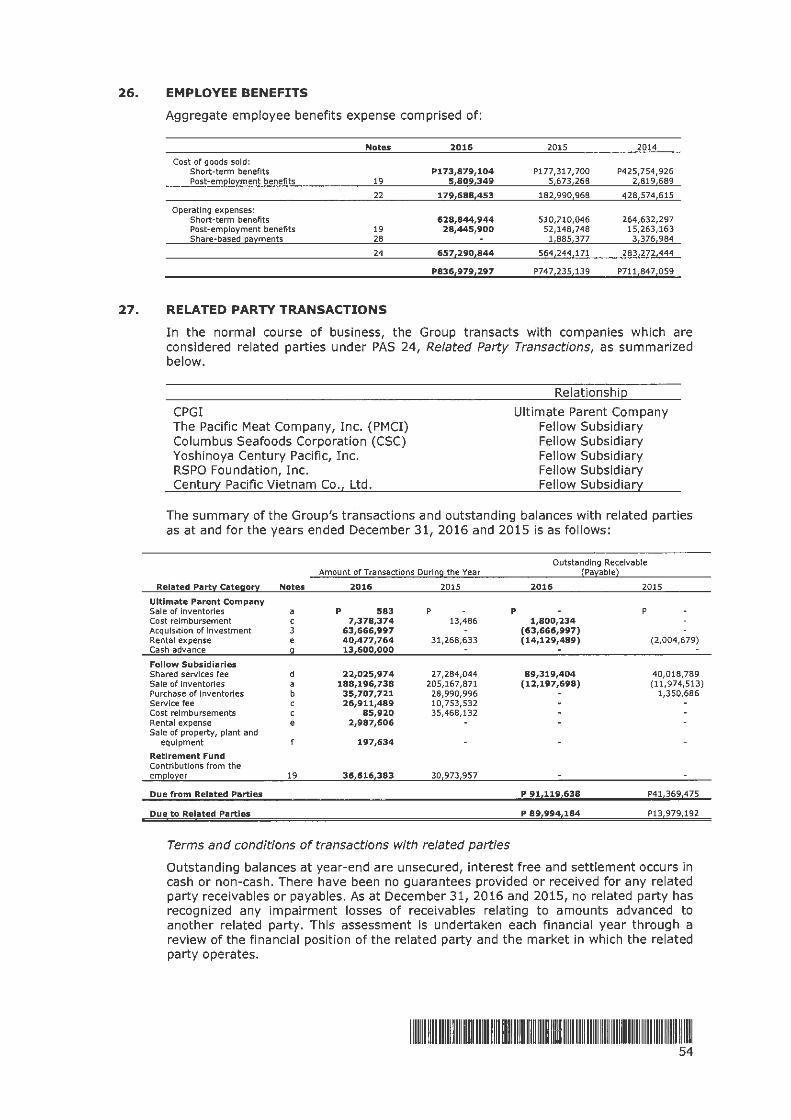

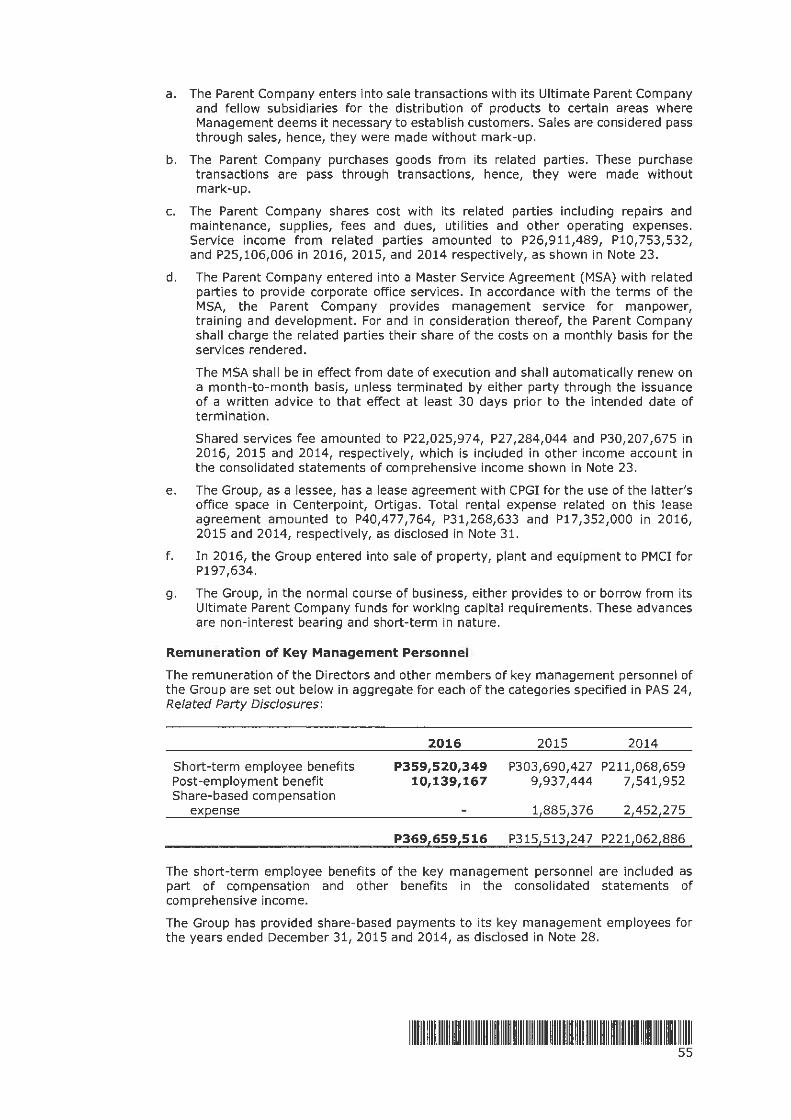

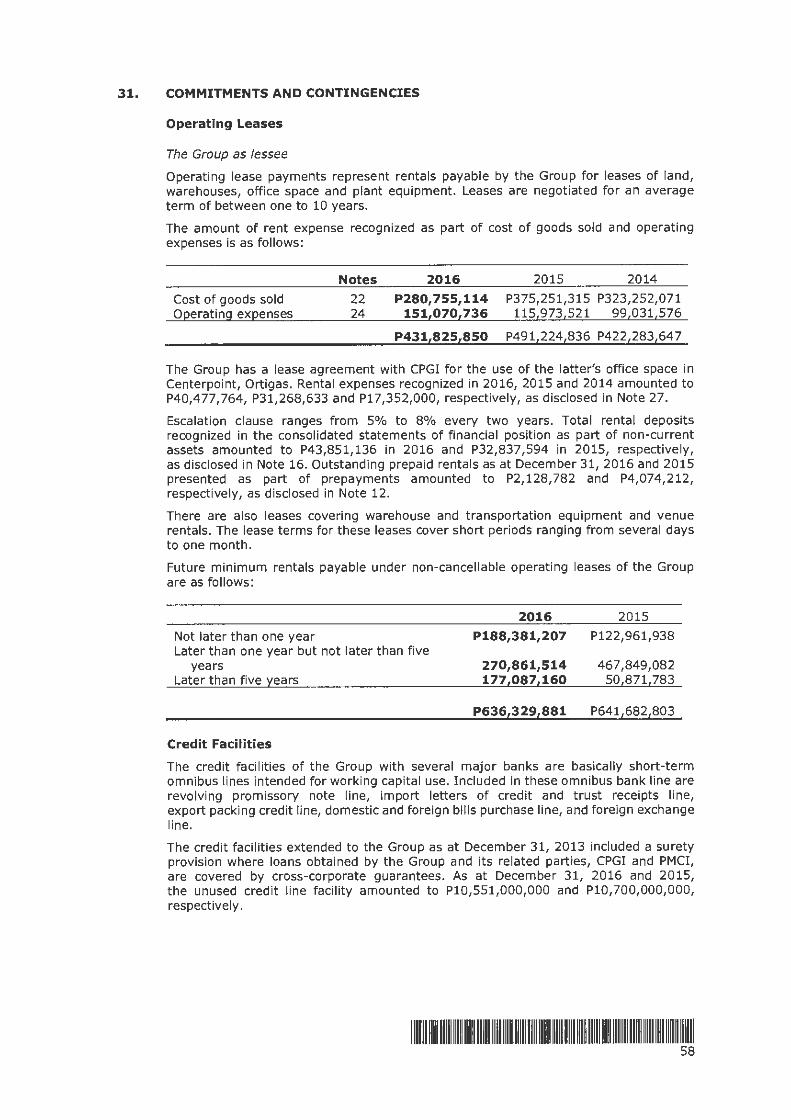

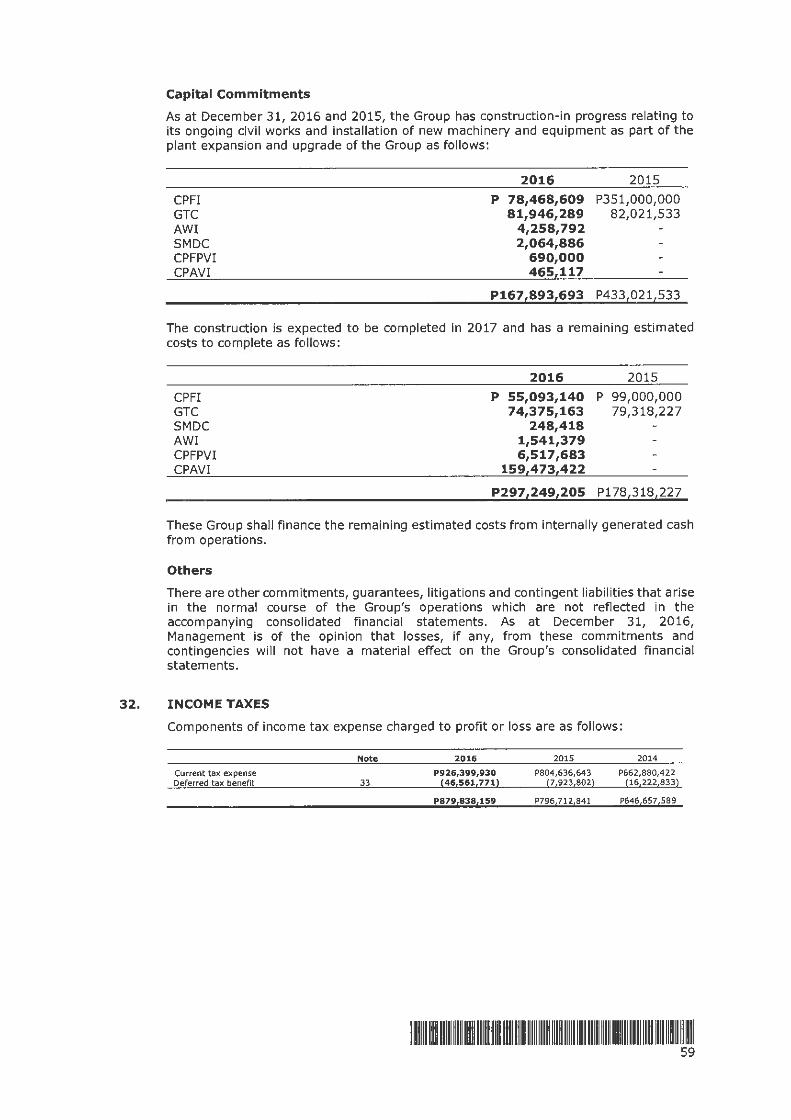

cl D I I I I - centurypacific.com.ph Reporting/ANNEX... · Amper & Co. which is the external...

81

C s 7 J C M E NIT u R y p u ej s D A R I I Principa TjH F L olo R u IL A vi A R EIN T E R , I p AIN L A I Form Type I A I A IF Is I Company's Email Address N.A. No. of Stockholders 22 . l COVER SHEET for AUDITED FINANCIAL STATEMENTS SEC Registration Number Company Name A C F I C FI 0 0 D IN cl AIN E s I I I I I I I I I I I I Office (No./S reet/Barangay/C ty/Town)Province) le E NjT E R p 0 I GjA s s T 0 Al s GI C T y I I Department requiring the report COMPANY INFORMATION Company's Telephone Number/s 633-8555 Annual Meeting Month/Day 6/30 N R CONTACT PERSON INFORMATION Tl B L D GI I , Tl G A s I I Mj E T R 0 I I I I I Secondary license Type, If Applicable Mobile Number N.A. Fiscal Year Month/Day 12/31 The designated contact person MUST be an Officer of the Corporati on Name of Contact Person Email Address Telephone Number/ s Mobile Number D MANUEL Z. GONZALES I [email protected] I 687-1195 I 1 0918-843-8888 Contact Person's Address 7TH FLOOR CENTERPOINT BLDG., JULIA VARGAS ST., ORTIGAS CENTER, PASIG CITY, METRO MANILA Note l: In case of d .. th, resicnatlon or cessation of office of the officer designated as contact person, such Incident shall be reported to the Commimlssl on within thirty (30) calendar days from the occurrence thereof with Information and complete contm details of teh new contact person desl&nated 2: All Boxes must be properly and completely filled-up. Failure to do so shall cause the delay In updating the corporation's records with the Commission and/ or non-receipt of Notice of Deficiencies. Futher, non-receipt of Notice of Oefeclencl es shall not excwe the corporation from liability for Its deficiencies. 111~1 111111 1 1111 1 111 11 ~II ~ 11111 1 111~ 11111 !Ii 11111 I~ 11!11 I~ 1 111 11 1111 ~ Ill 11 111 11

Transcript of cl D I I I I - centurypacific.com.ph Reporting/ANNEX... · Amper & Co. which is the external...

C

s

7

J

C M

E NIT u R y p

u ej s D A R

I I

Principa TjH F L olo R

u IL A vi A R

EIN T E R , I p

AIN L A I Form Type

I A I A IF Is I

Company's Email Address

N.A.

No. of Stockholders

22

. l

COVER SHEET for

AUDITED FINANCIAL STATEMENTS

SEC Registration Number

Company Name A C F I C FI 0 0 D IN cl AIN

E s I I I I I I I I I I I I

Office (No./S reet/Barangay/C ty/Town)Province) le E NjT E R p 0 I

GjA s s T 0

Al s GI C T y

I I Department requiring the report

COMPANY INFORMATION

Company's Telephone Number/s

633-8555

Annual Meeting Month/Day

6/30

N

R

CONTACT PERSON INFORMATION

Tl B L D GI I , Tl G A s I I Mj E T R 0 I I

I I I Secondary license Type, If Applicable

Mobile Number

N.A.

Fiscal Year Month/Day

12/31

The designated contact person MUST be an Officer of the Corporation

Name of Contact Person Email Address Telephone Number/s Mobile Number

D

MANUEL Z. GONZALES I [email protected] I 687-1195 I 1 0918-843-8888

Contact Person's Address

7TH FLOOR CENTERPOINT BLDG., JULIA VARGAS ST., ORTIGAS CENTER, PASIG CITY, METRO MANILA

Note l : In case of d .. th, resicnatlon or cessation of office of the officer designated as contact person, such Incident shall be reported to the Commimlsslon within thirty (30) calendar days from the occurrence thereof with Information and complete contm details of teh new contact person desl&nated

2: All Boxes must be properly and completely filled-up. Failure to do so shall cause the delay In updating the corporation's records with the Commission and/or non-receipt of Notice of Deficiencies. Futher, non-receipt of Notice of Oefeclencles shall not excwe the corporation from liability for Its deficiencies.

111~1 ~I~ 11111111111111111 ~II ~111111111~ 11111 !Ii 11111 I~ 11!11 I~ 1111111111 ~Ill 1111111

( (

CENTURY PACIFIC FOOD INC.

Centerpoint Building Julia Vargas Ave.,

Ortigas Center Pasig City, Metro Manila

Philippines

Tel : {632} 633 8555

Fax : (632} 638 6336

website : www.centurypacific.com.ph

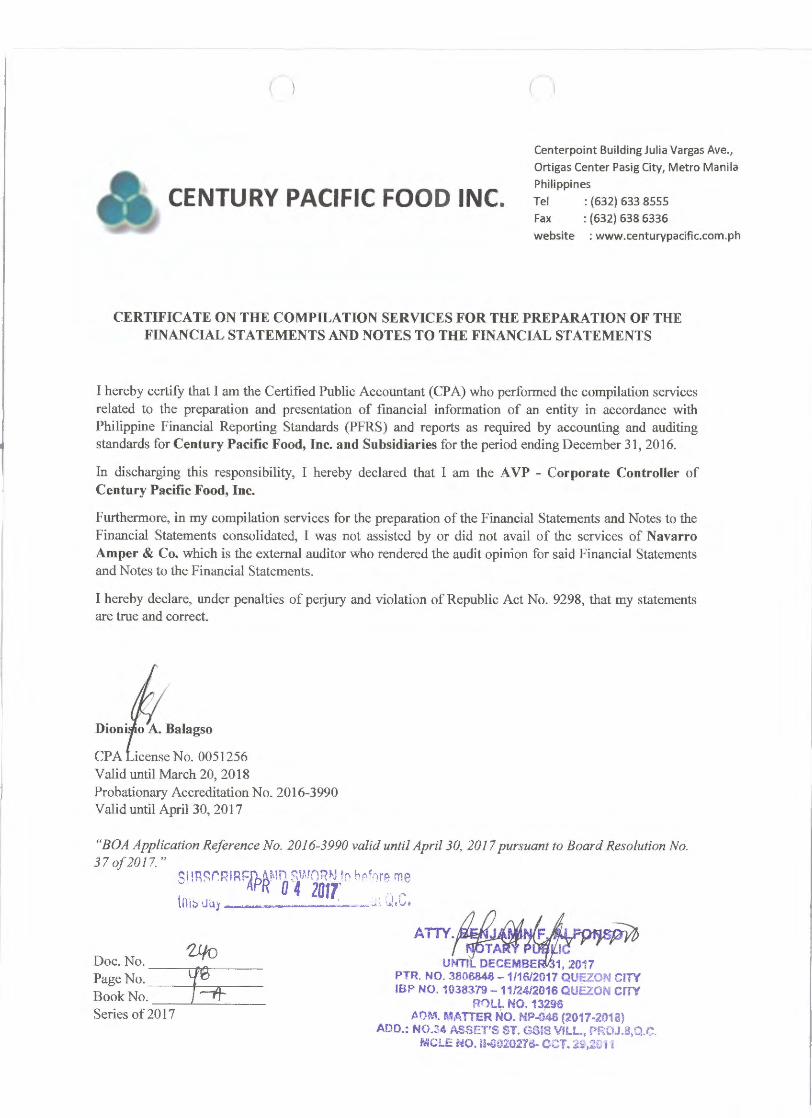

CERTIFICATE ON THE COMPILATION SERVICES FOR THE PREPARATION OF THE FINANCIAL STATEMENTS AND NOTES TO THE FINANCIAL STATEMENTS

I hereby certify that I am the Certified Public Accountant (CPA) who performed the compilation services related to the preparation and presentation of financial information of an entity in accordance with Philippine Financial Reporting Standards (PFRS) and reports as required by accounting and auditing standards for Century Pacific Food, Inc. and Subsidiaries for the period ending December 31, 2016.

In discharging this responsibility, I hereby declared that I am the A VP - Corporate Controller of Century Pacific Food, Inc.

Furthermore, in my compilation services for the preparation of the Financial Statements and Notes to the Financial Statements consolidated, I was not assisted by or did not avail of the services of Navarro Amper & Co. which is the external auditor who rendered the audit opinion for said Financial Statements and Notes to the Financial Statements.

I hereby declare, under penalties of perjury and violation of Republic Act No. 9298, that my statements are true and correct.

CPA icense No. 0051256 Valid until March 20, 2018 Probationary Accreditation No. 2016-3990 Valid until April 30, 201 7

"BOA Application Reference No. 2016-3990 valid until April 30, 2017 pursuant to Board Resolution No. 37 o/2017."

SI !R~r:R11:u:Af>R1 .. 1r, S'W)R"J '0 hr'."'rP. me 0 4 201T .

1 ,,

tni~ uu1 • --~' ..... ..,.

Via Doc. No.--~-----Page No. ---------+-----qe-_ BookNo. T=if __ _,__ ___ _ Series of 201 7

T y UNTIL OECEMBE 1, :Z017

PTR. NO. 3800846 - 1/16/2017 QUEZON CITY IBP NO. 1038371J-11/2412016 QUEZON CITY

RnLL N0.13296 J\OM. MATIER NO. NP-048 (2017-2018)

ADO.: N0.34 ASSET'S ST. GSIS 'i/lLL., f>ROJ.8,Q.C. MCLE N0.11~02027~-CCT. 29,2011

CENTURY PACIFIC FOOD INC.

(

Centerpoint Building Julia Vargas Ave., Ortigas Center Pasig City, Metro Manila Philippines Tel : (632) 633 8555 Fax : (632) 638 6336 website : www.centurypacific.com.ph

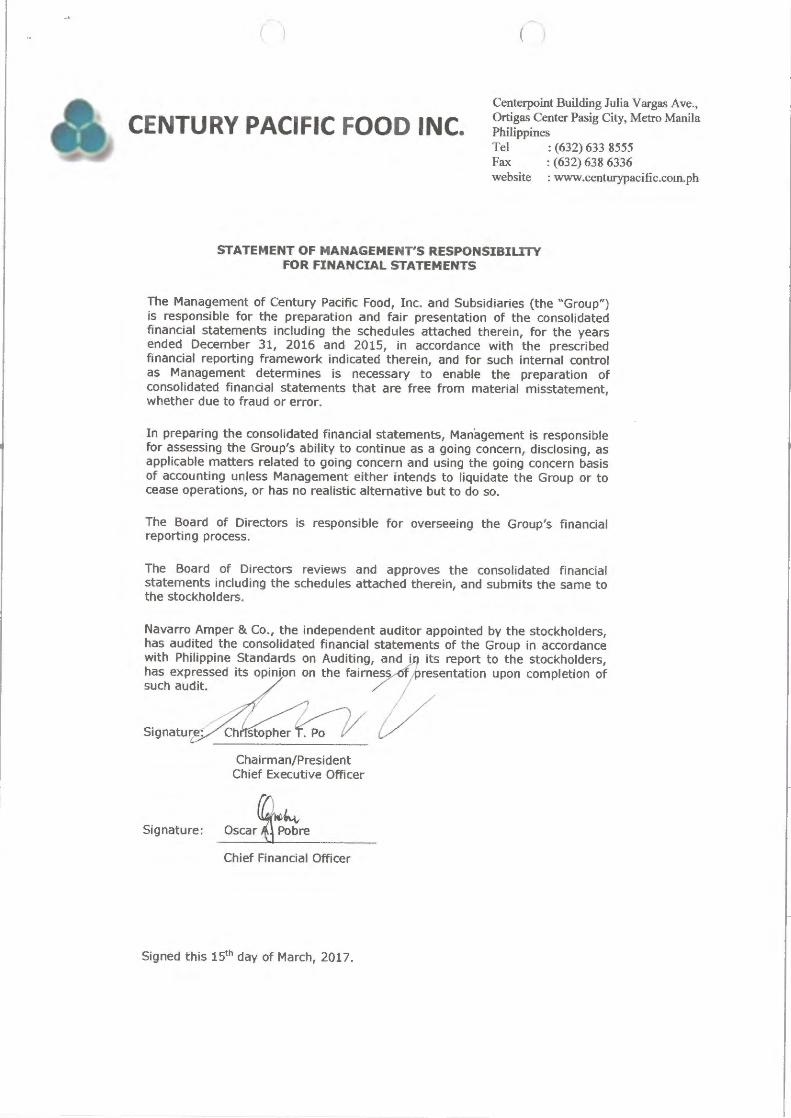

STATEMENT OF MANAGEMENT'S RESPONSIBILITY FOR FINANCIAL STATEMENTS

The Management of Century Pacific Food, Inc. and Subsidiaries (the "Group") is responsible for the preparation and fair presentation of the consolidated financial statements including the schedules attached therein, for the years ended December 31, 2016 and 2015, in accordance with the prescribed financial reporting framework indicated therein, and for such internal control as Management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, Management is responsible for assessing the Group's ability to continue as a going concern, disclosing, as applicable matters related to going concern and using the going concern basis of accounting unless Management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

The Board of Directors is responsible for overseeing the Group's financial reporting process.

The Board of Directors reviews and approves the consolidated financial statements including the schedules attached therein, and submits the same to the stockholders.

Navarro Amper & Co., the independent auditor appointed by the stockholders, has audited the consolidated financial statements of the Group in accordance with Philippine Standards on Auditing,nnd i its report to the stockholders, has expressed its opinion on the fairnes resentation upon completion of such audit.

Signatu, : stophec ~ / Chairman/President

Chief Executive Officer

Signature: Osca,~e

Chief Financial Officer

Signed this 15th day of March, 2017.

( ) ( \

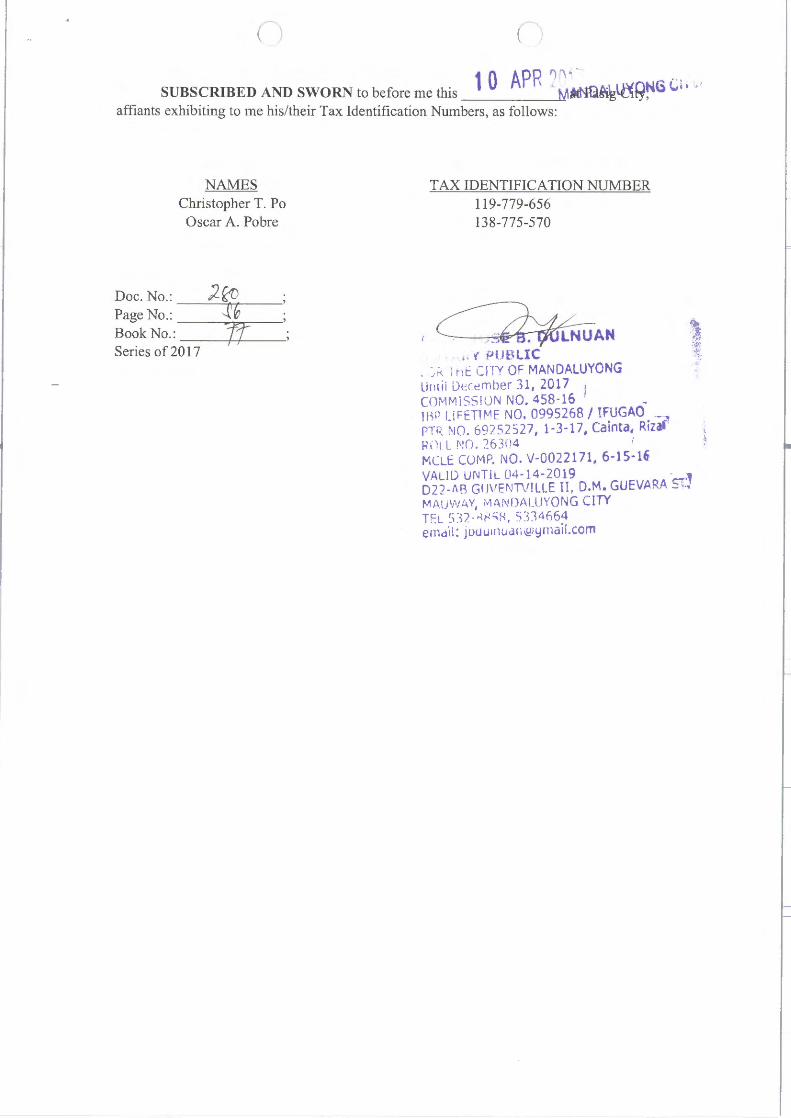

SUBSCRIBED AND SWORN to before me this affiants exhibiting to me his/their Tax Identification Numbers, as follows:

NAMES Christopher T. Po

Oscar A. Pobre

Doc.No.: 2~ -----,~......,.._,/: -Page No.: ___ "-\_...,..~ .---

Book No.: ---Yf+-+--Series of 201 7

TAX IDENTIFICATION NUMBER 119-779-656 138-775-570

~ ·l ;~

.. t PUBLIC , . . · ,,. , r1t CJTY OF MANDALUYONG U1lli i D(:Cember 31, 2017 l COMMISSION NO. 458-16 · _ IIW !_i FETlMt NO, 0995268 / !F,UGAO. ~ PTI< NO. 692 52527, 1-3-17, Cainta, Rtzar Ri)t l. r,!(). 263(14 I

MCLE COM P. NO. V-0022171, 6-15-16 VALID UNTIL 04-14-2019 · .1 D22 -t. B GIJ\IENTV!LLE II , D.M. GUEVARA S.J MAuw.,w, M,\ Nf)Af_LJYONG CITY Tf:L 5'.Q->l~;H, S314n6~ en1d·il: joou1nua1o~ymail.com

NavarroAmper&Co.

SUPPLEMENTAL WRITIEN STATEMENT OF AUDITORS

To the Board of Directors and Shareholders CENTURY PACIFIC FOOD, INC (A Subsidiary of Century Pacific Group, Inc.) 7th Floor, Centerpoint Building, Julia Vargas St., Ortigas Center Pasig City, Metro Manila

Gentlemen:

Navarro Amper & Co. 19th Floor Net Lima Plaza 5th Avenue corner 26th Street Bonifacio Global City, Taguig 1634 Philippines

Tel: +63 (2) 581 9000 Fax: +63 (2) 869 3676 www.deloitte.com/ph

BONPRC Reg. No. 0004 SEC Accreditation No. 0001-FR-4

We have audited the consolidated financial statements of Century Pacific Food, Inc. and Subsidiaries for the year ended December 31, 2016 in accordance with Philippine Standards on Auditing, on which we have rendered the attached report dated March 17, 2017. In connection with our audit, we wish to state that the Company is listed with the Philippine Stock Exchange.

Navarro Amper & Co _ BOA Registration No. 0004, valid from December 4, 2015 to December 31, 2018 SEC Accreditation No. 0001-FR-4, issued on January 7, 2016; effective until January 6, 2019, Group A TIN 005299331

By :

-Bonifacio F. Lumacang, Jr. Partner CPA License No. 0098090 SEC A.N. 0526-AR-3, issued on April 21, 2016; effective until April 21, 2019, Group A TIN 170035681 BIR A.N. 08-002552- 18-2015, issued on February 6, 2015; effective until February 5, 2018 PTR No. A-3264646, issued on January 5, 2017, Taguig City

Taguig City, Philippines March 17, 2017

Deloitte. llllllllllll lllll llllllllllllllllllllllllllllll llllllllll 1111111111111111111111111111111111111111111111111111111111

t-

i

NavarroAmper&Co. Navarro Amper & Co. 19th Floor Net Lima Plaza 5th Avenue corner 26th Street Bonifacio Global City, Taguig 1634 Philippines

• INDEPENDENT AUDITORS' REPORT

To the Stockholders and the Board of Directors CENTURY PACIFIC FOOD, INC. (A Subsidiary of Century Pacific Group, Inc.) 7m Floor, Centerpoint Building, Julia Vargas St., Ortigas Center Pasig City, Metro Manila

Opinion

Tel: +63 (2) 581 9000 Fax: +63 (2) 869 36 76 www.delo1tte.com/ph

BONPRC Reg. No. 0004 SEC Accreditation No. 0001-FR-4

We have audited the consolidated financial statements of Century Pacific Food, Inc. and Subsidiaries (the "Group") which comprise the consolidated statements of financial position as at December 31, 2016 and 2015, and the consolidated statements of comprehensive income, consolidated statements of changes in equity and consolidated statements of cash flows for the years ended December 31, 2016, 2015 and 2014, and the notes to the consolidated financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of the Group as at December 31, 2016 and 2015, and of its financial performance, and cash flows for the years ended December 31, 2016, 2015 and 2014, in accordance with Philippine Financial Reporting Standards (PFRSs).

Basis for Opinion

We conducted our audits in accordance with Philippines Standards on Auditing (PSAs). Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Group in accordance with the Code of Ethics for Professional Accountants in the Philippines (Code of Ethics), together with the ethical requirements that are relevant to our audit of the consolidated financial statements in the Philippines, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the Code of Ethics. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Deloitte. lllllll lllllllllllllll lll~IIIIIIIIII IIIIIIIIII IIIII IIIII IIIII IIIIIIIIII IIIII IIIIIIIIIIII IIIIIIIIIIIIIIII

Navarr0Am~2r<&Co.

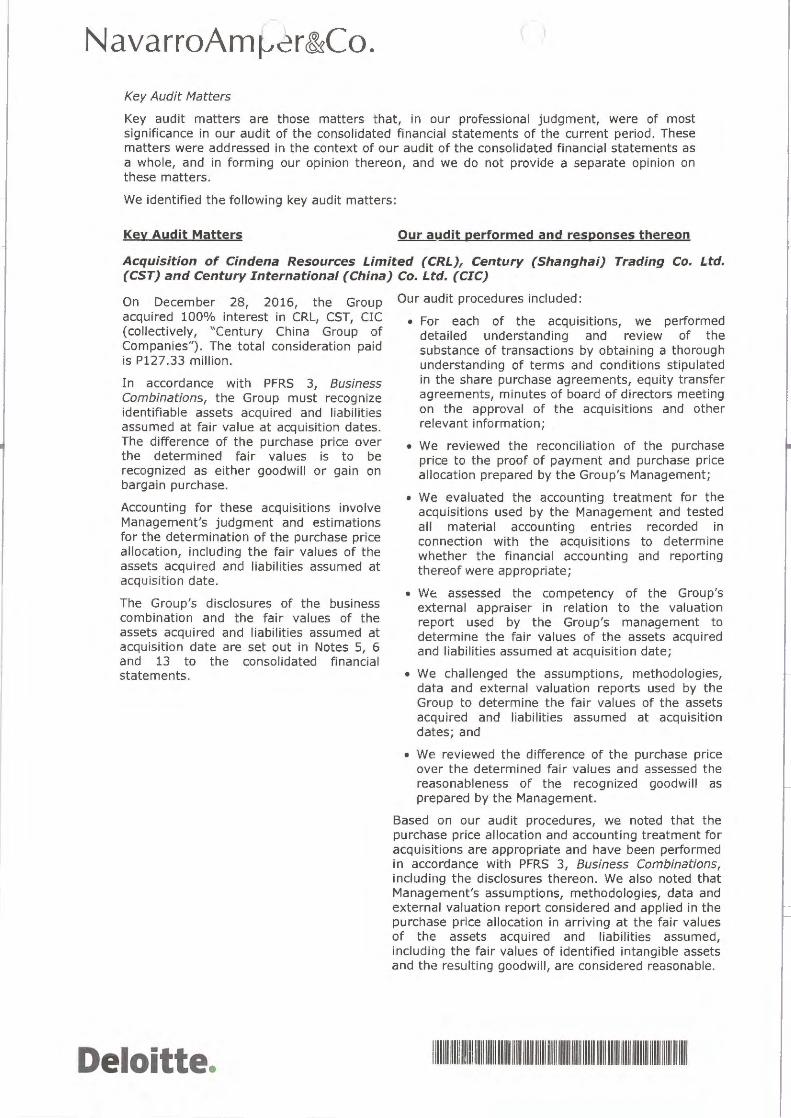

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

We identified the following key audit matters:

Key Audit Matters Our audit performed and responses thereon

Acquisition of Cindena Resources Limited (CRLJ, Century (Shanghai) Trading Co. Ltd. (CST) and Century International (China) Co. Ltd. (CIC)

On December 28, 2016, the Group acquired 100% interest in CRL, CST, CIC (collectively, "Century China Group of Companies"). The total consideration paid is P127.33 million.

In accordance with PFRS 3, Business Combinations, the Group must recognize identifiable assets acquired and liabilities assumed at fair value at acquisition dates. The difference of the purchase price over the determined fair values is to be recognized as either goodwill or gain on bargain purchase.

Accounting for these acquisitions involve Management's judgment and estimations for the determination of the purchase price allocation, including the fair values of the assets acquired and liabilities assumed at acquisition date.

The Group's disclosures of the business combination and the fair values of the assets acquired and liabilities assumed at acquisition date are set out in Notes 5, 6 and 13 to the consolidated financial statements.

Deloitte.

Our audit procedures included:

• For each of the acquisitions, we performed detailed understanding and review of the substance of transactions by obtaining a thorough understanding of terms and conditions stipulated in the share purchase agreements, equity transfer agreements, minutes of board of directors meeting on the approval of the acquisitions and other relevant information;

• We reviewed the reconciliation of the purchase price to the proof of payment and purchase price allocation prepared by the Group's Management;

• We evaluated the accounting treatment for the acquisitions used by the Management and tested all material accounting entries recorded in connection with the acquisitions to determine whether the financial accounting and reporting thereof were appropriate;

• We. assessed the competency of the Group's external appraiser in relation to the valuation report used by the Group's management to determine the fair values of the assets acquired and liabilities assumed at acquisition date;

• We challenged the assumptions, methodologies, data and external valuation reports used by the Group to determine the fair values of the assets acquired and liabilities assumed at acquisition dates; and

• We reviewed the difference of the purchase price over the determined fair values and assessed the reasonableness of the recognized goodwill as prepared by the Management.

Based on our audit procedures, we noted that the purchase price allocation and accounting treatment for acquisitions are appropriate and have been performed in accordance with PFRS 3, Business Combinations, including the disclosures thereon. We also noted that Management's assumptions, methodologies, data and external valuation report considered and applied in the purchase price allocation in arriving at the fair values of the assets acquired and liabilities assumed, including the fair values of identified intangible assets and the resulting goodwill, are considered reasonable.

illllllllllllllllllllllllll lllll lllll lllll lllllllllllllllllllllllll lllll llllllllllllllllllllll lllllllllll

Navarr0Am~2r&Co.

Key Audit Matters

Goodwill Impairment

Goodwill has been recognized in the consolidated statements of financial position resulting from acquisitions of the Group. Under PFRS, the Group is required to annually test the goodwill for impairment. This annual impairment test was significant to our audit because the aggregate balance of goodwill amounting to P2.95 billion is material to the consolidated financial statements and represents 14.81 % of the consolidated total assets of the Group as at December 31, 2016.

Under PFRS 3 and PAS 36, the Group is required to annually test the goodwill for impairment. Management conducts annual impairment test to assess the recoverability of the carrying values of goodwill. This annual impairment test involves a number of key sensitive judgments made in determining the inputs used in the assessment process.

The carrying values of goodwill as at December 31, 2016 are disclosed in Note 13 to the consolidated financial statements.

Deloitte.

Our audit performed and responses thereon

Our audit procedures were focused on performing a detailed understanding of the Management's assessment process and challenging the key sensitive judgments applied as follows:

• We reviewed the Group's position on the impairment of goodwill, including information about the Group's project plan, business outlook, revenue potential and market penetration assessment of the subsidiaries to which the goodwill relates to; and

• We assessed and challenged the reasonableness of the Group's position on the impairment of goodwill including consideration of various factors such as historical business performance, current year dev~lopments, current risk evaluations, business plans, outlook, revenue potential and other market considerations.

Based on our audit procedures, we have noted that the Group's assessment and the judgments used are reasonable .

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII

Navarr0Am~2r&Co.

Key Audit Matters

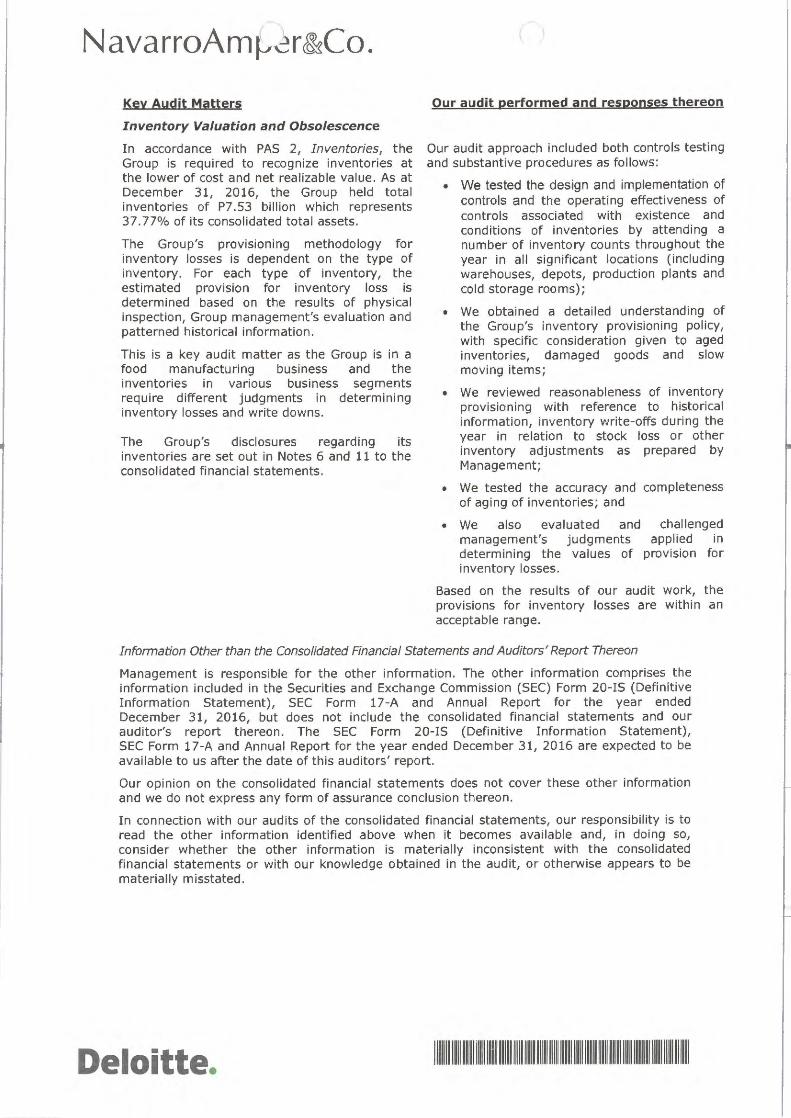

Inventory Valuation and Obsolescence

In accordance with PAS 2, Inventories, the Group is required to recognize inventories at the lower of cost and net realizable value. As at December 31, 2016, the Group held total inventories of P7 .53 billion which represents 37. 77% of its consolidated total assets.

The Group's prov1s1oning methodology for inventory losses is dependent on the type of inventory. For each type of inventory, the estimated prov1s1on for inventory loss is determined based on the results of physical inspection, Group management's evaluation and patterned historical information.

This is a key audit matter as the Group is in a food manufacturing business and the inventories in various business segments require different judgments in determining inventory losses and write downs.

The Group's disclosures regarding its inventories are set out in Notes 6 and 11 to the consolidated financial statements.

Our audit performed and responses thereon

Our audit approach included both controls testing and substantive procedures as follows:

• We tested the design and implementation of controls and the operating effectiveness of controls associated with existence and conditions of inventories by attending a number of inventory counts throughout the year in all significant locations (including warehouses, depots, production plants and cold storage rooms);

• We obtained a detailed understanding of the Group's inventory provisioning policy, with specific consideration given to aged inventories, damaged goods and slow moving items;

• We reviewed reasonableness of inventory provisioning with reference to historical information, inventory write-offs during the year in relation to stock loss or other inventory adjustments as prepared by Management;

• We tested the accuracy and completeness of aging of inventories; and

• We also evaluated and challenged management's judgments applied in determining the values of provision for inventory losses.

Based on the results of our audit work, the provisions for inventory losses are within an acceptable range.

Information Other than the Consolidated Financial Statements and Auditors' Report Thereon

Management is responsible for the other information. The other information comprises the information included in the Securities and Exchange Commission (SEC) Form 20-IS (Definitive Information Statement), SEC Form 17-A and Annual Report for the year ended December 31, 2016, but does not include the consolidated financial statements and our auditor's report thereon. The SEC Form 20-IS (Definitive Information Statement), SEC Form 17-A and Annual Report for the year ended December 31, 2016 are expected to be available to us after the date of this auditors' report.

Our opinion on the consolidated financial statements does not cover these other information and we do not express any form of assurance conclusion thereon.

In connection with our audits of the consolidated financial statements, our responsibility is to read the other information identified above when it becomes available and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or with our knowledge obtained in the audit, or otherwise appears to be materially misstated.

Deloitte. IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII

NavarroAmr.,~r&Co.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with PFRSs, and for such internal control as Management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, Management is responsible for assessing the Group's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless Management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Group's financial reporting process.

Auditors' Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with PSAs wi ll always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with PSAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by Management.

• Conclude on the appropriateness of Management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group's ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the Group to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Deloitte. 111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111

Navarr0Am~2r&Co.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor's report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

The engagement partner on the audit resulting in this independent auditor's report is Mr. Bonifacio F. Lumacang, Jr.

Navarro Amper & Co. BOA Registration No. 0004, valid from December 4, 2015 to December 31, 2018 SEC Accreditation No. 0001-FR-4, issued on January 7, 2016; effective until January 6, 2019, Group A TIN 005299331

By:

Bonifacio F. Lumacang, Jr. Partner CPA License No. 0098090 SEC A.N. 0526-AR-3, issued on April 21, 2016; effective until April 21, 2019, Group A TIN 170035681 BIR A.N. 08-002552-18-2015, issued on February 6, 2015; effective until February 5, 2018 PTR No. A-3264646, issued on January 5, 2017, Taguig City

Taguig City, Philippines March 17, 2017

Deloitte. IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII

(

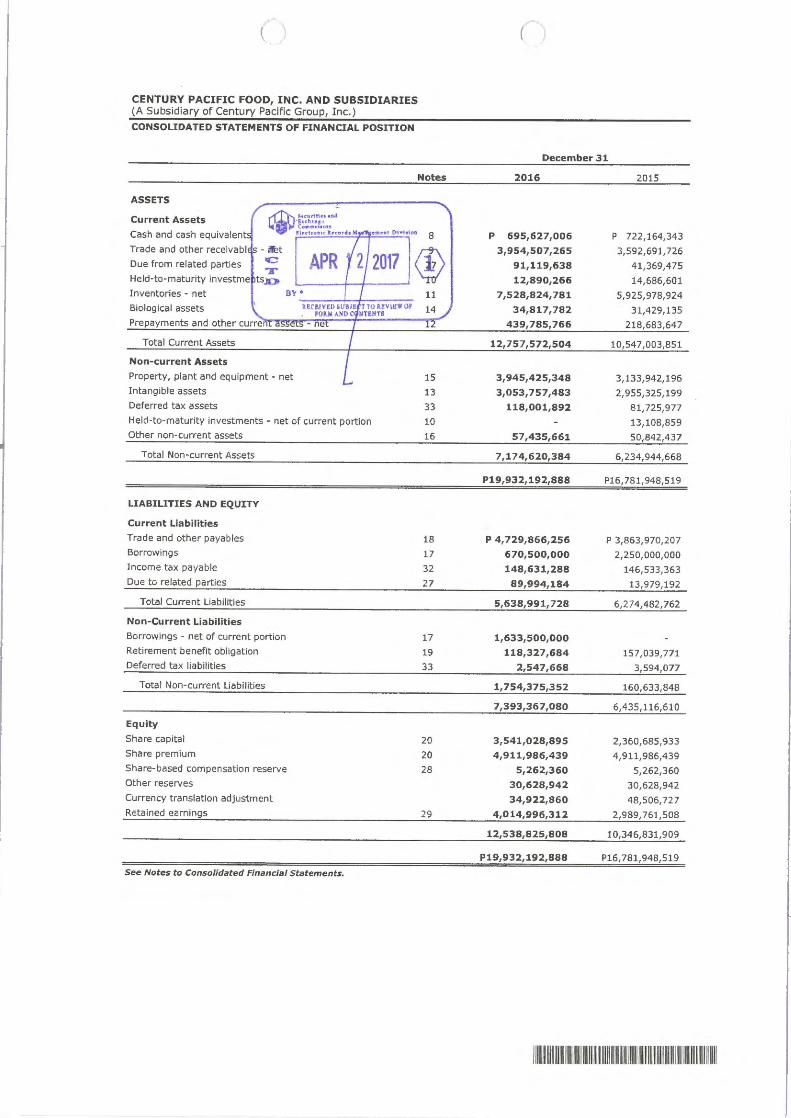

CENTURY PACIFIC FOOD, INC. AND SUBSIDIARIES (A Subsidiary of Century Pacific Group, Inc.)

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

Notes

ASSETS

Current Assets

Cash and cash equivalent

Trade and other recelvabl

Due from related parties

Held-to-maturity investme

Inventories • net

Biological assets

-Suur1Hn,M

· luhu•" c.-n•1os

Jl,ctte111c leur41 M • • nt EH.-1rin 8

11

14 Prepayments and other curr~e::,i,.."!'l"l~~ ~ r,;,.;,,.r,;,,;,;,,,,;,;,.. __ ___,r'l""""

Total Current Assets

Non-current Assets

Property, plant and equipment • net

Intangible assets

Deferred tax assets

Held-to-maturity investments • net of current portion

Other non-current assets

Total Non-current Assets

LIABILITIES AND EQUITY

Current Liabilities

Trade and other payables

Borrowings

Income tax payable

Due to related parties

Total Current Liabilities

Non-Current Liabilities

Borrowings • net of current portion

Retirement benefit obligation

Deferred tax liabilit ies

Total Non-current Liabilities

Equity

Share capital

Share premium

Share-based compensation reserve

Other reserves

Currency translat ion adjustment

Retained earnings

See Notes to Consolidated Financial Statements.

15

13

33

10

16

18

17

32

27

17

19

33

20

20

28

29

( )

December 31

2016 2015

p 695,627,006 p 722,164,343

3,954,507,265 3,592,691 ,726

91,119,638 41 ,369,475

12,890,266 14,686,601

7,528,824,781 5, 925,978,924

34,817,782 31,429,135

439,785,766 218, 683,647

12,757,572,504 10,547,003,851

3,945,425,348 3,133,942,196 3,053,757,483 2,955,325,199

118,001,892 81,725,977

13,108,859

57,435,661 50,842,437

7,174,620,384 6,234,944,668

P19,932,192,888 P16,781,948,519

P 4,729,866,256 P 3,863,970,207

670,500,000 2,250,000,000

148,631,288 146, 533, 363

89,994,184 13,979,192

5,638,991,728 6,274,482,762

1,633,500,000 118,327,684 157,039,771

2,547,668 3,594, 077

1,754,375,352 160,633,848

7, 393, 367,080 6,435,116,610

3,541,028,895 2,360,685,933 4 ,911,986,439 4,911,986,439

5 ,262,360 5,262,360 30,628,942 30,628,942

34,922,860 48,506,727

4,014,996,312 2,989,761,508

12,538,825,808 10,34 6,831,909

P19,932,192,88S P16,781,948,519

1111~~11 11111111111111 11~~1111111 m11111111111~111111~11111111 11m11111

CENTURY PACIFIC FOOD, INC, AND SUBSIDIARIES (A Subsidiary of Century Pacific Group, Inc.) CONSOUDATED STATEMENTS OF COMPREHENSIVE INCOME

Net Revenue, Cost of Goods Sold

Gro11 Profit Other Income

Operiitlng Expen1e1

Other Expenses

Finance Costs

Profit Before Tax

Income Tax Exeense

Profit for the Year

Other Comprehen11ve Income (Lou ) Jtem that wfll be recla11lned subsequently t o profit or 1011

Currency translatlon adjustments Ite m that will not be reclantned subsequently to proflt or 1011

Remeasurement 2a1ns ~losses) on retirement benefit obligation· net of tax

Total Comprehensive Income

Basic and DIiuted Earnings Per Share

See Notes to ConsoJJd•ted FJn• ncJ•J Statements.

Notes

21 22

23

24

25 17

32

19

30

For the Years Ended December 31

2016 2015 2014

P28,287,7 88, 370 P23,324,528,579 P20,438,555,008

19!677!984,326 17,128, 162,072 15,063,993,046

8,609,804, 0 44 6, 196,366,507 5,374,561,962

272,039,674 100, 151,771 190,857,007

8,881,843,718 6,296,518,278 5,565,418,969

5,217,647,358 3,529,030,226 3,272,303,364

51,334,489 35,942, 100 39,579,720

7 7,4 27,&50 1,158,333 15,287,944

5,3 4 6,409 497 3,566, 130,659 3 ,327, 171,028

3,535,434,221 2,730,387,619 2,238,247,941

879,838, 159 796,712,841 646,657,589

2 ,655,596,062 1,933,674,778 1,591,590,352

(13,583,867 ) 29,029, 136 5, 169,350

22,118,8 97 (24,203,701) (64,363,876)

8,535,030 4,825,435 (59,194,526)

P 2,6154,131,092 P 1,938,500,213 P 1,532,395,826

P0.7500 P0.8664 P0.7600

111111111111111111111

CENTURY PACIFIC FOOD, INC. AND SUBSIDI ARIES (A Subsidia~ of Centu~ Pacific Groue, Inq CONSOUDATED STATEMENTS OF CHANGES IN EQUITY

For the Years Ended December 31, 2016 , 2015 and 2014

Share -based Currency Retained Share Share Com pensation Other Translation Earnings

Notes Caeltal Premium Reserve Reserves Adjustment (Deficit} Total

Ba lance, January 1, 2014 20 Pl,500,000,000 p p P30,628,942 P14,308,241 (P 731,724} Pl,544,205,459

Profit for the year 1,591,590,352 1,591,590,352

Other comprehensive income (loss) : Currency translation adjustment 5,169,350 5,169,350

Remeasurement of retirement benefit obligation - net of tax 19 (64,363,876l (64,363,876l

Total Com(!rehenslve Income 5,169,350 1,527,226,476 1,532,395,826

Transaction with owners: Iss uance of share capital 20 P729,654,404 2,751,905,610 3,481,560,014

Subscription of capital stock 20 Pl ,367,200 17,431,800 18,799,000

Egui!;y-settled share-based com(lensatlon - net of tax 28 3,376,984 3,376,984

Balance, December 31, 2014 2,231,021,604 2,769,337,410 3,376,984 30,628,942 19,477,591 1,526,494,752 6,580,337,283

Profit for the year 1,933,674,778 1,933,674,778

Other comprehensive income (loss): Currency translation adjustment 29,029,136 29,029,136

Remeasurement of retirement benefit obligation - net of tax 19 (24,203,701) (24,203,701)

Total Coml!rehenslve Income 29,029,136 1,909,471,077 1,938,500,213

Transaction with owners: Issuance of share capital 20 129,664,329 2,142,649,029 2,272,313,358

Cash dividends 29 (446,204,321) (446,204,321)

Egui~ ·settled share-based comeensation - net of tax 28 1,885,376 1,885,376

Balance, December 311 2015 2,360,685,933 4,911,986,439 5,262,360 30,628,942 48,506,727 2,989,761,508 10,346,831,909

Profit for the year 2,655,596,062 2,655,596,062

Other comprehensive income (loss): Currency translation adjustment (13,583,867) (13,583,867)

Remeasurement of retirement benefit obligation - net of tax 19 22,118,897 22,118,897

Total Com(!rehenslve Income (13,583,867l 2,677,714,959 2,664,131,092

Transaction with owners:

Stock dividends 20, 29 1,180,342,962 (1,180,342,962)

Cash dividends 29 (472,137,193) (472,137,193)

Balance, December 31, 2016 P3,5411028,895 P4,911,986,439 P5,262,360 P30,628,942 P34,922,86 0 P4,0141996,312 P12,538,825,S0 8

See Notes to Consolidated Financial State ments.

111111111111111111111

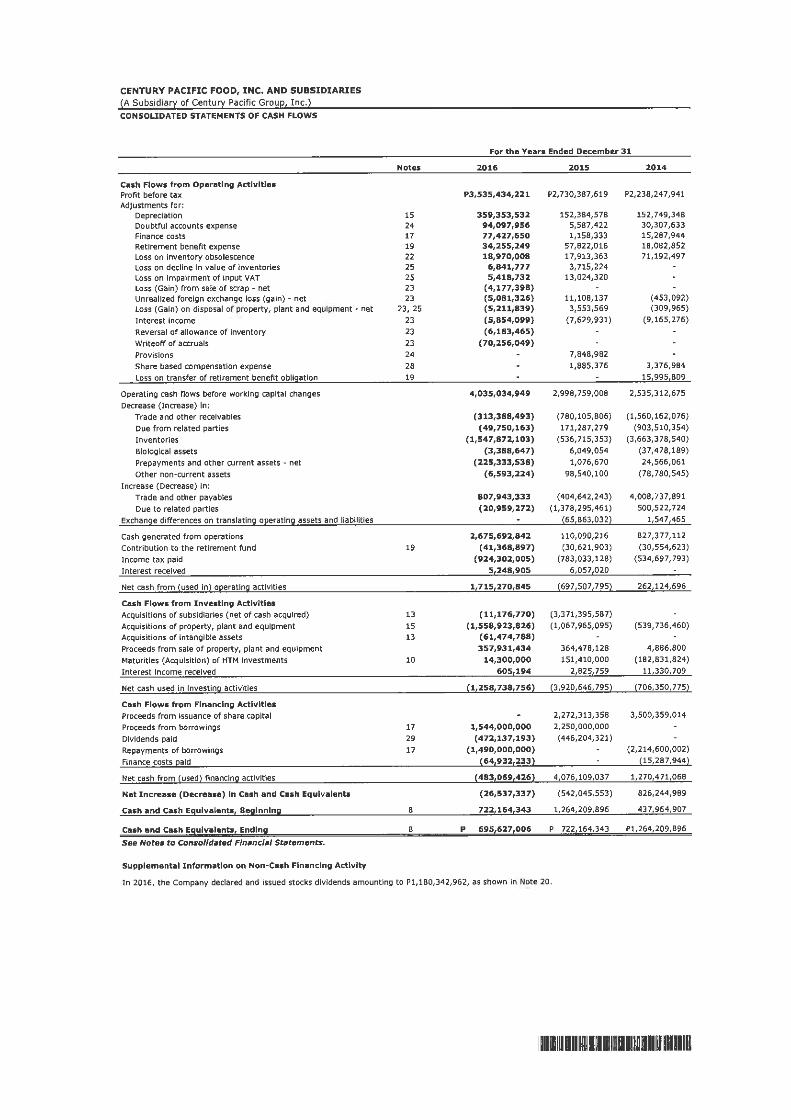

CENTURY PACIFIC FOOD, INC. AND SUBSIDIARIES (A Subsidiary of Century Pacific Group, Inc.) CONSOLIDATED STATEMENTS OF CASH FLOWS

Cash Flow• from Operating Activities Profit before tax Adjustments for:

Depreciation Doubtful accounts expense Finance costs Retirement benefit expense Loss on Inventory obsolescence Loss on decline In value of Inventories Loss on Impairment of Input VAT Loss (Gain) from sale of scrap - net Unrealized foreign exchange loss (gain) - net Loss (Gain) on disposal of property, plant and equipment - net

Interest Income Reversal of allowance of Inventory

Wrlteoff of accruals Provisions Share based compensation expense Loss on transfer of retirement benefit obligation

Operating cash flows before working capital changes Decrease (Increase) In:

Trade and other receivables Due from related parties Inventories Biological assets Prepayments and other current assets - net Other non-current assets

Increase (Decrease) In: Trade and other payables Due to related parties

Exchange differences on translating oeeratlng assets and llabilltles

Cash generated from operations Contribution to the retirement fund Income tax paid Interest received

Net cash from {used In) oeerat1n2 activities

Cash Flows from Inve.tlng Activities Acquisitions of subsidiaries (net of cash acquired) Acquisitions of property, plant and equipment Acquisitions of Intangible assets Proceeds from sale of property, plant and equipment Maturities (Acquisition) of HTM Investments Interest Income received

Net cash used In lnvest1n2 activities

Cash Flows from Financing Activities Proceeds from Issuance of share capital Proceeds from borrowings Dividends paid Repayments of borrowings

Finance costs eald

Net cash from (used) flnanc1n2 activities

Net Increase (Decrease) In Cash and Cash Equivalents

Cash and Cash Egulvalents, Be11Jnnln11

Cash and Cash E9ulvalents, Endln11

See Notes to Consolidated Financial Statements.

Supplemental Information on Non-Cash Financing Activity

Note•

15 24 17 19 22 25 25 23 23

23, 25 23 23 23 24 28 19

19

13 15 13

10

17 29 17

8

8

For the Years Ended December 31

2016 2015 2014

P3,535,434,221 P2, 730,387,619 P2,238,247,941

359,353,532 152,384,578 152,749,348 94,097,956 5,587,422 30,307,633 77,427,650 1,158,333 15,287,944 34,255,249 57,822,016 18,082,852 18,970,008 17,913,363 71,192,497

6,841,777 3,715,224 5,418,732 13,024,320

(4,177,398) (5,081,326) 11,108,137 (453,092) (5,211,839) 3,553,569 (309,965)

(5,854,099) (7,629,931) (9,165,276) (6,183,465)

(70,256,049) 7,848,982 1,885,376 3,376,984

15,995,809

4,035,034,949 2,998,759,008 2,535,312,675

(313,388,493) (780,105,806) (1,560,162,076) (49,750,163) 171,287,279 (903,510,354)

(1,547,872,103) (536,715,353) (3,663,378,540) (3,388,647) 6,049,054 (37,478,189)

(225,333,538) 1,076,670 24,566,061 (6,593,224) 98,540,100 (78,780,545)

807,943,333 (404,642,243) 4,008,737,891 (20,959,272) (1,378,295,461) 500,522,724

(65,863,032) 1,547,465

2,675,692,842 110,090,216 827,377,112 (41,368,897) (30,621,903) (30,554,623)

(924,302,005) (783,033,128) ( 534,697,793) 5 248 905 6,057,020

1,11s,210,s4s {697,507,795) 262,124,696

(11,176,770) (3,371,395,587) (1,558,923,826) (1,067,965,095) (539,736,460)

(61,474,788) 357,931,434 364,478,128 4,886,800

14,300,000 151,410,000 (182,831,824)

605,194 2,825,759 11,330,709

{1,258,738,756) {3,920,646,795) (706,350,775)

2,272,313,358 3,500,359,014

1,544,000,000 2,250,000,000

(472,137,193) (446,204,321) (1,490,000,000) (2,214,600,002)

{64,932,233) {15,287,944)

(483,069,426) 4,076,109,037 1,270,471,068

(26,537,337) (542,045,553) 826,244,989

722,164,343 1,264,209,896 437,964,907

p 695,627, 006 p 722,164,343 Pl,264,209,896

In 2016, the Company declared and Issued stocks dividends amounting to Pl,180,342,962, as shown In Note 20.

llmHHIUIIHHIIWIHIIIIIIU

CENTURY PACIFIC FOOD, INC. AND SUBSIDIARIES (A Subsidiary of Century Pacific Group, Inc.) NOTES TO CONSOLIDATED FINANCIAL STATEMENTS AS AT DECEMBER 31, 2016 AND 2015 AND FOR THE YEARS ENDED DECEMBER 31, 2016, 2015 AND 2014

1. CORPORATE INFORMATION

Century Pacific Food, Inc. (the "Parent Company") was incorporated and registered with the Philippine Securities and Exchange Commission (SEC) on October 25, 2013. The Parent Company is primarily engaged in the business of buying and selling, processing, canning and packaging and manufacturing all kinds of food and food products, such as but not limited to fish, seafood and other marine products, cattle, hog and other animals and animal products, fruits, vegetables and other agricultural crops and produce of land, including by-products thereof.

The Parent Company's shares of stocks were listed in the Philippines Stock Exchange (PSE) on May 6, 2014 through initial public offering (IPO) and listing of 229.65 million shares in the PSE at a total value of P3.3 billion, as discussed in Note 20.

The Parent Company is 68.68% as at December 31, 2016 and 73.72% as at December 31, 2015 owned subsidiary o9f Century Pacific Group, Inc. (CPGI), the ultimate parent, a corporation registered with the SEC and domiciled in the Philippines.

The Parent Company's registered office and principal place of business, is located at 7th floor, Centerpoint Building, Julia Vargas St., Ortigas Center, Pasig City.

2. FINANCIAL REPORTING FRAMEWORK AND BASIS OF PREPARATION AND PRESENTATION

Statement of Compliance

The consolidated financial statements of the Parent Company and its subsidiaries (the "Group") have been prepared in accordance with Philippine Financial Reporting Standards (PFRS), which includes all applicable PFRS, Philippine Accounting Standards (PAS), and interpretations issued by the International Financial Reporting Interpretations Committee (IFRIC), Philippine Interpretations Committee (PIC) and Standing Interpretations Committee (SIC) as approved by the Financial Reporting Standards Council (FRSC) and the Board of Accountancy (BOA), and adopted by the SEC.

Basis of Preparation and Presentation

The consolidated financial statements have been prepared on the historical cost basis, except for:

• certain financial instruments carried at amortized cost; • inventories carried at the lower of cost and net realizable value (NRV); and

• retirement benefit obligation recognized as the net of the present value of the obligation and fair value of plan assets.

Historical cost is generally based on the fair value of the consideration given in exchange for goods and services.

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 1

Fair value is the price that will be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, regardless of whether that price is directly observable or estimated using another valuation technique. In estimating the fair value of an asset or a liability, the Group takes into account the characteristics of the asset or liabil ity if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Fair value for measurement and/or disclosure purposes in these consolidated financial statements is determined on such a basis, except for share-based payment transactions that are with in the scope of PFRS 2, Share-based Payment, leasing transactions that are within the scope of PAS 17, Leases, and measurements that have some similarities to fair value but are not fair value, such as net realizable value in PAS 2, Inventories or value in use in PAS 36, Impairment of Assets.

In addition, for financial reporting purposes, fair value measurements are categorized into Levels 1, 2 or 3 based on the degree to which the inputs to the fair value measurements are observable and the significance of the inputs to the fair value measurement in its entirety, which are described as follows:

• Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the entity can access at the measurement date;

• Level 2 inputs are inputs, other than quoted prices included within Level 1, that are observable for the asset or liability, either directly or indirectly; and

• Level 3 inputs are unobservable inputs for the asset or liability.

Functional and Presentation Currency

These consolidated financial statements are presented in Philippine peso, the currency of the primary economic environment in which the Group operates. All amounts are presented in the nearest peso, except when otherwise indicated .

Functional currency

The separate financial statements of General Tuna Corporation (GTC) are presented in United States (US) Dollar, the currency of the primary economic environment in which it operates. In addition, the separate financial statements of Century International (China) Co. Ltd. (CIC), Century (Shanghai) Trading Co. Ltd. (CST) and Cindena Resources Limited (CRL) are presented in Chinese Yuan, the currency of the primary economic environment in which these companies operate.

Presentation currency

The financial statements of GTC, CIC, CST and CRL are presented in Philippine peso as its presentation currency. GTC translated its financial position and results of operations from US Dollar to Philippine Peso, while CIC, CST and CRL translated its financial position from Chinese Yuan to Philippine peso using the following procedures:

• assets and liabilities, except those assets presented at historical costs, for each statement of financial position presented, are presented at the closing rate at the date of that statement of financial position;

• for each period presented, income and expenses recognized in the period by GTC are translated using the average exchange rate at that period; and

• all resulting exchange differences are recognized in other comprehensive income (OCI) as currency translation adjustment.

1111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111 2

3. COMPOSITION OF THE GROUP

Details of the Parent Company's subsidiaries as at December 31, 2016 and 2015 are as follows:

Name of Subsidiary

General Tuna Corporation (GTC) Snow Mountain Dairy Corporation (SMDC) Allforward Warehousing Inc. (AWi) Century Pacific Agricultural Ventures, Inc. (CPAVI) Century Pacific Seacrest Inc. (CPSI) Centennial Global Corporation (CGC) Century Pacific Food Packaging Ventures, Inc. (CPFPVI) Century International (Ch ina) Co. Ltd. (CIC) Century (Shanghai) Trading Co. Ltd. (CST) Cindena Resources Limited (CRL)

Ownership Interest 2016 2015

100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

100% 100% 100% 100% 100% 100%

The significant financial information on the financial statements of who lly-owned subsidiaries of the Parent Company are shown below. The summarized financial information represents amounts before intragroup eliminations.

~

GTC was incorporated in the Philippines and was registered with the SEC on March 10, 1997. GTC is presently engaged in manufacturing and exporting private label canned, pouched and frozen tuna products. Its processing plant is located at Purok Lansong, Brgy. Tambler, General Santos City.

The significant information on the audited financial statements of GTC as at December 31, 2016 and 2015 and the resu lts of its operations for the years ended December 31, 2016, 2015 and 2014, as translated to its presentation currency, are as fo llows:

Financial Position Current assets Non-current assets

Total Assets

Current liabilities Non-current liabilities

Total Liabilities

Equity

Results of Operations Revenue Cost and expenses

Profit for the year

~

2016

PS,833,301,439 5,706,345,043

p 126,956,396

2016 2015

P2,838,253,195 P2,657,391,874 790,862,175 798,459,762

3,629,115,370 3,455,851,636

1,932,505,748 2,378,726,302 8,366,279 15,056,760

1,940,872,027 2,393,783,062

Pl,688,243,343 Pl,062,068,574

2015 2014

P5,484,596,163 P5,384,279,468 5,336,462,276 5,225,446,450

p 148,133,887 p 158,833,018

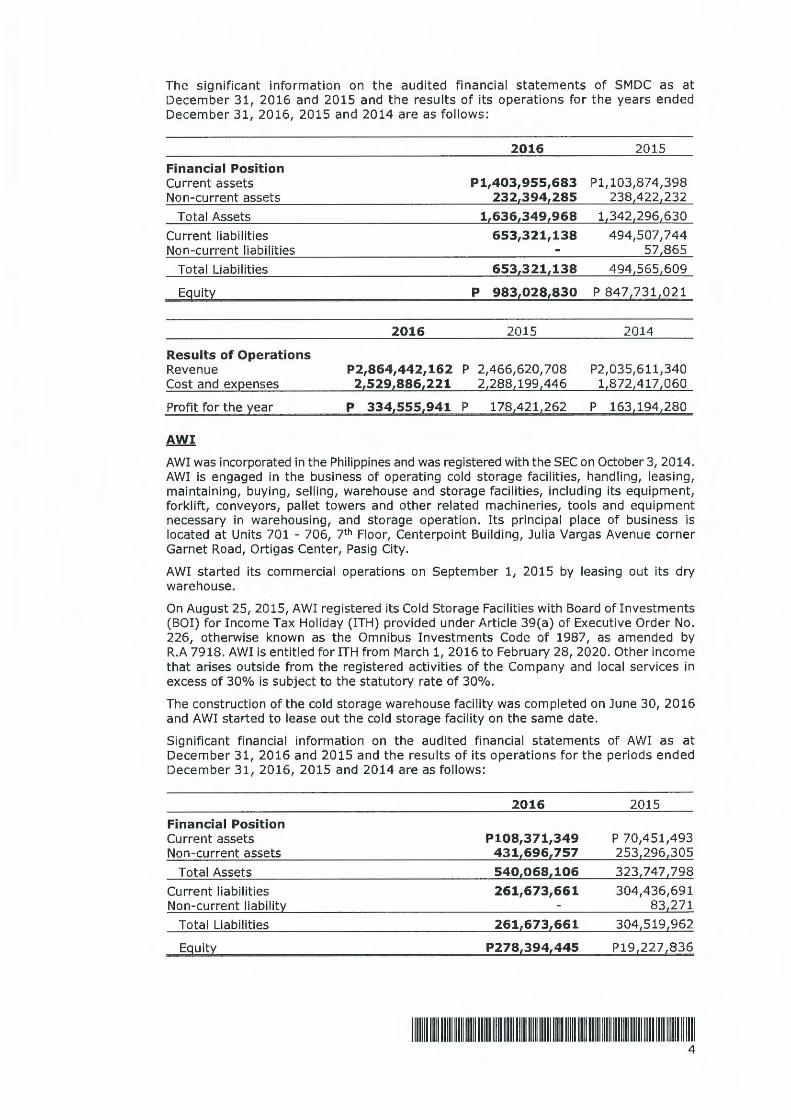

SMDC was incorporated in the Philippines and was registered with the SEC on February 14, 2001. SMDC is engaged in producing, canning, freezing, preserving, refining, packing, buying and selling at wholesale and retail, food products including all kinds of milk and dairy products, fruits and vegetab le juices and other milk or dairy preparations and by-products. Its principal place of business is located at 32 Arturo Drive, Bagumbayan, Taguig City.

1111111111111111111111111111111111111111111111111111 111111111111111111111111111111111111111111111111111111111111111 3

The significant information on the audited financial statements of SMDC as at December 31, 2016 and 2015 and the results of its operations for the years ended December 31, 2016, 2015 and 2014 are as fol lows:

2016 2015

Financial Position Current assets P1,403,955,683 Pl,103,874,398 Non-current assets 232L394L285 23814221232

Total Assets 1L636L349L968 1134212961630

Current liabilities 653,321,138 494,507,744 Non-current liabilities 57 865

Total Liabilities 653L321L138 49415651609

E9uity p 983,028,830 P 847?3 1,021

2016 2015 2014

Results of Operations Revenue P2,864,442,162 p 2,466,620,708 P2,035,611,340 Cost and ex12enses 2L529L886L221 2128811991446 1187214171060

Profit for the year p 334,555,941 p 178,421,262 p 163,194,280

AWi

AWi was incorporated in the Philippines and was registered with the SEC on October 3, 2014. AWi is engaged in the business of operating cold storage facilities, handling, leasing, maintaining, buying, selling, warehouse and storage faci l ities, including its equipment, forkl ift, conveyors, pallet towers and other related machineries, too ls and equipment necessary in warehousing, and storage operation. Its principal place of business is located at Units 701 - 706, 7th Floor, Centerpoint Building, Julia Vargas Avenue corner Garnet Road, Ortigas Center, Pasig City.

AWi started its commercial operations on September 1, 2015 by leasing out its dry warehouse.

On August 25, 2015, AWi registered its Cold Storage Facilities with Board of Investments (BOI) for Income Tax Holiday (ITH) provided under Art icle 39(a) of Executive Order No. 226, otherwise known as the Omnibus Investments Code of 1987, as amended by R.A 7918. AWi is entitled for ITH from March 1, 2016 to February 28, 2020. Other income that arises outside from the registered activities of the Company and local services in excess of 30% is subject to the statutory rate of 30%.

The construction of the cold storage warehouse facility was completed on June 30, 2016 and AWi started to lease out the cold storage faci lity on t he same date.

Significant financia l information on t he audited financial statements of AWi as at December 31, 2016 and 2015 and the results of its operations for the periods ended December 31, 2016, 2015 and 2014 are as follows:

2016 2015

Financial Position Current assets P108,371,349 P 70,451,493 Non-current assets 431L696L757 25312961305

Total Assets 540L068L106 32317471798

Current liabilit ies 261,673,661 304,436,691 Non-current liabilitt: 831271

Tota l Liabilities 261L673L661 30415191962

E9uity P278,394,445 P19,227 ,836

llllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllll~IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 4

Results of Operations Revenue Cost and expenses

Profit (Loss) for the year

CPAVI

2016 (Twelve Months)

P94,953,114 29,725,083

P65,228,031

2015 2014

(Twelve Months) (Three Months)

P?,311,541 p

5,547,315 764,055

Pl,764,226 (P764,055)

CPAVI was incorporated in the Philippines and was registered with the SEC on August 29, 2012. CPAVI is engaged in the business of manufacturing and distributing all kinds of food and beverage products and other foodstuffs derived from fruits and other agricultural products. Its principal place of business is located at 7th floor, Centerpoint Building, Julia Vargas St. corner Garnet Road, Ortigas, Pasig City.

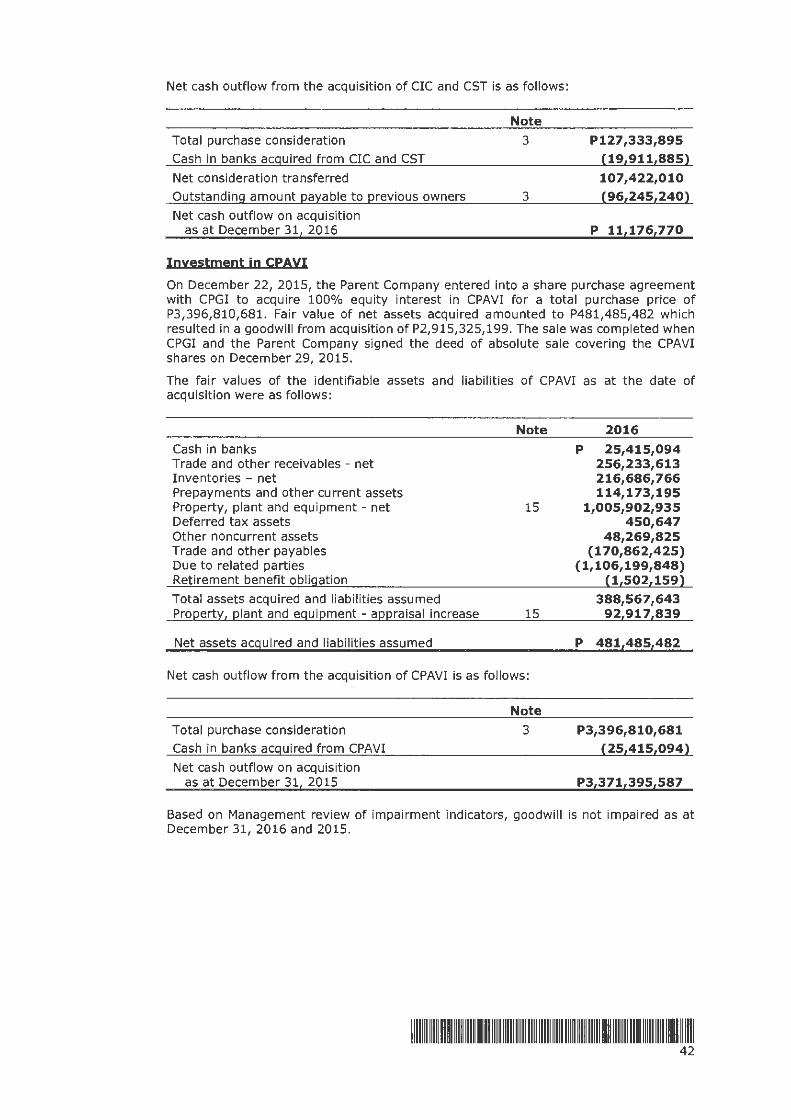

On December 22, 2015, the Parent Company entered into a share purchase agreement with CPGI to acquire 100% equity interest in CPAVI for a total purchase price of P3,396,810,681. To facilitate the acquisition, the Parent Company availed of short term loans of P2,250,000,000 from certain financial institutions, as disclosed in Note 17. The agreement also provided for the Parent Company to advance to CPAVI a total amount of Pl,103,189,333 for the latter to settle its advances to CPGI. The sale was completed when CPGI and the Parent Company signed the deed of absolute sale covering the CPAVI shares on December 29, 2015. On August 10, 2016, the SEC approved the increase in CPAVI's share capital from P350,000,000 to Pl,500,000,000. On the same date, the advances of the Parent Company was converted to equity shares of stock.

Significant information on the audited financial statements of CPAVI as at and for the years ended December 31, 2016 and 2015 are as follows :

Financial Position Current assets Non-current assets

Total Assets

Current liabilities Non-current liabilities

Total Liabilities

Equity

Results of Operations Revenue Cost and expenses

Profit for the year

~

2016 2015

p 961,982,769 P 581,892,639 1,569,075,810 1,085,239,441

2,531,058,579 1,667,132,080

782,074,282 1,277,062,273 1,052,933 1,502,160

783,127,215 1,278,564,433

P1,747,931,364 P 388,567,647

P2,842,256,837 p 2,578,739,846

p 263,516,991 p

CPS! was incorporated in the Philippines and was registered with the SEC on November 13, 2015. CPS! is engaged in the business of developing and designing, acquinng, selling, transferring, exchanging, managing, licensing, franchising and generally in exercising all rights, powers and privileges of ownership or granting any right or privilege of ownership or any interest to label marks, devices, brands, trademark rights and all other forms of intellectual property, including the right to receive, collect and dispose of any and all payments, dividends, interests and income derived from. On December 28, 2015, CPS! entered into a Trademark Purchase Agreement to purchase certain trademarks owned by CGC for a total consideration of P50,000,000. The trademarks purchased include brands such as "Century Tuna", "Argentina", "555", "Wow Ulam", "Birch Tree", "Fresca", " Lucky 7" and "Angel Evaporada" among others. The purchase price of P50,000,000 remains outstanding as of December 31, 2016. Its principal place of business is located at 7 th Floor, Centerpoint Building, J. Vargas Avenue corner Garnet Road, Ortigas Center, Pasig City.

1111111 111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111 5

CPSI started its commercial operations in 2016.

The significant information on the audited financial statements of CPSI as at December 31, 2016 and 2015 and for the periods ended December 31, 2016 and 2015 are as follows:

Financial Position Current assets Non-current assets

Total Assets

Total Liabilities

Equity

Results of Operations Revenue Cost and expenses

Profit (Loss) for the year

~

2016

P131,875,295 111,474,788 243,350,083 178,666,553

p 64,683,530

2016 (Twelve Months)

P776,737,104 142,507,320

P634,229,784

2015

P 50,000,761 50,113,012

100,113,773

50,376,357

P 49,737,416

2015

(Two Months)

p 1,111 263,695

(P262,584)

CGC was incorporated in the British Virgin Islands (BVI) on November 13, 2006. CGC is a company limited by shares. On February 25, 2015, the Parent Company acquired 100% interest in CGC for $100 or P4,438 from Shining Ray Limited, a who lly owned subsidiary of CPGI. CGC is the corporate vehicle that holds the various brands, trademarks, and related intellectual property of the Century Group of Companies. On December 28, 2015, CGC sold certain trademarks to CPSI for a total consideration of P50,000,000. CGC's registered office is at P.O. Box 957, Offshore Incorporations Centre, Road Town, Tortola, British Virgin Islands and its reg istered agent is Offshore Incorporations Limited.

The significant information on the financial statements of CGC as at December 31, 2016 and 2015 and the results of its operations for the years ended December 31, 2016 and 2015 are as follows:

2016 2015 (Unaudited) (Unaudited)

Financial Position Total Assets PS0,004,438 P50,004,438

Equity PS0,004,438 P50,004,438

Results of Operations Revenue p P50,000,000

Profit for the year p P50,000,000

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 6

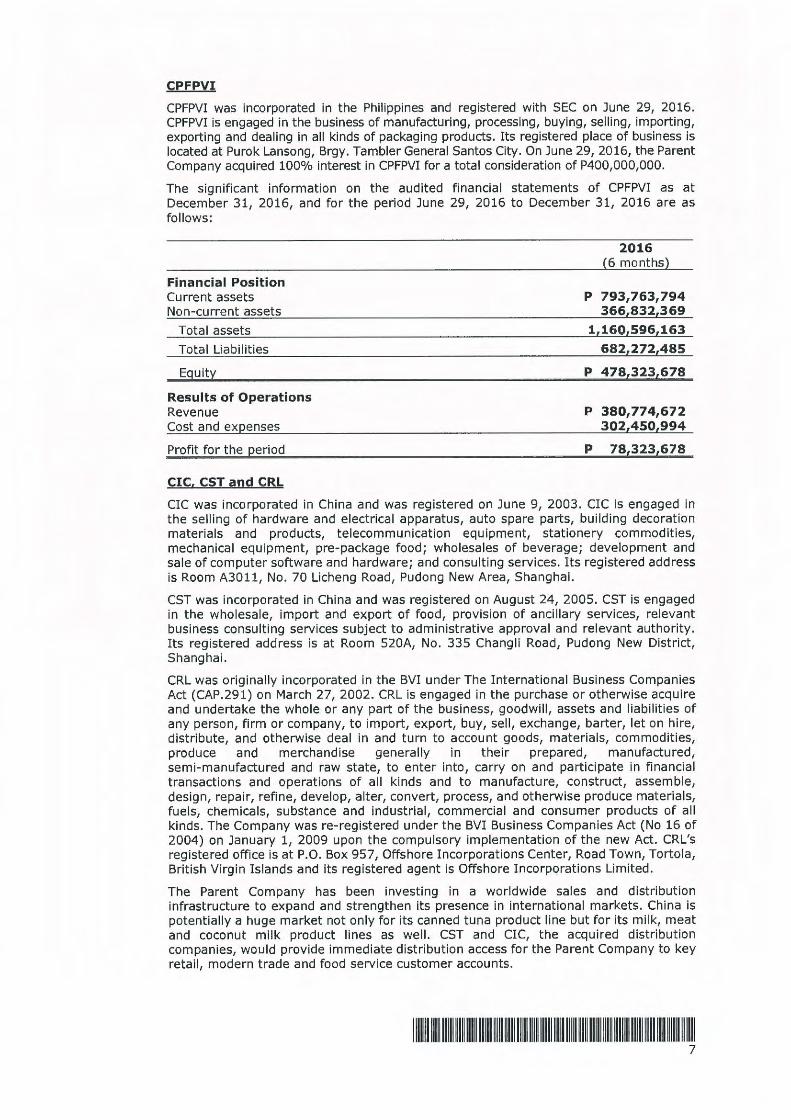

CPFPVI

CPFPVI was incorporated in the Philippines and registered with SEC on June 29, 2016. CPFPVI is engaged in the business of manufacturing, processing, buying, selling, importing, exporting and dealing in all kinds of packaging products. Its registered place of business is located at Purok Lansong, Brgy. Tambler General Santos City. On June 29, 2016, the Parent Company acquired 100% interest in CPFPVI for a total consideration of P400,000,000.

The significant information on the audited financial statements of CPFPVI as at December 31, 2016, and for the period June 29, 2016 to December 31, 2016 are as follows:

Financial Position Current assets Non-current assets

Total assets

Total Liabilities

Equity

Results of Operations Revenue Cost and expenses

Profit for the period

CIC. CST and CRL

2016 (6 months)

P 793,763,794 366,832,369

1,160,596,163 682,272,485

P 478,323,678

P 380,774,672 302,450,994

P 78,323,678

CIC was incorporated in China and was registered on June 9, 2003. CIC is engaged in the selling of hardware and electrical apparatus, auto spare parts, building decoration materials and products, telecommunication equipment, stationery commodities, mechanical equipment, pre-package food; wholesales of beverage; development and sale of computer software and hardware; and consulting services. Its registered address is Room A3011, No. 70 Licheng Road, Pudong New Area, Shanghai.

CST was incorporated in China and was registered on August 24, 2005. CST is engaged in the wholesale, import and export of food, provision of ancillary services, relevant business consulting services subject to administrative approval and relevant authority. Its registered address is at Room 520A, No. 335 Changli Road, Pudong New District, Shanghai.

CRL was originally incorporated in the BVI under The International Business Companies Act (CAP.291) on March 27, 2002. CRL is engaged in the purchase or otherwise acquire and undertake the whole or any part of the business, goodwill, assets and liabilities of any person, firm or company, to import, export, buy, sell, exchange, barter, let on hire, distribute, and otherwise deal in and turn to account goods, materials, commodities, produce and merchandise generally in their prepared, manufactured, semi-manufactured and raw state, to enter into, carry on and participate in financial transactions and operations of all kinds and to manufacture, construct, assemble, design, repair, refine, develop, alter, convert, process, and otherwise produce materials, fuels, chemicals, substance and industrial, commercial and consumer products of all kinds. The Company was re-registered under the BVI Business Companies Act (No 16 of 2004) on January 1, 2009 upon the compulsory implementation of the new Act. CRL's registered office is at P.O. Box 957, Offshore Incorporations Center, Road Town, Tortola, British Virgin Islands and its registered agent is Offshore Incorporations Limited.

The Parent Company has been investing in a worldwide sales and distribution infrastructure to expand and strengthen its presence in international markets. China is potentially a huge market not only for its canned tuna product line but for its milk, meat and coconut milk product lines as well. CST and CIC, the acquired distribution companies, would provide immediate distribution access for the Parent Company to key retail, modern trade and food service customer accounts.

1111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111 7

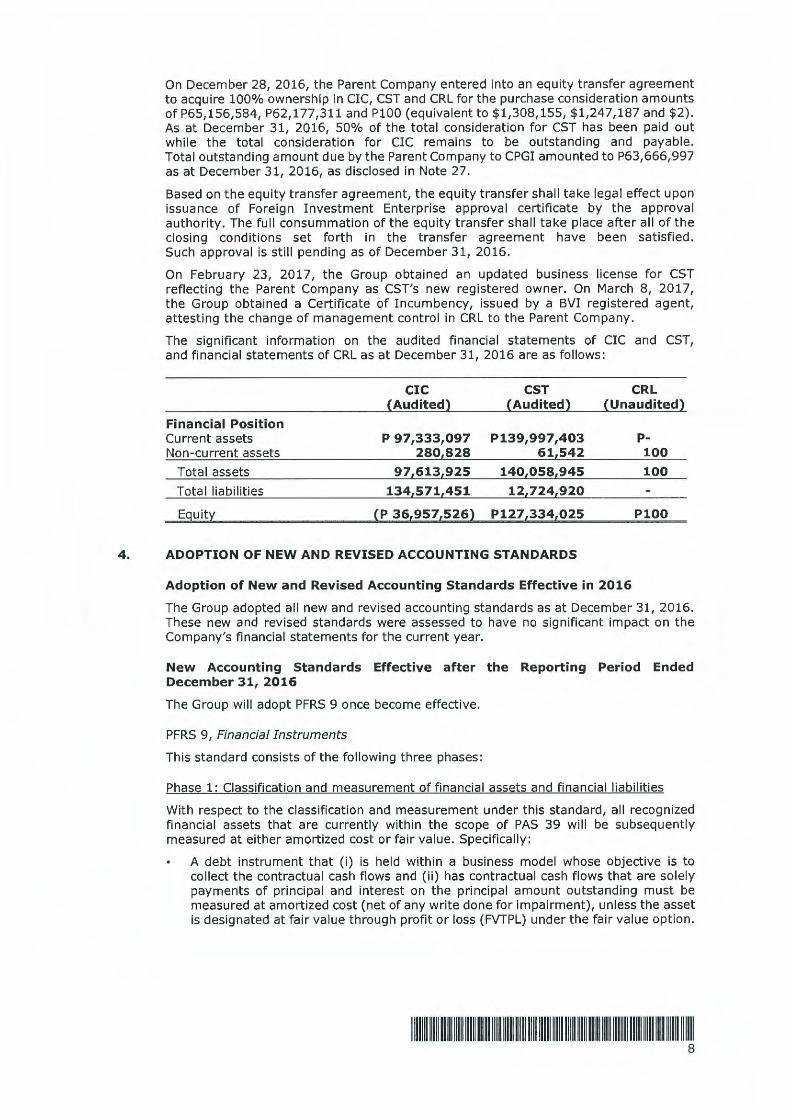

On December 28, 2016, the Parent Company entered into an equity transfer agreement to acquire 100% ownership in CIC, CST and CRL for the purchase consideration amounts of P65,156,584, P62,177,311 and P100 (equivalent to $1,308,155, $1,247,187 and $2) . As at December 31, 2016, 50% of the total consideration for CST has been paid out while the total consideration for CIC remains to be outstanding and payable. Total outstanding amount due by the Parent Company to CPGI amounted to P63,666,997 as at December 31, 2016, as disclosed in Note 27.

Based on the equity transfer agreement, the equity transfer shall take legal effect upon issuance of Foreign Investment Enterprise approval certificate by the approval authority. The full consummation of the equity transfer shall take place after all of the closing conditions set forth in the transfer agreement have been satisfied . Such approval is still pending as of December 31, 2016.

On February 23, 2017, the Group obtained an updated business license for CST reflecting the Parent Company as CST's new registered owner. On March 8, 2017, the Group obtained a Certificate of Incumbency, issued by a BVI registered agent, attesting the change of management contro l in CRL to the Parent Company.

The significant information on the audited financial statements of CIC and CST, and financial statements of CRL as at December 31, 2016 are as follows:

CIC CST CRL {Audited) {Audited) (Unaudited)

Financial Position Current assets P 97,333,097 P139,997,403 P-Non-current assets 280(828 61(542 100

Total assets 97(613(925 140l058l945 100

Total liabilities 134(571(451 12(724(920

E9uitl {P 36,957,526l P127,334,025 P100

4. ADOPTION OF NEW AND REVISED ACCOUNTING STANDARDS

Adoption of New and Revised Accounting Standards Effective in 2016

The Group adopted all new and revised accounting standards as at December 31, 2016. These new and revised standards were assessed to have no significant impact on the Company's financial statements for the current year.

New Accounting Standards Effective after the Reporting Period Ended December 31, 2016

The Group will adopt PFRS 9 once become effective.

PFRS 9, Financial Instruments

This standard consists of the following three phases:

Phase 1: Classification and measurement of financial assets and financial liabilities

With respect to the classification and measurement under this standard, all recognized financial assets that are currently within the scope of PAS 39 will be subsequently measured at either amortized cost or fair value. Specifically :

A debt instrument that (i) is held with in a business model whose objective is to collect the contractua l cash flows and (ii) has contractual cash flows that are so lely payments of principal and interest on the principal amount outstanding must be measured at amortized cost (net of any write done for impairment), unless the asset is designated at fair value through profit or loss (FVTPL) under the fair value option.

1111111 111111111111111111!1111111111111111111111111111111111111111111111111111111111111111111111111111111111111111 8

A debt instrument that (i) is held within a business model whose objective is achieved both by collecting contractual cash flows and selling financial assets and (ii) has contractual terms that give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding, must be measured at fair va lue through other comprehensive income (FVTOCI), unless the asset is designated at FVTPL under the fair value option.

All other debt instruments must be measured at FVTPL.

All equity investments are to be measured in the statement of financial position at fair value, with gains and losses recognized in profit or loss except that if an equity investment is not held for trading, an irrevocable election can be made at initial recognition to measure the investment at FVTOCI, with dividend income recognized in profit or loss.

This standard also contains requirements for the classification and measurement of financial liabilities and derecognition requirements. One major change from PAS 39 relates to the presentation of changes in the fair value of a financial liability designated as at FVTPL attributable to changes in the credit risk for the liability. Under this standard, such changes are presented in other comprehensive income, unless the presentation of the effect of the change in the liability credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss. Changes in fair va lue attributable to a financial liabil ity's credit risk are not subsequently reclassified to profit or loss. Under PAS 39, the entire amount of the change in the fair value of the financial liability designated as FVTPL is presented in profit or loss.

Based on the Group's assessment, the classification and measurement of the Group's financial assets at amortized cost and financial liabilities will be the same under both PFRS 9 and PAS 39.

Phase 2: Impairment methodology

The impairment model under this standard reflects expected credit losses, as opposed to incurred credit losses under PAS 39. Under the impairment approach of this standard, it is no longer necessary for a credit event to have occurred before credit losses are recognized. Instead, an entity always accounts for expected credit losses and changes in those expected credit losses. The amount of expected credit losses should be updated at each reporting date to reflect changes in credit risk since initial recognition.

The future adoption of the standard will result in initial measurement of financial assets at amortized cost, net of expected credit losses.

Phase 3: Hedge accounting

The general hedge accounting requirements for this standard retain the three types of hedge accounting mechanism in PAS 39. However, greater flexibility has been introduced to the types of transactions eligible for hedge accounting, specifically broadening the types of instruments that qualify as hedging instruments and the types of risk components of non-financial items that are eligible for hedge accounting. In addition, the effectiveness test has been overhauled and replaced with the principle of economic relationships. Retrospective assessment of hedge effectiveness is no longer required. Far more disclosure requirements about an entity's risk management activities have been introduced.

The standard is effective for annual reporting periods beginning on or after January 1, 2018. Earlier application is permitted.

The Group's initial assessment of PFRS 9's potential impact to its consolidated financial statements provides that it would change the classification of financial assets but it will not affect the measurement of its current types of financial assets. The Group wil l continue its assessment and will finalize the same upon the effective date of the new standard.

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 9

PFRS 16, Leases

This standard specifies how a PFRS reporter will recognize, measure, present and disclose leases. It provides a single lessee accounting model, requiring lessees to recognize assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value. Lessors continue to classify leases as operating or finance, with PFRS 16's approach to lessor accounting substantially unchanged from its predecessor, PAS 17.

The standard is effective for annual reporting periods beginning on or after January 1, 2019. Earlier application is not permitted, until PFRS 15, Revenue from Contracts with Customers, is adopted.

Future adoption of this standard will result in recognition of right-of-use of asset and lease liability and additional disclosure in the Group's consolidated financial statements.

Amendment to PAS 7, Disclosure Initiative

The amendment clarify that entities shall provide disclosures that enable users of financial statements to evaluate changes in liabilities arising from financing activities.

The amendment is effective for annual reporting periods beginning on or after January 1, 2017. Earlier application is permitted.

Future adoption of this amendment will not have a significant impact on the Group's consolidated financial statements.

Amendments to PAS 12, Recognition of Deferred Tax Assets for Unrealized Losses

The amendments clarify the following aspects:

• Unrealized losses on debt instruments measured at fair value and measured at cost for tax purposes give rise to a deductible temporary difference regardless of whether the debt instrument's holder expects to recover the carrying amount of the debt instrument by sale or by use.

• The carrying amount of an asset does not limit the estimation of probable future taxable profits.

• Estimates for future taxable profits exclude tax deductions resulting from the reversal of deductible temporary differences.

• An entity assesses a deferred tax asset in combination with other deferred tax assets. Where tax law restricts the utilization of tax losses, an entity would assess a deferred tax asset in combination with other deferred tax assets of the same type.

The amendments are effective for annual reporting periods beginning on or after January 1, 2017. Earlier application is permitted.

Future adoption of these amendments will not have a significant impact on the Group's consolidated financia l statements.

Amendments to PFRS 2, Classification and Measurement of Share-based Payment Transactions

The amendments to PFRS 2 include:

a. Accounting for cash-settled share-based payment transactions that contain a performance condition. The amendment added guidance that introduces accounting requirements for cash-settled share-based payments that follows the same approach as used for equity-settled share-based payments.

b. Classification of share-based payment transactions with net settlement features. The amendment has introduced an exception into PFRS 2 so that a share-based payment where the entity settles the share-based payment arrangement net is classified as equity-settled in its entirety provided the share-based payment would have been classified as equity-settled had it not included the net settlement feature.

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 10

c. Accounting for modifications of share-based payment transactions from cash-settled to equity-settled. The amendment has introduced the following clarifications:

• On modifications, the original liability recognized in respect of the cash-settled share-based payment is derecognized and the equity-settled share-based payment is recognized at the modification date fair value to the extent services have been rendered up to the modification date.

• Any difference between the carrying amount of the liability as at the modification date and the amount recognized in equity at the same date would be recognized in profit and loss immediately.

The amendments are effective for annual periods beginning on or after January 1, 2018 with earlier application permitted.

The Group's initial assessment of potential impact of adopting PFRS 2 to its consolidated financial statements in the future provides that its current classification and measurement of share-based payment transactions will not be significantly affected. The Group will continue its assessment and will finalize the same upon effective date of standard.

New Accounting Standards Effective After the Reporting Period Ended December 31, 2016 -Adopted by Financial Reporting Standards Council (FRSC) but pending publication in the Official Gazette by the Board of Accountancy

The Group will adopt the following once become effective.

Amendments to PFRS 4, Applying PFRS 9 'Financial Instruments' with PFRS 4 'Insurance Contracts'

The amendments provide two options for entities that issue insurance contracts within the scope of PFRS 4:

• an option that permits entities to reclassify, from profit or loss to other comprehensive income, some of the income or expenses arising from designated financial assets; this is the so-called overlay approach; and

• an optional temporary exemption from applying PFRS 9 for entities whose predominant activity is issuing contracts within the scope of PFRS 4; this is the so-called deferral approach.

The application of both approaches is optional and an entity is permitted to stop applying them before the new insurance contracts standard is applied. An entity applies the deferral approach for annual periods beginning on or after January 1, 2018.

Future adoption of the amendments will not have a significant impact on the Group's consolidated financial statements as the Group does not issue insurance contracts.

Annual Improvements to PFRSs 2014-2016 Cycle

The annual improvements address the following issues:

Amendments to PFRS 1, First- time Adoption of International Financial Reporting Standards

The amendments include the deletion of short-term exemptions stated in the appendix of PFRS 1, because they have now served their intended purpose. The amendments are effective for annual periods beginning on or after January 1, 2018 with earlier application permitted.

Future adoption of these amendments will not have an impact on the Group's consolidated financial statements as the Group is no longer a first time adopter of PFRS.

IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 11

Amendments to PFRS 12, Disclosure of Interests in Other Entities

The amendments clarify the scope of the standard by specifying that the disclosure requirements in the standard, except for those disclosures needed in the summarized financial for subsidiaries, joint ventures and associates, apply to an entity's interests that are classified as held for sale, as held for distribution or as discontinued operations in accordance with PFRS 5, Non-current Assets Held for Sale and Discontinued Operations.

The amendments are effective for annual periods beginning on or after January 1, 2017 with earl ier application permitted.

The Group will continue its assessment and will finalize the same upon the effective date of standard.

Amendments to PAS 28, Investments in Associates and Joint Ventures

The amendments clarify that the election to measure at FVTPL an investment in an associate or a joint venture that is held by an entity that is a venture capital organization, or other qualifying entity, is available for each investment in an associate or joint venture on an investment-by-investment basis, upon initial recognition.

The amendments are effective for annual periods beginning on or after January 1, 2018 with earlier application permitted.

Future adoption of the amendments will not have a significant impact on the Group's consolidated financial statements.

Amendments to PAS 40, Investment Property - Transfers of Investment Property

The amendments in Transfers of Investment Property (Amendments to IAS 40) are:

• Stating that an entity shall transfer a property to, or from, investment property when, and only when, there is evidence of a change in use. A change of use occurs if property meets, or ceases to meet, the definition of investment property. A change in management's intentions for the use of a property by itself does not constitute evidence of a change in use.

• The list of evidence in paragraph 57(a) - (d) was designated as non-exhaustive list of examples instead of the previous exhaustive list

The amendments are effective for periods beginning on or after January 1, 2018. Earlier application is permitted.

Future adoption of these amendments will not have a significant impact on the Group's consolidated financial statements as the Group does not have an investment property.

Philippine Interpretations IFRIC 22, Foreign Currency Transactions and Advance Consideration

The Interpretation covers foreign currency transactions when an entity recognizes a non-monetary asset or non-monetary liability arising from the payment or receipt of advance consideration before the entity recognizes the related asset, expense or income. It does not apply when an entity measures the related asset, expense or income on initial recognition at fair value or at the fair value of the consideration received or paid at a date other than the date of initial recognition of the non-monetary asset or non-monetary liability.

The interpretation is effective for periods beginning on or after January 1, 2018. Earlier application is permitted.

Future adoption of these interpretations will not have a significant impact on the Group's consolidated financial statements.

1111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111111 12

PFRS 15, Revenue from Contracts with Customers

The standard combines, enhances, and replaces specific guidance on recognizing revenue with a single standards. An entity will recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

It defines a new five-step model to recognize revenue from customer contracts.

• Identify the contract(s) with a customer;

• Identify the performance obligations in the contract;

• Determine the transaction price;

• Allocate the transaction price to the performance obligations in the contract; and

• Recognize revenue when (or as) the entity satisfies a performance obligation.

Application of this guidance will depend on the facts and circumstances present in a contract with a customer and will require the exercise of judgment.

The standard is mandatory for annual reporting periods beginning on or after January 1, 2018. Earlier application is permitted.

The Group's initial assessment of potential impact of adopting PFRS 15 to its consolidated financia l statements in the future provides that its current revenue recognition policy will not be significantly affected. The Group wi ll continue its assessment and will finalize the same upon the effective date of the new standard.

PIC Q&A No. 2016-04, Application of PFRS 15 "Revenue from Contracts with Customers" on Sale of Residential Properties under Pre-completion Contracts