City of Tshwane GDS 2055 3 August 2012. 2 Reputation promise/mission The Auditor-General of South...

16

City of Tshwane GDS 2055 3 August 2012

-

Upload

karen-burke -

Category

Documents

-

view

214 -

download

0

Transcript of City of Tshwane GDS 2055 3 August 2012. 2 Reputation promise/mission The Auditor-General of South...

City of Tshwane GDS 2055

3 August 2012

2

Reputation promise/mission

The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, it exists to strengthen our country’s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building public confidence.

33

Table of contents

• What is a clean audit?• How to achieve a clean audit?• Governance structures • Council, Executive and Leadership driving clean audits• Role of Council, Executive and Leadership• Specific focus areas for MPAC • Specific focus areas for Audit Committees• Specific focus areas for Internal Audit• 2010/11 Audit Outcomes • Impact of MPACs on audit outcomes• City of Tshwane Mayor’s commitments • Conclusion

4

What is a clean audit?

• A clean audit relates to only three aspects:

o The financial statements are free from material misstatementso There are no material findings on the annual performance reporto There are no material findings on compliance with key laws and

regulations

5

How to achieve a clean audit?

• Matters reported by external and internal auditors should receive timeous management attention

• Internal controls should address the following key areas:1. Leadership2. Financial and performance management3. Governance

1. Leadership– Establish a culture of honesty, ethical business practices and good

governance– Exercise oversight responsibility– Ensure effective human resource practices– Implement appropriate policies and procedures– Approve and monitor the implementation of action plans to address internal

control deficiencies– Approve appropriate IT governance frameworks

6

How to achieve a clean audit (cont.) ?

2. Financial and performance management– Ensure proper record keeping of all transactions

– Maintain effective controls over daily and monthly processing and reconciliations of transaction

– Produce regular, accurate and complete financial and performance (‘service delivery’) reports

– Review and monitor compliance with applicable laws and regulations

– Design and implement formal controls to mitigate IT risks

3. Governance– Ensure that risks are periodically identified, assessed and effectively

mitigated

– Maintain an adequately resourced and functioning internal audit unit that audits to accepted norms and standards

– Maintain an audit committee that performs its legislated duties and that promotes accountability and service delivery

7

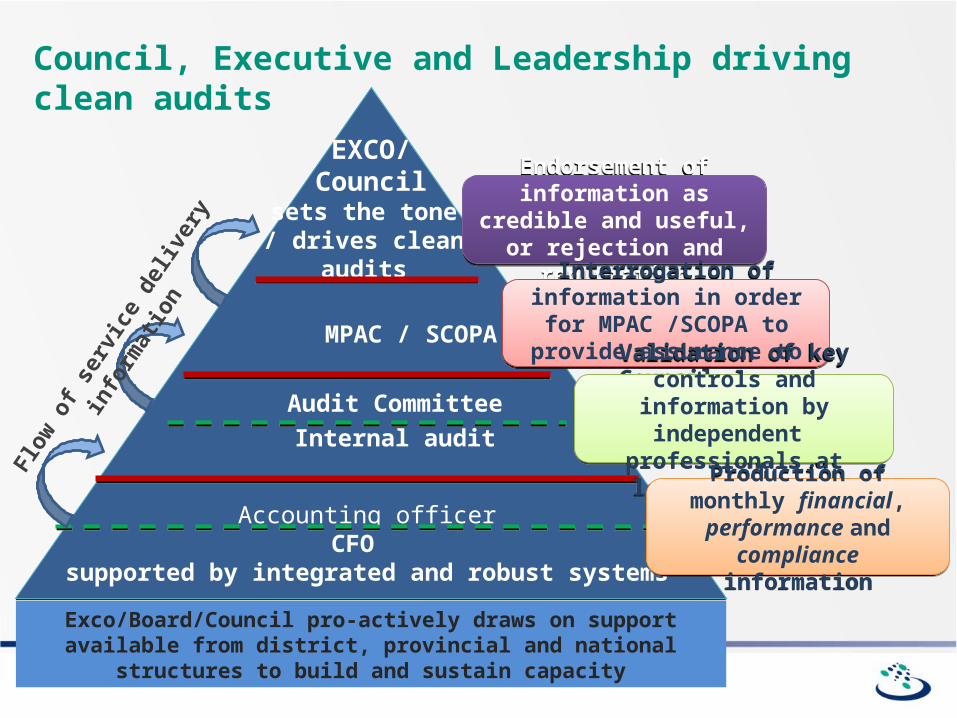

Governance Structures

• Council• Mayoral Committee• Sub committees of Council and Mayoral Committee• Municipal Public Accounts Committee• Audit committee• Intergovernmental relations forums

EXCO/Council

sets the tone / drives clean

audits

Accounting officerCFO

supported by integrated and robust systems

Audit CommitteeInternal audit

MPAC / SCOPA

Endorsement of information as credible and useful, or rejection and repudiation

Endorsement of information as credible and useful, or rejection and repudiation

Interrogation of information in order for MPAC /SCOPA to

provide assurance to Council

Interrogation of information in order for MPAC /SCOPA to

provide assurance to Council

Validation of key controls and information by independent

professionals at least quarterly

Validation of key controls and information by independent

professionals at least quarterly

Production of monthly financial, performance and

compliance information

Production of monthly financial, performance and

compliance information

Council, Executive and Leadership driving clean audits

Flow

of s

ervic

e del

ivery

info

rmati

on

Exco/Board/Council pro-actively draws on support available from district, provincial and national structures to build and sustain capacity

9

Role of Council (Legislature), Executive and Leadership

Executive

Other users

Leadership

Legislature Reporting by

department/entity

Cre

dib

le

info

rmati

on O

ve

rsig

ht

Cre

dib

le

info

rmati

on

Credible

information

Credible

information

Oversight

Mo

nit

ori

ng

Monitoring

Audit committee ensuring credibility of information and monitoring implementation of recommendations

1010

Specific focus areas for MPAC

• Consider and evaluate the contents of the annual report and make

recommendations to council when adopting an oversight report on the

annual report

• Review information relating to past recommendations made in the annual

report, including quarterly mid-year and annual reports

• Examine the financial statements and audit reports and consider

improvements on previous statements and reports

• Evaluate the extent to which recommendations of the audit committee

and the AGSA are being implemented

• Promote good governance, transparency and accountability in the use of

municipal resources

11

Specific focus areas for Audit Committee

• Reviews internal audit reports

• Reviews monthly budget statements, mid year performance reports and

AFS

• Advises Council on:

o internal financial controls and internal audits

o Risk management

o Accounting policies

o Annual Financial Statements

o Performance Management

o Performance evaluation

o Effective governance

o Compliance with MFMA, DORA, and other applicable legislation

12

Specific focus areas for Internal Audit

• Prepare a risk based audit plan and internal audit programme annually

• Accounting officer to respond to Audit Committee on implementation of

the annual audit plan

• Conduct frequent audits on internal controls and quality of Management

Accounts and Performance Information at Metro and Entities

• Issue reports in line with accepted norms and standards for review by the

Audit Committee

• Management to respond to reports at the Audit Committee and

implement recommendations

• Internal audit must expand its scope to include municipal entities

13

2010/11 audit findings: Key focus areas for all governance committees to address

• Supply chain management (Awards to persons in service of state;

SCM deviations; Irregular expenditure)

• Usefulness and reliability of reporting on Predetermined objectives

• Quality of monthly Financial management (Material amendments to

financial statements, Unauthorized expenditure)

• IT controls (Security, Access, Continuity)

• Human resource and performance management

• Effective management and use of consultants

• Sustainability of public finances (working capital, distribution losses)

• Governance structures in municipal entities

14

Impact of MPACs on audit outcomes

Interaction with Executive

Monitoring of implementation of

resolutions

Resolutions on financial

management reporting on PDO and compliance

Timeous hearings and resolutions

Resolution should not only deal with purely financial matters but should deal with financial management , PDO reporting and compliance for the committee to be truly effective.

The role within the municipality should submit quarterly reports to MPAC on the implementation of its resolution

A closer relationship with the portfolio committees id required to ensure coordination of resolutions an the monitoring thereof.

Training and capacity building

•New MPAC members should undergo a thorough induction session where all the concepts contained in the audit report are explained.•The AGSA is committed to enhancing the understanding of reports and will assist with this process where considered necessary.

MPAC hearings should be prioritised to ensure that the monitoring and review is conducive to the reporting timelines of municipalities and in a rapid response to audit committees.

15

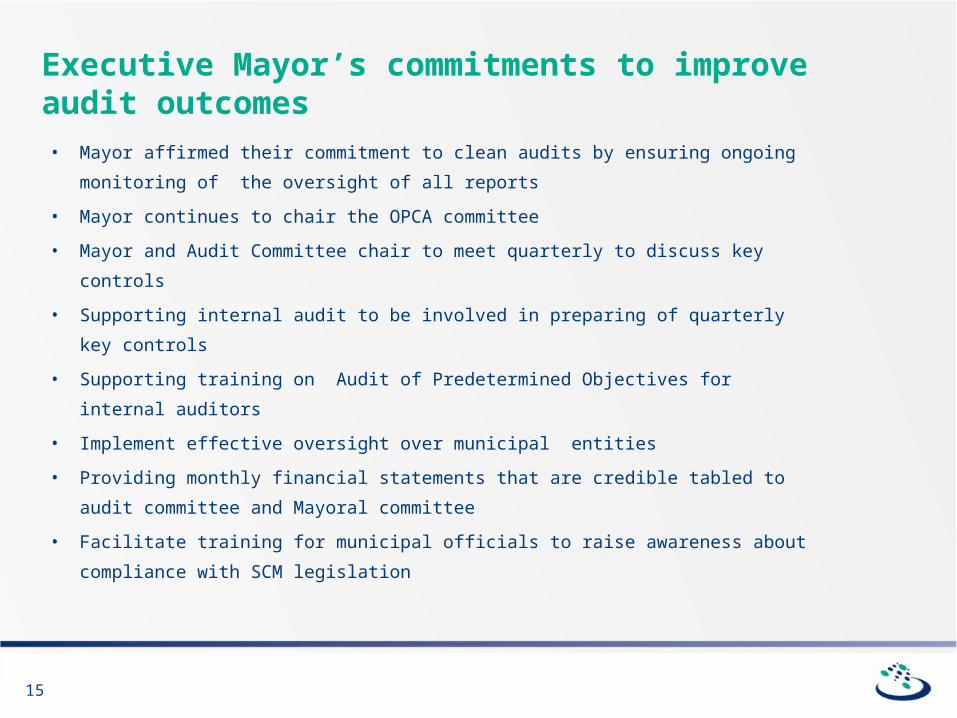

Executive Mayor’s commitments to improve audit outcomes

• Mayor affirmed their commitment to clean audits by ensuring ongoing

monitoring of the oversight of all reports

• Mayor continues to chair the OPCA committee

• Mayor and Audit Committee chair to meet quarterly to discuss key controls

• Supporting internal audit to be involved in preparing of quarterly key controls

• Supporting training on Audit of Predetermined Objectives for internal auditors

• Implement effective oversight over municipal entities

• Providing monthly financial statements that are credible tabled to audit

committee and Mayoral committee

• Facilitate training for municipal officials to raise awareness about compliance

with SCM legislation

1616

Conclusion

• The building blocks of good governance in the municipality exists

• The challenge lies in implementation of the basic principles to achieve clean audit outcomes

Thank you.