheet and corporate loan growth linked fee income.

• FX/ business banking/ Retail fees holding up: Large corporate/ non-fund based fee income remains weak while 3rd party distribution and capital market fee has shown improvement.

• We expect fee income trends to improve gradually over FY16-17E and estimate 12%-15% growth over next year.

Source: Company Data, PL Research

Source: Company Data, PL Research

Fee growth remains subdued for Pvt banks but picks up for PSBs

Core fee income growth display mixed trends among banks

Source: Company Data, PL Research

PSUs – typical fee income distribution

1/2/2015 23

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

Pvt Banks PSU Banks

Core fee gr (%) 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Axis 14.2% 6.6% 3.6% 10.0% 4.6% 30.0%

HDFCB 9.6% 28.4% 15.0% 12.0% 2.0% -5.3%

ICICIBC 8.9% 16.7% 12.8% 11.2% 8.0% 5.5%

IIB 30.7% 31.5% 29.6% 28.1% 38.4% 30.8%

Kotak 39.6% 11.6% 6.1% 19.0% 37.6% 51.4%

Yes 68.7% 41.8% 1.5% 19.4% 12.3% 37.0%

SBI -3.9% -0.2% 20.5% 17.6% 11.2% 29.4%

BOB 21.2% 26.8% 22.5% 10.5% 6.4% -29.1%

PNB -3.4% 13.8% 10.4% 17.9% 1.5% 5.0%

LilladherPrabhudas Regulations: RBI maintains its accommodative stance

• BASEL III Implementation : No impact for private banks but some PSU banks stretched – Recent 1 yr extension given to comply with capital conservation buffer will aid to lower capital raising need in FY15-16 for some PSU banks by 40-45% - This is a welcome relief considering current PSU bank valuations.

• Pension standardization norms: Near-term pain likely to continue for PSU banks but increase in provisioning in the last 2-3 years provides comfort on long-term shortfalls – Most banks except for BOI have moved on to new mortality table. Given that regulator seems more accommodative, PSU banks may be given time to comply with pension standardization norms. As per our analysis, SBI/PNB/Union is better provided on Pension. BOB is catching up but BOI’s pension provisioning remains the weakest.

• Dynamic provisions: Certain to be implemented but RBI to wait till the tide turns; Private banks to be little impacted.

• Re-financing of Infra loans: Apart from allowing a 2 yr COD push + one time restructuring, RBI has allowed re-financing of Infra loans with a longer moratorium even for the existing loans which are standard in the books at the time of reschedulement. While this is likely to reduce slippages in the near term we believe, forbearances given to Infra loans now is very high.

• 180 to 90 day NPA recognition for NBFCs: RBI stepped up the standard provisioning and reduced the NPA recognition timeline for NBFCs to 90 days from 180 days period currently. However ample time given to comply with the fresh norms will ensure that no disruption occurs.

• NBFC NCD regulations + Removal of Gold lending restrictions: Cap on retail NCD issuance will impact gold NBFCs to some extent but removal of LTV restrictions indicate regulator’s comfort on the asset class.

• Relaxation on Liquidity Coverage Ratio: RBI allowed banks to include a higher share (7% of NDTL, up from 2% earlier) of their SLR portfolio as part of HQLA which would help most banks to comfortably meet their near-term LCR requirement of 60%.

1/2/2015 24

LilladherPrabhudas Capital: Basel III concerns only on some PSU banks !

1/2/2015 25

Source: Company Data, PL Research

PSU banks – Better and Worst placed

Source: Company Data, PL Research

RBI’s BASEL – III requirements

LilladherPrabhudas Capital: Extension of timelines but time will start

running out if growth demand picks up

1/2/2015 26

LilladherPrabhudas Pension Standardization – Near-term impact

1/2/2015 27

LilladherPrabhudas Pensions standardization - Long-term impact

1/2/2015 28

LilladherPrabhudas Credit cycle : Macros disappointing v/s last cycle; pace

of recovery also looks modest

1/2/2015 29

Real GDP IIP WPI CPI

Global

GDP

Repo/

Rev. Repo SBI PLR

PSU Gross

NPAs

PSU Net

NPAs

PSU

Restrcuture

d book

Total

stresses

Assets

PSU Gross

Slippages

PSU Net

Slippages

1997 8.0% 6.1% 2.1% 7.3% 4.1% 15.0% 17.8% 9.2% 17.8%

1998 4.3% 6.6% 2.9% 13.2% 2.6% 14.0% 16.0% 8.2% 16.0%

1999 6.7% 4.1% 4.4% 4.8% 3.6% 13.0% 15.9% 8.1% 15.9%

2000 7.6% 6.6% 2.7% 4.0% 4.8% 9.1% 12.5% 14.0% 7.4% 14.0% 3.76%

2001 4.3% 4.9% 3.3% 3.8% 2.4% 9.0% 11.5% 12.4% 6.7% 12.4% 3.74%

2002 5.5% 2.8% 1.8% 4.3% 2.9% 8.0% 11.5% 11.1% 5.8% 11.1% 3.29% 1.27%

2003 4.0% 5.8% 2.6% 3.8% 3.7% 7.0% 10.8% 9.4% 4.5% 9.4% 2.95% 1.24%

2004 8.1% 7.0% 5.7% 3.8% 4.9% 6.0% 10.3% 7.8% 3.0% 7.8% 2.93% 1.34%

2005 7.0% 11.7% 6.3% 4.3% 4.6% 6.0% 10.3% 5.5% 2.0% 5.5% 2.08% 0.61%

2006 9.5% 8.6% 2.4% 5.8% 5.3% 6.5% 10.8% 3.6% 1.3% 3.6% 1.66% 0.37%

2007 9.6% 12.9% 5.7% 6.4% 5.4% 7.5% 12.3% 2.7% 1.1% 2.7% 1.51% 0.60%

2008 9.3% 15.5% 4.8% 8.3% 2.8% 7.8% 12.3% 2.2% 1.0% 1.3% 3.6% 1.47% 0.76%

2009 6.7% 2.5% 6.2% 10.8% -0.6% 5.0% 12.3% 2.0% 0.9% 3.0% 5.0% 1.53% 0.74%

2010 8.4% 5.3% 2.2% 12.1% 5.1% 5.0% 11.8% 2.2% 1.1% 4.8% 7.0% 1.79% 1.09%

2011 8.4% 8.2% 5.7% 8.9% 4.0% 6.8% 13.0% 2.2% 1.1% 4.4% 6.6% 1.91% 1.17%

2012 6.5% 6.4% 9.2% 9.3% 3.0% 8.5% 14.8% 2.9% 1.5% 6.2% 9.1% 2.52% 1.68%

2013 5.1% 1.1% 7.4% 10.9% 2.2% 7.5% 14.3% 3.6% 2.3% 7.7% 11.3% 3.00% 1.90%

2014 4.7% 0.0% 5.6% 7.5% 2.4% 8.0% 14.8% 4.4% 2.8% 7.7% 12.1% 3.20% 2.03%

2015E 5.7% 1.5% 1.5% 4.5% 2.8% 7.0% 13.8% 4.9% 2.9% 8.0% 12.9%

Source: Bloomberg, RBI, Company Data, PL Research

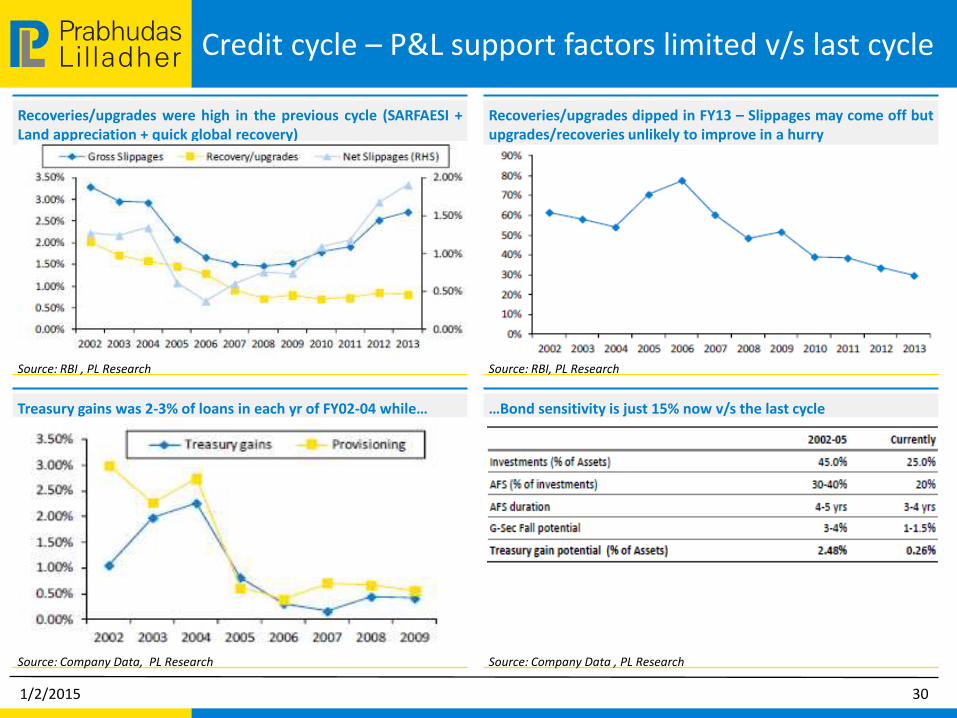

LilladherPrabhudas Credit cycle – P&L support factors limited v/s last cycle

Source: RBI, PL Research

Source: Company Data , PL Research

Recoveries/upgrades dipped in FY13 – Slippages may come off but upgrades/recoveries unlikely to improve in a hurry

…Bond sensitivity is just 15% now v/s the last cycle

Source: Company Data, PL Research

Treasury gains was 2-3% of loans in each yr of FY02-04 while…

Source: RBI , PL Research

Recoveries/upgrades were high in the previous cycle (SARFAESI + Land appreciation + quick global recovery)

1/2/2015 30

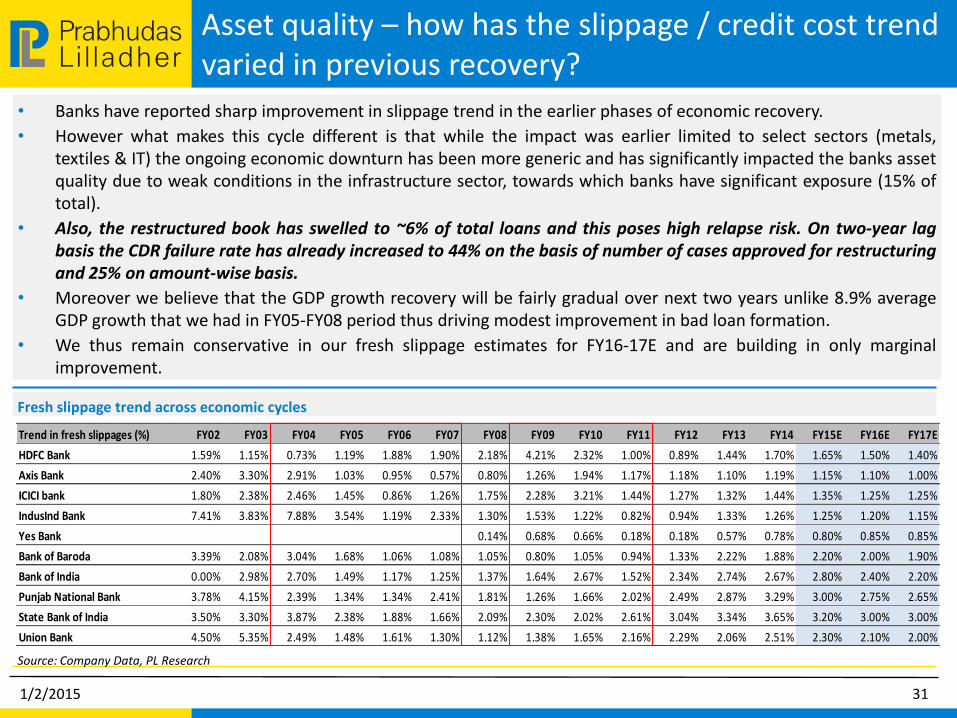

LilladherPrabhudas Asset quality – how has the slippage / credit cost trend

varied in previous recovery?

Source: Company Data, PL Research

Fresh slippage trend across economic cycles

• Banks have reported sharp improvement in slippage trend in the earlier phases of economic recovery.

• However what makes this cycle different is that while the impact was earlier limited to select sectors (metals, textiles & IT) the ongoing economic downturn has been more generic and has significantly impacted the banks asset quality due to weak conditions in the infrastructure sector, towards which banks have significant exposure (15% of total).

• Also, the restructured book has swelled to ~6% of total loans and this poses high relapse risk. On two-year lag basis the CDR failure rate has already increased to 44% on the basis of number of cases approved for restructuring and 25% on amount-wise basis.

• Moreover we believe that the GDP growth recovery will be fairly gradual over next two years unlike 8.9% average GDP growth that we had in FY05-FY08 period thus driving modest improvement in bad loan formation.

• We thus remain conservative in our fresh slippage estimates for FY16-17E and are building in only marginal improvement.

1/2/2015 31

Trend in fresh slippages (%) FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

HDFC Bank 1.59% 1.15% 0.73% 1.19% 1.88% 1.90% 2.18% 4.21% 2.32% 1.00% 0.89% 1.44% 1.70% 1.65% 1.50% 1.40%

Axis Bank 2.40% 3.30% 2.91% 1.03% 0.95% 0.57% 0.80% 1.26% 1.94% 1.17% 1.18% 1.10% 1.19% 1.15% 1.10% 1.00%

ICICI bank 1.80% 2.38% 2.46% 1.45% 0.86% 1.26% 1.75% 2.28% 3.21% 1.44% 1.27% 1.32% 1.44% 1.35% 1.25% 1.25%

IndusInd Bank 7.41% 3.83% 7.88% 3.54% 1.19% 2.33% 1.30% 1.53% 1.22% 0.82% 0.94% 1.33% 1.26% 1.25% 1.20% 1.15%

Yes Bank 0.14% 0.68% 0.66% 0.18% 0.18% 0.57% 0.78% 0.80% 0.85% 0.85%

Bank of Baroda 3.39% 2.08% 3.04% 1.68% 1.06% 1.08% 1.05% 0.80% 1.05% 0.94% 1.33% 2.22% 1.88% 2.20% 2.00% 1.90%

Bank of India 0.00% 2.98% 2.70% 1.49% 1.17% 1.25% 1.37% 1.64% 2.67% 1.52% 2.34% 2.74% 2.67% 2.80% 2.40% 2.20%

Punjab National Bank 3.78% 4.15% 2.39% 1.34% 1.34% 2.41% 1.81% 1.26% 1.66% 2.02% 2.49% 2.87% 3.29% 3.00% 2.75% 2.65%

State Bank of India 3.50% 3.30% 3.87% 2.38% 1.88% 1.66% 2.09% 2.30% 2.02% 2.61% 3.04% 3.34% 3.65% 3.20% 3.00% 3.00%

Union Bank 4.50% 5.35% 2.49% 1.48% 1.61% 1.30% 1.12% 1.38% 1.65% 2.16% 2.29% 2.06% 2.51% 2.30% 2.10% 2.00%

LilladherPrabhudas Asset quality – how has the slippage /credit cost trend

varied in previous recovery ?

Source: Company Data, PL Research

Stressed assets and restructuring pipeline

Source: Company Data, PL Research

Credit cost estimates and trend – we estimate modest improvement in credit cost for FY16/FY17E

1/2/2015 32

Banks Gross NPLs Net NPLs Std. restr. loans, Rs mn As % of o/s loans Net NPLs (%) Net stressed assets (%) Asset quality guidances

Private banks

AXSB 36,131 11,798 66,750 2.76 0.44 3.20 Guidance maintained at Rs65bn of fresh s tressed assets accretion

HDFCB 33,617 9,173 4,582 0.14 0.28 0.42 NA

ICICIBC 115,467 39,423 110,200 3.05 1.09 4.14 Stressed asset formation to be lower than FY15 excl . s l ippages from RA

KMB IN 11,654 6,809 1,615 0.26 0.84 1.10 Smal l restructuring in H2 FY15; asset qual i ty to remain s table

FB IN 10,311 3,185 29,000 5.98 0.66 6.64 Some fa l lout from restructuring can be there but keeping close monitor

SIB IN 5,532 3,184 17,480 4.94 0.90 5.84 NA

JKBK IN 21,869 11,085 12,693 2.73 2.46 5.19 1 NPA a/c could be upgraded; Flood restructuring package being implemented

SOE Banks

BOB IN 130,576 67,045 224,170 5.81 1.74 7.55 Sl ippages not to witness spikes above normal levels

BOI IN 141,260 90,047 117,380 3.03 2.29 5.32 Targeting GNPA of 3.15% & NNPAs of 2.0% from 3.6% & 2.3% currently

PNB IN 207,519 116,178 367,930 10.30 3.26 13.56 Rs10-12 bn of restructuring pipel ine in H2FY15

SBIN IN 607,124 329,972 439,620 3.44 2.73 6.17 Agri NPAs to trickle down gradual ly, Mid-corporate s tress has reduced

UNBK IN 109,825 62,717 126,030 5.06 2.71 7.77 Rs12-15 bn of restructuring pipel ine in H2FY15

Credit cost trend (%) FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

HDFC Bank 1.32% 1.50% 0.95% 1.21% 0.81% 1.58% 1.69% 1.86% 1.98% 1.73% 0.53% 0.61% 0.57% 0.60% 0.60% 0.60% 0.60%

Axis Bank 0.47% 3.75% 1.44% 2.94% 0.13% 0.67% 0.25% 0.71% 1.13% 1.46% 0.77% 0.55% 0.64% 0.61% 0.70% 0.70% 0.65%

ICICI bank 1.19% 1.01% 2.63% 0.67% 0.19% 0.67% 0.84% 1.21% 1.70% 2.18% 0.99% 0.42% 0.51% 0.90% 0.90% 0.85% 0.85%

IndusInd Bank 2.78% 3.29% 4.21% 2.54% 0.81% 0.99% 0.55% 0.51% 0.88% 0.72% 0.69% 0.47% 0.55% 0.63% 0.65% 0.65% 0.65%

Yes Bank 0.03% 0.38% 0.51% 0.13% 0.03% 0.34% 0.26% 0.65% 0.65% 0.60%

Bank of Baroda 2.94% 2.50% 2.74% 2.97% 1.62% 0.59% 0.59% 0.82% 0.34% 0.60% 0.52% 0.61% 1.00% 0.81% 0.75% 0.70% 0.70%

Bank of India 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 1.13% 0.55% 0.88% 1.38% 1.20% 1.00% 0.90% 0.90%

Punjab National Bank 1.29% 2.07% 2.23% 2.73% 0.31% 0.45% 0.70% 0.35% 0.60% 0.59% 0.93% 0.90% 1.11% 1.37% 1.30% 1.20% 1.15%

State Bank of India 1.35% 1.84% 2.01% 2.50% 0.67% 0.06% 0.48% 0.53% 0.52% 0.79% 1.27% 1.42% 1.11% 1.28% 1.18% 1.10% 1.05%

Union Bank 3.27% 2.36% 0.63% 0.33% 0.57% 0.69% 0.64% 0.65% 0.84% 0.92% 0.81% 0.96% 0.85% 0.80% 0.78%

LilladherPrabhudas PSBs in FY14 resorted to higher NPA sale to ARCs

• PSBs in FY14 resorted to heavy sale of NPAs to Asset Reconstruction Companies (ARCs) especially in the H2FY14 period.

• BOI/SBI/Canara/CBI have been the highest sellers of NPAs.

• BOI/SBI have received 50-60% consideration on assets sold, implying haircut of 40% on book value

• In H1FY15, PSBs had lower sale of NPAs v/s FY14 despite selling off two large accounts and was due to RBI’s change in norms for ARCs on participation and capital infusion to buyout assets. BOI continued to sell NPAs, while ICICI bank saw high NPA sale in H1.

1/2/2015 33

Source: Banks, Media Reports, PL Research

NPA sale of Banks to ARCs

% of

GNPAs

% of

Loans

Consideration

as per FY14 AR

2Q14 3Q14 4Q14 FY14 FY14 FY14 FY14 1Q15 2Q15 1H15

Yes Bank 1,300 600 120 2,020 115% 0.4% 1,953 - - -

I IB 250 240 350 840 14% 0.2% 1,002 500 - 500

ICICI - - - - 0% 0.0% 1,776 - 2,910 2,910

Federa l 1,860 1,580 3,440 32% 0.8% 3,081 1,400 - 1,400

BOI 3,130 17,440 23,430 44,000 37% 1.2% 26,286 17,640 1,060 18,700

Al lahabad bank 7,300 3,890 - 11,190 14% 0.8% 5,650 - - -

Indian Bank 10,610 - 10,610 23% 0.9% 9,409 - - -

SBI - - 32,500 32,500 5% 0.3% 16,049 5,566 - 5,566

UCO 9,250 9,250 14% 0.6% 10,463 - - -

IOB 9,830 9,830 11% 0.6% 10,151 - - -

UBI 3,250 3,250 5% 0.5% - - - -

BOM - 0% 0.0% 2,576 - - -

Syndicate - 0% 0.0% - - - -

OBC - - 5,300 5,300 9% 0.4% 3,952 1,600 - 1,600

Canara 14,000 14,000 18% 0.5% 11,664 - - -

Union - - 3,250 3,250 3% 0.1% 2,155 4,500 - 4,500

BOB - - 6,500 6,500 5% 0.2% 5,222 - - -

PNB - - - - 0% 0.0% - - 740 740

Dhanalaxmi Bank 1,000 1,000 NA NA

Centra l Bank of India 12,280 12,280 11% 0.7% 15,328

Total Estimated Sold 11,980 34,640 122,640 169,260 9% 0.4% 126,718 31,206 4,710 35,916

(Rs m) As Reported As Reported

LilladherPrabhudas Credit cycle : Corporate leverage at higher levels

Source: ACE Equity, PL Research

Source: ACE Equity, PL Research

Operating margins also at similar levels

This cycle – Issues more spread out among sectors

Source: ACE Equity, PL Research

Last cycle – Stress was commodity linked

Source: ACE Equity, PL Research

Interest coverage dipping to levels seen in 99-03 cycle

1/2/2015 34

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Standalone Consolidated

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

26.0%

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

OPM Standalone OPM Consolidated

Iron & Steel

26%

Textiles3%

Cement +

Materials

5%Engin.+ Constr.

4%

Autos- CVs2%

Breweries1%

Constr.-RE

0%

Others

59%

Iron & Steel

6% Textiles2%

Shipping1%

Power11%

Engin.+Constr.

16%

Constr. - Real Estate

4%Airlines1%

Hotels 1%

Others

58%

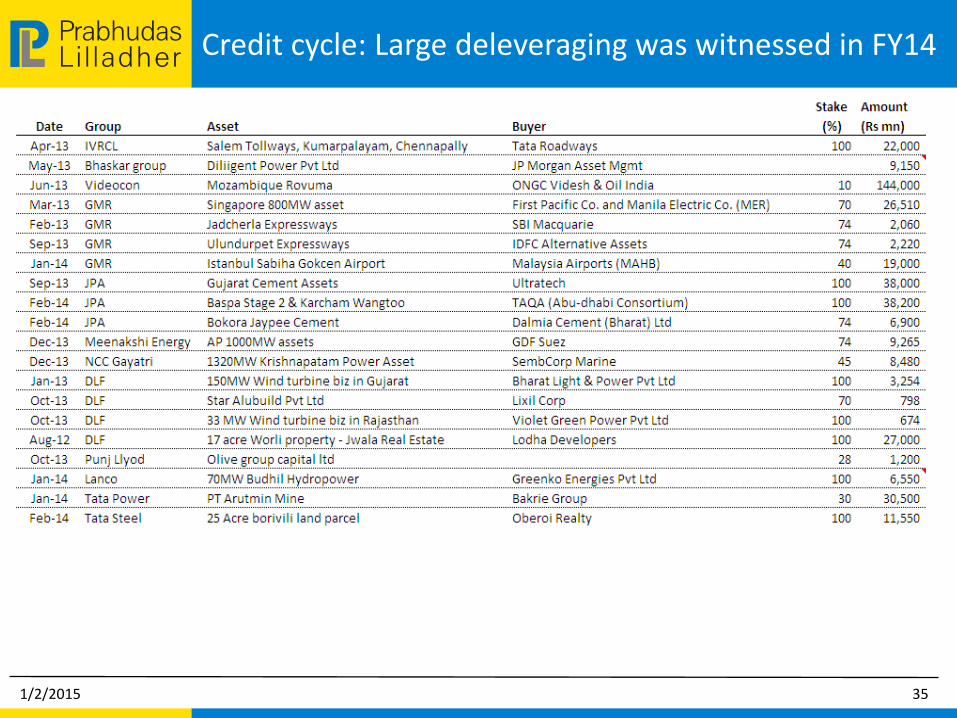

LilladherPrabhudas Credit cycle: Large deleveraging was witnessed in FY14

1/2/2015 35

LilladherPrabhudas Credit cycle: Early signs of stabilization visible

Source: : ACE Equity, PL Research

Source: Ace Equity, PL Research

..so has been the case in mid and small cap ICs

EBITDA margins have also remained stable on lower pricing power

Source: Ace Equity, PL Research

Interest expense to sales for companies has been moving up

Source: : ACE Equity, PL Research

Large cap Interest Coverage (ICs) has been stable for some period now

1/2/2015 36

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Mar

-05

Sep

-05

Mar

-06

Se

p-0

6

Ma

r-0

7

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Se

p-1

1

Ma

r-1

2

Se

p-1

2

Mar

-13

Sep

-13

Mar

-14

Sep

-14

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Mar

-05

Se

p-0

5

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Se

p-0

9

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Se

p-1

3

Mar

-14

Sep

-14

Mid Caps Small Caps

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4Q

06

2Q

07

4Q

07

2Q

08

4Q

08

2Q

09

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

Interest to Sales

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

4Q

06

2Q

07

4Q

07

2Q

08

4Q

08

2Q

09

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

EBITDA margins

LilladherPrabhudas Sector-wise Interest Coverage trends –

Airlines/Hotels/Shipbuilding/Construction stressed

1/2/2015 37

Avg. 05-

14

Avg. 07-

14

08-09

lows FY13 FY14 1H14 1H15

M -0.32 -0.96 -1.27 -1.35 -1.65 -0.58 -3.72

M 4.96 4.00 3.36 2.60 2.76 2.34 2.91

S 2.96 2.49 1.56 2.22 1.28 1.64 1.00

L 14.59 13.15 15.01 11.98 5.90 9.25 2.22

M 5.12 5.16 8.01 2.49 1.72 1.24 2.58

S 3.23 2.94 3.89 3.51 0.83 0.60 1.61

L 4.14 3.45 2.34 2.20 1.99 1.98 2.02

M 8.84 6.86 4.28 2.22 1.90 1.81 2.10

S 3.86 3.31 2.87 1.56 0.95 1.12 0.92

L 79.29 83.32 179.64 27.14 11.97 14.54 5.81

M 4.52 3.39 3.93 1.41 0.79 0.92 1.70

S 2.16 1.91 0.83 0.57 -0.32 1.03 0.38

L 5.12 4.86 4.17 3.95 3.10 3.26 2.63

M 5.38 5.34 6.90 1.63 3.03 2.22 2.79

S 4.24 4.11 5.12 0.02 0.73 1.13 0.54

M 4.50 8.78 16.87 -1.05 0.18 -0.16 1.50

S 1.99 1.58 2.83 1.07 0.21 0.85 1.21

M 4.34 3.41 4.37 1.45 0.69 1.03 0.18

S 2.16 1.78 2.89 -0.20 -0.46 -0.51 -2.57

Shipping

Shipbuilding

Mining & Mineral

Airlines

Auto Ancillary

Cement

Real Estate

Power

Avg. 05-

14

Avg. 07-

14

08-09

lows FY13 FY14 1H14 1H15

M 17.20 9.38 11.48 1.79 2.88 1.80 1.16

S 2.42 1.61 1.77 0.83 -0.30 -0.05 -1.07

L 3.73 3.73 3.92 2.08 1.07 1.24 1.71

M 4.21 4.04 3.81 2.17 1.60 1.40 0.98

S 1.91 1.67 1.90 0.69 0.12 0.15 -0.15

M 4.77 1.76 2.24 1.27 -0.37 -0.37 0.06

S 1.09 0.67 1.14 0.80 0.29 -0.23 -0.17

M 4.63 3.87 2.43 3.32 6.53 6.31 4.03

S 1.15 0.96 0.13 1.19 1.33 1.57 0.42

M 3.68 3.21 2.75 1.85 2.02 1.66 1.57

S 2.68 2.47 2.64 1.12 0.74 0.79 0.43

L 4.45 3.64 3.98 3.25 3.61 1.37 0.88

M 5.69 4.97 10.28 0.39 0.53 0.34 0.07

S 3.77 3.10 3.30 1.51 1.30 0.60 0.57

L 5.81 5.03 6.34 2.94 3.86 2.34 2.95

M 2.67 2.24 2.89 1.16 1.04 1.24 0.55

S 2.20 2.10 2.73 1.14 0.47 0.77 0.13

L 8.79 8.06 12.26 5.33 4.62 4.48 4.27

M 3.02 2.72 4.80 1.55 1.41 1.38 1.31

S 1.75 1.67 2.58 1.07 0.69 0.80 0.51

Industrial Equipment

Iron & Steel

Sugar

Textile - Spinning

Transmission towers

Hotels

Total

Construction/Infra conglomerates

LilladherPrabhudas CDR referrals have declined but approval rate going up

• CDR referrals have declined in past few quarters from peak of Rs453bn in Jun-Sep 2013 to Rs133bn in the Jun-Sep 2014 quarter.

• However approval rate has been trending higher and has increased to 82% on amount-wise basis and 79% on basis of number of cases approved.

• The average amount per successful referral remains lumpy indicating the continued stress faced by the mid-corporate and SME segment though number of such referrals have declined over past one year.

Source: CDR cell, PL research

Source: CDR cell, PL research

CDR referrals have declined in past two quarters – amount wise

…and by amount approved

Source: CDR cell, PL research

However approval rate has trended higher – both by no. of cases

1/2/2015 38

Rs bn Cases referred Amount Cases approved Amount Avg. amount per case

Jul -Sep 2012 33 189 18 189 11

Oct-Dec 2012 25 210 35 246 7

Jan-Mar 2013 30 311 39 170 4

Apri l -Jun 2013 27 394 14 213 15

Jun-Sep 2013 31 249 16 220 14

Sep-Dec 2013 25 453 12 170 14

Dec-Mar 2014 17 223 33 411 12

Mar-Jun 2014 2 29 10 181 18

Jun-Sep 2014 14 133 19 191 10

64%

66%

68%

70%

72%

74%

76%

78%

80%

82%

Ma

r‐1

1

Jun‐

11

Sep‐

11

Dec

‐11

Ma

r‐1

2

Jun‐

12

Sep

-12

Dec

‐12

Ma

r-1

3

Jun

-13

Sep

-13

Dec

-13

Ma

r-1

4

Jun

-14

Sep

-14

By number of cases (%)

60%

65%

70%

75%

80%

85%

Ma

r‐1

1

Jun‐

11

Sep‐

11

Dec

‐11

Ma

r‐1

2

Jun‐

12

Sep

-12

Dec

‐12

Ma

r-1

3

Jun

-13

Sep

-13

Dec

-13

Ma

r-1

4

Jun

-14

Sep

-14

By amount approved (%)

LilladherPrabhudas Is CDR success rate deteriorating?

Source: CDR Cell, PL Research

Source: CDR Cell, PL research

• The efficacy of CDR led restructuring has declined as the failure rate continues to increase. The CDR failure rate has increased to 29% on the basis of number of cases and 13% on amount-wise basis. This makes CDR restructuring only slightly better than the bilateral restructuring carried by banks where the failure rate has been typically ~20%.

• Nearly ~50% of total restructuring via CDR route has happened in past two years. We believe that as more number of cases comes out of moratorium over next six months the failure rate would trend higher.

• On two-year lag basis the CDR failure rate has increased to 44% on the basis of number of cases and 25% on amount-wise basis.

• Infrastructure, Iron & Steel and textiles account for ~60% of total restructuring

• The growth rate in CDR led restructuring has been the highest for sectors like textiles, pharmaceuticals and engineering besides infrastructure while sectors like petrochemicals, sugar and cement have shown reduction in the total outstanding restructured amount.

CDR failure rate –increasing by both amt approved and no. of cases

Composition of CDR restructuring: Infra & Metals a/c for >50%

1/2/2015 39

0%

2%

4%

6%

8%

10%

12%

14%

21%

22%

23%

24%

25%

26%

27%

28%

29%

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

By number of cases (%) By amount approved (%) (RHS)

Infrastructure

36%

Iron & Steel

16%

Textiles

9%

Construction6%

Ship Building / Ship-Breaking

4%

Engineering

4%

Pharmaceuticals

4%

Others20%

LilladherPrabhudas Restructuring Monitor – most restructured accounts continue

to remain under stress based on interest coverage ratio

1/2/2015 40

Source: Media Reports, ACE Equity, PL Research

LilladherPrabhudas Restructuring Monitor – most restructured accounts continue

to remain under stress based on interest coverage ratio

1/2/2015 41

Source: Media Reports, ACE Equity, PL Research

LilladherPrabhudas Restructuring Monitor – most restructured accounts continue to

remain under stress based on interest coverage ratio

1/2/2015 42

Source: Media Reports, ACE Equity, PL Research

LilladherPrabhudas Sensitivity - Earnings and Price Target sensitivity to

change in loan growth, credit cost and risk-free rate

• We have analyzed the earnings and PT sensitivity for major banks to changes in loan growth, credit cost, fresh slippages and reduction in risk-free rate.

• We note that this is not a blue sky scenario but a possible outcome if the macro scenario were to improve at a rate, slightly better than expected.

• We have built in three cases for earnings and PT sensitivity –

– Case I: 2% higher loan growth and 10bp lower credit cost

– Case II: Case I + 25bp decline in fresh slippages

– Case III: Case II + 50bp decline in risk-free rate Source: PL Research

Case 1: Our EPS and PT increases by ~4%/3% respectively in case-I

Source: PL Research

Base case estimates and PT

1/2/2015 43

Name of bank

Case I: 2% higher loan growth, 10bp lower credit cost

EPS change (%) ABV PT change (%)

FY16E FY17E FY16E FY17E Sep-FY16E

Axis 3% 3% 210.1 249.2 2.3%

HDFC 3% 4% 273.8 324.2 2.8%

ICICI 3% 3% 125.6 143.5 1.8%

IndusInd 3% 5% 227.5 279.1 3.0%

Yes 3% 4% 323.4 383.8 3.4%

Bank of baroda 5% 5% 843.8 983.5 3.1%

Bank of india 7% 6% 361.0 437.0 0.3%

Punjab National Bank 5% 6% 68.8 204.6 3.0%

State bank of india 6% 6% 132.0 153.0 2.8%

Union bank 6% 7% 238.5 291.5 1.9%

Name of bank EPS ABV PT - original P/ABV multiple - original P/E multiple - original

FY16E FY17E FY16E FY17E Sep-FY16E Sep-FY16E Sep-FY16E

Axis 37.7 45.9 210.2 248.6 545.0 2.4 13.0

HDFC 51.7 63.9 273.5 322.1 1,090.0 3.7 18.9

ICICI 23.4 27.9 125.7 143.4 390.0 2.4 12.8

IndusInd 44.5 58.8 227.5 277.3 855.0 3.4 16.6

Yes 58.5 71.4 323.1 379.1 815.0 2.3 12.6

Bank of Baroda 138.7 174.6 847.2 989.1 1,175.0 1.3 7.5

Bank of India 67.6 89.1 363.0 441.0 350.0 0.8 4.3

Punjab National Bank 29.8 35.3 169.2 205.1 208.0 1.1 6.4

State bank of India 22.3 27.7 132.0 154.0 350.0 1.9 10.7

Union bank 48.7 60.6 239.5 292.9 255.0 0.9 4.5

LilladherPrabhudas Sensitivity - Earnings and Price Target sensitivity to

change in slippages and risk free rate

Source: PL Research

Source: PL Research

• Under Case I our earnings estimate increases by ~4% on average while the increase in our PT remains at ~3%.

• If we are to build additional 25bp decline in fresh slippages over and above Case I (in previous recovery phases the pace of decline fresh slippages has been particularly sharp) than our EPS estimate increases by ~5% on average while our PT increase by 6% over our base case estimate.

• If we are to further build an additional 50bp decline in risk free rate, as we expect 10yr bond yield to decline to 7.5% over next three quarters, than our PT increase to ~14% over our base case estimate.

Case 2: Case I + 25bp decline in fresh slippages

Case 3: Case 2 + 50bp decline in risk-free rate

1/2/2015 44

Name of bank

Case 2: Case I + 25bp decline in fresh slippages

EPS change (%) ABV change (%) PT change (%)

FY16E FY17E FY16E FY17E Sep-FY16E

Axis 3% 3% 1% 2% 4.3%

HDFC 3% 4% 2% 2% 3.7%

ICICI 3% 3% 1% 3% 3.5%

IndusInd 3% 5% 2% 2% 4.9%

Yes 3% 4% 1% 1% 4.0%

Bank of baroda 5% 5% 3% 4% 7.9%

Bank of india 7% 6% 4% 5% 7.0%

Punjab National Bank 5% 6% 3% 5% 8.5%

State bank of india 6% 6% 4% 5% 7.0%

Union bank 6% 7% 4% 6% 7.8%

Name of bank

Case 3: Case 2 + 50bp decline in risk-free rate

PT P/ABV multiple P/E

multiple PT - original

Cumulative PT change

(%) Sep-FY16E Sep-FY16E Sep-FY16E Sep-FY16E

Axis 613.1 2.5 13.3 545.0 12.5% HDFC 1,225.3 4.0 19.7 1,090.0 12.4% ICICI 429.0 2.6 13.1 390.0 10.0% IndusInd 971.3 3.5 16.1 855.0 13.6% Yes 910.6 2.5 13.0 815.0 11.7% BOB 1,363.0 1.4 7.9 1,175.0 16.0% BOI 403.0 0.9 4.5 350.0 15.1% PNB 243.5 1.2 6.9 208.0 17.1% SBI 404.2 1.9 10.6 350.0 15.5% Union bank 294.7 1.0 4.8 255.0 15.6%

LilladherPrabhudas Appendix: Fund & Non fund based exposures – Private Banks

remain risk averse but have high Commercial RE exposures

Company Data, PL Research

Non fund based exposures – Private banks equally heavy weight

Company Data, PL Research

Fund Based exposures – Capex heavy industries dominate

1/2/2015 45

LilladherPrabhudas

COMPANIES

1/2/2015 46

LilladherPrabhudas Axis Bank

CMP: Rs503 TP: Rs545 Rating: BUY MCap: Rs1,181.8bn

We estimate AXSB to deliver an earnings CAGR of 21% YoY over FY15-17E led by healthy traction in NII and other income. This will be aided by reduction in fresh delinquency estimates to 1.1% for FY16E (~1.3% currently) on the back of gradual improvement in economic cycle and robust retail franchise which AXSB has build over past two years. Small restructured asset portfolio at 2.5% of total loans, and contained gross NPL ratio of 1.3% (78% coverage ratio) gives us comfort. We increase our PT on AXSB to Rs545 as we increase our FY15E/FY16E earnings by 3%/4% respectively and retain our BUY rating.

Retail franchise improving steadily: AXSB’s retail portfolio has steadily increased to ~40% of total loans and is dominated by secured loans. This has helped the bank in maintaining firm margins ably supported by steady growth in CASA mix at ~44% (~40% on daily average basis). We expect margins to move in a narrow band while management continues to remain conservative in its full year margin guidance at 3.5% (3.93% in H1FY15).

Asset composition remains stable; well placed to benefit from revival in investment cycle: The composition of corporate assets remain healthy as nearly 91% of corporate exposure remains above investment grade. The composition of SMEs with rating between SME1-SME3 also remains stable at 80%. The bank has a healthy Tier-I capital base of 12.6% and is thus well placed to benefit from any revival in investment cycle.

Asset quality has deteriorated but well under control: AXSB has reported 32%/41% rise in GNPL/Net NPLs over past one year however coverage ratio has remained stable at ~67%. AXSB conservatively maintains its Rs65bn of stressed asset guidance in FY15 despite only Rs26bn of stress loan formation in H1FY15. O/s RA portfolio remain stable at 2.5% of total loans. AXSB also maintained its credit cost guidance of 75‐80bps for FY15.

Valuation: We revise our PT to Rs545 based on 2.4x Sep-2016E ABV and reiterate our BUY rating on the stock.

1/2/2015 47

Key Financials (Rs m)

Y/e March FY13 FY14 FY15E FY16E FY17E