CLE Materials Corporate Social Responsibility for ... of energy, climate, and the... · CLE...

35

CLE Materials Panel 2: Corporate Social Responsibility for Practicing Attorneys 1. CORPORATE SUSTAINABILITY: A LEGAL PERSPECTIVE, by Jeff Civins 2. ADVICE FROM AN IN-HOUSE ATTORNEY, by Jeff Collins 3. SEA LEVEL CRIES: BEYOND MERE ETHICS IN THE REAL ESTATE PROFESSIONS, by Keith Rizzardi

Transcript of CLE Materials Corporate Social Responsibility for ... of energy, climate, and the... · CLE...

CLE Materials Panel 2: Corporate Social Responsibility for Practicing Attorneys

1. CORPORATE SUSTAINABILITY: A LEGAL PERSPECTIVE, by Jeff Civins 2. ADVICE FROM AN IN-HOUSE ATTORNEY, by Jeff Collins 3. SEA LEVEL CRIES: BEYOND MERE ETHICS IN THE REAL ESTATE PROFESSIONS, by Keith

Rizzardi

CORPORATE SUSTAINABILITY: A LEGAL PERSPECTIVE

by Jeff Civins

*This article is based on one of a similar name, which appeared in the May 2008 Texas Bar Journal, by the author and Mary Mendoza, also a partner in the Austin office of Haynes and Boone, LLP.

CORPORATE SUSTAINABILITY: A LEGAL PERSPECTIVE*

By Jeff Civins

Haynes and Boone, LLP Go to the website of virtually any major corporation and search for the terms “sustainability” and “social responsibility” and you are likely to be directed to a portal that discusses in great detail the company’s efforts to address the effect of the corporation’s activities on society and the environment. Walmart’s website, for example, proclaims that “[e]nvironmental sustainability has become an essential ingredient to doing business responsibly and successfully,” and identifies as its aspirational goals: to be supplied 100% by renewable energy; to create zero waste; and to sell products that sustain people and the environment. Some commentators suggest we are about to reach the sustainability “tipping point”--the point at which the idea of sustainability becomes a strategic business imperative--driven not by regulation, but rather by pressure from virtually the entire spectrum of corporate stakeholders. This paper provides an introduction to the concept of corporate sustainability and discusses its legal context and ramifications.

What’s It All About? The terms “corporate sustainability” and “corporate social responsibility” have a variety of definitions and sometimes are used interchangeably. Under one formulation, the term “corporate sustainability” embodies the concept of minimizing a company’s environmental footprint and thus adverse impacts on future generations, while the term “corporate social responsibility” refers to addressing environmental and social, as well as financial, concerns--the so-called triple bottom line, sometimes referred to as the 3 P’s--profit, people, and planet. This paper focuses on the environmental component of corporate social responsibility, using the term “corporate sustainability.” The concept of corporate sustainability embodies a number of aspects, including: waste reduction, reuse, and recycling; reduction in impacts on the environment; use and generation of less toxic materials; reduction in water use; reduction in energy use; reduction in use of resources; and carbon management. To better understand how corporate sustainability has become relevant to corporate decision-makers, a little context--both domestic and international-- is helpful.

Domestic Historical Context In response to the enactment of environmental legislation based on command and control, companies focused on developing programs to attain and maintain compliance. That focus was entirely consistent with the prime corporate objective of increasing shareholder value by reducing exposure to regulatory penalties and injunctive relief, though some companies may have decided at times that it was more cost-effective to violate laws and pay fines than to comply.

Page 2

With the enactment of Superfund—the Comprehensive Environmental Response, Compensation and Liability Act--in 1980, under which liability (for costs of investigation and remediation and for natural resource damages) was premised not on a violation, but rather on a nexus to contamination, companies began to understand the need to manage environmental risks, as well as to comply with environmental statutes. As a result, many companies began to go beyond compliance and to develop more comprehensive risk management programs. Recently, companies have begun to adopt a new paradigm – corporate sustainability – driven not by regulation, but rather by market forces. It is this paradigm and its legal ramifications that are the subject of this paper. Interestingly, one of the foundations of federal environmental law, the 1970 National Environmental Policy Act (NEPA) -- in section 101 -- specifically directed federal agencies to carry out their responsibilities so that the nation may, among other things, “fulfill the responsibilities of each generation as trustee for the environment for succeeding generations.” Despite this powerful directive, sustainability per se has not become a legal imperative for domestic, regulated industries, but there have been market pressures pushing towards sustainability, including internationally, and with regard to one aspect of sustainability--carbon management, regulatory pressure as well.

International Initiatives The European Union In 1997, sustainable development became a fundamental objective of the European Union (EU) when it was included in the Treaty of Amsterdam as an overarching objective of EU policies. At the Gothenburg Summit in June 2001, EU leaders launched the first EU sustainable development strategy based on a proposal from the European Commission. In 2006, the heads of state and governments of the EU adopted a renewed strategy for sustainable development that had been developed by the European Commission. See European Council Doc 10917/06. This document sets out “a single, coherent strategy on how the EU will more effectively live up to its long-standing commitment to meet the challenges of sustainable development.” It explains:

[s]ustainable development means that the needs of the present generation should be met without compromising the ability of future generations to meet their own needs…It is about safeguarding the earth’s capacity to support life in all its diversity and is based on the principles of democracy, gender equity, solidarity, the rule of law and respect for fundamental rights, including freedom and equal opportunities for all.

UN Initiatives In 1987, the UN’s Brundlant Commission – issued a report entitled “Our Common Future,” which coined the term “sustainable development.” The Commission explained that sustainability entails:

Page 3

The continual improvement of business operations to ensure long term resource availability though environmental, socially sensitive, and transparent performance as it relates to consumers, business partners, and the community.

The Commission’s mission was to unite countries to pursue sustainable development together. On January 30, 2012, the United Nations Secretary-General’s High-Level Panel on Global Sustainability issued a consensus report entitled, “Resilient People Resilient Planet – A Future Worth Choosing.” The UN Panel Report reached a number of important and relevant conclusions, including:

The world is experiencing unprecedented prosperity, while the planet is under unprecedented stress. Inequality between the world’s rich and poor is growing, and more than a billion people still live in poverty. In many countries, there are rising waves of protest reflecting universal aspirations for a more prosperous, just and sustainable world. The need to integrate the economic, social and environmental dimensions of development so as to achieve sustainability was clearly defined a quarter of a century ago. It is time to make it happen. [Our] long-term vision is to eradicate poverty, reduce inequality and make growth inclusive, and production and consumption more sustainable, while combating climate change and respecting a range of other planetary boundaries. This [vision] reaffirms the landmark Brundtland Report. For too long, economists, social activists and environmental scientists have simply talked past each other – almost speaking different languages, or at least different dialects. The time has come to unify the disciplines, to develop a common language for sustainable development to bring the sustainable development paradigm into mainstream economics. The scale of investment, innovation, technological development and employment creation required for sustainable development and poverty eradication is beyond the range of the public sector. The Panel therefore argues for using the power of the economy to forge inclusive and sustainable growth and create value beyond narrow concepts of wealth. [T]he Panel lays down a challenge for our Governments and international institutions: to work better together in solving common problems and advancing shared interests.

ISO Standards In the private sector, the International Organization for Standardization (ISO) has developed relevant international standards. Of particular relevance are ISO 14000, relating to environmental management, and ISO 26000, relating to social responsibility. ISO established ISO 14000 in 1996. ISO 14000 is a family of standards addressing various aspects of environmental management that “provide practical tools for companies and

Page 4

organizations looking to identify and control their environmental impact and constantly improve their environmental performance.” The purpose of ISO 14000 was “to provide a framework for a holistic strategic approach to the organization’s environmental policy, plans and actions,” which includes development of an environmental management system (EMS) and a commitment to compliance, continual improvement, and prevention of pollution. ISO 14001, relating to EMS’s, is under review with a final version expected by the end of 2015. With the goal to contribute to global sustainable development, ISO published ISO 26000 in 2010. This standard provides voluntary guidance on how organizations can operate in a socially responsible way by integrating social responsibility throughout their organization. Unlike other ISO standards, it is not intended for certification purposes. It addresses a number of subjects, including organizational governance, human rights, labor practices, the environment, fair operating practices, consumer issues, and community involvement and development. With regard to the environment, it addresses prevention of pollution, sustainable resource use, climate change mitigation and adaptation, and protection of the environmental and biodiversity and restoration of natural habitats.

The Role of the Market Place

Neither the directives of NEPA, the actions of the European Union, the urging of the UN, nor the establishment of ISO standards has necessarily been the driver for corporations to adopt sustainability programs. In the past several years, pressure to establish corporate sustainability programs has been building instead from the marketplace--from major corporate stakeholders including shareholders, customers, investors, lenders, insurers, corporate management and employees, governments, non-governmental organizations or NGO’s, and the public at large. This pressure has manifested itself in the form of: public attention to climate change and other sustainability issues; NGO and shareholder activism; and requirements of various stakeholders such as investors, lenders, insurers, business partners, and global supply chains. Before discussing corporate sustainability programs generally, we should take note of one aspect of corporate sustainability for which regulatory pressure has recently begun to build, that is, carbon management.

Carbon Management Carbon is shorthand for carbon dioxide or CO2, which is considered to be the most important greenhouse gas or GHG and which is the GHG to which other GHGs are compared. Up until the recent past, carbon management, like other aspects of corporate sustainability, was not a regulatory imperative. Although a number of states and regions had adopted GHG programs, federal legislative attempts in Obama’s first administration to comprehensively regulate GHGs foundered. In its decision in Massachusetts v. EPA, 549 U.S. 497 (2007), however, the Supreme Court found that the United States Environmental Protection Agency (EPA) had authority to regulate GHGs under existing law, in particular, under the federal Clean Air Act. The Supreme Court held that GHGs were air pollutants and that EPA must determine whether GHGs from mobile sources were contributing to an endangerment of public health.

Page 5

Beginning with its endangerment finding, EPA promulgated a cascading series of regulations to regulate GHGs. Those regulations included a requirement that major sources under the agency’s Title V operating permit program and that major new sources or modifications of existing sources under its prevention of significant deterioration or PSD permitting program address CO2 emissions. Various parties challenged the validity of those regulations. Although it found fault with aspects of EPA’s approach, the Supreme Court generally upheld EPA’s permitting of GHGs in Utility Air Regulatory Group (UARG) v. EPA (No. 12-1146, June 2014). Under the agency’s PSD program, major sources and modifications are required to employ best available control technology or BACT. In its March 2011 GHG BACT guidance, EPA notes the relevance of economic, energy, and other environmental impacts, and explains that, in most cases, energy efficiency improvements will satisfy BACT and may extend to non-emitting units like electric fans. Recent EPA GHG regulatory initiatives have focused on power plants. In September of 2013, EPA, after considering more than 2.5 million comments, reproposed rules establishing CO2 emission standards for fossil fuel-fired electrical generating units that would require that new coal-fired power plants meet standards for gas-fired units, presently achievable only by employing carbon capture and sequestration. In June of 2014, EPA proposed significant new requirements for existing power plants, as an outgrowth of the President’s climate action plan. The June 2014 EPA proposal is far reaching and would require states to develop implementation plans to reduce CO2 to achieve the best system of emission reduction or BSER. BSER comprises four building blocks: (1) lowering the carbon intensity of generation by effecting heat rate improvements at individual affected units; (2) reducing emissions of the most carbon-intensive affected units by shifting generation to less carbon-intensive existing natural gas combined cycle units; (3) reducing the emissions of carbon-emitting units by expanding the amount of new, lower (or no) carbon-intensity generation; and (4) reducing the emissions of carbon-emitting units by increasing demand-side energy efficiency. Once the rules are finalized, states then will determine what mix of building blocks to utilize and develop their own implementation plans to achieve compliance. Legal challenges have been filed to the proposed rule and assuredly will be filed to the final rules as well.

Unlike direct sources of GHG’s, like power plants, refineries, cement plants, and chemical plants, which are or may become subject to GHG regulation, indirect sources of GHGs, like big box retailers, are driven to control GHGs by market forces, and corporations involved in a wide range of business activities, from heavy industry to big box retailers, have developed carbon management programs. The Carbon Disclosure Project or CDP, a non-profit founded in 2000 with headquarters in London, which holds the world’s largest collection of self-reported climate change, water and forest-risk data, works with 767 institutional investors and thousands of companies to tackle climate change. On a related front, in February of 2010, the Council on Environmental Quality or CEQ issued draft NEPA guidance on the effects of climate change and GHG emissions. On December 18th of 2014, the CEQ issued revised draft guidance. The effect of GHG emissions resulting from

Page 6

agency action has been a key issue in governmental actions involving the Keystone XL pipeline and various proposed liquefied natural gas export facilities. Options to address carbon include strategies that are of value independent of GHG considerations such as: use of alternate energy, like renewables; use of alternative fuels, like biofuels; energy conservation; energy efficiency; carbon capture for use in enhanced oil recovery; and recycling and reuse of wastes and by products. Options to address carbon that relate directly to GHG control include: carbon treatment; carbon capture and storage; and obtaining of carbon offsets by controlling emissions or by construction of alternative projects such as reforestation. In 2008, the World Resources Institute established guidelines for CO2 capture, transport and storage, and Citigroup, JPMorgan-Chase, and Morgan Stanley joined together to establish “The Carbon Principles”--guidelines, which encourage lower CO2 emissions, renewable energy, and low emissions technology--for use in negotiating with clients seeking funding for power plant-related projects. As noted, carbon management is but one aspect of sustainability. A carbon-only focus may result in unintended impacts on other aspects of the environment. Companies should take a holistic view and consider all the environmental impacts of the implementation of their carbon management activities; for example, capturing and storing CO2 will result in increases in the energy and cost. Unfortunately, there presently is no common currency for quantifying various aspects of sustainability and weighing them against one other. In the private sector, Walmart, in collaboration with the Sustainability Consortium, an organization with 90 members, is developing a sustainability index to integrate various aspects of sustainability into the products it buys and sells.

Corporate Programs Corporate sustainability programs generally include as elements: strategic planning; corporate policies and goals, infrastructure, and procedures; a code of conduct; standards, manuals, and guides; stakeholder communication, including dialogue and reporting; performance and appraisal metrics; and line responsibilities. But under most formulations, a distinguishing feature of a corporate social responsibility program is the notion that long-term environmental, and social aspects, as well as economic aspects, be integrated into a corporation’s business strategy, rather than considered in isolation or as add-ons. There are numerous examples of corporate sustainability programs. CDP’s website indicates it is working with 4500 companies from more than 80 countries regarding global natural capital disclosure and that some 66 purchasing organizations, like Dell, Pepsico, and Walmart, are using CDP’s global system to mitigate environmental risks in their supply chains. The International Institute for Sustainable Development, which, in 2007, published an implementation guide on corporate social responsibility, reports of a survey by PricewaterhouseCooper that indicated that 85% of 140 chief executives of US-based multinational companies believed that sustainable development will be more important to their business model in five years than it is today.

What are the Legal Issues?

Page 7

Because sustainability programs focus on societal and environmental impacts in addition to economic ones and because they are not regulatorily compelled, they raise fundamental questions about their relevance to corporations seeking to maximize shareholder value. They also raise questions regarding how companies talk about their sustainability to their stakeholders, that is, whether and how to report corporate information concerning sustainability efforts and the risks associated with failure to report accurately. Philanthropy v. Shareholder Value Although we may well be approaching a tipping point for companies to implement corporate sustainability programs, the concept is not without its critics. Some argue that companies use corporate sustainability programs only as public relations “smokescreens”--to cover up corporate environmental shortcomings. Others argue that the only social responsibility of business is to increase its profits, that is, that “the business of business is business.” These critics maintain that other stakeholders, such as governments, individuals, and NGO’s, are better equipped to address social and environmental concerns and that corporations should not engage in philanthropy. The legal component of this argument is based on the fiduciary duties of directors and officers--of loyalty and care--to the corporation and the interests of shareholders. Courts generally permit directors to consider the impact of their decisions on constituencies other than shareholders, “provided there are rationally related benefits accruing to the stockholders.” See Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., 506 A2d 173, 182 (Del. 1985). Corporate sustainability supporters maintain that the conflict between the economic bottom line, on the one hand, and societal values and environmental protection, on the other, is for the most part illusory, because socially and environmentally progressive policies positively affect the bottom line in numerous ways. Those supporters assert there is a growing body of evidence that corporations can do well by doing good. Examples include: preemption of future burdensome regulatory requirements; obtaining benefits under existing regulatory programs, such as fewer inspections and greater flexibility in their operations; improvement of public image and engendering of good will with stakeholders; increased sales, investment, productivity and employee satisfaction; development of new business opportunities; and cost savings in reducing energy and waste management demands and environmental risks, as well as expenses and costs of insurance, worker compensation, and borrowing. A January 19, 2008 New York Times article, however, quoted a study that reviewed numerous studies and found that there was only a very small correlation between “good” corporate behavior and good financial results, one explanation being that companies that performed well over a long period of time have enough money to contribute positively to society.1 On the other hand, corporate misdeeds, once they become known, may have a significant negative impact on financial performance. The authors of the study found that only two percent of the studies reviewed showed that managers who dedicate corporate resources to take actions that consider the interests of society impose a direct cost to shareholders. So, restated, the point is “companies can do good and do well, even if they don’t do well by doing good.” Recognizing the distinction between making a profit and doing good, a number of states have adopted legislation, and others, proposed legislation, to authorize the creation of so-called benefit

Page 8

or “B” corporations. Benefit corporations are a new type of legal entity falling between standard for-profit or “C” corporations and non-profit corporations. Benefit corporations voluntarily meet higher standards of corporate purpose, accountability, and transparency. They have a corporate purpose to create a material positive impact on society and the environment; they are required to consider the impact of their decisions not only on shareholders, but also on workers, community, and the environment; and they are required to make available to the public an annual benefit report that assesses their overall social and environmental performance against a third-party standard. To Report or Not to Report In addition to having to decide whether to develop a corporate sustainability program, corporations face other, related issues regarding the need to disclose corporate sustainability information, especially with respect to climate change, and liabilities associated with erroneous sustainability disclosures. In response to the FY2008 Consolidated Appropriations Act, EPA issued its GHG reporting rule, now codified in 40 CFR Part 98, applicable to specified classes of GHG emitters. The 2013 GHG Reporting Program or GHGRP data set includes public information from facilities in nine industry groups that directly emit large quantities of GHGs, as well as suppliers of certain fossil fuels and industrial gases, that have been required to report their GHG emissions. On a broader front, there has been litigation to attempt to compel Securities and Exchange Commission (SEC)-reporting of certain components of sustainability programs, in particular, regarding climate change. Many companies, however, are not waiting for government regulation and are voluntarily issuing sustainability and climate change reports. SEC regulations provide some general guidelines that may bear on reporting on sustainability issues such as climate change. The SEC’s rules require that various filed reports contain discussions of trends, events or uncertainties that will be reasonably likely to have a material effect on the company. See 17 U.S.C. §§ 229.101, 229.303. Regulation S-K Item 101, regarding disclosure of capital expenditures, requires disclosure of any material effect that environmental compliance costs may have on earnings and competitive position. But presently, general corporate sustainability reporting is not regulatorily required. Regulation S-K Item 103 requires the disclosure of material pending legal proceedings, other than “ordinary routine litigation incidental to the business.” 17 C.F.R. § 229.103. Litigation is increasingly being used to determine corporate sustainability responsibilities, especially as regards climate change. Regulation S-K Item 303, which sets out guidance for management’s discussion and analysis (MD&A), creates a potential basis for corporate sustainability and climate change disclosure. The MD&A typically identifies and discusses “known trends or any known demand, commitments, events, or uncertainties that will reasonably result in or that are reasonably likely to result in the registrant’s liquidity increasing or decreasing in any material way,” and known trends or uncertainties reasonably expected to have a material impact on sales, revenues or income. See 17 CFR § 229.303(a)(1), (a)(3)(ii); Securities Act Release No. 33-6835. In 2008,

Page 9

the State of New York reached settlements with three power companies regarding disclosures of the risks and liabilities posed by CO2 emissions from new power plants. Various stakeholders have pressured the SEC to put more teeth into reporting requirements relating to corporate social responsibility in the area of GHGs. In September of 2007, a group of pension plans and institutional investors, in conjunction with Ceres (a network of investors, environmental organizations and public interest groups focused on sustainability issues) filed a petition calling for the SEC to issue an interpretive release clarifying that material climate change information must be included in corporate disclosures under existing law. In January of 2010, the SEC voted to provide public companies with interpretative guidance on existing SEC disclosure requirements as they apply to business or legal developments relating to the issue of climate change. The guidance is found at 75 Federal Register 6290 (Feb. 8, 2010). The guidance focused on four areas as examples of where climate change may trigger disclosure requirements: (1) impact of legislation and regulation; (2) impact of international accords; (3) indirect consequences of regulation or business trends; and (4) physical impacts of climate change. To reach customers, a critical class of corporate stakeholders, many companies have launched active green marketing campaigns, touting the sustainability of their products or their method of manufacture. To help corporate marketers avoid making environmental claims that are unfair or deceptive under Section 5 of the Federal Trade Commission Act, 15 U.S.C.§ 45, the Federal Trade Commission (FTC) has issued “Green Guides,” 16 CFR Part 260, which, though not independently enforceable, do provide the agency’s interpretation of the law. The FTC explains that the Green Guides “outline general principles that apply to all environmental marketing and then provide guidance regarding specific environmental claims.” In October of 2012, the FTC revised its guidelines to update and expand them, “to help marketers ensure that the claims they make about the environmental attributes of their products are truthful and non-deceptive.” The FTC also has begun actively enforcing against companies that overreach in their green marketing. In October of 2013, for example, the FTC announced that it had undertaken six enforcement actions focused on biodegradable plastic claims. Many of the benefits that companies pushing sustainability seek to achieve from stakeholders generally depend on the reporting and transparency of the initiatives and their results. More companies are including discussions on sustainability programs or components of such programs (such as climate change initiatives) in either their SEC reports or stand-alone Corporate Sustainability Reports. A survey of sustainability reports by KPMG reported the interesting fact that, while “almost all” companies included discussions of climate change in sustainability reports, most of these reports dealt with “potential opportunities rather than financial risk” from the issue. See Reporting the Business Implications of Climate Change in Sustainability Reports, KPMG, 2007. However, there are pitfalls for companies reporting on the results and benefits of a sustainability or climate change program. Nike v. Kasky2 is a cautionary tale on how a company communicates regarding its corporate social responsibility programs. In this case, Nike made claims in advertising and other communications regarding steps taken to improve conditions for overseas workers. A

Page 10

shareholder challenged Nike’s statements under California’s false advertising laws. Nike was unsuccessful in its efforts before the California Supreme Court to obtain a ruling that its statements were First Amendment-protected political speech. The case settled prior to a trial. This decision sends a warning signal to corporations that choose to speak out on social and public issues impacting the business of the company--that they should not overreach. Disclosure issues may arise not only under state law, but under federal securities law as well. Section 10(b) of the Securities Exchange Act of 1934, which makes it unlawful for anyone to make an untrue statement or to omit to state a material fact in connection with the purchase or sale of any security, may be viewed by the plaintiffs’ bar as a potential basis to complain of the adequacy of a company’s disclosure of its social responsibility activities. A key aspect of reporting relates to how various parameters of corporate social responsibility are to be measured. At present there are no regulatory metrics, but there are a number of voluntary frameworks that provide guidance. The Global Reporting Initiative (GRI) is a multi-stakeholder network of thousands of experts in dozens of countries who pioneered the world’s most widely used sustainability reporting framework. The GRI Sustainability Reporting Guidelines provide organizations detailed guidance on how to report their sustainability performance, including as regards: strategy and analysis; organization profile; report parameters; and governance, commitments and engagement.3 For carbon disclosure, the CDP asserts their methodology has become the gold standard.

Conclusion The bottom line is that corporate sustainability programs are becoming strategic business imperatives, driven by stakeholder pressures rather than by governmental directives. Because there is no true regulatory oversight, there are as yet no uniform, mandated definitions, performance metrics, and reporting standards. State, federal, and foreign governments, however, are beginning to climb on the sustainability bandwagon and perhaps one day will develop pertinent regulatory programs to complement or supplant the efforts of other stakeholders.4 For now, a corporation that decides to develop a corporate sustainability program should consider, among other things, how to address the issues of what, when, where, and how to report sustainability efforts and results. A-310944_4

1 Paul B. Brown, Bottom Line on Doing Good, January 19, 2008, available at http://www.nytimes.com/2008/01/19/business/19offline.html 2Nike v. Kasky, 27 Cal. 4th 939 (2002) (concluding corporation’s messages were commercial speech for purposes of applying state laws barring false and misleading commercial messages), cert. dismissed, 539 U.S. 654 (2003). 3 Global Reporting Initiative at http://www.globalreporting.org/Home. 4 An EPA advisory group, the National Advisory Council for Environmental Policy and Technology, has suggested that EPA reframe its mission to provide leadership and a collaborative, national focus on environmental stewardship. Amy Phillips, Advisers Urge EPA to ‘Reframe’ Mission With Focus on Stewardship, Collaboration, BNA Daily Environment Report, Mar. 31, 2008, at A-8.

© 2015 Chevron

Corporate Responsibility at Chevron

Jeff Collins, Senior Counsel Corporation Law Compliance, Investigations, and Policy February 2015

Jeff Collins Senior Counsel for International Policy Chevron Corporation February 2015

© 2015 Chevron 2

“There is no such thing as ‘CR’ and the ‘Business’. There is only responsible business.”

Rhonda Zygocki Executive Vice President , Policy and Planning

Our Philosophy

© 2015 Chevron

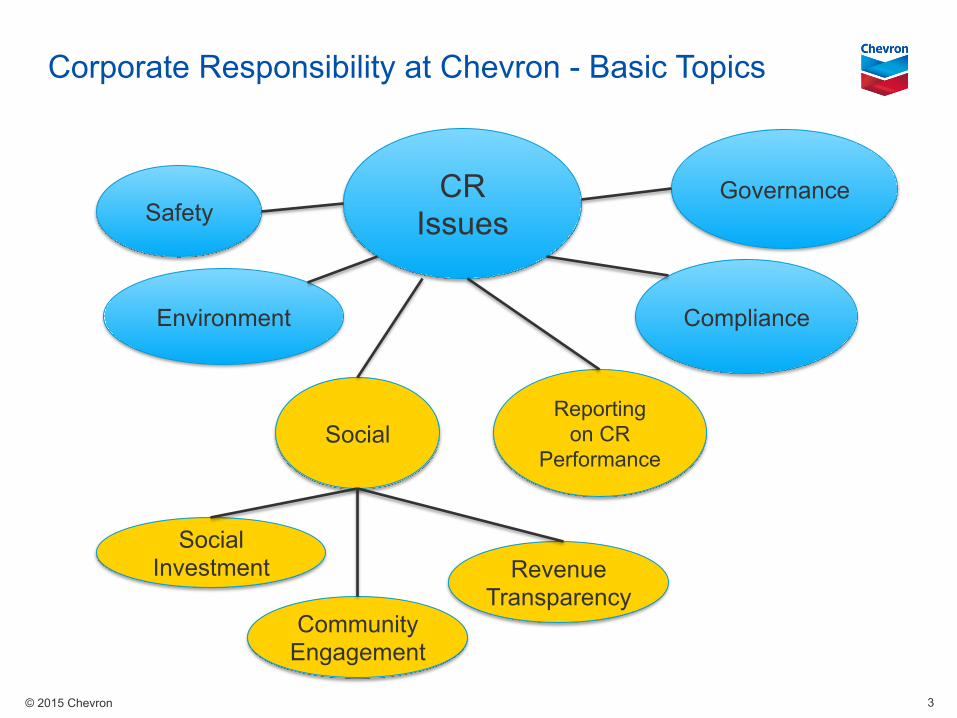

Corporate Responsibility at Chevron - Basic Topics

3

Revenue Transparency

CR Issues Safety

Environment Compliance

Reporting on CR

Performance Social

Community Engagement

Social Investment

Governance

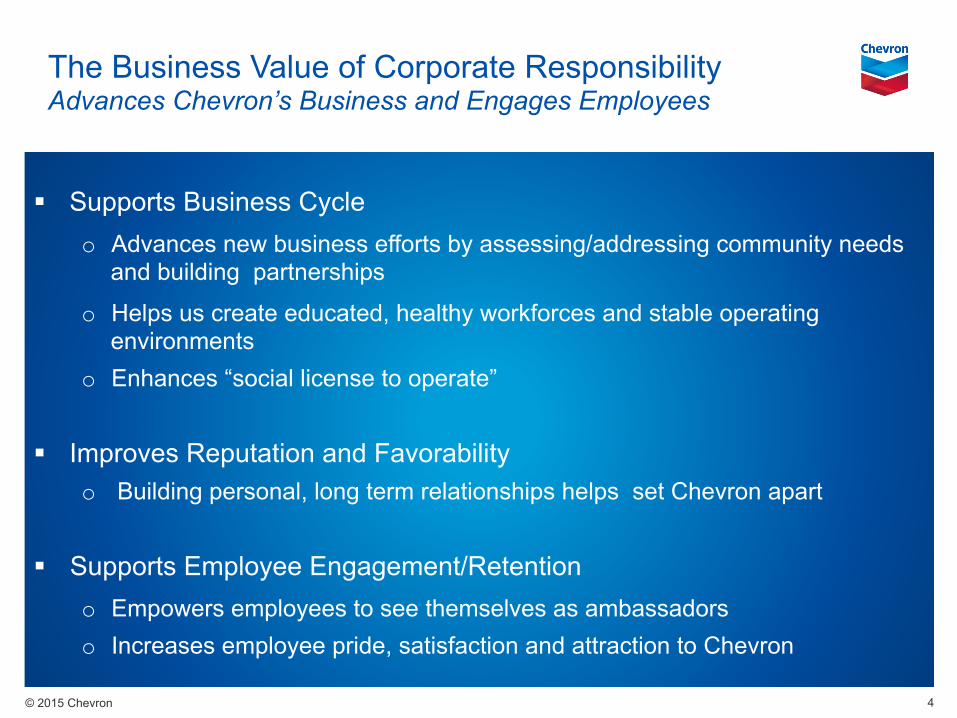

© 2015 Chevron 4

! Supports Business Cycle o Advances new business efforts by assessing/addressing community needs

and building partnerships

o Helps us create educated, healthy workforces and stable operating environments

o Enhances “social license to operate”

! Improves Reputation and Favorability

o Building personal, long term relationships helps set Chevron apart

! Supports Employee Engagement/Retention o Empowers employees to see themselves as ambassadors o Increases employee pride, satisfaction and attraction to Chevron

The Business Value of Corporate Responsibility Advances Chevron’s Business and Engages Employees

© 2015 Chevron

Case Study: Chevron’s Human Rights Journey

5

© 2015 Chevron

Evolution of Business’ Responsibility to Respect Human Rights

6

Traditionally, governments had responsibility to guarantee human rights

Broadened focus to include business’ responsibilities for their human rights impacts

UN “Protect, Respect, Remedy” framework (2008) asserts a corporate responsibility to respect human rights

© 2015 Chevron

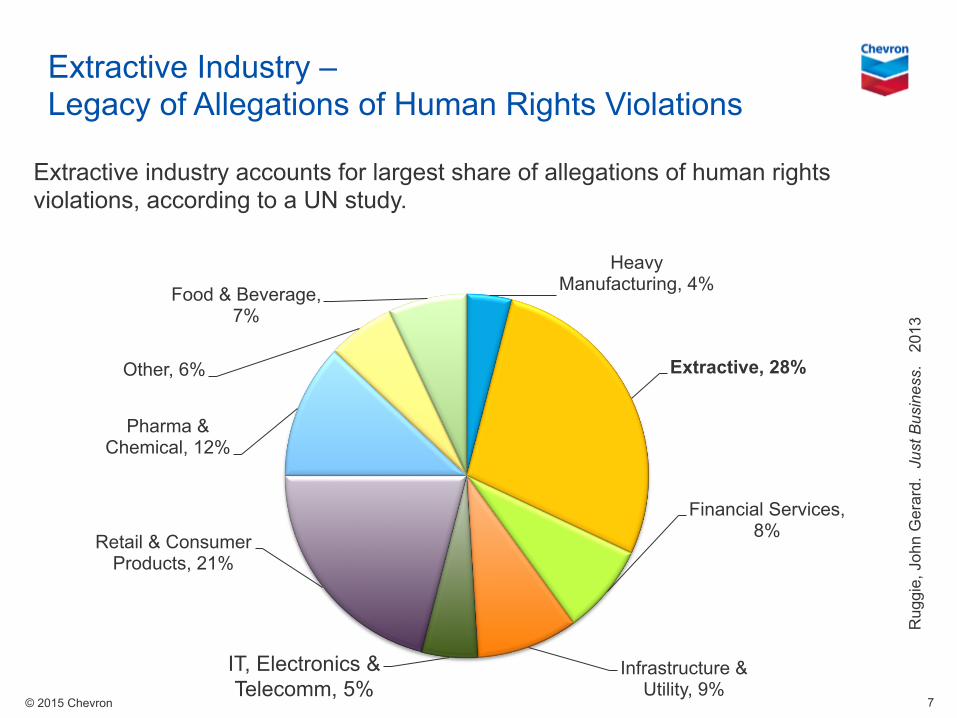

Extractive Industry – Legacy of Allegations of Human Rights Violations

7

Extractive industry accounts for largest share of allegations of human rights violations, according to a UN study.

Heavy Manufacturing, 4%

Extractive, 28%

Financial Services, 8%

Infrastructure & Utility, 9%

IT, Electronics & Telecomm, 5%

Retail & Consumer Products, 21%

Pharma & Chemical, 12%

Other, 6%

Food & Beverage, 7%

Rug

gie,

Joh

n G

erar

d. J

ust B

usin

ess.

20

13

© 2015 Chevron

Chevron’s Human Rights Journey

8

2006

• Human Rights Statement Adopted

2009-13

• Human Rights Policy 520 Implemented

2014-15

• Ongoing review, training, improvement

© 2015 Chevron

Chevron’s Human Rights Policy -- Overview

■ Aligns with UN framework

■ Expresses commitment to respecting human rights

■ Sets forth specific principles in four areas: employees, security, communities and suppliers

■ Governed by an executive leadership body and guided by a policy team

9

© 2015 Chevron

What are Human Rights Concerns in our Business?

! Infractions

10

! Association ! Discrimination ! Labor Infractions ! Working and Living

Conditions

Security Employees ! Security Infractions ! Environmental

Concerns ! Land Appropriation ! Relocation ! Livelihoods

Community ! Working and Living

Conditions ! Child Labor ! Trafficking ! Assurance

Supply Chain

© 2015 Chevron

Human Rights Policy Introduced Key Innovations

11

! Contract provisions related to human rights: security contracts; supply chain contracts

! Incorporated human rights considerations into existing

company systems and processes ! New Guidance on: Resettlement; Indigenous Peoples;

Community Engagement; Supplier Engagement

© 2015 Chevron

! Company culture

! Security ! Use of “leverage” to influence others

Impact of Human Rights Policy

12

© 2015 Chevron

Beyond Chevron

13

Industry Business

Multi-stakeholder

IPIECA

• Socially Responsible Working Group member

• Human Rights Task Force Co-Chair

• Responsible Security Task Forces Co-Chair

Voluntary Principles on Security & Human Rights

German Marshall Fund: Responsible Security Operations

International Bar Association: Corporate Responsibility Committee

American Bar Association Business & Human Rights Project

Global Business Initiative for Business and Human Rights

Business for Social Responsibility: Human Rights Working Group

Corporate Governance Board

© 2015 Chevron

! Reaching more companies o Small and medium-sized companies

o National Oil Companies

! Embedding principles in massive, complex organizations ! Overcoming language/communication hurdles

Challenges

14

© 2015 Chevron

What’s Next?

! Further uptake of UNGPs o Internal and external efforts o Is the treaty debate a distraction?

! National Action Plans ! Access to Remedy – the “third pillar”

15

© 2015 Chevron

&Questions

Answers

16

SEA LEVEL CRIES: BEYOND MERE ETHICS IN THE REAL ESTATE PROFESSIONS By Keith W. Rizzardi

Sea$Level$Cries:$Beyond$Mere$Ethics$in$the$Real$Estate$Professions$By#Keith#W.#Rizzardi1#

#I. Introduction$

!

Despite!a!scientific!consensus,!the!United!States!political!leadership!remains!embroiled!in!a!legislative!

and!policy!debate!over!the!existence!of!sea!level!rise,!and!the!responses!to!it.!Meanwhile,!homeowners!

and!businesses!face!real!questions!and!serious!risks!when!they!make!long@term!investment!decisions!–!

including,!significantly,!whether!and!where!to!buy!real!estate.!Climate!change!and!rising!seas!will!affect!

our!human!habitats,!and!our!densely!developed!coastal!communities!provide!the!homes,!workplaces,!

recreational!opportunities!and!governmental!tax!bases!that!drive!our!economies.!The!land!use!

development!and!real!estate!professionals,!when!discussing!these!matters,!have!an!ethical!and!moral!

responsibility!to!do!better!than!our!political!leaders.!

II. Truth,$Material$Facts$and$Omissions:$the$Minimum$Professional$Standards.$$

Coastal!development!is!an!interdisciplinary!human!activity.!Investments!are!made,!finances!secured.!

Lands!are!modified,!waters!managed.!Permits!are!obtained,!buildings!and!habitats!are!constructed.!The!

whole!enterprise!requires!the!collective!effort!of!corporations!and!professionals!such!as!lawyers,!

planners,!engineers,!real!estate!and!compliance!professionals.!All!of!these!professions!have!ethical!

codes,!too,!which!establish!essential!duties.!These!professional!duties!are!not!limited!to!clients.!Again!

and!again,!the!professions’!various!ethical!codes!all!make!it!clear!that!honesty!–!to!everyone!–!is!

expected.!Material!facts!must!be!disclosed,!and!as!the!following!ethical!directives!make!clear,!

professionals!cannot!participate!in!the!concealment!of!truth,!particularly!if!it!leads!to!fraud!or!

misconduct:!

Legal#ethics#and#the#ABA#Model#Rules#of#Professional#Conduct#

• Rule!2.1!Advisor:!“In!representing!a!client,!a!lawyer!shall!exercise!independent!professional!

judgment!and!render!candid!advice…!not!only![as]!to!law!but!to!other!considerations!such!as!

moral,!economic,!social!and!political!factors,!that!may!be!relevant!to!the!client's!situation.”!

• Rule!4.1!Truthfulness!In!Statements!To!Others”!“In!the!course!of!representing!a!client!a!lawyer!

shall!not!knowingly:!(a)!make!a!false!statement!of!material!fact!or!law!to!a!third!person;!or!(b)!

fail!to!disclose!a!material!fact!to!a!third!person!when!disclosure!is!necessary!to!avoid!assisting!a!

criminal!or!fraudulent!act!by!a!client,!unless!disclosure!is!prohibited!by!Rule!1.6.”!

• Rule!1.13!Rule!1.13!Organization!As!Client:!“(b)!If!a!lawyer!for!an!organization!knows!that!an!

officer,!employee!or!other!person!associated!with!the!organization!is!engaged!in!action,!intends!

to!act!or!refuses!to!act!in!a!matter!related!to!the!representation!that!is!a!violation!of!a!legal!

obligation!to!the!organization,!or!a!violation!of!law!that!reasonably!might!be!imputed!to!the!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

1

!Keith!W.!Rizzardi!is!a!law!professor!at!St.!Thomas!University!in!Miami!Gardens,!Florida,!where!he!teaches!

environmental!law!and!professional!responsibility.!He!also!has!earned!board!certifications!in!state!and!federal!

administrative!practice!and!in!corporate!compliance!and!ethics.!

organization,!and!that!is!likely!to!result!in!substantial!injury!to!the!organization,!then!the!lawyer!shall!proceed!as!is!reasonably!necessary!in!the!best!interest!of!the!organization.”!

Other#professional#ethical#mandates:#

• The!American!Institute!of!Certified!Planners,!Code!of!Conduct,!(B)(1):!certified!planners!“shall!not!deliberately!or!with!reckless!indifference!fail!to!provide!adequate,!timely,!clear!and!accurate!information!on!planning!issues.”!

• American!Institute!of!Architects!Code!of!Ethics!and!Professional!Conduct,!Rule!of!Conducts!2.106!and!2.104,!architects!shall!not!counsel!or!assist!a!client!in!conduct!that!the!architect!knows,!or!reasonably!should!know,!is!fraudulent!or!illegal,!nor!engage!in!conduct!involving!the!wanton!disregard!of!the!rights!of!others.!

• American!Society!of!Civil!Engineers!Code!of!Ethics,!Canon!3,!emphasizes!that!“Engineers!shall!issue!public!statements!only!in!an!objective!and!truthful!manner,”!noting!that!civil!engineers!“should!endeavor!to!extend!the!public!knowledge!of!engineering!and!sustainable!develop!and!shall!not!participate!in!the!dissemination!of!untrue,!unfair!or!exaggerated!statements!regarding!engineering.”!

• National!Association!of!Realtor’s!Code!of!Ethics,!!Article!I!provides!that!realtors!have!an!obligation!“to!treat!all!parties!honestly,”!and!Article!II!says!realtors!“shall!avoid!exaggeration,!misrepresentation,!or!concealment!of!pertinent!facts!relating!to!the!property!or!the!transaction.”!

• The!Rules!of!Conduct!by!the!Society!for!Corporate!Compliance!and!Ethics!holds!truthfulness!paramount!for!compliance!professionals,!who!“shall!not!aid,!abet!or!participate!in!misconduct,”!who!“shall!take!such!steps!as!are!necessary!to!prevent!misconduct!by!their!employing!organizations,”!!and!who!must!pursue!their!professional!activities!“with!honesty,!fairness!and!diligence.”!!!!!

III. What$is$Truth,$Anyway?$Law,$Policy,$Facts$and$Projections$for$Coastal$Real$Estate.$$

The!risks!of!climate!change!for!coastal!communities!have!been!repeatedly!acknowledged!in!case!law,!statutes,!rules!and!official!findings.!

• In!Massachusetts!v.!EPA,!a!sharply!divided!Supreme!Court!held!that!“the!rise!in!sea!levels!associated!with!global!warming!has!already!harmed!and!will!continue!to!harm!Massachusetts.!The!risk!of!catastrophic!harm,!though!remote,!is!nevertheless!real.”!!!

• In!Section!1102!of!the!Global!Climate!Protection!Act!of!1987,!Congress!recognized!the!potential!for!increased!temperatures,!altered!weather!patterns!and!agricultural!productivity,!and!“thermal!expansion!of!the!oceans!and!partial!melting!of!the!polar!ice!caps!and!glaciers,!resulting!in!rising!sea!levels.”!!!!

• In!its!findings!associated!with!a!Clean!Air!Act!rulemaking!exercise!on!whether!greenhouse!gases!endangered!public!health,!the!U.S.!Environmental!Protection!Agency!explained!that!evidence!of!adverse!impacts!in!the!areas!of!water!resources!and!sea!level!rise!and!coastal!areas!were!of!special!concern!to!current!and!future!generations,!!and!that!the!“most!serious!potential!adverse!

effects!are!the!increased!risk!of!storm!surge!and!flooding!in!coastal!areas!from!sea!level!rise!and!more!intense!storms.”!!!!

• Similar!published!findings!have!been!made!by!Army!Corps!of!Engineers,!Global!Climate!Research!Program,!National!Academy!of!Sciences,!the!National!Research!Council,!U.S.!Navy,!and!the!Nobel!Prize@winning!work!conducted!by!the!Intergovernmental!Panel!on!Climate!Change!(IPCC).!

• Florida!Statutes!Sec.!163.3164:!Local!governments!can!define!an!“[a]daptation!action!area”!to!identify!“one!or!more!areas!that!experience!coastal!flooding!due!to!extreme!high!tides!and!storm!surge!and!that!are!vulnerable!to!the!related!impacts!of!rising!sea!levels!for!the!purpose!of!prioritizing!funding!for!infrastructure!needs!and!adaptation!planning.”!!!!

• The!Kingdom!of!the!Netherlands!announced!the!Delta!Programme:!for!the!next!40!years,!the!Dutch!plan!to!use!€!1!billion!annually!for!flood!risk!management!and!fresh!water!protection!and!maintenance,!with!€!600!million!available!for!investments.!!!

As!a!factual!matter,!the!risks!of!climate!change,!and!sea!level!rise,!are!extraordinary.!Conservative!estimates,!with!a!low!rate!of!sea!level!rise,!project!more!than!3!feet!of!sea!level!rise!before!2100,!and!potentially!by!2060.!!In!Miami!and!Coastal!Virginia,!the!risks!are!acute:!

• According!to!studies!by!the!South!Florida!Regional!Climate!Change!Compact!and!the!four!Southeast!Florida!counties,!the!upper!estimate!of!taxable!property!values!vulnerable!to!inundation!across!the!region!is!greater!than!$4!billion!at!just!one!foot!of!sea!level!rise.!Affected!property!values!rise!to!over!$31!billion!at!the!3!foot!scenario.!!!

• Whereas!the!7!foot!storm!surge!flood!historically!occurred!rarely!(once!every!28!years!in!Virginia,!once!every!76!years!in!Florida),!projections!are!that!just!2!feet!of!sea!level!rise!will!mean!much!more!major!flooding!(every!other!year!or!even!more!frequently).!In!Coastal!Virginia,!three!feet!of!sea!level!rise!could!trigger!major!flooding!three!times!every!year.!!

IV. Are$Mere$Ethics$Enough?$Sea$Level$Lies$and$Human$Rights.$$

Despite!the!law!and!facts,!the!stark!reality!remains!that!governments!in!the!United!States!can!(and!do)!choose!to!do!absolutely!nothing!about!the!risks!of!sea!level!rise.!!!Emergency!managers!are!expected!to!assess!risks,!hazards,!and!potential!losses,!and!to!prepare!plans!to!mitigate!those!risks,!yet!the!Federal!Emergency!Management!Agency!does!not!mandate!the!consideration!of!estimated!sea!level!rise!in!hazard!mitigation.!In!low@lying!South!Florida,!despite!absolute!evidence!of!rising!seas!!and!even!with!periodic!tidal!flooding!triggering!National!Weather!Service!flood!warnings,!coastal!development!continues!to!boom.!Meanwhile,!in!Coastal!Virginia,!many!properties!have!been!repeatedly!flooded,!yet!there,!too,!properties!are!rebuilt.!Neither!federal!nor!state!law!have!mandated!or!even!proposed!large!scale!solutions!for!the!future.!!

Yet!every!day,!people!buy!homes,!committing!to!30@year!mortgages,!in!places!where!sea!level!rise!and!its!consequences!present!extraordinary!risks!–!perhaps!even!before!their!mortgage!has!been!paid!off.!!Bloomberg!characterized!the!situation!as!rational:!governments!encourage!the!building!boom!to!ensure!tax!revenue!to!deal!with!the!problems.!Perhaps!the!only!applicable!ethical!rule!is!an!old!one:!caveat!emptor!!Floods!are!projected!to!last!longer,!droughts!are!expected!to!increase!fire!risks,!saltwater!

intrusion!will!adversely!impacted!aquifers!and!freshwater!supplies,!and!sewer!and!septic!system!infrastructure!could!be!vulnerable.!Indeed,!climate!change!and!sea!level!rise!has!human!rights!implications.!Consider!the!following:!

• Article!25!of!the!United!Nations’!Universal!Declaration!of!Human!Rights!suggests!that!everyone!has!a!right!to!housing!and!security,!even!in!circumstances!beyond!our!control.!!!

• Article12!of!the!International!Covenant!on!Economic!Social!and!Cultural!Rights!which!recognizes!a!right!to!physical!and!mental!health,!has!been!interpreted!to!include!a!right!to!safe!drinking!water!and!sufficient!sanitation.!!!

• The!Republic!of!the!Marshall!Islands,!fearing!the!potential!loss!of!their!national!lands!as!a!result!of!sea!level!rise,!has!submitted!a!resolution!to!the!United!Nations!decrying!the!threats!to!the!human!rights!to!life,!property,!culture,!food,!housing,!health!and!water.!

• John!Ruggie,!in!a!UN!Report,!Framework!for!Business!and!Human!Rights,!explained!the!minimum!responsibilities!of!corporations!to!ensure!that!human!rights!are!realized.!First,!he!emphasized!governments’!duty!to!protect!against!human!rights!abuses!by!third!parties,!including!businesses!(which,!of!course,!suggests!the!need!for!corporations!to!comply.)!Second,!he!noted!businesses’!responsibility!to!respect!all!human!rights.!Third,!he!acknowledged!the!need!for!more!effective!access!to!remedies!for!people!affected!by!corporate!related!human!rights!abuses.!

But!will!remedies!exist?!Decision!paralysis!could!leave!insufficient!time!for!planning!and!implementation!of!solutions.!Insured!losses!for!the!global!insurance!industry!due!to!weather!related!events!have!already!risen!dramatically:!from!$6.4!billion!per!year!in!the!1980s!to!$40!billion!for!the!first!decade!of!the!2000’s.!As!a!result,!insurance!becomes!more!costly!and!less!available.!In!Florida,!the!state!already!bears!the!risks!of!insurance!for!many!coastal!properties,!and!the!prices!of!insurance!continue!to!rise.!!In!Coastal!Virginia,!many!areas!are!below!the!floodlines,!and!cannot!be!insured!at!all.!Our!political!leadership!may!be!waiting!for!the!uninsured!catastrophe!to!force!action.!But!by!then,!it!may!already!be!too!late.!

V. Taking$the$High$Ground:$Professionalism$and$Corporate$Social$Responsibility.$

Professionals!have!duties!to!the!community!of!which!they!are!a!part.!Among!them!are!restrictive!duties!not!to!lie,!and!affirmative!duties!to!inform.!Speculations!that!scientists!are!wrong,!and!deflections!about!“scientific!uncertainty,”!do!not!conform!with!those!duties.!In!truth,!the!ethical!questions!that!must!be!asked!by!each!profession!are!certain.!Are!the!planners!really!providing!adequate,!timely,!clear!and!accurate!information!on!planning!issues?2!Are!the!architects!engaged!in!false!statements!of!material!fact,!or!conduct!involving!the!wanton!disregard!of!the!rights!of!others?3!Are!the!civil!engineers!being!honest!and!impartial!and!serving!with!fidelity!the!public?4!Have!the!realtors!concealed!pertinent!facts!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!2!AICP!Code!of!Ethics,!https://www.planning.org/ethics/ethicscode.htm!3!American!Institute!of!Architects!Code!of!Ethics!and!Professional!Conduct,!Rule!of!Conducts!2.106!and!2.104!and!4.103!available!at!http://www.aia.org/aiaucmp/groups/aia/documents/pdf/aiap074122.pdf!4!http://www.asce.org/Ethics/Code@of@Ethics/!

relating!to!the!property!or!the!transaction?5!And!are!the!compliance!professionals!really!ensuring!that!

the!companies!are!acting!with!honesty,!fairness!and!diligence?6!And!have!the!lawyers!participated!in!a!

client’s!fraud,!or!otherwise!failed!to!disclose!material!facts!to!their!clients!or!third!parties?!!

To!adapt!to!the!coming!changes,!and!to!engage!in!truly!ethical!behaviors,!the!real!estate!and!land!use!

development!professionals!must!embrace!their!own!professional!aspirations!and!their!employers!and!

clients!must!engage!in!corporate!social!responsibility.!!

• The!planners!should!emphasize!the!rights!of!others,!demonstrate!concern!for!the!long@range!

consequences!of!present!actions,!and!promote!“excellence!of!design!and!endeavor!to!conserve!

and!preserve!the!integrity!and!heritage!of!the!natural!and!built!environment.”7!!

• The!ethical!codes!of!both!the!architects!and!the!civil!engineers!call!for!a!focus!upon!sustainable!

communities.!Architects!should!“should!advocate!the!design,!construction,!and!operation!of!

sustainable!buildings!and!communities,”8!and!civil!engineers!should!“hold!paramount!the!safety,!

health!and!welfare!of!the!public!and!shall!strive!to!comply!with!the!principles!of!sustainable!

development!in!the!performance!of!their!professional!duties.”9!The!engineers’!ethical!code!even!

adds!a!definition!of!sustainable!development:!“the!process!of!applying!natural,!human,!and!

economic!resources!to!enhance!the!safety,!welfare,!and!quality!of!life!for!all!of!society!while!

maintaining!the!availability!of!the!remaining!natural!resources.”10!!

• As!for!the!lawyers,!they!have!a!discretionary!duty!to!advise!their!client,!rendering!candid!advice,!

even!on!matters!of!economics,!politics!and!morality,!and!the!Preamble!to!the!Rules!of!

Professional!Conduct!notes!that!lawyers,!as!members!of!a!learned!profession,!“should!cultivate!

knowledge!of!the!law!beyond!its!use!for!clients”!and!“employ!that!knowledge!in!reform!of!the!

law.”!!

But!perhaps!the!preamble!to!the!realtor’s!code!of!ethics!says!it!best:!

Under!all!is!the!land.!Upon!its!wise!utilization!and!widely!allocated!ownership!depend!

the!survival!and!growth!of!free!institutions!and!of!our!civilization.!Realtors!should!

recognize!that!the!interests!of!the!nation!and!its!citizens!require!the!highest!and!best!

use!of!the!land!and!the!widest!distribution!of!land!ownership.!They!require!the!creation!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!5National!Association!of!Realtor’s!Code!of!Ethics,!http://www.realtor.org/mempolweb.nsf/pages/code!6!Society!for!Corporate!Compliance!and!Ethics,!Code!of!Professional!Ethics!for!Compliance!and!Ethics!Professionals,!!Rule!3.1!available!at!http://www.corporatecompliance.org/Portals/1/Users/169/29/60329/SCCE%20Code%20Of%[email protected]!!7!American!Institute!of!Certified!Planners,!in!its!Code!of!Ethics!and!Professional!Conduct,!https://www.planning.org/ethics/ethicscode.htm!8!American!Institute!of!Architects!Code!of!Ethics!and!Professional!Conduct,!Canon!VI,!Ethical!Standard!E.S.!6.2!(Sustainable!Development)!available!at!http://www.aia.org/aiaucmp/groups/aia/documents/pdf/aiap074122.pdf!!9!American!Society!of!Civil!Engineers!Code!of!Ethics,!http://www.asce.org/Ethics/Code@of@Ethics/!!10!American!Society!of!Civil!Engineers!Code!of!Ethics,!http://www.asce.org/Ethics/Code@of@Ethics/!!

of!adequate!housing,!the!building!of!functioning!cities,!the!development!of!productive!

industries!and!farms,!and!the!preservation!of!a!healthful!environment.11!

In!the!foreseeable!future,!our!cities!might!not!function,!and!some!lands!may!be!under!the!sea.!When!it!

comes!to!confront!the!truths!of!sea!level!rise,!the!evidence!suggests!that!our!many!real!estate!

professions!are!falling!far!short!of!their!professional!aspirations.!The!corporate!employers!and!clients!

must!help,!too.!Mere!compliance!with!law!is!not!enough!when!there!are!questions!as!to!whether!a!

company’s!real!estate!endeavors!fail!to!protect!human!rights.!Principles!of!corporate!social!

responsibility!must!apply.!!

Consider!the!guidance!offered!by!the!Urban!Land!Institute,!an!80@year!old!international!interdisciplinary!

organization!dedicated!to!“creating!and!sustaining!thriving!communities!worldwide,”!even!published!its!

Ten!Principles!for!Coastal!Development.12!Many!of!the!principles!focus!on!safety!and!sustainability.

13!

The!10th!principle!–!“Commit!to!Stewardship!That!Will!Sustain!Coastal!Areas”!–!provides!a!noteworthy!

insight!on!the!role!of!corporations!in!coastal!development.!!Achieving!sustainable!development!requires!

the!corporation!to!become!a!partner!with!the!public!sector!and!the!community!as!a!whole:!!

To!effectively!implement!a!program!of!sustainable!development,!the!community!must!share!a!vision!

of!its!future.!This!vision!involves!a!strategy!for!implementation,!which!includes!funding!mechanisms!

(public!and!private),!potential!partners!(and!their!responsibilities),!and!an!agenda!or!time!frame!for!

achieving!the!vision.!One!way!to!implement!the!strategy!to!achieve!the!vision!is!to!build!

partnerships!that!maximize!benefits!for!the!community!and!the!environment.!A!partnership!is!a!

process,!not!a!product.!Successful!navigation!through!the!process!results!in!benefits!for!all!parties.!

Unfortunately,!the!voluntary!conduct!of!an!honorable!few!will!not!suffice.!In!the!absence!of!a!well@

planned,!coordinated,!and!comprehensive!public!and!private!sector!response!to!the!real!threats!of!

climate!change,!the!entire!community!will!remain!at!risk.!The!status!quo!–!allowing!some!to!engage!in!

blissful!or!intentional!ignorance,!or!worse!yet,!in!tortious!misconduct!and!denials!–!is!simply!

unacceptable.!Whether!physical!or!metaphysical,!one!breach!in!the!levee!still!means!widespread!floods.!

Instead,!everyone!should!be!held!to!the!highest!standards!of!ethics!and!corporate!social!responsibility..!!

Ethical!and!responsible!behavior!by!the!business!community,!including!the!professionals!and!the!

corporations,!requires!leadership,!informing!the!people!and!consumers,!and!partnering!with!our!public!

sector!leaders,!to!protect!the!public!interest!and!to!ensure!a!sustainable!future.!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!11!National!Association!of!Realtor’s!Code!of!Ethics,!http://www.realtor.org/mempolweb.nsf/pages/code!!

12!Urban!Land!Institute,!Ten!Principles!for!Coastal!Development!available!at!www.uli.org/wp@content/uploads/ULI@

Documents/Ten@Principles@for@[email protected]!!The!organization’s!members!include!developers,!

builders,!property!owners,!investors,!architects,!public!officials,!planners,!real!estate!brokers,!appraisers,!

attorneys,!engineers,!financiers,!academics,!students,!and!librarians.!13!The!ten!principles!are!(1)!Enhance!Value!by!Protecting!and!Conserving!Natural!Systems;!(2)!Identify!Natural!

Hazards!and!Reduce!Vulnerability;!(3)!Apply!Comprehensive!Assessments!to!the!Region!and!Site;!(4)!Lower!Risk!by!

Exceeding!Standards!for!Siting!and!Construction;!(5)!Adopt!Successful!Practices!from!Dynamic!Coastal!Conditions;!

(6)!Use!Market@Based!Incentives!to!Encourage!Appropriate!Development;!(7)!Address!Social!and!Economic!Equity!

Concerns;!(8)!Balance!the!Public’s!Right!of!Access!and!Use!with!Private!Property!Rights;!(9)!Protect!Fragile!Water!

Resources!on!the!Coast;!and!(10)!Commit!to!Stewardship!That!Will!Sustain!Coastal!Areas.!Id.#

![[Shiseido’s Corporate Social Responsibility] · Shiseido's Corporate Social Responsibility Back Issues 2010 [Shiseido’s Corporate Social Responsibility] "Beautiful Society, Bright](https://static.fdocuments.us/doc/165x107/5f170ccfbe73e76f437bb14c/shiseidoas-corporate-social-responsibility-shiseidos-corporate-social-responsibility.jpg)